Abstract

The current housing affordability crisis, driven mainly by the financialization of housing and the government's retrenchment of social policies and provision of affordable housing, have affected growing inequalities in access to housing. The crises have hit young people especially hard. The recent trends call for systematic studies on the mechanisms generating such intergenerational inequality, considering the specifics of the prevailing housing regimes. Housing affordability in Tallinn has decreased due to fast-growing housing prices, as a result of an ultra-liberal housing regime, exemplified by housing financialization, capital accumulation, low level of governmental interventions and an overall increase in social inequalities. Based on EU-SILC data, it is shown how the recent trends during the decade between 2010 and 2020 have negatively impacted young people's access to homeownership—access has been greatly reduced for young cohorts, and it has become more differentiated, based on the socio-economic and labor market performance of households, as well as intergenerational transfers. Young households are increasingly residing in private rental dwellings, and many still rely on parental housing until their 30s. Rental housing, as compared to homeownership, has fewer advantages compared to homeownership—it brings no capital gains and is less secure, and rental stock tends to be located unevenly across urban space and to be in slightly worse condition compared to owner-occupied housing. This positions young people in an unfavorable position in the perspective of their housing career, and this can have severe consequences on their social inclusion.

Introduction

For most people, housing has become the greatest expenditure item in their household budget. It is also the main driver of wealth accumulation for a large share of households (Quigley and Raphael, 2004; Fuller et al., 2020). Due to these financial matters housing has become one of the key drivers of inequality and socio-spatial segregation in contemporary cities (Tammaru et al., 2016b). Housing, and the neighborhood in which people live, can also have important implications for individual health, employment and educational outcomes, often leading to a “vicious cycle of housing inequality” in terms of social inclusion (van Ham et al., 2018; Tammaru et al., 2021)—the effects of which can begin in childhood and last a lifetime or even over subsequent generations (Arundel, 2017; Manley et al., 2020). The housing market may become a more significant barrier to social inclusion for some groups, such as low-income and migrant background households, children, youth or seniors. Housing inequalities manifest in locational disadvantages driving the concentration of vulnerable groups into socially and spatially disadvantaged areas (James et al., 2022).

The growing pressure on housing prices in areas with intense labor markets, as well as the COVID-19 pandemic and the energy crises have furthermore generated housing-related inequalities (Wetzstein, 2017; Seebauer et al., 2019; Waldron, 2022). The dominating trend (especially up to the mid-2010s) in European countries has been the decreasing role of public expenditure on supply-side housing measures, manifesting in reduced shares of social housing in most countries (OECD, 2022). In parallel, there has been an increase of public expenditure on demand-side housing measures—public expenditure on universal or income-based social benefits, i.e., housing and energy allowances, which rather than improving housing affordability tend to lift up housing prices (Caturianas et al., 2020). Only from the 2010s there has been a slow but noticeable turn in governmental perspectives on housing policy—governments have increasingly started to question the “neoliberal” approach and a few policy efforts to tackle the declining housing affordability have been made (Bohle and Seabrooke, 2020; Kadi et al., 2021).

Following the global financial crisis, the private rental sector has witnessed exceptional growth at the expense of younger households who are lacking access to homeownership due to high prices and restrictive lending conditions by banks (Wetzstein, 2017; Waldron, 2022). Young people increasingly have to rely on market-price rental dwellings (Smith et al., 2022), or rely on their parents' housing for a prolonged period of time (Schwanitz et al., 2021).

The faith in neoliberal housing markets, and economic system in general, has also been the prevailing trend in Estonian socio-political system over the past three decades. The government has mostly withdrawn from regulating the housing market (Kährik and Kõre, 2013). Next to the predominant home-ownership sector, the private rental sector, which mostly functions as an un-official “black-market”, has grown since the 2000s considerably (Lux et al., 2012). This has been established primarily based on private individuals who have accumulated their wealth by investing in more than one property and let out their vacant dwellings. After the economy recovered from the 2008 to 2010 recession, there has been a rapid increase in housing prices in Tallinn; in parallel the wage gap and socio-economic inequalities also have increased, resulting in growing socio-spatial segregation (Tammaru et al., 2016a). The increase slowed during the COVID-19 pandemic (2020–2021), but the prices continued growing afterwards. Young people's wages are much lower and their unemployment levels are twice as high than the older working age groups (UPLIFT Urban Report Tallinn, 2022).1

In this context of growing housing affordability challenges and increasing social and housing inequalities, our study focused on the housing market outcomes for young people in Tallinn urban area during the 2010s. Our aims were to find out, first, to what extent have young people been affected by the affordability challenges in accessing homeownership (and the associated inequality patterns among the same age group), and second, whether this differential access has manifested itself in growing inequalities in terms of housing conditions and residential patterns. The three questions we aimed to answer are: (1) To what extent has the access to homeownership for young household been affected by the changes on the housing market? (2) Has access to homeownership over time become more differentiated based on socio-economic, demographic and ethnic factors? and (3) To what extent has the tenure-based sorting been reflected in locational patterns as well as in housing quality differences?

Based on the background described, we can assume a growing differentiation in entering homeownership between cohorts, as well as growing intersectional differences among young people where social inequalities translate into housing inequalities, which in turn has an impact on social inclusion in different life domains.

In the analysis we compared the two cohorts of young people, those aged 20–34 in 2010, and (b) those aged 20–34 in 2020 (i.e., a different cohort), and their achievements in the housing market—whether they have entered homeownership or have continued to rely on the rental market (both private and public) in Tallinn urban area. The binary regression analysis was based on EU-SILC data for Tallinn in 2010 and 2020.

The analysis demonstrates that entering homeownership was clearly more challenging for young people in 2020 as compared to the decade before and, furthermore, the socio-economic inequalities among the youth link to housing market outcomes to a greater extent. Differences by tenure status have a less clear link to the quality of housing as perceived by residents, and the locational impacts are not as straightforward, since a significant part of rental stock where young people live is found in the inner city but also in the outskirts. However, the more affordable rental housing is predominantly found in the high-rise outskirts of the city where young people with lower incomes tend to live.

Housing affordability and access to homeownership

The concept of housing affordability

Affordability is used to express the challenge each household faces in balancing the cost of its actual or potential housing, and its non-housing expenditures, within the constraints of its income (Stone, 2006). According to Haffner and Heylen (2011, p. 593) housing affordability can refer to “short-term affordability”, referring to financial access to a dwelling, and “long-term affordability”, which concerns the cost of housing consumption. Both types of affordability influence access to the housing market and decisions made during the housing career, such as opting for either homeownership or renting a dwelling, or the different size, state-of-repair or location of a dwelling. Housing affordability can refer to the ability to obtain a mortgage, the income situation of a household in relation to their housing expenditure or, from a structural perspective, the conditions affecting the supply of housing or public policies affecting housing accessibility (Stone, 2006).

Although problems with housing affordability tend to be more frequently experienced by renter households as their income tends to be lower in average, owner households may occasionally pay higher share of their income when the interest rates increase or when they actually pay for housing more than they realistically can afford (Bogdon and Can, 1997). Housing affordability literature generally says that the maximum a family should pay for housing is 30% of their income (Bogdon and Can, 1997; Kutty, 2005). However, the lowest income households may not even afford to spend a quarter of their income on housing (Stone, 1990, 1993).

In many Western societies, ownership is perceived as a social norm for life qualities and the option to meet lower housing costs in a longer perspective (Foye et al., 2018). The social pressure for ownership in certain age and stage of life may force households to choose higher housing costs to enter ownership. Depending on the available opportunities on the rental market, ownership may be an option to meet higher housing standards (Stone, 2006).

Housing affordability is thus a complex phenomenon related to various individual and structural factors: income, housing prices, demand and supply in the housing market, policies and land-use planning restrictions but also household decisions, miscalculations in assessing the income and housing costs in longer run (e.g., Calder, 2017).

Differences in housing affordability manifest in different types of inequality (e.g., Dewilde and De Decker, 2016; James et al., 2022). Haffner and Hulse (2021) argue that the concept of housing affordability should refocus away from the role of housing costs in contributing to disadvantages in social services and toward the urban policy challenges of growing inequities in accessing urban resources.

The most commonly used measure of housing affordability in relation to accessing housing is the criterion of housing price-to-income ratio which is calculated from the total housing price. From the long-term housing consumption point-of-view, a housing affordability problem is recognized (either statistically or in relation to housing policies) when a household's spending on housing as a proportion of its total income exceeds a certain threshold (Hulchanski, 1995). For example, Eurostat considers a household to be “housing-poor” or overburdened by housing costs if the expenditure-to-income ratio exceeds 40%, measured by the equivalized disposable income of household.

Housing affordability crises—financialization of housing markets

Rents and housing prices have increased over the past decades across Europe while wages have lagged behind, decreasing housing affordability. This has been mainly related to the accelerated (re)urbanization of capital and people, the provision of cheap credit, the austerity policies pursued by governments, and the rise of social inequality in society (Lennartz and Ronald, 2017; Ronald and Dewilde, 2017; Wetzstein, 2017; Whitehead and Goering, 2021; James et al., 2022). Also, housing-related household expenses have increased and households are dedicating an increasingly larger share of their budget to housing costs (Anacker, 2019; Fuller et al., 2020). Housing financialization, which has been the dominant trend across Europe since the 1990s, has been increasingly dependent on the global financial markets, and especially the financial markets for mortgages (Wetzstein, 2017; Fikse and Aalbers, 2021).

