José Luis Morales Rocha1*

José Luis Morales Rocha1* Teófilo Lauracio Ticona2

Teófilo Lauracio Ticona2 Mario Aurelio Coyla Zela1

Mario Aurelio Coyla Zela1 Jarol Teófilo Ramos Rojas1

Jarol Teófilo Ramos Rojas1 Genciana Serruto Medina1

Genciana Serruto Medina1 Nakaday Irazema Vargas Torres1

Nakaday Irazema Vargas Torres1 Nilton Juan Zeballos Hurtado2

Nilton Juan Zeballos Hurtado2- 1Professional School of Public Management and Social Development, National University of Moquegua, Moquegua, Peru

- 2Professional School of Accounting, Jose Carlos Mariátegui University, Moquegua, Peru

The objective of this article was to explore the impact of social conflict and fiscal centralism on the efficiency and fiscal governance of Peruvian sub-national governments between 2016 and 2023, a period of extreme political instability and social conflict. Data was collected from disaggregated official sources for the 24 departments and the provinces of Lima and Callao. The results were: the effectiveness of public spending by subnational governments has a limited impact on the development and welfare of the populations of the regions. Even in contexts without social conflict, subnational governments are unlikely to achieve effective governance or fiscal autonomy, due to contradictory state policies on fiscal decentralization. Despite the fiscal centralism reflected in administrative and technical practices, local governments are trying to improve their fiscal governance processes.

1 Introduction

Social conflicts are long-standing in the country, just review the Peruvian history of the last 200 years: numerous coups, several armed uprisings, prolonged strikes, numerous revocations of authorities, etc. (Menchero, 2020; Paredes and Encinas, 2020); but it began to exacerbate along with political instability, from 2016. The recent social conflict and political crisis, are extremely deteriorating social coexistence, institutional stability, sustainable preservation of the environment, production systems and commercialization of goods and services, public and private finances; it happened to slow down, if not undermine, sustainable development; despite the commitment made by the country when signing the 2030 Agenda along with 192 other States (Cosme, 2018) and requesting admission to the Organization for Economic Cooperation and Development (OECD).

It has also negatively impacted the country’s international image as an investment destination, according to Fitch Ratings (El Comercio, 2022; Gestión, 2023), due to the high level of political uncertainty and a further deterioration of public governance; undermining domestic and foreign private investment, slowing or scaring off future prospects for sustained economic growth.

The paralysis of the State with respect to the governance of public policies, if not sustainable, at least consistent with the aspirations of the great majorities, is remarkable. It is now more clearly perceived that the 6% annual growth between 2010 and 2013 (Jurado and Tasayco, 2021) was not used to initiate equitable growth (ODS 10), particularly in the Andean, Amazonian and some coastal departments; or seen from another classification, in the departments that make up the northern, central, southern and eastern macro-regions, with respect to Metropolitan Lima and the province of Callao. This bonanza was not used intensively to promote industrial development (ODS 9), reduce informality and generate decent employment for hundreds of thousands of young people who apply to any labor market each year (ODS 8), the construction of sustainable territories (ODS 11), sustainable production and consumption systems (ODS 12), etc.

The national government is the competent authority to resolve more than 60% of social conflicts in the country (Ombudsman’s Office, 2024). However, it is struggling in a maelstrom of political instability, ungovernability, lack of citizen confidence, with tax revenues in constant deterioration, without resources to finance large public investment projects. As of November 2023, the government of Dina Boluarte and the Congress of the Republic reached a disapproval of 85 and 91%, respectively; 85% of the citizens consider that the Congress does not respect the separation of powers of the State, 65% consider that it is necessary to renew the entire Otárola cabinet (LR Data, 2024).

The purpose of decentralization is to contribute to the design and implementation of regional and local public policies consistent with their economic, social, political, cultural, technological, environmental, etc. context. It is also to promote the effectiveness of the governance of their finances, so as to enable them to sustainably finance such policies, ensure the fiscal balance of the regions and municipalities, guarantee the effective participation of citizens in the planning, management and control of investments and the provision of public services; ensure growth with equity, administrative efficiency and productive competitiveness, timely accountability and the generation of sources for the sustained growth of regional or local revenues (Baylon and Quispe, 2022; Tirard, 2020). Public finance governance does not necessarily imply applying the same legal rules in all sub-national governments (Tirard, 2020). The basic strategy of governance implies the exercise of authority, but with a leadership style and skills for negotiation and conflict management (Garcia and Suárez, 2015), in an environment that recognizes public entities and civil society, including companies and other related parties, as equals.

In Peru, sub-national public governance can be traced in the legal framework inherent to the democratization of public management, transparency and accountability such as Law 27680 referring to the right of citizens to participate in public affairs, Law 27806 inherent to transparency and access to public information, the organic laws of regional (Law 27867) and local governments (Law No. 27806) that establish mechanisms of social control, oversight and accountability (Tumi, 2020); also in Law 28056 of the participatory budget, focused on results by R. D. N° 007-2010-EF. D. N° 007-2010-EF-76.0, among others. It begins to consolidate in 2014 with the implementation of the Country Program promoted by the OECD Secretary General Angel Gurría and the President of Peru Ollanta Humala. One of its objectives was to study and promote decentralization for more inclusive growth, in the framework of “better governance to achieve more competitive and resilient regions and cities” (OCDE, 2016). Along these lines, digitalization continues, focused on the restructuring of public services, administrative processes, tax collection, ensuring citizen participation, among many others, using digital technologies intensively (Huamán and Medina, 2022); also, science, technology and research (STI) policies, focused on promoting productivity and inclusive competitiveness, recognizing ancestral knowledge, endogenous social innovations, climate change, community institutions (Harman et al., 2023).

In 2016, the National Government received from the OECD the studies on public governance in Peru (OCDE, 2016), which contains the contextualization of public governance reform in Peru, conclusions and recommendations on the modernization of public management, decentralization, digital government, open government, among others. In this perspective, some sub-national governments have taken encouraging steps towards a new public governance in the country, although under the tutelage of the National Government, thus losing the principle of autonomy.

However, in the context of deep political instability and social conflict from 2016 to the present, the process of orderly decentralization apparently moved away (Caballero, 2023). Central government officials appealed with greater emphasis to political and administrative controls to direct the governance of sub-national governments (Quispe E., 2021); consequently, fiscal centralism presumably increased.

In the above context, the objective of this article is to explore the impact of social conflict and fiscal centralism on the efficiency and fiscal governance of Peruvian sub-national governments between 2016 and 2023, a period of extreme political instability and social conflict.

There are theoretical reasons to expect decentralization to have a positive impact on various aspects of public action, especially in the social sphere. Although not a universal solution, with the right design and in the right context, decentralization can be an effective reform that meets multiple social expectations. This paper examines the relationship between fiscal decentralization (measured as subnational public revenues as a percentage of GDP) and four social outcomes: infant mortality, literacy rate, access to safe drinking water, and human development index (Pinilla et al., 2014).

Various indicators have been used to strengthen the analysis. For example, GDP per capita reflects a country’s average economic capacity and serves as a reference measure to assess whether public spending is fostering economic growth. Efficient financial management should contribute to improving productivity through strategic public investment and stimulating key sectors such as education, health, and infrastructure, which have multiplier effects on the economy. If public spending is properly channeled, a positive correlation between increased public expenditure and per capita GDP growth would be expected.

The Gini index measures income inequality and thus reflects the State’s capacity for redistribution. Therefore, efficient and equitable public spending should aim to correct market failures through subsidies, transfers, public education, and social services, as well as reduce the income gap between different segments of the population. A decrease in the Gini index associated with sustained public spending suggests that financial management is not only economically efficient but also fair and socially oriented.

Finally, the Human Development Index (HDI) combines income, health, and education—dimensions that are directly influenced by public spending. It serves as a comprehensive indicator of how spending affects the overall well-being of the population, reflecting improvements in human capabilities and measuring sustainable social outcomes beyond mere economic growth. Efficient public spending should be positively correlated with increases in the HDI, indicating sound resource management in terms of human development.

