Activity-Based Costing Using Multicriteria Drivers: An Accounting Proposal to Boost Companies Toward Sustainability

Heitor F. Marinho Neto1

Heitor F. Marinho Neto1  Feni Agostinho1*

Feni Agostinho1*  Cecília M. V. B. Almeida1

Cecília M. V. B. Almeida1  Roberto R. Moreno García2

Roberto R. Moreno García2  Biagio F. Giannetti1

Biagio F. Giannetti1- 1Laboratory of Cleaner Production and Environment, Post-Graduation Program in Production Engineering, Paulista University, São Paulo, Brazil

- 2Faculty of Economics and Business Sciences, Oriente University, Santiago de Cuba, Cuba

Recognizing that natural environment is reaching its maximum limits in providing resources and diluting the waste generated by human production systems, efforts toward more sustainable production systems are mandatory to secure the development of future generations. For this purpose, changing the productivity model adopted by companies that are almost exclusively rooted on circulating money to generate profit, named business as usual, is an important issue. In this sense, an alternative would be establishing the relationship of stocks and flows of energy, material, and information with environmental, economic and social outcomes, thus resulting in new accounting approaches. This work aims to propose an activity-based costing (ABC) based on multicriteria drivers including economic, emissions, and emergy (with an “m”) values. The proposed ABC costing allocates each one of the multicriteria drivers into a specific part of the sustainability conceptual model, in an attempt to embrace a holistic perspective and allow for a sustainable-based decision, rather than considering purely economic drivers. The goal programming (GP) method is considered so as to support a decision based on multicriteria aspects. Results show that the proposed accounting approach known as ABCsustain allows for decisions toward a company's sustainability by acting on both the amount and kind of a company's product that should be managed, as well as on the effective increase of a specific company's activity or process. The proposed ABCsustain could make the insertion of environmental issues into companies strategic planning more effective. It is expected that environmental issues go beyond a simple diagnoses and begin to be considered as action in factum in the companies' decisions toward achieving a more sustainable world system.

Introduction

“Freedom in a commons brings ruin to all” (Hardin, 1968). Since the 1960's this statement has brought concerns on the limits of human growth, recognizing that humans live in a finite planet with limited resources availability; this highlights the need for appropriate management of natural storages of resources to maintain the commons. According to Franz and Campbell (2005), the ecological ethic represented by the “vivantary responsibility” can be adduced as follows: (i) human life is dependent on life support system; (ii) we ought to protect human life; (iii) therefore, we ought not to do anything that imperils the life support system. Franz (2001) states that “vivantary responsibility” stands for the human obligation to protect the life support system, an ecological ethic of care. Advances toward an understanding of the relationship between human kind and nature has been carried out more densely these last 50 years. Among others experts, Odum (1996) argues that natural capital and ecosystem services are the real source of wealth, despite the common belief held by economists that it is labor and economic capital that are such source. In this sense, obtaining indicators of sustainability for diagnostic studies under biophysical bases (e.g., life cycle assessment, emergy accounting, etc.) could be considered crucial in supporting decision toward a sustainable society.

Although the indicators calculated under biophysical basis can provide important information on sustainability, those indicators usually have low practical use in supporting decisions for the management of companies at any scale. The point is that managers mainly consider economic indicators for their decisions, and this pattern will hardly be changed. Looking toward a sustainable development, efforts have been carried out aiming to include biophysical indicators expressing sustainability in the companies' decisions. On this issue, some examples can be found in scientific literature. Thorton (2013), for instance, highlights the importance of green accounting, by suggesting the inclusion of the so-called asset-retirement obligations (AROs) within the bookkeeping practices; in short, the AROs are a way to account for the action of allowing the company to establish its operation in return for exacting a promise to clean up the environment when operations cease. Similarly, based on the idea that emergy (with an “m”; Odum, 1996) content of a flow or storage is a measure of value, quality and real wealth, emergy could be considered as a proper measure of the Commons. Under this perspective, Bimonte and Ulgiati (2002) proposed the emergy and environmental taxation schemes (Envitax) as a way to quantify and tax companies. As another example, Campbell (2005, 2013) proposed the emergy-based environmental debt accounting as a new scheme for the traditional bookkeeping techniques. According to author, emergy and emdollars fit logically into the format of standard financial accounting and bookkeeping tools, resulting in an unified system of emergy and money accounting that could support political decisions on questions of appropriated debt load to be carried by society, and repaying the existing debts. All in all, there are possibilities in what concerns quantifying, taxing, and even adding environmental loads within the traditional accounting schemes as standardized by the International Financial Reporting Standards (IFRS), however, who will manage the received money and who will decide where that money should be applied to restore and preserve natural capital are still questions without proper answers.

According to Ulgiati et al. (2009), these aspects need special attention since the reinforcement feedback from humans to nature plays a crucial role in the whole process of keeping the natural system functioning and able to generate new resources and essential services for societal development. Rather than taxing companies for their environmental load (i.e., acting after the problem has been created; an action done by external decisors), a promising alternative would be considering sustainability indicators within company's decision tools (i.e., acting before creating the problem; an action done by company's internal decisors). In this sense, incorporating sustainability-related indicators in management decision tools that are already accepted and widely used by the companies could lead to practical actions toward sustainability. Among others, the activity-based cost (ABC; Cooper and Kaplan, 1988) tool appears as the most promising one. It is important to point out that ABC is not related to a company's balance sheet, so it is not subject to the international accounting rules and it is not considered by the government for tax calculations.

ABC is a method used by companies for internal management and useful to create scenarios under simulation considering product-cost, production volume, and products diversification, providing subsidies for decisions toward profit increase. Since profits are the current main target for the company managers, economic drivers are considered when applying the ABC procedure, however, those drivers could be replaced by environmental-related ones to subsidize decisions for sustainability. Among others, efforts in this sense have being developed by Tsai et al. (2010, 2012, 2015); Bagliani and Martini (2012), and Yang et al. (2016) by integrating environmental cost-accounting and emissions inventory within the traditional ABC, however, none of these approaches recognize the quality of energy, the hierarchical energy scale, and the energy donor side perspective as emergy accounting does.

This work aims to integrate the environmental sustainability aspect into the traditional ABC method as an attempt to provide an innovative business model to replace the current practices exclusively focused on economic issues. Specifically, the inclusion of emergy flows as drivers into the traditional ABC method in managing a company's overheads is put forward. The procedure includes the contextualization of a sustainability model, followed by the establishment of economic and environmental drivers to be used into the ABC, and the application of goal programing to deal with multicriteria approaches. The hypothesis is that the proposed procedure results in an optimized choice to reach better balance between economic and environmental performances for companies.

