Nathalie Peña-García

Nathalie Peña-García Mauricio Losada-Otálora

Mauricio Losada-Otálora Enrique ter Horst

Enrique ter Horst- 1Research Department, CESA Business School, Bogotá, Colombia

- 2Departamento de Administración, Pontificia Universidad Javeriana, Bogotá, Colombia

- 3Facultad de Administración, Universidad de los Andes, Bogotá, Colombia

Purpose: This study investigates how customers perceive corporate social responsibility (CSR) efforts by banks during times of crisis, particularly following the COVID-19 pandemic. It focuses on the authenticity and alignment of CSR actions with customer values and examines how these perceptions influence trust, commitment, and attitudes toward banks.

Design/methodology: Data were collected from banking customers in the United States, Spain, Mexico, Brazil, and Argentina who were aware of CSR initiatives by their banks. Bayesian statistics and linear regressions were used to analyze the significance of the relationships within the proposed model, providing a robust evaluation of CSR impacts as perceived by customers.

Findings: The study finds that functional CSR initiatives, such as lowering credit card interest rates and offering financial advice, influence CSR beliefs most during economic crises. These findings suggest that during challenging times, customers prioritize practical support over the more abstract CSR initiatives that are often effective in stable conditions.

Research limitations/implications: The sample was limited to customers aware of CSR initiatives, which may not fully represent the broader population. Additionally, the study captures a specific moment of economic crisis, and future research should assess whether these dynamics persist in different contexts or during more stable economic conditions.

Originality: This research is unique in providing insights into CSR perceptions during an economic crisis, diverging from prior studies focusing on stable environments. Analyzing specific bank initiatives offers a deeper understanding of how practical CSR efforts resonate with customers during financial distress, contributing valuable knowledge to the fields of CSR and consumer behavior.

1 Introduction

The COVID-19 pandemic impacted all aspects of human life, particularly the economy, causing business closures, supply chain disruptions, and widespread financial instability (Deloitte, 2022). Global GDP loss reached 6.7%, with advanced economies experiencing a 6.5% decline and Latin America suffering an 8.5% contraction (Statista, 2022). Amidst this crisis, banks played a crucial role in supporting their customers’ financial well-being (objective and subjective) (Hussaien et al., 2020). The pandemic reinforced the importance of corporate social responsibility (CSR) in strengthening relationships between businesses, their stakeholders, and communities (Gokarna and Krishnamoorthy, 2021). Companies were called to undertake initiatives in favor of their employees and the support of customers and society (Raimo et al., 2021). For banks, these initiatives include offering loan deferrals, reducing interest rates, and providing financial counseling. However, the varying customer perceptions of these initiatives, from skepticism to trust, highlight the complex nature of CSR in the banking sector.

Economic cycles are inherent and inevitable, marked by alternating periods of growth and downturns. While the pandemic represents a particularly severe crisis, economic hardships recur due to financial crises, natural disasters, and geopolitical events (Krawczyk et al., 2023). During such difficult times, banks are pivotal in stabilizing the economy and providing necessary customer support (Collegenp, 2023; Ennis, 2023). However, how customers perceive these efforts can significantly impact their trust and loyalty toward the institution (Martínez and Del Bosque, 2013). Understanding customer beliefs and expectations regarding CSR is essential for fostering long-term relationships, particularly during financial distress. Banks that demonstrate a genuine commitment to social responsibility and customer well-being are more likely to reinforce customer loyalty (Gokarna and Krishnamoorthy, 2021). Economic crises alter customer priorities and expectations, making CSR efforts more susceptible to scrutiny. While CSR is often associated with a positive brand reputation and customer trust, in times of financial uncertainty, customers perceive CSR initiatives as either authentic support or opportunistic tactics to maintain a positive corporate image (Afzali and Kim, 2021).

Perceived CSR motives play a crucial role in shaping these perceptions. Research suggests that CSR initiatives are driven by different motives—egoistic, value-based, strategic, and stakeholder-driven (Engizek and Yaşin, 2018). These perceived motives can influence customer responses, potentially leading to corporate hypocrisy and skepticism. Corporate hypocrisy arises when there is a perceived inconsistency between a company’s CSR claims and actual practices (Wagner et al., 2009), while skepticism refers to doubts regarding the sincerity of CSR efforts (Skarmeas and Leonidou, 2013). Both constructs can shape CSR beliefs, impacting trust, attitude toward the bank, and customer commitment (Bae et al., 2021).

While extensive research has explored CSR’s impact on brand reputation, customer loyalty, and competitive advantage in stable economic conditions, a noticeable gap exists in understanding how these initiatives are perceived during financial crises (Bhattacharya et al., 2020). Economic downturns shift customer expectations, making CSR efforts vulnerable to criticism or skepticism. Customers may prioritize practical support over symbolic CSR initiatives, and what is considered valuable in stable times may not hold the same weight during financial distress. Despite the well-documented relationship between CSR and customer outcomes, limited research examines how these relationships shift in economic instability (He and Harris, 2020). Additionally, perceptions of CSR authenticity during crises remain underexplored, as customers may question whether these initiatives genuinely aim to provide relief or serve primarily as a reputation management strategy (Afzali and Kim, 2021).

This study aims to bridge this gap by empirically analyzing how CSR initiatives influence trust, commitment, and customer attitudes during economic hardship. By examining customers’ perceptions across five countries—United States, Spain, Mexico, Brazil, and Argentina—this research provides insights into which CSR initiatives are most effective in strengthening customer relationships during financial crises. Moreover, this study offers practical recommendations for banks to refine their CSR strategies, ensuring their initiatives resonate with customer expectations and reinforce trust.

The structure of this paper is as follows: first, it provides a literature review on CSR beliefs, corporate hypocrisy, and skepticism, followed by an exploration of customer perceptions and motivations behind CSR initiatives. The paper then discusses the desired customer outcomes from CSR, explicitly focusing on trust, attitudes toward the bank, and commitment. Next, the research methodology is presented, followed by a discussion of the results and their academic and managerial implications. The paper concludes with the study’s limitations and suggestions for future research.

2 Theoretical background and research hypotheses

The literature on CSR beliefs highlights that customers often hold favorable views of CSR activities when they perceive them as genuine efforts to contribute to societal well-being. However, these positive perceptions are frequently undermined by CSR skepticism and concerns about corporate hypocrisy, where customers suspect that CSR efforts may be more about enhancing the bank’s image rather than addressing real social issues. This skepticism can be exacerbated during economic downturns when customers are susceptible to the motives behind corporate actions.

To address the theoretical background and posit the research hypotheses, we present a literature review for perceived CSR motives, corporate hypocrisy, CSR skepticism, CSR beliefs, and desirable customer outcomes.

