Aamir Aijaz Syed

Aamir Aijaz Syed- Institute of Management, Commerce and Economics, Shri Ramswaroop Memorial University, Barabanki, India

This study intends to find out how the bank or industry-specific variables like banking regulation, banking efficiency, and banking operations affect non-performing loans in South Asia. To achieve this objective this study has employed robust 1st and 2nd generation Unit root tests, CIPS test, PMG and Dynamic Correlated Model approach on the panel data set of selected South Asian countries from 1995 to 2019, to avoid the implications of Cross-sectional dependency on the result analysis. The finding of the study shows that loose banking operations, lower exchange rate, and volatile interest rate have a significant positive relationship with non-performing loan whereas lower banking efficiency have a significant negative relationship with non-performing loans. The study also confirms the importance of cross-sectional dependencies in getting more accurate and robust results. This study will be useful for policy implementation and to understand the importance of micro banking variables in controlling non-performing loans, apart from contributing toward the literature of cross-sectional dependency.

Introduction

Banking Industry plays a key role in the development of an economy by accelerating the cycle of credit creation [1]. Over the years the banking industry around the world is suffering from the issue of non-performing loans, which are those loans that cease to generate returns. Non-performing loans not only created a negative impact on the bank balance sheet but also hampers further credit growth leading to lower investments and consumption levels in the society [2, 3]. Due to financial liberalization banks have become a central point for economic growth and this excessive dependency has created a burden on banking businesses. Bankers around the world are struggling with the problem of meeting their targets of credit creation leading to bad management practices, faulty know your customers' documentations, and finally ending with non-performing loans.

South Asian countries in the near future will be more dependable on domestic driven demand and domestic investments for their sustainable growth as projected by world bank. The Current corona outbreak will also impact considerably the growth fundamentals of South Asian countries. Thus, to revive the economic growth and investment options banks has to take the leading roles in term to credit creations resulting into chances of default loans.

Previous studies have segregated the major reasons or the determinants of non-performing loans into two categories i.e., bank-industry specific or macroeconomic factors. Researchers concluded in previous studies that macroeconomic factors are the major reason for non-performing loans which ultimately affect banking variables. Studies conducted by researchers like Bernanke et al. [4], Kyotaki [5], Rinaldi and Sanchis-Arellano [6] provided a theoretical relationship between inflation, consumption, economic growth, credit acceleration, and non-performing loans.

Apart from these views, there is another school of studies that pointed on micro or bank-specific factors. Such studies highlighted that sometimes due to bad management practices, bank inefficiencies and performance bank leads to non-performing loans. Some prominent researchers who contributed to these thoughts are Salas and Saurina [7] and Williams [8]. Berger and DeYoung [9] which is one of the oldest and prominent studies focusing on NPL determinants pointed out that bad management and moral hazard are also one of the reasons for increasing non-performing loans. The literature review section of this paper highlights a comprehensive detail of such studies, but during the review, it been found that almost all the studies suffer from some sort of criticism either in terms of variables selection or in terms of method of analysis.

Based on the previous review this study focus on the industry or bank-specific determinants of non-performing loans as these segments is still not so thoroughly investigated. This study tries to study how bank efficiency (in context to profitability), banking regulations (in context to regulatory capital), and operations (in context to credit creation) affect non-performing loans in South Asia, covering the period from 1995 to 2019 and by employing the dynamic common correlated effect (DCCE) panel approach.

This study is novel and will be very helpful for researchers, academicians, and policymakers, as this study empirically shows that how banking regulations, efficiency, and operations affect banking performance in terms of non-performing loans by using a new theoretical DCCE approach which provides authentic result in case of cross-sectional dependency among time-series data, thus adding a new dimension to the previous work of bad management practices. The sample countries which are taken for analysis are also unique as they meet the similar banking, economic and environmental conditions thus provide more robust results apart from adding a new region of analysis as previous work is mainly focused on certain developed and developing countries. Along with this the period of study is also unique as the world is facing corona outbreak and banking is the only medium to revive the economy thus studying banking variables and its effect on the non-performing loan will add a new paradigm in the current scenario apart from that there is no conclusive study in South Asia which has covered the data of last 25 years, the time period during which most of the countries has witnessed global financial recession, the surge in globalization and financial internationalization.

