Shaiku Shahida Saheb1*

Shaiku Shahida Saheb1* Venkata Krishna Reddy Chinnapareddy2

Venkata Krishna Reddy Chinnapareddy2 Divya Devalla1Sirisha Charugulla1Naga Bhavani Chakka1Kunchakara Raja Sekhar1

Divya Devalla1Sirisha Charugulla1Naga Bhavani Chakka1Kunchakara Raja Sekhar1- 1VIT-AP University, Amaravati, India

- 2Anurag Engineering College, Kodad, India

Introduction: The initiation of blockchain has brought about revolutionary changes across multiple industries, including finance. This study analyzes published research related to existing financial reporting and audit practices relevant to the implementation and efficacy of blockchain technology. The decentralized, immutable, and transparent blockchain ledger is set to change traditional practices by enhancing accuracy, reducing fraud, and ensuring real-time data accessibility.

Methods: This study identifies and measures the factors influencing blockchain implementation in specific auditing areas, particularly financial reporting. This research analyzed accounting professionals’ awareness of information and communication technologies (ICT), data security, data privacy, and training among accounting professionals. Hence, the study conducted a survey that targeted accounting practitioners, chartered accountants, financial analysts, and auditors with the aim of analyzing and testing hypothesized relationships using structural equation modeling in AMOS software.

Results: It presents an empirical analysis that examines the extent to which these factors influence blockchain technology implementation in financial reporting and auditing. We found a significant influence of blockchain technology use on the practices of financial reporting and auditing, leading to enhanced accuracy and transparency, reduced audit time, and increased trust in financial reports. Key findings indicate that while blockchain technology offers significant advantages, widespread implementation faces hurdles such as regulatory compliance, technological integration, and stakeholder acceptance.

Discussion: Researchers can use these findings to determine potential areas for further research. In addition, this research provides valuable information to practitioners in the field, academics, industry professionals, and policymakers considering the integration of blockchain technology with financial reporting and auditing.

1 Introduction

Blockchain technology has sparked a global revolution. Rapid progress in blockchain’s application across various sectors has been witnessed in the past 5 years, expanding its reach beyond cryptocurrencies to supply chain management and the internet of things. The technology’s development has been marked by rapid global market growth and is expected to increase quickly and exceed USD 39 billion by 2025 (Tandon et al., 2021). Today, blockchain technology is increasingly adopted in diverse industries, revolutionizing processes and offering secure, transparent, and efficient solutions (Gokoglan and Cetin, 2022). Technologies and frameworks are not made to be adaptable to different domains, including blockchain (Sarwar et al., 2021). The distributed ledger technology known as “blockchain” distributes information across a network instead of being stored in one central place. Every blockchain has its network of addresses used for transactions. Each block contains transaction information, and altering it is a challenge due to the unique hash values and secure hashing algorithms like SHA-256 (Tandon et al., 2021). Having transparent and auditable data in financial reporting is advantageous as it reduces the need for time-consuming reconciliation processes and better assures the reliability of financial statements (Javaid et al., 2022). Reconciliation automation raises concerns among small and medium-sized audit firms that it could jeopardize the profession and reduce their clientele; their lack of professional and technological resources to effectively compete in the blockchain-based accounting environment may be the cause of this concern (Anis, 2023). This study looks at how blockchain addresses issues like crypto asset reporting and regulatory compliance while increasing transparency and lowering errors in accounting procedures (Pimentel and Boulianne, 2020).

When blockchain technology developed, it was created only for use with cryptocurrency bitcoin and was not meant for application in other fields. However, critics in recent years have contended that blockchain can address specific needs such as privacy and permanence, leading to its potential applications beyond just cryptocurrency (Sarwar et al., 2021). Blockchain technology is now being widely applied in the accounting field. Transaction processing, voucher generation, inventory management, and contract execution are all possible due to their functionality (Chowdhury et al., 2023). Blockchain’s current development level is at a point similar to the internet in the mid-1990s and has emerged as a highly disruptive innovation post-internet era, acknowledged for its broad implications (Yu et al., 2018) and receiving significant attention for its potential to transform multiple sectors including finance and accounting (Liu et al., 2019). Its noteworthy features such as transparency, security, permanence, real-time reporting, and immutability made it increase in popularity, leading to much interest and addressing limitations of traditional accounting systems (Atadoga et al., 2024). This technological advancement has been applied in areas such as corporate governance, equity financing, and cryptocurrencies (Yu et al., 2018).

In the current environment, stakeholders mostly need to depend on the financial records of business organizations because of the prevalence of fraudulent practices in accounting and auditing. Financial records contain crucial data for internal and external users when making decisions. These are key aspects for accounting, providing reliable and accurate information on companies’ financial performance to their stakeholders. Traditional financial reporting systems and auditing processes have proven vulnerable to manipulation, fraud, error, and inefficiency (Dyball and Seethamraju, 2022); blockchain can minimize accounting mistakes and instances of fraud. According to Ankenbrand and Bieri (2018), using blockchain technology in audit processes can bring about a significant transformation by enabling a decentralized system of record-keeping that facilitates ongoing audits during the year. This would allow auditors to identify risks and crimes early instead of only doing year-end company evaluations. By using blockchain technology, businesses can guarantee the reliability and fairness of their financial documents, resulting in a substantial decrease in fraudulent activities.

2 Literature review

2.1 Blockchain technology in the finance/accounting sector

Blockchain technology was recognized due to the development of Bitcoin in the financial industry. It has evolved through different stages, from focusing on cryptocurrencies to smart contracts and broader applications in various industries (Tandon et al., 2021). Blockchain enhances financial transparency by securely recording trades of stocks, bonds, and derivatives in verifiable blocks. Each transaction is authorized by local regulators, aiding in fraud and money laundering detection by enabling the clear tracking and analysis of trading activities over time (Foroglou and Tsilidou, 2015). Blockchain technology has the potential to enhance ESG reporting, guarantee data integrity, and encourage sustainability in financial disclosures (Almadadha, 2024). In order to enhance psychological theoretical research, this study examines the internal mechanism of fintech’s influence on word-of-mouth from a micro psychological perspective. According to Li et al. (2023) and Mahdani et al. (2024), blockchain technology can reform financial reporting in accounting by enhancing data accuracy, reliability, and timeliness through its decentralized nature. Furthermore, blockchain smart contracts simplify financial report preparation by automating accounting rules. Demirkan et al. (2020) expand on this by discussing blockchain’s current and future business applications, particularly in accounting and cybersecurity. According to them, blockchain enables transaction recording, generates financial statements, and eliminates double-entry accounting by recording transactions directly onto the synchronized blockchain with real-time updates from other participants (Krichen et al., 2022). Blockchain technology streamlines processes by automating contracts, reducing costs, and accelerating cross-border transactions. It improves financial efficiency through asset tokenization and decentralized finance, while ensuring secure, tamper-resistant operations. Its applications span finance, healthcare, government, and defense, enhancing transparency, data protection, and operational efficiency across systems such as IoT, smart grids, and digital record management. Danach et al. (2024) explain that blockchain technology can improve regulatory compliance, maintain audit trail integrity, reduce costs, and ensure the accuracy of financial reporting through smart contracts, which are self-executing digital contracts that automate promises and agreements between parties by encoding the blockchain (Vokerla, 2019).

2.2 Other blockchain technology applications

Blockchain offers opportunities for automation, security, and authenticity verification in sectors like art, tourism, and accountability in financial and environmental data (Bellucci et al., 2022), and it finds applications in sectors such as finance, healthcare, and supply chain management, enabling tamper-proof digital ledgers and smart contracts that automatically execute predefined terms (Foroglou and Tsilidou, 2015). Smart contracts, decentralized autonomous organizations (DOA), and super-secured networks are predicted to become prevalent in the next 10 years, transforming how people and businesses conduct transactions and structure organizations (Makridakis and Christodoulou, 2019). Beyond cryptocurrency, blockchain is transforming industries by securing legal contracts, managing inventory, tracking goods, enabling digital IDs, and supporting voting systems, Entrepreneurs are rapidly developing diverse applications, reflecting the technology’s growing influence across social and professional sectors worldwide (Cekerevac and Cekerevac, 2022).

