Mingjie Yang1

Mingjie Yang1 Yaolong Li

Yaolong Li Fanglei Zhong

Fanglei Zhong- 1Information and Communication Company of State Grid Gansu Electric Power Company, Lanzhou, China

- 2School of Economics, Minzu University of China, Beijing, China

The mechanism for realizing the value of ecological products is a critical issue bridging the global Sustainable Development Goals (SDGs) and China's ecological civilization construction. Addressing a key methodological gap between the international TEEB framework (based on natural capital accounting and marginal utility pricing) and China's Gross Ecosystem Product (GEP) accounting, this study employs concept movement theory to deconstruct the dynamic evolutionary path of ecological products from “natural gifts” to “factors of production.” The results reveal an interactive five-stage mechanism of “stipulation-unfolding-transformation-perfection-realization.” Through policy text and case analysis, we find that the relativity of concept movement is reflected in the dynamic adjustment of policy tools, while technological innovation reduces transaction costs by reconstructing property rights boundaries. This study proposes that China's practice is centered on “institutionally embedded innovation,” which localizes the natural capital paradigm through the labor theory of value. This forms a “global consensus-local innovation” dual-drive framework, providing a practical pathway for developing countries to overcome the challenges of measurement, transaction, and monetization.

1 Introduction

Realizing the value of ecological products is a core issue linking the global Sustainable Development Goals (SDGs) with China's ecological civilization construction. Since the concept of “ecological products” was first defined in the National Main Functional Area Plan in 2010, its connotation has undergone a paradigm shift from a “collection of natural elements” to a “product of nature-labor synergy” (Kumar, 2010). This evolution is essentially a typical manifestation of concept movement: the internationally accepted The Economics of Ecosystems and Biodiversity (TEEB) framework has constructed a common language for global ecological governance through natural capital accounting, while China's unique Gross Ecosystem Product (GEP) accounting has formed a more institutionally embedded localized path through the ecological transformation of the labor theory of value (Ouyang et al., 2013). However, current practices face a dual contradiction: first, the institutional friction between the global standardization demands of TEEB (such as the EU's Carbon Border Adjustment Mechanism, CBAM) and China's localized innovation (such as GEP accounting), and second, the governance dilemma of ecological resources being “difficulty in measurement, transaction, and monetization” (Wang, 2024). How to resolve these contradictions through the dynamic evolution mechanism of concept movement has become a key theoretical and practical proposition.

2 Literature review and methodology

2.1 Literature review

Integrating the value of nature into socio-economic decision-making constitutes a core challenge in global sustainable development, Traditional national accounting systems, particularly GDP, have been widely criticized for ignoring the depletion and degradation of natural capital, spurring a theoretical and practical movement to “capitalize” and “value” nature (Costanza et al., 1997). This movement is driven by two major processes: first, ecosystem service (ES) valuation research advanced by the TEEB framework (Spash and Aslaksen, 2015), the Millennium Ecosystem Assessment (MA) (Tinch et al., 2021), and the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (Christie et al., 2021), which seeks to “price” nature through neoclassical economic methods; second, the standardization of natural capital accounting led by international organizations including the United Nations, culminating in the System of Environmental-Economic Accounting—Ecosystem Accounting (SEEA EA) as an international statistical standard in 2021 (United Nations, 2021). These efforts aim to establish a global consensus and a common language for ecological governance. However, this attempt to incorporate nature into commodity logic has been accompanied from the outset by profound theoretical critiques and practical tensions, sparking extensive debate on environmental governance and the commodification of nature.

Ecosystem service (ES) assessment methods form the theoretical and practical foundation of natural capital accounting and have evolved from single economic valuation toward pluralistic value integration (Manes et al., 2022). Early methods, rooted in environmental economics, relied heavily on neoclassical marginal utility pricing theory to make the value of ES “visible” and comparable through monetization. These include market pricing, revealed preference methods, and stated preference methods (Zhao et al., 2022; Rey-Valette et al., 2017). Given the inherent limitations of monetization, non-monetary evaluation methods—such as biophysical assessments and socio-cultural valuation—have gained increasing attention as complements or alternatives (Harrison et al., 2018). To address large-scale assessment needs, Value Transfer methods are widely used, applying results from studied sites to policy sites (Brown et al., 2016). However, high demands for geographical and ecological similarity make value transfer a major source of uncertainty, and its misuse often leads to flawed decisions. The latest advancements involve Integrated Assessment Models (IAMs). For example, the UK's Enabling a Natural Capital Approach (ENCA) provides a comprehensive framework that integrates multiple tools rather than prescribing a single approach (Department for Environment FRA, 2020). It guides users in comparing natural capital changes between business-as-usual (BAU) and projected scenarios through cost-benefit analysis (CBA), thereby supporting public project decisions. Such models seek to bridge the gap between assessment and decision-making.

The TEEB framework epitomizes these monetization approaches, aiming to render ecosystem contributions visible through marginal utility pricing. Its methodology has provided a toolbox for global ecological valuation and influenced policy in many countries. Yet, this paradigm faces sustained and deep criticism. Firstly, its theory of value is reductive. Critics argue that TEEB's overreliance on market-based pricing simplifies and reshapes nature into “capital” and “services,” inevitably neglecting non-market, intrinsic, ecological, and cultural values (Tom and Read, 2015). This constitutes an “over-simplification,” compressing incommensurable plural values into a single monetary metric, thereby failing to reflect the complex value of nature comprehensively and authentically. Secondly, it faces practical methodological challenges. For instance, value transfer is often questioned for applicability, while stated preference methods are prone to multiple biases. These issues hinder the acceptance of TEEB's economic valuations by local governments and industries (Martin et al., 2018), thus impeding its integration into practical decision-making. The United Nations' SEEA EA framework (2021) seeks to overcome the fragmentation of valuation methods through standardized accounting. It classifies ecosystem services into provisioning, regulating and maintenance, and cultural services, explicitly excluding “supporting services” to avoid double-counting, and attempts to align with national accounts. Pilot projects in the EU and China demonstrate its significant potential for revealing value and institutionalizing policy (Bank et al., 2025; Ji et al., 2025). However, its application encounters challenges such as data limitations, scaling issues, and the static nature of accounts.

Critiques of TEEB and SEEA EA must be situated within broader debates on the “commodification of nature.” Critics warn that these approaches may lead to a “commodification trap,” wherein conservation efforts are directed only toward ecosystems that can be monetized, thereby reinforcing a neoliberal logic of environmental governance (Kosoy and Corbera, 2010). In response, scholars have proposed alternative assessment and governance paradigms (Martinez-Harms et al., 2015; Frantzeskaki et al., 2010). More constructive responses emerge from localized theoretical innovations. Chinese scholars, reconstructing ecological value theory through Marxist political economy, propose the concept of “generalized labor” (Xu, 2010), which incorporates labor maintaining ecosystem functions into value creation. By distinguishing between direct and indirect labor (Hai and Huan, 2022), a hierarchical assessment model is constructed. Utilizing Marx's capital circulation formula (M-C-M′) (Cai and Chen, 2021), they analyze how capital expansion compresses the regeneration cycle of ecosystem services, providing theoretical support for China's “Three Red Lines” policy (Zhou and Jiang, 2019). This marks a process of conceptual translation within China's unique political-economic context, where the global concept of “ecosystem services” is reinterpreted as “ecological products” –a distinctively Chinese concept emphasizing the process of value realization while attempting to avoid purely market-based pitfalls.

Despite these advances, significant gaps remain in the literature, revealing three critical disconnects between theory and practice: (1) The black box of value transformation mechanisms: Most literature focuses on static accounting (e.g., GEP = EPV + ERV + ECV), lacking a systematic deconstruction of the dynamic mechanism from “natural resources → ecological assets → ecological capital.” (2) Global-local tension in institutional friction: The global public good attribute presupposed by TEEB is difficult to reconcile with the administrative empowerment needs of developing countries (e.g., China's collective forest tenure reform). (3) Unclear dynamics of conceptual movement: The process through which global concepts (e.g., ES) interact with local knowledge (e.g., “Two Mountains” theory) and are ultimately “translated” into local institutions (e.g., GEP accounting) remains poorly understood. For instance, divergent bamboo carbon sink measurement methods in Fujian and Zhejiang provinces cause value discrepancies, hindering market recognition (Fu et al., 2024; Wu et al., 2020).

This study introduces “conceptual movement theory” to address these gaps, constructing a dynamic framework driven by both “global consensus” and “local innovation.” Its contributions are 2-fold: (1) Theoretically, deconstructing the five-stage evolutionary law of realizing ecological product value (stipulation-unfolding-transformation-perfection-realization), revealing the key role of the labor theory of value in the “transformation” stage. (2) Practically, proposing the “three-stage transformation model” (natural resources → ecological assets → ecological capital), clarifying the mechanism by which property rights definition significantly reduces transaction costs by reconstructing property rights boundaries. This framework provides a Chinese solution with both theoretical explanatory power and practical operability for developing countries to overcome the dilemma of ecological governance.

To address the gap between global consensus and local practices, the Section 3 introduces a dynamic theoretical framework based on concept movement theory, which integrates global consensus with local innovation.

2.2 Methodology

To systematically examine the dynamic evolution pathways and institutional logic behind the realization of ecological product value, this study employs a qualitative multi-method research design that integrates comparative multi-case analysis and policy text content analysis. Guided by a “theory-driven, empirically-verified, mechanism-refined” approach, the research ensures the reliability and validity of its findings through triangulation of multiple data sources. Data collection and analysis cover the period from 2010 to 2023, beginning with the formal introduction of the concept of “ecological products” in China and encompassing all major subsequent policy developments and local practical innovations.

