Gaia R. Greco

Gaia R. Greco Marco Cinquegrani

Marco Cinquegrani- 1General Services, Stazione Zoologica Anton Dohrn, Naples, Italy

- 2Istituto di Calcolo e Reti ad Alte Prestazioni, Consiglio Nazionale delle Ricerche, Naples, Italy

Marine biology made in the last four decades giant leaps. Several scientific and technological breakthroughs shaped research in the marine environment. Thanks to the revelation of the enormous width and complexity of sea life, marine biotechnology began a fast path of development that involved both the public and the private domain. Although there exist some studies on the dimensions and the evolution of the industry, few and scattered is the knowledge about the firms and the dynamics that characterize the sector. The authors carry out a first investigation of the private organizations that belong to blue biotechnology through the construction of an “ad hoc” sample of firms. It is analyzed the geographical and temporal distribution, the products and services offered and the markets served.

Introduction

Several progresses in the scientific and technological fields shaped marine biological research in the last 40 years. Marine biology has been shaken by molecular biology revolution first and “omic” sciences later. At the same time, underwater exploration made giant leaps with the continuous advancements in scuba-diving and, more recently, with the introduction of Remotely Operated Underwater Vehicles (ROVs), unmanned vehicles and gliders (and the increase of their relative affordability).

Technological developments opened new ways to collect organisms and brought new discoveries. While in 1970 s the investigation of marine ecosystems began with the collection of large creatures (sponges, soft corals, red algae), it evolved then with the exploration of inaccessible areas and the classification of microorganisms. In Hu et al. (2011) the trend of novel products of marine origin is described from the early 1950 s to 2008. Before 1985 only a small number of compounds were discovered each year, never reaching a significant amount. The trend changed importantly at the end of 1980 s, peaking up to 400–500 products each year.

The incredible width and complexity of marine organisms revealed its uniqueness (compared to terrestrial one). The biological, chemical, and genetic differences of aquatic habitats showed their biotechnological potential. The new developments of knowledge on marine environments changed the way in which scientists pursue research, while opening the way to new stakeholders. Public institutions, Governments, and companies took great interest in the potential of these resources, hoping to create new wealth and new inventions to bring to the market.

In Horizon 2020, Blue Growth Strategy, it is underlined that “marine biodiversity and biotechnology research have a huge potential to contribute to new knowledge for high value products and processes and increase marine resources and biodiversity understanding”1 Blue Growth budget for 2014–2015 amounts to €145 million, providing €8 million for Small and Medium Enterprises (SMEs), not considering that there are also other cross-thematic opportunities (in food security, energy, transport, materials, and research infrastructures).

Although the importance of marine resources has been recognized in the scientific, political, and economic environments, a clear picture of the firms that live the sector and their characteristics is not easy to find.

Aim of this paper is to provide scientists and research managers who desire a deeper understanding an up-to-date picture of the dynamics that shape marine biotechnology industry. The authors particularly wish to be of some help to researchers that conduct basic research that could easily become applied, giving them an idea of the actors of the marine sectors and the benchmarks to which to refer.

In the first place, the main reports on the general sector and the investigations realized on the organizations that belong to it will briefly introduced, trying to delineate the state of the art of the knowledge on marine industries. Afterwards, some first evidences result of the construction and the analysis of an original database will be presented and discussed. It will be described the main types of firms and their geographical distribution, the main products, and services offered, the interdependence among the markets served by the companies.

After giving a definition of what is meant for “blue” and “biotechnology” in the economic and institutional literature, some recent studies on the industry will be presented. As it will be showed afterwards, many questions remain unanswered. Through the construction of a specific sample, the authors wish, as it is described in the “finalities of the project,” to understand the main trends and the dynamics of marine industries. The methodology of the report followed a multiple phases process to gather the information on the companies that belong to blue biotechnology. Although, as it will be explained later, this is a secondary data analysis, several issues have come to light. In the “results” paragraph, main results are presented and discussed. The paper concludes with some considerations on the actors that participate to the growth of the industry, stressing the need for further investigations.

The Blue Biotechnology Industry

Blue is the color of the oceans and of the seas and that's simply why it defines the world of biotechnology that uses molecules and substances of marine origin. While the other biotechnology sectors are defined by colors because of the use in specific industries (red for pharmaceuticals, white for industrial biotechnology, green for agricultural), blue biotech is the only one that is defined by the resources involved in the offering of products and services, not by his markets2.

In “Beyond borders, Unlocking value”3,4,5, Ernst and Young, one of the most important consulting firm of the world, elaborates its annual report on the biotechnology industry, analyzing the main actors, and the principal trends that shape the sector. Much attention is dedicated to red biotechnology, as it results as the driving segment of all the industries. It is underlined the very importance of research and development activities inside the company, with other firms and, above all, with academic institutions. There is no mention to marine biotechnology as an industrial sector.

In the Deloitte report “2015, Global life sciences outlook”6 too, the general discourse on sales and growth data doesn't take in consideration directly the marine environment and his firms.

In the first report, anyway, different companies that use marine compounds are mentioned. In specific, there are Perrigo and Elan Corporation, Jazz Pharmaceuticals and Gentium, Allergan, and MAP cited in the “best” Mergers and Acquisition of 2013.

Of course, the fact that companies that use marine compounds don't appear directly in the reports realized on the general sector is not a consequence of the lesser importance or of the novelty of blue biotechnology. Firms that belong to the blue industry are biotechnology companies. By now, marine organisms (and the substances derived) are, as it will be shown in the continuum, employed in the production of drugs, enzymes, nutritional additives, cosmetics, and many more products and services. So they belong to all the sub-sectors related to biotechnology: red, green, and white. This makes clear why it is not easy to define the dimension of blue biotechnology markets.

It would be also stressed in this paper the definition given by OECD (Organization for Economic Co-operation and Development) in 2009 of what a biotechnology firm is, as it is not trivial: “a firm that is engaged in biotechnology by using at least one biotechnology technique to produce goods or services and/or to perform biotechnology R&D. Some of these firms may be large, with only a small share of total economic activity attributable to biotechnology”7. So it refers to all the companies that use a biotechnology technique in the production or in the Research and Development activities (not necessarily as core activities). The spectrum of analysis is therefore effectively wide8.

Different business cases are cited to describe the importance raised by blue biotechnology in these last years. In the pharmaceutical sector, the Spanish company Pharmamar co-developed with Johnson & Johnson Pharmaceutical R&D Yondelis (Trabectedin, ET-743). The product, used for the treatment of advanced soft tissue sarcoma, reached the market in 2007. The marine substance was isolated from Caribbean sea squirt (Ecteinascidia turbinata), taking 30 years to understand the structure of the active compound. Aquaculture and mariculture gave the company the chance to carry on clinical development, but they were too expensive to ensure industrial manufacturing. A long research process took Pharmamar through total synthesis first and semi-synthetic route later (Martins et al., 2014). Currently nine are the marine molecules approved to be used as medicines (Adcetris, Vira-A, Retrovir, Prialt, Lovaza, Halaven are some examples), while at least 13 find themselves on advanced clinical trials (Rangel and Falkenberg, 2015). Still the fluorescent protein (GFPs) finds its best application in biomedical research and cell and molecular biology. It works as a marker that emits light in the infra-red region of the electromagnetic spectrum, allowing visualization of processes invisible to normal light (Burgess, 2012). Shimokura, Chalfie, and Tsien received the Nobel prize in Chemistry in 2008 for the discovery and development of the protein, originally described from the jellyfish Aequorea Victoria (Arrieta et al., 2010). In the cosmetic industry, Estée Lauder gave birth to his skin care product Resilience which uses pseudopterosin, an anti-inflammatory extracted from a seafan. The natural compound was originally developed for the pharmaceutical sector, but reached the market much faster as a skin lotion (Martins et al., 2014).

Many “champions of innovation” can be found in blue biotechnologies both in pharmaceutics, cosmetics and other sectors (nutraceutical, food). Although of great interest and predictive of the difficulties faced by companies in the development of their technologies, they don't tell us much on the current status and future development of the blue biotechnology sector. Much of the scientific literature is produced on marine biomolecules, on the marine organisms that seem more promising, on the limiting factors related to harvesting and to chemical synthesis, but it is often untied to markets developments, to firms organization, to collaborative mechanisms between companies and research centers.

BCC Research, a provider of market research reports and a consulting firm, attempts to define the value of the marine-derived drugs. The marine pharma market is expected to rise by 2016, reaching a total value of €8.6 billion at a compound annual growth rate (CAGR) of 12.5% for the 5 years period from 2011 to 20169.

Global Industry Analysts10, a market research agency, forecasts a slightly below trend for blue biotechnologies as a whole, envisaging an annual growth rate of 4–5% and a market value of €3.5 billion by 201811.

OECD (2013), on the contrary, in its first publication on marine biotechnology, chooses to provide data on the value of potential markets for specific products, not providing odd estimation12.