2.1 Perceived CSR motives

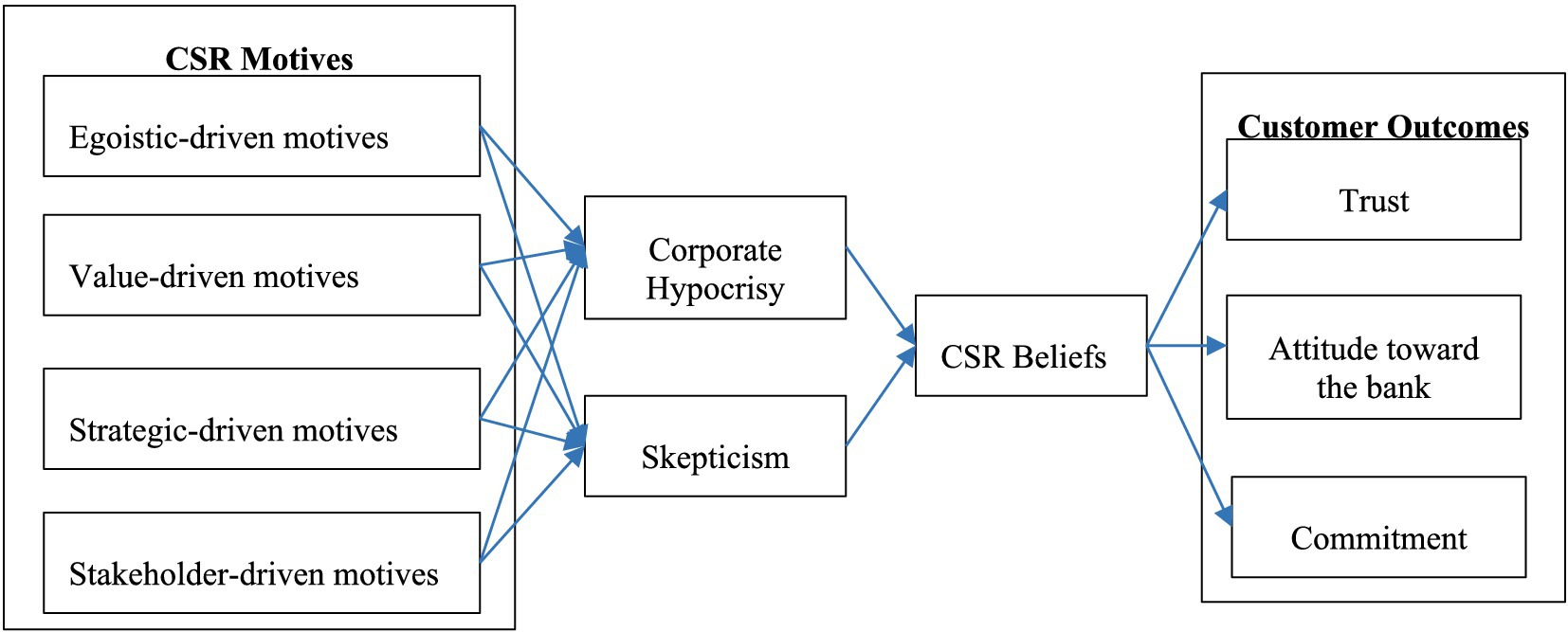

The literature identifies four primary dimensions of CSR motives: value-driven, stakeholder-driven, egoistic-driven, and strategic-driven. Value-driven motives reflect a firm’s commitment to ethical principles and social responsibility, prioritizing societal well-being over profit. Stakeholder-driven motives emphasize the importance of addressing the needs and concerns of various stakeholders, including employees, suppliers, and the local community. In contrast, egoistic-driven motives suggest that the firm engages in CSR primarily to serve its interest, often aiming to enhance its reputation. Finally, strategic-driven motives indicate that the firm adopts CSR initiatives to gain a competitive advantage and improve financial performance.

The effectiveness of perceived CSR motives can vary significantly depending on the cultural, industrial, and market context. Studies have shown that value-driven and stakeholder-driven motives are generally well-received in markets where corporate ethics and social impact are highly valued, such as Europe and North America, where customers prioritize environmental and social sustainability (Taliento and Netti, 2020). However, in emerging markets, such as some Asian regions, strategic-driven motives may resonate more with customers, as CSR activities that demonstrate financial gain and competitive advantage align with market expectations (Engizek and Yaşin, 2018). Moreover, the industry in which a company operates can influence how these motivations are perceived. For instance, in sectors like finance, where trust is paramount, egoistic-driven motives can lead to significant reputational damage, while in industries like technology or fashion, these motives may not result in such adverse outcomes (Fatma and Khan, 2023). Therefore, it is crucial to consider the context in which CSR initiatives are implemented, as the effectiveness of different motives can be highly dependent on the socio-economic and industrial backdrop.

This research proposes to examine the impact of customers’ perceived CSR motives on two critical outcomes: corporate hypocrisy and customer skepticism. By analyzing how different motives influence these perceptions, we aim to provide a deeper understanding of how customers interpret CSR activities.

2.2 Corporate hypocrisy

Corporate hypocrisy is the perceived inconsistency between a company’s expressed commitments, particularly in CSR initiatives, and its values, principles, commitments, and actions (Wagner et al., 2020). This perception arises when stakeholders notice a disconnect between what a company claims to support and what it practices, leading to judgments that the firm is not genuinely committed to its stated values. Recent studies define corporate hypocrisy as a form of moral inconsistency that damages trust and erodes a company’s credibility. For example, Chen et al. (2020) discuss how perceived corporate hypocrisy intensifies when stakeholders believe that a company’s CSR efforts are merely symbolic rather than genuine, particularly when CSR and corporate actions do not align. Similarly, Wang et al. (2022) explain that perceived hypocrisy often emerges when companies adopt CSR strategies but fail to act consistently with them, especially in times of crisis.

Over the past years, corporate hypocrisy has been increasingly examined for its adverse effects on customer trust, brand loyalty, and corporate reputation. Scholars have found it particularly relevant in industries where ethical behavior is critical, such as banking (Hur and Kim, 2020; Jung and Hur, 2023). Studies have also used corporate hypocrisy with a mediating role between CSR initiatives and consumer attitudes, demonstrating that when customers perceive hypocrisy, their trust in the brand significantly declines, often leading to reduced loyalty and increased skepticism (Babu et al., 2020).

Customers scrutinize corporate action more closely during economic crises or hardship, expecting companies to contribute meaningfully to societal well-being rather than pursuing self-serving agendas. Research suggests that in times of financial instability, value-driven and stakeholder-driven motives become more critical, as customers are more likely to support companies that prioritize community welfare and ethical behavior over profit (Ashraf et al., 2017). Conversely, egoistic-driven or strategic-driven motives can backfire, as they are seen as opportunistic and insincere, leading to a loss of trust and customer loyalty (Engizek and Yaşin, 2018).

When companies engage in CSR activities that appear self-serving, such as those driven by egoistic or strategic motives, customers are more likely to view these actions as hypocritical, especially during periods of hardship (Wang et al., 2022). This perception of hypocrisy can severely damage a company’s reputation, as customers expect organizations to prioritize community welfare and ethical behavior during crises rather than focusing on profit or image-building (Chen et al., 2020). As such, we propose the first set of research hypotheses:

H1a. Egoistic-driven motives perceived by bank customers positively and directly impact corporate hypocrisy.

H1b. Strategic-driven motives perceived by bank customers positively and directly impact corporate hypocrisy.

On the other hand, CSR efforts driven by genuine concern for stakeholders and aligned with ethical values can strengthen trust, as customers are more inclined to support companies that contribute meaningfully to societal well-being during difficult times (Zhao et al., 2020). Therefore, maintaining authenticity in CSR initiatives is crucial to mitigate negative perceptions such as corporate hypocrisy.

H1c. Value-driven motives perceived by bank customers negatively and directly impact corporate hypocrisy.

H1d. Stakeholders-driven motives perceived by bank customers negatively and directly impact corporate hypocrisy.

This first section will examine how different CSR motives influence perceptions of corporate hypocrisy. Later, we will explore how these perceptions shape customers’ beliefs about CSR initiatives.

2.3 Customer CSR skepticism

Consumer skepticism regarding CSR refers to the doubt or disbelief that consumers express towards a company’s social responsibility initiatives and commitment, often questioning the sincerity and motivation behind these efforts (Skarmeas and Leonidou, 2013). According to Ham and Kim (2020), consumer skepticism can emerge when consumers perceive CSR activities as mere crisis response strategies rather than genuine commitments to societal well-being. Similarly, Dalal (2020) emphasizes that consumer skepticism is influenced by the motives behind CSR initiatives, mainly when companies act out of self-interest rather than social responsibility. Joireman et al. (2018) added that consumer skepticism is particularly strong when CSR claims are vague or unsupported by concrete evidence, reinforcing the importance of transparency in CSR communication.

Consumer skepticism has recently gained significant attention, especially as companies increasingly adopt CSR into their marketing strategies. Research consistently shows skepticism can negatively impact customer trust, purchase intentions, and brand loyalty, making it a critical variable in understanding consumer behavior (e.g., Ham and Kim, 2020). For instance, Arli et al. (2019) highlight the role of skepticism in mediating the relationship between corporate hypocrisy and perceived CSR efforts, demonstrating that customers are less likely to trust companies whose CSR actions appear insincere. Meanwhile, Teah et al. (2023) affirm that studying customer skepticism in the context of CSR is essential for understanding the motives that shape customers’ perceptions, brand resonance, and resilience to negative information, which influence consumer advocacy. Additionally, research suggests that examining customer skepticism helps policymakers grasp CSR initiatives’ significant impact on consumer behavior and marketing outcomes (Fatma and Khan, 2023).

Since CSR skepticism arises as a consumer response to their perceptions of the underlying motives behind CSR initiatives, this research seeks to establish the relationship between different CSR motives and customer skepticism by exploring how various motives, such as egoistic, strategic, value-driven, and stakeholder-driven, impact customer CSR skepticism, we aim to gain a deeper understanding of how these perceptions shape consumer trust, attitudes, and behaviors toward CSR efforts in the banking industry.