The paper proceeds as follows, section Review Literature focuses on review literature and theoretical framework, section Methodology and Data Analysis focus on data methodology and empirical analysis, section Findings and Discussion covers results, and lastly, section Conclusion and Recommendation covers the concluding remarks.

Review Literature

Various studies have been conducted focusing on the macroeconomic determinants and their impact on non-performing loans but there are very few studies that focus exclusively on the banking specific determinants and their impact on non-performing loans. So this section of the study will only focus on the impact of banking specific variables on non-performing loans.

One of the oldest studies which were focused on studying the impact of banking variables on non-performing loans was conducted by Berger and DeYoung [9] on US banks and covering the period from 1985 to 1994. The findings suggested that bad management, skimming, and lack of adequate capital adequacy are the prime causes of an increased amount of non-performing loans in US commercial banks. Keeton and Morris [10] in his work on the commercial banks of the United States from 1982 to 1996 also supported the findings of Berger and DeYoung [9].

Jimenez and Saurina [11] performed a similar study on the Spanish banking sector from 1984 to 2003 using a dynamic model. The findings of the study concluded that lenient credit terms during the boom period of economic growth ultimately result in huge bad loans at times of recession.

Hu et al. [12] conducted a study on the panel data set of Taiwan commercial banks covering the data from 1996 to 1999. The findings of the study suggested that bank size is inversely related to non-performing loans. Similar findings were also reported by Rajan and Dhal [13] which concluded that disbursement of credit and size of the bank has a significant effect on the non-performing loans in Indian commercial banks.

Espinoza and Prasad [14] investigated 80 banks of GCC(Gulf Cooperation Council) countries using dynamic panel data and covering the time frame from 1995 to 2008. The study concluded that the interest rate charged by banks and credit disbursement has a direct effect on the increasing non-performing loans. Nkusu [15] also supports the findings of Espinoza and Prasad [14], that the banking loan portfolio is major determinants which affect non-performing loans among the dynamic panel of developed and developing countries.

Podpiera and Weill [16] analyzed the role of cost efficiency and management discipline among the Czech banking industry, covering the period from 1994 to 2005. The findings of the study suggested that banks should focus more on managerial efficiency to control non-performing loans. Swamy [17] also strengthen the above findings by conducting a similar study which was focused on Indian commercial banks. The study concluded that banking credit terms have a significant impact on non-performing loans apart from other macroeconomic variables.

Some of the recent studies which were focused on Banking variables and non-performing loans are Khaled Subhi Rajha [18] which studied Jordanian banking sector and Umar and Sun [19] which was focused on the Chinese banking sector, Pop et al. [20] which explored the determinants of NPL in Romania over the period 2007–2016 and Koju et al. [21] which examined the internal determinants of NPL(Non-Performing Loans) in Nepal over the period 2003–2015. The major findings of all the above studies were that inefficiency in banking practices, low productivity, and size of banks have a profound impact on the non-performing loans in the above regions. Apart from the above, the prominent studies which are also conducted on similar variables are Boudriga et al. [22], Castro [23], Vogiazas and Nikolaidou [24], Rupeika-Apoga et al. [25], and Rupeika-Apoga and Syeda [26].

The above review literature shows that although various studies were conducted concerning banking and non-performing loans they suffer some of the other limitations. Firstly they all were solely focused on country-specific conditions and have ignored cross-sectional dependency, thus by employing DCCE approach this study adds a new paradigm to the previous literature, secondly, all the studies have taken both macroeconomic and banking variables thus there is a need to study separately the impact of banking or industry-specific variables on the non-performing loans, thirdly there is no conclusive study which focuses on South Asia banking conditions on three broad parameters of efficiency, regulation, and operations, thus providing a suitable literature gap to encourage us to proceed further.

Theoretical Background

As I went through previous literature I found that there are various variables and models which are used in earlier studies. Based on those inputs I have tried to segregate the banking variables into three broad categories of efficiency, regulation, and operations, for efficiency I have taken return on assets of banks as a proxy, for regulation capital adequacy has been taken as a proxy a lastly for operations credit disbursement is considered apart from these three categories other banking variables are also incorporated to see the overall impact of banking variables on non-performing loans. The idea of these three broad categories has been taken from the concept of bad management hypothesis, which emphasizes that bad performance of an organization may lead to lower results and lower outputs thus hampering the overall growth of the organization or the industry.