Blockchain ensures security, transparency, and efficiency in different sectors. In the financial industry, virtual currencies like Bitcoin, Ethereum, and Ripple are prominent applications of blockchain technology (Kim, 2020). This technology can enhance the security and privacy of transactions in fintech and e-commerce by enabling peer-to-peer transactions without intermediaries, thus ensuring data privacy and trust within decentralized networks (Mittal, H. (2021)). Likewise, blockchain has found applications in auditing processes, offering self-verifiable audit trails and driving cost efficiencies in the audit environment (Abreu et al., 2018). The evolution of blockchain tools showcases their adaptability and crucial role in enhancing security, transparency, and efficiency across diverse industries and applications.

2.3 ICT awareness among accounting and finance professionals

The implementation of new technologies in any field requires knowledge and skills to use information and communication technology (ICT). Studies show the need for increased awareness of blockchain technology among accountants and auditors, emphasizing the importance of training and education to bridge the knowledge gap (Anis, 2023). Factors such as experience, technical skills, and industry exposure influence auditors' awareness of disruptive technologies like blockchain (Upadhyay, 2020). Lack of knowledge and awareness can hinder the widespread adoption of blockchain technology (Agrif et al., 2022). Blockchain enhances the security, safety, and transparency of accounting information, impacting the way accountants work (Duong, 2020). Accountants with a high level of ICT awareness are expected to appreciate the benefits and functionalities of blockchain technology, thereby facilitating its adoption. As per Coyne and McMickle (2017), accountants who are well-versed in ICT are better equipped to learn blockchain tools for financial reporting and auditing. This awareness not only includes technical knowledge but also drives the demand for more advanced tools and systems that incorporate blockchain features.

2.4 Data security and data privacy

This study finds that blockchain’s decentralized, transparent, and immutable structure significantly enhances data security by preventing unauthorized access and tampering. Despite challenges like scalability and regulation, ongoing advances suggest strong potential for blockchain to transform data protection across industries (Verma and Ram, 2024). Earlier blockchain technology was created for recording cryptocurrencies. It is a decentralized system of multiple computers that secure transactions and prevent hacking. One factor that makes this technology attractive is its security. Transactions cannot be altered or deleted and are hard for hackers to tamper with (Anwar et al., 2019). Moreover, transactions involve a two-step authentication process. Even as investors continue to add digital transactions, the blockchain updates automatically. Ensuring data security and privacy becomes important because of the decentralized structure of blockchain technology. Integrating distributed ledger technology with existing accounting systems requires addressing scalability, flexibility, architecture, and cybersecurity issues to effectively report on crypto assets in financial statements and ensure effective financial reporting (Nakamoto and System, 2008). Blockchain ensures data immutability, transparency, and privacy through public keys, enabling peer-to-peer transactions without intermediaries while maintaining strong security, especially vital in financial operations Puthal et al. (2018) describe blockchain as a decentralized security framework that offers enhanced protection against unauthorized access and tampering. Some of the main concerns of financial professionals are addressed by the cryptographic nature of blockchain that ensure the security and privacy of financial statements.

2.5 Training and professional development

According to Danach et al. (2024), it is unlikely that all company transactions will be stored on blockchains as recent studies indicate that organizations currently employing blockchain technology only record specific transactions, typically related to accounts receivable and payable (Dai and Vasarhelyi, 2017). A new generation of accountants and auditors will be required to manage the evolving world of blockchain technology and its impact on their roles. This shift signifies a change from current accounting and auditing standards. Auditors skilled in IT will improve efficiency and effectiveness in financial reporting tasks.

According to Tapscott and Tapscott (2016), comprehensive training programs can help accountants and auditors understand the functionalities and benefits of blockchain tools. Such training programs should cover both technical aspects and practical applications, ensuring that accountants and auditors can effectively utilize blockchain technology in their work (Danach et al., 2024). Traditional audits fall short in the digital era, prompting firms like Deloitte and PwC to adopt continuous auditing powered by AI and blockchain. This will enable real-time transaction analysis, automate processes, use smart contracts, and enhance business insights, which demands that accountants develop advanced technological competencies (Schmitz and Leoni, 2019). Blockchain enhances educational efficiency, security, and transparency by enabling secure academic credential verification, while adoption challenges exist such as technical skills, data privacy, and regulation. Ongoing research, training, and collaborative efforts can enable ethical, scalable implementation across educational systems (El Koshiry et al., 2023).

The “Big Four” firms (the four largest audit firms: Deloitte, EY (Ernst & Young), KPMG, and PwC (PricewaterhouseCoopers)) are investing in new technologies like data analytics, AI, and blockchain, necessitating IT skills for auditors (Brende et al., 2019). Deloitte pioneered blockchain adoption, launching its first blockchain lab in Dublin in May 2016. Since then, it has partnered with major Irish banks to manage staff credentials via blockchain. The firm also installed a public Bitcoin ATM at its Toronto office, showcasing its commitment to cryptocurrency innovation. Deloitte has recently begun supporting a new blockchain accelerator initiative, “startup studio”, in collaboration with 22 other companies. This initiative is designed to enhance the capabilities of participating startups, equipping them with the tools and resources needed to achieve business success. Thereafter, the company also launched a platform based on blockchain technology for users to perform demonstrations and experiments (O’neal, 2025; Bonyuet, 2020).

2.6 Scandals and recent advancements in accounting and auditing

Sheela et al. (2023) provides a comprehensive analysis of blockchain integration in accounting and auditing, identifying three fundamental themes: the use of blockchain to strengthen financial reporting systems, auditing impacts, and cryptocurrency valuation. According to Pimentel and Boulianne (2020), researchers are in the early stages of examining how the accounting field could be impacted by blockchain technology, with the most significant academic research advancing in the auditing field. According to Atadoga et al. (2024), qualitative analysis supports the transformative power of blockchain technology in the accounting industry, anticipating changes in the roles of accountants and enhancements in process efficiency, transparency, and financial reporting reliability.

The Enron and AA scandals are the best-known fraudulence cases in financial reporting where auditors failed to prevent them. These cases have been discussed in the academic literature. Various aspects concerning financial data were being released to the investment community (Roszkowska, 2021). Anwar et al. (2019) examined rising financial statement fraud, exemplified by scandals like Satyam and Enron, and these underscore the need for stronger oversight. Experts advocate blockchain in auditing to enhance transparency and supervision. AICPA and CPA Canada emphasize that while blockchain will not replace audits, it improves financial reporting efficiency, requiring auditors to adopt the new technologies.

Thus, as mentioned earlier regarding the Big Four firms, there are many companies that validate blockchain’s value in financial reporting and that benefit from reduced delays, improved industry-wide efficiency, and accurate tracking. In supply chain management, Walmart and IBM utilize blockchain for authenticating and monitoring product origin data, thus enhancing auditing and reporting (IBM, 2023). Research has shown a growing interest in the application of blockchain to auditing to enhance efficiency and effectiveness, detect fraud, and prevent business risks (Qin, 2022). Exploring the use of blockchain-enabled smart contracts in financial reporting can lead to improved transparency, accuracy, and accountability in accounting practices (Hakami et al., 2023).

3 Problem statement

Blockchain’s immutable ledgers are distributed around the world and are built on the internet. In contrast to traditional systems of just one copy of a central leger, now we have thousands of these copies of the same ledger all linked together and constantly synced, making it cryptographically safe. Hakami et al. (2023) suggested an examination of the use of blockchain technology in such areas of auditing as financial reporting, internal controls, and assurance services. Due to the publicly accessible nature of blockchain, all users on the network can see transaction data. Although this may raise privacy concerns, it also introduces an opportunity to improve transparency in financial reporting. An increased availability of transaction data could encourage stakeholders to perform independent verifications, restricting the chance for manipulation and enhancing accountability. Mahdani et al. (2024) and Bonyuet (2020) have called for more research in this area to address issues such as data security, privacy, and integration with existing accounting systems. Accounting for crypto assets presents challenges such as classification debates, as they may not fit existing standards like cash or property, lack clear standards, and require data security. The lack of appropriate classification under existing standards such as IFRS is complicated because of the distinct nature of crypto assets for mining and initial coin offerings (ICOs). Investors and sceptics have been forced to reconsider cryptocurrencies like Bitcoin, Ethereum, Litecoin, Tether, and Dogecoin due to their increasing popularity and growth. Approximately 15 million Indians are estimated to have invested in private crypto assets (Economic Times, 2021). The lack of clear standards requires careful consideration in financial reporting.