Egoistic-driven and strategic-driven CSR motives are often seen as self-serving, with companies prioritizing their interests, such as enhancing their image or financial performance, over genuine social or environmental concerns. When consumers perceive CSR initiatives as primarily egoistic, they tend to believe that the company engages in CSR purely for self-promotion (Jeon and An, 2019). Similarly, strategic motives, which emphasize gaining competitive advantage, can also lead customers to view CSR efforts as opportunistic. This perception of self-serving intentions directly increases consumer skepticism, as consumers question the authenticity of the company’s CSR initiatives (Ham and Kim, 2020; Teah et al., 2023). Therefore, both egoistic and strategic motives are expected to heighten skepticism toward CSR efforts:

H2a. Egoistic-driven motives perceived by bank customers positively and directly impact customer CSR skepticism toward the bank’s CSR efforts.

H2b. Strategic-driven motives perceived by bank customers positively and directly impact customer CSR skepticism toward the bank’s CSR efforts.

On the other hand, value-driven and stakeholder-driven CSR motives are perceived as more authentic by customers, as these motives reflect a genuine commitment to ethical principles and the welfare of various stakeholders rather than self-serving objectives. When CSR initiatives are perceived as value-driven, consumer skepticism tends to decrease because these actions align with societal expectations of ethical responsibility (Dalal, 2020). Jeon and An (2019) found that value-driven CSR motives positively impact perceptions of authenticity, reducing consumer doubt about a company’s intentions. Similarly, Teah et al. (2023) highlight that values-driven motives lead to lower consumer skepticism, particularly when consumers feel that the company prioritizes social good over profit. Therefore, we propose that both value-driven and stakeholder-driven motives are expected to lower consumer skepticism toward CSR initiatives:

H2c. Value-driven motives perceived by bank customers negatively and directly impact customer CSR skepticism toward the bank’s CSR efforts.

H2d. Stakeholders-driven motives perceived by bank customers negatively and directly impact customer CSR skepticism toward the bank’s CSR efforts.

2.4 CSR beliefs

According to Osakwe and Yusuf (2021), CSR beliefs refer to customers’ attitudes and perceptions about a firm’s CSR initiatives and activities. These beliefs play a significant role in shaping customers’ attitudes, behaviors, and loyalty toward the organization, especially during times of hardship when corporate actions are subject to heightened scrutiny (Sharma et al., 2022). CSR beliefs originate from the broader notion of corporate social responsibility, first in the early 20th century as a social obligation for businesses to address social and environmental concerns (Amin-Chaudhry, 2016). Over time, CSR has evolved into a more integrated business practice supported by various theories and frameworks (Księżak and Szkolmowska, 2018). In the 1980s, the stakeholder and business ethics theories became pivotal in supporting and complementing CSR research, further embedding CSR into modern business strategy (Carroll, 1999).

Recent research on CSR beliefs has increasingly focused on understanding how these beliefs influence consumer behavior, particularly regarding purchase intentions and brand loyalty (Osakwe and Yusuf, 2021; Harrison and Huang, 2023). CSR beliefs have been shown to significantly impact consumers’ support intentions and their subsequent purchasing behavior. Studies have demonstrated that positive CSR beliefs can increase consumer support for a company’s initiatives, enhancing customer loyalty and trust. For instance, research has found that CSR beliefs not only foster greater consumer confidence in firms but also serve as a critical mediator between CSR initiatives and consumer behavior, such as repeat purchases and word-of-mouth recommendations (Fatmawati and Fauzan, 2021; Zasuwa and Stefańska, 2023). This emerging body of literature underscores the utility of CSR beliefs in guiding companies to design CSR strategies that resonate deeply with consumers, reinforcing their brand image and sustaining long-term customer relationships (Harrison and Huang, 2023).

H3. Corporate hypocrisy perceived by bank customers negatively and directly affects CSR beliefs.

H4. CSR Skepticism perceived by bank customers negatively and directly affects CSR beliefs.

2.5 Customer outcomes

Traditional relationship marketing literature has demonstrated that CSR initiatives can contribute to forming long-term commercial relationships between customers and companies, leading to desirable outcomes like trust, loyalty, and commitment (Zhang et al., 2021). These customer-company relationships are critical during economic crises, as they can help firms weather the adverse effects of such events on their performance (Morgeson et al., 2024). To understand the impact of customers’ CSR beliefs on these desirable outcomes for the firms, it is essential to explore the customer perceptions of brand trust, attitude, and commitment.

Understanding customer trust, attitude, commitment, and the influence of CSR beliefs is essential for long-term business success. Trust, built on the perception of responsible and ethical actions, encourages customer loyalty and brand preference (Singh et al., 2012; Raza et al., 2020). A positive attitude, fostered by identifying with a company’s CSR values and practices, may drive brand advocacy and recommendation (Xie et al., 2019). Finally, commitment, reinforced by trust and a favorable attitude, may lead to lasting and profitable relationships (Morgan and Hunt, 1994). In today’s increasingly competitive and socially conscious business environment, cultivating these elements through authentic and meaningful CSR practices is a competitive advantage and strategic imperative.

2.5.1 Brand trust

Brand trust is a critical concept in relationship marketing and the banking sector. Trust is the foundation for building long-term customer relationships and enhancing brand loyalty. Traditionally, brand trust has been associated with reliability, competence, and honesty. Classic studies such as Delgado-Ballester and Luis Munuera-Alemán (2005) highlighted that brand trust fosters consumer loyalty and plays a significant role in developing brand equity. More recent studies have highlighted that trust is a critical key and significantly influences loyalty and satisfaction, especially in industries like banking and insurance, where customer trust is vital for sustained engagement and competitive advantage (Langat and Atheru, 2023). Trust mitigates uncertainty, fosters a sense of security, and strengthens customer commitment, which is essential for maintaining customer relationships over time (Sanchez-Franco, 2009). In the context of the banking sector, trust also mediates the effectiveness of marketing strategies, particularly in an increasingly competitive environment, where transparency and consistent communication are critical for ensuring customer retention (Hidayat and Idrus, 2023).

Research supports that trust is significantly strengthened when CSR efforts align with customer values and are perceived as sincere (Fatma and Khan, 2023). This relationship becomes even more crucial in the banking sector, where trust is essential for maintaining customer relationships. While trust is traditionally built on reliability and transparency, CSR initiatives also play a vital role in enhancing trust when perceived as authentic and aligned with customers’ values. Recent research shows that CSR initiatives designed to meet customer expectations and societal needs significantly strengthen trust in the institution (Glaveli, 2021). When banks’ CSR efforts are seen as genuine rather than profit-driven, they reduce customer skepticism and deepen commitment (Raza et al., 2020). Thus, we propose the following research hypothesis.

H5a. CSR beliefs have a positive and direct impact on bank customers’ trust.

2.5.2 Attitude toward the bank

Attitude toward the brand reflects customers’ overall favorable or unfavorable evaluations of a particular brand (Aaker and Keller, 1990). In the highly competitive banking sector, where services are often perceived as similar, a positive brand attitude is crucial for attracting and retaining customers. Research shows that brand attitude influences desirable customer outcomes such as purchasing behavior (Peña-García et al., 2020). Additionally, positive brand attitudes can lead to greater brand loyalty, particularly when customers perceive the brand as offering high-value and quality services (Dewi and Handriana, 2021).

CSR beliefs may significantly shape customers’ attitudes toward a bank by influencing their perceptions of its ethical values and commitment to societal well-being. CSR activities focusing on environmental sustainability, ethical practices, and community support can enhance identification with the bank, positively influencing their attitudes (Prasetya, 2019). This connection highlights the importance of CSR in building strong, favorable customer relationships within the competitive banking industry. Thus, we propose:

H5b. CSR beliefs positively and directly impact customers’ attitudes toward the bank.

2.5.3 Commitment

Commitment refers to the psychological attachment and ongoing relationship between a customer and a company (Marshall, 2010). Commitment is critical in shaping long-term customer relationships and loyalty in the banking sector. Customers who are highly committed to their bank are more likely to exhibit loyalty and resist switching to competitors, even when alternatives are available (Peña García et al., 2018). In banking, fostering strong commitment through reliable services and ethical practices is crucial for maintaining customer relationships, especially in highly competitive markets.

CSR activities have been shown to strengthen emotional bonds between customers and banks (Hur et al., 2020). When customers perceive that a bank is genuinely engaging in socially responsible activities, it fosters an emotional attachment beyond mere transactional relationships. For instance, research by Hur et al. (2020) found that CSR activities in the banking sector can cultivate emotional brand attachment, leading to deeper customer loyalty and advocacy. These emotional bonds are critical in service industries like banking, where trust and long-term relationships are crucial for customer retention. Moreover, CSR initiatives focusing on community support or environmental responsibility enhance customers’ emotional connections, further reinforcing their commitment to the brand (Tirado et al., 2023). As a result, customers are more likely to remain loyal and committed to banks that they perceive as socially responsible, aligning with the hypothesis that CSR beliefs positively and directly impact customer commitment. Based on this understanding, we propose the following hypothesis:

H5c. CSR beliefs have a positive and direct impact on bank customers’ commitment.