Methodology and Data Analysis

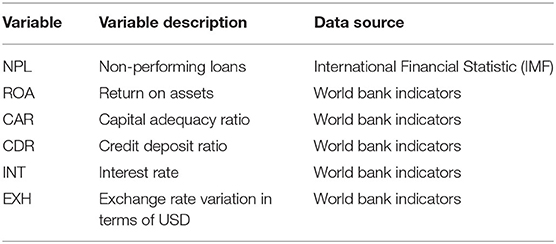

This research work measures the impact of banking efficiency (in terms of profitability), banking regulations (in terms of regulatory capital) and banking operation (in terms credit creation) on banking performance among the South Asian countries (India, Pakistan, Nepal, Sri Lanka, and Bangladesh), covering the annual data from 1995 to 2019, due to lack of data available some of the countries are not considered in this research. Based on review literature and consultation with previous government working papers like Caselli et al. [27], Williams [8] and Imbierowicz and Rauc [28] I have used return on assets as a proxy for banking efficiency [29], capital adequacy has been considered as a proxy for regulations [22], credit to deposit ratio is taken as a proxy for operation Petkovski and Kjosevski [1], Fiola Christaria [30], and lastly non-performing loans have been taken as a yardstick for measuring banking performances apart from these other banking variables like interest rate and exchange rate are also included, to measure the overall impact [31]. The data is collected from the International financial statistic database of International Monetary Fund and World Bank banking indicators. Table 1 shows the detail of the data source and variable descriptions.

Table 1. Variable and data source.

Testing of Cross-Sectional Dependency and Unit Root

Previous studies have pointed out that generally panel data suffers from the problem of cross-sectional dependencies due to unobserved elements and country-specific shocks which results in idiosyncratic dependencies. Most of the previous studies like Levin et al. [32] and Pesaran [33] have employed those unit root test which has either ignored the cross-sectional dependencies or were based on a false assumption of cross-sectional homogeneity. Thus to avoid false rejection of the null hypothesis on cross-sectional homogeneity, this study has used the unit root test proposed by Pesaran [34].

Using Equation 1 following hypothesis are tested to check cross-sectional dependencies

Here Null hypothesis says that there are no Cross-sectional dependencies again alternative hypothesis of Cross-sectional dependencies.

Test of Co-integration Among the Panel Data Set

There are various co-integrations techniques which are employed in the statistical or empirical analysis. Researchers always argued and scrutinized co-integration techniques based on the time frame of the data [35]. Thus, to study the long term relationship among the variables and also to keep structural break, this study has employed the bootstrap co-integration technique proposed by Westerlund and Edgerton [36]. This technique is also most suitable as it considers lead-lag length which is appropriate for a short duration of data. The below equation represents the Westerlund and Edgerton [36] model of bootstrap co-integration.

The stated Equation 4. Depicts the relationship of endogenous variables for a different dataset of cases and subscripts i and t shows cross-section and time period units, respectively.

Dynamic Correlated Effect Approach

Previous studies show that researches have generally considered homogenous slopes and has ignored cross-sectional effects. There are various panels analysis tools like Generalized methods of moments techniques, FE, and RE methods that pay more emphasis on intercept changes in cross-sectional units and thus ignoring homogeneity, thus giving misleading results.

The heterogeneous coefficient in cross-sectional units that too for a longer period of time was a key point of discussion among many researchers. All over the world studies pointed out the significance of cross-sectional dependencies among the data Meo et al. [37]. Leading this motive of cross-sectional dependencies Chudik and Pesaran [38] recently introduced a dynamic common correlated effect (DCCE). This approach work on four principle PMG estimation, MG estimation, CCE estimation, given by Shin et al. [39] and Pesaran [40], along with that also uses the estimation of Chudik and Pesaran [41]. The benefit of using this method is that it considers both homogenous and heterogeneous coefficient along with focusing on cross-sectional dependencies by taking into consideration the lag and means of cross-sectional data.

Apart from this, this approach also works well with structural break and small sample data with an unbalanced panel. To apply this approach I have employed and used the DCCE equation taken from Chudik and Pesaran [38].

Where NPL is non-performing loans, δxit shows the independent variables, pt represents lag limit in the cross-sections and ∂iNPLit−1 shows the lag of NPA as an independent variable.