In Bolivia, the objective of decentralization entailed the transfer of considerable resources to subnational levels, which caused significant fiscal deterioration. To correct this situation and establish more effective incentives, the second generation of reforms prioritized the stability of local finances, controlled debt, and an increase in taxation efforts at the municipal level. This process requires a solid institutional framework and must continue to promote true autonomy (Galindo and Medina, 1995).

In Latin American countries, the objective of decentralization entailed the transfer of considerable resources to subnational levels, which caused significant fiscal deterioration. To correct this situation and establish more effective incentives, the second generation of reforms prioritized the stability of local finances, controlled debt, and an increase in taxation efforts at the municipal level. This process requires a solid institutional framework and must continue to promote true autonomy (Pinilla et al., 2014).

Thus, the following research questions are posed: How has fiscal decentralization affected the efficiency of public spending in Peruvian subnational governments between 2016 and 2023, and in what way has this relationship been influenced by the increase in social conflict?, To what extent has the growing social conflict modified the impact of fiscal centralism on the governance and autonomy of subnational governments in Peru during the period 2016–2023? And How has the capacity of Peruvian subnational governments to improve their fiscal governance evolved in a context of limited decentralization and increasing political instability between 2016 and 2023?

Therefore, we can pose the following general hypothesis: “Social conflict and fiscal centralism had a negative impact on the efficiency and fiscal governance of Peruvian subnational governments between 2016 and 2023, a period characterized by extreme political and social instability.” And specifically, it can be stated that “The greater the social conflict, the lower the fiscal efficiency of Peruvian subnational governments will be between 2016 and 2023” and “Fiscal centralism has limited the management autonomy of subnational governments, negatively affecting their fiscal governance during the same period.”

2 Method

The coverage of the research includes the 24 departments, in addition to the provinces of Lima and Callao. The data on social conflicts by department was obtained from the Ombudsman’s Office (2024); the indicators related to fiscal governance from the web pages of the Ministry of Economy and Finance (MEF) and others, referring to the years 2016 to 2023.

The governance of public finances involves several variables, from which the efficiency of the execution of the public expenditure budget, in the accrual phase; and the propensity towards financial independence through the significance of the directly collected resources (DCR) with respect to the total revenues of sub-national governments (Oliva, 2018) were rescued.

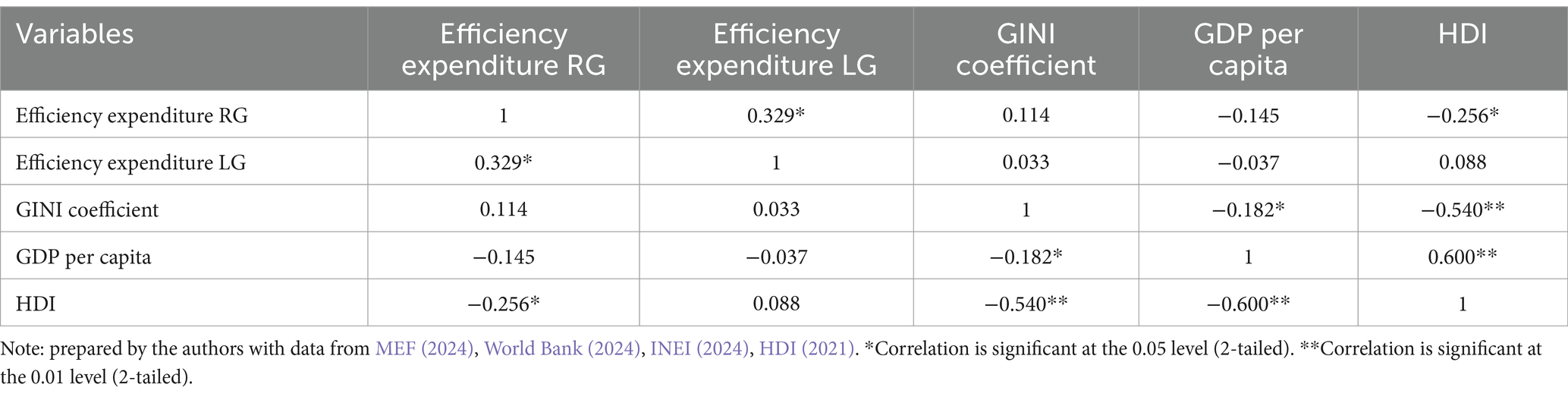

Following the Kolmogorov–Smirnov normality test, Pearson’s R correlation coefficient was calculated to assess the association between the public finance governance indicators of regional and local governments, both among themselves and in relation to fiscal centralism and the frequency of social conflict (see Table 1). Based on the significant correlation coefficients, five linear regression models were tested to examine whether any variables could help explain the causal relationship between social conflict, centralism, and fiscal governance (see Table 2).

Table 1. Association of sub-national fiscal governance with social conflict and fiscal centralism and decentralization.

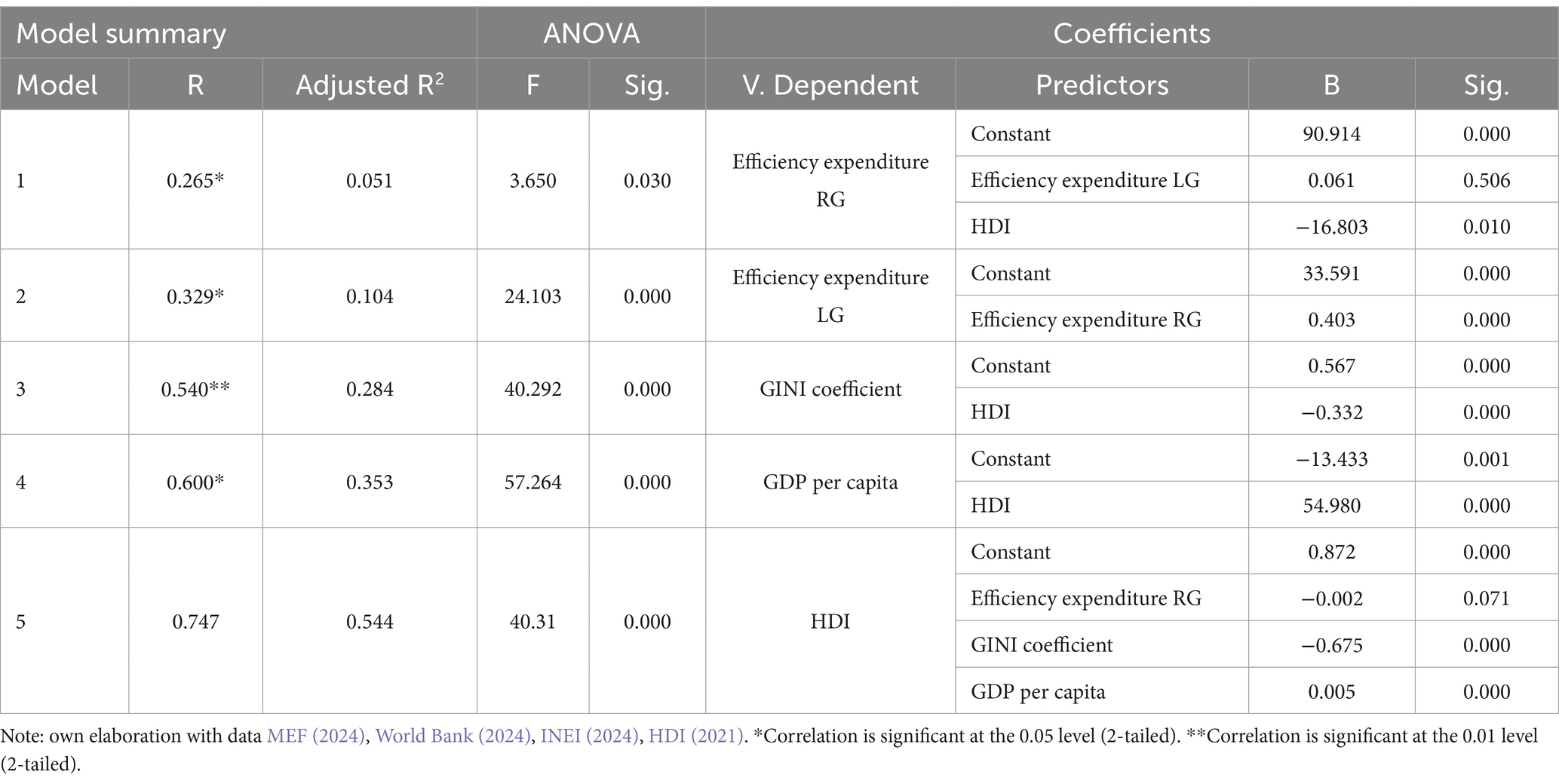

Table 2. Linear regression models related to social conflict, centralism and fiscal governance.