Figure 1 shows the research model proposed.

Figure 1. Model research.

3 Materials and methods

3.1 Sample and procedure

Before the pandemic (2019), we conducted a study on the co-creation of value in bank customers in five countries, according to the growth of electronic platforms and cultural similarities and differences. Thus, we were working with a base of more than 2,000 clients born and raised in the United States, Mexico, Brazil, Argentina, and Spain, who had at least one financial product with a bank in their country and used two or more platforms to interact with their clients.

When the pandemic hit, we extended the study to understand how the financial relief proposed by the banks had affected customers’ perceptions of their commitment to the financial well-being of their customers.

Thus, we asked these 2,000 clients to tell us which financial relief had been offered and what type. The most common are:

- decrease in interest caused by credit card purchases

- decrease in interest on arrears

- deferment of payment for pending or current installments

- granting of credits for natural or legal persons

- financial advice to improve the financial well-being of clients

- positive communications encouraging customers

Considering only those clients who were aware of some bank initiative, we asked them about their CSR beliefs about their banks. A structured questionnaire was developed using scales found in the literature, obtaining 525 valid and complete surveys.

3.2 Measures

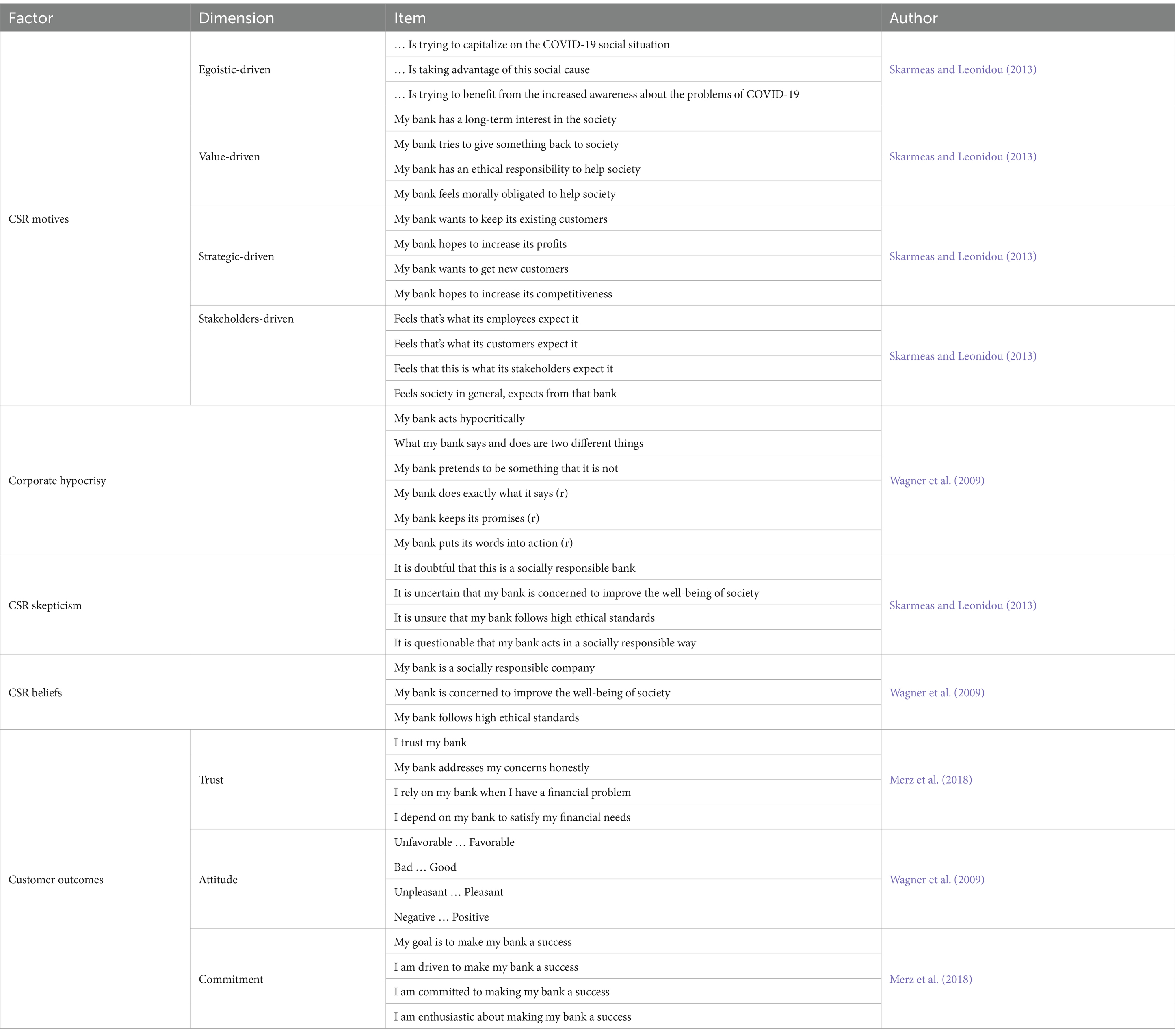

We used scales previously validated in the literature to measure the variables proposed in the study. The CSR beliefs and corporate hypocrisy measures were adapted from Wagner et al. (2009). The work of Skarmeas and Leonidou (2013) was used to measure egoistic-driven, value-driven, strategic-driven, stakeholder-driven motives, and skepticism. Trust and commitment were measured based on the work of Merz et al. (2018). Finally, attitudes toward the bank were adapted from Peña-García et al. (2020) work. Items are shown in Table 1.

Table 1. Items for the measurement instrument.

4 Method of analysis, measurement model analysis and results

Using the noisy observations of our latent item constructs and explanatory variables from Figure 1, we estimated a Bayesian hierarchical model approach like Siqueira et al. (2020). We chose a Bayesian approach over a traditional structural equation modeling because (1) they do not need to rely on asymptotic, normal approximations or large-dimensional datasets to achieve sufficient statistical validity; (2) our 2-layer hierarchy model is aligned with the reality of the Likert constructs, where surveys are naturally noisy and non-homogeneous between participants; and (3) as a Bayesian approach one can incorporate prior information, which offers a more flexible statistical approach that incorporates information from data and experts (Körding et al., 2004; Brantley and Körding, 2022). In the same spirit, the model of this paper was used successfully by Dakduk et al. (2017) and Siqueira et al. (2019, 2020).

The two hierarchies in the model are (A) the observation equation, which provides us with information about each of the constructs with individual-specific, construct-specific, and measurement item-specific sources of noise, and (B) the latent trait equation, which relates the variables according to Figure 1, while still allowing for individual-specific divergence from the theoretical model. The goal is to extract all the noise sources and estimate the model’s key parameters, namely the relationships between the latent constructs (beta parameters) within the measurement model. For the sake of space, we shall write Egoistic-driven motives, Value-driven motives, Strategic-driven motives, Stakeholder-driven motives, Corporate Hypocrisy, Skepticism, CSR Beliefs, Trust, Attitude toward the bank, and Commitment as EGO, VAL, STRA, STAKE, HYPO, SKEP, TRS, ATT and CMM, respectively, for the Likert variables. The Bayesian estimation approach for this problem encompasses the following elements.

4.1 General model

with standard hyperpriors and

4.2 Model-specific priors

for j = EGO, VAL, STRA, STAKE, HYP, SKEP, CSR, TRS, ATT and CMM.

4.3 Description of each variable, distribution, and subindex

MN(X|a,b,c) = Multinomial density with a observations of b categories occurring with probability vector c

= (C-1)-dimensional Gaussian cumulative density function ()

(X|a,b) = d-dimensional Gaussian density with mean a and precision parameter b

Ga(X|a,b) = Gamma distribution with parameters a and b

i = index for the individuals in the sample

j = construct of interest (EGO, VAL, STRA, STAKE, HYP, SKEP, CSR, TRS, ATT, and CMM, respectively, in our model)

k(j) = 1,…,K(j) measurement items about construct j

= Likert-based observation of individual i, for the k-th measurement item about construct j

T = Number of questionnaires per individual (T = 1)

C = Number of Likert categories per construct (C = 7, although the assumption of an equal number of Likert scales can be easily relaxed)

= (C − 1)-dimensional latent probability vector for each Likert scale for individual i and construct j, with

(C − 1)-dimensional vector of latent thresholds for construct j, mapping the space of a latent mean into probability areas

= Latent mean perception of individual i about construct j ( is the vectorized form)

= Precision factors (fixed vague hyperparameters)

= Hyperpriors for the distances between latent thresholds

4.4 Description of the model

We allow each of the observed measurement items to follow a multinomial ordered probit structure, with underlying latent probability vectors that are construct- and individual-dependent, and those will be linked with a latent individual-dependent mean, representing the standings of each individual about each construct. The Bayesian construct is completed with hyperpriors for each of the parameters, and the model is estimated using a standard Metropolis-Hastings algorithm, taking advantage of the conjugacy of the core construct. We allow for a 20,000 iteration burn-in and run the model for another 40,000 iterations, with no thinning necessary for this chain, as seen in Table 2.