Methods

Allocating Companies' Overheads Through Economic and Environmental Drivers

The more precise the cost allocation is, the more precise will be the information generated supporting a company's decision on which product should be prioritized in terms of production and sales to the market, or even which product-mix should be produced based on goals to thrive the companies' strategy (Ponisciakova et al., 2015). The costing management system known as Activity Based Costing (ABC) attempts to increase the accuracy in cost allocation to allow decisions on company's product-mix, break-even-point, and contribution margin. ABC was developed by Cooper and Kaplan (1988) from their professional skills as entrepreneur consultants, and was recently updated and named as Time Driven Activity Based Costing aiming to reduce the implementation difficulties and making adaptations by the users, whenever necessary, easier (Kaplan and Anderson, 2007). Both ABC approaches are largely applied in different production sectors and organizations, as detailed by Tsai et al. (2014), while the choice for one or the other depends on the company's management goals. For this present work, the traditional ABC is used considering different drivers for overheads costs allocation.

Ellis-Newman and Robinson (1998) argue that ABC supports decision makers in improving or eliminating all company's inefficient activities, thus resulting in an efficiency improvement and profitability. ABC allocates the company's overheads (i.e., indirect costs) to products following a different approach, when compared to the Traditional Costing Systems (TCS), which allocate overhead costs to the products without considering the complexity of production systems and their infrastructure, which also include administration offices; TCS can be considered useful when allocating direct costs, but the indirect costs are disregarded. Overheads have been receiving higher importance over the years, since their percentage in the company's total production costs have increased from 15 to 45% in average (in some cases reaching up to 90%; Kolosowski and Chwastyk, 2014); the reasons of overheads increase is mainly due to automation of manufacturing processes and outsourcing services.

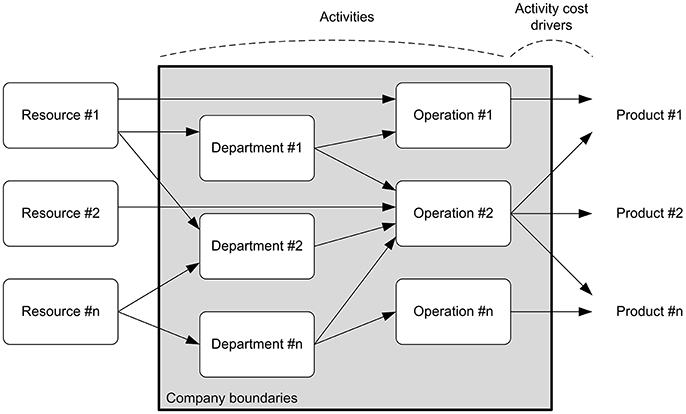

For a brief explanation on how the ABC works, Figure 1 shows the costs allocation drivers. Driver is a reference value carefully chosen to allocate the resource cost to activities demanding that resource, and to allocate the cost attributed by an activity to the products. To properly use the ABC, it is crucial to choose allocation drivers with strong cause-effect relation between the resources and activities, and between activities and products. The stronger the cause-effect relation, the more precise the results will be, which supports a better-based decision (Cooper, 1990). Traditional drivers used within the ABC are production time, industrial area occupied, machine power-rating, machine setup, and the amount of labor hours, which helps to understand which products should be reduced or eliminated, which materials to change, and what process should be modified in order to reach higher profits for the company.

Figure 1. Allocating company's overheads under the ABC framework.

Although recognizing that economic aspects are important in sustaining the company's perpetuation over time in a competitive market, the environmental and social aspects are beginning to be considered as having similar importance; this is related to the sustainable development definition by the Brundtland (1987) report. In this sense, some adaptations in the ABC framework are being assessed to better fit the companies' objectives and the way they operate. For instance, Tsai et al. (2010) applied a modified ABC to allocate the overheads, originated from the environmental sector of a given company, to their products; this approach was initially proposed by the United States Environmental Protection Agency (USEPA). The authors replaced the traditional cost drivers, which measure only economic aspects, with drivers related to the CO2 emissions released from the company's production processes. As a result, those products that release the most CO2 received more overheads (i.e., they were penalized) than others with lower emissions. The work of Tsai et al. (2010) is here considered as reference for primary data of overheads, as well for economic and environmental drivers. Since both approaches are well developed and known by the scientific community, the procedure in obtaining emergy drivers receives higher attention in this work.

Among other examples, Schulze et al. (2012) proposed a conceptual framework for ABC to assess inter-firms relationships instead of focusing on intra-firms as usual. In this study, a larger scale analysis is considered, under a supply chain perspective. Main outcomes emphasize that ABC can be applied in the supply chain for inter-firms purposes, but this has been done in a limited way, resulting in a decrease of efficiency in identifying key aspects for improvements. Tsai et al. (2012) applied emissions as drivers in allocating overheads for projects of buildings aiming to support a greener fleet with reduced CO2 emissions. Bagliani and Martini (2012) developed a framework to use the ABC and environmental pressures simultaneously (specifically the footprint method) associated with companies' production. Authors state that the proposed framework is useful for complex and multi-utility production systems, whose initial environmental impacts can hardly be directly assigned to final products. Authors suggest that the proposed framework enables for choosing processes with a high utilization of renewable resources and low carbon emissions.

Proposals to modify the ABC by including environmental aspects could be considered as a positive step in supporting companies' decisions toward more sustainable production systems. This is true since more than economic drivers are considered within the ABC framework. Although seen as an important advance, the proposed modifications considering emissions as drivers for company overheads still lacks a better defined conceptual model of sustainability. In other words, using emissions as drivers will support decisions based exclusively on emissions.