Governmental support measures to alleviate or prevent housing poverty have greatly reduced since the 1990s up until the 2010s, along the paradigm of the neo-liberalization of housing markets. Public subsidies have mostly supported homeownership. As a result, mortgage lending became deregulated, governmental funding for affordable housing has declined considerably across Europe (Lennartz and Ronald, 2017; Ronald and Dewilde, 2017; Caturianas et al., 2020). The social housing sector has become more residualized, increasingly providing accommodation only to those of the lowest incomes (Whitehead and Goering, 2021). The most dramatic drop of social housing and the governments' withdrawal from the regulation of the housing market took place in the former socialist countries (Hegedus et al., 2013; Lux and Sunega, 2014). Governments have shifted to paying more universal or income-based social benefits to households, such as housing and energy allowances. Also, schemes have often been used to reduce the tax burden on homeowners—home buyers have been supported by tax measures.

As a result of these trends, housing has been transformed into a financial asset or commodity affecting also the perceptions, meanings and discourses around housing ownership (Arundel and Ronald, 2021; Fikse and Aalbers, 2021). Housing is being increasingly viewed as an investment rather than a home—households are becoming “a frontier of capital accumulation, not just as producers and consumers, but also as financial traders” (Smith et al., 2022), undermining the stability of homeowner realities and practices (Fikse and Aalbers, 2021). Increasing house-price volatility is undermining the security of the homeownership tenure (Dewilde and De Decker, 2016; Arundel and Ronald, 2021).

In the 2010s, after the global financial crises, the need to respond to the affordability crises and growing segregation levels in cities has forced governments to apply new measures to tackle the growing inequalities. It has even been debated whether the new era of “post-neoliberalism” has arrived in the approach to housing policies (Kadi et al., 2021). New regulations to protect tenants from rent increase, the regulation of mortgage lending, newly constructed municipal housing programs, non-profit housing developments and subsidy programs as well as more social mix in new developments have been examples of new approaches applied across many European countries, e.g., in Germany, Austria, Hungary and Ireland (Bohle and Seabrooke, 2020; Kadi et al., 2021). Recently, mortgage interest tax reliefs have been phased out or abolished in several European countries (Caturianas et al., 2020). The new measures have brought some alleviation to the affordability crises however the housing prices continue to skyrocketing.

As a result of the prescribed trends access to homeownership has been in decline and inequalities based on the concentrations of housing wealth are increasing since homeowners accumulate more wealth than tenants (Wind and Dewilde, 2019; Arundel and Ronald, 2021). While many homeowners, investors and speculators have accrued financial gains from the “asset-based” housing market conditions, increasingly higher numbers of households are facing severe consequences (Lennartz and Ronald, 2017). The financialization of housing and urban restructuring tend to affect lower and middle-income households in cities (Haffner and Hulse, 2021). New spatial and social inequalities have emerged as a result of the concentration of housing wealth, while access to homeownership has become more differentiated. The rise of short-term accommodation platforms, such as Airbnb, add to the falling rate of homeownership by reducing supply of housing for local residents as well as raising housing costs (Caturianas et al., 2020). Arundel and Lennartz (2020) discuss housing inequality outcomes as growing divides between “high-gain ‘hotspot' markets and more peripheral ‘cooler' markets”. Housing unaffordability tends to drive vulnerable groups to move to more disadvantaged areas (James et al., 2022)—the spatial manifestations of housing inequalities in the form of residential segregation and its consequences have been discussed by many authors (Hochstenbach, 2018; Arundel and Hochstenbach, 2020; Le Goix et al., 2021).

While housing has increasingly been seen as an investment asset, the private rental sector has also expanded in response to the financialized homeowner societies initiated by the institutional investment interests (Fields and Uffer, 2016; Aalbers et al., 2021; Aigner, 2022). Private renting has been considered to be the fastest growing tenure (Wetzstein, 2017). Following the global financial crisis, the private rental sector has witnessed exceptional growth as access to homeownership is increasingly denied for younger households due to high prices and restrictive lending (Ronald, 2018; Fuster et al., 2019). Private rental sector has often considered as an insecure and precarious tenure since it is usually characterized by weak protection of tenants, limited duration contracts (which is especially problematic for families who are less flexible in terms of moving) and few restrictions on rent setting (Huisman and Mulder, 2022; Waldron, 2022).

The housing affordability crisis is being further exacerbated by the energy crisis. Low-income groups are at the highest risk of energy poverty (i.e., household is unable to secure the socially and materially needed level of energy service in the home)—as they tend to live in low-quality and inefficient multi-storey rental housing in cities and in times of surging energy prices (Seebauer et al., 2019; Bouzarovski et al., 2021).

Despite the described common trajectories in housing markets across Europe driven mainly by global financial markets and “neo-liberalization”, institutional and local differences between countries remain significant (Wind et al., 2017; Anacker, 2019; Wijburg and Waldron, 2020). Housing systems and the degree of financialization vary between countries, even among those which are often grouped together based on their ideological orientations or existing welfare systems (Stephens, 2020; Lee et al., 2022). Housing systems affect the tenure structure and the distribution and cost of housing and, in turn, the accessibility which mediates the link between social inequality and housing inequality (Arbaci, 2007; Wijburg and Waldron, 2020). Housing cost overburden is a particularly significant problem in Greece and some of the Balkan countries (Caturianas et al., 2020). In societies with poorly regulated market-based systems, tenants experience more of an economic burden related to their housing than homeowners (James et al., 2022).

Young adults and other vulnerable groups

Staying in rental housing can also be considered as a choice for young people related to their life-course stage (Mulder, 2007), as there may be a reluctance to take up long-term financial obligations, especially when studying or the employment situation is still insecure. This has also been discussed by Arnett (2000) when referring to the phenomenon of “emerging adulthood”. Emerging adulthood is used to describe a period from about ages 18–29, experienced by most people in their twenties in Western cultures marking the starting point of an independent life moving apart from the childhood home. Arundel and Ronald (2016) have shown that emerging adults in Western societies tend to postpone events generally associated with the start of independent adult life such as the finishing of education, marriage, and financial independence from parents. It also translates into the later access to home ownership. Various studies have shown that the attainment of independent housing is replaced by more flexible, adaptable housing “arrangements” such as shared living and periods of parental co-residence (Hochstenbach and Boterman, 2015; Arundel and Ronald, 2016).

Starting one's housing career is an expensive activity and young people without parental support often struggle with paying a deposit or downpayment, as they usually do not have a previous dwelling to sell or use as collateral to obtain a mortgage. The differentiated access to higher quality housing and different housing tenures has become more pronounced according to the socio-economic, demographic and ethnic characteristics of households (Wiesel, 2014; Dewilde and De Decker, 2016). Housing inequality occurs within and between different population groups. Affordability gaps are particularly pronounced among low-income households, renters in the private sector, and youth—the effects of which are multiplied in case of accumulated disadvantages. Low-income groups, especially minority ethnicities and those with migrant backgrounds, are more likely to encounter poor quality housing and to reside in rental tenures as a result of poor access to ownership (e.g., Lukes et al., 2019; Soaita and Mckee, 2019). Also, an increasing share of the middle-class face affordability issues (Caturianas et al., 2020). In 2018, almost 40% of households at risk of poverty spent more than 40% of their disposable income on housing, and about one third of tenants whose rent was at market price perceived overburden, whereas among homeowners the rate was <5% (Caturianas et al., 2020). Housing inequality patterns have become more persistent over time, and over generations.

The house price inflation has hit the chances of young people in the housing market especially hard. Their material ability to start an independent housing career or step into homeownership from the rental sector has worsened, and the role of parental wealth has risen (Ronald and Lennartz, 2018). Entering homeownership has been postponed for many young households; there is a deepening structural gap for moving from the parental home to owning or renting one's own home (Forrest and Hirayama, 2018; Ronald and Lennartz, 2018; Arundel and Ronald, 2021). The differential between the younger adults (under-35s) compared to the more established over-45s has widened over time. The rates of owner-occupation among the young are shrinking disproportionately (Smith et al., 2022). In the US, Clark (2019) finds the share of young people in homeownership to be at the lowest level in half a century.

Young people are also more exposed to experience the risk of housing cost overburden compared to the older generations. However, the risk tends to be lower for young people in countries where they tend to leave home at much higher age (Southern Europe or some former socialist countries) (Schwanitz et al., 2021). Acquiring homeownership has become increasingly family-dependent and intergenerational and, as a result, more unequal, as not everyone can rely on intergenerational transfers and inheritances (Arundel, 2017; Cigdem and Whelan, 2017; Lennartz and Helbrecht, 2018; Hedman and van Ham, 2021).

Housing affordability in relation to social inequality and social inclusion

Housing inequality is often a function and outcome of social inequality and labor market outcomes, and it can also produce new inequalities (Filandri and Olagnero, 2014; Wind et al., 2017; Arundel and Lennartz, 2020). Housing is considered the key element that structures social and spatial inequalities in cities (Sorando et al., 2021). Households marginalized in the least desirable housing and neighborhoods have less access to high quality schools and job opportunities. Exposure to concentrated poverty reproduces itself over generations and, hence, segregation is also reproduced (van Ham et al., 2018). Young families with children, as well as the elderly, can be particularly disadvantaged by their housing and neighborhood situation, because they are often more bound to the residential neighborhoods in which they live. The implication of housing inequalities for younger people can also relate to the decision to have children. There is a strong intergenerational transmission of poverty and living in poverty neighborhoods from parents to children (De Vuijst et al., 2017; Hedman et al., 2017).

Housing is key to inclusive growth (OECD, 2020). Spending too much on housing in relation to income can have severe consequences on individuals—it can reduce investment in education, healthcare and other fields, leading to exclusion and a vicious circle of segregation and housing (OECD, 2020). For many households housing “may eat up so much of their income that their food choices, healthcare needs, educational prospects and sustainable commuting options are heavily compromised” (Wetzstein, 2017, p. 3160).