Table 2. MCMC output for data 1.

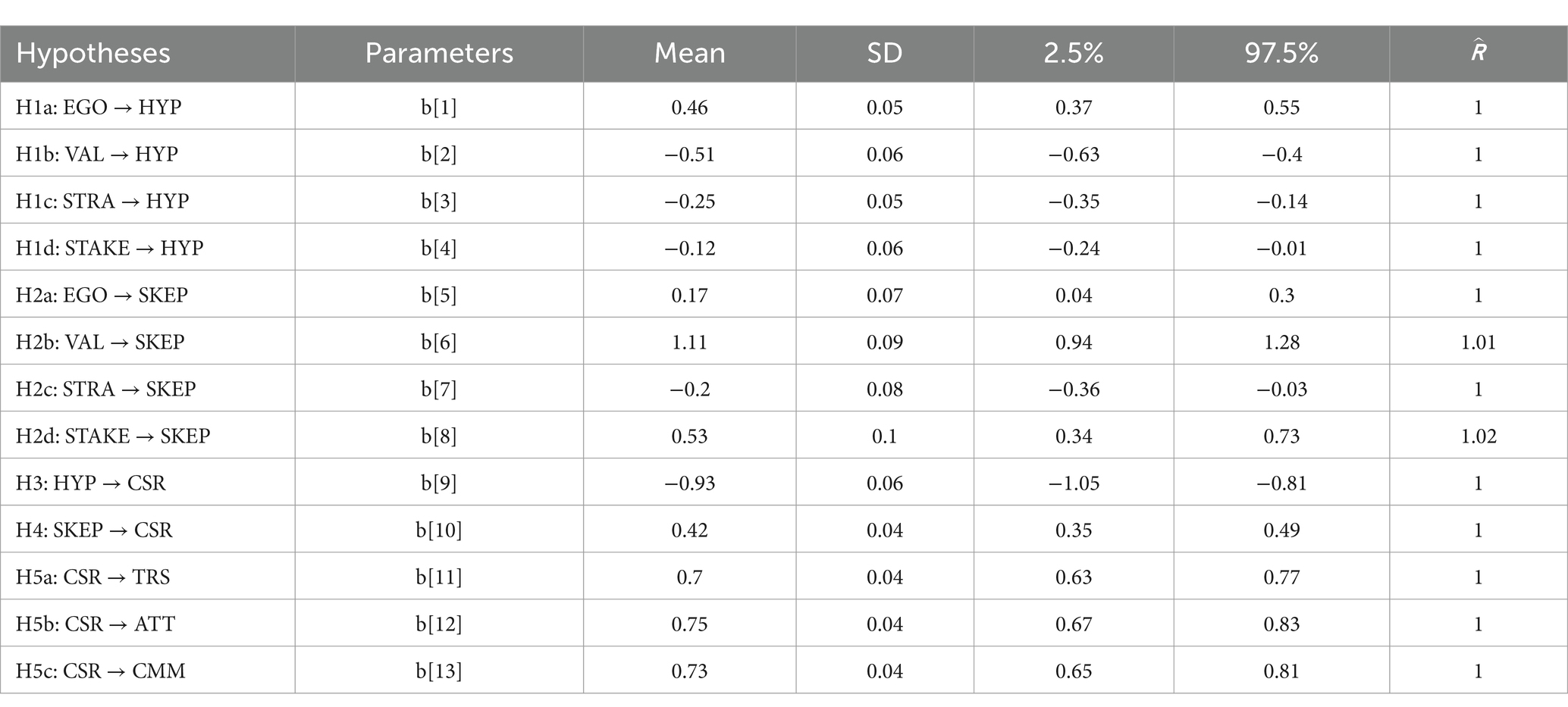

4.5 Interpretation of numerical results

We ran the model with a 40,000-run with a burn-in of 20,000 and no thinning; we gathered the following 20,000 MCMC iterations. All the posterior densities for the parameters have a negligible mass below zero, indicating strong evidence of the significance of the relationships between the constructs, as seen in Figure 1 (Green strong, Yellow moderately strong). There was good evidence of good mixing of the Markov Chain from the statistic, which is close to 1 for all model parameters and means that the MCMC converged well (please see Gelman et al., 2013). In Table 1, we see strong significance in green color (negative or positive), moderately strong in yellow, and next to the parameter is the word (Positive or Negative) when it is significantly different from zero and has a positive or negative relationship, respectively.

The results presented in Table 2 confirm the strength and significance of the relationship between the examined variables, supporting all proposed hypotheses.

4.6 Testing the mediating effect of trust

To further explore the relationships between CSR beliefs, trust, commitment, and attitude, we conducted a Bootstrap analysis with 5,000 iterations to estimate the 95% confidence intervals of the key coefficients in an alternative model where trust acts as a mediator. The results provide robust evidence supporting the mediating role of trust in the relationships between CSR and customer commitment (CMM) and attitude (ATT).

The results of the Bootstrap analysis confirm the mediating role of trust in the relationship between CSR beliefs and customer commitment and attitude. Specifically, CSR beliefs significantly positively affect trust (β = 0.681, 95% CI [0.614, 0.743]), indicating that customers who perceive CSR initiatives as genuine are more likely to trust their bank. In turn, trust strongly predicts commitment (β = 0.751, 95% CI [0.701, 0.802]) and attitude toward the bank (β = 0.702, 95% CI [0.630, 0.769]). These findings suggest that trust serves as a key psychological mechanism through which CSR beliefs translate into deeper customer relationships.

This result provides an alternative perspective on the direct effects initially tested in our primary model. While our original model considered commitment and attitude as direct outcomes of CSR beliefs, this alternative analysis suggests that trust plays a crucial mediating role. These findings align with prior research emphasizing the foundational role of trust in relationship marketing (Riza and Santoso, 2023). Thus, this study reinforces the idea that CSR initiatives primarily strengthen customer-brand relationships by fostering trust, subsequently enhancing commitment and positive brand attitudes.

5 Discussion

The proposed model demonstrated that all hypotheses were supported based on their beta parameters (Figure 1 and Table 2). The hypotheses are listed in the first column of Table 3, which highlights strong relationships among the variables under analysis. Most relationships are relatively strong and statistically significant, except for H1d, H2a, and H2b, which, although slightly weaker, are still significant. The Bayesian statistical analysis provides credible intervals (2.5 and 97.5%) that confirm the robustness of the relationships, as indicated by Rhat values close to 1, ensuring convergence of the models.

Table 3. PLS-SEM for bank initiatives and CSR beliefs.

Some of the results of this study align with the existing literature on CSR motives, corporate hypocrisy, and consumer skepticism while contributing to new insights. For instance, the strong impact of egoistic-driven motives on corporate hypocrisy (H1a) mirrors the findings of Jeon and An (2019), who demonstrated that customers tend to view egoistic CSR efforts as self-serving and inauthentic, thereby fostering negative perceptions of the company’s sincerity. Similarly, Teah et al. (2023) found that egoistic motives heighten consumer skepticism, consistent with the significant positive relationship between the variables. This suggests that consumers are more susceptible to motives that appear self-promotional in the banking sector. The strategic-driven motives (H1c), which were expected to have a positive relationship with corporate hypocrisy, instead show a negative relationship (b = −0.25). Typically, the literature suggests that when CSR is seen as strategic or driven by profit motives, it should increase perceptions of hypocrisy (Jeon and An, 2019). However, the findings suggest that strategic-driven CSR may be viewed as more favorable, possibly because customers recognize the business logic behind CSR as a legitimate and expected part of a company’s strategy. This may indicate that, in some instances, customers accept strategic CSR efforts if they see clear benefits, both for the business and society, which might reduce perceptions of hypocrisy.