Findings and Discussion

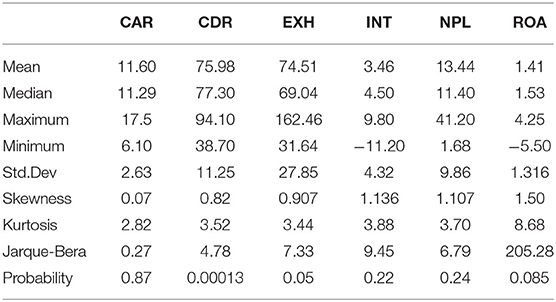

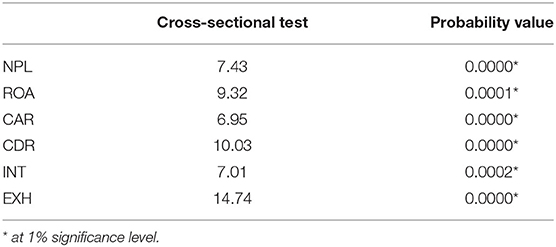

In this study to remove the issue of cross-sectional dependencies and spurious results as highlighted in previous studies, I have used a cross-sectional dependency test as proposed by Pesaran [34] which emphasized the cross-sectional dependencies and units significance. The test was employed on the residual of pairwise correlated OLS. The cross-sectional dependency test is also useful as it helps in choosing which generation of the test is more significant. Result of descriptive and Cross-sectional dependency test are presented in Tables 2, 3 respectively.

Table 2. Descriptive statistics.

Table 3. Cross-sectional dependency test.

The results from Table 3 show that the data suffers from the problem of cross-sectional dependency by rejecting the null hypothesis of no cross-sectional dependency. Further to avoid any wrong inferences or spurious inferences this study has also employed both the 1st and 2nd generation of cross-sectional dependency test as proposed by Chang [42] and Kahia et al. [43] under which one test assumes data cross-section homogeneity and second consider cross-sectional dependency. Table 4 represents the results of 1st generation test.

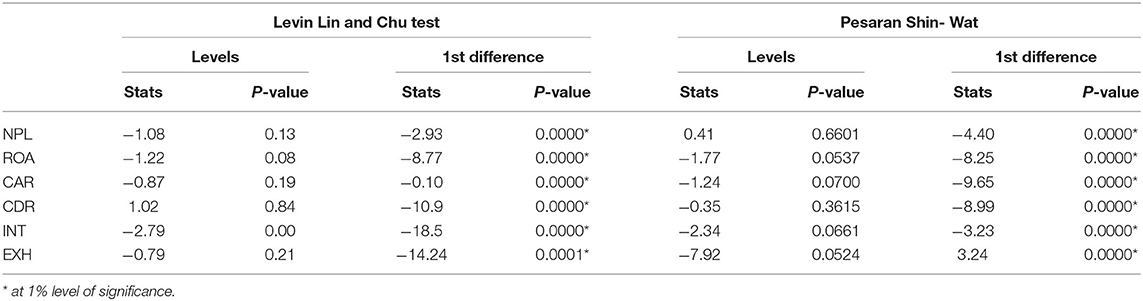

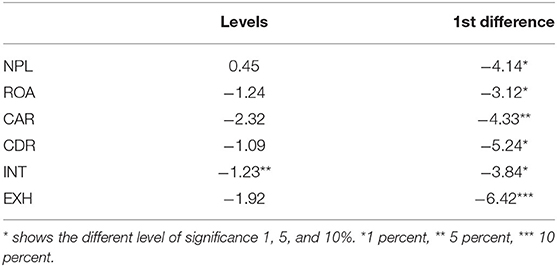

Table 4. Levin Lin and Pesaran Shin test.

Results of Table 4 shows that all variables are stationary at first difference except for interest rate which is stationary at levels. For reassessment of the result of the Levin Lin and Pesaran Shin test, this study further employed a 2nd generation test given by Pesaran [33] called CIPS test which is best suited for checking the cross-sectional dependencies in comparison to the above test employed. Results of the CIPS test are presented in Table 5 which shows that except for interest rate which is stationary at a level all the other variables are stationary at first difference.

Table 5. CIPS Unit root test.