2.2.1 Data collection

Data were collected from multiple sources, including policy documents, academic and case publications, secondary statistical data, news, and industry reports. A total of 67 policy documents—such as laws, plans, guidelines, implementation plans, and standards—were obtained from central government bodies (e.g., National Development and Reform Commission, Ministry of Ecology and Environment) and local governments of the selected cases. Additionally, 73 academic articles focusing on the case regions were retrieved from databases such as CNKI and Web of Science. Official quantitative data, including Gross Ecosystem Product (GEP) statistical bulletins, national economic and social development statistical bulletins, and environmental status reports, were also collected. Supplementary information was gathered from authoritative media and think tanks.

2.2.2 Case selection

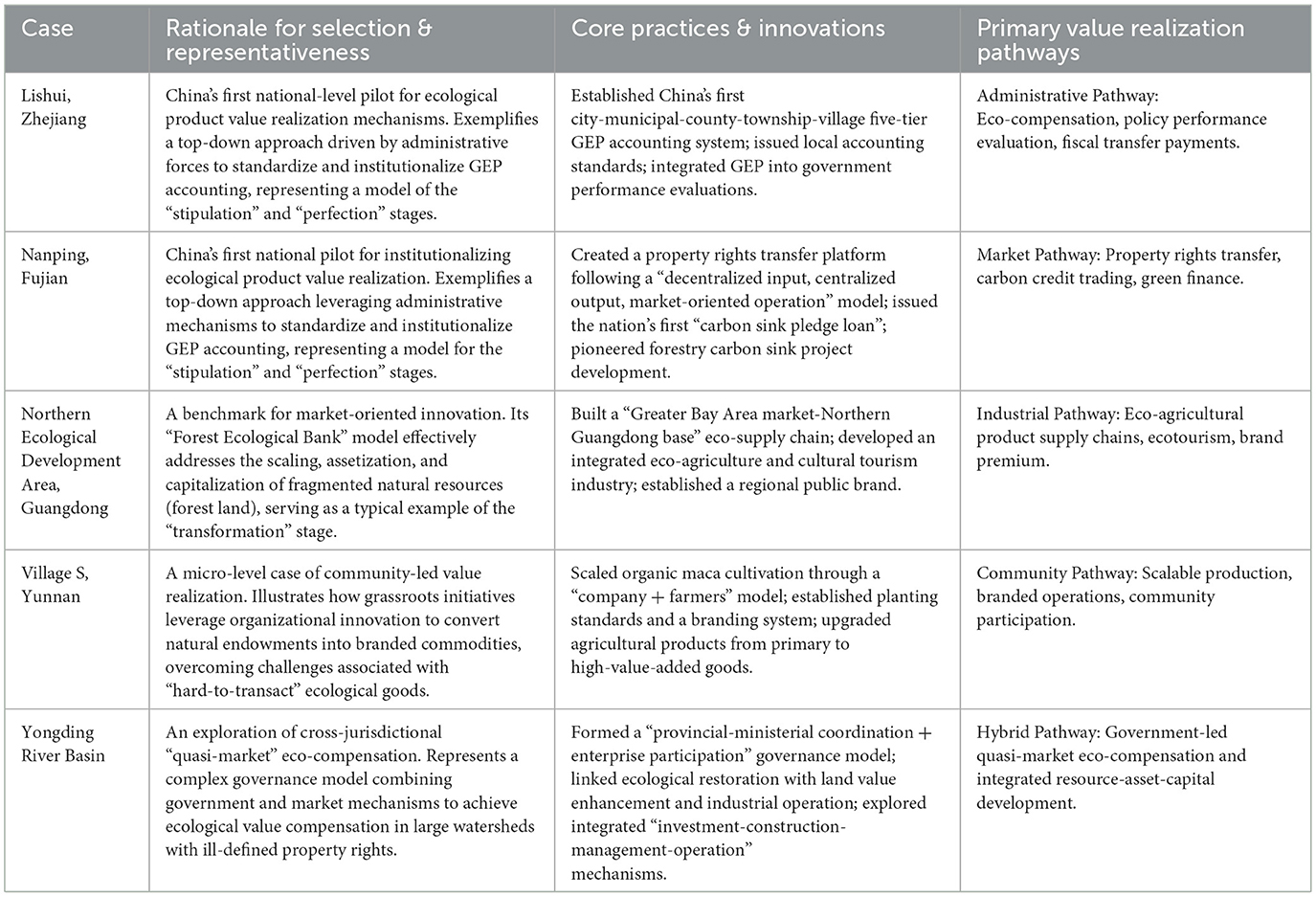

Based on the principles of typicality and maximum variation, a purposive sampling strategy was adopted to select five representative and pioneering regions as case studies (Table 1): Lishui (Zhejiang Province), Nanping (Fujian Province), the Northern Ecological Development Area of Guangdong Province, Village S in Yunnan, and the Yongding River Basin. We acknowledge that such a sampling approach may introduce selection bias, as these cases may not fully represent all regional contexts. To mitigate this, we:

• Clearly defined the boundaries of representativeness, noting that findings are primarily applicable to regions similarly committed to ecological value transformation and equipped with certain policy resources;

• Examined not only successful experiences but also in-depth challenges and failures observed in practice, such as difficulties in GEP application and carbon accounting inaccuracies;

• Treated cases as analytical units for revealing mechanisms and processes, rather than statistical units for inference, focusing on deriving theoretically insightful and transferable institutional logics from these pioneering practices.

Table 1. Representative cases and characteristics.

2.2.3 Analytical procedure

Policy text analysis employed a directed content analysis approach. Collected policy documents were imported into NVivo 12, with sentences or paragraphs as coding units. The coding scheme included conceptual codes such as ecological products, value accounting, value realization, GEP, property rights definition, eco-compensation, and technological innovation, as well as process codes like establishing mechanisms, piloting initiatives, refining standards, and promoting application. The process involved three steps: (1) Two researchers independently pilot-coded 20% of randomly selected texts, compared results, discussed discrepancies, and achieved high inter-coder reliability (Cohen's Kappa > 0.8); (2) One researcher completed full-text coding, while another reviewed the coding; (3) Axial coding was conducted to identify relationships among codes, ultimately distilling a five-phase model: stipulation-unfolding-transformation-perfection-realization, which constitutes the dynamic evolution framework of this study.

Case data analysis utilized pattern matching and cross-case synthesis. Each case was first analyzed internally to examine its context, specific practices, outcomes, and challenges. Cross-case comparison was then performed to identify common and divergent patterns across cases in terms of value realization pathways, drivers, bottlenecks, and solutions, thereby validating and enriching the theoretical framework.

2.2.4 Reliability and validity

Rigor was ensured through multiple strategies: (1) Data triangulation: Integrating policy texts, academic publications, statistical data, and news reports to corroborate findings; (2) Theoretical matching: Comparing the theoretically derived five-phase model with empirical patterns observed in cases, while considering alternative explanations and ruling out rival causal relationships through evidentiary chains; (3) Cross-case replication: Demonstrating that the five-phase model recurred across all five cases in varying contexts, indicating theoretical generalizability beyond individual cases; (4) Transparency and auditability: Maintaining a case study database containing raw data and analytical memos, along with detailed coding manuals and operational protocols, to ensure replicability and auditability of the research process.

3 Theoretical framework: the dynamic evolution mechanism of concept movement

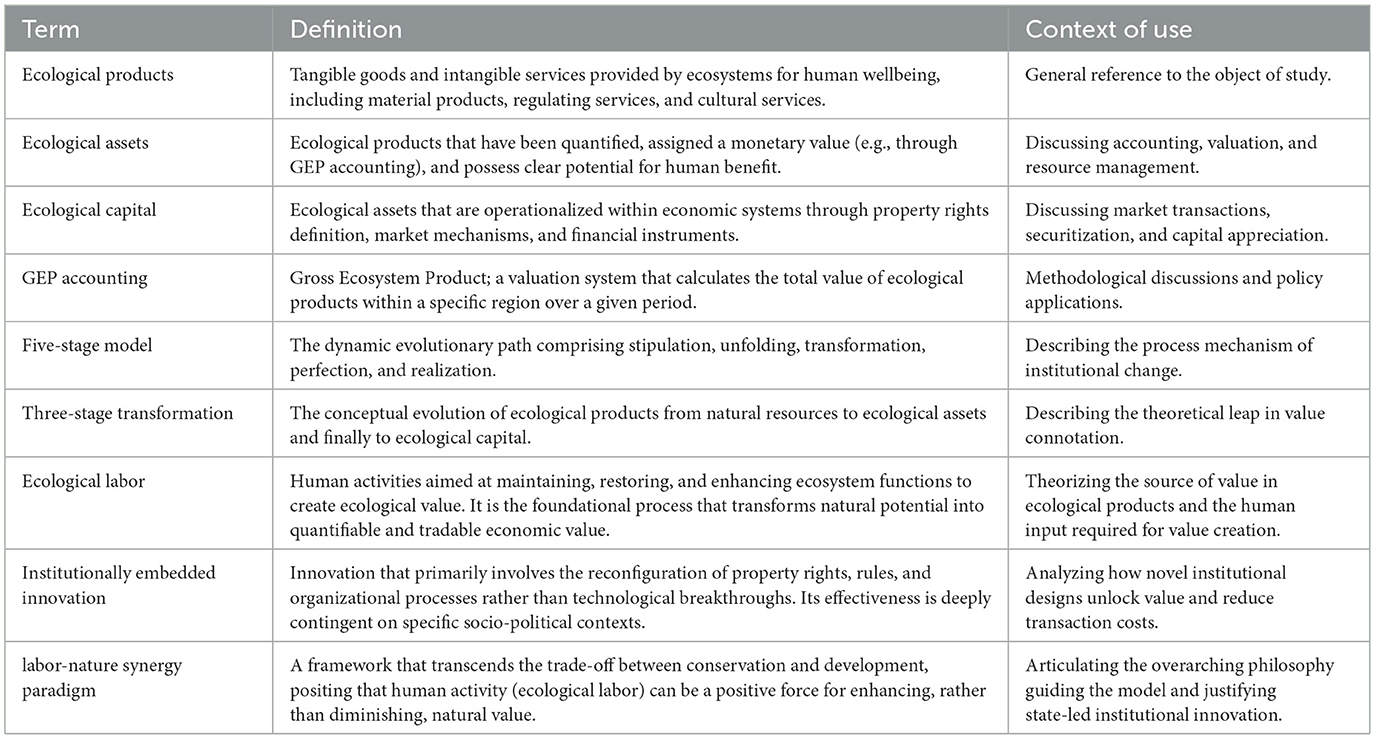

3.1 Conceptual clarification: key terms and definitions

To clarity terminological ensure conceptual and consistency throughout the following analysis, we first define the key terms that form the backbone of our theoretical framework. These definitions are distilled from the literature and refined through our policy text analysis and case studies (Table 2).