In the “Study in support of Impact Assessment work on Blue Biotechnology” (DG Maritime Affairs and Fisheries, 2014) a conservative estimate values blue biotechnology in percentage of the EU bio-economic sector as a whole. In 2012, Marine biotechnology would represent the 2–5% of the sector (between around €300 and 750 millions). The growth rate being slightly below of the biotech sector (around 4–5%)13.

At present, there is no clear understanding of the main trends of the marine sectors as a complete picture is not easy to find. Leary et al. (2009) claim that, because of the commercially sensitive nature, information about blue biotechnology is scattered in multiple locations: patent database, companies and public research centers. Pietrabissa (2005) argues that 80% of all information on innovations is available exclusively in patent documents, not being propagated by any other communication channel.

In the “Study in support of Impact Assessment work on Blue Biotechnology” (DG Maritime Affairs and Fisheries, 2014) a stakeholder analysis is conducted, including not only companies, but also research centers, funding agencies, networks (286 stakeholders representing 236 institutions in 25 countries)14. With a mirroring exercise based on the total number of biotechnology firms in Europe in 2013 (1799), representing blue biotechnology 2–5% of the sector, the authors expect a number of companies between 36 and 90 (maybe higher considering new start-ups and new spin-offs). They found 97 private organizations, of which 71 were small and medium firms, while 26 big companies. Europe appears to be a major player in Blue Biotechnology at the international level thanks to its research and development activities and its infrastructure to support the access to marine resources. Other key players would be North America, in particular the US taking a leading role in algal biofuel sector and East Asia, leader in bioinformatics.

The Joint Research Centre of the European Commission (Vigani et al., 2015) analyses the market and the economic opportunities of micro-algae-based food and feed sector in the world. They underline the fact that data on algae-based food and feed products are firm-specific, there are available only estimated studies and there is no information on the products offered. They found 50 companies mainly distributed in North America, Europe (10 firms) and the Asian countries. Europe shows a high level of professionals in engineering and technical skills in the biofuel sector and great promises in the agro-food sector characterized by a solid tradition and high quality. The commercial production of microalgae would still be in its infancy, not representing a competitor for traditional agricultural commodities.

Are marine organisms still an underutilized resource? How many are the companies that use marine compounds in their production and R&D processes? Where are these firms? Are the big majority Small and Medium Enterprises (SMEs)? Are these organizations young? Do they serve one or more markets? What recent applications are (if any)?

Methodology

Finalities of the Project

The Flagship Project Ritmare is one of the National Research Programs funded by the Italian Ministry of University and Research for the period 2012–2016. It involves an integrated effort of the scientific community working on marine and maritime issues and some major industrial groups15 One of the objective of the program for all the academic institutions involved is to strengthen cooperation with the private sector in two complementary directions: inducing the research community to respond to the needs of industry and encouraging the latter to contribute to a relaunch of the technologies available to marine researchers.

For the Zoological Station Anton Dohrn, within the process of research valorization, one of the action envisaged was the drawing up of a database of possible users of the knowledge produced inside the institution. In the following, the finalities of the database, the methodology implemented, the sources of the information of the companies and the major difficulties faced will be explained.

Several purposes drove the carrying out of the database of firms that operate inside marine biological and biotechnological sector. In particular:

1. to investigate firms that effectively conduct research and production projects, utilizing organisms, and substances of marine origin;

2. to draw up a list of firms representative of the blue biotechnology business world;

3. to enlarge as much as possible the sample of organizations considered (as for the geographical scope, as for the sectors involved);

4. to gather up-to-date information about the organizations considered;

5. to have a set of variables on which to draw some first considerations.

A first analysis, although conducted through the descriptive and qualitative investigation of the sample, provides valuable insights, shedding some light onto the different mechanisms that characterize this young industry.

A Multiple Phases Methodology

It is possible to recognize three different phases in the sampling. At the beginning of the project the authors tried to understand the reliable sources from where to extrapolate the names of the firms interested by this research (scientific literature, reports). Then the main interest was to understand if these organizations were really involved in the production of goods and services of marine origin. In the last phase, they chose which variables to consider and they collected the data for all the firms in the sample. The research has been made between July and December 2014.

Phase 1—The Different Sources of Information

The collection of the companies' names followed a step-by-step process that reflects the use of different sources of information. Initially the authors gathered and analyzed the scientific literature on marine biotechnology firms and products (see Brar and McLarney, 2001; European Science Foundation, 2001; National Research Council, 2002; Atlantic Canada Opportunities Agency, 2003; Sea Grant Florida, 2004; InterMareC – Interregional Maritime Cluster, 2007; Sea Grant Florida, 2004; Atlanpole BlueCluster, 2009; Ellingsen and Tromso, 2010; Germany Trade & Invest, 2010; Lundquist et al., 2010; Marine Cluster, 2010; Nordwest-Verbund Meeresforschung, 2010; Cooke et al., 2011; Balasubramanian, 2012; Carlberg, 2012; Delving Deeper, 2012; Frahm, 2012; Norgenta DSN Analysen & Strategien, 2012; NetAlgae Project, 2012; Maritime Clusters in Västra Götaland, 2013; NC Biotechnology Center, 2013; 16, 17, 18, 19, 20, 21, 22, 23). Then they collected reports describing blue biotechnology sector structure in a general way and studies on maritime and biotechnology clusters of firms (Porter, 1998). Still, to have an idea of the companies directly involved in the research on marine bioactive compounds they investigated the marine pharmaceutical clinical pipeline (phase 1, 2, and 3) published by the Midwestern University24.

In different scientific and management papers on blue biotechnology emerged the participation of firms in several EU projects on marine issues. The authors decided to find if there were private partners that participated to the research programs. In Table 1, you can find for the Sixth and the Seventh Framework Programs considered for the drawing of the sample.

Table 1. European framework programs related to marine biotechnology.

With the aim to consider not only companies established in a European country, they found out private organizations participating to International Marine Associations. In particular, they collected the businesses members of EABA (European Algae Biomass Association), Algae Biomass Organization, NAABB (National Alliance for Advanced Biofuels and Bio-products)25, Japan Society of Marine Biotech, Pan-America Marine Biotech Association and ESMB (European Society for Marine Biotech).

Participants in international trade fairs and international organizations summit are another meaningful source of marine firms. Trade fairs always show companies active on different markets, looking for new clients, new partnerships, and new collaborations. In particular, the authors considered firms participating in: BIT's 4th Annual World Congress of Marine Biotechnology, Algae Biomass Organization Summit 2014, Biomarine International Cluster Business Convention 2014, CSA Marine Biotech 2013 ERA-NET.

They concluded the phase with a free research on the Google search engine26. This activity brought them to consider different companies lists associated to producers, association, and on-line magazines27.

Phase 2—The List of Firms

The various sources gave birth to a first list of companies that exploit marine-based organisms. Many firms, of course, were cited a number of times in the papers, in the economic reports and on the websites. For every single organization, the authors preliminarily verified whether this company belonged to the marine biotech sector. They gathered this information through the firm's website, that describe the products or the services offered, the markets served and the research processes they are conducting. In the case of companies' websites that resulted poor in the description of the activities or, on the contrary, too big to understand if there exists a clear link with compounds of marine origin, they made use of other sources, particularly of newspapers and magazines' articles (interviews and business' cases presented on the firms' websites on the page “Press releases or media”)28.

Phase 3—Variables and Limits

The information gathered for all the companies in the sample are:

• Business name

• Head Office (city, state)

• Websites URL

• Year of foundation

• Number of patents

• Short description of the products or services offered

• Markets served

• Multi National Corporation (MNC)

• Spin-off

• Others (general notes)

The information has been collected from the official webpage of the firms. In some cases the year of establishment was not clearly defined. In this case, the authors used the official linkedin or facebook page of the company.

Source: Thorndyke et al., 2013.

On the contrary, the data about the patents published were not gathered from the official webpage. To give coherence inside the sample, the authors chose to use the same source for all the companies involved in the research. Espacenet is, in fact, a service offered by the European Patent Office. It gives free access to more than 90 million patent (mainly applications) documents worldwide, containing information about inventions and technical developments from 1836 to today29. They made a research by applicant (the one who applies for and holds the rights deriving), investigating directly the company involved, trying to have an idea of the dimension of patents' portfolios30.