The use of secondary data is essential in economic and social research due to: its availability and reliability, which allows access to official data systematized by national agencies, ensuring their validity. It also allows for temporal and comparative analysis, facilitating the study of trends over time, in this case, between 2016 and 2023, allowing for the evaluation of the evolution of social conflict and fiscal centralism. The level of representativeness provides aggregated data at the national and subnational levels, allowing for a more complete assessment of fiscal governance and spending efficiency.

The analysis of budget execution and public spending is key to assessing how subnational governments manage their resources in contexts of instability. Its importance lies in: measuring the degree of efficiency in the allocation and use of resources, identifying patterns of deficiency in the allocation of public funds, and evaluating the relationship between budget execution and the quality of public services.

The use of the GINI coefficient allows for the measurement of economic inequality within each subnational government, a factor that can influence social conflict. GDP per capita represents the level of economic development and wealth-generating capacity, which directly impacts tax collection and spending efficiency. The HDI integrates key aspects such as education, health, and income, providing a holistic view of human development and its link to the quality of government. At a general level, these indicators allow us to assess the socioeconomic conditions of regions and their relationship with fiscal governance.

The selection of the Gini index, GDP per capita, and the Human Development Index (HDI) as key variables to evaluate the efficiency of public spending and the quality of financial management is based on their ability to comprehensively and complementarily reflect the socioeconomic impacts of the State’s fiscal and budgetary decisions. These indicators not only reveal aggregate economic outcomes but also capture dimensions related to income distribution and human well-being, offering a holistic perspective on the effects of public spending.

First, the Gini index is a key variable to consider in this study, as one of the primary objectives of efficient public spending is to enhance social equity. Well-targeted public expenditure—particularly in sectors such as health, education, and social protection—should be reflected in a reduction of inequality. Therefore, by monitoring the Gini index, it is possible to assess whether fiscal policies have effectively contributed to greater distributive justice, an essential component of high-quality public financial management.

Secondly, Gross Domestic Product (GDP) per capita is a fundamental indicator, as it serves as a key reference for assessing the efficiency of public spending in terms of economic growth. A sustained increase in GDP per capita may indicate an efficient allocation of public resources that fosters productivity, infrastructure investment, human capital development, and innovation. When analyzed in conjunction with other indicators, it allows for the evaluation of whether economic growth has been accompanied by improvements in equity and the population’s living conditions.

Finally, the Human Development Index (HDI), as a composite measure, allows for an analysis that goes beyond purely economic dimensions. Its use is particularly relevant for evaluating the quality of public spending, as it reflects the extent to which public investments enhance human capabilities and expand individual opportunities. An increase in the HDI can largely be attributed to effective public policies and sound financial management that prioritize the comprehensive development of the population.

Together, these three indicators enable a balanced assessment of economic efficiency, social equity, and human development, making them ideal tools for analyzing the quality of public spending. Their complementary nature allows for a multidimensional interpretation of the impact of public finances, aligned with the principles of sustainability, accountability, and effectiveness that should guide state management in the use of public resources.

Finally, the use of the Pearson R correlation coefficient allows us to determine the strength and direction of the relationship between social conflict, fiscal centralism, and fiscal governance efficiency. It also allows us to identify significant correlations between budget execution and socioeconomic indicators and statistically support hypotheses about the impact of political and fiscal instability on the performance of subnational governments.

3 Result and discussion

3.1 Efficiency of sub-national government public expenditure

The public budget transfers to the financial level the public policies, development plans, objectives and goals that the State has proposed to materialize in a calendar year, through its three levels of government (Eslava et al., 2019). It includes both the collection of income from all sources: ordinary resources (RO: Corresponds to income from tax collection and other concepts), directly collected resources (RDR: Includes income generated by public entities and directly administered), determined resources (RD: Corresponds to the income that the budgetary documents must receive, in accordance with the Law, for the economic exploitation of natural resources extracted from their territory and other concepts), donations and transfers and resources from credit operations. Sub-national governments have taxing power only over DCR, although they receive DR by transfer from the public treasury and need collateral to obtain credits (Zacnich, 2022).

The execution of public spending in Peru, including sub-national governments is based on the principles of the National Budget System: budget balance, fiscal balance, operational decentralization, fiscal responsibility, fiscal sustainability, restriction of discretion in budget execution to what is allocated, to the purpose for which they have been authorized, oriented to human welfare and environmental conditions, with criteria of efficiency, equity and probity (D. Leg, 2018; gob.pe, 2024).

The evaluation of the efficiency of public spending, in the framework of the results-based budgeting approach, in force in Peru since 2018, seeks to link the allocation and application of public resources with the improvement of the welfare of the target population or its environment or its capacity for improvement (MEF, 2024). This, in operational terms, consists of relating the allocation and level of expenditure execution with performance indicators of the results and outputs of the different Budget Programs designed using the Results-Based Budgeting approach. Additionally, it facilitates the comparison between the progress of performance and the financial execution of each budget program.

The need for the adoption of this approach can be seen in (Chávez, 2019), who argues that the budget for results corrects “the gaps of the traditional budget, through the articulation of Output and Outcome, applying criteria of efficiency and equity.” In addition, (Vargas and Zavaleta, 2020) confirmed a direct and significant relationship between performance budget management and expenditure quality, with a practically high correlation coefficient: 0.69.

In the country, 80% of the public budget is managed under the results-based budgeting approach, but the expected results have not been achieved; possibly due to the gap between actual and expected performance, particularly in the improvement of Budget Programs, in aspects such as the cultivation of a results-oriented organizational culture, explicit precision of objectives in budget programs, adoption of decisions based on verifiable and measurable evidence, as well as the establishment of an adequate value chain (Arana and Huaman, 2020).