The Conceptual Model of Sustainability Behind the Proposed Modified ABC

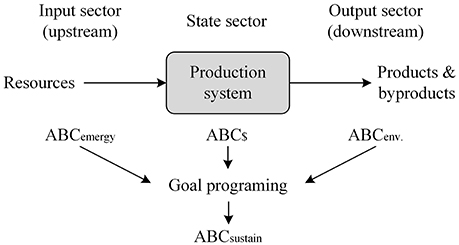

Pulselli et al. (2015) emphasize that sustainability is an issue of relationship among compartments. The conceptual sustainability model developed by Pulselli et al. (2011) shows the evolution of the triple bottom line sustainability model based on a triangle divided in levels of priority, in which the environment is the basis and supports societal development (intermediary level), while the upper level represents the economy. These authors argue that ecosystems are open systems where energy and matter cross their boundaries to perform and maintain their functions, aiming to maximize the conversion of system inputs into useful goods and services outputs. Thus, through an analogy between the sustainability model represented by an inverted triangle with the energy flows crossing the open system boundaries, the input-state-output (ISO) sustainability model is established (Figure 2); this model can be applied to different natural and human-made systems (Pulselli et al., 2011; Bastianoni et al., 2016), including companies.

Figure 2. Production systems as open systems showing the sectors in which the three different ABC approaches are focused on.

Figure 2 presents the proposed model of sustainability in an attempt to better represent the sustainability of companies, including input resources flows, the production processes, and the output of products and by-products. As representatives of each sector in the ISO model, emergy accounting (with an “m”; Odum, 1996), technical-economic approach and emissions are respectively considered. Pulselli et al. (2011) argue that using emergy accounting as a system input can represent the biophysical counterpart of the system output, i.e., emergy accounting is able to quantify the effort of natural environment in providing resources for human activities to reach the desirable societal well-being. Still regarding the input sector, the importance of quantity and quality of resources as key elements for system development is recognized. Thus, environmental accounting using emergy rather than other biophysical approaches is important because it is based on a systemic view and considers a donor-side perspective that takes into account all resources from nature and from a larger economy required by the transformation system to provide a service or a product, which enables it to recognize the quality of energy (Agostinho et al., 2016); in this sense, the input is represented in this work by the ABCemergy measured in solar emjoules (abbreviated as sej).

The state sector is represented by the ABC$ in monetary units ($) as traditionally used. The “machine hours” driver was here considered in allocating overheads for the ABC$, however, other drivers are usually included as “hours of man-work” or even “employees training sections” that could represent the social aspect of ISO sustainability conceptual model. The output sector is represented by the ABCenv. (Tsai et al., 2010, 2012) which includes the emissions released into the environment by the productive process (e.g., kgCO2eq).

By considering the proposed model of sustainability and its corresponding indicators for ABC, it is expected that the company's internal management also consider the prerogative of sustainability in their decisions, which would be beneficial for the economic aspects of companies as well as for the entire society through the increase of Earth's biocapacity. The goal of this work is not to change the already acceptable and widely used ABC's framework managing method, but to present an alternative to replace the traditional use of ABC focused on economic aspects with a more holistic perspective of sustainability. And to reach this goal, the drivers used in allocating a company's overhead are changed according to different methodological approaches supporting the proposed sustainability model. Since calculating traditional and environmental (emissions) drivers are well presented in literature, the next section presents, in detail, drivers based on emergy accounting.

ABCemergy: Using Emergy Drivers to Allocate Company's Overheads

According to Odum (1996, p. 7), emergy is the available energy of one kind previously used up directly and indirectly to make a service or product. Emergy accounting is routed on thermodynamic bases and system theory, with features that make it a powerful scientific-based tool when assessing sustainability, including a donor- side approach in quantifying value, biophysical basis; it recognizes the quality of energy, and suggests a universal energy hierarchy based on the energy quality concept. Emergy accounting can be applied for different purposes, but usually, its use is related to the calculation of environmental performance indicators. Among those, the Unit Emergy Value (UEV) evaluates the emergy efficiency or the global efficiency in converting resources into goods and services; its unit relates the emergy demanded by the production system (in solar emjoules or sej) with the system output (usually in kg, J, or $ units). Although firstly expressing the efficiency in converting resources into goods and services, the UEV could also be related to the sustainability concept since using lower amounts of resources (renewable and/or nonrenewable) could increase the Earth's biocapacity. Indirectly, the same comment can be applied to the total emergy demanded by systems: using lower amounts of emergy suggests, at principle, more sustainable systems due to lower amount of global resources needed in their production processes—this is an important premise of this work. It is also recognized that a system demanding a high amount of emergy from renewable sources is also more sustainable, however, this hardly happens when it comes to companies since they are mostly dependent on resources from the economy, which are classified as non-renewable. A potential advancement of the proposed ABCemergy approach could be by identifying the origin of resources (renewable or non-renewable sources) and including this information when accounting for the emergy demanded by production systems; this could support more accurate results about the sustainability of the evaluated systems.

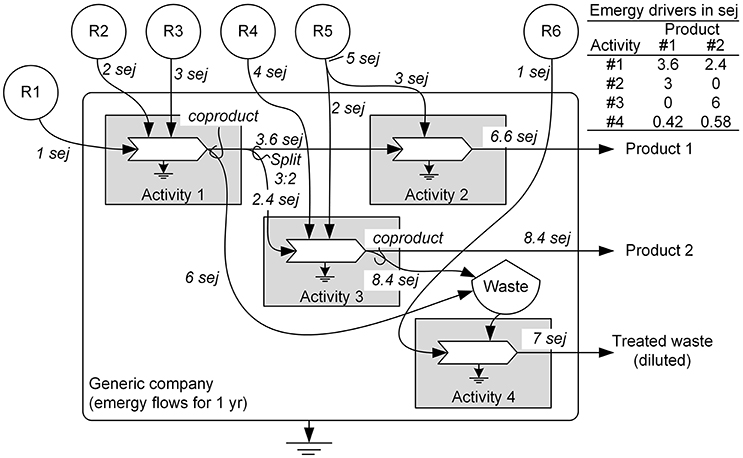

As a result of the increasing number of published emergy studies and the strengthening of emergy society (emergysociety.com), the amount of UEVs available in scientific literature and databases is increasing exponentially, making its usage more accessible. It must be emphasized that rules for emergy algebra are respected, as described by (Brown, 2015, p. 273): Rule #1—emergy is the available energy (exergy) of one kind that is used up in transformations directly and indirectly to make a product or service; Rule #2—in processes having one output, all independent emergy inputs are assigned to the processes' output; Rule #3—when a pathway splits, the emergy is assigned to each branch of the split based on its percent of the total available energy flow (or mass) on the pathway before the split; Rule #4—in processes having two or more co-products, all independent input emergy is assigned to each co-product; Rule #5—within a system, emergy cannot be counted twice, (a) emergy in feedbacks cannot be doubled counted, (b) co-products, when reunited cannot be added to equal a sum greater than the source emergy from which they were derived. Figure 3 shows the application of emergy rules in a generic company for illustrative purposes.