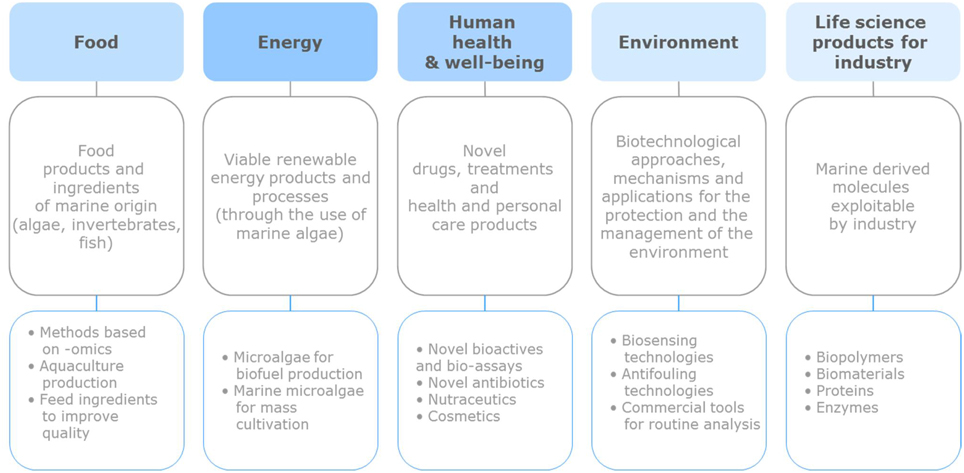

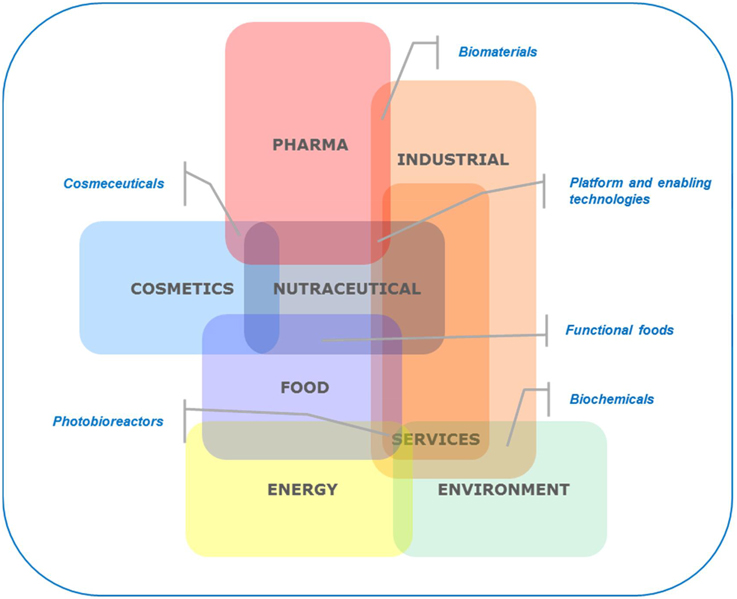

In order to have an equal and clear classification of the markets served, the authors have been inspired by the taxonomy of the sectors interested by marine biotechnology realized by the European Science Foundation in 2010 as it still represents the wider description of the products and sectors existing all taken together (a schematization of that taxonomy is offered in Figure 1). They decided, nevertheless, to add other served markets in the analysis, splitting “human health and well-being” in the pharmaceutical, nutraceutical and cosmetic sectors. At the same time, they didn't consider the aquaculture production sector as a whole, but only the research services devoted.

Figure 1. The sectors served by marine biotech.

In the general notes, they collected additional information about the way the company was born (spin-off, joint-venture), if it belonged to a group, if there were other sites of production. Part of these notes were worth the analysis and they decided to construct two more variables: spin-offs and multinational corporations. For spin-offs the authors decided to re-check the firms that showed professors and PhDs as entrepreneurs (or as members of the Board of Directors). To create a subclass of organizations that could shed some light onto the dimensional issue, they took the classifications (Forbes, 2010—first 2000, and Fortune, 2014—first 500) of the world's biggest companies.

There are different limits to this analysis. First, the authors want to stress the fact that this is a “desk” research. It means that they have used mainly secondary data, even if they have built their own database of firms (Cassell and Symon, 1994). In the second phase of the Flagship Program Ritmare, they will pass to the field research phase through the direct survey of the organizations of the sample.

Still, they developed this enquiry in English. Even if they think that the majority of companies show (at least some) website's pages in English, this is not the case for small firms or for the companies that have at the beginning a local market.

This investigation, although tries to be comprehensive, analyses mainly reports, documents and funded projects of European Union.

There are several companies that work in related and support sectors, but not directly with marine organisms. This is the case, for example, of firms that offer tools for the aquaculture sector or in the food sector use ingredients of marine origin developed by other companies. The authors tried to clear the sample of firms.

They have tried to keep track of all the changes that characterized the companies of the sample (birth, mergers, take-overs), of course this monitoring activity was not the central goal of the project.

Results and Discussions

The Geographical Distribution

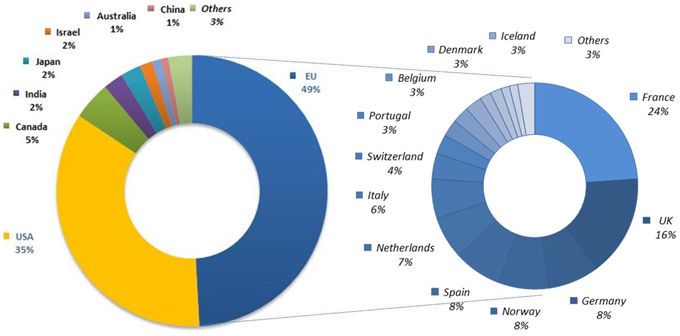

The methodology described allowed the authors to draw up a sample of 465 firms. More than 35 countries are represented (39). The countries that have more than three companies each are 22.

As it can be noticed in Figure 2, inside this sample few nations show a significant percentage on the total number of organizations. Above all, European countries and United States hold the biggest share, with Canada following slightly (with respectively 226, 162, and 21 organizations).

Figure 2. The geographical distribution of the sample (world and EU; n = 460).

Inside European Union also there is a wide distribution of firms linked to blue biotechnology, even though only two countries (France and UK) represent 40% of the total of the sector of the continent. Germany, Norway, Spain, and Netherlands show almost the same number of firms (15/18 organizations).

It is to underline the fact that the numerousness as the width of the sample are a first result of the investigation. As previously highlighted, the dimension of the industry is still to be defined.

A Fast-Changing Environment

Of 465 firms, 53 (nearly 11%) are the organizations no longer active on the markets. Of these 53, 13 have been acquired by other companies (included in the sample). There are inside the sample other 12 cases of buy-out, these organizations maintained nevertheless their independence from the purchaser. To mention some examples: ABK-Gaspesie, a spin-off from the University of Québec, has been purchased by Ocean Nutrasciences in 2010; Lallemand acquired Aquapharm Bio-discovery in 2013; still BASF went through Pronova Biopharma in 2013 and Pfizer purchased Wyeth Pharmaceuticals in 2009.

The authors found eight joint-ventures created by two or more firms. Butamax Advanced Biofuels, for example, is a company formed by British Petroleum and DuPont in 2009; HR Petroleum and Royal Dutch Shell (who will go out from the company shares in 2011) gave birth to Cellana in 2007.

It is to stress that 43 companies of the sample belong to a group of firms. Moreover, there are other forms of development on the markets as mergers. Diversa Corporation and Celunol gave life to Verenium Corporation in 2007 (now part of BASF).

As first evidences, Blue biotechnology emerges a sector marked out by a certain vitality, where companies born, end their activities, merge, are sold, form alliances, and joint-ventures. A market signed by a certain degree of instability, where changes become a normal way of living of companies. It seems that some firms are involved in the processes that is characteristic of the industry to which they belong, as the dynamic of industrial concentration that defines the pharmaceutical sector.

“With a few notable exceptions, most industrial contributions to Marine Biotechnology in Europe are generated through specialized Small and Medium-sized Enterprises (SMEs). These small companies assume most of the risks inherent in RTD in a highly unstable economic environment and are characterized by a rapid turn-over” European Science Foundation (2010).

“It is interesting to see how development has progressed. Unfortunately, I don't think a lot has happened in the bioreactor field in 10 years. There is a lot of development work to be done and many companies have gone bankrupt in the process. I think there is a lot to learn from them,” Aina Charlotte Wennberg, NIVA.

The Multi-National Corporations Trend

“Marine biotechnology is still a very small industrial sector, mainly dominated by academic institutions.(…) In particular, there is insufficient awareness within the pharmaceutical industry of the potential for novel drug discovery based on bioactive molecules and compounds derived from marine organisms,” European Science Foundation (2010).