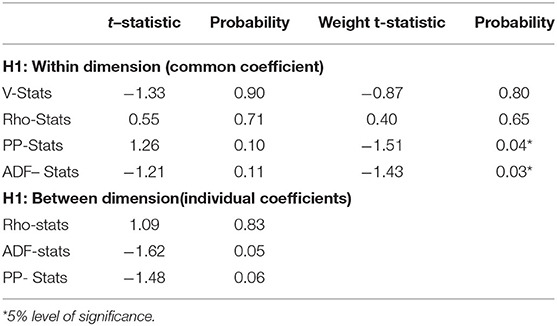

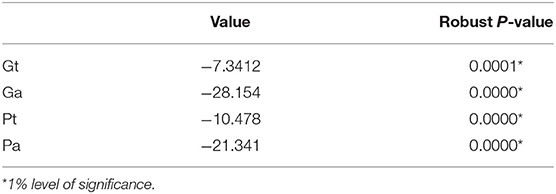

As none of the variables is of the second order of integration I further check the long term relationship among the independent and dependent variables using the novel DCCE technique. But before proceeding with the DCCE model I also check for long run co-integration technique among the variables using the Co-integration technique of Pedroni, along with the Westerlund ECM co-integration technique. Westerlund and Edgerton [44] pointed that many of the co-integration technique ignores structural breaks which result in giving misleading results thus they suggested ECM co-integration approach which considers structural breaks along with serial correlation, cross-sectional slopes, and heteroskedasticity thus provide robust results. Results of Pedroni and Westerlund ECM co-integration is presented in Tables 6, 7.

Table 6. Pedroni co-integration test.

Table 7. ECM co-integration test.

Pedroni co-integration test result shows that the variables are not co-integrated as the p-value is more than a 5% level of significance, meaning I cannot reject the null hypothesis of no co-integration. Thus, Westerlund ECM co-integration is employed to reassess the result, Table 7 summarized the ECM co-integration result which shows that banking operations, banking regulations, banking performance, and banking efficiency have a long run association as the probability value is <5% meaning I cannot reject the null hypothesis of no co-integration.

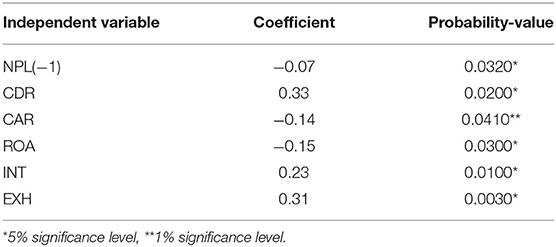

The result of the PMG model which has been used in the study is presented in Table 8 which shows that except for capital adequacy ratio which is considered as a proxy for banking regulation all the other independent variables have a significant association with the dependent variable which is non-performing loans (as the p < 5%, meaning credit deposit, exchange rate, interest rate and return on assets has a significant impact on non-performing loans. Credit deposit, Exchange rate, and Interest rate have a positive impact on non-performing loans whereas the return on assets has a negative impact on non-performing loans in South Asia.

Table 8. Result of PMG estimate.

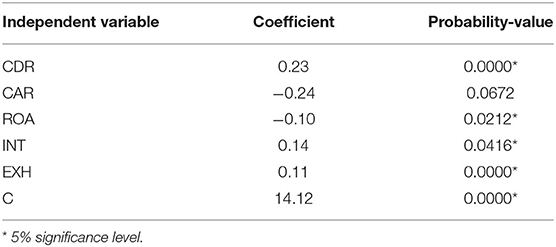

As the PMG estimate misses the concept of cross-sectional dependency, thus to avoid any misleading interpretation I have also presented the result of the DCCE model in Table 9.

Table 9. DCCE result.

Findings from the DCCE model confirms that credit deposit ratio (a proxy of banking operations), interest rate and exchange rate have a positive and significant relationship with non-performing loans (as the coefficient are positive and the p < 5%, whereas the return on asset (a proxy for banking efficiency) has a negative and significant association with non-performing loans in South Asia (as the coefficient are negative and the p < 5%).

The coefficient value of DCCE is more as compared to PMG estimate meaning in the case of cross-section dependency dynamic correlated model provides a more authentic and robust result. The results of DCCE approach confirms that in case of banking or industry-specific variables faulty banking operations in terms of higher credit disbursement without proper scrutiny of borrowers creates a positive pressure on non-performing loans whereas lower banking efficiency in context to banking profitability and management practices create a negative impact on non-performing loans meaning bank with greater efficiency in management practices have a lower non-performing loan compared to inefficient banks, which support the bad management hypothesis. In case of macroeconomic variables findings of the study confirm that higher interest rate lowers the debt servicing capacity of borrowers thus non-performing loan rises and vice versa, similarly, exchange rate volatility also hampers the debt servicing capabilities of export-oriented firms, as most of the South Asian countries have a high percentage of export as compared to import both in terms of goods and services.