The “vicious circle of segregation” occurs through the transmission of effects from one domain to another—e.g., the sorting of people into certain types of houses and neighborhoods affects school choices as well as employment opportunities, as the location of homes affects access to schools and jobs. The way housing and tenure structures are distributed in urban space, and how this distribution is mediated by the institutional set-up can be considered as a crucial factor affecting housing inequality (Torpan et al., 2020; Friesenecker and Kazepov, 2021). The vicious circles of housing inequalities suggest that housing and locational disadvantages experienced early in life are often reproduced later in life and transmitted from parents to children (Tammaru et al., 2021; van Ham et al., 2021). Housing inequalities can thus have a negative effect on the probability of the upward social and spatial mobility of individuals.

Likewise, measures taken up at the household level to keep housing costs under control can negatively affect health, children's educational attainment and occupational opportunities, which can have especially severe impacts on the young. The more time spent at home (e.g., working from home and distance learning during the COVID-19 pandemic) means greater exposure to higher energy costs and, in case of lower quality housing standards, higher exposure to possible health risks.

Tallinn: housing and residential context

Housing market dynamics and housing policies in Tallinn

After the renewal of Estonia's political independence in 1991, there was a faith in neoliberal market mechanisms in the housing market alongside the withdrawal of state from its regulation (Kein and Tali, 1995; Tammaru et al., 2016a). This political-ideological view led to the adoption of the market-liberal model of housing provision, consumption, and finance (Saunders, 1990; Ronald, 2008) in Estonia. The belief in “homeownership” as the preferred tenure has been guiding the prevailing housing policy since privatization, making Estonia a typical “homeowner society” for decades. The privatization took place in the 1990s and was completed by 2000 (Kährik, 2000). The reforms were generous to all who had resided in public subsidized rental dwellings when the reforms started and whose dwellings were not subject to restitution (Lux et al., 2012).

By the end of the reforms, the rate of homeownership in Estonia was superhigh (close to 96%) (compared to 39%, in 1992). The ownership reform paved the way for relatively egalitarian tenure distributions in socio-economic terms, although the extent to which homeowners gained from the reforms varied widely, depending on the location and condition of the building/apartment. This ranged from those living in low-value properties and had to incur high expenditures to maintain their properties to those occupying high market value properties in prosperous neighborhoods of growing cities. These gains have now manifested in intergenerational inequalities as the privatized units are transferred from parents to children.

The homeownership society created by mass privatization could not sustain for a long time. By the turn of the millennium, and even 10 years later the homeownership rate had come down (to 83% by 2000 and 80% by 2010 in Tallinn based on census data) but was still relatively high since the global financial markets and national incentives were supportive for the tenure. The more dramatic tenure shift took place during the 2010s. By 2021, according to the census, 70.4 of the population were owning their dwelling in Tallinn, down by 10% compared to 2010 (in Tallinn urban region, including also the commuting zone, the rate was 76%). The provision of affordable rental dwellings (referred to as social or municipal housing in Estonia) only accounts for 2% of the total housing stock in Tallinn, so its impact on affordability has been rather modest. The sector mostly caters to either those with additional needs (e.g., disabled) or “young families” and “workers vital to the city” (e.g., nurses, teachers) (Kährik and Kõre, 2013). Between 2002 and 2012 two new social housing construction programs were also implemented in Tallinn. Building new municipal housing was meant to address the lack of housing affordability issue in the city and to decelerate the rapid inflation of housing prices. Altogether nearly three thousand new rental dwellings were constructed with the first program addressing mainly the need to resettle tenants of restituted housing, while the second program aimed at offering modern living space for the labor force needed for the city (so called “key workers”) and improving the housing conditions of young families.