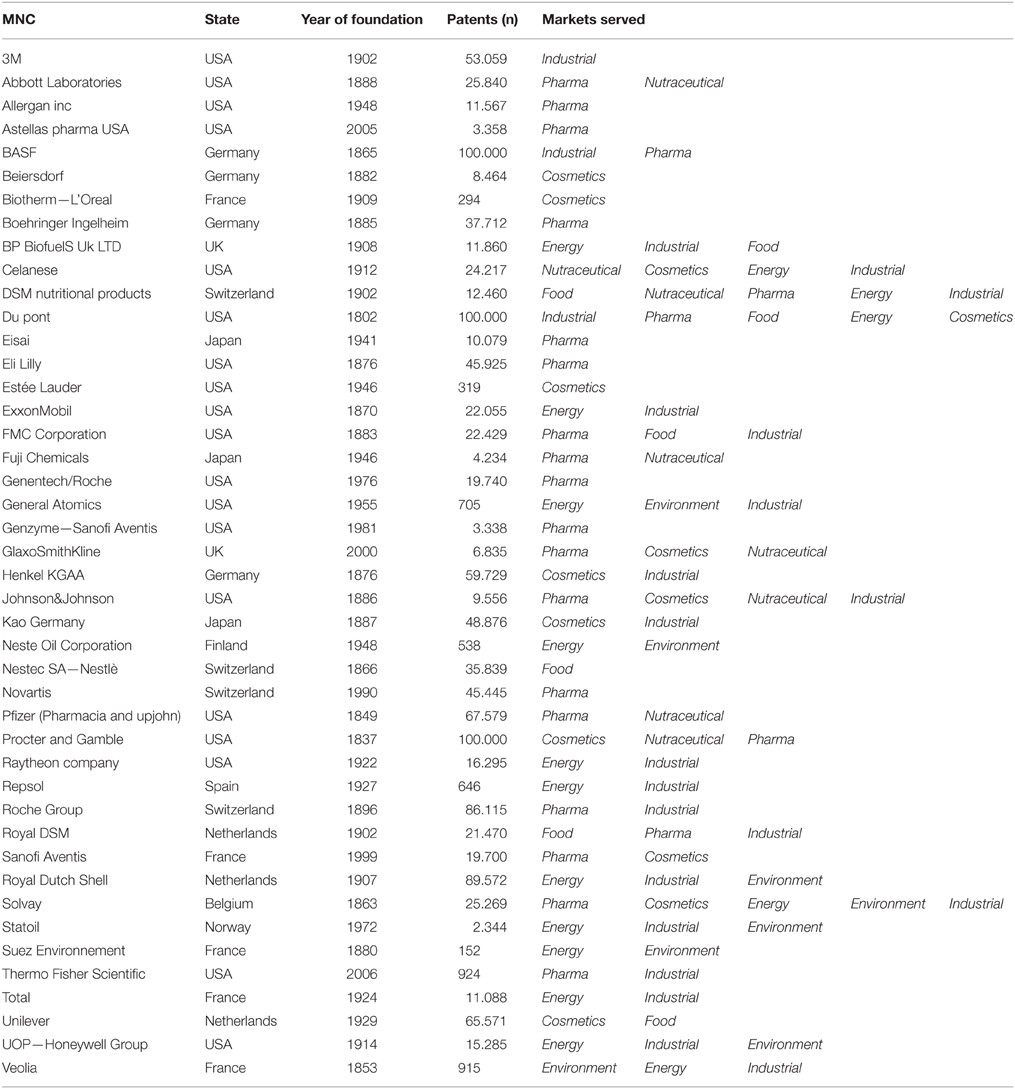

From the analysis of the sample, it emerged that the companies recognized as being global players in their respective markets are 44 (in Table 2 there is the complete list of firms). All the industries of interests of blue biotechnology are well-represented.

Table 2. The Multi-National Corporations of the sample.

In the cosmetic sector you can recognize a strong participation of firms. Besides Estée Lauder, you can find Beiersdorf, L'Oreal, GlaxoSmithKline, Johnson&Johnson, Procter and Gamble, Unilever, Sanofi Aventis, Solvay, Henkel. All the actors that you can find on the large-scale retail trade.

The pharmaceutical industry also shows his main participants engaged directly or indirectly in the blue biotechnology sector: Novartis, Pfizer, Boehringer Ingelheim, Eisai, Eli Lilly, BASF, and others. Molinski et al. (2009) underline the fact that big pharmaceutical companies declined their participation during the 1990's, letting research and development niches, then exploited by entrepreneurial scientists, mainly in collaboration with companies. The developments in analytical technology, spectroscopy, and high-throughput screening and the partial failure of combinatorial chemistry in delivering new drugs brought new interests on the field in recent years.

Royal Dutch Shell, Statoil, Total, UOP, British Petroleum are the energy giants that began projects on micro and macro algae. Experts of the industry sustain that investments necessary to the production on a large scale of marine biofuels go beyond the possibilities of Small and Medium Enterprises and that MNCs, on the contrary, have the financial resources to reach the market in a short time. ExxonMobil, for example, after a first investment of $ 100 million to develop algae-based fuel, decided in 2009 to refocus the project on a more productive species in collaboration with Synthetic Genomics (forecasting an investment of further $ 600 million). In 2013, the company conveyed that the project was renewed as a “basic science research program.”

It is to underline that different technologies live now together: Sapphire Energy is developing big cultivations in South-West of United States of America, trying to demonstrate the possibility to grow algae all year long, as a normal industrial cultivation; Algenol Biofuels is developing his own bio-refinery, using a potentiated algal species grown in plastic bag exposed to sun and carbon dioxide. After years of stability, the recent collapse of crude oil price could still re-shape competition dynamics.

“When the biotechnology revolution began, big pharmaceutical companies understood nothing about biology. They began their research and development projects and all failed. They could never invent new products, because they were not entrepreneurial. Nimble biotech firms such as Genentech showed how to do that (before it was purchased by Roche). As yesterday, companies of the bio-energetic sector will show giants companies the way to produce earnings from alternative fuels,” Ed Legere, AD, Algenol Biofuels31.

It seems that the interest of MNCs vs. blue biotechnology is growing in importance in these last years, not only in the pharmaceutical industry. MNCs need to know new technologies, to dominate them, to find new ways to reach the market with innovations. Marine compounds grab new attention and they represent a new ground of competition.

Incumbents vs. Newcomers

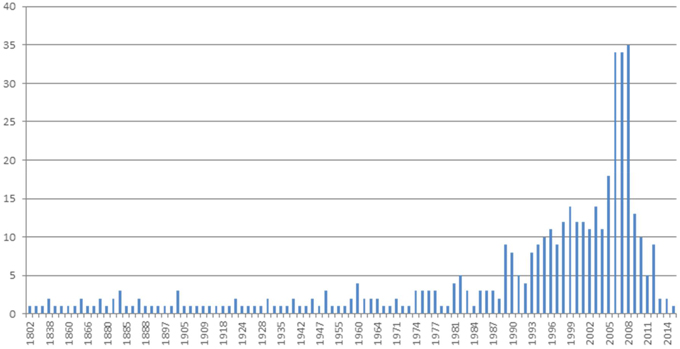

The analysis of the years of establishment of blue biotechnology firms shows a clear trend (see Figure 3). In the first place, it is evident that companies with a long history (mainly MNCs) compete with firms of new generation and start-ups.

Figure 3. The temporal distribution of the firms of the sample (n = 460).

While till the mid 1990's the number of new companies remains moderate, it grows then constantly, reaching a peak in 2006, 2007, and 2008 (with 34, 34 and 35 firms)32. It is undoubted that the trend is the consequence of the technology shifts lived in molecular biology at the beginning of 2000s. “The man hated by both worlds (public and private)”33, as he defines himself, Craig Venter, founded Synthetic Genomics in 2005, after the Sorcerer II expedition in the Sargasso Sea revealed the discovery of 1800 new species and more than 1.2 million new genes and his shotgun approach became the new standard method of decoding genomes. Evidently he was not the only one to believe in the potential of marine compounds.

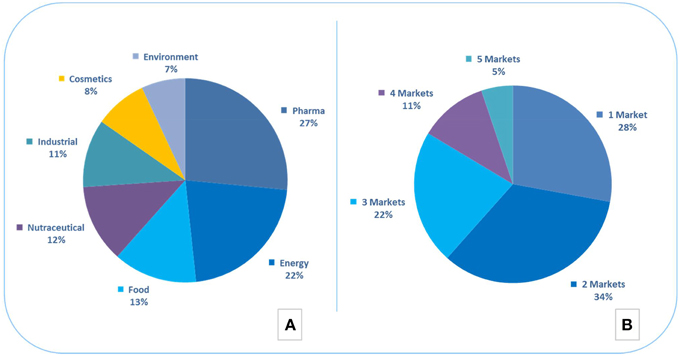

The Markets Served

Considering the main markets served by blue biotechnology firms, 27% of the sample work for the pharmaceutical sector, followed by the energy industry (22%), food (13%), nutraceutical (12%), industrial (11%), cosmetics (8%), and environment (7%) (see Figure 4A). Considering not only the first market served, but all the markets serviced by companies, the percentages change slightly. The sector that shows the biggest change is the industrial one (from 11 to 22%). There is a significant percentage of firms that work in a business-to-business environment, not reaching the final consumer.

Figure 4. The markets served (n = 445). (A) Represents the first market served by the firms (%). In (B) it is described the number of markets served by each organization.

It is interesting to analyze the number of markets served by firms. Only 28% of the sample serves, in fact, a single market. It follows that 72% of the companies investigated operate on more than one market (see Figure 4B). It is a simple evidence on which one could drive some first conclusions. The authors ask themselves if it is right for blue biotechnology then to consider one industrial sector at a time when gathering information, or this could lead to a partial reading of the dynamics of the industry.

Subsectors—The Need for an Interdisciplinary Approach

“Many companies have chosen to go along the functional product route as it offers lower risk and a quicker potential return on investment than the high-risk high-reward pharmaceutical market” European Science Foundation, 2010.

Vigani et al. (2015) emphasize the importance of the spill-over effects between the algae biofuel sector and the food/feed industry. While some firms chose to operate on single markets as dietary or cosmetics supplements, others preferred to be present on several market niches, benefiting of the productive synergies that shape the industrial sectors.