Table 2. Key terminology and definitions.

3.2 Philosophical foundation and contradiction-driven mechanism

3.2.1 The dual tension of value ontology

Marx emphasized in Volume I of Capital: “Labour is not the source of all wealth. Nature is just as much the source of use values... as labour is” (Marx, 1992). This assertion reveals the dual dimension of ecological product valuation: natural matter as the material carrier of use value, and human labor as the active subject of value appreciation. Under the tension between globalization and localization, this duality evolves into two competing paradigms.

The first paradigm is the natural capital paradigm (TEEB). Its theoretical core inherits the neoclassical economic tradition, simplifying ecosystem services into divisible and tradable stocks of natural capital. This approach assumes that nature possesses intrinsic value and can be transacted in markets through marginal utility pricing, without labor intervention. However, this paradigm faces practical difficulties. Market mechanisms often fail to reflect the full complexity and dynamism of ecosystems. Moreover, the marketization of natural capital may lead to the privatization and commercialization of nature, potentially eroding its intrinsic value (Igoe, 2014).

The second paradigm is the labor-nature synergy paradigm (GEP). It is based on Marxist political economy, proposing that “ecological products are the synergistic outcome of natural matter and human labor” (Ouyang et al., 2013). In the labor process and value concept of ecological products, socialist ecological civilization construction based on Marx's historical materialism emphasizes the synergistic relationship between labor and nature, defining ecological products as the result of the joint action of human labor and natural matter (Zhuang et al., 2024).

3.2.2 The contradiction between TEEB and GEP

TEEB (The Economics of Ecosystems and Biodiversity) and GEP (Gross Ecosystem Product), as the two major theoretical frameworks for ecological value accounting, exhibit significant differences in theoretical foundations and methodologies, while also showing deep-seated contradictions in practical application.

Theoretically, TEEB's foundation stems from the market equilibrium analysis of neoclassical economics, focusing on promoting the market-based allocation of natural capital by quantifying the market economic value of ecosystem services (Groot et al., 2018). This method emphasizes using market-based tools like the replacement cost method and contingent valuation method to assess the economic value of ecosystem services, but its strategy of over-relying on market simulation pricing overlooks the integrity and irreplaceability of ecosystems (Costanza et al., 1997). Conversely, GEP's theoretical system is rooted in the ecological transformation of Marx's labor theory of value, viewing ecological products as special commodities embodying socially necessary labor time, attempting to construct an ecosystem accounting indicator parallel to GDP (Shi and Chen, 2022). This theoretical difference is theorized to a fundamental conflict in the definition of value connotation: TEEB simplifies ecological value into market transaction prices, whereas GEP emphasizes the social use value attribute of ecological products. Furthermore, regarding the applicability of theoretical foundations, TEEB aligns more with the weak sustainability paradigm, advocating the substitutability of natural and man-made capital, while GEP's accounting logic implies a strong sustainability concept, emphasizing the irreplaceability of critical natural capital (Jin and Lu, 2021).

Methodological contradictions are particularly prominent. TEEB constructs refined market transaction mechanisms by decomposing ecosystem services into tradable units, but its methodology suffers from assessment biases in pricing non-material ecological products like cultural and regulating services (Zhang et al., 2023). Case studies show that the Contingent Valuation Method (CVM) used by TEEB often yields distorted valuation results when implemented in developing countries due to variations in respondents' environmental awareness levels (Ouyang et al., 2020). In contrast, GEP accounting, despite establishing a three-level indicator system including material products, regulating services, and cultural services, faces a dual dilemma in technical implementation: first, the valuation of regulating services heavily relies on indirect pricing methods like the shadow engineering method, leading to subjective biases in calculating the marginal value of complex processes such as ecological hydrology (Wei et al., 2024); second, the overlap between the scope of material products and GDP accounting raises concerns about double counting, for instance, the output value of forest products already reflected in national economic statistics is still treated as an independent accounting item under the GEP framework (Wang, 2024). This methodological incompatibility makes cross-regional GEP comparisons lack a scientific basis; GEP accounting results for the Yellow River Basin from 2015 to 2020 showed value fluctuations up to 37% for the same ecological unit due to differences in parameter selection (Hua and Tong, 2023).

Contradictions in practical application are manifested in institutional adaptability and policy tool effectiveness. TEEB faces an “institutional transplant dilemma” in its global promotion, as its market-dominated value realization model struggles to land in regions with imperfect property rights systems (Kumar, 2010). Taking ecological compensation in the Amazon basin as an example, the carbon trading system suffered from low execution efficiency due to land tenure disputes, with the forest protection target completion rate below 60% between 2010 and 2020 (Islar, 2019). While China's GEP practice has developed innovative tools like ecological credit points and GEP loans, it remains trapped in the predicament of “hot accounting, cold application.” A 2023 survey across 15 provinces showed that only 29.6% of counties substantially applied GEP accounting results to the formulation of ecological compensation standards, with most applications remaining superficial for performance assessment (Sun, 2023). This “theoretical gap” exposed in practice manifests as the difficulty in effectively integrating TEEB's market-oriented path with GEP's administrative promotion model, especially in the reform of separating operational rights for ecological products, where the two conflict in defining ownership rules for different types of ecological products (Li and Ouyang, 2021).

A deeper contradiction stems from cognitive divergence regarding the value transformation mechanism. TEEB and GEP differ fundamentally in their theoretical logic: the former focuses on promoting the explicit value transformation of natural capital through market mechanisms; the latter's accounting goal explicitly emphasizes the realization of the implicit social value of natural capital protection, with government performance weighting higher than market pricing principles. This is intended to incompatibility between the two systems in practice. A typical case is Zhejiang Province's early exploration of a “GEP-GDP conversion rate,” which created a logical paradox in theory and practice by mistakenly equating GEP (a flow) directly with the economic value of tradable capital stock, ultimately leading to the removal of related indicators through policy revision in 2021 (Shi and Chen, 2022). Institutional economic analysis indicates that the root of this contradiction lies in the differentiated definition of value attributes: TEEB largely follows the marginal utility theory of value, while GEP embodies the labor theory of value and strong sustainability concepts.

These systemic contradictions provide a realistic basis for introducing concept movement theory. By analyzing the reconstruction process of conceptual elements in ecological governance practices, this theory can effectively bridge the institutional logic gap between TEEB and GEP. Specifically, concept movement theory focuses on the dynamic process of generation, evolution, and institutional solidification of key concepts in policy texts. For example, the evolution of the “ecological regulating services” concept in GEP accounting shows clear institutional shaping characteristics, its connotation shifting from the academic discourse of “ecological process services” to the policy text's “quantifiable ecological products.” This conceptual reconstruction essentially reflects the practical needs of ecological civilization institutional innovation. By constructing a five-stage analytical model of “stipulation- unfolding- transformation-perfection- realization,” concept movement theory can explain the “institutional rejection” phenomenon encountered when applying TEEB in developing countries and provide theoretical support for the Sinicization innovation of GEP (Qi, 2025). This framework reveals how the localized recreation of ecological governance concepts can overcome the dilemma of theoretical transplantation, for instance, by creatively applying the labor theory of value to ecological asset assessment, forming an accounting system with Chinese paradigm characteristics.

3.2.3 Contrasting the TEEB and GEP paradigms: operational challenges and contextual applications

The Economics of Ecosystems and Biodiversity (TEEB) and Gross Ecosystem Product (GEP) represent two distinct paradigms for integrating ecological values into decision-making. Moving beyond abstract theoretical differences, our analysis highlights the operational complexities and contextual applications that define and differentiate these frameworks. Rather than monolithic or directly competing systems, they reflect divergent priorities and governance contexts.

TEEB, grounded in neoclassical environmental economics, emphasizes the quantification of ecosystem service values in monetary terms to make ecological conservation legible to market and policy actors. However, it encompasses a diverse suite of valuation methodologies—from contingent valuation to benefit transfer—which can yield significantly different results for the same service. This methodological plurality, while flexible, leads to challenges in comparability and standardization across studies. Moreover, TEEB's core strength in raising awareness and advocating for biodiversity conservation globally is often tempered by its limited direct integration into national accounting systems or subnational performance evaluation. Its application can be constrained in institutional contexts where market mechanisms are less developed or where non-use and intrinsic values are difficult to express in monetary terms.