Figure 3. Energy diagram of a generic company to exemplify the emergy-based drivers calculation. R, external resources.

To be considered as a driver within the ABC framework, the interpretation of emergy algebra rule #1 needs to be adapted to fit into the cause-effect relation required when allocating overheads. Precisely, only the emergy from external sources applied in a company transformation activity (i.e., the emergy flowing from outside the company boundaries) is accounted for, disregarding the emergy carried with a product from the previous internal transformation activity. This adaption is important to avoid that a company activity located on the right side of a production chain be always penalized with the emergy of previous activities. To exemplify this approach, Figure 3 shows the emergy flows for a generic company and its emergy drivers. Focusing on activity #1, it demands emergy from R1, R2, and R3 external sources totalizing 6 sej, while activity #2 demands a total of 3 sej from R5. Similarly, activity #3 requires 6 sej from R4 and R5 sources, and activity #4 demands 1 sej from R6. The emergy demand by activity #4 of 1 sej from R6 is an indirect cost of products #1 and #2, thus it is allocated to them according to the ABC theory; for this, the total emergy of products #1 and #2 are considered as parameters for allocation. When focusing on both activities and products at the same time to establish the emergy drivers, the reading is as follows: product #1 receives 3.6 sej in activity #1, added to 3.0 sej in activity #2 and 0.44 sej in activity 4; product #2 receives 2.4 sej in activity #1, added to 6 sej in activity #3 and 0.56 sej in activity #4. Final emergy drivers are shown in the above-right table at Figure 3.

Although emergy rule #1 is differently interpreted to fit the ABC concepts and goals, the emjoules flows from external sources that are carried by products within the company still embody all previous directly and indirectly available energy to make the external source available due to the usage of UEVs. As a result, those companies' activities demanding more emergy will receive larger amounts of total overheads, which means they are causing a larger load (or stress) on the environment by demanding larger amounts of resources than all other activities. For example, the emergy drivers provided on the table in Figure 3 indicate that product #1 should receive about 60% of total overheads in activity #1 (3.6 sej of 6 sej in total), whereas product #2 should receive the remaining 40% (2.4 sej). This implies that, in an attempt to reduce the emergy demanded by company, product #1 should receive more attention for actions from managers than product #2 during activity #1.

The ABCemergy puts in evidence the companies' products that demand higher efforts from the natural environment to be produced, in other words, a larger part of total overheads will be allocated to them. The same approach is used as for the ABC$ and ABCenv., however these will focus on economic and emissions drivers and will put in evidence a perspective other than emergy. For this reason, and also by considering the conceptual model of sustainability as presented in the Figure 2, the use of multicriteria techniques [goal programming (GP) in this work] are mandatory to support decision makers.

Goal Programming Supporting a Multicriteria-Based Decision

Goal Programming (GP) is a subset of multi-objective optimization (MOO) based on linear or nonlinear programming to solve multidimensional and contradictory issues (Marler and Arora, 2004). Linear programming considers the goals as hard constraints, while GP can deal with conflicting goals, or soft constraints. Introduced by Charnes and Cooper (1977), the GP aims to minimize the unwanted deviation from a goal, represented mathematically as . GP can mathematically be expressed as ∫i(x)+ni−pi = , where di = ni−pi of a function (Hanks et al., 2017). Mathematical modeling is necessary to assign the equations represented in a general form as Min , subject to ∫i(x)+ni−pi = . Among others, similar techniques derived from the GP are The Lexicographic Goal Programming, Weighted Goal Programming, and Chebyshev Goal Programming.

GP is a widely recognized and used tool supporting decisions based on multi-criteria perspectives in the scientific and non-scientific communities. Among several other examples, its application includes a decision making process to choose among potential renewable energy plants considering contradicting goals, like social aspects, financial, and location (Zografidou et al., 2017), or to support a better choice between public transport projects considering social and financial aspects (Yang et al., 2016), or to choose a community energy plan among several options with different performances for techno-economic aspects (Huang et al., 2017). The usage of GP requires a deeper understanding about how the production system assessed works, and precise information supported by primary data. Considering that its application varies from system to system, rather than provide all mathematical theory behind GP, the next section presents data, assumptions and the complete models used in this work to allow results replication; for deeper mathematics details and concepts supporting GP please see Charnes and Cooper (1977).

Results and Discussion

The ABC$ is widely known and used by companies, and the usage of ABCenv. has been increasing over the last few years. Thus, in this work the ABCemergy receives higher attention, as well as the junction of these three approaches in the goal programing to provide better information for decision makers. As the main goal is to provide sustainability-based information regarding the procedure proposed rather than a real study case, a generic company is used as reference by considering primary data from Tsai et al. (2010).

Applying the ABC$ and ABCENV. in a Generic Company

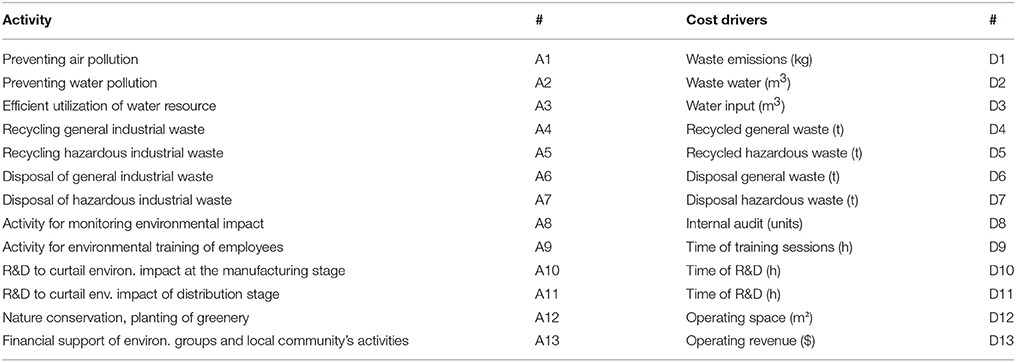

Table 1 presents the activities and cost drivers as used by Tsai et al. (2010), who modified the initial framework of EPA (1995) by replacing the technical cost drivers with others, representing the end of pipe emissions, environmental damages prevention, environmental regulation, environmental taxes, and environmental training hours.

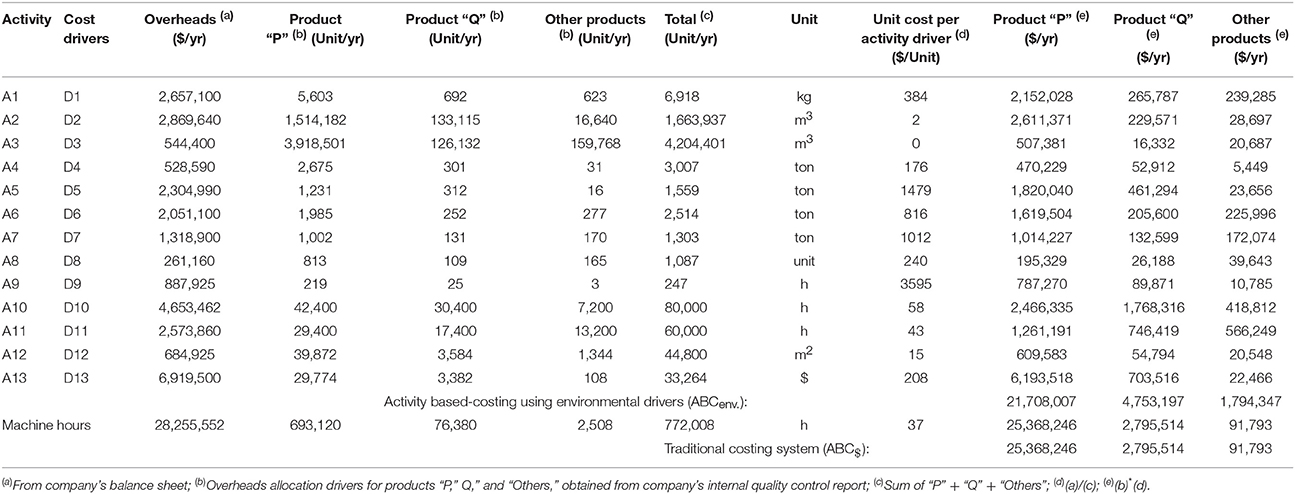

Table 1. Company's activities and drivers considered by Tsai et al. (2010).

After defining new drivers representing the ABCenv., Table 2 shows the overhead allocation for the studied company through traditional (ABC$) and environmental (ABCenv.) approaches. Using the ABC$, product “P” receives 25.3 million USD/yr, while “Q” receives 2.7 million and all other products with 92 thousand USD/yr altogether. Although providing important indication about what product is responsible for most of the company's overhead, this ABC approach does not provide any information regarding which activity is the most representative in causing that overhead. Thus, the likely actions that company's manager can take are essentially focused on products, i.e. reducing or increasing the production amount of those products with higher influence on overheads (i.e., product “P” in this case), or replacing them with others, or even changing product processes.

Table 2. Activity- based costing using environmental drivers (ABCenv.) and traditional costing system (ABC$) for the environmental sector evaluated by Tsai et al. (2010).

Differently from ABC$, the ABCenv. considers the company's activities when allocating overheads and, mainly, it considers different drivers for allocation according to the either stronger or weaker relationship between activities and their overhead-related costs. In so doing, Table 2 shows the following overhead allocation for ABCenv.: about 21.7 million USD/yr for product “P,” 4.7 million for “Q,” and 1.7 million for all other company products. The first reading is that results are different between ABC$ and ABCenv., since different allocation drivers were considered. This implies that managers can take different decision toward the overhead reduction according to method used for calculations. Notwithstanding, decisions will be based on the meaning of the drivers used, i.e., rather than focusing on pure economic purposes as done by ABC$, the ABCenv. focuses on environmental issues as the ones listed on Table 1. Under a sustainability perspective, this can be deemed important since environmental issues are being, mainly over the last few years, mandatory aspects basing decisions at any level. The second observation on Table 2 is that ABCenv. enables to verify which company's activity is more intensively affecting the final results. Thus, decisions can be made not exclusively based upon the amount and kind of company products, but now the activities can also be the target for improvements in order to achieve total overhead reduction.

In short, the ABCenv. can be seen as an advancement of the ABC$ in the following two aspects: (i) environmental drivers are strictly related to sustainability issues and they are now also considered for decisions rather than exclusively economic ones; (ii) distinguishing the company's activities allows for decisions focused on both products and activities.

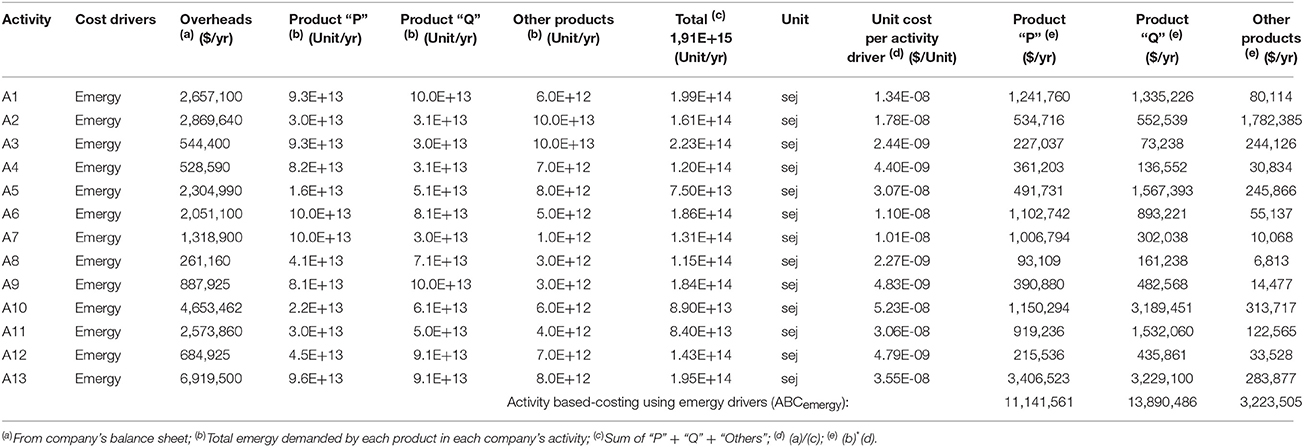

Applying the ABCemergy

Both ABC approaches previously presented consider economic and emissions aspects as drivers, but emergy is now considered as a cost driver to fulfill the conceptual model of sustainability adopted in this work. The ABCemergy appears as a new variable to be taken into consideration by the decision maker, which aims to quantify the environmental efforts in providing resources for the company's production activities. Under this approach, the overheads are allocated based on the global resources demanded by the company. Table 3 shows the following allocation results from the ABCemergy: about 11.1 million USD/yr are allocated to product “P,” 13.8 million to “Q,” and 3.2 million for all other products.

Table 3. Activity based-costing using emergy drivers (ABCemergy) for the environmental sector evaluated by Tsai et al. (2010).

It is important to highlight that emergy drivers considered on Table 3 (precisely columns #4-6) were randomly assumed without a deeper evaluation, due to lack of precise data regarding the production system evaluated by Tsai et al. (2010), which is the source of primary data for this work. Although this could be considered as a limitation of this present work, our intention herein was not to provide a real and precise ABC diagnostic, instead, the main goal is to propose an alternative framework in using the ABC that could result in better sustainability-based final indicators for managers. Notwithstanding, in possession of all the descriptive information about a company's production flowchart, the procedure presented in Figure 3 can be easily applied by someone in obtaining precise emergy drivers.

As expected, Tables 2, 3 show different values for a company's overhead allocation to products, since different cost drivers were used in the allocation procedure; ABC$ focuses on monetary aspects, whereas ABCenv. focuses on emissions and ABCemergy focuses on the effort of natural environment in providing resources. When simultaneously used, the three approaches for ABC respect the conceptual model of sustainability adopted in this work, which means that jointly considering all three approaches will result in sustainability-based indicators to be further used by managers in reducing company's overheads. For this, it is necessary to merge the obtained numbers that result on a multicriteria issue, and this subject is discussed in the next section by applying GP.

Goal Programming Supporting Decisions Toward Higher Degrees of Companies' Sustainability

More than overheads in USD/yr distributed among products under the three different ABCs approaches as previously presented, the managers usually demand information on units that allow them to more easily understand the current company's performance and take decisions toward improvements as promptly as possible. In this sense, managers prefer information in units of “amount of products” that should be produced rather than values in “USD/yr”. Therefore, Table 4 shows the overheads distributed for the three ABCs individually viewed in units of “amount of products.” To obtain these numbers, different GP models were performed (Appendices 1–4) and run by using the LINGO® 11 software. It is important to emphasize that proposed models do not represent a real company, but rather, as previously mentioned, our intention is to provide essential information to readers who may wish to replicate this work and/or apply the same approach in a specific case study. In so doing, the models in Appendices can be changed to pursue different goals, however, always respecting the conceptual model of sustainability as established herein.

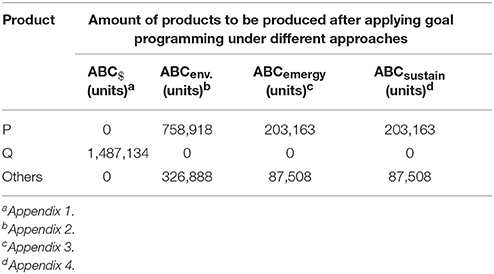

Table 4. Amount of products that should be produced by the studied generic company, according to different ABC approaches.

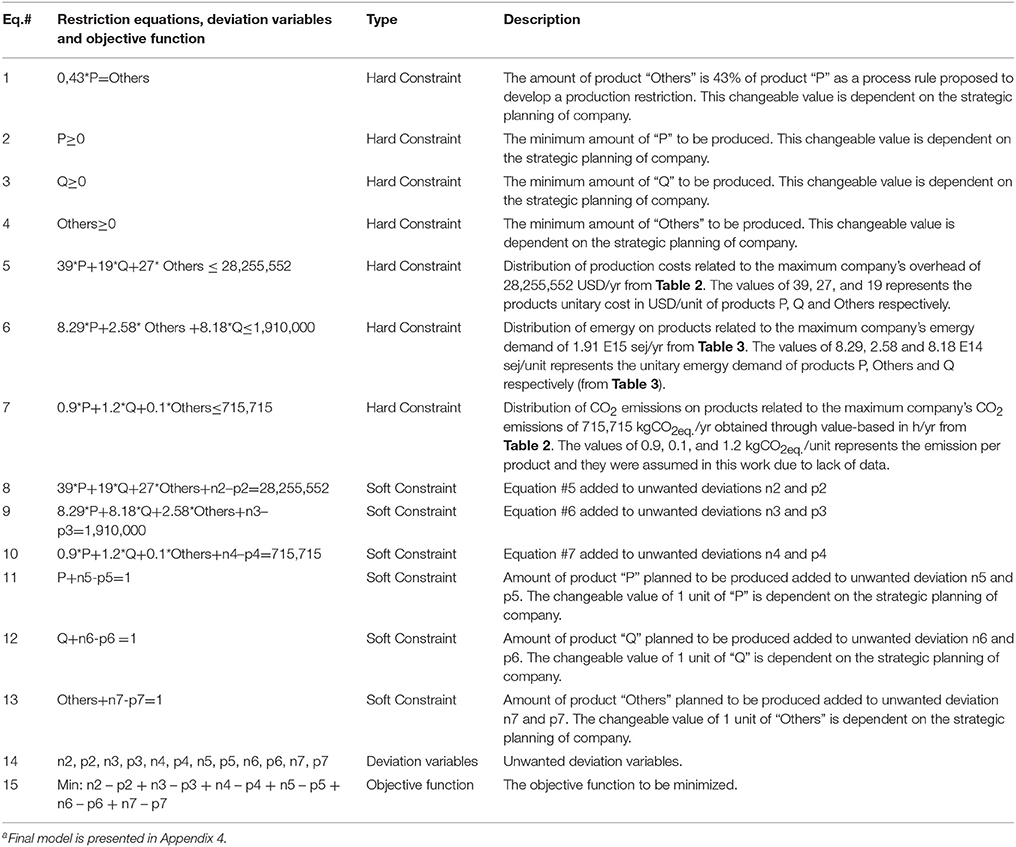

Table 4 shows different values for the “amount of products” for the different ABCs. For instance, while the ABC$ promotes the production of “Q,” the ABCenv. and ABCemergy promote essentially “P” and a moderate amount of “Others.” Although providing important information for managers, none of these three approaches alone is able to represent sustainability-based information, which claims for a joint assessment perspective as proposed by the conceptual model of sustainability as presented in Figure 2. For this, the results of all three individual ABC approaches can now be modeled under the concepts of GP, including the restrictions (hard or soft constraints) for each ABC approach, deviation variables and objective function as described in Table 5. Modeling this integrated ABC (named ABCsustain heretofore) demands some efforts, however the basic idea is to merge all advantages of every individual ABC (emergy, economic and emissions) to obtain final indicators to provide managers with sustainable-based information.

Table 5. Description of the variables considered in modeling the final goal programming merging the three ABCs approachesa.

After running the ABCsustain model, a plausible solution provided by GP is presented in the last column on Table 4. The numbers indicate that the amount of product “P” should be approximately 203 thousand units, while product “Others” should receive lower priority with 87 thousand units. It is interesting to note that product “Q” should not be produced at all in order to allow for higher degrees of sustainability to be achieved by the company. Additionally, final numbers from the ABCsustain is the same as those provided by the emergy perspective; this is a result of the modeling specificities assumed in this work, however any change in the boundary conditions will induce to different results.

According to the premises of this work, if the manager aims to increase the company's degree of sustainability, the amount of products provided by the ABCsustain must be respected; this is the main goal of this work. Interesting to note that ABCsustain provided different figures compared to the traditional ABC$, implying that whether the managers accept the indicators from the proposed ABCsustain, the reduction of monetary costs probably will not be maximized. This could affect the company's profitability, since costs management is an important aspect as the amount of products sold and their market price.

It is important to emphasize that, instead of a real case study, the goal of this work was to propose the ABCsustain supported by all three different allocation drivers and a conceptual model of sustainability. Thus, the assumptions on primary data can be easily overcome when applying the proposed approach in a real case study with available data. For advances over this study, future efforts could be focused on considering additional constraints in the proposed model, including company profit, process capacities, market demand for products, “takt time,” and others. This could lead to an even more detailed and generalized model to be applied in different production systems, however always respecting the conceptual model of sustainability as proposed in this work.

Conclusions

The result of the ABCsustain provides a mix of products considered as an optimized solution by the GP supporting a multi-criteria-based decision. Results indicate that producing 203 thousand units of product “P,” 87 thousand units of “Others” and zero of “Q” will lead to a higher degree of sustainability for the evaluated company. Rather than using exclusively economic drivers that lead to a company's costs reduction and, consequently, profit increase, the proposed change in the business as usual thinking respect the company's budget designed for production and it also considers environmental aspects in its strategic planning. The goal is to reach economic growth based on sustainable principles, i.e., it is crucial maintain the health of natural capital while also recognizing the fundamental importance of economy.

The inclusion of emergy drivers into the activity-based cost method could represent an innovative business approach in allocating a company's overheads to products. This is true since it supports a decision also based on a reduced emergy demand and, a priori, causing lower load on the natural environment by requesting a lower amount of energy and materials for the production processes. Using emergy as driver comes to collaborate in a synergic manner with the already established approaches in allocating overheads under economic and environmental (i.e., emissions) perspectives. Establishing a conceptual model of sustainability that embraces these three perspectives shown, at least theoretically, comes to be a more scientific-based approach in supporting quantitative information aligned with sustainable development. Thus, managers in charge of strategic decisions within companies can use this optimized tool and put it into practice in the production processes in order to reach a better balance (complying with the restrictions modeled) among emergy, economic and emissions performance for companies.

Author Contributions

HM: General work organization and raw data obtainment. FA: General work organization, ABC drivers calculation and discussions. CA: Emergy-based drivers obtaintion and discussions. BG: Economic and environmental drivers discussions. RM: Goal programming application and discussions.

Conflict of Interest Statement

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Acknowledgments

The first draft of this work was first presented during the Biennial Workshop Advances in Energy Studies (BIWAES) held in Naples, Italy, September 2017. Authors are grateful for the financial support from Paulista University (UNIP), CAPES Brazil via the Prosup Program, and CNPq Brazil (307422/2015-1). Thanks also to José Hugo de Oliveira for the English language review, and for the valuable comments of the reviewers.

Supplementary Material

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenrg.2018.00036/full#supplementary-material

References

Agostinho, F., Sevegnani, F., Almeida, C. M. V. B., and Giannetti, B. F. (2016). Exploring the potentialities of emergy accounting in studying the limits to growth of urban systems. Ecol. Indic. doi: 10.1016/j.ecolind.2016.05.007. Available online at: https://www.sciencedirect.com/science/article/pii/S1470160X16302400

Bagliani, M., and Martini, F. (2012). A joint implementation of ecological footprint methodology and cost accounting techniques for measuring environmental pressures at the company level. Ecol. Indic. 16, 148–156. doi: 10.1016/j.ecolind.2011.09.001

Bastianoni, S., Coscieme, L., and Pulselli, F. M. (2016). The input-state-output model and related indicators to investigate the relationships among environment, society and economy. Ecol. Modell. 325, 84–88. doi: 10.1016/j.ecolmodel.2014.10.015

Bimonte, S., and Ulgiati, S. (2002). “Exploring biophysical approaches to develop environmental taxation tools. Envitax, to face the “new scarcity”,” in Economic Institutions and Environmental Policy, eds M. Franzini and A. Nicita (Aldershot, UK: Ashgate Publishing Limited), 177-200.

Brown, M. T. (2015). Emergy and form: accounting principles for recycle pathways. J. Environ. Account. Manag. 3, 259–274. doi: 10.5890/JEAM.2015.09.005

Brundtland, G. H. (1987). Report of the World Commission on Environment and Development: Our Common Future. Available Online at http://www.un-documents.net/our-common-future.pdf. [Accessed 2nd October 2017].

Campbell, D. E. (2005). “Financial accounting methods to further develop and communicate environmental accounting using emergy,” in Emergy Synthesis 3, Theory and Applications of the Emergy Methodology, eds M. T. E. Brown, D. E. Bardi, V. Campbell, S. Comar, T. Huang, D. T. Rydberg, and S. Ulgiati (Gainesville, FL: Center for Environmental Policy, University of Florida), 185–198.

Campbell, D. E. (2013). Keeping the books for the environment and society: the unification of emergy and financial accounting methods. J. Environ. Account. Manag. 1, 25–41. doi: 10.5890/JEAM.2012.01.003

Charnes, A., and Cooper, W. W. (1977). Goal programming and multiple objective optimizations: part 1. Eur. J. Oper. Res. 1, 39–54. doi: 10.1016/S0377-2217(77)81007-2

Cooper, R. (1990). Implementing an activity-based cost system. J. Cost Manage. Manufact. Ind. 4, 33–42.

Cooper, R., and Kaplan, R. S. (1988). Measure costs right: make the right decisions. Harv. Bus. Rev. 66, 96–103.

Ellis-Newman, J., and Robinson, P. (1998). The cost of library services: activity-based costing in an Australian academic library. J. Acad. Librar. 24, 373–379. doi: 10.1016/S0099-1333(98)90074-X

EPA (1995). United States Environmental Protection Agency. An Introduction to Environmental Accounting as a Business Management Tool: Key Concepts and Terms. EPA 742-R-95-001. Available online at: https://www.epa.gov/sites/production/files/2014-01/documents/busmgt.pdf. (Accessed 23rd January 2018).

Franz, E. H. (2001). Ecology, values, and policy. Bioscience 51, 469–474. doi: 10.1641/0006-3568(2001)051[0469:EVAP]2.0.CO;2

Franz, E. H., and Campbell, D. E. (2005). “Vivantary responsibility and emergy accounting,” in Emergy Synthesis 3, Theory and Applications of the Emergy Methodology, eds M. T. E. Brown, D. E. Bardi, V. Campbell, S. Comar, T. Huang, D. T. Rydberg, and S. Ulgiati (Gainesville, FL: Center for Environmental Policy, University of Florida), 229–234.

Hanks, R. W., Weir, J. D., and Lunday, B. J. (2017). Robust goal programming using different robustness echelons via norm-based and ellipsoidal uncertainty sets. Eur. J. Oper. Res. 262, 636–646. doi: 10.1016/j.ejor.2017.03.072

Hardin, G. (1968). The tragedy of the commons. Science 162, 1243–1248. doi: 10.1126/science.162.3859.1243

Huang, Z., Yu, H., Chu, X., and Peng, Z. (2017). A goal programming based model system for community energy plan. Energy 134, 893–901. doi: 10.1016/j.energy.2017.06.057

Kaplan, R. S., and Anderson, S. R. (2007). Time-Driven Activity-Based Costing: a Simpler and More Powerful Path to Higher Profits. Brighton; Boston, MA: Harvard Business School Press.

Kolosowski, M., and Chwastyk, P. (2014). Economic aspects of company processes improvement. Proc. Engineer. 69, 222–230. doi: 10.1016/j.proeng.2014.02.225

Marler, R. T., and Arora, J. S. (2004). Survey of multi-objective optimization methods for engineering. Struct. Multidiscip. Optimiz. 26, 369–395. doi: 10.1007/s00158-003-0368-6

Odum, H. T. (1996). Environmental Accounting: Emergy and Environmental Decision-Making. New York, NY: John Wiley & Sons.

Ponisciakova, O., Gogolova, M., and Ivankova, K. (2015). Calculations in managerial accounting. Proc. Econ. Fin. 26, 431–437. doi: 10.1016/S2212-5671(15)00837-0

Pulselli, F. M., Coscieme, L., and Bastianoni, S. (2011). Ecosystem services as a counterpart of emergy flows to ecosystems. Ecol. Modell. 222, 2924–2928. doi: 10.1016/j.ecolmodel.2011.04.022

Pulselli, F. M., Coscieme, L., Neri, L., Regolim, A., Sutton, P. C., Lemmi, A., et al. (2015). The world economy in a cube: a more rational structural representation of sustainability. Glob. Environ. Change 35, 41–51. doi: 10.1016/j.gloenvcha.2015.08.002

Schulze, M., Seuring, S., and Ewering, C. (2012). Applying activity-based costing in a supply chain environment. Int. J. Prod. Econ. 135, 716–725. doi: 10.1016/j.ijpe.2011.10.005

Thorton, D. B. (2013). Green accounting and green eyeshades twenty years later. Critic. Perspect. Account. 24, 438–442. doi: 10.1016/j.cpa.2013.02.004

Tsai, W., Chang, Y., Lin, S., Chen, H., and Chu, P. (2014). A green approach to the weight reduction of aircraft cabins. J. Air Transp. Manag. 40, 65–77. doi: 10.1016/j.jairtraman.2014.06.004

Tsai, W., Lee, K., Liu, J., Lin, H., Chou, Y., and Lin, S. (2012). A mixed activity-based costing decisions model for green airline fleet planning under the constraints of the European Union Trading Scheme. Energy 39, 218–226. doi: 10.1016/j.energy.2012.01.027

Tsai, W., Lin, T. W., and Chou, W. (2010). Integrating activity-based costing and environmental cost accounting systems: a case study. Int. J. Bus. Syst. Res. 4, 186–208. doi: 10.1504/IJBSR.2010.030774

Tsai, W., Tsaur, T., Chou, Y., Liu, J., Hsu, J., and Hsieh, C. (2015). Integrating the activity-based costing system and life-cycle assessment into green decision-making. Int. J. Prod. Res. 53, 451–456. doi: 10.1080/00207543.2014.951089

Ulgiati, S., Zucaro, A., and Franzese, P. P. (2009). “Emergy and a policy of the commons,” in Emergy Synthesis 5, Theory and Applications of the Emergy Methodology, eds M. T. Brown, S. Sweeney, D. E. Campbell, S. Huang, E. Ortega, T. Rydberg, D. Tilley, and S. Ulgiati (Gainesville, FL: Center for Environmental Policy, University of Florida), 1–14.

Yang, C., Lee, K., and Chen, H. (2016). Incorporating carbon footprint with activity-based costing constraints into sustainable public transport infrastructure project decisions. J. Clean. Prod. 132, 1154–1166. doi: 10.1016/j.jclepro.2016.06.014

Keywords: activity based costing, emergy, goal programming, overhead allocation drivers, sustainable companies

Citation: Marinho Neto HF, Agostinho F, Almeida CMVB, Moreno García RR and Giannetti BF (2018) Activity-Based Costing Using Multicriteria Drivers: An Accounting Proposal to Boost Companies Toward Sustainability. Front. Energy Res. 6:36. doi: 10.3389/fenrg.2018.00036

Received: 13 February 2018; Accepted: 16 April 2018;

Published: 04 May 2018.

Edited by:

Federico Maria Pulselli, University of Siena, ItalyReviewed by:

Giulia Goffetti, University of Siena, ItalyXiang yun Gao, China University of Geosciences, China

Elliott Thomas Campbell, Maryland Department of Natural Resources, United States

Copyright © 2018 Marinho Neto, Agostinho, Almeida, Moreno García and Giannetti. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Feni Agostinho, feniagostinho@gmail.com; feni@unip.br