The findings of our study also support the work of Beck [45], Nkusu [15], Chaibi and Ftiti [46], and Partovi and Matousek [47] who argued that bank efficiency and too much credit flow is detrimental for non-performing loans in different developed and developing countries.

Apart from this, findings of the study also clearly highlight the importance of first and second generation unit root test and DCCE approach in case of time series data dealing with cross sectional dependency issue to provide more accurate and robust results.

Conclusion and Recommendation

This study tries to figure out how banking efficiency, regulation, and operations affect banking performance in South Asian countries using a novel dynamic co-integration approach on the panel data set of five countries covering the period 1995–2019. This study considers the importance of cross-sectional dependencies in time series data, thus add toward the theoretical background of review literature. Along with this, this study also considers three broad parameters of the banking industry which are banking regulation, operation, and efficiency by including cross-sectional dependency which is also not considered in previous studies.

The findings of the study show that excessive bank credit, poor banking profitability, exchange rate fluctuations, and interest rate are the main factors that contribute to banks' non-performing loans. Based on the findings of the study it can be concluded that banking operations in terms of credit disbursement and banking efficiency in terms of profitability are the major reason which affects banking performance in South Asia along with macroeconomic variables like interest rate volatility and exchange rate.

Therefore, based on the results this study suggest that banks in South Asia should focus more on banks profitability through effective management and quality loan disbursement as lower profitability promotes more risk leading to the risky decision of excessive credit disbursement without adequate scrutiny of the borrowers, along with that banks in South Asia should also focus more on other banking operation like an investment, security trading and commodity trading apart from relying only on credit deposit spread, as South Asian banking system lack effective credit recovery mechanism thus chances of default loans are higher.

Based on the report of Asian Development Bank South Asian countries should also plan for effectively reducing too much government interference on Public sector banks, as public sector banks constitute 70% of the banking industry in South Asia.

In the current scenario due to corona outbreak, world bank reported that economic recession will be hitting hard to the South Asian region thus bank should start focusing how to tackle this issue in context to looming banking industry as in the coming future due to unemployment and persistent lockdown non-performing loan will see a huge surge. Apart from banking variable interest rate and exchange rate also need considerable scrutiny as they are also the significant factor contributing toward non-performing loans in South Asia.

As only a few countries of South Asia are considered for this study thus posing as a limitation and apart from this all the proxies are not incorporated in this work which represents banking efficiency, regulation, and operations thus providing a literature gap for future study.

Furthermore, researchers may include more macroeconomic or bank-specific variables to see the impact on non-performing loans in the coming future as well.

Data Availability Statement

Publicly available datasets were analyzed in this study. This data can be found here: World Bank Indicators, International financial Statistics.

Author's Note

In this study the author tried to establish how banking specific variables affect non-performing loans in South Asia. The author raises the issues of cross sectional dependency and using new DCCE approach along with first and second generation unit root test to resolve and provide authentic results in case of cross sectional dependency when working on time series data. The findings of the study will help in understanding this issue of banking management practices and nonperforming loans in South Asia in a better perspective especially during the time of COVID 19 when banks are working as a key driver in promoting the sluggish economic growth.

Author Contributions

The author confirms being the sole contributor of this work and has approved it for publication.

Conflict of Interest

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

References

1. Petkovski M, Kjosevski J. Does banking sector development p- mote economic growth? An empirical analysis for selected countries in central and south eastern. Europ Econ Res. (2014) 27:55–66. doi: 10.1080/1331677X.2014.947107

2. Stiglitz J, Weiss A. Credit rationing in markets with imperfect information. Am Econ Rev. (1981) 71:393–410.

3. Stijepovic R. Recovery and reduction of non-performing loans – podgorica approach. J Central Banking Theory Pract. (2014) 3:101–10. doi: 10.2478/jcbtp-2014-0017

4. Bernanke BS, Gertler M, Gilchrist S. The financial accelerator in a quantitative business cycle framework. Handbook Macroec. (1998) 1:1341–95. doi: 10.1016/S1574-0048(99)10034-X

6. Rinaldi L, Sanchis-Arellano A. Household debt sustainability: What explains household non-performing loans? An empirical analysis. In: ECB Working Paper No. 570, Kaiserstrasse 29 60311 Frankfurt am Main. (2006). p. 1–45.

7. Salas V, Saurina J. Credit risk in two institutional regimes: Spanish commercial and savings banks. J Fin Serv Res. (2002) 22:203–24. doi: 10.1023/A:1019781109676

8. Williams J. Determining management beaviour in European banking. J. Bank. Fin. (2004) 28:2427–60. doi: 10.1016/j.jbankfin.2003.09.010

9. Berger AN, DeYoung R. Problem loans and cost efficiency in commercial banks. J Bank Fin. (1997) 21:849–70. doi: 10.1016/S0378-4266(97)00003-4

12. Hu J, Li Y, Chiu Y. Ownership and non-performing loans: evidence from Taiwan's banks. Dev Econ. (2004) 42:405–20. doi: 10.1111/j.1746-1049.2004.tb00945.x

13. Rajan R, Dhal SC. Non-Performing Loans and Terms of Credit of Public Sector Banks in India”: An Empirical Assessment. Reserve Bank of India Occasional Papers Vol. 24 (2003). p. 81–121.

14. Espinoza R, Prasad A. Non-Performing Loans in the GCC Banking Systems and Their Macroeconomic Effects. IMF Working Paper 10/224. Washington: International Monetary Fund (2010). doi: 10.5089/9781455208890.001

15. Nkusu M. Non-Performing Loans and Macro-Financial Vulnerabilities in Advanced Economies. International Monetary Fund (2011). doi: 10.5089/9781455297740.001

16. Podpiera J, Weill L. Bad luck or bad management? Emerging banking market experience. J Finance Stab. (2008) 4:135–48. doi: 10.1016/j.jfs.2008.01.005

17. Swamy V. Impact of macroeconomic and endogenous factors on non-performing bank assets. Int J Bank Fin. (2012) 9:27–47. doi: 10.2139/ssrn.2060753

18. Khaled Subhi Rajha. Determinants of non-performing loans: evidence from the jordanian banking sector. J Fin Bank Manag. (2016) 4:125–36. doi: 10.15640/JFBM.V5N1A5

19. Umar M, Sun G. (2018). Determinants of non-performing loans in Chinese banks. J Asia Busin Studies 12:273–89. doi: 10.1108/JABS-01-2016-0005

20. Pop ID, Chicu N, Radutu A. Non-performing loans decision M- ing in the romanian banking system. Manag Mark Challenges Knowl Soc. (2018) 13:761–76. doi: 10.2478/mmcks-2018-0004

21. Koju L, Koju R, Wang S. Macroeconomic and bank-specific det- minants of non-performing loans: evidence from nepalese banking system. J Centr Bank Theory Practice. (2018) 7:111–38. doi: 10.2478/jcbtp-2018-0026

22. Boudriga A, Taktak N, Jellouli S. Bank specific, business, and institutional environment determinants of non-performing loans: evidence from MENA countries. In: Paper Presented at Economic Research Forum 16th Annual Conference. Cairo (2009).

23. Castro V. Macroeconomic determinants of the credit risk in the banking system: the case of the GIPSI. Econ Model. (2013) 31:672–83. doi: 10.1016/j.econmod.2013.01.027

24. Vogiazas and Nikolaidou. Investigating the determinants of non-performing loans in the romanian banking system: an empirical study with reference to the greek crisis. Eco Res Int. (2011) 2011:214689. doi: 10.1155/2011/214689

25. Rupeika-Apoga R, Zaidi SH, Thalassinos YE, Thalassinos EI. Bank stability: the case of nordic and non-nordic banks in latvia. Int J Econ Business Administ. (2018) 6:39–55. doi: 10.35808/ijeba/156

26. Rupeika-Apoga R, Syeda HZ. The determinants of bank's stability: evidence from Latvia's banking industry. In: New Challenges of Economic and Business Development-2018: Productivity and Economic Growth (2018). p. 579–586.

27. Caselli S, Stefano G, Francesca Q. The sensitivity of the loss given default rate to systematic risk: new empirical evidence on bank loans. J Financial Ser Res. (2008) 34:1–34.