Conversely, China's GEP accounting framework emerged from a need for standardized, policy-applicable metrics that align with domestic governance priorities. It represents a more prescriptive approach, aiming for consistency and comparability across regions for the purpose of performance assessment and ecological compensation. Nevertheless, significant methodological inconsistencies persist within the GEP system itself. Variations in parameter selection, valuation techniques for regulating services, and the treatment of double-counting across material products, regulating, and cultural services remain contentious. For instance, valuation outcomes for similar forest ecosystems can vary considerably between provinces due to differences in underlying models and localized accounting guidelines. This underscores that GEP is not a fixed, perfected system but an evolving, and at times inconsistent, practice of techno-political standardization.

Fundamentally, the two frameworks serve different primary purposes. TEEB often functions as a global advocacy and awareness-raising tool, highlighting the economic costs of degradation and the benefits of conservation. In contrast, GEP is designed primarily as a domestic policy-integration and performance-management tool, explicitly linked to cadre evaluations, fiscal transfer payments, and territorial development planning. This distinction in purpose explains their differing methodological choices: TEEB's flexibility supports its communicative goals, while GEP's drive for standardization supports its administrative functions.

Therefore, a simplistic comparison that pits one framework against the other is inadequate. A more nuanced understanding recognizes that TEEB and GEP are applied in different contexts and are designed to solve different problems. The choice between or integration of these frameworks depends on the specific policy objectives, institutional capacities, and governance contexts at hand.

3.3 Deconstruction and dynamic evolution of the five-stage model for realizing ecological product value

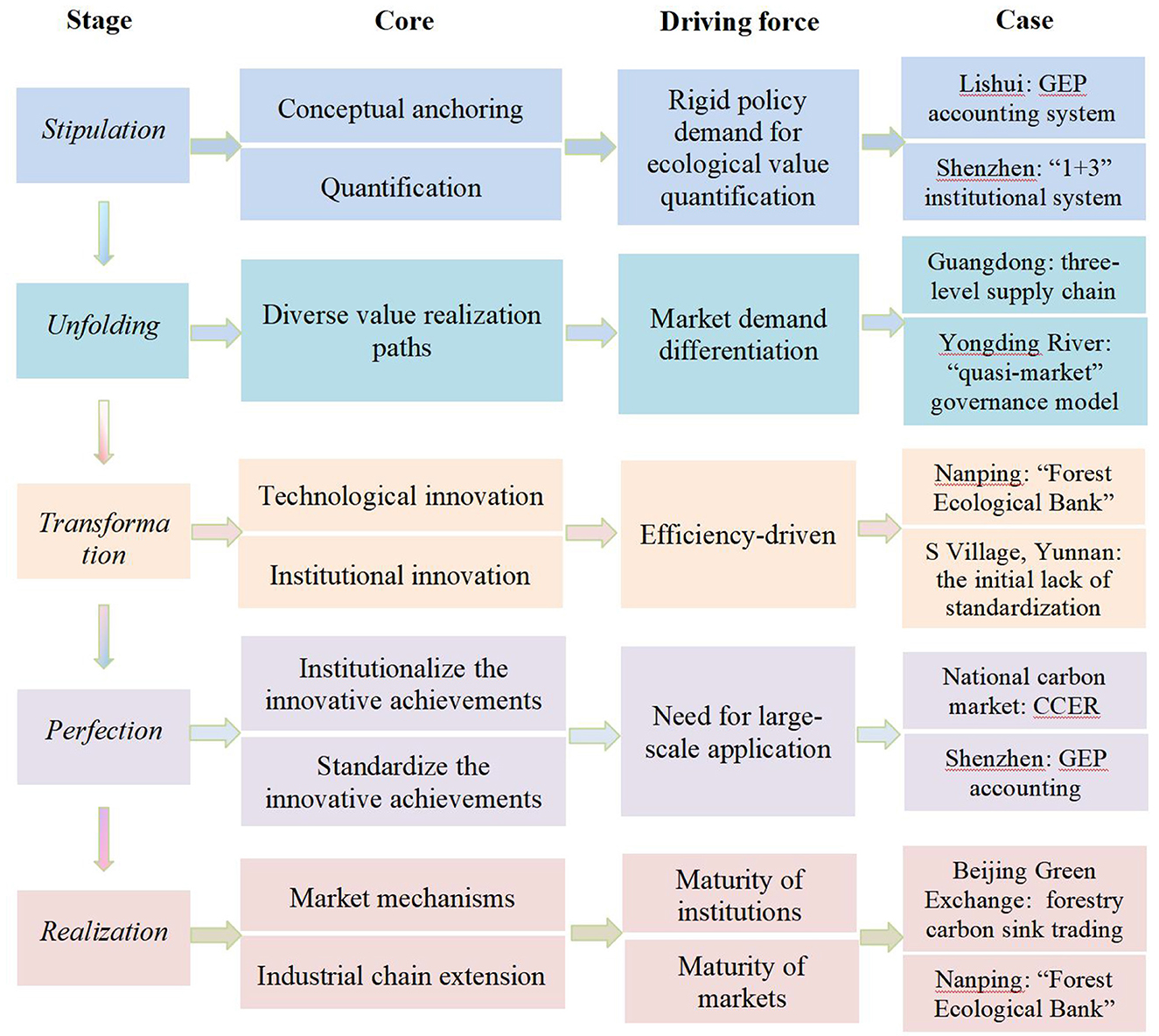

The five-stage division for realizing ecological product value is based on a full-process deconstruction of the transformation from “lucid waters and lush mountains” to “gold and silver mountains” (Figure 1). Each stage independently carries specific functions while forming an organic whole through logical progression. This framework starts with “stipulation” as the logical beginning, progresses through “unfolding,” “transformation,” and “perfection,” and finally achieves value closure in the “realization” stage. Its internal logic relies heavily on the synergistic effects of policy drive, market demand, and technological innovation.

Figure 1. The five-stage division for realizing ecological product value.

3.3.1 The “stipulation” stage

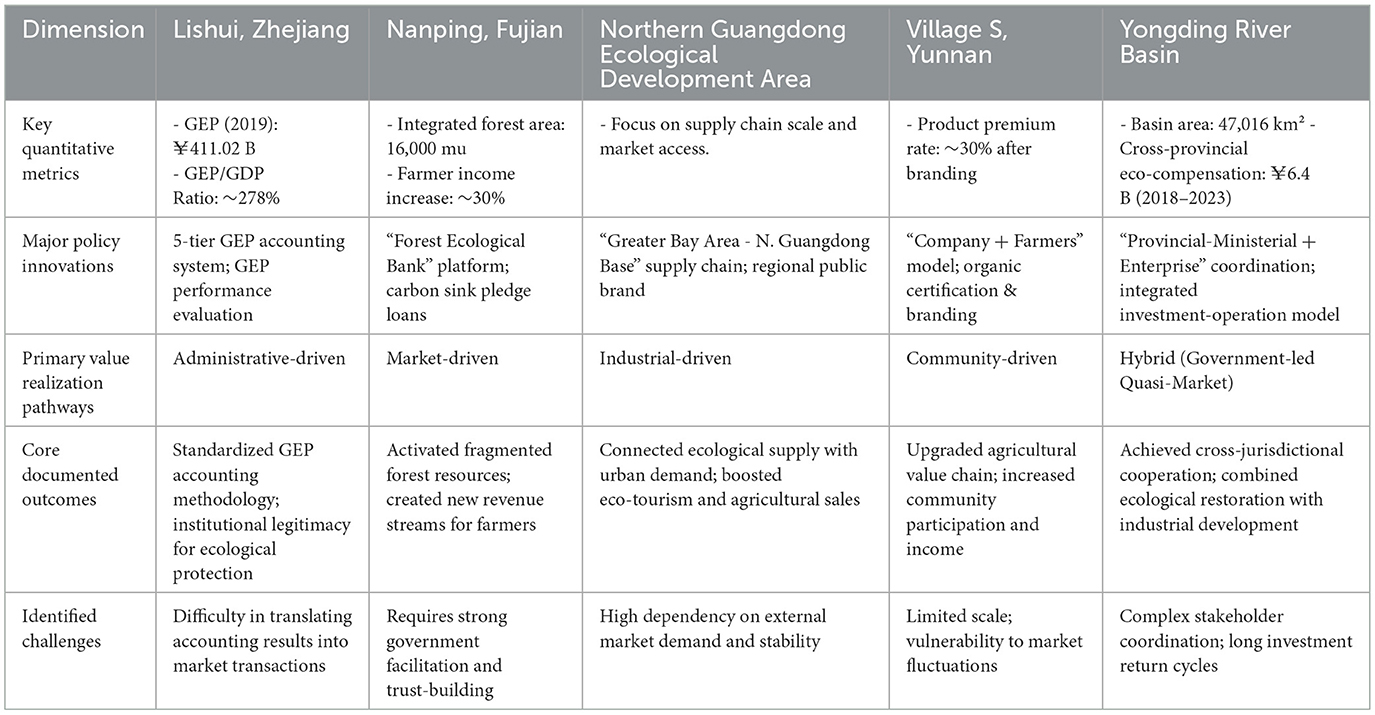

The “stipulation” stage, as the foundation of value realization, addresses the conceptual anchoring and quantification basis of ecological products. Its core lies in defining the scope, value attributes, and accounting framework of ecological products through theoretical construction and standard setting. For example, defining ecological products as a composite system of material products (e.g., agricultural products, timber), regulating services (e.g., carbon sinks, water conservation), and cultural services (e.g., ecotourism), and monetizing ecological service value through the Gross Ecosystem Product (GEP) accounting system. In practice, Lishui, Zhejiang, established a four-level GEP accounting system (city, county, township, village) covering 13 types of ecological products, while Shenzhen pioneered a “1+3” institutional system (implementation plan, local standards, statistical reports, accounting platform) to standardize the accounting process (Ouyang et al., 2013; Shi and Chen, 2022). In 2019, Lishui City recorded a Gross Ecosystem Product (GEP) of 411.021 billion yuan, with the realized value of ecological products reaching 101.749 billion yuan—an ecological product value realization rate of 24.76%. Notably, regulating services such as water conservation and carbon sequestration accounted for more than 75% of the total GEP, quantitatively underscoring the critical role of non-market ecological functions. The driving force of this stage stems from the rigid policy demand for ecological value quantification, such as the Opinions on Establishing and Improving the Mechanism for Realizing the Value of Ecological Products, which explicitly requires “establishing mechanisms for ecological product investigation, monitoring, and value assessment,” compelling local governments to overcome the “difficulty in measurement” through institutional innovation.