On the other hand, the negative and significant effect of non-egoistic motives (value-driven and stakeholder-driven) on corporate hypocrisy (H1b and H1d) closely follows the literature’s consensus on these types of CSR. Studies by Fatma and Khan (2023) and Zhao et al. (2020) support the idea that when customers perceive CSR initiatives as genuinely wellbeing-driven, the sense of trust increases. In contrast to expectations and the literature, the findings show that value-driven and stakeholder-driven motives positively affect customer skepticism (H2b). These results deviate from what previous studies suggest. One possible explanation for this unexpected result might be that consumers perceive an overemphasis on value-driven motives as disingenuous or “too good to be true,” leading to skepticism. This could suggest that in some contexts, especially when consumers are highly critical or cynical, even genuinely well-intended CSR motives might be scrutinized or met with suspicion.

Regarding the relationship between corporate hypocrisy and CSR beliefs, the findings align with Arli et al. (2019), who identified that perceived insincerity in the form of hypocrisy negatively impacts how customers form CSR beliefs. This study confirms that consumers are more likely to distrust and create negative attitudes toward companies perceived as hypocritical or insincere in their CSR motives. This study found, however, that customer skepticism has a positive relationship with CSR beliefs (H4), going against the general expectation. Literature typically shows that increased skepticism undermines consumer trust and CSR perceptions (Ramasamy et al., 2020). However, a positive relationship could imply that skeptical customers still form CSR beliefs, perhaps more critically or cautiously. Consumers may engage more deeply with CSR efforts in a highly skeptical context and still develop favorable beliefs if companies convincingly address their concerns. This could suggest that even skeptical consumers adjust their beliefs if the company’s CSR actions withstand scrutiny.

Finally, the strong positive relationship between CSR beliefs and outcomes such as trust, attitudes, and commitment (H5a, H5b, and H5c) echoes earlier research by Hur and Kim (2020), which found that positive CSR beliefs significantly enhance customer trust and loyalty. These results reinforce the established understanding that well-executed, genuine CSR efforts build stronger consumer-brand relationships, encouraging loyalty and advocacy.

Additionally, our Bootstrap analysis provides further insights into the role of trust as a key mediating factor in the relationship between CSR beliefs and customer outcomes. The results confirm that CSR beliefs have a strong positive effect on trust, significantly predicting both customer commitment and attitudes toward the bank. This reinforces the idea that trust acts as a crucial mechanism through which CSR perceptions influence customer relationships. These findings align with prior literature emphasizing the centrality of trust in shaping consumer perceptions of corporate responsibility (Hur et al., 2020). Moreover, they highlight that trust plays a fundamental role in strengthening customer commitment and shaping favorable attitudes toward financial institutions in the banking sector.

The findings reveal expected and unexpected relationships between CSR motives and consumer skepticism and beliefs, highlighting the complexity of consumer perceptions. We ran an additional regression analysis on the identified initiatives to identify which specific CSR activities had the most significant impact on CSR beliefs. This additional regression analysis may be found in Section 5.1.

5.1 Bank initiatives and impact on CSR beliefs

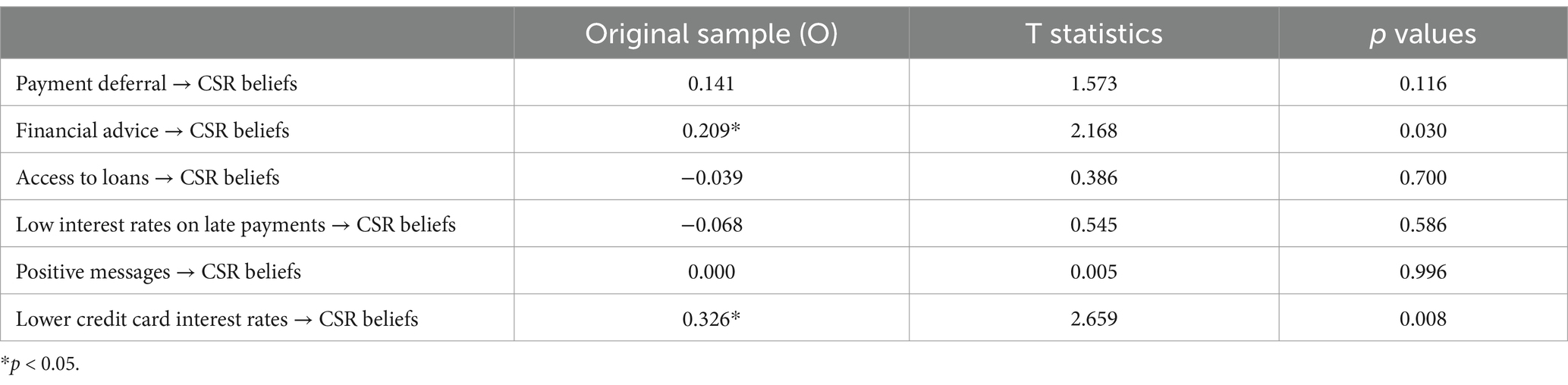

To evaluate the impact of various bank initiatives on customers’ CSR beliefs, we analyzed six specific factors: payment deferral, financial advice, access to loans, low interest on late payments, positive messages, and lower credit card interest rates. Each of these initiatives was examined for its influence on customer beliefs regarding the bank’s CSR efforts.

The analysis utilized a structural equation modeling (SEM) approach, which is particularly effective in understanding the relationships between observed variables and latent constructs like CSR beliefs. SEM allows for the simultaneous analysis of multiple pathways and can accommodate the complex interrelations among the variables. The path coefficients generated from the SEM analysis indicate the strength and direction of the relationship between each initiative and CSR beliefs. The significance of these coefficients was determined using T-statistics and corresponding p-values, where a lower p-value indicates a statistically significant effect. PLS-SEM was used to assess the strength and significance of the relationship between each CSR initiative and CSR beliefs. The path coefficients (original sample values) indicate the direct influence of each factor on CSR beliefs. At the same time, the T-statistics and p-values were used to test the significance of these relationships. A p-value of less than 0.05 was considered significant, indicating that the corresponding CSR initiative has a statistically meaningful impact on CSR beliefs.

The results revealed that financial advice and lower credit card interest rates had statistically significant positive effects on CSR beliefs, as indicated by their p-values of 0.03 and 0.008, respectively. This suggests that these specific initiatives resonate strongly with customers and positively shape their perceptions of the bank’s CSR efforts. On the other hand, other initiatives, such as payment deferral and positive messaging, did not show significant effects, implying that these actions may be seen as standard customer service rather than impactful CSR efforts in this context.

This analysis underscores the importance of selecting CSR initiatives that resonate with customers’ needs and concerns, particularly during economic hardship. The significant influence of financial advice and credit card interest management suggests that customers value practical financial support, thereby positively influencing their perception of the bank’s CSR efforts. This finding aligns with existing research emphasizing the importance of providing tangible benefits to customers to foster positive CSR perceptions (Ahn et al., 2021; Islam et al., 2021).

In contrast, the lack of significant effects from initiatives like payment deferral and positive messaging may suggest that these actions are either expected as part of customer service or perceived as insufficiently impactful to be considered genuine CSR efforts. Though not statistically significant, negative coefficients for access to loans and low interest on late payments could indicate customer concerns about revenue-generating activities rather than genuine CSR initiatives.

For banks aiming to enhance their CSR strategies, this analysis suggests focusing on initiatives that offer customers clear, immediate financial benefits. Additionally, the results highlight the need to carefully consider how different CSR initiatives are perceived, particularly during economically challenging times, to avoid unintended negative perceptions that could undermine the bank’s CSR efforts.

6 Theoretical and practical contributions

6.1 Theoretical implications

The theoretical implications of this study are particularly noteworthy, given that several findings diverge from established literature. Traditional CSR research often posits that value-driven motives reduce skepticism and increase positive consumer perceptions. In contrast, strategic or egoistic-driven motives tend to heighten perceptions of corporate hypocrisy and skepticism. However, our results challenge these assumptions in several key areas. For example, value-driven motives increased consumer skepticism (H2b), contrary to most literature, which typically suggests that values-based CSR initiatives foster trust and authenticity (Teah et al., 2023; Fatma and Khan, 2023). Similarly, strategic-driven motives were expected to increase corporate hypocrisy (H1c). Still, our study showed a negative relationship, indicating that consumers might view strategic initiatives as acceptable and beneficial rather than hypocritical. These results suggest that consumers may respond differently to CSR efforts depending on external factors such as economic crises or socio-economic conditions in contexts like the one examined.

A critical factor influencing these results could be the economic crisis brought on by the COVID-19 pandemic. During heightened financial uncertainty, consumers may focus more on immediate survival and practical support rather than questioning the motives behind CSR efforts. For instance, the positive impact of strategic-driven motives on reducing hypocrisy may stem from consumers being more forgiving of companies’ profit-seeking activities if they provide financial relief. Similarly, the increased skepticism toward value-driven motives could reflect a heightened sensitivity to perceived insincerity when consumers struggled and expected more direct support.