In the sample, on 143 companies active in energy industry, only 16 concentrate on a single market, while nearly 89% operate in other sectors. In micro and macro algae sector, well-invested companies were born with the idea to focus on biofuel production, but in the run they decided to turn to nutraceuticals and cosmeceuticals (and others). Heliae, Aurora, Cellana, and the same Synthetic Genomics (with Genovia Bio) produce algae-based bio-products for the other industries. Even though some firms declared they were ready to reach the market in 2015 (Algenol Biofuel is one example), scaling-up production represents still a big challenge. Cultivation, harvesting and downstream processing have revealed their difficulties in the way from the laboratory phase through the large scale production.

Reaching the market with new products or services could have different implications for the firms: raising visibility, earning new funds to invest (securing survival), looking for new collaborations, finding new applications, understanding market needs. It changed the modus operandi of companies, taking in the long run a life-cycle development approach.

“Heliae is currently developing high value nutraceutical ingredients and specialty products for agriculture and aquaculture. Our long term vision includes the application of our technology for environmental remediation; providing sustainable low cost sources of nutrition for a growing world population; and the application of both conventional biotechnology and responsible genetic engineering to unlock the potential of algae”34.

Not only in the energy industry companies operate on more than one market. Food/feed sector and nutraceuticals show the same levels of diversification of activity (consequently).

In the cosmetic industry too, only about 15% of firms (17 on 116) operates or make products or services for the beauty care sector. The pharmaceutical industry show a much lesser percentage with 51 companies on 186 working only for the firms that belong to this sector (nearly 28%). It is clear, anyway, the interdependence with other markets such as cosmetics and nutraceuticals. In Figure 5, the authors have tried to give a graphical representation of the areas of overlap among the markets served by the firms of the sample.

Figure 5. The intersections between the markets served.

“BioLume's business strategy has two broad components; (1) developing and commercializing the medical imaging applications covered by its patents, (2) developing and commercializing the food, beverage, personal care, and cosmetic applications covered by its patents.

These strategies are complementary as the data needed for development of either will benefit both components. However, from a funding standpoint, the development process is faster and less expensive for ingredients added to food and other consumer products than medical imaging agents yet the market opportunity is likely larger, so BioLume will pursue this first and use the cash from ingredient sales to develop the medical imaging products.”35

From the investigation of the activities performed by companies, several different uses of marine compounds and marine scientific know-how came out, witnessing the wide spectrum of possible exploitations. Biolume, as described above in the business strategy of the firm, develops the biochemical mechanisms used by living organisms to produce light, known as bioluminescence. The company wish to slip from the biomedical research to the production of ingredients for the food sector. The aim of the organization is to produce food (such as lollipops) that glows thanks to the contact with a liquid (in this case the saliva).

Still, Amadeite, a French company, develops active ingredients from algae bio-resources to produce nutraceuticals for the animal health sector (poultry, cattle, and pigs)36. The biochemical sector emerged as one of the most underrated and much promising. Lubricants, coatings, cleaners, enzymes, natural foams, marine biocides, biomaterials and bioplastics are some examples of the possibilities just reached in this field.

Furthermore, it is to highlight the impressive number of companies that offer services to other firms. It deals mainly with consulting activities on:

- access to marine organisms' libraries;

- bioprospecting;

- bioprocessing;

- metabolomics and statistical analysis (NMR);

- platform and enabling technologies;

- laboratory services;

- harvesting systems and sustainable production;

- photobioreactors;

- equipment for biofuel production;

- circular and sustainable aquaculture;

- specialty ingredients;

- mitigation strategies (or studies);

- business and technical marketing;

- risk assessment;

- IPRs.

The big width of activity that marine biotechnology shows, open the way for different considerations. First, there is a need to participate to interdisciplinary projects, as it is also stressed in the report of European Science Foundation (2010).

Still, it is important to highlight that researchers could contribute not only to the development of research for the pharmaceutical sector, but they could explore a broad set of alternatives.

Significant advances in physics, mathematics, or chemistry often need decades before optimization, improved instrumentation, and increased awareness, allow the use of these new techniques in biotechnology. It would therefore be interesting to ask our colleagues in those disciplines what the key break-troughs have been in the last few years, so that we might deliberately accelerate their uptake in biotechnology of the sea (Burgess, 2012).

The Value Chains

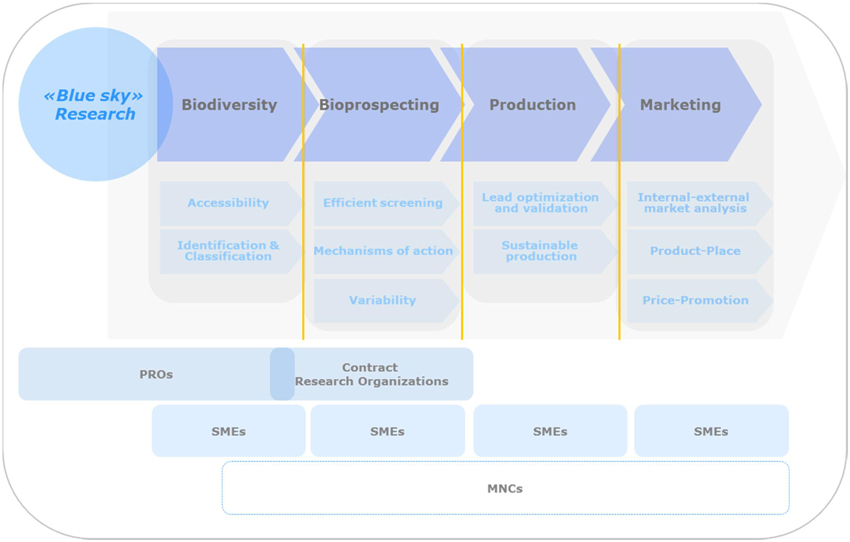

The analysis of the activities of the firms revealed that companies focused in specific phases of production, coexist with organizations marked by a strong degree of differentiation. Firms tend to take their position along the value chain (Porter, 1985) of blue biotechnology: some companies are specialized in the discovery or in the science-based phases, while others in the development activities, upscaling, and in the industrial part.

The authors of the Study in support of Impact Assessment work on Blue Biotechnology (2014) underline the importance of the role of small and medium enterprises as they bridge the gap between public research and commercialization of products and services, mainly realized by multinational companies37. SMEs are described as often single-focus marine bioactive companies, placed at the initial product development stage of the value chain. SMEs activity in fact would stop at the industrial adaptation stage of the value chain. The authors of this investigation observed a broader universe with Small and Medium Enterprises focusing on all the stages of the value chain, especially in consulting activities.

In Figure 6 it is described the value chain for blue biotechnology companies as it results from the investigation realized. Just the first part of the graph, where “blue sky research” meets the commercial phase is worth to mention. A strong international debate is, in fact, ongoing on what are the activities that public research centers have to develop and what are in the “private” domain. It is mainly a science politics' choice. In these recent years, many countries (or regions) have chosen to offer scientific commercial services, through the privatization of public research institutes. Contract Research Organizations, for example, could offer their activities, raising funds for other researches (and researchers), benefiting of a more flexible management (that could advantage directly the companies involved).

Figure 6. The value chain.

Leary et al. (2009) underline the fact that there is no evidence that any company had mounted its own dive to collect samples for the purposes of research and development in relation to marine biotechnology. It is an interesting statement. On one side, evidently the collection of organisms has been in the past supplied by research institutions. A consequence is that all the products/services now on the markets are the result of the collaboration of companies with scientific organizations. On the other side, from the investigation of the activity of companies (some cases are described also in Table 3), it emerges a number of private organizations that offer (as their core activities) the access to libraries, collection of marine organisms or cultured species.