28. Imbierowicz B, Rauch C. The relationship between liquidity risk and credit risk in banks. J. Bank. Fin. (2014) 40:242–56. doi: 10.1016/j.jbankfin.2013.11.030

29. Abdioglu N, Aytekin S. Takipteki kredi oranini etkileyen fak- törlerin belirlenmesi: mevduat bankalari üzerinde bir dinamik panel veri uygulamasi. Isletme Arastirmalari Dergisi. (2016) 8:538–55. doi: 10.20491/isader.2016.159

30. Fiola Christaria. The impact of financial ratios, operational efficiency and non- performing loan toward commercial bank profitability. In: Accounting and Finance Review (AFR) Vol 1.1. (2016).

31. Tanaskovic S, Jandric M. Macroeconomic and institutional determinants of non-performing loans. J Cent Bank Theory Pract. (2015) 1:47. doi: 10.1515/jcbtp-2015-0004

32. Levin A, Lin CF, Chu CSJ. Unit root test in panel data: asymptotic and finite sample properties. J Econ. (2002) 108:1–24. doi: 10.1016/S0304-4076(01)00098-7

33. Pesaran MH. A simple panel unit root test in the presence of cross-section dependence. J Appl Econ. (2007) 22:265–312. doi: 10.1002/jae.951

34. Pesaran HM. General Diagnostic Tests for Cross-Section Dependence in Panels. Cambridge, MA: Cambridge Working Papers in Economics (2004), 435.

35. Perron P. Test consistency with varying sampling frequency. Econ Theory. (1991) 7:341–68. doi: 10.1017/S0266466600004503

36. Westerlund J, Edgerton DL. A panel bootstrap co-integration test. Econ Lett. (2007) 97:185–90. doi: 10.1016/j.econlet.2007.03.003

37. Meo S, Saeed S, Aria H, Nazar, R. Water resources and tourism development in South Asia: an application of dynamic common correlated effect (DCCE) model. Environ Sci Pollut Res. (2020) 3:2020. doi: 10.1007/s11356-020-08361-8

38. Chudik A, Pesaran MH. Common correlated effects estimation of heterogeneous dynamic panel data models with weakly exogenous regressors. J Econ. (2015) 188:393–420. doi: 10.1016/j.jeconom.2015.03.007

39. Pesaran, M. Hashem, Yongcheol S, Ron PS. Pooled mean group estimation of dynamic heterogeneous panels. J Am Stat Assoc. (1999) 94:621–34.

40. Pesaran MH. Estimation and inference in large heterogeneous panels with a multifactor error structure. Econometrica. (2006) 74:967–1012 doi: 10.1111/j.1468-0262.2006.00692.x

41. Chudik A, Pesaran MH. Large panel data models with cross-sectional dependence: a survey. In: Baltagi BH, editor. The Oxford Handbook of Panel Data, Oxford: Oxford University Press (2015). p. 2–45.

42. Chang Y. î Bootstrap Unit root tests in panels with cross-sectional dependency î J Econ. (2004) 120:263–93. doi: 10.1016/S0304-4076(03)00214-8

43. Kahia M, Aïssa MSB, Charfeddine L. Impact of renewable and non-renewable energy consumption on economic growth: new evidence from the MENA Net Oil Exporting Countries (NOECs). Energy. (2016) 116:102–15. doi: 10.1016/j.energy.2016.07.126

44. Westerlund J, Edgerton DL. A simple test for co-integration independent panels with structural breaks. Oxf Bull Econ Stat. (2008) 70:665–704. doi: 10.1111/j.1468-0084.2008.00513.x

46. Chaibi H, Zied F. (2015). Credit risk determinants: evidence from a cross-country study. Res Int Bus Fin. 33, 1–16. doi: 10.1016/j.ribaf.2014.06.001

Keywords: non-performing loans, cross-section dependency, banking, PMG, unit root

JEL Classification: G21, G33, C22, C23.

Citation: Syed AA (2020) Does Banking Efficiency, Regulation, and Operations Affect Banking Performance in South Asia: Dynamic Correlated Model Approach. Front. Appl. Math. Stat. 6:38. doi: 10.3389/fams.2020.00038

Received: 06 July 2020; Accepted: 27 July 2020;

Published: 14 September 2020.

Edited by:

Eleftherios Ioannis Thalassinos, University of Piraeus, GreeceReviewed by:

Ramona Rupeika-Apoga, University of Latvia, LatviaInna Romānova, University of Latvia, Latvia

Copyright © 2020 Syed. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Aamir Aijaz Syed, YWFtaXJhbmtAZ21haWwuY29t