The study’s sample from developing countries may have contributed to these differing results. In developing economies, consumers often have distinct expectations and experiences with financial institutions compared to those in developed countries. Prior research on CSR is frequently based on studies conducted in more stable and developed markets, where consumers may have different thresholds for judging CSR authenticity. In developing countries, where economic hardship and instability are more prevalent, consumers may be more critical of CSR efforts that seem disconnected from their immediate financial needs, even if they are value-driven. This context could explain why initiatives focused on practical financial support, such as financial advice and lower interest rates, had a significant positive impact. At the same time, more abstract value-driven efforts increased skepticism.

These findings suggest that context matters significantly when studying CSR and consumer perceptions, particularly during times of crisis and in developing economies. They challenge the universality of traditional CSR theories and underscore the need for more research that considers economic and cultural contexts in shaping consumer responses to CSR initiatives. This opens new avenues for further exploration, particularly in how CSR is perceived in different economic climates and developing versus developed markets.

6.2 Practical contributions

The managerial implications derived from these findings offer critical insights for banks in optimizing their CSR strategies. Financial advice and lower credit card interest rates impacted CSR beliefs significantly. Specifically, financial advice had a statistically significant effect (p = 0.030), suggesting that customers value the support that directly addresses their financial anxiety during economic hardship. Offering financial advice helps alleviate stress and uncertainty, allowing customers to feel more secure and supported by their bank. This type of initiative provides practical assistance and strengthens the perception that the bank genuinely cares about the well-being of its customers.

Similarly, the initiative to reduce credit card interest rates had an even more substantial positive effect (p = 0.008) on CSR beliefs, as many customers rely heavily on credit cards during periods of financial strain. Lowering interest rates on credit card debt was a meaningful relief, offering significant financial support to customers who may have been using credit cards as a primary means of funding during the crisis. This action was likely viewed as a tangible benefit that directly addressed an urgent customer need, further solidifying the bank’s reputation as a socially responsible institution.

On the other hand, initiatives such as payment deferral and low interest rates on late payments were not perceived positively, and this could be due to customers viewing them as self-serving. For example, payment deferral may be interpreted as an action driven by egoistic motives, where the bank’s goal is primarily to secure future repayments rather than to help customers genuinely. Similarly, lowering interest rates on late payments might be seen as a tactic to facilitate debt collection rather than a sincere effort to support struggling customers. In the same vein, although weak, the negative effect of access to loans suggests that customers may perceive this as a sales-driven initiative rather than a CSR effort, further highlighting the importance of intention and communication.

7 Conclusions, limitations, and future research lines

This study provides valuable insights into how consumers perceive CSR initiatives during periods of economic hardship across different countries, including developing and developed economies. While specific findings align with traditional CSR literature—such as the positive impact of practical financial support on CSR beliefs—other results diverge significantly, suggesting that consumer perceptions of CSR motives may vary depending on the socio-economic context. Notably, the positive relationship between value-driven motives and skepticism and the negative relationship between strategic-driven motives and corporate hypocrisy challenge existing assumptions about how consumers respond to CSR. These findings emphasize the importance of tailoring CSR strategies to meet consumers’ specific needs and expectations, particularly during times of crisis, where practical support may be more valued than abstract or symbolic efforts.

This study has some limitations that open avenues for future research. First, the sample, while geographically diverse, was relatively small since not all participants were aware of their banks’ CSR efforts. This may have limited the ability to capture broader CSR perception trends fully. Future research could benefit from larger, more representative samples to confirm the generalizability of these findings. Additionally, while this study examined five countries, including developed and developing economies, further exploration could assess whether the observed differences in consumer responses hold across more diverse regions and contexts. Finally, the study occurred during the economic crisis brought on by the COVID-19 pandemic, which likely shaped consumer perceptions. Future research should explore whether these dynamics persist in more stable economic conditions or under different crises to understand better how external factors influence CSR effectiveness.

Data availability statement

The datasets presented in this study can be found in online repositories. The names of the repository/repositories and accession number(s) can be found at: doi: 10.17632/txcwh85rj7.1.

Ethics statement

The studies involving humans were approved by CESA Ethics Committe. Colegio de Estudios Superiores de Administración. The studies were conducted in accordance with the local legislation and institutional requirements. The participants provided their written informed consent to participate in this study.

Author contributions

NP-G: Conceptualization, Formal analysis, Supervision, Writing – original draft. ML-O: Conceptualization, Supervision, Writing – original draft. EH: Data curation, Investigation, Methodology, Resources, Writing – original draft.

Funding

The author(s) declare that financial support was received for the research and/or publication of this article. This project was funded by CESA through its internal call, project number 32004, and by Pontificia Universidad Javeriana.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Generative AI statement

The author(s) declare that no Gen AI was used in the creation of this manuscript.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Aaker, D. A., and Keller, K. L. (1990). Consumer evaluations of brand extensions. J. Mark. 54, 27–41. doi: 10.1177/002224299005400102

Afzali, H., and Kim, S. S. (2021). Consumers’ responses to corporate social responsibility: the mediating role of CSR authenticity. Sustain. For. 13:2224. doi: 10.3390/su13042224

Ahn, J., Shamim, A., and Park, J. (2021). Impacts of cruise industry corporate social responsibility reputation on customers’ loyalty: mediating role of trust and identification. Int. J. Hosp. Manag. 92:102706. doi: 10.1016/j.ijhm.2020.102706

Amin-Chaudhry, A. (2016). Corporate social responsibility – from a mere concept to an expected business practice. Soc. Responsib. J. 12, 190–207. doi: 10.1108/SRJ-02-2015-0033

Arli, D., Esch, P., Northey, G., Lee, M. S. W., and Dimitriu, R. (2019). Hypocrisy, skepticism, and reputation: the mediating role of corporate social responsibility. Mark. Intell. Plan. doi: 10.1108/MIP-10-2018-0434

Ashraf, S., Ilyas, R., Imtiaz, M., and Tahir, H. M. (2017). Impact of CSR on customer loyalty: putting customer trust, customer identification, customer satisfaction and customer commitment into equation-a study on the banking sector of Pakistan. Int. J. Multidiscip. Curr. Res. 5, 1362–1372.

Babu, N., Roeck, K. D., and Raineri, N. (2020). Hypocritical organizations: implications for employee social responsibility. J. Bus. Res. 114, 376–384. doi: 10.1016/J.JBUSRES.2019.07.034

Bae, K.-H., El Ghoul, S., Gong, Z. J., and Guedhami, O. (2021). Does CSR matter in times of crisis? Evidence from the COVID-19 pandemic. J. Corp. Finance 67:101876. doi: 10.1016/j.jcorpfin.2020.101876

Bhattacharya, A., Good, V., and Sardashti, H. (2020). Doing good when times are bad: the impact of CSR on brands during recessions. Eur. J. Mark. 54, 2049–2077. doi: 10.1108/EJM-01-2019-0088

Brantley, J. A., and Körding, K. P. (2022). Bayesball: Bayesian integration in professional baseball batters. bioRxiv, 2022–2010. doi: 10.1101/2022.10.12.511934

Carroll, A. B. (1999). Corporate social responsibility: evolution of a definitional construct. Bus. Soc. 38, 268–295. doi: 10.1177/000765039903800303

Chen, Z., Hang, H., Pavelin, S., and Porter, L. (2020). Corporate social (Ir)responsibility and corporate hypocrisy: warmth, motive and the protective value of corporate social responsibility. Bus. Ethics Q. 30, 486–524. doi: 10.1017/beq.2019.50

Collegenp (2023). Preventing bank runs in today’s economy: an in-depth analysis. Available online at: https://www.collegenp.com/article/preventing-bank-runs-in-the-modern-economy/ (Accessed September 13, 2024).

Dakduk, S, ter Horst, E, Santalla, Z, Molina, G, and Malavé, J. (2017). Customer Behavior in Electronic Commerce: A Bayesian Approach. J. Theor. Appl. Electron. Commer. Res, 12, 1–20. doi: 10.4067/S0718-18762017000200002

Dalal, B. (2020). The antecedents and consequences of CSR skepticism: An integrated framework. J. Sustain. Mark. 1, 1–9. doi: 10.51300/josm-2020-18

Delgado-Ballester, E., and Luis Munuera-Alemán, J. (2005). Does brand trust matter to brand equity? J. Prod. Brand. Manag. 14, 187–196. doi: 10.1108/10610420510601058

Deloitte (2022). El impacto económico de COVID-19 (nuevo coronavirus). Deloitte Ecuad. Available online at: https://www2.deloitte.com/ec/es/pages/strategy/articles/el-impacto-economico-de-covid-19--nuevo-coronavirus-.html (Accessed February 15, 2022).