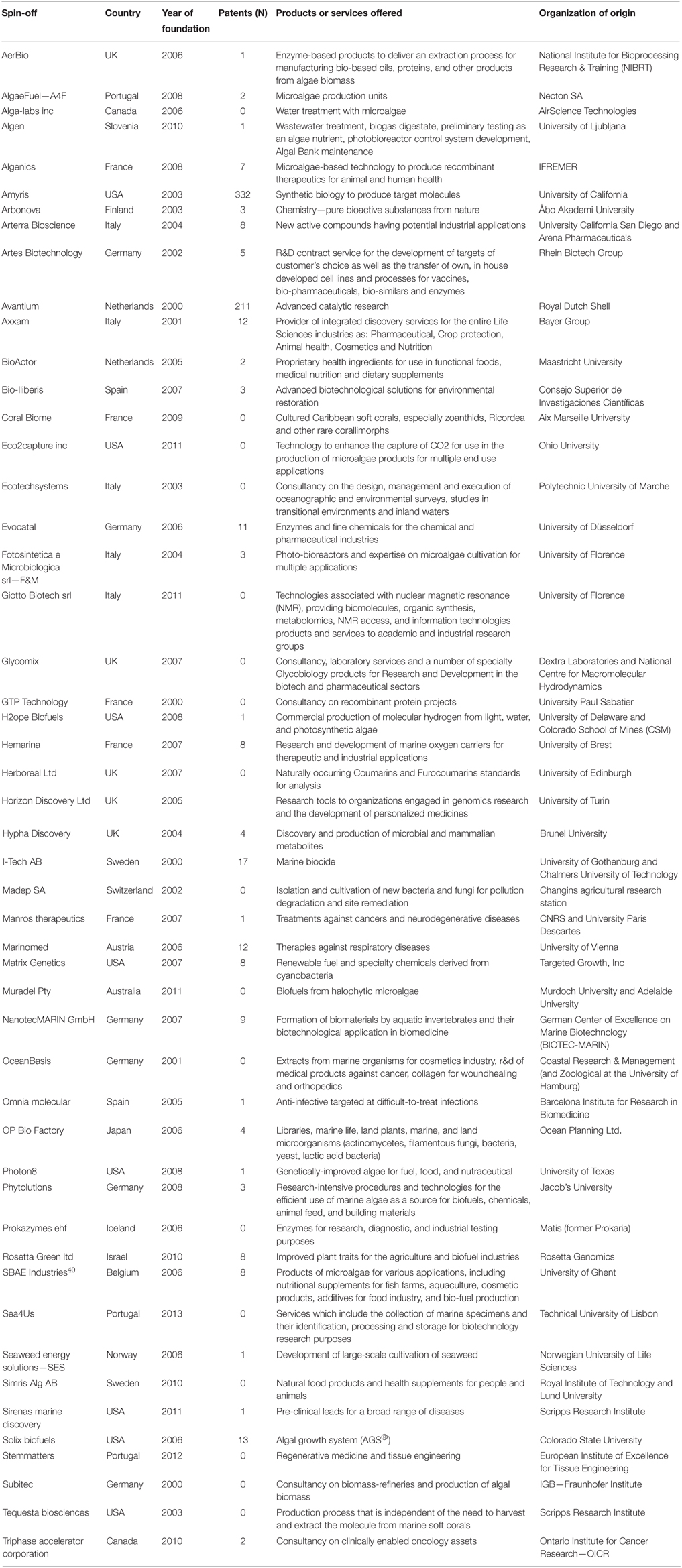

Table 3. The spin-offs of the sample (from 2000 to today).

Analyzing the classification of companies made by Ernst and Young in their report on red biotechnology, the several similarities they share with the world of marine substances could be noticed. The firms are divided in: pipeline centric, technology centric, and know-how centric. In the pipeline centric organizations, an example of products are biotech therapeutics, the time of development are long and costly, but future source of sales are high; the management of Intellectual Property Rights (IPRs) is kept inside the firm from basic research to commercialization and the licensing of IPRs happen normally after the first stages of research or after the preclinical studies. Technology centric organizations exploit their well-established technology to develop a wide range of products or services or to speed up basic research and clinic development phases; they use to manage IPRs of the technology from basic research to commercialization, licensing the products deriving from the technology. Know-how centric hold and offer research, development, regulation, production, commercialization competences. Drug discovery and CROs services are some examples; they usually work in co-development projects, form alliances to produce and commercialize products and in-license products or technologies38.

In the Study in support of Impact Assessment work on Blue Biotechnology (2014) the authors highlight that the blue biotechnology sector would not encompass the whole value chain. In fact when the processes or stages become part of a wider industry, they are separated from the marine component and began to make part of another value chain39.

“the market does not care where the product comes from. For the pharma and industrial biotech sector the source of product innovation remains unimportant. They both look for novel solutions to deal with the problems they address. Talking to many people in these industries, they consider marine biotech as difficult and unproven.”41

If this statement is understandable for the pharmaceutical and industrial sectors, this is not the case for nutraceuticals and for cosmetics. Several firms have built their communication strategies exactly on the origin of the compounds used in their products. If this could be a valuable choice in the long run, it's another question in point. The brand “Biotherm” created is campaign “water lovers” to raise awareness on the importance of biodiversity of the seas42. If one aim of the firm is the respect of nature, the other one is to highlight the importance of new discoveries and of the innovation capacity of the organization. The credibility of the company is, moreover, enhanced by the important collaborations the firm has built with the academic world (Stanford University and the Roscoff Marine Biological Station).

Several firms, also in the business-to-business environment, chose to differentiate their company brand using words such as “algae,” “ocean,” “mar.” This could give an idea of the originality and innovativeness of the organizations, increasing the attractiveness to investors.

The Spin-Off Dynamic

Science-based industries ground the construction and maintenance of their competitive advantage on research (both basic and applied). Aerospace, electronics, robotics, new material, are some example. They don't represent an homogeneous group: Research &Development (R&D) activities may vary from one sector to another, very old companies in mature industries cohabit with younger firms in new fields of competition (as for biotechnology and software; Niosi, 2000). Gomory (1987) considers biotechnologies as “stair” technologies, in the sense that a new idea becomes dominant and the products take shape on this idea or technology. Those who understand the meaning of the technology are, in most cases, scientists. They play, consequently, a pivotal role in the introduction of new ideas and technologies, making a strong connection between basic and applied research. The commercial orientation of public laboratories is an essential part of this game. Where the cultural distance from “the market” is perceived as wide, there will be a moderate flow of knowledge between the public and private domains.

Spin-offs are organizations where the products or services offered to the market are the result of scientific technologies or know-how developed inside the academic environment. It is not relevant if this person is a professor, a researcher, or a PhD student or if he/she leaves the organization of origin or he/she continues to carry his research out.

Spin-offs represent the virtual bridge between public research institutions and private organizations. They are seen as not damaging the principal role carried out by public research centers, offering an alternative to commercialization of knowledge, creating economic benefits at a local, regional, and national level (Rappert et al., 1999).

The authors found 69 spin-offs inside the sample, representing 14% of total firms. You can recognize not only academic spin-offs, but also industrial ones. There is than another typology of firm that is the result of the process of privatization on public research centers as in the case of IGV Biotech and VESO, the Norwegian Contract Research Organization.

As previously underlined, the authors considered only the companies that described themselves as spin-offs in their websites. they believe that the phenomenon in marine biotechnology is really wider. Furthermore, they found an important number of scientists being part of the board of directors of the companies. In Table 3, there is the list of spin-off firms formed from 2000 to today. In this case, they chose to describe the products or services offered as they could represent a model of action or of competition to which to refer.

The Collaboration Trend

“Collaboration with large companies, who may also be your target customers or licensees, can fulfill a number of requirements: validate your technology, provide a potential route to market, provide early collaboration fees/milestone revenue, provide commercialization expertise you lack, and can be an ‘image enhancer.”43

Chiaroni et al. (2008) analyze the role of collaboration in the bio-pharmaceutical industry, assessing the extent, and variety of organizational modes. They studied how collaboration changes in the different stages of the value chain and the different typologies of partners involved in each phase. Due to biotechnology characteristics (risk management, articulation of the innovation process, IPRs management), the industry is the sector where Open Innovation takes place (Chesbrough, 2003).

Martins et al. (2014) argue that industry-academia partnerships benefit both the participants in a win-win collaboration system. Academia get closer to what is defined “the market issue,” having more funds to manage and learning to address very important questions from the early stages of the development programs, while industry gets higher chances to bring new natural products to the final market and clients.

Phil Baran, professor of Chemistry of Scripps Research Institute and founder of Sirenas Marine Discovery, describes the experience of consulting to large firms as necessary, essential, and critic. Consulting to big pharmaceuticals helped the scientist to realize problems and difficulties faced by biotechnology firms day by day, but also to find contacts for licensing activities, reaching potential clients for the research activities. Collaboration with research directors and managers, at the same time, has been of great importance to understand how to sell a product on the market and on the way to present it to buyers44.

“Technologies can come into being only if they are commercially viable. They are often the end result obtained jointly by academia and industry. Quite often, neither of these players can fully develop every one of the numerous steps involved in achieving success in technology development. In their research relating to organisms, their applications and the processes, academia and industries participate at the different levels of established, emerging, or exploratory technologies,” (Raghukumar, 2011).

Conclusion

In the case of biotechnology in general and marine biotechnology in particular, theorists, and practioneers agree on the necessity to build and develop relationships between the academic and private world. As underlined by the professor of Chemistry of Scripps Research Institute, collaboration helped his group of research to learn dynamics that they didn't know. You can perceive in his experience a process of development of knowledge (on companies, products, markets, IPRs) that leaves from consulting services, through collaboration and, then, ends with an entrepreneurial activity.

Of course, the fact that collaboration brings mutual advantages to all the parties, it doesn't mean that people are keen to be involved in it.

“If academics think their role is only to teach and publish papers, they will resist any attempt to create spin-off firms, to patent technology, or license it out” (Niosi, 2011).

As mentioned earlier not all the research institutions share the same level of commercial orientation. Niosi (2011) argues that in most OECD countries institutions have not been designed to cope with complex and fast-changing science-based industries. United States still enjoys his first-mover advantage, in spite of many efforts deployed by several countries in continental Europe.