3.3.2 The “unfolding” stage

The “unfolding” stage builds upon “stipulation” by differentiating practical pathways, focusing on the systematic design of diverse value realization paths. Its core is to construct differentiated transformation paths based on the type differences of ecological products (material, regulating, cultural services) and spatial endowments. For example, the ecological development zone in northern Guangdong constructed a three-level supply chain (“Greater Bay Area central cities - northern Guangdong city/county centers - northern Guangdong villages/towns”), with central cities responsible for R&D and trading, and villages focusing on ecological product production, forming a composite model of “ecological agriculture + cultural tourism integration” (Yao et al., 2023). The Yongding River basin, through a “quasi-market” governance model of “ministry-province coordination + enterprise participation,” integrates ecological restoration with land development and industrial operation, achieving an integrated “investment, construction, management, operation” system. The driving force of this stage comes from market demand differentiation: urban consumption upgrades create demand for high-quality agricultural products and ecotourism, while “dual carbon” policies activate the market potential for regulating services like carbon sink trading, promoting the unfolding of ecological products from single supply to diverse business formats.

3.3.3 The “transformation” stage

The “transformation” stage addresses the practical bottlenecks encountered during “unfolding” by enhancing value realization efficiency through technological and institutional innovation. Technologically, digital tools like GIS and remote sensing are used for dynamic monitoring of ecological products (e.g., automated GEP accounting platforms), while green finance tools (e.g., “ecological loans,” “carbon sink pledge loans”) overcome the “difficulty in collateralizing” ecological assets. Institutionally, the “Forest Ecological Bank” in Nanping, Fujian, establishes a property rights circulation mechanism of “dispersed input, centralized output” through the collection, storage, and confirmation of forestland management rights (Sun, 2023; Ji, 2022). These innovations directly respond to the pain points exposed in the “unfolding” stage—for example, the initial lack of standardization in Village S, Yunnan, for Maca cultivation led to market fluctuations, forcing the local government and enterprises to establish planting specifications and brand systems (Zhu et al., 2023). The driving force of this stage is essentially efficiency-driven: when diverse paths encounter technical barriers (e.g., insufficient accounting accuracy) or institutional obstacles (e.g., ambiguous property rights), innovation becomes the necessary choice to break through bottlenecks.

3.3.4 The “perfection” stage

The “perfection” stage aims to institutionalize and standardize the innovative achievements formed during “transformation,” building a sustainable value realization system. Its core tasks include establishing unified accounting standards (e.g., Zhejiang's Guidelines for Ecological Product Value Accounting), improving assessment systems (e.g., Guizhou's exploration of dual GEP and GDP assessment), and standardizing market rules (e.g., Guangzhou Carbon Exchange trading rules). Shenzhen links ecological value with performance evaluation by incorporating GEP accounting results into the ecological civilization assessment system (Shi and Chen, 2022). At the national level, standardizing CCER trading rules integrates forestry and agricultural carbon sinks into the national carbon market, addressing the “fragmentation” issue in trading (Sun, 2023). The driving force of this stage comes from the need for large-scale application: when technological innovations (like green finance products) require cross-regional promotion, standardization becomes key to reducing transaction costs and enhancing credibility, while institutional solidification provides guarantees for long-term, stable value realization.

3.3.5 The “realization” stage

The “realization” stage represents the substantive leap from ecological value to economic benefits, achieving value closure through market mechanisms and industrial chain extension. It manifests in two types of paths: first, direct trading, such as Sanhua plums from northern Guangdong supplied directly to the Greater Bay Area via e-commerce platforms, shortening circulation links; second, rights trading, such as the promotion of forestry carbon sink trading by the Beijing Green Exchange, converting ecological regulating services into carbon assets (Sun, 2023; Yao et al., 2023). Nanping, Fujian, through its “Forest Ecological Bank,” develops collected forestland on a large scale, returning profits to village collectives and farmers based on shares, forming a cycle of “resources to assets, assets to capital” (Ji, 2022). As of now, through the mechanism of “decentralized input-integrated operation-equity transformation,” Nanping's “Forest Ecological Bank” has intensified the management of 16,000 mu of scattered forest land, increasing the average annual income of 92,800 forest farmers by over 30%. It has also diversified into carbon sink trading and underforest economy, among other models, achieving a cumulative total forestry output value of 115.9 billion yuan. The driving force of this stage stems from the dual maturity of institutions and markets: standardized accounting systems (“perfection” outcomes) ensure ecological products are measurable and tradable, while green finance tools (“transformation” outcomes) lower financing barriers, jointly promoting the conversion of ecological value from theoretical form to real benefits.

The logical progression of the five stages is essentially a dynamic process of “problem-oriented → innovation response → system solidification → value release”: dual demands from policy and market drive “stipulation” and “unfolding,” practical bottlenecks compel “transformation” and “perfection,” ultimately achieving a virtuous cycle between ecology and economy through “realization.” Among these, policy drivers run throughout (e.g., top-level national strategic design), market drivers determine path selection (e.g., consumption demand guides business format innovation), and technological drivers overcome efficiency bottlenecks (e.g., digital technology improves accounting accuracy). These three together constitute the internal dynamic mechanism of the five-stage evolution. This logical structure not only provides an operational framework for ecological governance from concept to practice but also reveals the synergistic laws of institutional innovation, market cultivation, and technological support in the “Two Mountains” transformation.

The five-stage model detailed above provides a dynamic process framework for the realization of ecological product value. This processual evolution is intrinsically linked to a parallel conceptual evolution in understanding what ecological products are and how their value is constituted. As empirically demonstrated in Table 3, the policy innovations and quantitative outcomes across diverse cases directly reflect and operationalize these evolving conceptualizations. The following section (Section 4) examines this complementary dimension in depth: the three-stage leap in the connotation of ecological products themselves, from natural elements to factors of production to capitalizable assets.

Table 3. . Empirical overview of case performance and outcomes.

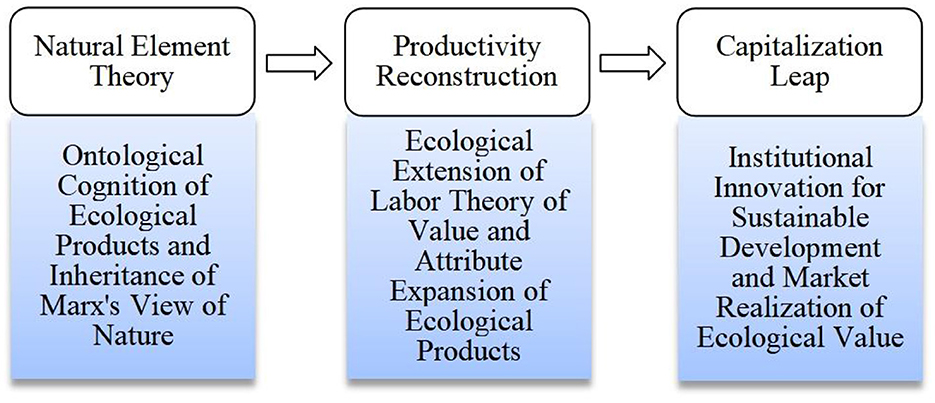

4 Three-stage leap in the connotation of China's ecological products

The evolution of the connotation of China's ecological products has undergone a three-stage leap: “natural element theory → productivity reconstruction → capitalization leap” (Figure 2). This process is both an inheritance of Marx's labor theory of value and an innovative interpretation of sustainable development theory.

Figure 2. The evolution of the connotation of China's ecological products.

4.1 Natural element theory: ontological cognition of ecological products and inheritance of Marx's view of nature

Early cognition of ecological products focused on their natural attributes, defining them as a collection of natural elements spontaneously provided by ecosystems to sustain human existence. This stage is represented by the definition in the National Main Functional Area Plan, emphasizing that ecological products are “natural elements that maintain ecological security, guarantee ecological stipulation functions, and provide a good living environment,” including fresh air, clean water, pleasant climate, etc. (Ma et al., 2020; OuYang et al., 2020). This cognition aligns with the assertion in Marxist view of nature that “nature is the primary source of all means and objects of labor”—Marx believed that nature, as the material basis unprocessed by labor, is the prerequisite for human survival and development. For example, Marx pointed out in Capital that “land is the source of all production and all existence,” and the natural element theory of ecological products is a concretization of this idea, viewing natural endowments like air and water as indispensable ecological foundations for human society.

In practice, ecological products in this stage were primarily public goods, mainly protected passively through systems like ecological protection red lines and nature reserves. For instance, the construction of the Sanjiangyuan National Park focused on protecting the authenticity of the ecosystem, emphasizing its natural stipulation function as the “Water Tower of China,” without yet involving value quantification or market transformation (Shi and Chen, 2022; OuYang et al., 2020). The theoretical limitation of this stage lies in viewing ecological products as purely natural gifts, failing to fully reveal the interactive relationship between human labor and ecosystems, yet it laid the ontological foundation for subsequent theoretical evolution.