Dewi, R., and Handriana, T. (2021). Unlocking brand equity through brand image, service quality, and customer value. BISMA Bisnis Dan Manaj. 13, 94–107. doi: 10.26740/bisma.v13n2.p94-107

Engizek, N., and Yaşin, B. (2018). Influence of consumer attributions and service quality on support of corporate social responsibility. Organ. Mark. Emerg. Econ. doi: 10.15388/OMEE.2018.10.00005

Ennis, H. M. (2023). Perspectives on the banking turmoil of 2023. Econ. Brief, 23–35. Available at: https://www.richmondfed.org/publications/research/economic_brief/2023/eb_23-35

Fatma, M., and Khan, I. (2023). How do Bank Customers’ perceptions of CSR influence marketing outcomes: their trust, identification, and commitment? Sustain. For. 15:6000. doi: 10.3390/su15076000

Fatmawati, I., and Fauzan, N. (2021). Building customer trust through corporate social responsibility: the effects of corporate reputation and word of mouth. J. Asian Finance Econ. Bus. 8, 793–805. doi: 10.13106/jafeb.2021 vol8. no 3. 0793

Gelman, A., Carlin, J., Stern, H., Dunson, D., Ventari, A., and Rubin, D. (2013). Bayesian Data Analysis. 3er edition. Taylor and Francis: CRC Press.

Glaveli, N. (2021). Corporate social responsibility toward stakeholders and customer loyalty: investigating the roles of trust and customer identification with the company. Soc. Responsib. J. 17, 367–383. doi: 10.1108/SRJ-07-2019-0257

Gokarna, P., and Krishnamoorthy, B. (2021). Corporate social responsibility in the time of COVID-19 pandemic: an exploratory study of developing country corporates. Corp. Gov. Sustain. Rev 5, 73–80.

Ham, C., and Kim, J. (2020). The effects of CSR communication in corporate crises: examining the role of dispositional and situational CSR skepticism in context. Public Relat. Rev. doi: 10.1016/J.PUBREV.2019.05.013

Harrison, K., and Huang, L. (2023). What do these tweets mean for us? How analysis of consumer tweets sheds light on Consumers’ CSR beliefs and firm confidence. Bus. Res. Proc. 1, 1–55. doi: 10.51300/brp-2023-66

He, H., and Harris, L. (2020). The impact of Covid-19 pandemic on corporate social responsibility and marketing philosophy. J. Bus. Res. 116, 176–182. doi: 10.1016/j.jbusres.2020.05.030

Hidayat, K., and Idrus, M. I. (2023). The effect of relationship marketing towards switching barrier, customer satisfaction, and customer trust on bank customers. J. Innov. Entrep. 12:29. doi: 10.1186/s13731-023-00270-7

Hur, W.-M., and Kim, Y. (2020). Customer reactions to bank hypocrisy: the moderating role of customer–company identification and brand equity. Int. J. Bank Mark. 38, 1553–1574. doi: 10.1108/IJBM-04-2020-0191

Hur, W.-M., Moon, T.-W., and Kim, H. (2020). When does customer CSR perception lead to customer extra-role behaviors? The roles of customer spirituality and emotional brand attachment. J. Brand Manag. 27, 421–437. doi: 10.1057/s41262-020-00190-x

Hussaien, A. S. A., Hansani, H. L., Thelijjagoda, S., and Madhavika, W. D. N. (2020). Service quality and customer satisfaction in banking sector during COVID−19–An empirical analysis of Sri Lanka. Glob. J. Manag. Bus. Res. 20, 23–29.

Islam, T., Islam, R., Pitafi, A. H., Xiaobei, L., Rehmani, M., Irfan, M., et al. (2021). The impact of corporate social responsibility on customer loyalty: the mediating role of corporate reputation, customer satisfaction, and trust. Sustain. Prod. Consum. 25, 123–135. doi: 10.1016/j.spc.2020.07.019

Jeon, M. A., and An, D. (2019). A study on the relationship between perceived CSR motives, authenticity and company attitudes: a comparative analysis of cause promotion and cause-related marketing. Asian J. Sustain. Soc. Responsib. 4, 1–14. doi: 10.1186/s41180-019-0028-4

Joireman, J., Liu, R. L., and Kareklas, I. (2018). Images paired with concrete claims improve skeptical consumers’ responses to advertising promoting a firm’s good deeds. J. Mark. Commun. 24, 83–102. doi: 10.1080/13527266.2015.1126757

Jung, C. M., and Hur, W.-M. (2023). How does corporate hypocrisy reduce customer co-creation behaviors? Moderated mediation analysis of corporate reputation and self-brand connection. Int. J. Bank Mark. doi: 10.1108/ijbm-08-2022-0375

Körding, K. P., Ku, S., and Wolpert, D. M. (2004). Bayesian integration in force estimation. J. Neurophysiol. 92, 3161–3165. doi: 10.1152/jn.00275.2004

Krawczyk, D., Martynets, V., Opanasiuk, Y., and Rekunenko, I. (2023). Socio-economic development of European countries in times of crisis: ups and downs. Sustain. For. 15, 1–18. doi: 10.3390/su152014820

Księżak, P., and Szkolmowska, J. (2018). The development of the CSR concept and theories. J. Corp. Responsib. Leadersh. 5, 27–46. doi: 10.12775/JCRL.2018.010

Langat, B., and Atheru, G. (2023). Customer relationship management and competitive advantage of commercial banks in Kenya. Int. J. Bus. Manag. Entrep. Innov. doi: 10.35942/hjxgxf95

Marshall, N. W. (2010). Commitment, loyalty and customer lifetime value: investigating the relationships among key determinants. J. Bus. Econ. Res. JBER 8. Available online at: https://www.researchgate.net/profile/Palvi-Bhardwaj/post/is_there_any_scale_to_measure_customer_satisfaction_and_customer_loyalty/attachment/59d61d8c79197b8077977e7e/AS%3A271484883042304%401441738448427/download/commitment+and+loyalty.pdf (Accessed September 27, 2024).

Martínez, P., and Del Bosque, I. R. (2013). CSR and customer loyalty: the roles of trust, customer identification with the company and satisfaction. Int. J. Hosp. Manag. 35, 89–99. doi: 10.1016/j.ijhm.2013.05.009

Merz, M. A., Zarantonello, L., and Grappi, S. (2018). How valuable are your customers in the brand value co-creation process? The development of a customer co-creation value (CCCV) scale. J. Bus. Res. 82, 79–89. doi: 10.1016/j.jbusres.2017.08.018

Morgan, R. M., and Hunt, S. D. (1994). The commitment-trust theory of relationship marketing. J. Mark. 58, 20–38. doi: 10.1177/002224299405800302

Morgeson, F. V., Sharma, U., Schultz, X. W., Pansari, A., Ruvio, A., and Hult, G. T. M. (2024). Weathering the crash: do customer-company relationships pay off during economic crises? J. Acad. Mark. Sci. 52, 489–511. doi: 10.1007/s11747-023-00947-1

Osakwe, C. N., and Yusuf, T. O. (2021). CSR: a roadmap towards customer loyalty. Total Qual. Manag. Bus. Excell. 32, 1424–1440. doi: 10.1080/14783363.2020.1730174

Peña-García, N., Gil-Saura, I., Rodríguez-Orejuela, A., and Siqueira-Junior, J. R. (2020). Purchase intention and purchase behavior online: a cross-cultural approach. Heliyon 6:e04284. doi: 10.1016/j.heliyon.2020.e04284

Peña García, N., Saura, I., and Orejuela, A. (2018). E-loyalty formation: a cross-cultural comparison of Spain and Colombia. J. Electron. Commer. Res. 19, 336–356.

Prasetya, P. (2019). The effect of corporate CSR on customer attitudes. J. Mark. Consum. Res. doi: 10.7176/jmcr/53-08

Raimo, N., Rella, A., Vitolla, F., Sánchez-Vicente, M.-I., and García-Sánchez, I.-M. (2021). Corporate social responsibility in the COVID-19 pandemic period: a traditional way to address new social issues. Sustain. For. 13:6561. doi: 10.3390/su13126561

Ramasamy, S., Dara Singh, K. S., Amran, A., and Nejati, M. (2020). Linking human values to consumer CSR perception: the moderating role of consumer skepticism. Corp. