Andrea Christie

Andrea Christie- Global School of Business and Law, RMIT University, Melbourne, VIC, Australia

This paper presents a literature review on the role of the distributed ledger technology in promoting stakeholder trust for charitable organizations. The purpose of this review is to capture existing knowledge on the relationship between the following key variables: charity, trust and accountability, and distributed ledger technology—with emphasis on blockchain technology as a primary example of this technology. After shortlisting the discovered literature pool to 35 papers, the following three themes were identified. The first theme presents the various definitions of key concepts in crypto-philanthropy literature. The second theme captures existing views on why stakeholder trust is declining in charitable conduct. These views include: (1) organizational boundary shifts; (2) monitory complexity; and (3) poor regulatory design. The third and final theme presents a hypothesis on how the distributed ledger technology can promote trust for charities. The technology is hypothesized to promote trust by drawing on the following three elements: (1) decentralization; (2) provenance; and (3) rule-enforcement. A number of shortcomings are then highlighted in the literature pool. The first shortcoming pertains to the inconsistent treatment of key concepts in crypto-philanthropy studies. The second shortcoming pertains to the lack of discussion on whether the distributed ledger technology may potentially decrease stakeholder trust if implemented irresponsibly by charities. In conclusion, a series of future research pathways are provided. These recommendations include: (1) clarifying key concepts; (2) suggesting “crypto-philanthropy” as a formal disciplinary title; (3) highlighting under-researched areas; and, (4) recommending strategies for building a new crypto-philanthropic theory. From an academic perspective, the findings contribute to literature by bridging the gap between crypto-economic, institutional governance and non-profit accountability theories. The findings may also guide charity managers, regulators and policy-makers in understanding the capacities of the distributed ledger technology in legitimizing charitable conduct.

Introduction

An emerging hypothesis in crypto-literature states that the distributed ledger technology may assist charitable organizations in promoting greater stakeholder trust in their donation allocation activities. Distributed ledger technology (DLT) is a digitally-secure record of transactions that distributes data across the peer-to-peer network without reliance on centralized authorities (Reinsberg, 2019). A popular example of the DLT is blockchain technology, which was formally introduced by pseudonymous Satoshi Nakamoto in a 2009 whitepaper. In this whitepaper, he introduces the very first application of blockchain technology, called Bitcoin—[i.e., a digital peer-to-peer financial system whereby users can send digitally encrypted coins (i.e., cryptocurrency) to other network-users without reliance on traditional banking intermediaries]. He also discusses how the technology promotes trust between socially-distant non-intimates through a combination of cryptography, consensus mechanisms, and distributed computing. Since this whitepaper was released, literature has witnessed an exponential surge in publications on the role of the DLT in governing market transactions. While many of these publications analyse the technology's applications in the capital market, including supply chain and logistics, marketing, banking, accounting, and law, there has recently been rising interest in the technology's applications in the charity sector (Podder et al., 2017).

To understand how the DLT applies to the charity sector, consider UNICEF as a case-study example. UNICEF currently uses the DLT to accept digital donations in the form of popular cryptocurrencies, including Bitcoin and Ether (Taylor, 2019). UNICEF can then send these digital donations directly to beneficiaries while bypassing issues associated with poor banking facilities, lengthy bureaucratic processes, and international conversion fees. A second case study example is Oxfam Australia's cash disbursement program in Vanuatu (Michael, 2019). In this program, the beneficiary is provided with a voucher that can be exchanged for emergency supplies with an Oxfam-partnered vendor (Carnaby and Hallwright, 2019). Once the exchange has occurred, the vendor records this transaction on the blockchain-powered application using their smartphone. This system then enables Oxfam to accurately track the donation transactions in real-time, such as how many blankets were purchased by beneficiaries and which vendors later need to be compensated.

Literature suggests that the DLT may enhance several key improvements in the traditional donation supply chain process, including transactions speed, donation liquidity, economic power redistribution, and administrative cost-savings (Davies, 2015; MercyCorps, 2017). However, perhaps more significantly in the context of trust, literature hypothesizes that the DLT can enhance provenance for charities by enabling donations to be accurately traced dollar-for-dollar in real-time at every stage of supply chain process. For this reason, a rising number of authors such as Reinsberg (2019) and Kshetri (2017a,b) hypothesize that the DLT may assist charities in accounting for their donation activities, along with other resource allocation tasks routinely conducted in their social missions. Some of these resource allocation tasks include: (1) volunteer and employee task assignment (e.g., as piloted by the Australian Red Cross, in conjunction with crypto-software developer, TypeHuman1; (2) identity management systems for beneficiaries (e.g., as piloted by the United Nations in conflict areas and war zones); (3) supply chain tracking of perishable goods (e.g., rice, tuna, and coffee beans) for vulnerable farmers (e.g., as piloted by the World Wildlife Fund in conjunction with crypto consulting firm, ConsenSys2, and (4) micro-financing assistance for minority groups who would otherwise lack financial inclusion, such as women in developing nations (e.g., as piloted by Bitpesa in Sub-Saharan Africa, and discussed by the Women's World Banking Global Network3.

However, there is no literature review to date that explores the relationship between the DLT, trust, and charity. This serves as a critical research gap in the social scientific literature. While a few key papers discuss the impacts of the DLT on charity governance, this knowledge remains largely buried in the literature pool, perhaps unbeknown to the researcher. If the researcher struggles to identify this existing knowledge, it renders difficulty in appropriately testing, discarding or extending these theories. Consequently, this paper seeks to guide future scientific enquiry into crypto-philanthropic related themes.

In addition to furthering knowledge for the academic reader, this paper seeks to provide valuable knowledge to the practitioner. More specifically, it seeks to inform charity managers who might wish to learn more about the capacities of the DLT in combatting allegations of charitable misconduct. This research topic is highly topical, given recent regulatory reports of distrust in the charity sector (Adena et al., 2019)4. As contended by Jegers and Wellens (2014), a number of globally reported charity scandals have caused relational breakdowns between stakeholder groups, including donors, beneficiaries, regulators, and charity managers. To alleviate trust concerns, several multinational charities such as the Red Cross, the Brotherhood of St. Laurence and WaterAid have begun investing significant capital into DLTs with the hopes of demonstrating greater accountability in how they account for their donation pools. These actions suggest the following two ideas. Firstly, it suggests that charities are highly responsive toward resolving stakeholder concerns. Secondly, it suggests that charities are greatly interested in learning if the DLT can help alleviate trust concerns in how they account for their donation transactions. Therefore, it is possible that the charity manager would benefit from the findings of this literature review.

The rest of this paper is divided into the following sections: (1) research method; (2) critical analysis of key themes appearing in literature; and (3) discussion, conclusion, and recommendations for future research pathways.

This paper contributes to the academic domain by representing a novel attempt to bridge the gap between extant charity accountability and crypto-innovation theories. The findings of this review may increase scientific understanding of DLT impacts on social welfare delivery. From an industry perspective, the findings may also inform charity managers, policy-makers, and regulators in designing appropriate accountability models that increases charity credibility. Ultimately, it is hoped that this knowledge will help charities consider new technological methods of maximizing stakeholder trust and, in turn, the donation pools required to support vulnerable recipients worldwide.

Literature Review—Research Method

Key Aims, Objectives, and Scope

The primary aim of this literature review was to capture existing knowledge on the relationship between the DLT, trust, and charity. To achieve this purpose, it was necessary to fulfill to the following three research objectives. The first objective was to identify common themes interweaved throughout the discovered literature. The second objective was to determine the common research methods and treatments of key concepts in the discovered literature. The third and final research objective was to identify relevant research pathways for the academic and charity practitioner who may be interested in conducting future enquiry on the topic.

The review's scope encompasses several aspects. Firstly, the scope includes all literature that discusses the following themes: stakeholder trust and charity, and the DLT and blockchain technology. Secondly, the scope comprises of all literature that defines the concept of trust as follows: a firm belief in someone's reliability, honesty, and ability to fulfill a certain task. In the context of this review, someone refers to the charity manager, while task specifically refers to the act of allocating donations for a social purpose. Third and finally, the paper acknowledges that the concept of trust is highly abstract and broad. Consequently, the paper's scope has been confined to a single ingredient of trust. This ingredient is accountability, which is defined as the process of explaining one's conduct and taking ownership for one's mistakes.

Having established the scope and objectives of this literature review, it is necessary to explain the search, screen and selection process for gathering appropriate literature. These steps are documented in the subsections below.

Search Process

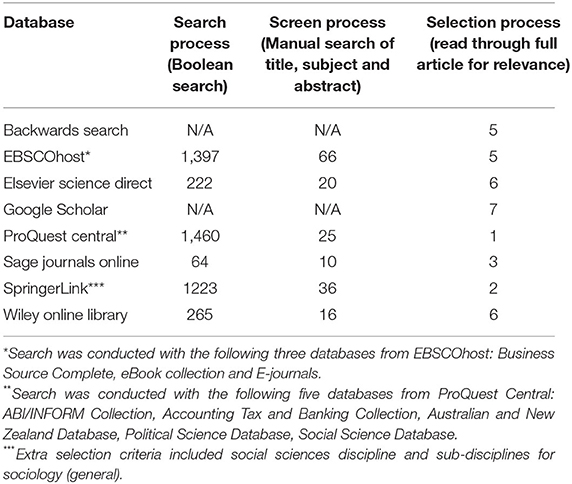

The literature review process comprised of a 12-years search (i.e., 2008–2019) of extant academic and non-academic publications. The search consisted of the following publication types: peer-reviewed journal articles, book sections, conference papers, literature reviews, government reports, and industry research.

The first step in the search process comprised of a search for academic sources. The search was conducted with the following six databases: EBSCOhost, Elsevier ScienceDirect, ProQuest Central, Sage Journals Online, SpringerLink, and Wiley Online. To discover publications, it was necessary to conduct a Boolean search in each of these databases. The Boolean search consisted of key terms relating to DLT, trust, and charity. To address word interchangeability error, papers were included if their title and/or abstract contained the following search term combinations:

° Group 1: charity OR charitable giving OR donation OR non-profit OR philanthropy;

° AND Group 2: trust OR accountability OR opportunism OR governance; and,

° OR Group 3: distributed ledger technology OR DLT OR blockchain OR crypto.

Exclusion Criteria

During the search process for academic sources, several exclusion criteria were used to determine literature appropriateness. The first criterion stated that the paper must use English as its main language source. The second criterion stated that the paper must be published between the period of January 2008 and December 2019. These dates were selected on the basis that they coincide with blockchain technology's introduction in literature [see Nakamoto (2009) whitepaper on Bitcoin]. The third and final criterion stated that publication must pertain to one of the following publication types: article, book entry, company report, conference paper, industry paper, government report, literature review, market report, or proceeding. Fourthly, the criterion stated that the article must be peer-reviewed to ensure that all reviewed knowledge has been fully cross-checked by the academic community. This method yielded 4,631 publications.

Note: Table 1 depicts the article count derived at each step of the search-screen-selection process.

Table 1. Article count breakdown (literature search, screening, and selection process).

Screening and Selection Process—Academic Sources

Upon completion of the search process for academic sources, it was necessary to screen the literature. The screening process involved a manual assessment of the publication's title, subject, and abstract to determine whether it satisfied the conditions of relevancy and research methodology. Firstly, the relevancy condition implied that all publications that failed to satisfyingly engage in key concepts were to be manually excluded. Secondly, the research methodology condition implied that all publications that failed to draw upon a sound research methodology—such as a framework, model, theory literature review, survey, case study, interview, experiment, or simulation—were to be similarly excluded. The screening process took a total of 4 weeks. Many of these publications contained one concept, but did not address its linkages to one or more other key concepts and were therefore excluded. This process eventually reduced the pool to 473 publications. Finally, each publication was individually screened to determine whether the article fully engaged with two or more key concepts, using a sound methodology. This process took a process of 2 weeks and eventually reduced the pool to 473 academic publications in total.

Before proceeding to discuss the following steps in the literature review process, it is perhaps worth explaining the sharp and sudden drop in article count—from 4,631 to 473 and, finally, 23 academic papers. Recall that these three concepts are each widely observed by numerous socio-economic disciplines, including law, accounting, political-economics, marketing, and finance. Consequently, the initial search for these key concepts yielded thousands of papers. However, upon screening the literature, it became evident that a majority of these articles discussed these concepts in siloes, instead of drawing linkages between these three concepts. Why is there such a small pool of academic papers engaging with two or more of these concepts? This can be explained by the following three reasons. Firstly, the multidisciplinary nature of the topic renders difficulty for the scholar in uncovering direct relationships between these concepts, or in building on pre-existing theoretic platforms. A second reason lies with the charity sector's historical struggle with adopting new technological developments in contrast to the public and private sectors. There are currently very few charity case-studies for researchers to empirically test and confirm the relationships between these three key concepts. By contrast, the capital market has demonstrated greater agility in rolling out their DLT-powered solutions to a mainstream audience. Consequently, this has perhaps prompted crypto-researchers to funnel their efforts toward testing DLT impacts in capital market applications. A third and final reason perhaps lies with the academic publication process, which involves an average timeframe of 2 years. This lengthy timeframe implies that the databases may be slow to incorporate knowledge on recent economic advancements, particularly in crypto-philanthropy advancements. In conclusion, these three reasons explain why there was a sudden drop in the article count in the literature search process.

Search, Screening, and Selection Process—Non-Academic Publications

Once the search for academic articles was completed, it was necessary to search for non-academic sources. To ensure a comprehensive coverage of the topic, the search was extended to industry, market and government papers, including discussion papers, market reports, and charity commission audits. These documents were identified and screened by: (1) conducting a forward/backwards reference search via Web of Science and Google Scholar; and (2) manually searching high ranking author profiles in relevant domains. These articles were screened and selected based on the same exclusion criteria used for academic sources (listed in section exclusion criteria). Further, a third criteria was used to screen non-academic sources. The criteria stated that the non-academic publication must derive from a well-recognized source for legitimacy purposes, such as official charity auditors, government departments and widely cited industry leaders in the crypto-philanthropy community—for example, charity innovators, such as the Charities Aid Foundation and MercyCorps, who are some of the first multinational charities to explore the use of DLTs in philanthropy. This final step resulted in 12 additional documents, bringing the total to 35 publications.

Classifying the Final Literature Pool

Once the shortlisted literature pool was finalized, the publications were clustered into the following two groups:

° Group A: all publications that investigate linkages between trust and charity; and,

° Groups B: all publications that investigate the linkages between the DLT and charity.

This division was made for analytic purposes. Due to the novel nature of the topic, there are currently very few publications that discuss all three variables (i.e., DLT, trust, and charity) in a single study. Instead, a majority of the publications discuss merely a portion of the review topic. Group A discusses the relationship between charity and trust, while Group B discusses the relationship between DLT and charity. While these two groups of examination appear to discuss different topics, these groups are, in fact, presenting pieces of compatible knowledge that can be amalgamated into a new and exciting field—a field that investigates linkages between charity, trust AND the DLT.

In conclusion, by combining knowledge from these two separate groups of examination, this literature review has been able to capture knowledge that would otherwise have remained in regimented siloes.

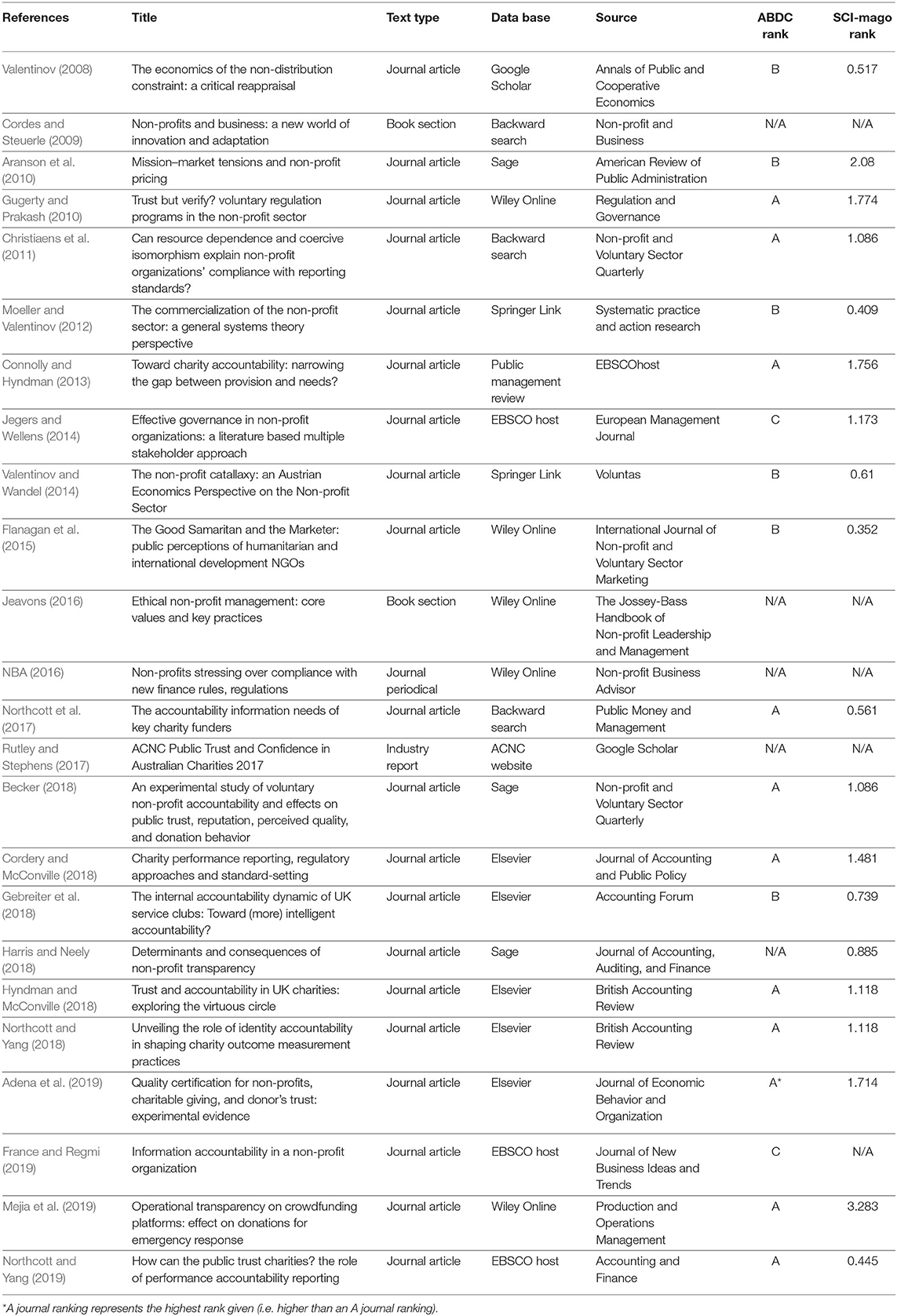

Note: See Tables 2, 3 to view the final list of shortlisted literature. Table 2 shows all publications classified as Group A literature, while Table 3 shows all publications classified as Group B literature.

Table 2. Shortlisted literature (Group A).

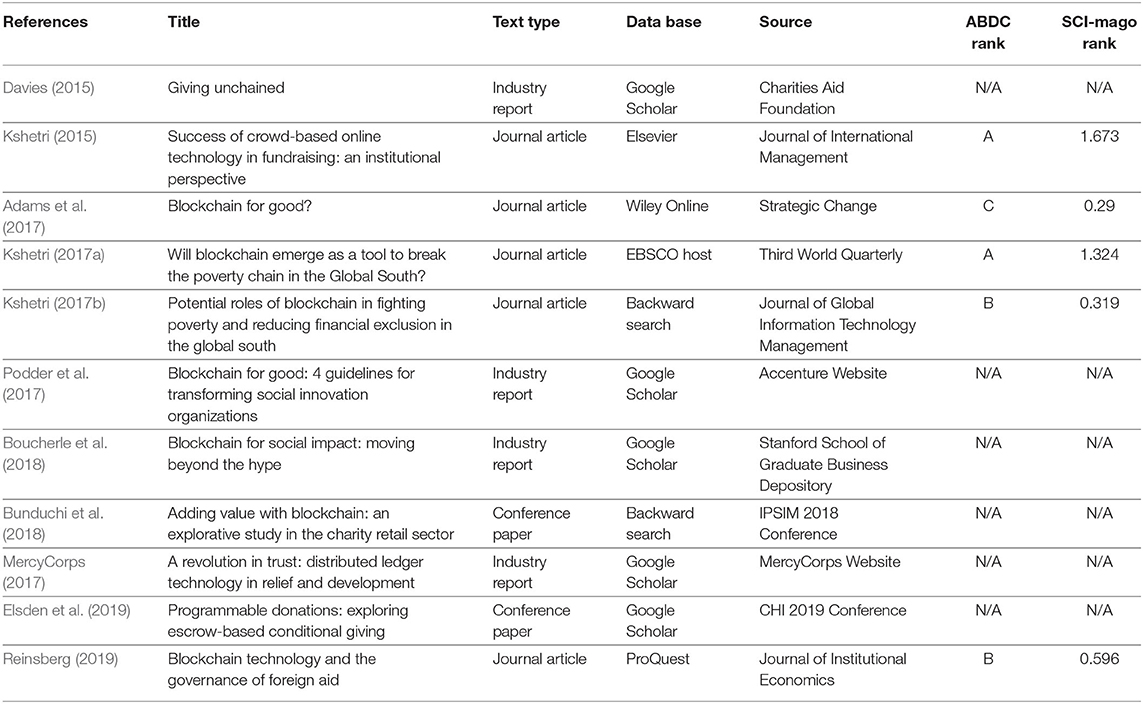

Table 3. Shortlisted literature (Group B).

Overview of Discovered Literature

Once the discovered literature was clustered into two distinct groups, a number of general observations were made with respect to research diversity. From an overview, the literature derives from a highly diverse range of disciplines and geographical locations. These disciplines include: management accounting, institutional economics, crypto-economics, non-profit accountability, information technology, political sciences, ethical management, and marketing. Geographical locations include the following: Australia, Belgium, England, Germany, New Zealand, Poland, Scotland, and the United States. Listing these locations and fields, one perhaps gains a sense of the multi-disciplinary nature of the topic, as well as the vast diversity of research ideologies, theories, and frameworks in examining this topic.

What does this observation imply for researchers moving forward? On the upside, a diversity of researchers may represent a unique opportunity for cross-collaborative research spanning across many cultures, locations, and academic fields that are commonly regimented in siloes. On the downside, however, this diversity may lead to conflicting academic debates on how to treat key concepts. Therefore, it is suggested that authors heed the recommendations posed in section Recommendations and Suggestions for Future Research Pathways to ensure a seamless and unified research pathway moving forward.

Overall Quality of Discovered Literature

When observing the discovered literature, it was also necessary to analyse the overall research quality of the pool. The quality was assessed using a combination of the Australian Business Dean Council (ABDC) ranking and SCImago (SJR) ranking. Firstly, the ABDC ranking was selected for its intuitive use and appropriateness in comparing business publications. For comparative purposes, the SJR ranking was selected to crosscheck these rankings across a wide array of social scientific disciplines. The SJR ranking was calculated by using the ratio of the journal's average number of weighted citations for that given year and the total number of documents published in the past 3 years. This ranking has been acknowledged as useful in considering both the journal's aggregate citations and the prestige of such citations according to the journals they derive from (LaTrobe, 2019).

Upon comparing the two rankings, the average SJR score for A/A* ranking journals in the literature pool was 1.417, while the average for B/C ranking journals was 0.709. Given that the average B/C journal ranking equals roughly half of the average A/A* ranking, these calculations imply that the two rankings are consistent. It should be noted, however, that there were minimal outliers. One outlier appearing in the list was the European Management Journal—a C grade journal with an SJR score of 1.173. This score is significantly higher than other B/C ranked publications in the ABCD list. A second outlier appearing in the list was the Accounting and Finance Journal—an A grade journal with an SJR score of 0.445. However, given these outliers are minimal, it can be concluded that the two rankings are consistent. Another point worth noting on the overall literature quality is that the majority of the A/A* ranking journals appeared in Group A literature (i.e., 11 in total). By contrast, only two articles in the Group B list appeared in A/A* journals, while three appeared in B/C journals and six were ungraded. These results suggest that a majority of DLT-based information is contained in non-academic sources, thereby justifying a need for a more rigorous academic enquiry into this topic.

Themes Identified in Discovered Literature

Once the quality of the literature pool was analyzed, it was necessary to identify core themes that are interwoven in the literature. The following three key themes were identified in the literature pool:

- Theme 1: Definitions and Treatments of key concepts;

- Theme 2: Views on why contemporary charities suffer from trust concerns; and,

- Theme 3: A hypothesis on how the DLT promotes trust for charities.

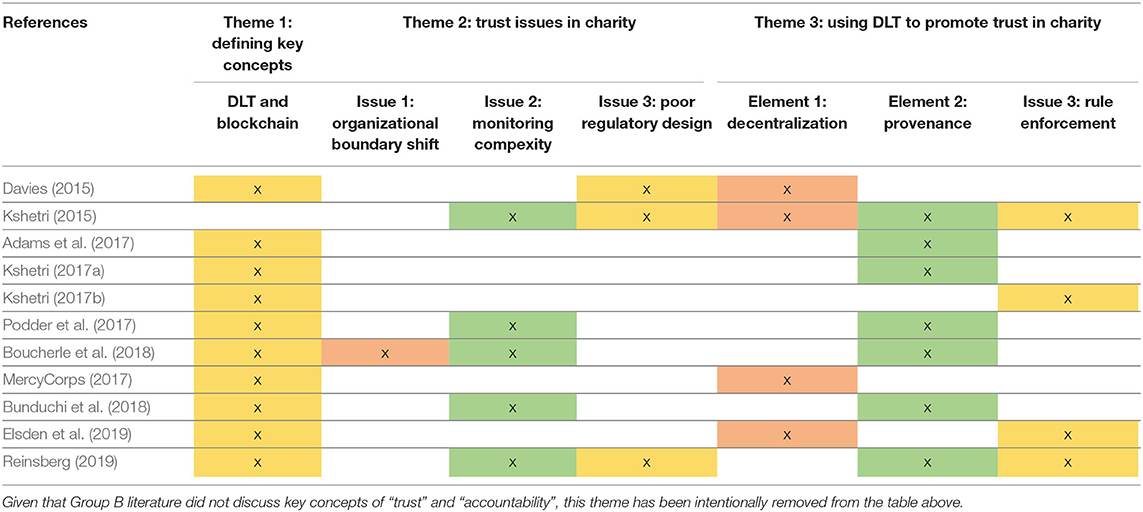

Note: See Tables 4, 5 to determine the themes appearing in each article.

Table 4. Thematic analysis of Group A literature.

Table 5. Thematic analysis of Group B literature.

These four themes will be discussed in the sections below.

Theme 1: Defining Key Concepts

The first theme identified in the literature pool comprised of a detailed discussion on the definition and treatment of key concepts. These concepts included: (1) DLT and blockchain technology; (2) trust and accountability; and (3) charity.

Defining the DLT and Blockchain Technology

Beginning with the discussion on the DLT, its definition was unanimously described by Group B studies as a digitally-secure record of transactions that records economic ownership at any given time point. Data is maintained, verified, and distributed across the peer-to-peer network using independent devices (i.e., nodes) without third-party assistance (Kshetri, 2017a,b). The network achieves data sanctity through automated consensus mechanisms, whereby users must agree on the data's true state and be collectively responsible for recording and verifying additions (Reinsberg, 2019). For this reason, it is considered as a decentralized database whose records are owned and maintained by the system (Davies, 2015; Boucherle et al., 2018).

Authors commonly referred to the blockchain ledger as a popular example of the DLT. They described the blockchain as a shared digital record book in which users (i.e., nodes) record and maintain a constantly developing list of economic transactions. These transactions are sequentially organized into data blocks and are cryptographically linked together in the form of a chain—hence receiving the title, the blockchain. Cryptography is the mathematical technique used to encrypt and decrypt data to ensure strict privacy is maintained when either digitally stored or transmitted between users (Kshetri, 2017a). This design increases ease of identifying block tampering and secures the system against fraudulent activity (MercyCorps, 2017). Security is also maintained through its element of immutability, whereby it is theoretically difficult to alter or remove data once recorded (Kshetri, 2017b). In combination, these aspects ensure that the ledger is both highly “transparent” and “incorruptible” (Bunduchi et al., 2018, p. 1–2).

However, while the DLT was consistently defined by authors as per the discussion above, there was heavy debate on how the DLT should be classified in crypto-philanthropy analysis. Authors debated on the following three classifications: (1) an operational tool for enhancing technical efficiency for charities; (2) an institutional technology for governing charity; and (3) both an operational tool and an institutional technology.

Beginning with the first classification, a majority of authors classified the DLT as an operational tool, otherwise known as a general-purpose technology. This was on the basis that the technology's raison-d'être is to enhance technical efficiencies for businesses, including charities. Such efficiencies include transaction speed, administrative savings, and reporting errors (Boucherle et al., 2018). When analyzing the DLT's role in the charity context, these authors mainly observed how the technology might create organizational value for charities in insular and tactical contexts. Examples include improving value exchanges, internal markets for social goods, and transaction ease between charities, customers, stores, and donors (Bunduchi et al., 2018).

However, some authors treated the DLT as both an operational tool and an institutional technology. These authors argued that the DLT not only decreases financial costs for establishing identity with legal certainty, but performs civic duties “typically associated with a sovereign government,” thereby representing an “alternative to the traditional trusted identity authority” (MercyCorps, 2017, p. 20). Further, while the DLT enhances the “functioning of existing institutions” by decreasing information asymmetries, the technology also replaces existing institutions by performing comparable functions at a reduced cost to society (Reinsberg, 2019, p. 6).

Alternatively, a number of authors treated the DLT as an institutional technology for governing economic interactions in a polity. In particular, scholars from the institutional economic discipline applied Davidson et al.'s (2018) classification of the DLT as a form of distributed governance. Following on Reinsberg (2019), the DLT represents an institutional technology for overseeing resource allocation. The DLT assists institutions in enforcing network rules that reward socially desirable behavior. These rules ensure that a given group of network actors can transact without fear of opportunism and can reach consensus on economic facts. Consequently, the DLTs deployment is useful in environments whereby traditional institutions fail to facilitate consensus amongst participants, otherwise known as low-trust environments (Reinsberg, 2019). In the charity context, the primary role of the DLT is to assist charity managers, regulators, donors, and policy-makers in governing their common pool resource allocation. One popular example of a common resource pool allocation is the distribution of monetary or non-monetary donations to beneficiaries, such as food, water and clothes. The DLT reduces “institutional bottlenecks” in developing economies by nurturing foreign aid at national and international levels in with semi-trusted environments (Kshetri, 2017b, p. 1725; Reinsberg, 2019). More specifically, the DLT has a direct impact on the “economic, social, and political outcomes” of foreign aid distribution in its capacities to fulfill the following three duties: (1) its duty to increase transparency and to prevent corruption; (2) its duty to empower donors by effectively gathering and communicating missing information, including whether funds have reached recipients; and (3) its duty to disintermediate international remittances and trade finances (Kshetri, 2017b, p. 1,711). Meanwhile, authors argued that any operational efficiencies, including increased speed and cost-savings, are merely a “second kind of benefit” (Kshetri, 2017b).

Further, several authors claimed that the DLT can replace systems and structures of government altogether. For example, Davies (2015, p. 5) recalls the world's first blockchain marriage in 2015 to enforce the notion that the blockchain currently performs “citizenship duties” and other legally enforceable procedures on behalf of governments. For this reason, the DLT is hypothesized to promote trust as a technological governance tool.

Yet how does literature define trust in non-profit analysis? This will be answered in the section below.

Defining Trust and Accountability

In parallel to their discussions on the DLT, authors discussed another key concept—trust. This concept was conceptualized as a “belief” in an entity's honesty, dependability or capacity to perform a given task or action (Hyndman and McConville, 2018, p. 7). In an organizational context, trust is demonstrated to stakeholders through effective accounting practices (Northcott and Yang, 2019, p. 1683), which signals that the firm is being “answerable for one's conduct and responsibilities” (Connolly and Hyndman, 2013, p. 946). Consequently, non-profit trust-building models are entwined heavily with accountability themes. In bridging the gap between charity, trust and accountability, literature proposed that “charities owe a duty of accountability to the public” (Northcott and Yang, 2019, p. 1682), whereby an erosion in perceived stakeholder trust can reduce charitable support for the sector at large (Mejia et al., 2019). Further, authors warned that a charity's long-term survival depends on its capacities to both develop and maintain stakeholder trust in its donation allocation activities.

Yet charity accountability research remains generally “underdeveloped” (Northcott and Yang, 2019, p. 1682), with literature uncertain as to how to treat this concept—both in traditional analysis and in DLT-related analysis. One explanation rests in the “ill-defined” nature of the concept of accountability (2017, p. 28). On an operational level, accountability represents the process of disclosing information on a firm's activities, including performance effectiveness in achieving mission goals (France and Regmi, 2019). However, with a recent thematic shift toward corporate governance, its definition has since been broadened to encompass the act of demanding and providing explanations for conduct (Gebreiter et al., 2018). In reconciliation, Northcott et al. (2017) consider accountability as follows: the process of allocating a charity's assets responsibly in alignment with its designated purpose, whereby all information pertaining to its use is fully disclosed.

In addition to defining charity accountability, Group A studies also discussed the primary function of accountability. In a charity organizational context, these studies contend that the primary function of accountability is to encourage efficient social mission delivery and responsible donation allocation for the purposes of fulfilling stakeholders' legitimate aspirations (Connolly and Hyndman, 2013; Flanagan et al., 2015). It is conventionally discharged on a financial reporting level since it directly “empowers stakeholders” with performance monitoring and evaluation (France and Regmi, 2019, p. 28). However, Northcott and Yang (2018, 2019) have also broadened this view to include non-financial information pertaining to a charity's social mission goals, plans, institutional structures, results, outputs, effectiveness, and efficiency.

A number of authors drew upon a common set of theories and frameworks when analyzing non-profit accountability. These included: (1) stakeholder theory; (2) trustworthiness and reputational theories; (3) agency theory; and (4) institutional work theory.

Various classifications of accountability include Northcott et al.'s (2017, p. 1685) differentiation between “imposed” and “elective” accountability. While imposed forms prioritize information provision in alignment with high-salience stakeholder demand, elective forms are purposed toward connecting with small donors, recipients, and other low-salience groups in an informal setting. Further, while imposed forms rely on financial reports and formal methods of disclosure, elective forms uses emotive disclosures such as photographs and personal testimonies. The authors also delineate a third mode: “grassroots” accountability, or relational/face-to-face. This mode is appropriate for informally delivering performance to low-salience groups with limited influence in holding charities accountable.

Alternatively, accountability was classified as “upwards vs. downwards,” “internal vs. external,” and “functional vs. strategic”—the last of which was categorized by France and Regmi (2019) in the following four forms: strategic, fiduciary, financial, or procedural. A small pool of studies analyzed accountability on an internal level. For example, Northcott and Yang (2018) contend that internal stakeholders not only strive to be accountable to external forces, but to themselves through organizational values. Similarly, Gebreiter et al. (2018, p. 2) used the accountability framework to analyse the micro-level relationship between individuals using structural factors such as “how the charity operates” (e.g., codes-of-conduct) and personal internalizations of “what it means to be a member.” These authors argued that this framework is an “intelligent” form compared to prior studies, which focus solely on performance measurement controls (Gebreiter et al., 2018). Consequently, they concluded that the accountability framework is highly appropriate in capturing managerial needs, values, and behaviors in discharging charity accountability.

However, while Gebreiter et al. (2018) heralded the use of the accountability framework, they did not discuss the framework's appropriateness in analyzing non-traditional governance tools—most notably, the DLT. Instead, authors tended to confine their analysis to traditional governance tools, including charity boards, annual financial reports, independent star ratings, and regular charity commission audits.

In conclusion to this section, the concepts of trust and accountability appear to be as allusive as the concept of the DLT. Yet how does literature treat the concept of charity? This treatment will be revealed in the subsection below.

Defining Charity

The third and final key concept appearing in the selected literature pool was the concept of charity. The term was defined amongst authors as one of the following three classifications: (1) a social organization; (2) an entity defined by its non-distribution constraint; and (3) an institution.

Beginning with the first classification, a majority of authors conceptualized the charity as a social organization. The social organization is a relatively durable combination of resources roughly ordered into some kind of hierarchy and coordinated to achieve a given social goal (Aranson et al., 2010). As a collective group, charities are said to operate in a space somewhere in between the public and private sector, conceptualized not by “what it is,” but instead “via a negative definition” (Gebreiter et al., 2018, p. 3). The primary difference between the non-profit sector and for-profit sector rests in their external dependence on government grants and private funding. This dependence renders it vulnerable to changes in both regulatory pressures and resource flows (Christiaens et al., 2011, p. 201).

A second classification witnessed another group of authors treat the charity as an entity defined by its non-distribution contrast. This classification stems from Hansmann's definition (Hansmann, 1980, p. 838), which was later quoted by Cordes and Steuerle (2009) as follows: an organization that is “barred from distributing its net earnings, if any, to individuals who exercise control over it, such as members, officers, directors, or trustees.” The distinction between the for-profit and non-profit firm lies in its “non-distribution constraint”—a term which refers to the lack of formal profit function preventing the owners from appropriating any economic surplus generated by the non-profit (Cordes and Steuerle, 2009). The constraint represents an important antecedent in creating trust since owners cannot legally appropriate any economic surpluses generated by the charity (Moeller and Valentinov, 2012). This potentially lowers the incentive to cheat customers by cutting corners on quality or unnecessary provision, thereby signaling responsible donation allocation.

The third and final definition of a charity comprises of an institution. In the context of charity literature, an institution is conceptualized as governing mechanism that monitors, controls, and facilitates interactions between non-profit actors by enforcing rules and punishment/reward systems (Valentinov and Wandel, 2014). As a collective-action mechanism, the institution represents the sum of various interrelated contracts between principals (funders) and agents (charity mangers) who agree to perform certain tasks on behalf of the principal.

In addition to debating charity treatment in literature, Group A studies also discussed the primary purpose of a charity. Generally, authors agreed that the charity exists for the purpose of public benefit provision. Examples include poverty relief, education, and all purposes rendered “beneficial to the community” (Connolly and Hyndman, 2013, p. 946). Charities are “instruments of collective action for serving the public good” and are “critical to building social capital”—consequently, these vehicles should be considered as “a concept that centers on trust” (Jeavons, 2016, p. 169). To function effectively, a charity must be perceived as highly trustworthy, with “integrity” placed at its core. Therefore, strong governing practices are needed to demonstrate to stakeholders that the charity is allocating its donations responsibly (Jeavons, 2016, p. 169).

In conclusion to this section, the discovered literature clearly enforces the concept that charities owe a duty of care to stakeholders in managing their donations appropriately, as well as taking ownership for their mistakes. Further, it discusses the role of different accountability disclosure methods in promoting trust for charities. However, there were a number of research shortcomings highlighted in the literature pool—these will be discussed in the critical analysis section below.

Critical Analysis of Theme 1

In relation to Theme 1, the first shortcoming identified in the literature pool relates to the limited linkages made between core concepts. Group B studies explained the general linkages between the concepts of the DLT, trust and charity without explaining how these concepts could be analyzed in greater detail. These findings are perhaps unsurprising, given that the technology is still being piloted by the charity sector. With only a limited number of proof-of-concepts available, this renders difficulty in investigating and confirming the relationship between the DLT, trust, and charity. Hence, any theoretical discussions relating to these key concepts tend to be highly broad and generalized in nature.

Another shortcoming in the identified literature pool was the inconsistent treatment of key concepts. Beginning with the concept of the DLT, authors disputed whether the DLT should be viewed as an operational tool for enhancing charity workplace efficiencies or as an institutional technology for governing charity. Similarly, the definition of accountability was defined inconsistently. As highlighted by Gebreiter et al. (2018, p. 4), there remains dispute on whether accountability should be classified as an “emancipatory force” or, in alignment with Roberts and Scapens (1990) argument, a vehicle for “establishing and maintaining control.” Finally, the concept of charity was also highly debated, with classifications varying in level of abstractedness, ease of application, and practicality.

In conclusion, literature has not reached formalized consensus on how to treat key concepts in crypto-philanthropy analysis. This is likely due to the multi-disciplinary nature of the topic, as mentioned earlier in section overview of discovered literature. With authors deriving from a plethora of fields, each author is likely to apply analysis that is consistent with his or her disciplinary field. To reconcile these differences in future studies, it is recommended that authors draw upon a single set of definitions when moving forwards. This suggested research pathway will be discussed in a later section.

Theme 2: View on Trust Issues in Charity

A second theme appearing in identified literature pool was the phenomenon of trust issues occurring in charities. Authors held conflicting views on why the contemporary charity sector is experiencing a decline in stakeholder distrust regarding how charities account for their donation allocation activities. Authors' views consisted of the following: (1) shifting organizational boundaries; (2) monitoring complexity; and (3) poor regulatory design. The three views are discussed in the sections below.

Shifting Organizational Boundaries

Beginning with the first view; authors stipulated that the recent rise in competition for limited grants and donations has prompted charities to adopt more commercial operation methods. This causes the charity sector's aggregate income-based activity level to increase, thereby reducing the non-distribution constraint's effects on stakeholder perceptions (Cordes and Steuerle, 2009).

How does a rise in income levels reduce perceived stakeholder trust? Authors offer two arguments. Firstly, Aranson et al. (2010, p. 154) argue that the pressure for more systematic performance evaluation might force charities to reframe their mission and allocate resources in a way that limits outcomes, thereby decreasing public confidence in their capacities to deliver on mission goals. This case was also made by Moeller and Valentinov (2012) and Christiaens et al. (2011), who respectively drew on General Systems Theory and Bertalanffy's “mechanistic” view of the charity sector to illustrate how the rise in income activities impairs the charity's capacities to deliver on mission outcomes. Secondly, authors argued that a rise in income-based activities has prompted stakeholders to treat the charity akin to a for-profit structure. This change in treatment increases the market expectancy for accountability reporting and other forms of trust-signaling pertaining to the private sector (Bunger, 2012; Moeller and Valentinov, 2012). As argued by Northcott et al. (2017, p. 173), the “changing expectations about the accountability needs of stakeholders” has led to an “increasing scrutiny of the charity sector.”

While neither argument rules out the other, both of these arguments provide convincing cases for how shifting organizational boundaries may have caused stakeholder trust perceptions to have declined in the contemporary charity sector.

Monitoring Complexity

Authors also presented a second view on why trust is declining for charities—this view shall be termed “monitoring complexity.” The view stipulates that monitoring complexity has increased due to a widely discussed theory referred as either the accountability problem (Becker, 2018) or as the principal-agent problem (Gugerty and Prakash, 2010). The problem can be explained as follows. The principal (otherwise known as the donor) grants full donation distribution responsibility to the agent (otherwise known as the charity manager) due to perceived expertise in delivering greater mission outcomes. Yet the charity manager—while unmotivated by profit generation—may possess motivations that conflict with that of the donor (Valentinov and Wandel, 2014). Since the donor cannot fully monitor donation distribution, this creates potential for “agency slack” (Reinsberg, 2019, p. 414), or “agency slippages” (Gugerty and Prakash, 2010, p. 22), whereby the charity manager may exploit these information asymmetries for private gains.

The non-profit structure poses monitoring challenges since there are few mechanisms to ensure that managerial and stakeholder incentives are aligned. Consequently, managers can abuse such regulatory deficits (Gugerty and Prakash, 2010). The principal rectifies this problem through precautionary arrangements, including contracts and monitoring controls. Yet his or her lack of expertise and resources in monitoring donation-use incurs transactions costs that undermine gains from aid delegation (Reinsberg, 2019). Consequently, this causes an erosion in stakeholder trust, along with increased stakeholder scrutiny on how funds are being allocated, thereby propagating a need for greater accountability and transparency measures (Podder et al., 2017).

Poor Regulatory Design

A third and final view discuss in the literature shall be termed “poor regulatory design.” According to institutional economic theory, governing success is dependent on the type of governance mechanism employed (Aligica, 2015). Not all institutions are equal in their capacities to govern economic activities. As explained by Kshetri (2015, p. 100) with respect to crowdfunding technologies, the success of an online charity campaign depends on the “formal and informal institutions” employed. Instead, certain sizes and types will be more effective than others (Kshetri, 2017b, p. 1713). Consequently, this theory stresses the importance of employing appropriate institutions to oversee the charity sector's activities. Yet which institutions should be employed? It appears that the discovered literature has not reached consensus on which types of institutions should ultimately govern the charity sector.

Indeed, there has been extensive debate on the optimum level of decentralization needed to govern charitable activity. One group of authors heralded decentralized institutions on the basis that these institutions ensure that “services are effectively monitored and valued” (Valentinov, 2008, p. 24). Contrastingly, “the state cannot manage its affairs any better than the non-market sector when pushed beyond a certain level of complexity” (Valentinov, 2008). Further, an empirical study on US charity regulations found that autocratic rules caused charity managers to become increasingly concerned with compliance and accountability reporting costs (NBA, 2016). Whenever a new institution rule was introduced, these managers would feel immense “dread” and “stress” regarding how these rules would impact on the charity's long-term survival (NBA, 2016, p. 7). Consequently, these authors concluded that spontaneous action should be used to oversee the charity sector.

However, not all authors agreed with this view. Some studies proposed that voluntary governance alone may not be sufficient, with Jegers and Wellens (2014) alluding to a number of charity scandals under the governance of informal institutional rules. Further, empirical analysis by Harris and Neely (2018) suggest that the strength of a charity's autocratic governance (i.e., board of directors) may perform a crucial role in promoting transparency and, in turn, building relational trust with its stakeholder base. Finally, Cordery and McConville (2018, p. 302) suggest that authoritative governance can provide significant benefits for charity oversight. These benefits include: (1) formalized detailed rules that simplify a charity's auditing process; (2) ease of monitoring and penalty enforcement over charities; and (3) clearly defining regulatory objectives.

However, in defense to their own arguments, Cordery and McConville (2018) suggested that an autocratic approach may lead to several disadvantages. Firstly, a hierarchical system may lead to rule inflexibility, whereby the institution cannot adapt fast enough to changing conditions. Secondly, an autocratic institution may generate high implementation and maintenance costs. Third and finally, an autocratic institution may lead to inappropriate or ineffective rules. For example, the charity regulator may create rules that fail to take in account differing charity sizes, activities, and stakeholder needs. These rules may force charities to make suboptimal donation distribution decisions, publically disclose performance data in a way that is detrimental to the charity, or else skews performance results against their favor.

Consequently, Cordery and McConville (2018) recommend that charity governance should consist of a combination of centralized and voluntary institutions, which will dynamically evolve over time. This would enable charity stakeholders to decide amongst themselves how donations should be effectively distributed, but with some level of independent, third-party oversight (Cordery and McConville, 2018). Given that the DLT allows for varying degrees of (de)centralization, it will be interesting to observe its capacities to govern charities over the coming decades. This observation will become clearer once DLT pilots are formally introduced into the mainstream market.

In conclusion to this section, authors provided comprehensive arguments for why trust perceptions are declining in the contemporary charity sector, including organizational boundary shifts, monitoring complexity, and poor regulatory design. Yet there are perhaps two minor shortcomings worth mentioning. These will be discussed in the section below.

Critical Analysis of Theme 2

In relation to theme 2, the first shortcoming in the discovered literature pool pertains to the assumptions applied in stakeholder analysis. Scholars tended to conduct stakeholder analysis based on the assumption that all stakeholder groups share the same expectations with respect to charity accountability. Yet, as argued by Northcott and Yang (2019, p. 173), not all stakeholder groups possess the same “accountability expectations.” Rather, each group holds a unique relationship with the charity which, in turn, impacts the group's perception of whether the charity is behaving responsibly.

To illustrate the difference in stakeholder perceptions, consider a group of major donors (i.e., those who donate significant amounts to a charitable cause) versus non-major donors (i.e., those who donate non-significant amounts per annum). Firstly, the major donor group may share a highly personalized experience with the charity through networking events, board meeting representation, and fundraising galas. By contrast, the non-major donor group may have minimal contact with the charity. Consequently, these two donor groups will likely hold differing perceptions on how the charity should account for and report their donation allocation activities.

Therefore, any study that treats all stakeholders as a single unit for analytic purposes may skew data results. One example is the bi-annual report commissioned by the national charity regulator, the Australian Charities and Not-for-Profits Commission (Rutley and Stephens, 2017). This report used a qualitative survey approach to capture the national trust and confidence levels in the Australian charity sector. The findings concluded that stakeholder trust perceptions had worsened since the previous report in 2015. However, the report did not acknowledge that all stakeholder group responses had been bundled together for analytic purposes. It is possible that the survey responses from non-major donors may have accounted for a disproportionately larger number of responses than major donors. Consequently, the major donor group responses may have been hidden amongst the wider group, despite holding a higher degree of reporting influence over charities than non-major donors.

Ultimately, this approach may present the researcher with a distorted view of trust perceptions in the charity sector. This approach, in turn, may prohibit the researcher from appropriately assessing the DLT's impacts on stakeholder perceptions. In conclusion, authors are strongly encouraged to address this shortcoming in future studies, as per the recommendations posed in a later section of this paper.

A second and final shortcoming in the discovered literature was the omission of the following controversial issue in contemporary charity: that public trust is declining due to the monied elite's self-seeking behavior in charitable giving. The term self-seeking refers to the elite's use of philanthropy as a vehicle for increasing one's own social credit while avoiding capital gains tax (Kramer, 2018; Lindsay, 2018). This issue was raised by New York Times foreign correspondent, Anand Giridharadas. In his book, Winners Take All: The Elite Charade of Changing the World5, Giridharadas condemns those in positions of privilege and wealth on the basis that they “dictate the terms of modern philanthropy”—to which a majority of the charity sector has “silently acquiesced” (Lindsay, 2018). Giridharadas explains that the elite refuse to give something up to retain his or her economic power, much to the detriment of social change. The following example illustrates the difference between the concepts of giving back and giving something up. Consider a TED talk, in which an audience of elites speculate how to combat poverty in Africa. If one were to give back, the audience members might ask themselves, “How do we raise more money for Africa?” (Lindsay, 2018). This question would likely prompt the audience to conduct a fundraising campaign, which would enable them to publicly “charade” their humanitarian efforts without fully addressing the social issue (Lindsay, 2018). Instead, if one were to truly give up something, the audience members would ask themselves, “how would we do that? how would we implement it?” (Lindsay, 2018). This action would likely prompt research efforts into finding the root cause, which may result in supporting a global capital tax. Although the tax agenda would redistribute economic away from the elite, the audience members would support this agenda on the basis that the tax would effectively reduce poverty. Yet Giridharadas argues that the elite rarely support such controversial research policy agendas. Instead, the elite choose to protect the very system that is causing the social issue that they wish to solve (Kramer, 2018).

In conclusion to this section, the authors have presented a number of views on why mistrust occurs in contemporary philanthropy. Consequently, the following section will proceed to discuss the scholars' views on how DLT can alleviate these trust issues for charities.

Theme 3: A Hypothesis on How the DLT Promotes Trust for Charities

The third and final theme in the discovered literature pool consisted of the following hypothesis: that the DLT can promote trust for charities. Generally, Group B studies adopted a highly positive view of the DLT in assisting charities with governing their donation allocation activities. Specifically, these studies hypothesized that the DLT can promote trust using the following three elements: (1) decentralization; (2) provenance; and (3) rule-enforcement. These elements are explained in the following section.

Elements of Decentralization, Provenance, and Rule-Enforcement

The first element that is hypothesized to promote trust for charities is the “decentralized” nature of the DLT (Davies, 2015; Kshetri, 2017a). Kshetri (2015) represents one of the earliest scholars in the discovered literature pool to speculate the significance of crowdfunding technologies in generating “legitimacy” and positive trust perceptions for charities. Given that the system is controlled and maintained by users instead of centralized institutions, this empowers non-profit parties to make collaborative donation distribution decisions. Further, as an “authoritative decentralized system that exists outside the control of a state government,” it shifts data control to the consumer and facilitates movement between polities and physical borders (MercyCorps, 2017, p. 20). Consequently, these consensus mechanisms are assumed to “guarantee higher levels of trust” (Davies, 2015, p. 7).

The second element that that is hypothesized to promote trust for charities is “provenance.” Authors explain that the DLT uses distributed computing and cryptographic hashing mechanisms to ensure immutability. Together, these ingredients create “opaque transactions” between agents (Kshetri, 2017a, p. 204). In the context of the charity, provenance enables donations to be tracked and accounted for at each step of the donation supply chain (Boucherle et al., 2018). It provides clarity on, which party has donated?, where did funds flow to?, how were they were spent?, and what percentage did the recipient receive? (Reinsberg, 2019). Further, provenance assures all charity stakeholders that falsified information can be accurately detected and opportunistic parties can be pinpointed. Consequently, this fosters a trusting environment, particularly in developing regions (Kshetri, 2017a). Additionally, provenance increases brand reputation since institutional efficacy depends on perceived legitimacy, whereby funders must recognize the charity as a highly credible authority for trusting donations.

The third and final element that promotes trust for charities is “rule-enforcement.” This element pertains to the use of automated protocols in facilitating civil behavior (Reinsberg, 2019). Kshetri (2015, p. 100) explains that the success of a given crowdfunding project depends on “formal and informal institutions” employed. More specifically, the crowdfunding technology is useful in monitoring actor behavior in the following four different types of crowdfunding projects: (1) donation-based crowdfunding; (2) crowdlending; (3) reward-based crowdfunding; and (4) crowdequity (Kshetri, 2015). As a “third-party enforcement mechanism,” rule-enforcement can assist charities with governing donation distribution in environments lacking effective oversight. The DLT achieves governing oversight by automatically enforcing shared rules overseeing donors, policy-makers, and NGOs (Kshetri, 2017b, p. 1,714). Many developing nations are characterized by a “lack of effective enforcement mechanisms” for “commercial contracts, social and economic rights, laws, and regulations” (Kshetri, 2017b, p. 1,713). Consequently, the DLT can strengthen governing oversight by cryptographically embedding donor conditionality and policy compliance terms into the token, which is often referred to as a “smart donation,” both in industry and in literature (Reinsberg, 2019).

Critical Analysis of Theme 3

Overall, the discovered literature pool exhibited a number of literary strengths. Reinsberg (2019) and Kshetri (2017a,b) provided some of the first building blocks for understanding blockchain's governing capacities in foreign aid using an institutional economic lens. Further, authors such as Elsden et al. (2019) offered a balanced assessment of the DLT in generating trust for charities by hinting to the potential risks and pitfalls of donation automation. The study revealed that, while DLTs offer exciting new monitoring possibilities for charities, the concept of a purely transactional approach to charity may elicit potential discomfort with the removal of the human element from a largely altruistic and human-centric activity. Therefore, charities will need to carefully incorporate the DLT into existing donation models to maintain stakeholder trust levels.

Adams et al. (2017) also acknowledged a number of potential accountability risks for charities. One risk that these authors discussed was the environmental consequences of Bitcoin mining—an activity which may lead to wasteful energy consumption and costs for businesses. A second ethical risk discussed by these scholars pertained to ledger types. The choice between public and private ledgers can have vast implications on how market actors interact with each other and in turn, form perceptions of trust and accountability. This concept has been observed in general DLT and trust related literature—for example, a research paper released by the Inter-American Development Bank addresses the virtues of each ledger type in great detail (López and Unda, 2018). Adams et al. (2017) agreed with this view in stipulating that a permissioned, private blockchain can lead to a highly centralized form of governance in which a small, centralized group of users access and control the database. However, these scholars did not tailor these aforementioned risks to the context of philanthropy; herein lies the first shortcoming in the discovered literature pool. Instead, the scholars may have found it useful to speculate the following question: how does the ledger type impact on the relations formed between charities and its broader stakeholder groups—specifically the groups to whom it is accountable? Given this question has yet to be answered specifically in the crypto-philanthropy context, it is recommended that these questions are explored in future studies.

A number of additional shortcomings were also identified in the discovered literature pool. These included the lack of discussion on: (1) DLTs for COVID-19; (2) DLTs for conflict aid and developing nations; (3) DLTs and the future of philanthropic decision-making; and (4) DLTs and the new charity players.

DLTs for COVID-19

One primary shortcoming in the discovered literature was the lack of discussion on DLT's application in COVID-19 humanitarian response programmes. The COVID-19 pandemic is acknowledged by the United Nations Development Program (UNDP, 2020) as the “defining global health crisis of our time” and the “greatest challenge we have faced since World War Two.” The virus initially emerged in the Asian region in December 2020 and has since spread to almost every continent, with cases reaching four million in May 2020 (UNDP, 2020). A rising number of humanitarian response plans are being designed to enhance socio-economic impact and recovery using DLT-based infrastructure. One initiative includes the TCN Coalition—a global community that seeks to support the use of digital contact tracing protocols in combatting COVID-19. Termed exposure notification applications, these protocols rely on all forms of open source software, including DLTs, to effectively notify users of COVID-19 exposure. Several industry and governmental groups have begun to develop these applications, including the Australian government's COVIDSafe application6, as well as international technology companies Apple and Google (Miller, 2020). Yet these initiatives are often overlapping in both mission and product, with little visibility on how these systems fit within a broader ecosystem (TCN, 2020). Further, a number of media articles have expressed concern as to data privacy risk, with the Australian Government's COVIDsafe app criticized on that basis that its centralized design may be a “target for attack” and could be possibly “misused by law enforcement” (Lazar and Sheel, 2020). To mitigate these privacy information risks, the TCN Coalition provides education, expert advice, and support on responsible application deployment that protects the citizen. More specifically, the Coalition provides a gathering place to promote cross-group communication, interoperability and to minimize resource allocation waste.

The TCN Coalition is just one example of how the global technological community is helping to alleviate the socio-economic impacts of COVID-19 using open source software, such as the DLT. In addition to the Coalition, a number of crypto-charity campaigns are being deployed to help track the flow of donations in combatting COVID-19. These include GiveTrack7, WaterAid8, BitGive9, and Huobi Charity Campaign10. With an exponential rise in DLT applications being used to combat COVID-19, the question remains: how can DLTs promote coordinative trust for citizens, developers, governments, and health officials in their combat against COVID-19? This question would serve as a useful platform for future research.

DLTs for Conflict Aid and Developing Economies

Another shortcoming in the discovered literature pertains to the minimal discussion on the DLT's role in promoting trust in conflict aid and in developing nations. DLTs are currently being deployed to address a number of socio-economic issues faced in disaster zones and developing regions, including financial, economic, and digital inclusion. The United Nation's World Food Programme is one such use-case that enables refugees to collect cash donations from local supermarkets and banks throughout Jordan (Frey and Gatzweiler, 2018). The initiative uses a combination of eye-scanning equipment and blockchain technology to manage the cash flows and beneficiary data (Frey and Gatzweiler, 2018). This initiative disrupts the dependent relationship between the refugee and the camp itself, with the refugees no longer confined to the camp for monitoring purposes. More specifically, it provides refugees with the autonomy to venture outside of the camp and connect socially with family and friends. This programme has demonstrated the enormous potential for DLT innovations to transform aid relief—by shifting toward a more “flexible and human-centered approach” (Frey and Gatzweiler, 2018). However, the DLT can also pose data infringement risk—a risk that remains highly underexplored in the discovered literature pool. By managing data on behalf of vulnerable individuals, the charity potentially makes the beneficiary vulnerable to the breach, theft or compromise of digital records, which may very well lead to further beneficiary persecution and discrimination—as seen with the Rohingya refugees in Bangladesh (Rahman, 2017). In conclusion, there is currently little scholarly examination into the role of the DLT in promoting trust for more recent economic developments, which serves as a missed opportunity to inform the reader of the current DLT use-cases in contemporary philanthropy.

DLTs and the Future of Philanthropic Decision-Making

An additional shortcoming in the discovered literature pertained to the lack of discussion on the future of philanthropy and its impacts on the decision-making practices traditionally employed in humanitarian programmes. This theme was discussed by Davies from the Charities Aid Foundation (CAF). In a discussion paper on the future of charitable giving, Davies (2017) speculates whether the DLT will cause the donations platform to be entirely or partially disintermediated. He also questions whether the use of DLTs might eliminate reliance on centralized governance by human individuals, such as board members. Such a future may be made possible by Distributed Autonomous Organizations (DAOs)—(i.e., a set of smart contracts that oversees the interactions of network users). The philanthropy sector has slowly begun its transition from a traditional governance structure—composed of charitable organizations that act as intermediaries—to direct donation platforms, such as GiveDirectly11. The platform acts as an intermediary and enables the donor to send donations directly to the beneficiary. This poses questions as to whether economic power will be shifted toward donors and beneficiaries, who are now able to “decide how best to use” the donations without centralized reliance from charitable organizations (Davies, 2017, p. 3). Yet Davies takes this speculation one step further with his discussion on AIDAOs—a concept that combines artificial intelligence (AI) with DAOs. In the charity context, the human would be responsible for deciding how best to distribute donations, based on both emotional and rational considerations. Meanwhile, the AI would be responsible for distributing the resources to accomplish the given philanthropic outcome. Following on Davies' example, the charity platform might use an AIDAO-controlled warehouse of smart objects, such as self-driverless vehicles. Traditionally, without the use of AIDAOs, the charity might store and operate a large vehicle fleet to distribute donated supplies to beneficiaries. Instead, these fleets could be replaced by an AIDAO-controlled network of vehicles, whereby the charity commands the AIDAO to distribute the resources as necessary.

In an extension of Davies' questions, how will AIDAOs shape the future of philanthropy from the perspective of trust? Do donors truly need monitoring mechanisms in the form of centralized institutions, such as charitable organizations, to ensure that his or her donations are being used responsibly? Or can he or she fully trust in the blockchain ledger to distribute the donations on his or her behalf? As mentioned by Davies (2017, p. 3), these platforms are likely to challenge one's assumptions on what it means to execute and structure charity - a concept that we “currently take for granted.” It may likely change how scholars define charity—with a newly added definition consisting of an institutional technology for governing charitable giving. In conclusion, as a proliferation of DLT and AI infused applications come to fruition over the coming years, scholars are recommended to research the technological impacts on the future of charity decision-making.

DLTs and the New Charity Players

The final shortcoming in the discovered literature pertains to the lack of discussion on how new crypto-charity players will impact on the traditional charity model. As noted in Waltman's (2019), The Decentralized Charity Ecosystem, there is rising pressure for charities to embrace new fundraising methods. He describes three new charity models in parallel to the traditional charity model: (1) crypto-charity foundations (e.g., GiveCrypto12); (2) native crypto-tokens built explicitly for a given charity effort (e.g., AidCoin13); (3) traditional charities that accept crypto-currencies (e.g., Save the Children14); and (4) payment and remittance crypto-charity organizations (e.g., the Airdrop Venezuela campaign by Airtm15). Such platforms will likely provide entirely new funding sources for charities and may assist the contemporary charity in securing limited funding in a historical period marked by fierce competition (as discussed in an earlier section on shifting organizational boundaries). Traditionally, charities use monitoring signals such as organizational brand or expensive star rating systems to signal credibility. Consequently, the researcher may benefit from investigating how these new charitable structures will impact on the interactions between donors, charities, regulators, and other parties in future aid initiatives.

In conclusion to the literature review, there are a number of shortcomings that will need to be addressed in future research. These shortcomings will be discussed further in the section below.

Discussion, Conclusion, and Research Implications

Discussion of Findings

Overall, the identified literature has provided some of the first building blocks for understanding the role of the DLT in charity governance. Yet there are a number of minor shortcomings that will need be addressed in future enquiries.

The first shortcoming that will need to be addressed pertains to the absence of an official disciplinary name. There is currently no formal name that delineates all academic enquiry into the relationship between the DLT, trust, and charity. The creation of a field name would likely assist future researchers in discovering extant knowledge on the topic. A field name would also likely assist academics in publishing their own findings for the benefit of their fellow peers.

A second shortcoming pertains to the limited reference to existing tools when building new DLT analytical constructs. Group B studies tended to build their own conceptual theories without drawing on existing scientific theories or frameworks (with the exception of Kshetri and Reinsberg). This represents a missed opportunity to build on, test and extend existing conceptual platforms that may be appropriate in this newly emerging research field.

A third shortcoming is the lack of discussion on whether the DLT could potentially erode stakeholder trust if implemented by charities without appropriate care. Authors tended to discuss the hypothetical benefits that DLTs may provide to charities, with minimal investigation into the potential risks that they pose, such as the risk of digital record breaches.

A fourth and final shortcoming is the lack of discussion on the DLT's implications for future of philanthropy. As discussed earlier in this paper, the DLT is likely to radically disrupt the charity governance model over the coming decades and provide new funding sources for charities.

In conclusion to the literature review, extant studies have provided an excellent rudimentary platform for understanding the role of the DLT in governing charity. However, much of the discussion remains highly generalized at this stage due to the limited pilots in current circulation. Such pilots are needed to test and verify extant hypotheses in the real-world. With a number of shortcomings highlighted, there is need to inform future investigators on suggested research pathways—these will be discussed in the section below.

Recommendations and Suggestions for Future Research Pathways

Scholars who wish to conduct serious examination into the crypto-philanthropy discipline are advised to consider the following research suggestions. The first recommendation is to use the field name, “crypto-philanthropy,” to pertain to all studies that investigate the role of the DLT in governing philanthropic activities. These activities include all those conducted by charities, NGOs, social impact organizations, philanthropists, and social entrepreneurs.

Secondly, it is recommended that future research funnel its efforts into investigating the linkages between DLT, trust, and charity. Authors should break down the core concept into incremental units for a more detailed analysis. For example, instead of investigating general linkages between “DLTs” and “trust,” one author might consider analyzing specific linkages between one type of DLT (e.g., the blockchain ledger) and an ingredient of trust (e.g., accountability). Authors are also encouraged to consider the various treatments of key concepts. For example, the DLT is often treated as an institutional technology, and operational tool, or both. Authors should justify their choice of treatment before venturing to apply analysis.

Thirdly, it is recommended that authors agree upon a single set of definitions when analyzing trust and charity. More specifically, they should draw upon the following definitions for clarity of key concepts:

a) Trust: a belief in an entity's honesty, dependability, or capacity to perform a given task or action;

b) Accountability: a willingness or obligation to explain one's actions and to take ownership for any direct or indirect externalities that arise from these actions; and,

c) DLT: a digitally-secure, peer-to-peer record book of transactions that captures economic ownership at any given time point, and in which the network is collectively responsible for recording, maintaining, and verifying changes to this record book without reliance on centralized authorities.

Fourthly, when approaching analysis, scholars are encouraged to adopt theories that have already been extensively tested in charity accountability literature. These theories include stakeholder theory, institutional work theory, and principal agent theory. Authors can use these theories as a platform for building a more cohesive, singular theory that enables the researcher to understand the relationship between DLTs, trust, and charity.

Fifthly, it is recommended that scholars treat various stakeholder groups as individual units for analytic purposes. As discussed in the critical analysis section for theme 2, each stakeholder group may share differing expectations with respect to charity accountability, such as major donors vs. non-major donors. Consequently, future studies are encouraged to analyse stakeholder perceptions in isolation before venturing to determine the role of the DLT in addressing any stakeholder concerns.