4.2 Productivity reconstruction: ecological extension of labor theory of value and attribute unfolding of ecological products

With the deepening practice of the theory that “lucid waters and lush mountains are invaluable assets,” the connotation of ecological products expanded from pure natural elements to “products of the joint action of nature and labor,” forming the “productivity reconstruction” stage. Marx's labor theory of value holds that labor is the core of value creation, and the realization of ecological product value requires processing and enhancement of natural elements through human labor. The theoretical breakthrough in this stage lies in distinguishing between “natural ecological products” and “labor ecological products”: the former refers to ecosystem services without human labor intervention (e.g., the carbon sink function of primary forests), while the latter emphasizes tradable products formed through human labor participation, including labor ecological products (e.g., organically grown agricultural products under standardized cultivation) and ecological commodities (e.g., ecotourism services operated through branding) (Ma et al., 2020).

In practice, this stage is characterized by ecological product value accounting (GEP) and industrialization. For example, Lishui, Zhejiang, constructed a GEP accounting system covering “material products—regulating services—cultural services,” incorporating forest carbon sinks, tourism landscapes, etc., into value measurement, where labor inputs such as artificial forest cultivation and ecotourism facility construction are considered key to value appreciation (Zhu et al., 2023). Village S in Yunnan developed Maca cultivation through an “enterprise + farmer” model, combining the natural endowments of high-cold mountains with standardized planting techniques, upgrading Maca from a primary agricultural product to a commodity with brand premium, reflecting the theoretical logic that “labor transforms natural elements into economic value.” The inheritance of Marx's labor theory of value in this stage lies in: adhering to “labor is the sole source of value,” while expanding the scope of labor—extending from traditional industrial and agricultural labor to “ecological labor” such as ecological management and environmental governance, interpreting the ecological reconstruction of the connotation of productivity in the new era.

4.3 Capitalization leap: institutional innovation for sustainable development and market realization of ecological value

The third stage leap in the connotation of ecological products is the “capitalization leap,” i.e., transforming the use value of ecological products into tradable capital forms through property rights systems, market mechanisms, and financial instruments, realizing the transformation from “ecological capital” to “financial capital.” This stage breaks through the static cognition of ecological value in traditional economics, draws on the concept of “natural capital” in sustainable development theory, and innovatively incorporates ecological products into the capital circulation system. Marxist political economy holds that capital is “value that can bring surplus value,” and ecological capitalization, through rights confirmation and registration, trading platforms, and financial innovation, endows ecological products with the value-appreciating attribute of capital. For example, the “Forest Ecological Bank” in Nanping, Fujian, integrates fragmented forest resources into tradable carbon sink assets by collecting and storing forestland management rights, achieving the transformation from “a piece of forest” to “an account”; the Guangdong Carbon Exchange promotes forestry carbon sink pledge loans, converting the carbon sequestration amount of trees into corporate financing certificates, reflecting the capitalization operation of ecological value.

At the level of institutional innovation, this stage forms a complete chain of “rights confirmation - accounting - trading - financing”: defining property rights boundaries through natural resource rights confirmation (e.g., unified real estate registration system), providing a value benchmark based on GEP accounting, achieving market-based pricing through trading platforms for carbon emission rights, water rights, etc. (Yao et al., 2023), and finally completing capital monetization through financial instruments like green bonds and asset securitization. For example, Shenzhen established the GEP accounting “1+3” institutional system, incorporating ecological value into performance assessment and financial credit systems, promoting the synergy between ecological capital and industrial capital. This practice not only responds to the requirement of sustainable development theory for ecological value to be “measurable and tradable” but also transforms the theoretical conception of “natural capital” in Marxism into an operational institutional framework through market mechanism innovation, achieving a dynamic balance between ecological protection and economic development.

4.4 Theoretical logic: from marxism to an innovative interpretation of sustainable development

Marxism holds that nature and labor together constitute the source of wealth, and the three-stage evolution of ecological products is always rooted in the labor theory of value: “natural element theory” acknowledges the fundamental status of nature, “productivity reconstruction” emphasizes the activation of ecological value by labor, and “capitalization leap” realizes the value redemption of labor outcomes through market mechanisms. Different from traditional theory, the ecological product theory incorporates “ecological labor” (such as ecological restoration, environmental monitoring) into the scope of value creation, expanding the ecological dimension of labor, which is a theoretical concretization of Marxism in the era of ecological civilization.

Western sustainable development theory focuses on the “balance” between ecological protection and economic development, while China's ecological product theory achieves their “synergy” through the “capitalization leap.” For example, the ecological development zone in northern Guangdong constructed a “Greater Bay Area market—northern Guangdong base” supply chain, reinvesting the premium income from ecological agricultural products into ecological protection, forming a positive feedback loop of “protection—value appreciation—re-protection,” breaking through the mindset of “protection and development being mutually exclusive” in traditional sustainable development theory. This innovation of incorporating ecological products into capital circulation not only follows the laws of market economy but also avoids the alienation of ecology by capital through institutional design, providing a dual-drive paradigm of “market + institution” for global sustainable development.

5 Global implications: adaptability and challenges of china's experience

The practice of institutional change in realizing the value of ecological products in China offers a potentially valuable reference paradigm of “theoretical innovation—institutional experimentation—practical iteration” for global sustainable development. Its core lies in integrating Marxist labor theory of value with the modernization of ecological governance, constructing a dynamic framework of “valuing natural elements—institutionalizing labor input—synergizing market mechanisms.” This experience may offer insights for countries in the Global South (such as Southeast Asia, Africa, Latin America) that are rich in ecological resources but relatively weak in governance capacity. However, its promotion needs to fully consider the differences in institutional environments, technological capabilities, and ideologies across different regions.

5.1 Reference value and limitations of China's experience

China's practice in realizing the value of ecological products offers a valuable reference paradigm of “theoretical innovation–institutional experimentation–practical iteration” for global sustainable development. Its core lies in integrating Marxist labor theory of value with ecological governance modernization, constructing a dynamic framework of “valuing natural elements–institutionalizing labor input–synergizing market mechanisms.” This experience provides insights for Global South countries rich in ecological resources but relatively weak in governance capacity, such as those in Southeast Asia, Africa, and Latin America.

However, the applicability of this model is contingent upon specific institutional and contextual prerequisites that limit its direct transferability. China's success rests on several foundational elements not universally present: strong state capacity and effective top-down mobilization, exemplified by the rapid scaling of Gross Ecosystem Product (GEP) accounting from local pilots to a national framework; well-established institutional foundations such as forest tenure reform and unified natural resource registration, which enabled the definition of property rights essential to ecological assetization; advanced technological and data infrastructure reliant on high-resolution remote sensing, geographic information systems, and specialized ecological modeling; and ideological alignment between Marxist political economy and ecological civilization, which legitimizes a strong state role in guiding market mechanisms—an approach that may encounter resistance in contexts influenced by neoliberal governance traditions.

Thus, rather than serving as a blueprint, China's experience offers a repertoire of concepts and tools—such as “ecological labor” valuation, hybrid governance models, and innovative financial instruments—that must be critically evaluated and adapted to diverse local realities.

5.2 Diversity of pathways: a comparative perspective with Costa Rica

The variability in institutional contexts across the Global South suggests that multiple pathways exist for achieving ecological value realization. China's model, with its emphasis on state-led standardization and macro-accounting, represents one approach—particularly suited to settings with strong administrative capacity and centralized governance.

By contrast, Costa Rica's Payment for Ecosystem Services (PES) program illustrates an alternative model emerging from a democratic polity with strong environmental advocacy and international support. Rather than relying on a comprehensive regional accounting framework like GEP, the Costa Rican system operates through direct contracts with landowners for specific services such as carbon sequestration and hydrological regulation. Its funding derives largely from a dedicated fuel tax and World Bank partnerships, reflecting a more decentralized, incentive-based structure.

This comparison underscores that the effectiveness of any model depends on a nation's unique governance structure, financial mechanisms, and political economy. China's approach thrives under conditions of high state capacity and ideological alignment, whereas systems like Costa Rica's may be more viable in contexts with robust civil society engagement and access to international environmental financing. China's experience should thus be contextualized not as a universal template, but as one of several viable models, each reflecting distinct institutional origins and adaptive strategies.

5.3 Potential risks and real-world challenges in institutional transplantation

While innovative, China's ecological civilization model also carries potential negative externalities and significant implementation challenges, both internally and for countries seeking to adopt its elements. Internally, strong administrative pressure to increase Gross Ecosystem Product (GEP) can create perverse incentives—prioritizing easily quantifiable services like carbon sequestration over complex biodiversity conservation, or favoring monoculture plantations over native forests, thereby undermining holistic ecosystem integrity. The model's focus on capitalization risks reducing multifaceted ecological and cultural values to a narrow financial metric, which may lead to “green grabbing” if local communities are excluded from monetization processes and dispossessed of their resource rights. Furthermore, financial innovations such as ecological asset pledge loans introduce new risks of market instability, as ecological disasters or policy shifts could trigger sudden devaluation of these assets. Externally, adopting countries face three major institutional obstacles: property rights disparities, as “multiple ownership” conflicts arising from tribal traditions and colonial legacies in regions like Sub-Saharan Africa, Southeast Asia, and Latin America hinder the direct application of China's “rights confirmation–trading” model and may trigger legal disputes; significant technological capacity gaps, since accurate GEP accounting depends on high-precision remote sensing, ecological modeling, and robust data infrastructure that many countries lack—exemplified by Vietnam's GEP pilot in the Red River Delta, where estimation errors for regulating services exceeded 40% due to insufficient satellite data; and ideological differences, whereby the model's foundation in Marxist political economy, emphasizing state leadership in ecological value distribution, may clash with neoliberal governance traditions prevalent in regions like Latin America, potentially provoking legitimacy debates and resistance.

5.4 Collaborative innovation: toward capacity co-building and contextual piloting

Given these limitations and challenges, the global dissemination of China's experience must avoid a prescriptive export model. Instead, it should leverage platforms like the Belt and Road Initiative to foster collaborative mechanisms centered on “capacity co-building” and “contextual piloting.”

Technical standard cooperation should shift from promoting a single Chinese standard to fostering dialogue and interoperability. This could involve supporting the establishment of a ‘Global Ecosystem Accounting Partnership' with institutions like UNEP to develop tiered accounting standards accommodating different national capacities. For technologically constrained regions, a simplified “GEP-Lite” system could be co-developed, prioritizing high-value ecosystem services. The goal is to create bridges between China's GEP and other systems (e.g., EU's NCA, US's ESSA) to facilitate recognition and integration for developing nations in global markets.

Capacity co-building must move beyond one-way technical training toward co-designed programs addressing specific needs. Initiatives should include “policy clinics,” “simulation workshops,” and “sister-city/province partnerships” for long-term knowledge exchange. Customized training programs—such as specialized workshops on “Ecological Value Accounting and Green Finance” for African countries—can cultivate local talents with both ecological knowledge and market operation capabilities. As of 2023, China has trained over 2,000 technical personnel from 46 countries through such programs.

Joint innovation in risk-sharing mechanisms is also essential. International development banks (e.g., World Bank, AIIB) could partner with local institutions to pilot “Ecological Performance Insurance” or hybrid financing models tailored to regional risks. The Chinese experience serves as a proof-of-concept and starting point for dialogue, not a pre-defined product.

Regionally, mechanisms like Lancang-Mekong Cooperation can serve as testing grounds for cross-border ecological product value realization. Countries can jointly conduct cross-border forest carbon sink accounting, establish a “Basin Ecological Contribution Proportion Allocation Model,” and explore composite models of “ecological compensation + industrial cooperation” through negotiated benefit-sharing arrangements. For example, establishing a “Cross-border Biodiversity Conservation Special Zone” between Yunnan, China, and northern Laos—where Chinese enterprises handle carbon sink monitoring and trading, Lao communities undertake forest management, and benefits are shared equally—demonstrates a practical, adaptive approach to collaborative ecological governance.

6 Conclusion, policy implications and discussion

6.1 Conclusion

China's practice in realizing the value of ecological products has established a complete cycle from theoretical development to market transformation through the dynamic mechanism of concept movement. This research demonstrates that the transition of ecological products from natural gifts to factors of production is fundamentally a process of institutional reconfiguration involving the interaction between the labor theory of value and natural capital theory. Framed within a five-stage model that includes stipulation, unfolding, transformation, perfection, and realization, this process highlights the synergy between policy tools and technological innovation. Policy drives, such as the standardization of GEP accounting systems, establish institutional foundations for valuation. Market mechanisms, including the securitization of forest carbon sinks, reduce transaction costs through property rights definition. Technological advancements, for example through remote sensing monitoring and automated GEP accounting platforms, address practical bottlenecks in measuring ecological resources.

6.2 Policy implications

The theoretical framework and empirical findings presented in this study offer actionable insights for policymakers and practitioners. The five-stage model not only elucidates the intrinsic process of realizing ecological value but also serves as a diagnostic tool for systematic policy design and implementation. Based on the distinct roles of various stakeholders, the relevant policy implications can be articulated as follows:

For central government, the five-stage model can function as a strategic framework for national-level ecological governance, guiding differentiated policy design and resource allocation. It is essential to move beyond a one-size-fits-all approach and tailor policies according to regional development stages. Specifically, the central government can use this model to assess each region's current conditions—determining their respective stages through audits or self-evaluations—and provide phase-appropriate policy support. Less developed western regions in the “definition and entitlement stage” should receive focused capacity building and institutional foundations, including technical assistance and funding to establish ecological resource surveys and GEP accounting systems. Meanwhile, more developed eastern coastal regions in the “transformation” or “perfection” stages should be granted greater autonomy to experiment with market-oriented mechanisms, while the central government works to build a unified national ecological market environment, promote standardization of trading rules for carbon sinks, water rights, and pollution permits, and establish legal safeguards for ecological financial innovation.

For local governments, as key implementing agents in realizing ecological value, should advance the following operational priorities: The primary task is to construct municipal-level ecological asset registries and dynamic monitoring platforms, providing a reliable and transparent ecological data foundation for the “entitlement stage” to support subsequent accounting, trading, and compensation mechanisms. Simultaneously, performance evaluation systems for officials should be reformed, particularly in key ecological functional zones, where assessments must be closely linked to ecological indicators such as GEP growth rates, ecological asset conversion efficiency, and the success of market-based projects—shifting emphasis away from GDP-centric metrics. Furthermore, during the “unfolding” and “realization” stages, local governments should transition from direct intervention to market facilitation by establishing ecological banks or asset management companies to integrate fragmented resources, creating green finance guidance funds to attract private capital, and developing e-commerce platforms to expand markets for ecological products.

For enterprises and financial institutions, the transformation of ecological products into assets and capital presents significant opportunities. Companies should proactively integrate ecological value into their strategic planning: on one hand, using GEP accounting to quantify and disclose their impacts and dependencies on ecosystem services in ESG reports, thereby enhancing transparency and attracting green investment; on the other hand, actively exploring new business models in collaboration with governments, such as investing in eco-tourism operations, developing branded eco-agricultural products, or participating in public-private partnerships for ecological restoration. Financial institutions should innovate green finance products by developing credit instruments based on ecological asset income rights, including carbon sink pledge loans, water rights financing, and eco-tourism revenue-backed loans. They should also collaborate with insurers and governments to design risk mitigation instruments such as ecological performance insurance, which protects against shortfalls in expected returns due to natural disasters, thereby reducing investment risks and leveraging more private capital for ecological restoration.

6.3 Discussion

6.3.1 Theoretical breakthrough and contextual adaptation

This study employs concept movement theory to develop a dynamic framework for institutional innovation in ecological product value realization. While the findings offer significant theoretical and practical insights, several broader issues warrant elaboration, and certain limitations must be acknowledged.

Theoretically, the three-stage transformation model (natural resources → ecological assets → ecological capital) challenges market-centric paradigms in ecological economics. By extending the labor theory of value into ecological domains and emphasizing institutional embeddedness, our framework demonstrates that value creation depends fundamentally on socio-technical institutional arrangements rather than pre-existing market mechanisms. The case of Fujian's forest carbon tickets exemplifies this institutional construction—where deliberate designs like management rights separation and certificate registration reconfigure property relations, reducing transaction costs by over forty percent. This perspective aligns with evolutionary institutional economics, viewing ecological value realization as a co-evolutionary process involving institutions, technologies, and markets. The progression of Xin'an River basin compensation from single-index to multi-dimensional evaluation further illustrates the adaptive learning characteristic of the transformation and perfection stages, highlighting how concept movement theory effectively captures non-linear policy innovation.

Practically, China's experience provides a valuable yet context-dependent toolkit for Global South nations. The synergy between local pilot programs (e.g., Zhejiang's GEP accounting) and subsequent national standardization offers a replicable strategy for adapting global frameworks like TEEB to local conditions. However, successful transplantation requires careful contextual adaptation. The effectiveness of hybrid governance tools (e.g., ecological banks with carbon finance) depends on specific preconditions: state capacity for institution-building, technological capabilities, and political willingness to experiment with state-market synergies. In contexts lacking these prerequisites, initial efforts should prioritize capacity building and straightforward payment for ecosystem services before advancing to complex assetization mechanisms. The development of simplified GEP accounting models represents a pragmatic response to technical and operational constraints.

6.3.2 Limitations and future research directions

This study has several limitations that indicate productive avenues for future research. First, as an in-depth analysis of Chinese institutional innovation, its findings are inherently context-specific. While the theoretical frameworks offer adaptable analytical lenses, systematic comparative research contrasting China's GEP system with other approaches (e.g., TEEB implementation in Europe, PES schemes in Latin America) is needed to assess relative effectiveness and identify context-dependent success factors.

Second, the relatively recent emergence of these institutional innovations creates a temporal limitation. Their long-term sustainability, performance stability, and adaptability to changing socio-economic conditions require longitudinal study. Future research should track these cases over time to evaluate their resilience and ecological outcomes, moving beyond institutional potential to assess proven sustainability.

Third, we acknowledge the persistent methodological challenges in ecosystem service valuation. The GEP system represents a pragmatic, policy-driven attempt to standardize measurement for governance purposes—not a definitive scientific resolution to epistemological problems of valuation. Challenges of double-counting, cultural service subjectivity, and regulating service uncertainty remain active academic debates. Future work must continue to refine GEP methodologies, improve ecological modeling precision, and transparently address uncertainties to enhance scientific credibility.

Looking forward, two critical frontiers emerge from this work. First, developing cross-border ecological product trading mechanisms (e.g., Lancang-Mekong River basin collaboration) would test the international applicability of our framework, requiring unprecedented diplomatic coordination and mutual recognition of accounting standards. Second, integrating digital technologies like blockchain for rights confirmation and transactions could enhance the transparency and efficiency of ecological asset markets, potentially reducing transaction costs and enabling innovative decentralized governance models. These advancements could help transform ecological governance from localized innovation into global public goods.

Data availability statement

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author/s.

Author contributions

MY: Writing – original draft, Conceptualization. XZ: Methodology, Writing – original draft. RG: Resources, Writing – review & editing. YL: Formal analysis, Writing – original draft, Data curation. FZ: Supervision, Conceptualization, Writing – review & editing.

Funding

The author(s) declare that financial support was received for the research and/or publication of this article. This work was supported by the Science and Technology Project of Information and Communication Company of Gansu Power Company, State Grid of China (Project No. 52272323000C).

Conflict of interest

MY, XZ, and RG were employed by the Information and Communication Company of Gansu Power Company.

The remaining authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as potential conflicts of interest.

Generative AI statement

The author(s) declare that no Gen AI was used in the creation of this manuscript.

Any alternative text (alt text) provided alongside figures in this article has been generated by Frontiers with the support of artificial intelligence and reasonable efforts have been made to ensure accuracy, including review by the authors wherever possible. If you identify any issues, please contact us.

Publisher's note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Bank, E., Lange, S., Czucz, B., Hinsch, M., and Burkhard, B. (2025). Towards standardized ecosystem condition assessments: selecting agroecosystem condition indicators based on SEEA EA with an example application in Lower Saxony, Germany. Ecol. Indic. 177:113813. doi: 10.1016/j.ecolind.2025.113813

Brown, G., Pullar, D., and Hausner, V. H. (2016). An empirical evaluation of spatial value transfer methods for identifying cultural ecosystem services. Ecol. Indic. 69, 1–11. doi: 10.1016/j.ecolind.2016.03.053

Cai, H., and Chen, H. (2021). Political economics foundation of the theory of socialist ecological civilization:why it is necessary and possible. Contemp. Econ. Res. 1, 43–50 (in Chinese).

Christie, M., Kenter, J., Bullock, C., Bruen, M., Penk, M., Feld, C., et al. (2021). Evaluating the Multiple Values of Nature–ESDecide: From an Ecosystem Services Framework to Application for Integrated Freshwater Resources Management; Research Report.

Costanza, R., Arge, R., de Groot, R., Farber, S., Grasso, M., Hannon, B., et al. (1997). The value of the world's ecosystem services and natural capital. Nature 387, 253–260. doi: 10.1038/387253a0

Department for Environment FRA (2020). Enabling a Natural Capital 823 Approach(ENCA):Guidance Natural Capital Approach(ENCA):Guidance. London: DEPARTMENT FOR ENVIRONMENT F R A. Available online at: https://www.gov.uk/government/publications/enabling-a-natural-capital-approach-enca-guidance/enabling-a-natural-capital-approach-guidance (Accessed January 22, 2020).

Frantzeskaki, N., Slinger, J., Vreugdenhil, H., and van Daalen, E. (2010). Social-ecological systems governance: from paradigm to management approach. Nature + Culture 5, 84–98. doi: 10.3167/nc.2010.050106

Fu, L., Su, J., and Hu, Z. (2024). Study on carbon sequestration of bamboo forest in Zhejiang Province. J. Southwest Forest. Univ. 8, 68–73. (in Chinese).

Groot, R., Costanza, R., Braat, L., Brander, L., Burkhard, B., Carrascosa, J., et al. (2018). Ecosystem services are nature's contributions to people: response to: assessing nature's contributions to people. Sci. Progr. 359, 1–7. doi: 10.1126/science.aap8826#elettersSection

Hai, M., and Huan, Q. (2022). Ecological products and their value realization in the perspective of marxist ecology. Marxism Reality 3, 119–127. doi: 10.15894/j.cnki.cn11-3040/a.2022.03.015

Harrison, P. A., Dunford, R., Barton, D. N., Kelemen, E., Martín-López, B., Norton, L., et al. (2018). Selecting methods for ecosystem service assessment: a decision tree approach. Ecosyst. Serv. 29, 481–498. doi: 10.1016/j.ecoser.2017.09.016

Hua, Z., and Tong, W. (2023). Gross ecosystem product (GEP): Quantifying nature for environmental and economicpolicy innovation. Ambio 52, 1952–1967. doi: 10.1007/s13280-023-01948-8

Igoe, J. (2014). “Nature on the move II: contemplation becomes speculation,” in Nature Inc.: Environmental Conservation in the Neoliberal Age, eds B. Büscher, W. Dressler, and R. Fletcher (University of Arizona Press), 205–221. doi: 10.2307/j.ctt183pdh2.12

Islar, M. (2019). “Policy options and tools for decision makers. IPBES, Global assessment report on biodiversity and ecosystem services of the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services,” in Global Assessment Report on Biodiversity and Ecosystem Services https://www.ipbes.net/system/tdf/ipbes_global_assessment_chapter_6_unedited_31may.pdf?file=1&type=node&id=35282

Ji, F. (2022). Exploration of “quasi-market” governance of river basins and realization of ecological product value. Gansu Soc. Sci. 5, 206–216. doi: 10.15891/j.cnki.cn62-1093/c.2022.05.023

Ji, J. Y., Zhu, T. S., Jia, C. G., Fan, Y., and Song, Y. T. (2025). Testing ecosystem accounting in northern China - a case study of SEEA EA in Liaoning Province. J. Environ. Plann. Manag. 68, 751–772. doi: 10.1080/09640568.2023.2269473

Jin, C., and Lu, Y. (2021). Review and prospect of research on value realization of ecological products in China. Econ. Geogr. 41, 207–213. doi: 10.15957/j.cnki.jjdl.2021.10.023

Kosoy, N., and Corbera, E. (2010). Payments for ecosystem services as commodity fetishism. Ecol. Econ. 69, 1228–1236. doi: 10.1016/j.ecolecon.2009.11.002

Kumar, P. (2010). The Economics of Ecosystems and Biodiversity: Ecological and Economic Foundations. London: Earthscan.

Li, P., and Ouyang, Z. (2021). Study on financial innovation in realizing the value of ecosystem products. Dev. Finan. Res. 3, 88–96. doi: 10.16556/j.cnki.kfxjr.2021.03.005

Ma, X., He, R., and Hong, J. (2020). Exploration on the path to realize the value of ecological products. Study Pract. (2020) 3, 28–35. doi: 10.19624/j.cnki.cn42-1005/c.2020.03.003

Manes, F., Buonocore, E., Paletto, A., and Franzese, P. P. (2022). natural capital, ecosystem services, and environmental accounting. J. Environ. Account. Manag. 10, 215–217. doi: 10.5890/JEAM.2022.09.001

Martin, A., Coolsaet, B., Corbera, E., Dawson, N., Fisher, J., Franks, P., et al. (2018). “Land use intensification: The promise of sustainability and the reality of trade-offs,” in Ecosystem Services and Poverty Alleviation: Trade-offs and Governance (1 ed.), eds K. Schreckenberg, G. Mace, and M. Poudyal (London: Routledge). Available online at: https://www.taylorfrancis.com/books/e/9780429016295

Martinez-Harms, M. J., Bryan, B. A., Balvanera, P., Law, E. A., Rhodes, J. R., Possingham, H. P., et al. (2015). Making decisions for managing ecosystem services. Biol. Conserv. 184, 229–238. doi: 10.1016/j.biocon.2015.01.024

Marx, K. (1992). Capital: A Critique of Political Economy, 3 Vols. Chicago Charles H Kerr & Company.

OuYang, Z., Lin, Y., and Song, C. (2020). Research on Gross Ecosystem Product (GEP):case study of Lishui City, Zhejiang Province. Environ. Sustain. Dev. 45, 80–85. doi: 10.19758/j.cnki.issn1673-288x.202006080

Ouyang, Z., Song, C., Zheng, H., Polasky, S., and Daily, G. C. (2020). Using gross ecosystem product (GEP) to value nature in decision making. Proc. Natl. Acad. Sci. 117:201911439. doi: 10.1073/pnas.1911439117

Ouyang, Z., Zhu, C., Yang, G., Xu, W., Zheng, H., Zhang, Y., et al. (2013). Gross ecosystem product: concept, accounting framework and case study. Acta Ecol. Sin. 33, 15.(In Chinese). doi: 10.5846/stxb201310092428

Qi, Y. (2025). Can GEP Accounting Promote Corporate R&D. Finan. Econ. Res. 40, 89–100. (in Chinese).

Rey-Valette, H., Mathé, S., and Salles, J. M. (2017). An assessment method of ecosystem services based on stakeholders perceptions: The Rapid Ecosystem Services Participatory Appraisal (RESPA). Ecosyst. Serv. 28, 311–319. doi: 10.1016/j.ecoser.2017.08.002

Shi, M., and Chen, L. (2022). Theoretical connotation and practical challenges of GE, accounting in China. Chin. J. Environ. Manag. 14, 5–10. (in Chinese). doi: 10.16868/j.cnki.1674-6252.2022.02.005

Spash, C. L., and Aslaksen, I. (2015). Re-establishing an ecological discourse in the policy debate over how to value ecosystems and biodiversity. J. Environ. Manag. 159, 245–253. doi: 10.1016/j.jenvman.2015.04.049

Sun, B. (2023). To establish the mechanism for realizing ecological product value: difficulties and optimization paths. Tianjin Soc. Sci. 4, 87–97. doi: 10.16240/j.cnki.1002-3976.2023.04.017

Tinch, R., Ankamah-Yeboah, I., and Armstrong, C. W. (2021). Exploring perspectives of the validity, legitimacy and acceptability of environmental valuation using Q methodology. J. Ocean Coast. Econ. 8:12. doi: 10.15351/2373-8456.1151

Tom, G., and Read, R. (2015). Where value resides: making ecological value possible. Environ. Ethics 37, 321–340. doi: 10.5840/enviroethics201537331

United Nations European Commission, Food and Agriculture Organization of the United Nations, Organisation for Economic Co-operation, and Development, and World Bank Group. (2021). System of Environmental-Economic Accounting—Ecosystem Accounting. New York, NY: United Nations. Available online at: https://seea.un.org/ecosystem-accounting