Financial fraud, which accounted for 81% of cases in 2011, was linked to undisclosed data, fake documents, and mismanagement. It can be minimized by securely storing data in permissioned blockchains. This technology enables immediate access to financial statements, decreasing the chance of fraud. Private firms are advised to store their data on permissioned blockchains to avoid data breaches and criminal activities. The growing need for secure data management highlights challenges in preventing unauthorized access and tampering (Verma and Ram, 2024). More empirical studies on the impact of blockchain on auditing processes is needed to address the gaps in the existing literature, specifically in areas like financial reporting, internal controls, and assurance services (Chowdhury et al., 2023). According to El Koshiry et al. (2023), the adoption of blockchain in education faces significant challenges, including limited technical expertise, data privacy concerns, regulatory gaps, and system interoperability issues. This can result in increased trust in financial reports and a reduction in the incidence of financial fraud and error. The influence of these factors will be investigated empirical study.

4 Broad objectives

The research objectives of the study outline the relationship among the following factors.

1. Examine accountants’ ICT knowledge about blockchain technology.

2. Assess the influence of data security and privacy on the usage of blockchain tools.

3. Analyze the role of training in promoting blockchain technology adoption.

4. Determine the overall effect of blockchain technology on financial reporting and auditing.

The main purpose of this research is to evaluate the influence of various technological factors: ICT awareness, data security, data privacy, and training in the implementation of new technologies as blockchain technology in financial reporting and auditing.

5 Conceptual model and hypotheses

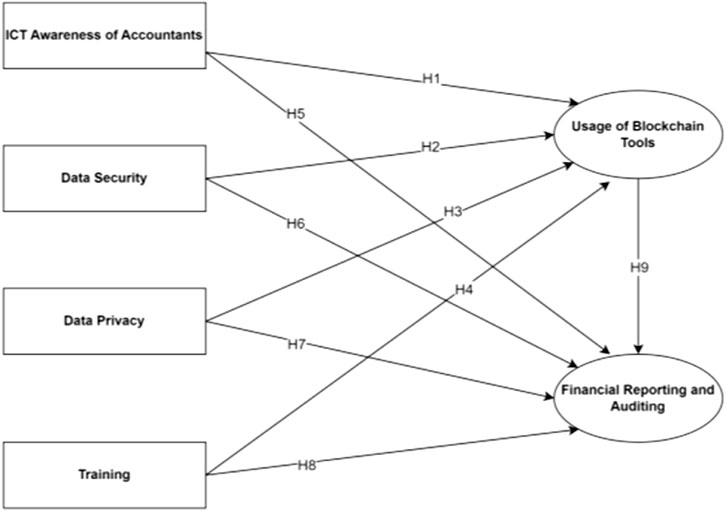

This research employs a quantitative approach to understand and examine the factors which influence blockchain technology’s application in financial reporting and auditing. The model is developed from objectives consisting of specific constructs and proposes specific hypotheses (H1 to H9) to observe their interrelationships. The following hypotheses were examined in the research.

H1:. ICT awareness of accountants influences the usage of blockchain-based tools.

H2:. Data security affects the usage of blockchain tools.

H3:. Data privacy issues affect the usage of blockchain tools.

H4:. Training has an impact on the usage of blockchain tools.

H5:. ICT awareness of accountants affects financial reporting and auditing.

H6:. Data security affects financial reporting and auditing.

H7:. Data privacy affects financial reporting and auditing.

H8:. Training influences financial reporting and auditing.

H9:. The use of blockchain-based tools has an impact on financial reporting and auditing.

The formulation of these constructs is similar to the approach of Giang and Tam (2023) in their investigation of the effects of blockchain on accounting in businesses by specifically examining manufacturing firms. Figure 1 illustrates the relationships between the constructs and the suggested theoretical framework.

Figure 1. Conceptual model.

6 Research design

6.1 Methods

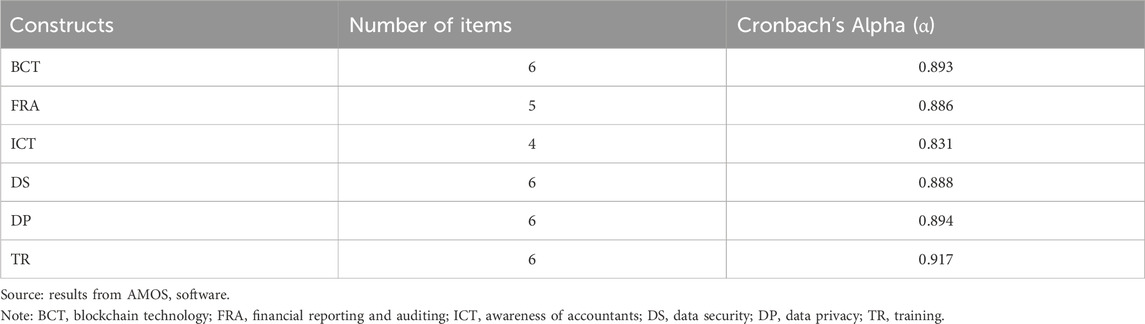

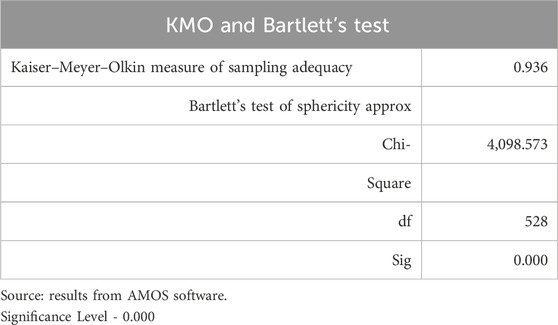

A questionnaire survey was chosen to gather data and evaluate the hypotheses of the study. The current study is part of a temporal study series because the data were gathered using a questionnaire within a specific and short period. A pilot test was conducted with 25 respondents to verify the study’s completeness, the time required to complete it, and to measure the validity and reliability of the items. The reliability of the scales was found to have a Cronbach’s alpha value above 0.8. The measurement items used in this study were drawn from established literature related to information systems, blockchain, and financial reporting. To ensure the reliability and validity of these adapted items, the study conducted rigorous statistical testing. Internal consistency was assessed using Cronbach’s alpha, with all constructs demonstrating strong reliability, with values from 0.831 to 0.917 well above the standard threshold for acceptability (Hair et al., 2014a). To evaluate the data’s suitability for factor analysis, a Kaiser–Meyer–Olkin (KMO) test yielded a value of 0.936, indicating excellent sampling adequacy. Additionally, Bartlett’s test of sphericity produced a statistically significant result (p < 0.001), confirming that the variables were appropriately correlated for further multivariate analysis. These results collectively support the robustness and appropriateness of the measurement model used in the study. This quantitative research design enables numerical data collection and statistical analysis to test the formulated hypotheses.

6.2 Sampling procedure and data collection

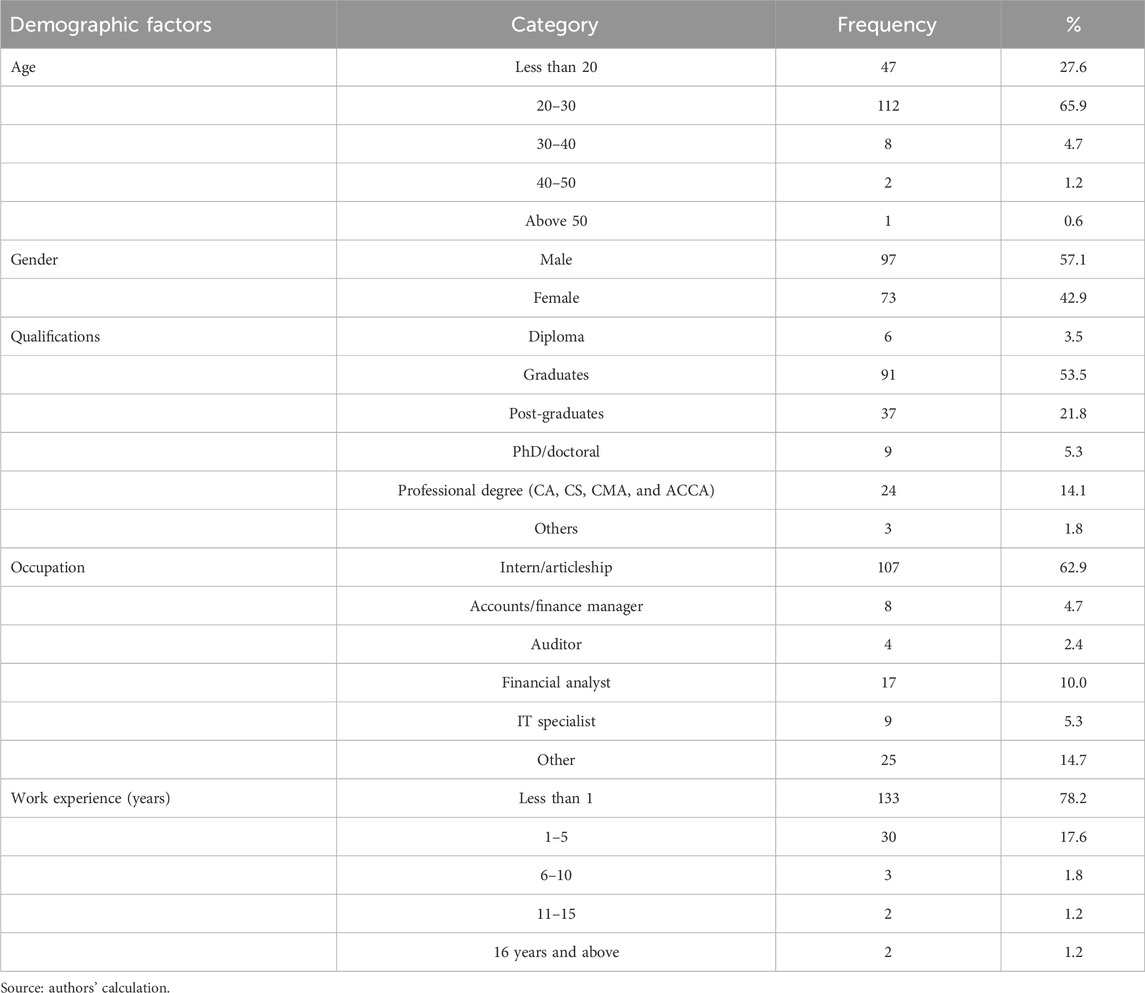

A survey-based method was used to gather the main empirical data for this study. Google Forms was used to design the questionnaire, which was then distributed to the author’s LinkedIn professional network. This was done to reach out to a diverse range of professionals, varying in gender, age, education, and technological experience (Table 1). The questionnaire items were designed based on the previously validated scales and adjusted to fit the context of blockchain technology with financial reporting and auditing. The items in the questionnaire were measured on a five-point Likert scale, from 1 as “strongly disagree” to 5 as “strongly agree.” The data obtained was reviewed with AMOS-SPSS statistical software to filter the correct sample.

Table 1. Demographic data.

The population of this study comprised professionals and practitioners in the accounting, auditing, and finance fields with expertise in financial reporting and auditing processes. Respondents to the questionnaire were auditors, finance/accounts managers, articleship practitioners, management students specializing in finance, and technical experts like blockchain developers and engineers. The inclusion of interns in the sample can be justified on the basis that they represent the next-generation of professionals entering the accounting and auditing fields. These individuals are often more familiar with modern technological advances, including blockchain, as they are exposed to such innovations during their academic training (Anis, 2023; Chowdhury et al., 2023). Their views can offer a forward-looking perspective on how emerging technologies may be embraced in the future. Furthermore, the study’s focus on aspects such as awareness, training, and attitudes toward blockchain tools is equally relevant to those at the beginning of their careers (Atadoga et al., 2024; Li et al., 2023). Insights gathered from this demographic provide an understanding of how new professionals are likely to adapt to and influence the integration of blockchain into financial reporting. Despite the limited experience of this group, their input remains valuable in assessing the potential direction of technological adoption within the industry (Han et al., 2023).

Through practical exposure to real-world financial and auditing procedures, an articleship can offer insights into the operational difficulties and uptake of cutting-edge technologies such as blockchain. This experience allows researchers to assess how blockchain affects efficiency, compliance, and transparency by bridging the gap between theoretical knowledge and real-world application. Data from audits and client interactions collected in the field add useful evidence to back up the research findings here and increases this study’s relevance.

To assess the influence of demographic factors, this study conducted further analysis to explore whether age, gender, and work experience affected its key relationships. The results revealed that age had a noticeable impact, particularly participants aged 20–30, who showed greater engagement and understanding of blockchain-related concepts than other age groups. Gender did not significantly influence the responses, indicating that both male and female participants shared similar perceptions. However, work experience showed a marginal effect, with those having less than 1 year of experience being more receptive to technological advances, possibly due to recent academic exposure. These insights have been integrated into the interpretation section of the study to provide a clearer understanding of how demographic variations shape participants’ perspectives.

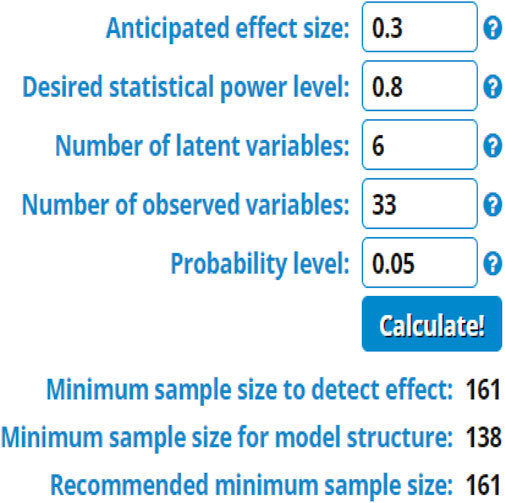

The questionnaire comprised items including the demographic details of the respondents and 33 items for the measurement of factors. A total of 183 people participated in this survey, but 13 of them were removed due to incompleteness and the nature of their engagement, such as pattern responses and faster completion time. This is why the analysis was conducted using the responses from 170 people. The sample size for the study was determined using Daniel Soper’s (2021) online sample size calculator based on Cohen (2013) and Christopher Westland (2010). For structural equation modeling, a priori sampling was chosen to identify the required sample size. Six latent constructs, 33 items, a 0.05 probability level, an anticipated effect size of 3, a desired statistical power level of 0.8, and 161 as minimum sample size were all required (Figure 2). A sample of 170 respondents was collected for the paper, which exceeded the sample’s threshold level.

Figure 2. Daniel soper sample size calculation. Source: https://www.danielsoper.com/statcalc/calculator.aspx?id=89.

7 Data analysis

Structural equation modeling with AMOS-SPSS was used to examine the hypothesized paths of the research model. Survey findings were obtained by processing data with AMOS data analysis software. The survey was conducted from March to June 2024.

This research used structural equation modeling with AMOS-SPSS to examine relationships between constructs related to blockchain technology implementation in financial reporting and auditing. AMOS-SEM is a robust statistical technique for exploring complex interactions and dependencies among multiple factors. The analysis section includes different statistical analyses and tests, one of which is factor analysis. Before conducting factor analysis, pre-analysis was done to verify the appropriateness of the data.

7.1 Measurement model assessment

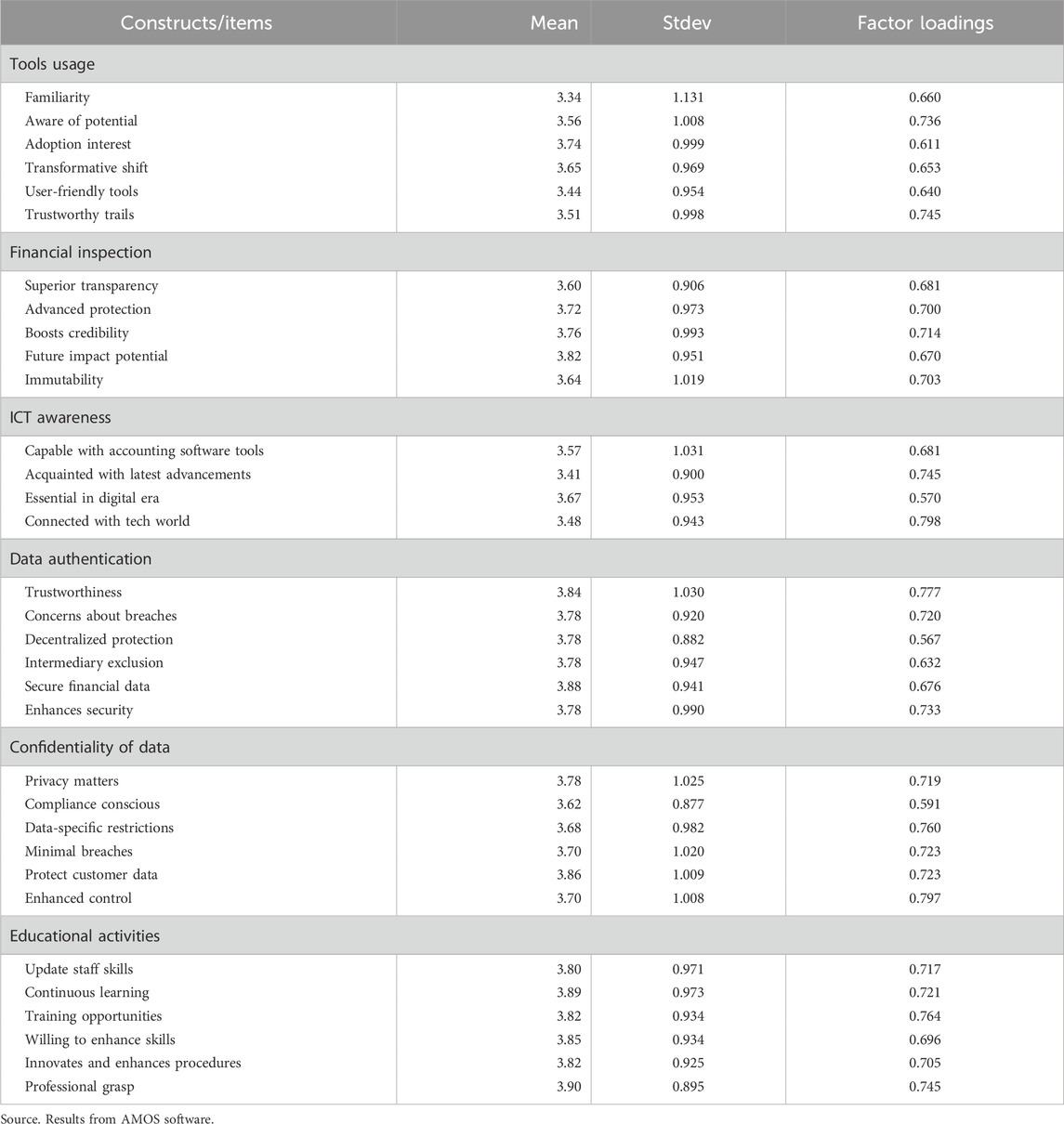

Structural equation modeling (SEM) involves two processes: testing the measurement model and developing the structural model. The measurement model shows how the underlying constructs and the response items are related. Through factor analysis and the reliability estimations of all scale items, preliminary analysis showed that the data were suitable for further statistical analyses. Table 2 depicts the measurement used with their corresponding mean and standard deviation and factor loadings to assess the measurement model validity.

Table 2. Measurement items.

Based on this analysis, six factors contained at least one pair of items with strong relationships to their respective factors (factor loadings >0.7). Ultimately, the reliability of each item’s Cronbach’s alpha was assessed. Each coefficient greater than 0.60 for adapted scales and 0.70 for existing scales was considered a reliable measure of the constructs under study (Hair et al., 2014a). Reliability analysis obtained scores in the range of 0.831 to 0.917.

7.2 Reliability test

The data collected from the participants were input into Excel spreadsheets in preparation for transfer to the statistical software. Statistical analysis was then conducted on the selected data sample. The validity of the sample size was assessed for this purpose. Reliability results are summarized in Table 3.

Table 3. Reliability assessment for all constructs.

The data were analyzed with IBM SPSS Statistics 23. Before using Amos, the data’s reliability was tested using SPSS, which provided the Cronbach’s alpha of each factor to estimate the construct reliability. The results showed the blockchain tools usage scale with six items (α = 0.893); the financial reporting and auditing scale with five items (α = 0.886) were found reliable. Likewise, the ICT awareness scale with four items (α = 0.831), the data security scale with six items (α = 0.888), the data privacy scale with six items (α = 0.894), and the training scale with six times (α = 0.917) all also found reliable. A construct is reliable if the Alpha (α) value is more than 0.70 (Hair et al., 2014b). Accordingly, it can be said that it is acceptable based on the reliability statistics.

The results of Table 4 reveal that there is excellent sampling adequacy, as indicated by the KMO (Kaiser–Meyer–Olkin measure of sampling adequacy) value of 0.936 > 0.5. Additionally, the significant Bartlett’s test (p < 0.05) specifies the existence of significant correlations between the factors and suitability of the data for factor analysis. Bartlett’s test of sphericity resulted in a chi-square value of 4,098.573, 528 degrees of freedom, and a significant p-value (p < 0.001), resulting in the strong rejection of the null hypothesis that assumed no factor correlations. In this case, the data contain sufficient correlations, meeting another important requirement for effective factor analysis.

Table 4. KMO and Bartlett’s test of sphericity.

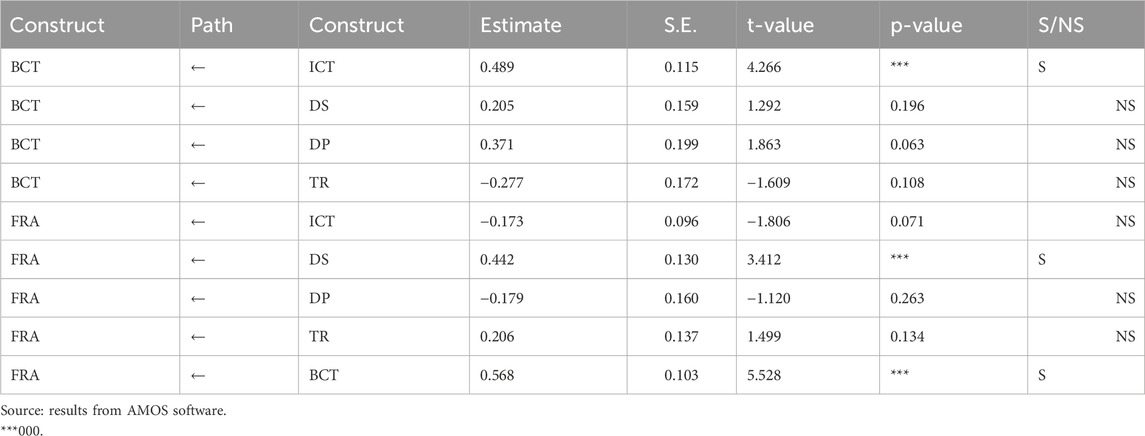

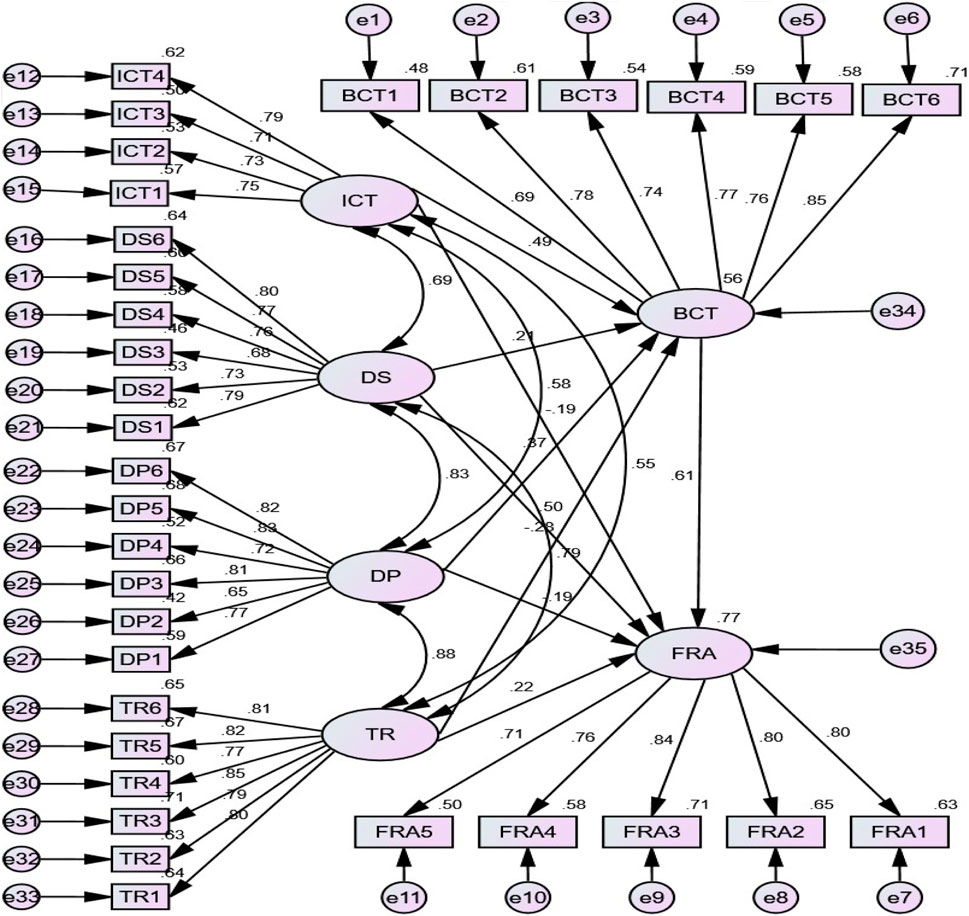

Path coefficients from a structural equation model are depicted in Table 5, showing hypothesized relationships between constructs. The significant positive path includes ICT to BCT with a significant weight of 0.489, DS to FRA with significant weight of 0.442, and BCT to FRA with significant weight of 0.568. Non-significant paths include DS, DP, and TR to BCT, with non-significant weights of 0.205, 0.371, and −0.277 respectively. However, ICT, DP, and TR to FRA had non-significant weights of −0.173, −0.179, and 0.206, respectively.

Table 5. Regression weights: (Group number 1—Default model).

The structural model results indicate several non-significant relationships that warrant further interpretation. The path from blockchain technology (BCT) to digital skills (DS) (β = 0.205, p = 0.196) and data privacy (DP) (β = 0.371, p = 0.063) suggests that although blockchain may influence these areas, the effect was not statistically strong in this context. Similarly, BCT’s negative relationship with trust (TR) (β = −0.277, p = 0.108) indicates that the implementation of blockchain may not necessarily foster trust and could potentially raise concerns among users. Additionally, the path from financial reporting and auditing (FRA) to ICT (β = −0.173, p 0.071), DP (β = −0.179, p = 0.263), and TR (β = 0.206, p = 0.134) also did not reach significance, implying that the influence of auditing practices on these constructs may be limited or context-dependent. These non-significant findings highlight areas where further investigation is needed to understand the conditions under which blockchain and financial reporting influence these variables.

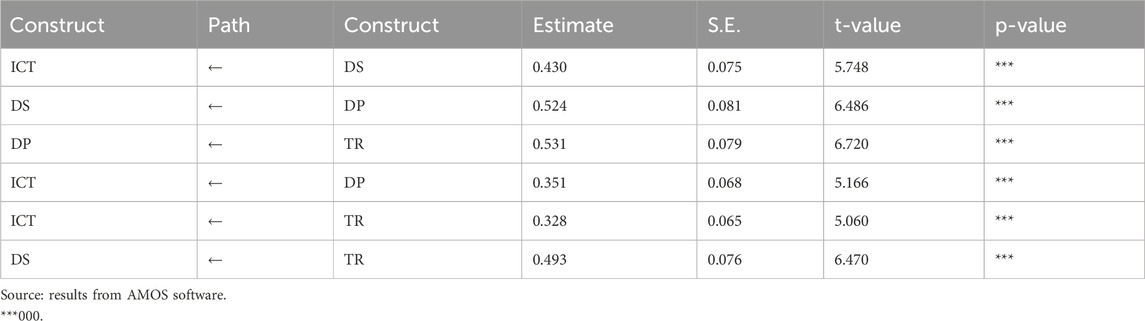

Table 6 shows covariances between pairs of variables. All covariances appear statistically significant and P-values less than 0.05. The table indicates the strong connections between ICT, data security, data privacy, and training in today’s technology-focused world. An improved cycle that supports financial reporting and auditing procedures can be generated by increased the knowledge and understanding of ICT results in enhanced data security, privacy, and training methods.

Table 6. Covariances: (Group number 1—Default model).

7.3 Model fitness

Confirmatory factor analysis (CFA) was used to assess the model fit of the measurement model that included all six components (Figure 3). Different criteria were examined to test the model fit. Implied by 480 degrees of freedom and a chi-square(x2) test result of 1.791 is a balanced relationship between the model’s complexity and data fit. The p-value (p = 0.000) indicates the true correlation present in the data. The comparative fit index (CFI = 0.902), standardized root mean square residual (SRMR = 0.05), and root means square error of approximation (RSMEA = 0.068) reflect perfect fit (Malkanthie, 2019; Zarifis and Cheng, 2022). Fit index values thus indicate that the model fits the dataset well.

Figure 3. Structural model with results. Source: Results from AMOS software.

8 Findings and discussion

Traditional accounting systems process transactions using cash, bank transfers, and digital payments. However, with the increasing adoption of cryptocurrencies like Bitcoin, the financial landscape is evolving. Cryptocurrencies offer advantages such as lower transaction fees, faster transfers, and enhanced security. If the future’s financial transactions predominantly occur through cryptocurrencies, the need to adopt blockchain technology in financial reporting and auditing becomes imperative. According to Javaid et al. (2022), financial or technological companies see blockchain as an innovative technology and aspire to become experts in how it can offer services to clients. This pertains to companies or firms that specialize in creating blockchain technologies and assist them in incorporating them to enhance efficiency, scalability, and expansion.

The use of blockchain tools by accountants in financial reporting and auditing was shown to be positively correlated with their ICT awareness, with more awareness resulting in greater technological adoption. This finding is consistent with earlier studies (Coyne and McMickle, 2017) which emphasized the role of ICT knowledge in effectively implementing new technologies. The role of ICT awareness in blockchain adoption is significant as it influences how accountants perceive and utilize this technology. The more familiar accountants are with blockchain and its potential, the more likely they are to integrate it into their workflow, thus improving the efficacy and accuracy of financial reporting and audits. Data security was a critical factor influencing blockchain tool adoption, while data privacy had a positive but not statistically significant effect. Blockchain’s cryptographic security features are a significant factor in its popularity as they address major concerns about data integrity and protection against unauthorized access. The strong covariance between data security and privacy suggests that these factors are closely linked, and improvements in one area probably to benefit the other. Organizations must focus on implementing strong security and privacy measures to build trust and confidence in blockchain technology, and this is validated by the study that demonstrates psychological disposition, sociological factors, trust in organizations, and trust in artificial intelligence all have an impact on trust, validating a unified trust model for fintech and insurtech. Trust in artificial intelligence is greatly impacted by preconceived notions about the technology (Malkanthie, 2019). Another study also highlighted the same perspectives that fintech technology adoption is highly influenced by price value, habit, social influence, performance expectancy, effort expectancy, and facilitating conditions, with performance and effort expectancy being the most powerful predictors. Service quality, reputation, and regulatory support all influence trust, whereas perceived risk undermines trust, with a focus on fostering trust, user-centric design, and regulatory support. Behavioral intention is a powerful predictor of use (Zarifis and Cheng, 2022). Training lacked statistical significance, but its positive relationship indicates that it is still an important factor. Current blockchain tool usage was 40%, with a strong interest in future adoption. Thorough training programs that address both the technical aspects and real-world applications of blockchain technology are essential. Such programs aim to boost the confidence and expertise of accounting professionals in utilizing blockchain tools. Accountants must pursue continuous professional development to keep up with technological advances and be capable of exploiting new tools and systems effectively.

Blockchain technology positively impacted financial reporting and auditing, improving accuracy and transparency, leading to reduced audit time and increased trust in financial reports. These findings matched the perspectives of Schmitz and Leoni (2019), who emphasized the ability of blockchain to transform financial processes. Blockchain technology has the potential to significantly enhance the reliability and integrity of financial reporting by offering a secure and transparent ledger system (Atadoga et al., 2024). As organizations increasingly recognize its benefits, the adoption of blockchain is expected to grow, leading to improved quality, accuracy, and trustworthiness in financial reporting and auditing processes.

9 Conclusion

This research is among the few empirical studies that have analyzed the influence of blockchain technology on financial reporting and audit practices as possible factors for its effectiveness. It examines the factors influencing the implementation of blockchain technologies in financial reporting and audit processes. Information and communications technologies (ICT), data security (DS), data privacy (DP), and training (TR) are factors which influence the use of blockchain technology and financial reporting and audit processes. With a sample size of 170 participants, the measurement items’ internal consistency reached the required value. The lowest Cronbach’s alpha value was 0.831 and the highest was 0.917, indicating the acceptability of this model and its associated factors. Blockchain’s integration into existing financial reporting and auditing systems requires careful planning and collaboration among accountants, auditors, and blockchain developers. The integration process should involve raising accountants’ ICT awareness, providing adequate training, ensuring robust data security measures, and addressing data privacy concerns.

10 Limitations and future scope

The use of a cross-sectional research design in this study, while suitable for capturing respondent views at a specific moment, presents a limitation in understanding how perceptions and adoption patterns might shift over time. To gain more comprehensive insights into the dynamics of blockchain implementation in financial reporting, future studies could benefit from adopting a longitudinal design. This would allow researchers to track developments and changes as both the technology and regulatory environments continue to evolve.

Another important consideration is the reliance on self-reported data, which may be subject to biases such as respondents providing answers they believe are socially acceptable rather than reflecting their actual experiences or behaviors. Although measures like pre-testing and reliability analysis were conducted to ensure consistency, incorporating more objective metrics such as verified usage statistics or adoption case studies would enhance data accuracy and reduce potential bias.

In addition, the exclusive use of quantitative methods limits the ability to explore the deeper contextual and organizational influences that affect technology adoption. Future research would benefit from a mixed-methods strategy, combining statistical analysis with qualitative approaches such as interviews, focus group discussions, or detailed case evaluations. These methods could offer richer, more nuanced perspectives on factors such as institutional readiness, cultural attitudes toward innovation, and perceived implementation challenges. Such an approach would lead to a more thorough understanding of how blockchain is being integrated into financial reporting and auditing in real-world settings.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors without undue reservation.

Ethics statement

Ethical approval was not required for the study involving human samples in accordance with the local legislation and institutional requirements. Written informed consent for participation in this study was provided by the participants’ legal guardians/next of kin.

Author contributions

SS: Methodology, Writing – review and editing. VC: Writing – review and editing, Data curation, Methodology, Formal analysis. DD: Methodology, Software, Writing – original draft. SC: Writing – review and editing, Methodology, Investigation, Software. NC: Writing – original draft, Data curation, Investigation, Visualization. RK: Writing – review and editing, Methodology, Conceptualization, Formal analysis, Visualization, Software.

Funding

The author(s) declare that no financial support was received for the research and/or publication of this article.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Abreu, P. W., Aparicio, M., and Costa, C. J. (2018). Blockchain technology in the auditing environment. Iber. Conf. Inf. Syst. Technol. Cist., 1–6. doi:10.23919/CISTI.2018.8399460

Agrifoglio, R., and de Gennaro, D. (2022). New ways of working through emerging technologies: a meta-synthesis of the adoption of blockchain in the accountancy domain. J. Theor. Appl. Electron. Commer. Res. 17 (2), 836–850. doi:10.3390/jtaer17020043

Almadadha, R. (2024). Blockchain technology in financial accounting: enhancing transparency, security, and ESG reporting. Blockchains 2 (3), 312–333. doi:10.3390/blockchains2030015

Amnas, M. B., Selvam, M., Raja, M., Santhoshkumar, S., and Parayitam, S. (2023). Understanding the determinants of FinTech adoption: integrating UTAUT2 with trust theoretic model. J. Risk Financ. Manag. 16 (12), 505. doi:10.3390/jrfm16120505

Anis, A. (2023). Blockchain in accounting and auditing: unveiling challenges and unleashing opportunities for digital transformation in Egypt. J. Humanit. Appl. Soc. Sci. 5 (4), 359–380. doi:10.1108/jhass-06-2023-0072

Ankenbrand, T., and Bieri, D. (2018). Assessment of cryptocurrencies as an asset class by their characteristics. Invest. Manag. Financ. Innov. 15 (3), 169–181. doi:10.21511/imfi.15(3).2018.14

Anwar, S., Shukla, V. K., Rao, S. S., Sharma, B. K., and Sharma, P. (2019). Framework for financial auditing process through blockchain technology, using identity based cryptography. ITT 2019 - Inf. Technol. Trends Emerg. Technol. Blockchain IoT, 099–103. doi:10.1109/ITT48889.2019.9075120

Atadoga, A., Asuzu, O. F., Ayinla, B. S., Leonard Ndubuisi, N., Ike, C. U., and Adeleye, R. A. (2024). Blockchain technology in modern accounting: a comprehensive review and its implementation challenges. World J. Adv. Res. Rev. 21 (2), 218–234. doi:10.30574/wjarr.2024.21.2.0440

Bellucci, M., Cesa Bianchi, D., and Manetti, G. (2022). Blockchain in accounting practice and research: systematic literature review. Meditari Acc. Res. 30 (7), 121–146. doi:10.1108/MEDAR-10-2021-1477

Bonyuet, D. (2020). Overview and impact of blockchain on auditing. Int. J. Digit. Acc. Res. 20, 31–43. doi:10.4192/1577-8517-v20_2

Brender, N., Gauthier, M., Morin, J.-H., and Salihi, A. (2019). The potential impact of blockchain technology on audit practice. J. Strateg. Innov. Sustain. 14 (2), 1–45. doi:10.33423/jsis.v14i2.1370

Cekerevac, Z., and Cekerevac, P. (2022). Blockchain and the application of blockchain technology. Mest. J. 10 (2), 14–25. doi:10.12709/mest.10.10.02.02

Chowdhury, E. K., Stasi, A., and Pellegrino, A. (2023). Blockchain technology in financial accounting: emerging regulatory issues. Rev. Econ. Financ. 21, 862–868. doi:10.55365/1923.x2023.21.94

Christopher Westland, J. (2010). Lower bounds on sample size in structural equation modeling. Electron. Commer. Res. Appl. 9 (6), 476–487. doi:10.1016/j.elerap.2010.07.003

Coyne, J. G., and McMickle, P. L. (2017). Can blockchains serve an accounting purpose? J. Emerg. Technol. Acc. 14 (2), 101–111. doi:10.2308/jeta-51910

Dai, J., and Vasarhelyi, M. A. (2017). Toward blockchain-based accounting and assurance. J. Inf. Syst. 31 (3), 5–21. doi:10.2308/isys-51804

Danach, K., Hejase, H. J., Faroukh, A., Fayyad-Kazan, H., and Moukadem, I. (2024). Assessing the impact of blockchain technology on financial reporting and audit practices. Asian Bus. Res. 9 (1), 30. doi:10.20849/abr.v9i1.1427

Demirkan, S., Demirkan, I., and McKee, A. (2020). Blockchain technology in the future of business cyber security and accounting. J. Manag. Anal. 7 (2), 189–208. doi:10.1080/23270012.2020.1731721

Duong, T. Q. L. (2020). Impact of blockchain technology to field accounting and auditing. Eur. J. Econ. Manag. Sci. (4), 3–6. doi:10.29013/ejems-20-4-3-6

Dyball, M. C., and Seethamraju, R. (2022). Client use of blockchain technology: exploring its (potential) impact on financial statement audits of Australian accounting firms. Account. Audit. Acc. J. 35 (7), 1656–1684. doi:10.1108/AAAJ-07-2020-4681

El Koshiry, A., Eliwa, E., Abd El-Hafeez, T., and Shams, M. Y. (2023). Unlocking the power of blockchain in education: an overview of innovations and outcomes. Blockchain Res. Appl. 4 (4), 100165. doi:10.1016/j.bcra.2023.100165

Foroglou, G., and Tsilidou, A. L. (2015). Further applications of the blockchain. Conf. 12th Stud. Conf. Manag. Sci. Technol. Athens, 0–8.

Giang, N. P., and Tam, H. T. (2023). Impacts of blockchain on accounting in the business. SAGE Open 13 (4), 1–13. doi:10.1177/21582440231222419

Gokoglan, K. G., and Cetin, S. (2022). Blockchain technology and its impact on audit activities. Pressacademia 9, 72–81. doi:10.17261/pressacademia.2022.1567

Hair, J. A. R., Babin, B., and Black, W. (2014b). Multivariate data analysis.pdf. Aust. Cengage, United States, 7, 758.

Hair, J. F., Black, W. C., Babin, B. J., and Anderson, R. E. (2014a). Multivariate data analysis. 7th ed. Pearson Education.

Hakami, T., Sabri, O., Al-Shargabi, B., Rahmat, M. M., and Nashat Attia, O. (2023). A critical review of auditing at the time of blockchain technology – a bibliometric analysis. EuroMed J. Bus. 19, 1173–1201. doi:10.1108/EMJB-01-2023-0010

Han, H., Shiwakoti, R. K., Jarvis, R., Mordi, C., and Botchie, D. (2023). Accounting and auditing with blockchain technology and artificial intelligence: a literature review. Int. J. Acc. Inf. Syst. 48, 100598. doi:10.1016/j.accinf.2022.100598

Javaid, M., Haleem, A., Singh, R. P., Suman, R., and Khan, S. (2022). A review of blockchain technology applications for financial services. BenchCouncil Trans. Benchmarks, Stand. Eval. 2 (3), 100073. doi:10.1016/j.tbench.2022.100073

Kim, J. W. (2020). Blockchain technology and its applications: case studies. J. Syst. Manag. Sci. 10 (1), 83–93. doi:10.33168/jsms.2020.0106

Krichen, M., Ammi, M., Mihoub, A., and Almutiq, M. (2022). Blockchain for modern applications: a survey. Sensors 22 (14), 5274–27. doi:10.3390/s22145274

Li, Y., Ma, X., Li, Y., Li, R., and Liu, H. (2023). How does platform’s fintech level affect its word of mouth from the perspective of user psychology? Front. Psychol. 14 (1), 1085587. doi:10.3389/fpsyg.2023.1085587

Liu, M., Wu, K., and Xu, J. J. (2019). How will blockchain technology impact auditing and accounting: permissionless versus permissioned blockchain. Curr. Issues Audit. 13 (2), A19–A29. doi:10.2308/ciia-52540

Mahdani, R., Risnafitri, H., and Risnafitri, H. (2024). Exploring the potential applications of blockchain technology in accounting practice: a systematic literature review. J. Din. Akunt. Dan. Bisnis 11 (1), 15–32. doi:10.24815/jdab.v11i1.33476

Makridakis, S., and Christodoulou, K. (2019). Blockchain: current challenges and future prospects/applications. Futur. Internet 11 (12), 258–16. doi:10.3390/FI11120258

Malkanthie, A. (2019). Chapter-1 the basic concepts of structural equation modeling, 1.1. Introduction. doi:10.13140/RG.2.1.1960.4647

Mittal, H. (2021). Blockchain technology: architecture, consensus protocol and applications. Blockchain, 3, 1–7.

Pimentel, E., and Boulianne, E. (2020). Blockchain in accounting research and practice: current trends and future opportunities. Acc. Perspect. 19 (4), 325–361. doi:10.1111/1911-3838.12239

Puthal, D., Malik, N., Mohanty, S. P., Kougianos, E., and Yang, C. (2018). The Blockchain as a Decentralized Security Framework [Future Directions]. IEEE Consum. Electron. Mag. 7 (2), 18–21. doi:10.1109/MCE.2017.2776459

Qin, S. (2022). A review of research on the impact of blockchain on financial reporting. Account. Audit. Financ. 3 (1), 51–58. doi:10.23977/accaf.2022.030108

Roszkowska, P. (2021). Fintech in financial reporting and audit for fraud prevention and safeguarding equity investments. J. Acc. Organ. Chang. 17 (2), 164–196. doi:10.1108/JAOC-09-2019-0098

Sarwar, M. I., Iqbal, M. W., Alyas, T., Namoun, A., Alrehaili, A., Tufail, A., et al. (2021). Data vaults for blockchain-empowered accounting information systems. IEEE Access 9, 117306–117324. doi:10.1109/ACCESS.2021.3107484

Schmitz, J., and Leoni, G. (2019). Accounting and auditing at the time of blockchain technology: a research agenda. Aust. Acc. Rev. 29 (2), 331–342. doi:10.1111/auar.12286

Sheela, S., Alsmady, A. A., Tanaraj, K., and Izani, I. (2023). Navigating the future: blockchain’s impact on accounting and auditing practices. Sustainability 15 (24), 16887. doi:10.3390/su152416887

Tandon, A., Kaur, P., Mäntymäki, M., and Dhir, A. (2021). Blockchain applications in management: a bibliometric analysis and literature review. Technol. Forecast. Soc. Change 166, 120649. doi:10.1016/j.techfore.2021.120649

Tapscott, D., and Tapscott, A. (2016). Blockchain Revolution: How the Technology Behind Bitcoin Is Changing Money, Business, and the World. United States: Penguin Publishing Group.

Upadhyay, N. (2020). Demystifying blockchain: a critical analysis of challenges, applications and opportunities. Int. J. Inf. Manage. 54, 102120. doi:10.1016/j.ijinfomgt.2020.102120

Verma, P., and Ram, B. (2024). Application of blockchain technology in data security. IP Indian J. Libr. Sci. Inf. Technol. 1, 51–55. doi:10.18231/j.ijlsit.2024.008

Vokerla, R. R. (2019). “An overview of blockchain applications and attacks,” in Proc. - int. Conf. Vis. Towar. Emerg. Trends commun. Networking, ViTECoN 2019, 1–6. doi:10.1109/ViTECoN.2019.8899450

Yu, T., Lin, Z., and Tang, Q. (2018). Blockchain: the introduction and its application in financial accounting. J. Corp. Acc. Financ. 29 (4), 37–47. doi:10.1002/jcaf.22365

Keywords: Blockchain technology, smart contracts, accounting, financial reporting, auditing, ICT, data security, data privacy

Citation: Saheb SS, Chinnapareddy VKR, Devalla D, Charugulla S, Chakka NB and Raja Sekhar K (2025) Factors leading to the adoption of blockchain technology in financial reporting. Front. Blockchain 8:1491609. doi: 10.3389/fbloc.2025.1491609

Received: 05 September 2024; Accepted: 17 July 2025;

Published: 20 August 2025.

Edited by:

Marcelle Michelle Georgina Maria Von Wendland, Bancstreet Capital Partners Ltd, United KingdomReviewed by:

Alex Zarifis, University of Southampton, United KingdomHebatallah Badawy, Egypt-Japan University of Science and Technology, Egypt

Copyright © 2025 Saheb, Chinnapareddy, Devalla, Charugulla, Chakka and Raja Sekhar. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Shaiku Shahida Saheb, c2hhaGlkLnNrQHZpdGFwLmFjLmlu