“The important thing for me is that I do my research on something that's of primary interest to industry. If that leads to an innovation of some kind it will be interesting and exciting, but it's not necessary to me. We have industrial partners and partnerships and are open to taking advantage of the innovative ideas that come up,” Eva Albers, Professor at Chalmers.

Blue biotechnology is living a phase of big developments, while institutions on marine research are among the world most ancient. From the “blue sky” research domain, public institutes come to the applied one. It would be relevant to investigate how scientific community perception of the industry evolved in these last years and how public research centers are managing (if) this cultural change.

The authors have to underline the fact that in the last 30 years economic and institutional research on biotechnology industries and on the mechanisms of knowledge transfer between companies and public research centers has become really wide and important. One of the tool to manage the new complexity that characterize marine biotechnology could be to look to the experiences lived by the other sectors, learning few lessons from them.

As they underlined earlier, this paper is based on a “desk” investigation. Further, detailed research is necessary on the firms that populate marine industry, on the genesis of their birth, on their collaboration mechanisms, on the relationships they build and nurture with academy, on the importance of knowledge transfer and the most appropriated tools.

Author Contributions

GG and MC both participated in the conception and design of the manuscript “Firms plunge into the sea. Marine Biotechnology Industry, a first investigation.” Both the authors contributed to the drafting of the article, revisited it critically, and gave the final approval of the version to be submitted.

Conflict of Interest Statement

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Acknowledgments

The authors wish to thank the Flagship Program “Ritmare” for the financial support. The work is in fact an output of the activity on technology transfer of the project (SP6_WP4_AZ1). They would also like to thank Dr. Graziano Fiorito and Dr. Maurizio Ribera d'Alcalà for precious suggestions and comments.

Footnotes

1. ^EU, DG Internal Policies, “Ocean Research in Horizon 2020: The Blue Growth Potential,” 2015. http://www.europarl.europa.eu/RegData/etudes/STUD/2015/518775/IPOL_STU(2015)518775_EN.pdf.

2. ^http://www.glycomarblog.com/.

3. ^“Beyond borders. Unlocking value,” Biotechnology Industry Report 2014, Ernst and Young.

4. ^Biotechnology Industry Report 2013, Beyond Borders. Matters of evidence, Ernst and Young.

5. ^Italian Biotechnology Report 2012, BioInItaly, Ernst and Young.

6. ^http://www2.deloitte.com/global/en/pages/life-sciences-and-healthcare/articles/2015-global-life-sciences-outlook.html.

7. ^van Beuzekom and Arundel (2009), OECD Biotechnology Statistics.

8. ^Not only, then, what in Biotechnology Industry Report (2014) by Ernst and Young is defined as “pure biotech,” but also “multi-core” and “GPET—Genomics, Proteomics, Enabling Technologies.”

9. ^http://www.bccresearch.com/market-research/pharmaceuticals/marine-derived-pharma-markets-phm101a.html.

10. ^Global Industry Analysts Inc. (2013).Marine Biotechnology, Global Strategic Business Report.

11. ^http://www.slideshare.net/GlobalIndustryAnalystsInc/marine-biotechnology-a-global-strategic-business-report.

12. ^OECD, “Marine Biotechnology: Enabling Solutions for Ocean Productivity and Sustainability,” 2013.

13. ^“Study in support of Impact Assessment work on Blue Biotechnology,” Revised Final Report FWC MARE/2012/06—SC C1/2013/03, 2014.

14. ^Ibidem.

15. ^http://www.ritmare.it/en/.

16. ^La bolla delle alghe, 9 Aprile 2009, Nova, Sole24Ore.

17. ^Defined by the sea: Nova Scotia's Ocean Technology Sector present and future (2010). JobsHere.

18. ^Thinking Blue: Addressing Today's Challenges with Marine Biotechnology (2012). Blue Bio Report.

19. ^Strategy for the marine biotechnology cluster in Tromso 2012- 2015, Biotech North.

20. ^Seeing Purpose and Profit in Algae, New York Times.

21. ^Biomass Alternative Energy. Available online at: www.prezi.com.

22. ^Keywords were: marine biotechnology, marine bioactive compounds, marine biomaterial (firm, company).

23. ^What Happened to Biofuels (2013). The Economist, Technology Quarterly n. 3, 7, September.

24. ^http://marinepharmacology.midwestern.edu/clinPipeline.htm.

25. ^NAABB, National Alliance for Advanced Biofuels and Bio-products (2014). Synopsis.

26. ^Keywords were: marine biotechnology, marine bioactive compounds, marine biomaterial (firm, company). The authors checked all the results of the first fifteen pages.

27. ^www.environmental-expert.com, www.biomarine-resources.com, Algae fuel producers on en.wikipedia.org, www.cleantick.com/companies, www.ethanolproducer.com, biopharmguy.com, biomarine-resources.blogspot.it, www.oilgae.com, www.seao2.com/algaebiofuels, www.algaeu.com.

28. ^Main generic and specialized magazines consulted are: www.oilalgae.com, www.biofuelsdigest.com, www.investing.businessweek.com, www.economist.com, www.scientificamerican.com, www.strategyr.com.

29. ^To have more information about the function of the search engine, visit www.epo.org/searching/free/espacenet.html.

30. ^Patents' portfolios could be, in some cases, be undervalued. For Asian companies this could happen because of the non-perfect dialogue between the patent systems. In the case of start-ups and spin-offs, this could happen because the patents could be registered with the name of the inventor, not by the firm itself (so you lose the information).

31. ^“Going Commercial. Algenol boosts yields, cuts costs for biofuel production,” Jerry Perkins, Biofuels Journal, 2° trimester 2014.

32. ^Last years of the inquiry would probably underestimate the number of new firms, not reaching them still the visibility to be involved in this sample.

33. ^“Craig Venter's Epic Voyage to Redefine the Origin of the Species”, Wired, August 2004.

34. ^“Our focus”, http://heliae.com/company/.

36. ^http://www.amadeite.com/English/Amadeite/marine-biotechnology-firm.html.

37. ^“Study in support of Impact Assessment work on Blue Biotechnology,” Revised Final Report FWC MARE/2012/06—SC C1/2013/03, 2014.

38. ^“BioInItaly,” Italian Biotechnology Industry Report 2014, Ernst and Young.

39. ^“Study in support of Impact Assessment work on Blue Biotechnology,” Revised Final Report FWC MARE/2012/06—SC C1/2013/03, 2014.

40. SBAE Industries is no longer active. In 2011 they went through reorganization, but authors didn't found any up-to-date information.

41. ^http://www.glycomarblog.com/.

42. ^http://www.biotherm.it/about-biotherm/index.aspx#!/water-lovers.

43. ^http://www.glycomarblog.com/.

44. ^“Evolution from Academia to Industry—Interview with Professor Phil Baran,” Oxbridge Biotech Roundtable Review, 26th February 2013.

References

Ali Ahmed, A. B., and Mat Taha, R. (2011). Marine phytochemical compounds and their cosmetical applications. Acad. Edu. 51–61. Available online at: http://www.academia.edu/4018101/Marine_phytochemical_compounds_and_their_Cosmeceuticals_applications

Arrieta, J. M., Arnaud-Haond, S., and Duarte, C. M. (2010). What lies underneath: conserving the oceans' genetic resources. Proc. Natl. Acad. Sci. U.S.A. 107, 18318–18324. doi: 10.1073/pnas.0911897107

Balasubramanian, P. (2012). North German Maritime Industry Analysis Report. Discovering Opportunities for Knowledge & Technology Transfer. Kuehne Logistics University.

Bijlwan, A., Sharma, M. K., Thakur, T., and Kush, L. (2013). Potential of marine biomolecules as the promising life-style drugs. Int. J. Innovat. Res. Dev. 2, 9–13. Available online at: www.ijird.com/index.php/ijird/article/viewFile/37251/29769

Brar, B., and McLarney, C. (2001). Poised for Success? An Analysis of the Halifax Biotechnology Cluster. Halifax: the Centre for International Trade and Transportation. CITT discussion paper no. 187.

Breznitz, S. M., and Anderson, W. P. (2005). Boston metropolitan area biotechnology cluster. Canad. J. Reg. Sci. XXVIII, 249–264. Available online at: https://www.researchgate.net/publication/242176053_Boston_Metropolitan_Area_Biotechnology_Cluster

Burgess, J. (2012). New and emerging analytical techniques for marine biotechnology. Curr. Opin. Biotechnol. 23, 29–33. doi: 10.1016/j.copbio.2011.12.007

Cassell, C., and Symon, G. (1994). Qualitative Methods in Organizational Research: A Practical Guide. London: Sage.

Chiaroni, D., Chiesa, V., De Massis, A., and Frattini, F. (2008). The Knowledge bridging role of Technical and Scientific Services in knowledge-intensive industries. Int. J. Technol. Manag. 41, 249–272. doi: 10.1504/IJTM.2008.016783

Cooke, P., Porter, J., Cruz, A. R., and Pinto, H. (2011). Maritime Clusters – Institutions and Innovation Actors in the Atlantic Area. University of Algarve.

DG Maritime Affairs Fisheries (2014). Study in Support of Impact Assessment Work on Blue Biotechnology. Final Report FWC MARE.

Dhabarde, D. M., Potnis, V. V., Kamble, M. A., Ingole, A. R., and Sant, A. P. (2013). Marine cosmeceuticals. Univ. J. Pharm. 2, 20–22.

Doloreux, D., and Melançon, Y. (2008). On the dynamics of innovation in Quebec's coastal maritime industry. Technovation 28, 231–243. doi: 10.1016/j.technovation.2007.10.006

Doloreux, D., and Melançon, Y. (2009). Innovation-support organizations in the marine science and technology industry: the case of Quebec's coastal region in Canada. Mar. Pol. 33, 90–100. doi: 10.1016/j.marpol.2008.04.005

Ellingsen, M., and Tromso, N. (2010). “Innovation in Marine Biotechnology: Clustering or Trust and Entrepreneurship? An explorative study of an issuant industry in the High North,” in Paper Presented at 5th International Seminar on Regional Innovation Policies, 14–15 October (Grimstad).

European Science Foundation (ESF) (2001). Marine Biotechnology: A European Strategy for Marine Biotechnology. Marine Board, Position Paper n. 4.

European Science Foundation (ESF) (2010). Marine Biotechnology: A New Vision and Strategy for Europe. Marine Board, Position Paper n. 15.

Faberger, J., Mowery, D. C., and Verspagen, B. (2009). Innovation, Path Dependency and Policy. Oxford: Oxford University Press.

Frahm, T. (2012). A Regional Development Strategy for Marine Biotechnology in Schleswig-Holstein. Submarine, Baltic Sea Region.

Gendy, T. S., and El-Temtamy, S. A. (2013). Commercialization potential aspects of microalgae for biofuel production: an overview. Egypt. J. Petrol. 22, 43–51. doi: 10.1016/j.ejpe.2012.07.001

Hu, G.-P., Yuan, J., Sun, L., She, Z.-G., Wu, J.-H., Lan, X.-J., et al. (2011). Statistical research on marine natural products based on data obtained between 1985 and 2008. Mar. Drugs 9, 514–525. doi: 10.3390/md9040514

Iceland Ocean Cluster (2012). The importance of the Ocean Cluster for the Icelandic Economy. Islandsbanki.

InterMareC – Interregional Maritime Cluster (2007). The Benefit of Interregional Cooperation, Booklet INTERREG IIIC.

La Barre, S., and Kornprobst, J. (2014). Outstanding Marine Molecules. Weinheim: Wiley-Blackwell. doi: 10.1002/9783527681501

Leary, D., Vierros, M., Hamon, G., Arico, S., and Monagle, C. (2009). Marine genetic resource: a review of scientific and commercial interest. Mar. Pol. 33, 183–194. doi: 10.1016/j.marpol.2008.05.010

Linder, T. (2008). Biofuels from Algae and Other Renewable. Available online at: www.genstrom.net.

Løvdal, N., and Neumann, F. (2011). Internationalization as a strategy to overcome industry barriers—An assessment6 of the marine energy industry. Energy Pol. 39, 1093–1100. doi: 10.1016/j.enpol.2010.11.028

Lundquist, T. J., Woertz, I. C., Quinn, N. W. T., and Benemann, J. R. (2010). A Realistic Technology and Engineering Assessment of Algae Biofuel Production. Energy Biosciences Institute.

Maritime Clusters in Västra Götaland (2013). Region Västra Götaland. Gothenburg: University of Gothenburg, Chalmers.

Marris, E. (2006). Marine natural products: drugs from the deep. Nature 443, 904–905. doi: 10.1038/443904a

Martins, A., Vieira, H., Gaspar, H., and Santos, S. (2014). Marketed marine natural products in the pharmaceutical and cosmeceutical industries: tips for success. Mar. Drugs 12, 1066–1101. doi: 10.3390/md12021066

Mascarelli, A. L. (2009). Algae: fuel of the future. Environ. Sci. Technol. 43, 7160–7161. doi: 10.1021/es902509d

Mayakrishnan, V., Kannappan, P., Abdullah, N., and Ahmed, A. B. A. (2013). Cardioprotective activity of polysaccharides derived from marine algae: an overview. Trends Food Sci. Technol. 30, 98–104. doi: 10.1016/j.tifs.2013.01.007

Molinski, T. F., Dalisay, D. S., Lievens, S. L., and Saludes, J. P. (2009). Drug development from marine natural products. Nat. Rev. Drug Discov. 8, 69–85. doi: 10.1038/nrd2487

Murray, M. P., Moane, S., Collins, C., Beletskayat, T., Thomas, O. P., Duarte, A. W., et al. (2013). Sustainable production of biologically active molecules of marine based origin. New Biotechnol. 30, 839–850. doi: 10.1016/j.nbt.2013.03.006

National Research Council (2002). Marine Biotechnology in the XXI Century: Problems, Promise and Products. Ocean Studies Board, National Academy Press.

NC Biotechnology Center (2013). Biorenewable and Biotechnology Asset Inventory in North Carolina's Southeast Region.

Niosi, J. (2000). Science based industries. A new schumpeterian typology. Technol. Soc. 22, 429–444. doi: 10.1016/S0160-791X(00)00028-2

Niosi, J. (2011). Complexity and path dependence in biotechnology innovation systems. Indust. Corp. Change 20, 1795–1826. doi: 10.1093/icc/dtr065

Norgenta DSN Analysen & Strategien (2012). Marine Biotechnology Schleswig-Holstein. A Regional Development Strategy.

Norwegian Centre for International Cooperation in Higher Education (SIU). (2008). Marine Studies in Norway.

Pietrabissa, R. (2005). “Da Brunelleschi al Post-it: il brevetto e il suo uso nel progresso basato sulle invenzioni,” in Bonaccorsi Andrea, Granelli Andrea, Pietrabissa Riccardo (2005). “Brevettare? La proprietà delle idee nel Terzo Millennio” (Milano: Edizioni Medusa).

Porter, M. E. (1985). Competitive Advantage: Creating and Sustaining Superior Performance. New York, NY: Free Press.

Porter, M. E. (1998). “Clusters and competition: new agendas for companies, governments, and institutions,” Harvard Business School Working Paper. No. 98–080.

Qin, S., Lin, H., and Jiang, P. (2012). Advances in genetic engineering of marine algae. Biotechnol. Advan. 30, 1602–1613. doi: 10.1016/j.biotechadv.2012.05.004

Raghukumar, S. (2011). Marine biotechnology: an approach based on components, levels and players. Ind. J. Geo Mar. Sci. 40, 609–619. Available online at: https://www.researchgate.net/publication/279555791_Marine_biotechnology_An_approach_based_on_components_levels_and_players

Rangel, M., and Falkenberg, M. (2015). An overview of the marine natural products in clinical trials and on the market. J. Coast. Life Med. 3, 421–428. doi: 10.12980/JCLM.3.2015JCLM-2015-0018

Rappert, B., Webster, A., and Charles, D. (1999). Making sense of diversity and reluctance: academic-industrial relations and intellectual property. Res. Pol. 28, 873–890. doi: 10.1016/S0048-7333(99)00028-1

Thorndyke, M., Kloareg, B., Canário, A. V. M., Ribera d'Alcalà, M., Johnston, I. A., Kooistra, W. H. C. F., et al. (2013). EMBRC Business Plan. Available online at: www.embrc.eu/sites/default/files/EMBRC Business Plan.pdf

Trincone, A. (2014). Increasing knowledge: the grand challenge in marine biotechnology. Front. Mar. Sci. 1, 1–3. doi: 10.3389/fmars.2014.00002

van Beuzekom, B., and Arundel, A. (2009). OECD Biotechnology Statistics. OECD Report, Paris. Available online at: www.oecd.org/science/inno/42833898.pdf

Vigani, M., Parisi, C., Rodríguez-Cerezo, E., Barbosa, M. J., Sijtsma, L., Ploeg, M., et al. (2015). Food and feed products from micro-algae: market opportunities and challenges for the EU. Trends Food Sci. Technol. 42, 81–92. doi: 10.1016/j.tifs.2014.12.004

Keywords: marine biotechnology, industry, firm, multinational corporation, market served, spin-off, value chain

Citation: Greco GR and Cinquegrani M (2016) Firms Plunge into the Sea. Marine Biotechnology Industry, a First Investigation. Front. Mar. Sci. 2:124. doi: 10.3389/fmars.2015.00124

Received: 11 November 2015; Accepted: 22 December 2015;

Published: 26 January 2016.

Edited by:

Antonio Trincone, Istituto di Chimica Biomolecolare, Consiglio Nazionale delle Ricerche, ItalyReviewed by:

Avinash Mishra, Council of Scientific and Industrial Research-Central Salt and Marine Chemicals Research Institute, IndiaWeiqi Fu, New York University Abu Dhabi/University of Iceland, United Arab Emirates

Copyright © 2016 Greco and Cinquegrani. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) or licensor are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Gaia R. Greco, Z2FpYS5ncmVjb0Bzem4uaXQ=