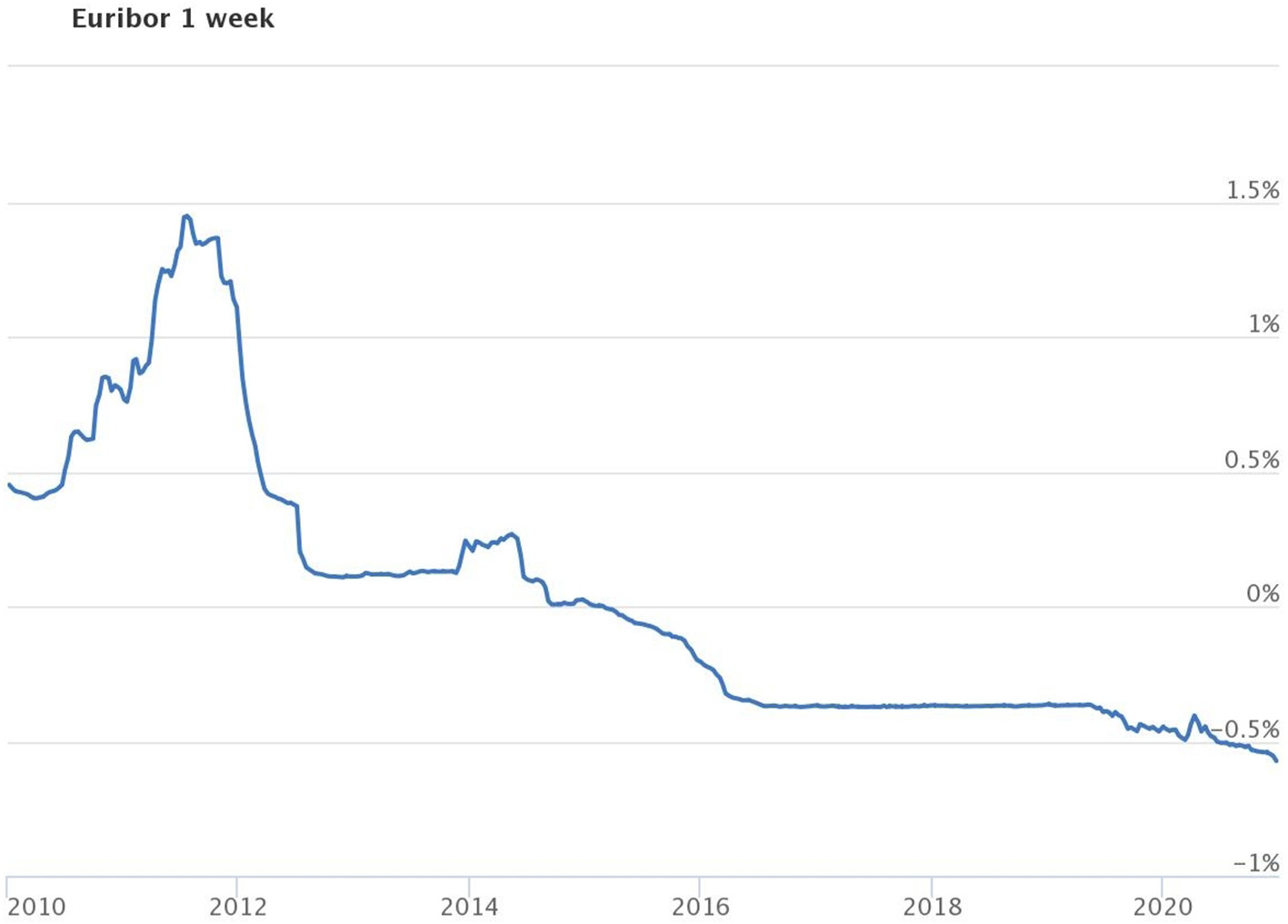

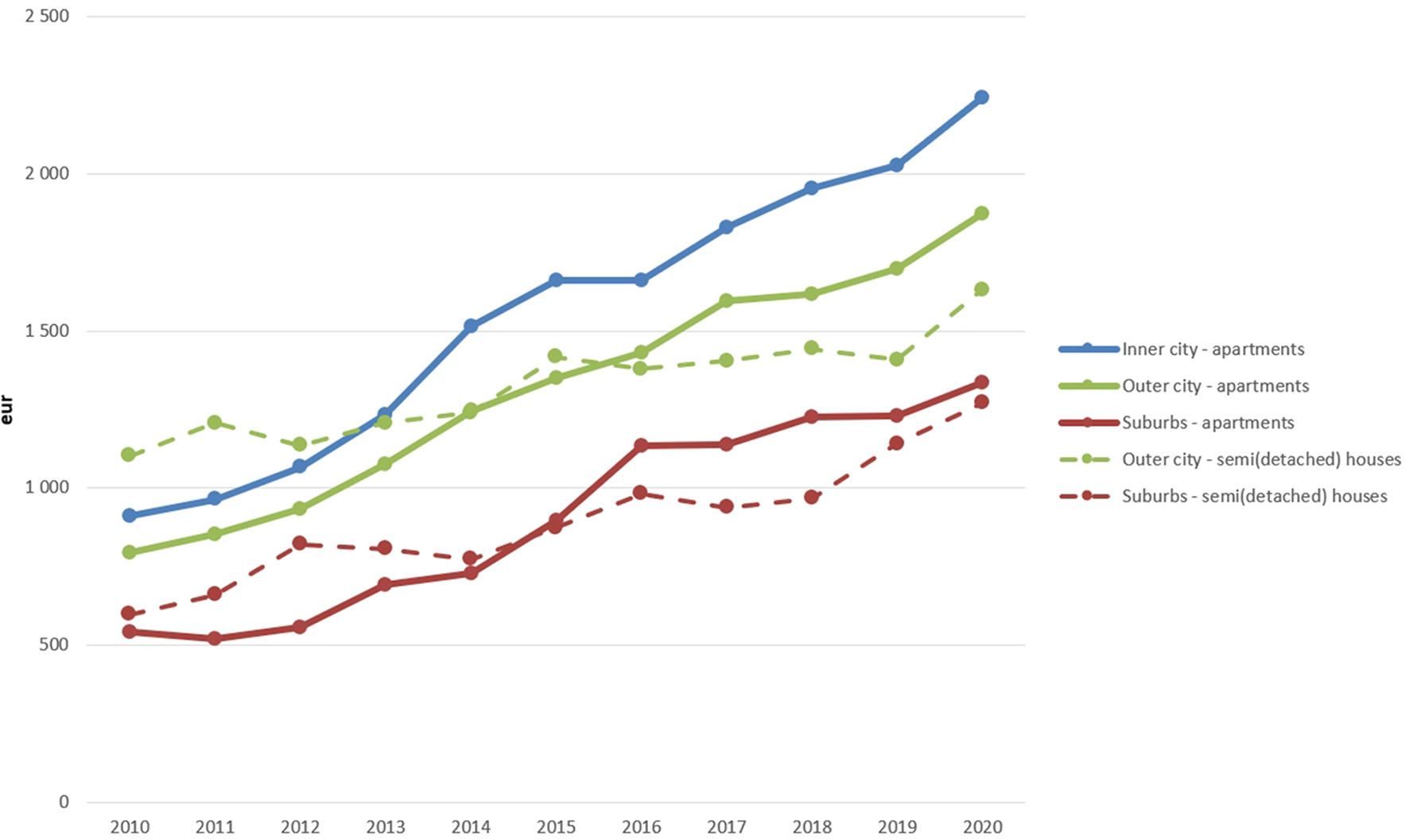

The rate of Euribor,2 which is affecting the interest rate when issuing housing loans the most, has been very low since 2005 (Figure 1), making borrowing in general very attractive to households, although the economic cycles have also had a significant effect on borrowing conditions. Since March 2015, Euribor has been below zero, which has further increased borrowing and reduced monthly expenses related to mortgages. At the same time, low Euribor rates have not guaranteed better financial access to housing for younger age groups, because the downpayment to obtain a loan has substantially increased as the housing prices have increased (Figure 2). Prices for apartments have increased more than for detached or semi-detached houses. Banks have also tightened lending requirements, such as setting higher criteria for the borrower's monthly income or increasing the deposit required for a mortgage.

Figure 1

Euribor one week value from 2010 to 2020 (Source Euribor-rates.eu).

Figure 2

Housing median price per square meter in Tallinn urban region (Data source_Estonian Land Board 2023).

The price-boom has also affected the number of residential property transactions. After the increase between 2010 and 2016 (apartments in the inner city by 51%, in the outer city by 65%, and suburban areas by 58%), the number of sales of apartments has slowed down since then. Housing prices rose rapidly after the market recovered from the 2008 to 2010 economic crises, but the average income has not been able to keep up. Apartments in the outer city are to a larger extent, located in high-rise panel housing estates that are more affordable than apartments in the inner city and outer-city low-rise areas, and are preferred by young people and lower-income groups (Mägi et al., 2016; Kährik et al., 2019). Detached and semi-detached houses in city fall in the relatively high price range and are characterized by low affordability.

At the same time the number of transactions for suburban housing has increased throughout the period almost twice. It is also recognizable that, in Tallinn's suburbs, the number of sales of detached and semi-detached houses is more than five times lower than the number of apartments, which illustrates the high volume of moving into apartments in Tallinn's suburban area.

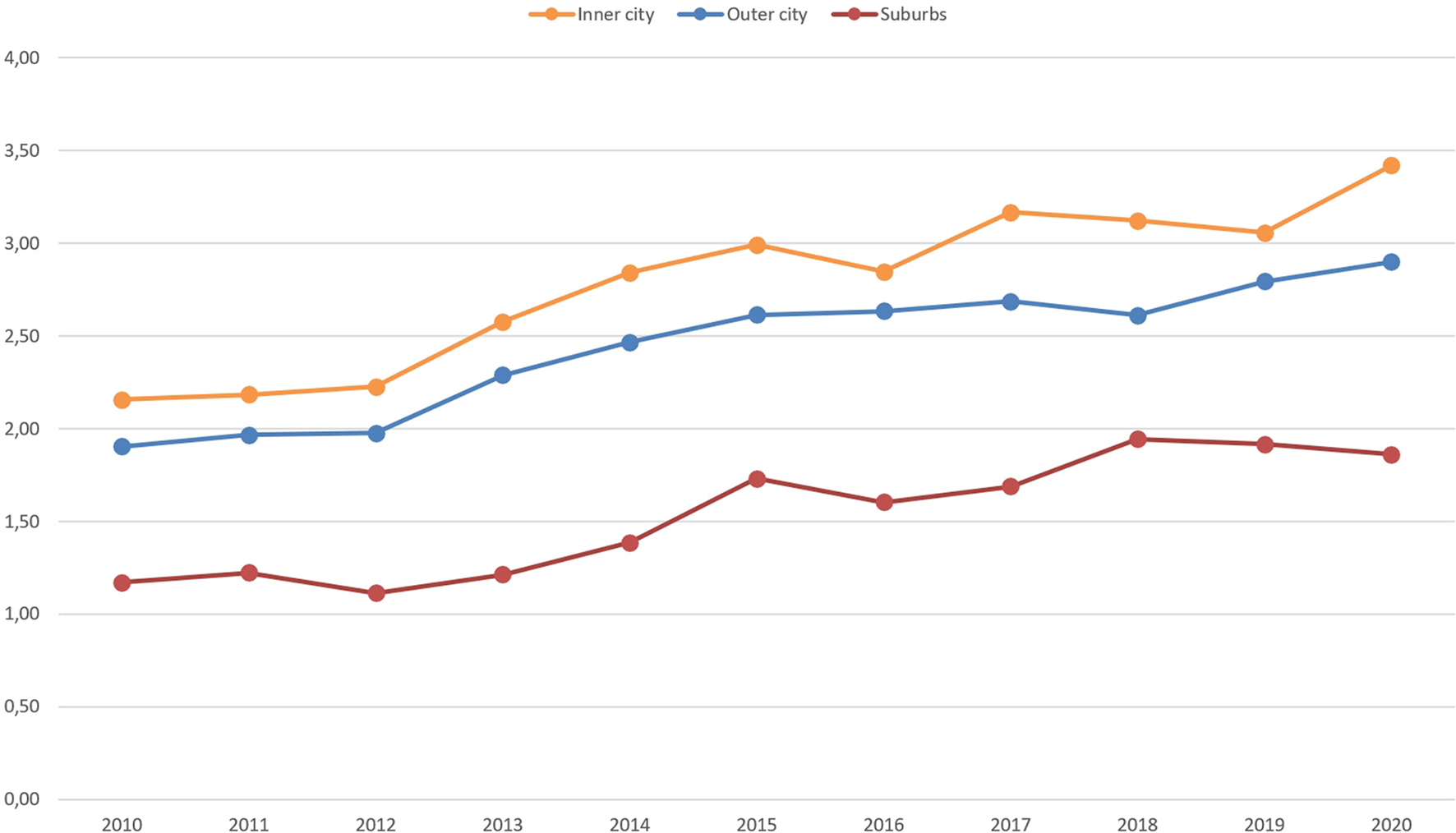

The housing price-to-income ratio for Tallinn urban region demonstrates a rising trend (Figure 3). Housing price-to-income ratio was calculated by multiplying the price per square meter of a two room (one bedroom) apartment by the average size of a two room (one bedroom) apartment and dividing with the yearly net income of a two-person household in the area (city district or local municipality). The differences in housing price-to-income ratios are remarkable between the inner city and the outskirts. Outer city apartments are in average by 25 percent more affordable than in the inner city while the suburban apartments are twice more accessible on average as in the inner city.

Figure 3

The housing-price-to-income-ratio. Data source_Population Statistical Register, 2023_Estonian Land Board 2023.

Among housing policy measures, the most common are subsidies that support existing or prospective homeowners (such as extra guarantees on mortgages, tax relief to facilitate home ownership), and which are more likely to benefit medium- and higher-income households. The state's fiscal policies to stimulate property ownership in the housing market have contributed to the increase in housing prices. Meanwhile, housing support allowances target only the lowest-income social groups. Private rental markets are poorly regulated functioning mainly on black-market bases and tenants live in rather precarious legal conditions (e.g., limited duration contracts, few restrictions on rent setting).

Investments have been made in improving the energy efficiency and quality of the housing stock in Estonia. This is aimed at not only tackling climate issues, but also reducing energy poverty among households. The Estonian government recently set out a very comprehensive and ambitious long-term national renovation strategy. The main ambition of the strategy is the “full renovation, by 2050, of buildings erected before 2000”. Studies, however, refer to regional and urban-level spatial inequality when it comes to taking up renovation loans and carrying out energy-efficiency renovation projects (Lihtmaa et al., 2018).

Residential context

In 2020, Tallinn city has a registered population of 438,000, which increases to 605,000 when the wider urban region is included. Fifty-two percentage of the population comprises Estonians, 38% Russians, and 10% Ukrainians, Belarussians, and other ethnicities. Compared to 2010, the population has increased by 50,000 inhabitants in the urban region. The population increased at the expense of positive foreign migration since 2018, and by the internal migration in Estonia. Labor migrants have added to the demand for both rental and owner-occupied housing in the capital city region.

A total of 80% of inhabitants live in apartment buildings, and one fifth of the population occupy detached buildings (Kährik and Väiko, 2019). The large share of apartment buildings originates from the mass-construction period between the 1960s and 1990s. Large-scale housing estates were built on the outskirts of the city center, and the vast majority of the Russian-speaking minorities was accommodated there. Nowadays, ethnic Estonians who in average have a higher income have more opportunities and options when it comes to choosing single-family housing or apartments in other districts, while Russian-speaking minorities tend to stay put in the large housing estates (Mägi et al., 2016). Suburbanisation processes only began to accelerate in Tallinn urban region in the 2000s, as the provision of single-family houses remained underdeveloped for about 50 years (Roose, 2019).

After privatization, the private rental sector developed very slowly. The demand for housing has increased in Tallinn urban region due to growing rate of population, which has resulted in upward pressure on house prices. Tallinn currently experiences a deficit of housing, which is increasing housing demand (Kährik and Väiko, 2019). This has also accelerated the development of the private rental market. The latter has mainly been based on the activities of individual landlords, as private developers have only more recently become involved in constructing private rental dwellings.

After the economy recovered from the 2008 to 2009 recession, there has been sharp housing price inflation in Tallinn, visible across the urban region. The inflation slowed during the COVID-19 pandemic, but prices soon continued on an upward trend. Although, by national averages, housing affordability has remained relatively stable during 2010–2019 across Estonia as a whole, in Tallinn region the affordability has considerably decreased (Figure 3).

Figures from Eurostat show that the percentage of low-income households in Estonia living in sub-standard dwellings has declined steadily, the rate dropping from close to 40% in 2004 to around half that in recent years, putting the country below the EU average. To a great extent, however, the housing stock originates from the socialist period and, therefore, is more than 30 years old. Only every fifth household in Tallinn lives in a dwelling which was built after 1991 (Kährik and Väiko, 2019). This makes the quality of housing and need for repair an urgent issue that needs to be addressed by residents and the government (Kährik and Väiko, 2019).

Estonia, by contrast, with its high homeownership rate, is amongst the countries with the lowest shares of people perceiving housing cost overburden in general. When split down by tenure status it, however, appears that nearly every third tenant living in market-rent dwellings perceives cost overburden—the rate being amongst the highest in EU (Caturianas et al., 2020). Thus, high housing costs relative to residents' incomes characterize the private rental tenure in Estonia.

Youth vulnerability in the housing market

The core form of youth inequalities in the housing domain in Tallinn urban region run along socio-economic and ethnic lines as these have been the main identified drivers leading to increased urban housing inequalities (Tammaru et al., 2016a; UPLIFT Urban Report Tallinn, 2022). The labor market and housing market outcomes are also related to the inequalities in the educational system. The labor market outcomes tend to differ for Estonians and Russian-speakers in Tallinn. Only one out of three Russian-speaking respondents perceives their opportunities to get a good job in the private sector to be equal to those of Estonians (Estonian Integration Monitoring Study, 2015). Besides socio-economic barriers ethnic minorities in Tallinn also tend to have different housing and neighborhood preferences as well as mobility patterns (Mägi et al., 2016). Estonia has also the largest horizontal and vertical gender segregation in the European Union and the largest gender wage gap (Kallaste et al., 2010).

Studies refer to the growing socio-economic inequalities and wage gaps since 2000 which has manifested in growing levels of socio-spatial segregation (Tammaru et al., 2016a,b). Young people who rely on financial circumstances the most (i.e., those who did not benefit from the ownership reform) are especially sensitive to these societal changes. Young people have wages lower than the older working age groups, they work more often in precarious work conditions, and their unemployment rate is twice as high. Low education and non-native backgrounds are the main risk factors increasing the level of youth vulnerability in the labor market.

Low education levels are one of the main factors that increase the unemployment risk, which also reduces youth's housing market opportunities. Income is usually linked to solvency, especially in the case of borrowing constraints for mortgage loans (e.g., loan-to-income requirements). Young age cohorts usually face a more difficult situation in the housing market than other age groups because their incomes are lower, and they do not have available capital for buying real estate. Inequality is often passed down from generation to generation, as young people often depend upon the wealth of their parents when, for example, paying a mortgage deposit or providing the wealth or property as collateral for mortgage.

Young people living in urban areas (15–29 years) perceive housing cost overburden almost twice as often as the older generations (8% in 2018) which is to large extent caused by young people residing more frequently in private rental housing.

Data and methods

The analytical part focuses on two cohorts of young people in Tallinn urban region and their achievements in the housing market by looking at whether they have entered homeownership and how the transition to homeownership is mediated by their socio-economic and other characteristics. The two cohorts we examine are (a) those who were aged 20–34 in the year 2010, and (b) those who were aged 20–34 in the year 2020 (i.e., different but overlapping cohorts). Young people younger than 20 were not included in the cohorts as they still mostly rely on their parents for housing and are often still in education.

The analysis is based on EU-SILC data for Tallinn in 2010 and 2020. EU-SILC provides cross-sectional data on households' living conditions over a longer time period (data available from the year 2004) and, every 5 years, a special module of questions was added to the questionnaire which included questions on environmental quality and residents' perception of housing quality. The same survey methodology has been applied every year. Due to the binary character of the dependent variable (owner-occupation vs. rental sector), binary logit models have been applied in the regression analysis.

The household characteristics included in the model are age of the household head (the category ‘young households'/‘young people' are also categorized by the age of the household head), income per household member, occupational status, ethnic status of household, and household situation. Ethnicity was measured by the main home language: whether it was Estonian or other (mainly Russian). Rented housing included both private rental and public rental sectors, and both the market rent sector as well as the below-market rent sector (this also includes units that are in use without rental contract but are owned by persons/legal entities other than the tenants). The location is measured by three categories: inner city, outer city, and suburban area. Housing type is a binary variable: “detached or semi-detached housing” and “multi-apartment housing”.

Results and discussion

Young people entering homeownership: the influence of macro-economic context

After the economy recovered from the 2008 to 2009 recession, there has been sharp housing price inflation in Tallinn urban area. Concerning affordability rates, homeownership has become less affordable over time (Figure 3).

First, we compared the achievements in the housing market in regards to accessing homeownership of two cohorts of young people—those aged 20–34 in both 2010 and 2020. Placing these long-term trends in the macro-economic context, we expected to find evidence of increasing socio-economic barriers lowering access to homeownership over the decade, especially for lower-income and less educated young people. Contrary to the older cohorts, young people have been especially sensitive to the harsh market conditions as they were in the beginning of their housing career during the period of rapidly increasing housing prices.

The described housing market dynamics resulted in a drop in the proportion of homeowners from 83.4% in 2010 to 75.1% in 2020 among the total population. Meanwhile, the share of tenants grew from 16.6 to 24.9% (Table 1). Young cohorts are the most affected by such a drop-in accessibility and availability of owner-occupied housing. Younger age groups (Table 2) already relied on rental properties to a much greater extent in 2010 than middle- and older age groups (one-third of young people, compared with 10% of middle-aged groups, and 16% of the elderly). Between 2010 and 2020, the gap in the level of accessibility of homeownership between younger age groups (20–34 years) and older generations widened by 10% points (Table 1).

Table 1

| 2010 | 2020 | |||||

|---|---|---|---|---|---|---|

| Home ownership | Rental | Total | Home ownership | Rental | Total | |

| Total | 83.4 | 16.6 | 100 | 75.1 | 24.9 | 100 |

| 20–34 yrs | 68.1 | 31.9 | 100 | 52.3 | 47.7 | 100 |

| 35–49 yrs | 89.9 | 10.1 | 100 | 82.5 | 17.5 | 100 |

| 50–64 yrs | 93.5 | 6.5 | 100 | 86.7 | 13.3 | 100 |

| 65+ | 84.2 | 15.8 | 100 | 79.1 | 20.9 | 100 |

Tenure structure by age groups in 2010 and 2020.

Table 2

| 2010 | 2020 | |||||

|---|---|---|---|---|---|---|

| Home ownership | Rental | Total | Home ownership | Rental | Total | |

| Total | 68.1 | 31.9 | 100 | 52.3 | 47.7 | 100 |

| 20–24 yrs | 52.6 | 47.4 | 100 | 26.0 | 74.0 | 100 |

| 25–29 yrs | 64.3 | 35.7 | 100 | 54.8 | 45.2 | 100 |

| 30–34 yrs | 79.9 | 20.1 | 100 | 60.8 | 39.2 | 100 |

Tenure structure by youth age groups in 2010 and 2020.

By 2020, approximately every second young person was relying on rental housing. Within-group differences are noticeable among young people as well—on average, 74% of the 20/24 age group lived in rental accommodation, while the rate decreases with increasing age. Most remarkable, however, is that, even among 30–34-year-olds, nearly 40% are still tenants (the share doubled over 10 years), which exceeds the same share of middle-aged people by two-to-three times.

The housing market preferences and choices of young people are linked to life-course circumstances. Many of them are still in education, are single and their decisions to rent rather than own can be driven by many youth-specific life-course factors. The start of the housing career does not always exhibit a straightforward path to homeownership, and the periods studying in higher education may postpone the decision to obtain a loan and buy their own home. To what extent is this declining ownership rate caused by the structural barriers accessing homeownership, and what is the role of the changes caused by the “emerging adulthood” and related possible postponement of the start of the independent adult life (Arnett, 2000; Arundel and Ronald, 2016), is hard to conclude from the analysis, but most probably both factors play a crucial role in this shift.

Such a drastic drop in the proportion of owner-occupiers over one decade, especially for younger age groups, suggests that, although individual choices and strategies play a part, increased structural barriers and hardships made homeownership harder to achieve. The price inflation, together with greater mortgage restrictions, have affected younger age groups more than older generations, who mostly acquired their housing through the privatization process, or under the circumstances of better housing affordability. Lowering access to homeownership means that young people must rely on rental housing for longer, and the dream of buying one's own home will be postponed for many young people. The next section will shed more light on the issue of structural inequality in assessing homeownership.

Access to homeownership—sorting based on socio-economic and household variables

Labor market performance is an important factor explaining young people's success in entering homeownership. In 2010, the homeownership rate for younger age groups had a moderate link to the socio-economic background (household income and labor market status). However, a decade later, the socio-economic background had become significantly correlated with the status of homeownership (Table 3). By 2020, only 14% of those without an employed household member, and 19% of young low-income groups, succeeded in owning a home. For low-income young people, the success-rate was three times lower than for young age groups on average. Education also plays a role, but the impact of educational attainment is less pronounced.

Table 3

| 2010 | 2020 | |||||

|---|---|---|---|---|---|---|

| Home ownership | Rental | Total | Home ownership | Rental | Total n = 449 | |

| Total | 68.1 | 31.9 | 100 | 52.3 | 47.7 | 100 |

| Income | ||||||

| Highest 20% | 69.0 | 31.0 | 100 | 76.3 | 23.7 | 100 |

| Middle 60% | 69.6 | 30.4 | 100 | 49.3 | 50.7 | 100 |

| Lowest 20% | 61.2 | 38.8 | 100 | 19.0 | 81.0 | 100 |

| Work status ** | ||||||

| In employment | 69.4 | 30.6 | 100 | 54.9 | 45.1 | 100 |

| Not in employment | 55.6 | 44.4 | 100 | 14.0 | 86.0 | 100 |

| Education | ||||||

| Primary | 65.0 | 35.0 | 100 | 44.6 | 55.4 | 100 |

| Secondary | 65.0 | 35.0 | 100 | 47.1 | 52.9 | 100 |

| Tertiary | 71.9 | 28.1 | 100 | 57.3 | 42.7 | 100 |

| Ethnic status * | ||||||

| Native | 62.7 | 37.3 | 100 | 50.9 | 49.1 | 100 |

| Other | 79.5 | 20.5 | 100 | 54.7 | 45.3 | 100 |

| Gender | ||||||

| Male head | 75.4 | 24.6 | 100 | 55.3 | 44.7 | 100 |

| Female head | 56.0 | 44.0 | 100 | 47.2 | 52.8 | 100 |

| Partnership | ||||||

| Single | 36.2 | 63.8 | 100 | 32.6 | 67.4 | 100 |

| In partnership | 78.0 | 22.0 | 100 | 65.2 | 34.8 | 100 |

| Other | 78.6 | 21.4 | 100 | 65.9 | 34.1 | 100 |

| Dep. children | ||||||

| No children | 60.5 | 39.5 | 100 | 45.5 | 54.5 | 100 |

| Children | 78.6 | 21.4 | 100 | 69.9 | 30.1 | 100 |

Twenty to thirty-four years of age access to homeownership in 2010 and in 2020.

*Main spoken language at home.

**At least one person from household active in labor force.

Significance at 0.005 level.

Model 1 considers household income as a driver for accessing homeownership. Without any control variables in the model, income had a slight impact on entering homeownership in 2010—middle- and high-income groups were 1.4-times more likely to end up in homeownership compared to low-income earners. By 2020, the effect of income had increased dramatically—the odds for high-income earners becoming homeowners were 14-times the odds for low-income earners, while the odds for middle-income groups were 4-times those for low-income earners. Almost 20% of variance in the share of homeownership was explained by income alone in 2020, whereas, in 2010, income explained only 1% of variance (Model 1, Table 4).

Table 4

| 2010 | 2020 | |||||

|---|---|---|---|---|---|---|

| B | Sig. | Exp(B) | B | Sig. | Exp(B) | |

| Low income—ref.* | ||||||

| Middle income | 0.374 | 0.001 | 1.453 | 1.424 | 0.000 | 4.155 |

| High income | 0.344 | 0.001 | 1.411 | 2.625 | 0.000 | 13.802 |

| Constant | 0.457 | 0.001 | 1.579 | −1.453 | 0.000 | 0.234 |

Income affecting homeownership (logit regression—Model 1).

* Total household income per household member.

Nagelkerke R Square 0.038 for 2010 and 0.183 for 2020.

Ethnicity was also significantly related to the rate of homeownership, although a little unexpected. While there was almost 20% points difference in the homeownership rate in 2010 to the benefit of ethnic minorities, this difference had, to large extent, diminished over the following decade (down to 4% by 2020). This situation can be explained by the ownership reform. The initial starting position favored Russian–speaking minorities, since they were over-represented in apartments that were subject to privatization, while Estonian-speaking population more often lived in restituted housing (Kährik, 2000). Those living in restituted housing could receive a municipal rental apartment for compensation, but did not have the possibility to privatize. Although the generation which actively participated in privatization is situated among the older age groups, these ethnic inequalities were also transmitted to the next generation. Another explanation is that the Estonian background young people are more likely to be mobile—changing their place of residence more likely thus postponing the decision to buy home. While Russian-speakers are more often from Tallinn originally, Estonians are more likely to have moved to Tallinn and have had no permanent residence there.

Russian-speakers have, however, had less success in the labor market as their incomes and employment rates tend to be lower than those for the majority population. This explains the fall in homeownership rate for ethnic minorities, which caused the gap in homeownership between ethnic categories to greatly diminish.

We also looked at gender and household differences in access to homeownership. Female-headed households, single people and households without children are related to lower homeownership rate. While gender difference diminished during the decade 2010–2020, as gender gaps in wages and employment levels also decreased in Estonia and Tallinn, household structure remained an important factor in tenure segmentation. More people living in a household can translate into better economic opportunities which play a key role in achieving homeownership, whereas the household structure and having a family also contributes to seeking more security in terms of finding a more permanent, stable and secure home (depending on the life course circumstances).

When adding ethnicity, household and demographic variables to the model explaining homeownership rate (Model 2, Table 5), we see that these additional variables add another 10% explanation of the variance in addition to income for 2020 20–34 cohort. Income remains the most significant determinant of homeownership in 2020. By adding additional variables, for example, whether at least one household member is in labor market, the importance of income is only slightly reduced. Having at least one employed person in the household has an odds ratio of 2.6, indicating that it is an important factor in homeownership as well. Besides income and labor market variables, having secondary or tertiary education increased the chances of entry into the homeownership (almost two–times more likely).

Table 5

| 2010 | 2020 | |||||

|---|---|---|---|---|---|---|

| B | Sig. | Exp(B) | B | Sig. | Exp(B) | |

| Low income—ref.* | 0.001 | 0.000 | ||||

| Middle income | −0.535 | 0.001 | 0.585 | 1.121 | 0.001 | 3.069 |

| High income | −0.597 | 0.001 | 0.550 | 2.312 | 0.000 | 10.096 |

| Work status—not in employment—ref.* | ||||||

| In employment | 0.682 | 0.001 | 1.977 | 0.978 | 0.001 | 2.659 |

| Low education—ref. | 0.001 | 0.001 | ||||

| Middle education | 0.106 | 0.002 | 1.112 | 0.605 | 0.001 | 1.832 |

| High education | 0.799 | 0.001 | 2.223 | 0.535 | 0.001 | 1.708 |

| Ethnicity—non-Estonian—ref. | ||||||

| Estonian household | −0.598 | 0.001 | 0.550 | −0.160 | 0.001 | 0.852 |

| Household head female—ref. | ||||||

| Male | 0.787 | 0.001 | 2.196 | 0.278 | 0.001 | 1.320 |

| Household type single—ref. | 0.000 | 0.0000. | ||||

| Couple | 1.531 | 0.000 | 4.624 | 0.645 | 0.001 | 1.906 |

| Other type of household | 1.782 | 0.000 | 5.940 | 1.159 | 0.001 | 3.188 |

| No children—ref. | ||||||

| Children | −0.168 | 0.001 | 0.846 | 0.719 | 0.001 | 2.052 |

| Age of head 20–24—ref. | 0.001 | 0.001 | ||||

| Age of head 25–29 | 0.052 | 0.067 | 1.053 | 0.946 | 0.001 | 2.576 |

| Age of head 30–34 | 1.000 | 0.001 | 2.717 | 0.825 | 0.001 | 2.283 |

| Constant | −1.261 | 0.001 | 0.283 | −4.119 | 0.000 | 0.016 |

Individual level factors affecting homeownership (logit regression—Model 2).*

*At least one person per household.

Source: authors' computation, EU-SILC 2010, 2020.

*Low—lowest 25%, high—highest 25%.

*Nagelkerke R Square 0.272 for 2010 and 0.317 for 2020.

In terms of ethnicity, ethnic minority status had a positive impact. Chances were also increased by having a male head of household (1.3-times more likely to be homeowners), living with a partner (1.9-times more likely), living in a household type other than a couple (3.2-times more likely), and by having children in the household (2.1-times more likely). According to age structure, those aged 20–24 years have the lowest chances of living in an owner-occupied dwelling, while for 25–29 and 30–34-year-olds, the chances are reasonably uniform.

For the 2010 20–34 cohort, adding additional variables improves the explanatory power of the model to almost 30%. However, factors other than income have the main explanatory power. When the work status variable is added to the model, the impact of income becomes insignificant. Instead, having employed household members doubles the chances of being homeowners. Education remains significantly related as well, but only higher education. Ethnicity plays a stronger role for the 2010 (20–34 years) cohort than for the 2020 one, with non-Estonian households in better position in terms of homeownership.

Having a male head of household had a stronger effect in 2010 (2.2-times more likely in homeownership), while couples and other types of household were more significant determinants in 2010. One possible explanation is that, in 2010, the rate of young people who still lived with their parents was higher, and their parents' homes were more likely to be owner-occupied. Meanwhile, the 30–34 age group stood out with a higher propensity to be homeowners.

Housing quality and locational differences between the tenures

Furthermore, we argue that the growing barrier to entry into homeownership for young people is coupled with side-effects related to housing quality and spatial disadvantages. Rental dwellings are often not evenly distributed in space, but are found either in attractive inner-city areas or in less affluent suburban high-rise neighborhoods. Previous studies in Tallinn note that housing quality differs according to location (e.g., urban/rural), and that municipal housing units are spatially concentrated (Kährik and Kõre, 2013). However, there are no previous studies on the locational characteristics of private rental units.

In 2010, rental housing was over-represented both in new (built since 2000) and old (pre-1960) housing stock, while homeownership was over-represented in Soviet era-built dwellings. The higher rate of rental dwellings in older houses is explained by the restitution process retaining the rental status of these buildings (Lux et al., 2012). As we can see, the difference in homeownership and rental sectors between Soviet era and older dwellings had slightly reduced by 2020. As Ruoppila and Kährik (2002) argue, in the period immediately after the housing reforms, the private rental sector became quite polarized in terms of the quality of the housing stock as well as the residential structure.

In 2020, rental units were over-represented in older housing (built before 1960, comprising one-third of the rental stock). In Tallinn, this is especially the case in the inner city and the high-rise outer city neighborhoods, while fewer rental units are located in the outer suburbs (Table 6). As expected, rental housing is situated in multi-family buildings. Owner-occupied housing is more often found in newer houses, low-rise outer city neighborhoods and in outer suburban locations, and is over-represented in detached and semi-detached buildings.

Table 6

| 2010 | 2020 | |||||

|---|---|---|---|---|---|---|

| Home ownership | Rental | Total (n = 1,192) | Home ownership | Rental | Total (n = 2,094) | |

| Total | 83.4 | 16.6 | 100 | 75.1 | 24.9 | 100 |

| Building period | ||||||

| 2000 or after | 75.7 | 24.3 | 100 | 76.9 | 23.1 | 100 |

| 1980–1999 | 84.0 | 16.0 | 100 | 77.9 | 22.1 | 100 |

| 1960–1979 | 90.7 | 9.3 | 100 | 77.0 | 23.0 | 100 |

| Before 1960 | 75.8 | 24.2 | 100 | 67.7 | 32.3 | 100 |

| Building type | ||||||

| (Semi)detached house | 86.6 | 13.4 | 100 | 84.3 | 15.7 | 100 |

| Multi-family building | 82.8 | 17.2 | 100 | 73.1 | 26.9 | 100 |

| State of repair | ||||||

| Very good/good | 83.6 | 16.4 | 100 | 75.0 | 25.0 | 100 |

| Needs repair | 83.0 | 17.0 | 100 | 75.2 | 24.8 | 100 |

| Neighb quality | ||||||

| Good env quality | 83.3 | 16.7 | 100 | 73.8 | 26.2 | 100 |

| Problems with env quality | 16.4 | 83.6 | 77.4 | 22.6 | 100 | |

| Neighb location | ||||||

| Inner city | 78.3 | 21.7 | 100 | 70.1 | 29.9 | 100 |

| Outer city (high-rise) | 83.9 | 16.1 | 100 | 73.9 | 26.1 | 100 |

| Outer city (low-rise) | 88.6 | 11.4 | 100 | 76.9 | 23.1 | 100 |

| Suburban | 86.7 | 13.3 | 100 | 81.7 | 18.3 | 100 |

| Location | ||||||

| Tallinn | 82.4 | 17.6 | 100 | 72.9 | 27.1 | 100 |

| Outer suburb | 86.7 | 13.3 | 100 | 81.7 | 18.3 | 100 |

Dwelling characteristics (homeownership vs. rental sector), 2010 and 2020.

Rental units are over-represented in Tallinn compared to the outer suburbs, especially the inner city, and owner-occupied dwellings are over-represented in the low-rise and outer suburbs of Tallinn. The high-rise suburbs were yet to be over-represented in rental market.

There are no significant differences based on the “state of repair” assessment by owners and tenants in both years. In terms of neighborhood quality (assessment of noise level, pollution and/or criminality), owners tended to be slightly more critical toward their neighborhood than tenants.

According to the Model 3 predicting homeownership share based on housing and neighborhood factors shows a lower explanatory power compared to the model comprising residential characteristics. For the 2020 model, the explanatory power is 4% and, for 2010, it is 8% (Table 7).

Table 7

| 2010 | 2020 | |||||

|---|---|---|---|---|---|---|

| B | Sig. | Exp(B) | B | Sig. | Exp(B) | |

| Construction period—before 1960–ref.* | 0.000 | 0.000 | ||||

| 1960–1979 | 1.316 | 0.000 | 3.730 | 0.628 | 0.000 | 1.875 |

| 1980–1999 | 0.593 | 0.001 | 1.809 | 0.633 | 0.000 | 1.884 |

| 2000- | −0.319 | 0.001 | 0.727 | 0.411 | 0.001 | 1.508 |

| Housing quality with deficiencies—ref. | ||||||

| Good | 0.267 | 0.001 | 1.306 | 0.168 | 0.001 | 1.183 |

| Neighborhood has certain problems—ref. | 0.865 | 0.000 | 2.376 | |||

| Neighborhood without problems | −0.019 | 0.142 | 0.981 | 0.286 | 0.001 | 1.332 |

| Inner city location -ref. | ||||||

| Outer-city (high-rise) | 0.036 | 0.048 | 1.036 | −0.046 | 0.001 | 0.955 |

| Outer-city (low-rise) | 0.781 | 0.001 | 2.184 | 0.064 | 0.001 | 1.066 |

| Suburban (outside Tallinn) | 0.474 | 0.001 | 1.606 | 0.225 | 0.001 | 1.253 |

| In multiapartment building—ref. | ||||||

| Detached (semidetached) | 0.452 | 0.001 | 1.572 | 0.662 | 0.000 | 1.939 |

| Constant | 0.702 | 0.000 | 2.018 | 0.294 | 0.001 | 1.342 |

The influence of housing quality and the location of housing on homeownership (logit regression—Model 3).

*Nagelkerke R Square 0.082 (2010), 0.038 (for 2020).

In Model 3 (Table 7), living in a post-1960 built dwelling continues to be significantly related to homeownership status in 2020 (especially Soviet-era dwellings), however the likelihood of older socialist apartments to be used as an owner-occupied tenure has sharply decreased over the period. Owner-occupied housing is over-represented in low-rise Tallinn suburbs. (1.1-times more likely), as are outer suburban neighborhoods (1.3-times more likely). The best predictor of homeownership among housing characteristic variables is building type: detached and semi-detached buildings were associated with nearly twice the likelihood of homeownership than renting (1.9-times). Good housing quality is also positively related to homeownership (1.2-times more likely).

In 2010, Soviet-era buildings had an even higher propensity to be owner-occupied (especially those built between 1960 and 79, 3.7-times more likely). Consequently, this has been the housing segment that has particularly expanded within the rental sector by 2020. This is because the apartments are usually smaller, and the location is either in or close to the city center compared to dwellings built between 1980 and 1999. Rental apartments are far the most overrepresented in historical inner city neighborhoods—the housing units which to large extent remained in the rental sector as a result of the restitution to pre-WWII owners. Trends over the 10 years indicate that housing densification has taken place in the city outskirts—more apartment buildings were built in previously low-rise homogeneous suburbs (inside Tallinn as far as beyond the city border).

Conclusions

The current housing affordability crisis, which has been driven mainly by the financialization of housing and the government's retrenchment of social policies and the lack of provision of affordable housing over previous decades, has had a major impact on growing inequalities in access to housing. The crisis has hit the opportunities of young people in the housing market especially hard. Moving out from the parental home into independent housing, and especially homeownership, has become more challenging over time. The structural differences between those who can afford to buy and those who cannot is growing across Europe (Ronald and Lennartz, 2018; Smith et al., 2022). Governments have increasingly introduced incentives in response to the growing affordability crises from the 2010s onwards by moving toward a new era of post-neoliberalism (Kadi et al., 2021). However, it is yet to be seen to what extent these measures can alleviate the affordability gap, since housing prices overall continue to climb.

Although there were small-scale incentives to implement new social housing programs in the 2010s, the government's supply-side measures to tackle housing affordability in Tallinn have overall been marginal. Since the mass-privatization of the housing stock in the 1990s, housing market dynamics in Tallinn have been driven by an ultra-liberal housing regime, with new housing developments being almost entirely in the hands of private developers. Hence, the market has been highly dependent on global economic cycles. Such a neo-liberal housing market context, with a very high rate of homeownership up to the beginning of the 2010s, makes Tallinn special in terms of understanding the shifting patterns and mechanisms driving inequalities in accessing homeownership for younger people in subsequent years.

Homeownership remains much larger than the rental sector in Tallinn, but, since 2010, a significant tenure shift has taken place, as the private rental stock has expanded considerably, constituting a quarter of the total housing stock by 2020. The period 2010–2020 was when property prices increased greatest since the completion of the ownership reform, and the structural barriers to entering homeownership have increased. While the transformation in tenure structure resulted in more choice in the housing market and made Estonia more similar to Western European countries, the new inequalities this tenure shift brought about, based on the socio-economic circumstances of households, migration background and intergenerational wealth transmission, need special attention. The structural barriers and sorting mechanisms experienced by young households in the housing market increasingly affect their life opportunities (OECD, 2020), and may lead to a vicious circle of housing inequality (van Ham et al., 2021).

This study showed that new patterns and drivers of inequality have developed in the housing market of Tallinn over the housing boom of the 2010s, seriously affecting housing affordability. Entering homeownership has become much more challenging for early-career households (those aged 25–34 years) in Tallinn in 2020, compared to a decade earlier. Money buys choice, and the labor market performance of households increasingly influences the housing market outcomes for young households. Young people, who often have a weaker labor market position with more precarious work conditions compared to older cohorts, face growing difficulties in meeting the financial criteria for loans and mortgages set by banks, resulting in significantly reduced rates of homeownership. Younger cohorts increasingly rely on wealth transfers from their parents, which leads to further socio-economic sorting across tenure divisions. Older cohorts, who entered the housing market during the 1990s and 2000s, had more favorable conditions for becoming homeowners, in terms of socio-economic standing, when they were at the same life stage.

In addition to the financial gains that accrue to homeowners but not tenants, who incur high monthly housing expenditures without financial gain and experience high cost overburden due to higher overall housing costs, private rental status also has a slight negative link to housing quality as well as locational disadvantages, especially for those with lower socio-economic status. Private tenants generally perceive their dwellings as slightly lower quality (i.e., state of repair) than owner-occupiers. Lower dwelling quality usually correlates with higher energy costs due to the energy-inefficiency of multifamily buildings. Although a concentration of rental dwellings is found in the inner-city areas, the bulk of rental units are located in outer city high-rise multifamily buildings, which are especially attractive to households with lower socio-economic standing due to their greater affordability. Consequently, tenure-based socio-economic segmentation also gradually turns to manifest in spatial disadvantage and overlap with socio-spatial segregation (e.g., Tammaru et al., 2016a).

These somewhat more precarious housing conditions—the insecure nature of private renting, less satisfactory living conditions and associated locational disadvantages—as well as the overburden of housing costs in the private rental sector can translate into severe consequences for young people in terms of health, social inclusion and life opportunities, including even family formation. Therefore, to break the vicious circle of housing inequality, more proactive measures could be implemented to counteract the negative impacts of housing financialization and the subsequent unregulated tenure shift on social equity. Being unable to start an independent housing career or move into homeownership can have long-term consequences for individuals and perpetuate the intergenerational transmission of wealth and housing inequality. The issue of the increasing unaffordability of housing should be made a systemic part of urban policy in relation to access to urban resources (Haffner and Hulse, 2021; OECD, 2021). Stricter planning and zoning regulations could be pursued, along with affordable housing construction and allocation policies that target younger households with unmet housing needs alongside other vulnerable groups.

Statements

Data availability statement

Publicly available datasets were analyzed in this study. This data can be found here: https://ec.europa.eu/eurostat/web/income-and-living-conditions/data/database.

Author contributions

AK: original idea, study design, data analysis, interpretation of results, and writing the manuscript. IP: original idea, study design, interpretation of results, and writing the manuscript. All authors contributed to the article and approved the submitted version.

Funding

This work was supported by the funding from the European Union's Horizon 2020 research and innovation programme (grant agreement No. 870898: UPLIFT), and Estonian Research Council (PRG306: ‘Understanding the Vicious Circles of Segregation. A Geographic Perspective’).

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Footnotes

1.^ UPLIFT project funded by EU H2020 programme aimed at (1) understanding patterns and trends of inequality among young people and how individuals experience and adapt to inequality through participatory research, and (2) co-designing a policy tool aimed at addressing and reducing inequality and socio-economic divisions among the vulnerable youth. See more https://uplift-youth.eu/.

2.^ The Euribor (the Euro InterBank Offered Rate) refers to the price at which European banks lend money to each other. The Euribor has a direct influence on the conditions of borrowing for private persons.

References

1

Aalbers M. B. Hochstenbach C. Bosma J. Fernandez R. (2021). The death and life of private landlordism: How financialized homeownership gave birth to the buy-to-let market. Hous. Theory Soc.38, 541–563. 10.1080/14036096.2020.1846610

2

Aigner A. (2022). What's wrong with investment apartments? On the construction of a ‘financialized' rental investment product in Vienna. Hous. Stud.37, 355–375. 10.1080/02673037.2020.1806992

3

Anacker K. B. (2019). Introduction: Housing affordability and affordable housing. Int. J. Hous. Policy19, 1–16. 10.1080/19491247.2018.1560544

4

Arbaci S. (2007). Ethnic segregation, housing systems and welfare regimes in Europe. Eur. J. Hous. Policy7, 401–433. 10.1080/14616710701650443

5

Arnett J. J. (2000). Emerging adulthood: A theory of development from the late teens through the twenties. Am. Psychol.55, 469–480. 10.1037/0003-066X.55.5.469

6

Arundel R. (2017). Equity inequity: Housing wealth inequality, inter and intra-generational divergences, and the rise of private landlordism. Hous. Theory Soc.34, 176–200. 10.1080/14036096.2017.1284154

7

Arundel R. Hochstenbach C. (2020). Divided access and the spatial polarization of housing wealth. Urban Geogr.41, 497–523. 10.1080/02723638.2019.1681722

8

Arundel R. Lennartz C. (2020). Housing market dualization: linking insider-outsider divides in employment and housing outcomes. Hous. Stud.35, 1390–1414. 10.1080/02673037.2019.1667960

9

Arundel R. Ronald R. (2016). Parental co-residence, shared living and emerging adulthood in Europe: semi-dependent housing across welfare regime and housing system contexts. J. Youth Stud.19, 885–905. 10.1080/13676261.2015.1112884

10

Arundel R. Ronald R. (2021). The false promise of homeownership: Homeowner societies in an era of declining access and rising inequality. Urban Stud.58, 1120–1140. 10.1177/0042098019895227

11

Bogdon A. S. Can A. (1997). Indicators of local housing affordability: comparative and spatial approaches. Real Estate Econ.25, 43–80. 10.1111/1540-6229.00707

12

Bohle D. Seabrooke L. (2020). From asset to patrimony: the re-emergence of the housing question. West Eur. Politics43, 412–43410.1080/01402382.2019.1663630

13

Bouzarovski S. Thomson H. Cornelis M. (2021). Confronting energy poverty in Europe: a research and policy agenda. Energies14, 858. 10.3390/en14040858

14

Calder V. (2017). Zoning, Land-Use Planning, and Housing Affordability. Washington, DC: Cato Institute Policy Analysis, 823.

15

Caturianas D. Lewandowski P. Sokołowski J. Kowalik Z. Barcevičius E. (2020). Policies to Ensure Access to Affordable Housing. Luxembourg: European Parliament.

16

Cigdem M. Whelan S. (2017). Intergenerational transfers and housing tenure – Australian evidence. Int. J. Hous. Policy17, 227–248. 10.1080/19491247.2017.1278580

17

Clark W. A. V. (2019). Millennials in the housing market: the transition to ownership in challenging contexts. Hous. Theory Soc.36, 206–227. 10.1080/14036096.2018.1510852

18

De Vuijst E. Van Ham M. Kleinhans R. (2017). The moderating effect of higher education on the intergenerational transmission of residing in poverty neighbourhoods. Environ. Plan. A49, 2135–2154. 10.1177/0308518X17715638

19

Dewilde C. De Decker P. (2016). Changing inequalities in housing outcomes across Western Europe. Hous. Theory Soc.33, 121–161. 10.1080/14036096.2015.1109545

20

Estonian Integration Monitoring Study (2015). Available online at: https://www.ibs.ee/wp-content/uploads/Integration-Monitoring-Estonia-2015.pdf (accessed January 10, 2023).

21

Fields D. Uffer S. (2016). The financialisation of rental housing: a comparative analysis of New York city and Berlin. Urban Stud.53, 1486–1502. 10.1177/0042098014543704

22

Fikse E. Aalbers M. B. (2021). The really big contradiction: homeownership discourses in times of financialization. Hous. Stud.36, 1600–1617. 10.1080/02673037.2020.1784395

23

Filandri M. Olagnero M. (2014). Housing inequality and social class in Europ?Hous. Stud.29, 977–993. 10.1080/02673037.2014.925096

24

Forrest R. Hirayama Y. (2018). Late home ownership and social re-stratification. Econ. Soc.47, 257–279. 10.1080/03085147.2018.1459368

25

Foye C. Clapham D. Gabrieli T. (2018). Home-ownership as a social norm and positional good: subjective wellbeing evidence from panel data. Urban Stud. 55, 1290–1312. 10.1177/0042098017695478

26

Friesenecker M. Kazepov Y. (2021). Housing Vienna: the socio-spatial effects of inclusionary and exclusionary mechanisms of housing provision. Soc. Inclusion9, 77–90. 10.17645/si.v9i2.3837

27

Fuller G. W. Johnston A. Regan A. (2020). Housing prices and wealth inequality in Western Europe. West Eur. Politics43, 297–320. 10.1080/01402382.2018.1561054

28

Fuster N. Arundel R. Susino J. (2019). From a culture of homeownership to generation rent: housing discourses of young adults in Spain. J. Youth Stud.22, 585–603. 10.1080/13676261.2018.1523540

29

Haffner M. E. A. Heylen K. (2011). User costs and housing expenses. Towards a more comprehensive approach to affordability. Hous. Stud.26, 593–614. 10.1080/02673037.2011.559754

30

Haffner M. E. A. Hulse K. (2021). A fresh look at contemporary perspectives on urban housing affordability. Int. J. Urban Sci.25, 59–79. 10.1080/12265934.2019.1687320

31

Hedman L. Manley D. van Ham M. (2017). Sorting Out Neighbourhood Effects Using Sibling Data. IZA Discussion Papers, 11178. Bonn: Institute of Labor Economics (IZA).

32

Hedman L. van Ham M. (2021). Three generations of intergenerational transmission of neighbourhood context. Soc. Inclusion9, 129–141. 10.17645/si.v9i2.3730

33

Hegedus J. Lux M. Teller N. (2013). Social Housing in Transition Countries. New York: Routledge.

34