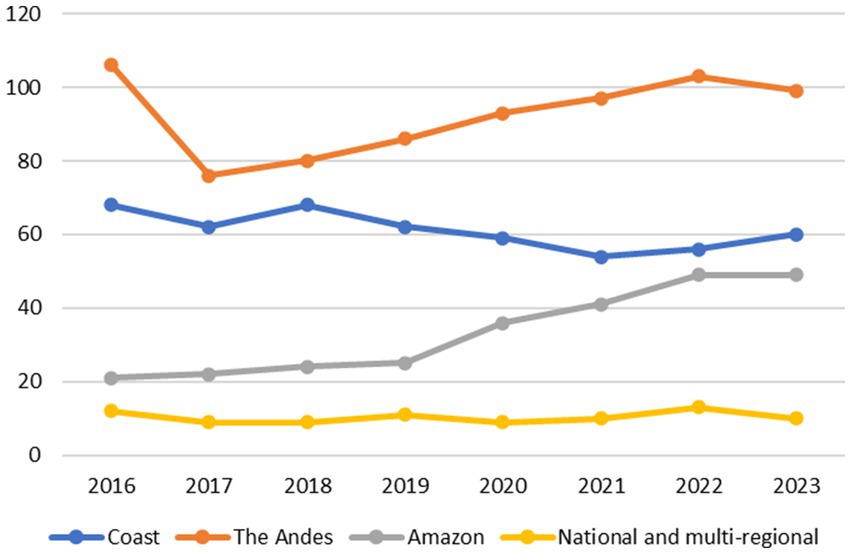

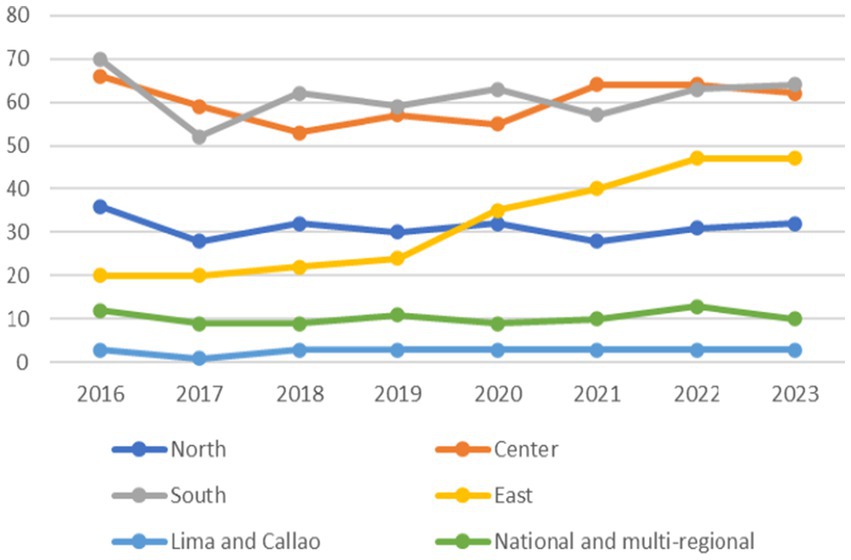

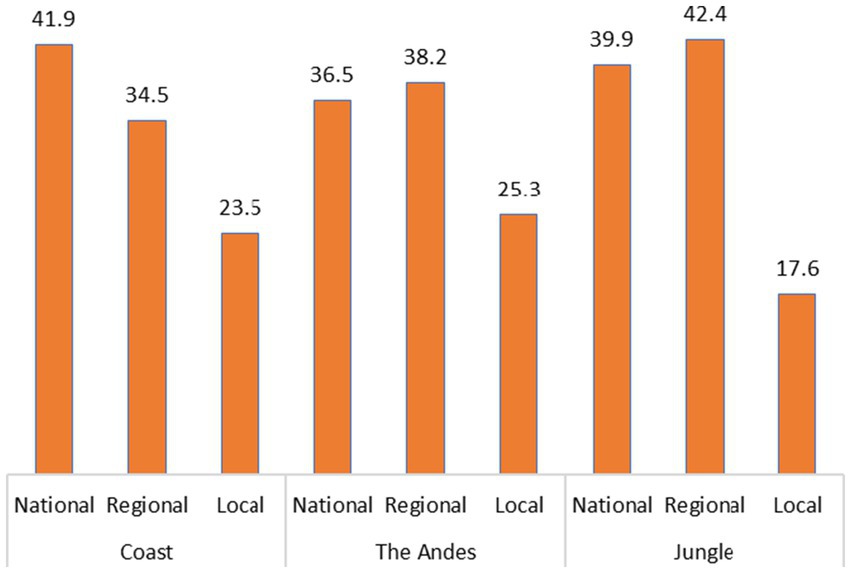

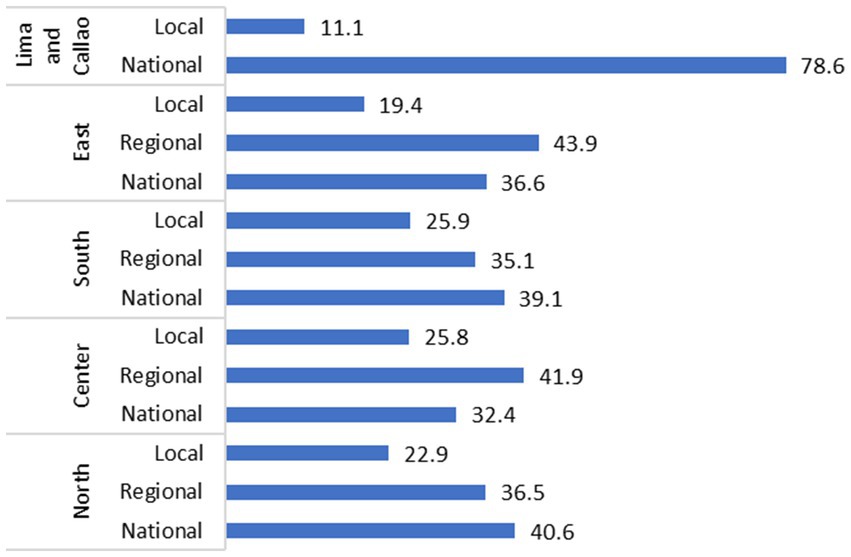

According to the report (MEF, 2024), the progress of the execution of the national government’s expenditure budget in the macroregional areas (Northern Region, Southern Region, Central Region, Eastern Region and Lima and Callao) and in the natural regions (Coast, The Andes and the Amazon), exceeds 90%, closely followed by the regional governments; however, local governments lagged behind, reaching only around 70% (see Figure 1); which would be equivalent to the non-attention of 30% of the demands by local governments and more or less 10% by the national and regional governments, despite the budgetary availability for this purpose. From a macro regional perspective (see Figure 2), the highest percentage of budget execution corresponds to the national government, in Lima and Callao it reached 93%, the lowest was in the north: 87.1%. The execution of the regional governments is also of second order. The efficiency of local government execution, including those of Lima and Callao, is around 70%.

Figure 1. Efficiency of public expenditure execution in percentages by natural regions and levels of government, 2016–2023. Note: prepared by the authors with data from MEF (2024).

Figure 2. Efficiency of public expenditure execution in percentages by macro regions and levels of government, 2016–2023. Note: prepared by the authors with data from MEF (2024).

The above statement is supported by the fact that the budget allocated to regional and local governments, whose expenditures are directed towards exclusive and shared competencies established by Law 27783, the Law of Regionalization, is limited. The Regional Government is tasked with planning the comprehensive development of its region and implementing the corresponding socioeconomic programs, while Local Governments are responsible for planning and promoting both urban and rural development within their jurisdiction. However, the largest portion of the development and welfare budget is allocated and centralized in the Ministries of Education, Health, and Development and Social Inclusion, which manage budgetary programs at the national level.

In addition to the designations as departments or macro regions South, North, Center and East, Lima and Callao are considered separately because they are the metropolises with the highest population concentration, largest budget allocation, highest GDP production, concentration of all government organizations, in addition to being the seat of the national government and Callao as a Constitutional Province with the main port of the country and a strategic location for the concentration of international trade companies.

Peru has 24 departments, including Metropolitan Lima, as well as the Constitutional Province of Callao, which has a regional government but does not belong to any department. There is also Lima Provincias, which does not fall under the regional government of its homonymous department; instead, its municipality holds the powers and responsibilities of a regional government, although it is excluded from the regionalization process. These geographical designations are established in the Law of Regionalization Foundations, which grants political, economic, and administrative autonomy.

These results are usually attributed to inefficient performance in public expenditure management, among others, due to the executive limitations of administrative personnel in terms of the management of administrative systems, but mainly due to the political and economic interests of the actors in each government. In recent years, although the execution of the public budget has increased, the efficiency of public spending has not (Niño de Guzmán, 2022). On the other hand, Escobar et al. (2021) found that “regional governments present worse investment management performance than local governments, since the decrease is 5.53 and 1.30%, respectively.” These findings ratify the insensitivity of sub-national governments to resolve the claims and aspirations of their regional or local fellow citizens, as stated in the previous paragraph.

The efficiency of public spending is conceptualized as the capacity to use the resources allocated by the State to meet its objectives and is a fundamental aspect of the country’s fiscal policy, consistent with the methodology established by MEF (2024), has been evaluated based on three indicators: GDP per capita by department, at 2007 prices (INEI, 2024), with the purpose of estimating whether sub-national public expenditures induced an improvement in the income of their inhabitants; the Gini coefficient to estimate whether such expenditures have induced a reduction in inequality among the inhabitants of each department (World Bank, 2024); and, the human development index (HDI), which involves the most recognized sub dimensions to measure such development (HDI, 2021).

Public spending includes both current and capital expenditures or public investment. The efficiency of public spending by regional governments is positively related, although low, with the efficiency of local government spending, which is attributable to the beneficial effect of cooperation between both sub-national governments; on the other hand, it is negatively related, and also low, with the HDI, reinforcing the theory of the vicious circle of poverty (López, 2021), which will only be broken if the capacities of the poor are strengthened. In addition to the HDI, this is positively and moderately related to GDP per capita; and negatively and moderately related to the GINI coefficient. Explainable, because both indicators are also economic components of the HDI.

In Peru, the low effectiveness of local government actions cannot be attributed to a single cause, but rather to a combination of structural, institutional, and managerial factors. One of the key issues lies in the financing structure, which heavily relies on transfers from the central government and non-recurring revenues, such as the mining canon. This dependence limits fiscal autonomy and leads to short-term planning, often disconnected from the actual territorial needs.

This is compounded by inefficient public spending, reflected in limited budget execution, low technical capacity, deficiencies in project formulation and low transparency in management. In many cases, local governments lack qualified personnel and modern control and monitoring systems.

Other relevant factors include territorial fragmentation, weak articulation between levels of government and lack of effective citizen participation. All of this creates an environment where the allocation of resources does not necessarily translate into tangible improvements for the population. Overcoming these challenges requires comprehensive reforms that strengthen local capacities, promote effective decentralization and improve territorial governance.

The efficiency of regional government public spending, by itself, is not determinative of human development; the same is true for GDP per capita, not to mention the efficiency of local government public spending, due to its low correlation with HDI (see Table 3); instead, it is close to the highly negative determination of the Gini coefficient (see model 5 in Table 4). Together, the efficiency of sub-national public spending, inequality and per capita income explain 54.4% of the variations in human development.

Table 3. Association of sub-national public expenditure efficiency with the GINI coefficient, GDP per capita and HDI.

Table 4. Linear regression models related to subnational spending efficiency, GINI coefficient, GDP per capita and HDI.

In turn, human development explains 35.3% of GDP per capita and 28.4% of inequality (see models 3 and 4 in Table 4); on the other hand, the efficiency of local government spending, together with human development, explains only 5.1% of the efficiency of regional government spending (see model 1 in Table 4); and, conversely, the efficiency of regional government spending explains only 10.4% of the efficiency of regional government spending (see model 1 in Table 4). 1% of the efficiency of regional government spending (see model 1 in Table 4); and, conversely, the efficiency of regional government spending explains only 10.4% of the efficiency of local government spending (see model 2 in Table 4).

The heterogeneity of the efficiency of public spending among the different levels of government is notorious (see Figures 1, 2); but in addition, (Niño de Guzmán, 2022) found a decrease in the acquisition of capital goods, stagnation of HDI; highlighting that a higher level of fiscal spending, even more efficient, is not necessarily accompanied by better results in sustainable sub-national development. In this regard, it suggests the adoption of stronger sub-national institutional frameworks, well-defined political rights, and better coordination between levels of government. To some extent, our findings are consistent with those of this author.

3.2 Impact of social unrest on sub-national fiscal governance

Sub-national social conflict in Peru is the challenge of society, particularly sub-national, to the authoritarian and centralist actions of the country’s economic, political and social elites. From the perspective of fiscal governance, it is commonly the result of the neglect or non-compliance with the right to sustainable development of a locality or region, due to the misuse of public resources by those who are obliged to do so. One trigger is the neglect of environmental sustainability assurance by the State and by those who use those resources. More than 60% of social conflicts are environmental (Ombudsman’s Office, 2024). A second is the dishonest actions of authorities and public officials at all levels of government. It can be triggered by the suspicion or prosecution of authorities for the “misuse of public funds and corruption crimes” (Quispe E., 2021), authoritarian practices, manipulation of processes, passivity, collusion, etc.

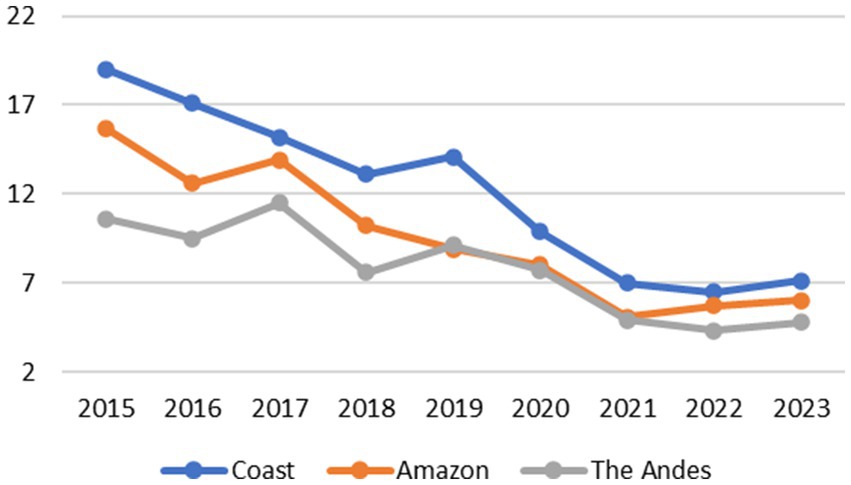

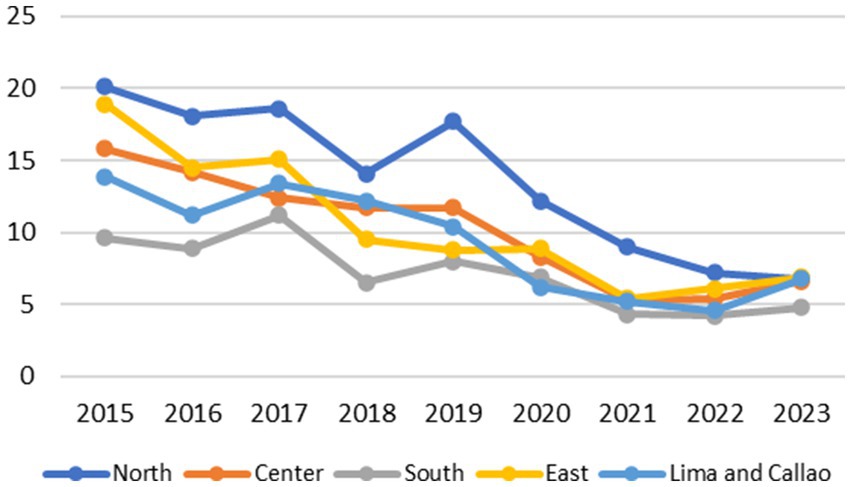

In the regions and localities, with the exception of the provinces of Lima and Callao, social conflict began to exacerbate as of 2016, on a par with political instability. By region, after a short decline in 2017, social conflicts in the Andean departments escalated again to more than a hundred in 2022. Conflict in the Amazon, doubles in 2022 and 2023. On the coast, the frequency of conflicts remained at low levels (see Figure 3). From a macro-regional perspective, social conflict in the center and south remained much higher than in the north, and much higher in the provinces of Lima and Callao. In the eastern departments it escalated to double (see Figure 4).

Figure 3. Peru: dynamics of social conflict 2016–2023 by natural regions. Note: own elaboration with data from Ombudsman’s Office (2024).

Figure 4. Peru: dynamics of social conflict 2016–2023 by macro-region. Note: own elaboration with data from Ombudsman’s Office (2024).

The departments with the most conflicts were: Loreto: 17, Ancash: 16, Cusco: 15, Apurímac: 13, Puno: 13, Piura: 10, Cajamarca: 9, Ayacucho: 8, Junín: 7. These departments are the ones where natural resource extraction is most intense, mining in the Andes and forestry in the Amazon. This is corroborated by the fact that the socio-environmental type is the most frequent.

By level of responsibility and competence, about 60% of these conflicts correspond to the national government to manage and resolve them, 30% to regional governments and 10% to local governments (Ombudsman’s Office, 2024). In Peru, the effective implementation of public policies is limited; for example, social programs focused on the social development of a broad spectrum of regions and localities were not effective (Caldas et al., 2021); probably due to the centralism with which these programs are designed and directed. Then, it could be valid to attribute social conflicts to the public policies of the national government. Particularly, from 2016 to the present, political instability has hindered the introduction of adequate public policies; although it should be recognized that these are generally often incompatible with sub-national cultural practices and environmental settings (Alanoca and Apaza, 2018). In this context of political instability, it is undeniable that the national government is delegitimized to seek consensus about public policies aimed at sustainable development, nor does it have the capacity to deepen or innovate public policies for the modernization of the State, let alone extend it to regional and local governments (Cruz et al., 2023).

Sub-national social conflict between 2016 and 2023 negatively impacted, although not significantly, the capture of directly collected resources (DCR) of regional and local governments (see Table 1), as well as fiscal centralism; and positively the fiscal decentralization of local governments. This finding reveals the presumption of the negative effects of social conflicts on the governance of sub-national public finances; statistically irrelevant for the moment, but which may become significant if conflict escalates further. The aforementioned reduced statistical significance can be attributed to several other factors, such as the taxing power and fiscal efforts made by regional and local governments to collect DCRs, as well as the tax base for it.

Despite what can be deduced from the second paragraph of Article 74 of the Constitution of the Republic, the underlying legal norms restrict, one could say annul, the taxing power of regional and local governments (Ruiz, 2009). The DCR of the regional governments come almost exclusively from the income from their properties, taxes and provision of services; thus, their financing in the last 5 years “relied almost entirely on transfers from the National Government” (Zacnich, 2022). In local governments, such revenues are collected through municipal taxes regulated by the Congress of the Republic, such as property tax, vehicle tax, betting tax, alcabala and others, as well as fees and contributions for the public services they provide.

Under the current regulatory framework, the possibility of moving towards fiscal autonomy is practically nil for regional governments. Local governments also have their taxing power curtailed, but at least they have relative autonomy to establish their own mechanisms and strategies for collecting their DCR. Claiming real decentralization on this understanding is illusory (Quispe et al., 2023). It is time to break the structures, the wall, more than a “rudder blow” (Cruz et al., 2023) so that decentralized fiscal governance flows through natural channels; that is, autonomous, effective, efficient, compatible with its context; and only in this way will it also contribute to solve the endogenous problems of sustainable development in the diversity of the country’s regions and localities.

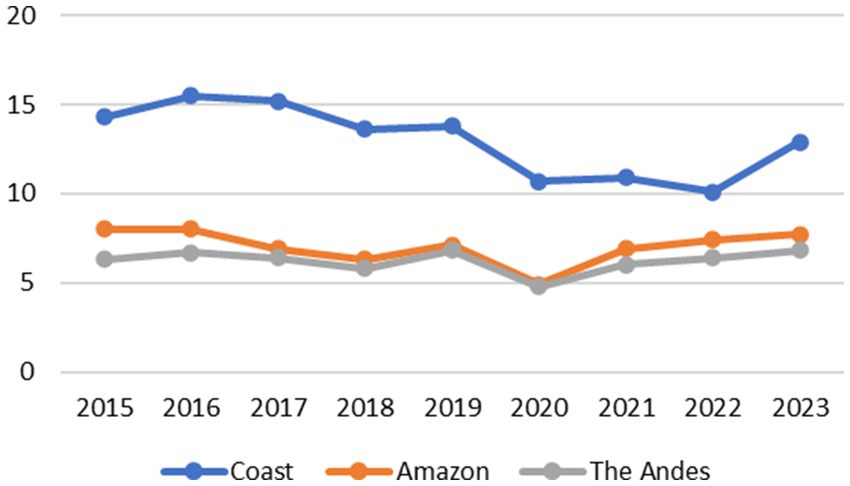

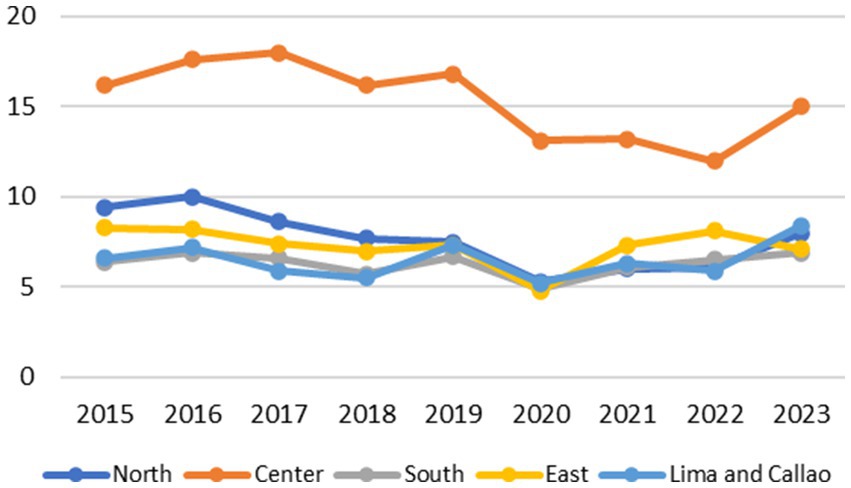

The uptake of DCRs from regional governments decreased ostensibly from 2015 to 2023, in the departments of the three natural regions; the same, from the macro regional perspective, from 20 to less than 8% (see Figures 5, 6). That decrease is smaller in local governments, from an average of 8% in 2016 to less than 6% in 2020. The DCRs of the local governments of the provinces Lima and Callao, is definitely much higher than the other municipalities in the country; their drop in this difficult time trance was also remarkable: from 18% in 2018 to 12% in 2022 (see Figures 7, 8). This finding, apparently corroborates the different parameter of taxation power between regional and local governments, reinforcing the need to abide by the letter of the mandate of Art. 74 of the Political Constitution of the State.

Figure 5. DCR of local governments by natural regions (%). Note: prepared by the authors with data from MEF (2024).

Figure 6. DCR of the regional governments by macro regions (%). Note: prepared by the authors with data from MEF (2024).

Figure 7. DCR of the regional governments by natural regions (%). Note: prepared by the authors with data from MEF (2024).

Figure 8. DCR of local governments by macro-regions (%). Note: prepared by the authors with data from MEF (2024).

DCR collection depends on the tax base and the fiscal effort made by regional and local governments, either to broaden the base or to make collection more effective. The tax base is made up of the value of assets, the activities carried out by taxpayers or the public services they receive. The greater the economic development, the greater the availability of human capacities, urban planning, services, material, environmental, cultural, technological resources, etc., the greater the possibility of collecting and broadening the tax base. The tax effort is related to the collection strategies that may be adopted by regional or local governments, within the framework of tax principles such as equity, uniformity, among others (Quispe E. M., 2021). In a research study conducted in 15 cities of the Peruvian Andes, Orihuela and Quispe (2021) found that the following have a positive influence on the local tax base: urban population, modern markets, commercial and service production centers, and per capita income; and a negative influence on the magnitude of poverty. Tax governance is influenced by institutional capacity in the form of specialized human resources (Orihuela and Quispe, 2021).

In isolation, it is estimated that social conflict determines only 3.7% of the DCR collection of regional governments and 13.8% of local governments, 8.4% of fiscal centralism and 11% of fiscal decentralization of governments; but together with other variables, this determination is moderate if not high (see models 3, 4 and 5 in Table 4). On the other hand, the fiscal governance variables: DCR collection, centralism and fiscal decentralization determine 22.6% of social conflict. This finding corroborates that, even in a scenario without social conflict, sub-national governments are unlikely to achieve an effective collection of their DCRs, in the first place, but also to move towards effective governance of their fiscal autonomy. In short, the current regulatory framework on the taxation powers of sub-national governments does not contribute to an effective decentralization of public finances (see model 7 in Table 2). The DCR of regional governments decreases the frequency of social conflicts by 0.157, that of local government by 0.33; on the other hand, fiscal centralism increases the frequency of social conflicts by 0.103 and fiscal decentralization of local governments by 0.352. It is explained that the greater DCR contributes to improving the attention to the needs of the population, but centralism hinders it. Fiscal decentralization increases social conflict because citizens distrust the proper administration of public funds by their rulers (Quispe E., 2021).

3.3 Impact of fiscal centralism on the efficiency of subnational public spending

Centralism was defined at the beginning of the century by Contreras (2001) as the political regime that hierarchizes the geopolitical spaces into which the country is divided, articulates the exercise of power, socioeconomic, cultural, political and institutional activities around an urban center, at the same time market, of large dimensions; on the other hand, decentralization implies the equitable, autonomous and sustainable exercise of political and economic powers, and other dimensions of sustainable development. On the factual level, in terms of geopolitical spaces, the visible face of centralism in Peru is metropolitan Lima and Callao, which concentrate the most decisive political and administrative powers of the country, more than 30% of the Peruvian population, is the largest market for all goods and services and enjoys comparative advantages that allow it to claim socioeconomic, political and institutional leadership in the country.

Fiscal centralism consists of concentrating the exercise of public finances in a central government entity, such as the Ministry of Economy and Finance, which particularly dictates the processes and criteria for tax collection and the execution of public spending; on the other hand, fiscal decentralization demands that sub-national governments have fiscal autonomy and self-sufficiency, as well as the capacity for self-government of their finances.

The importance of the national government’s public spending is greater in the coastal departments and less in the Andean departments (see Figure 9); that of the regional governments is greater in the Amazon, and even exceeds that of the national government. This importance is far less in the local governments of the three natural regions, but even less in the Amazon. From a macro-regional perspective, this importance is by far greater in the provinces of Lima and Callao (see Figure 10), thus reiterating fiscal centralism. The relevance of the national government is less than half in the central macro region.

Figure 9. Average public expenditure execution by natural regions and levels of government, 2015–2023 (%). Note: prepared by the authors with data from MEF (2024).

Figure 10. Average public expenditure execution by macro regions and levels of government, 2015–2023 (%). Note: prepared by the authors with data from MEF (2024).

Among other points on the agenda, in the recent social conflict, the discontent of the citizens of the periphery, that is to say of the macro regions of the south and center mainly, with respect to the competitive advantages of metropolitan Lima and Callao, was perceived and confirmed. It is noted that the “taking of Lima” is the consequence of the absence of an effective response from the State to the requirements of the population regarding public goods and services, public investment projects, human rights, the rule of law, etc., particularly in the regions and localities; “therefore, the need is identified to strengthen the mechanisms of foresight and resolution of social conflicts in order to guarantee the right of people to their use and enjoyment” (Castilla and Benavides, 2023).

The centralist tradition of the Peruvian State is so deeply rooted that all sub-national authorities perceive the need to go to the offices of national government authorities and officials to “process” technical and administrative attention to solve the problems and demands of their fellow citizens, including regional and local development projects (Quispe et al., 2023). The imbalance of power is such that even in this conflictive time between the center and the periphery, a recentralization of sub-national public finances seems to have been conceived or faced. The economic and political power of the Peruvian elites concentrated in Lima and Callao have mediatized the voices of protest from the “provinces of the interior.”

Indeed, as expected from the previous literature review, the relationship of fiscal centralism is high and negative with the fiscal decentralization of local governments. This relationship is moderate, but also negative with the fiscal decentralization of regional governments (see Table 1). Fiscal centralism is positively and highly significantly related to the uptake of DCRs by local governments; that is, greater fiscal centralism drives local governments to optimize their fiscal governance processes. It is also positively related to the efficiency of local governments’ public expenditure execution, although in a less than moderate way; that is, the more fiscal centralism, the more efficiently local governments try to execute their financial resources. Consistent with theory and common economic reasonableness. However, it does not seem to be consistent with the fact that greater centralism corresponds to a decrease in social conflict, albeit at a low level. With the necessary reservations, the concurrence of real or perceived coercive mechanisms in sub-national budgetary governance could be presumed.

In isolation, fiscal centralism determines 52.2% of local government fiscal decentralization, 38.6% of regional government fiscal decentralization, 54.3% of local government DCRs, 6.7% of local government budget execution efficiency and 8.4% of social conflicts.

With an approximation level of 52.2%, the response of local government fiscal decentralization to fiscal centralization can be estimated (see model 11 in Table 2). For every ten percentage points that fiscal centralization increases, local government fiscal decentralization decreases by 3.81%. The remaining 47.8% is attributable to factors not studied in this paper. Similarly, it can be estimated how fiscal centralization determines the importance of DCRs in local government budgets (see model 13 in Table 2). With a low level of approximation, only 38.6%, the response of fiscal decentralization of regional governments to fiscal centralism can also be determined (see model 12 in Table 2).

4 Conclusion

The efficiency of public spending by sub-national governments has a rather limited impact on the development and welfare of the populations of the regions and localities.

It is notable that local governments in the provinces of Lima and Callao show a considerably higher DCR collection capacity than other municipalities in the country. These results seem to support the significant difference in taxation power between regional and local governments, which underlines the importance of complying with the mandate established in Article 74 of the Political Constitution of the State.

The effective implementation of public policies in the country is limited, which has led to a lack of effectiveness in social programs designed for social development in various regions and localities, possibly due to centralism in the planning and execution of these programs and the social conflicts that have intensified since 2016.

Even in a scenario without social conflict, sub-national governments are unlikely to move towards effective governance and fiscal autonomy, due to the contradictory policies of the State regarding fiscal decentralization.

This finding suggests the presumption of negative effects of social conflicts on the governance of subnational public finances, although for the moment these effects are statistically irrelevant, they could become significant if conflict escalates further.

Data availability statement

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

Author contributions

JM: Investigation, Methodology, Software, Writing – original draft, Writing – review & editing. TL: Conceptualization, Formal analysis, Investigation, Methodology, Writing – original draft, Writing – review & editing. MC: Conceptualization, Formal analysis, Investigation, Methodology, Supervision, Writing – original draft, Writing – review & editing. JR: Conceptualization, Formal analysis, Resources, Supervision, Visualization, Writing – original draft, Writing – review & editing. GS: Formal analysis, Investigation, Methodology, Resources, Visualization, Writing – original draft, Writing – review & editing. NV: Conceptualization, Data curation, Formal analysis, Investigation, Visualization, Writing – original draft, Writing – review & editing. NZ: Formal analysis, Investigation, Resources, Supervision, Writing – original draft, Writing – review & editing.

Funding

The author(s) declare that no financial support was received for the research and/or publication of this article.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Alanoca, V., and Apaza, J. (2018). Knowledge of environmental protection and discrimination in the Aymara communities of Ilave. High Andean Res. J. 20, 95–108. doi: 10.18271/ria.2018.333

Arana, P., and Huaman, K. (2020). Analysis of the factors in the implementation of the budget for results (BfR) reform in Peru at the national level by 2019. In PUCP (Vol. 1). Available online at: https://www.contraloria.gob.pe/wps/wcm/connect/CGRNew/as_contraloria/as_portal/Conoce_la_contraloria/Normatividad/NormasControl/ (Accessed February 18, 2024).

Baylon, E. G., and Quispe, Y. (2022). Progress and limitations in decentralization, new challenges through governance. Cienc. Latina Multidiscip. Sci. J. 6, 1287–1306. doi: 10.37811/cl_rcm.v6i4.2661

Caballero, V. (2023). Peru has a permanent political instability that is having an impact on the economy. Regional Communication Network. Available online at: https://www.rcrperu.com/victor-caballero-el-peru-tiene-una-inestabilidad-politica-permanente-que-esta-impactando-en-la-economia/ (Accessed October 15, 2023).

Caldas, R., Santa, B. C., and Castillo, F. W. (2021). Territorial governance for sustainable development in Peru. Met. J. Appl. Sci. 4, 47–54. doi: 10.62452/zj9dnv26

Castilla, J. G., and Benavides, A. M. (2023). Social conflict against public goods: between the right to protest and public use. ESCPOGRA PNP 2, 1–13. doi: 10.59956/escpograpnpv4n1.1

Chávez, E. L. (2019). ESSALUD budgetary execution in Peru as a management instrument. Crit. Thinking 24, 103–120. doi: 10.15381/pc.v24i1.16561

Contreras, C. (2001). Peruvian centralism in its historical perspective. Iep, 1–22. Available online at: https://repositorio.iep.org.pe/bitstream/IEP/810/2/documentodetrabajo127.pdf (Accessed May 30, 2022).

Cosme, J. (2018). The objectives of sustainable development and the academy. Medisan, 22, 1089–1100. Available online at: http://scielo.sld.cu/pdf/san/v22n8/1029-3019-san-22-08-838.pdf

Cruz, M. A., Cortez, R., and Morales, A. (2023). The necessary and urgent “change at the helm” of public management in Peru. Apuntes 51, 37–65. doi: 10.21678/apuntes.96.1913

El Comercio. (2022). Political instability and weak governance put the Peruvian economy and its rating at risk. Available online at: https://elcomercio.pe (Accessed May 15, 2022).

Escobar, K. R., Terry, O. F., Zavaleta, W. E., and Zárate, G. E. (2021). Performance of subnational governments in the management of public investment in Peru. Venezuelan Manage. Mag. 26, 595–609. doi: 10.52080/rvgluz.27.95.10

Eslava, R. A., Chacón, E. J., and Gonzalez, H. A. (2019). Gestión del Presupuesto Público: alcance y limitaciones. Vis. Int. (Cúcuta) 2, 8–14. doi: 10.22463/27111121.2603

Galindo, M., and Medina, F. (1995). Fiscal decentralization in Bolivia. United Nations. Regional Fiscal Decentralization Project. CEPAL/GTZ, 10, 84. Available online at: https://repositorio.cepal.org/handle/11362/9691

Garcia, E., and Suárez, W. (2015). Governance in public administration: experience of the administrator of the energy social inclusion fund. FISE 3:29. Available at: https://www.fise.gob.pe

Gestión. (2023). Fitch on Peru: “political and governance uncertainty undermines private investment.” Gestion

gob.pe (2024). Municipal information up to date. Principles of the National Budget System. Available online at: https://www.gob.pe/34058-principios-del-sistema-nacional-de-presupuesto

Harman, U., Corilloclla, P., and Alayza, B. (2023). Towards a more inclusive science, Technology and innovation policy in Peru. Ibero-American J. Sci. Technol. Soc. CTS 18, 11–33. doi: 10.52712/issn.1850-0013-360

HDI. (2021). Human Development Index. Available online at: https://www.ipe.org.pe/portal/indice-de-desarrollo-humano-idh/ (Accessed May 15, 2022).

Huamán, P. L., and Medina, C. G. (2022). Digital transformation in public administration: challenges for active governance in Peru. Comuni@cción 13, 93–105. doi: 10.33595/2226-1478.13.2.594

INEI. (2024). Gross domestic product by departments, 2007–2022. Available online at: https://m.inei.gob.pe/estadisticas/indice-tematico/producto-bruto-interno-por-departamentos-9089/ (Accessed June 3, 2024).

Jurado, J., and Tasayco, D. (2021). Changes in geopolitics and territorial occupation: Peru 2000-2020. Scientia 23, 69–89. doi: 10.31381/scientia.v23i23.4554

López, G. (2021). The social Encyclic Laudato si’ as an radical answer to the breaking of the vicious circle of poverty and disease. Salmanticensis 68, 509–538.

LR Data. (2024). All IEP surveys. Available online at: https://data.larepublica.pe/encuesta_iep_peru/ (Accessed January 23, 2024).

MEF. (2024). Economic transparency Peru. Friendly Consultation MEF. Available online at: https://apps5.mineco.gob.pe/transparencia/mensual/default.aspx?y=2023&ap=ActProy (Accessed March 1, 2024).

Menchero, M. (2020). Instability, violence and tourism in Peru: an approach from the role of the state. Araucaria 22, 350–367. doi: 10.12795/araucaria.2020.i43.19

Niño de Guzmán, J. M. (2022). Analysis of the determinants of public spending efficiency at the regional level during the period 2015-2020 in Peru. PUCP.

OCDE. (2016). OECD public governance studies: Peru. Integrated Governance for Inclusive Growth. doi: 10.1787/9789264265226-es

Oliva, C. (2018). Public finance management in Peru. Economic Development Cooperation Program. doi: 10.1787/8b6b289c-es

Ombudsman’s Office. (2024). Social Conflicts Report. Available online at: https://www.defensoria.gob.pe/areas_tematicas/paz-social-y-prevencion-de-conflictos/ (Accessed May 20, 2024).

Orihuela, J. A., and Quispe, N. (2021). Determinants of the fiscal autonomy of the provincial municipalities that administer cities in the highlands of Peru [Universidad Nacional del Centro del Perú]. Available online at: https://repositorio.uncp.edu.pe/handle/20.500.12894/7909 (Accessed May 30, 2024).

Paredes, M., and Encinas, D. (2020). Peru 2019: political crisis and institutional outcome. Rev. Cienc. Polít. (Sant.) 40, 483–510. doi: 10.4067/s0718-090x2020005000116

Pinilla, D., Jiménez, J. D. D., and Montero, R. (2014). Fiscal decentralization in Latin America. Soc. Impact Determinants LXXIII, 79–110. doi: 10.1016/S0185-1667(15)30004-7

Quispe, E. (2021). Corruption, conflicts and crisis of democratic governance in Puno, Peru. Labor Soc., 22, 419–437. Available online at: http://www.scielo.org.ar/scielo.php?script=sci_arttext&pid=S1514-68712021000200419

Quispe, E. M. (2021). Effects of intergovernmental transfers on the generation of income of local governments: evidence for the case of Peru. Econ. Sem. 10, 11–31. doi: 10.26867/se.2021.v10i2.117

Quispe, E., Borda, W. Q., and Gebera, O. T. (2023). Recentralization, intergovernmental conflicts and territorial inequality: perspective of local governments in Peru. J. Public Admin. 57:57. doi: 10.1590/0034-761220220245x

Ruiz, F. (2009). Regional and local government taxing powers. Tax Law, 33, 1–9. Available online at: https://dialnet.unirioja.es/descarga/articulo/7792961.pdf

Tirard, M. (2020). Good governance of public finance and economic development. Giuristi Corp. Law Rev. 1, 308–317. doi: 10.46631/giuristi.2020.v1n2.05

Tumi, J. E. (2020). Accountability in the management of the municipal government of Puno-Peru (2011-2018). Comuni@cción 11, 63–76. doi: 10.33595/2226-1478.11.1.393

Vargas, J. A., and Zavaleta, W. E. (2020). La gestión del presupuesto por resultados y la calidad del gasto en gobiernos locales. Vision Future 24, 37–59. doi: 10.36995/j.visiondefuturo.2020.24.02.002.es

World Bank. (2024). Gini Index. Available online at: https://datos.bancomundial.org/ (Accessed February 14, 2024).

Zacnich, R. (2022). State of sub-national public finances in Peru. Comexperu. 1, 1–30. Available at: https://www.comexperu.org.pe/upload/articles/reportes/reporte-finanzas-publicas-001.pdf

Keywords: public expenditure efficiency, fiscal governance, subnational governments, fiscal autonomy, fiscal centralism, political instability, social unrest

Citation: Morales Rocha JL, Lauracio Ticona T, Coyla Zela MA, Ramos Rojas JT, Serruto Medina G, Vargas Torres NI and Zeballos Hurtado NJ (2025) Impact of social conflicts and fiscal centralization on fiscal efficiency and governance of subnational governments in Peru, 2016–2023. Front. Polit. Sci. 7:1451195. doi: 10.3389/fpos.2025.1451195

Edited by:

Alexander C. Tan, University of Canterbury, New ZealandReviewed by:

Ahmad Sururi, Sultan Ageng Tirtayasa University, IndonesiaMałgorzata Gałecka, Wroclaw University of Economics and Business, Poland

Copyright © 2025 Morales Rocha, Lauracio Ticona, Coyla Zela, Ramos Rojas, Serruto Medina, Vargas Torres and Zeballos Hurtado. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: José Luis Morales Rocha, am1vcmFsZXNyQHVuYW0uZWR1LnBl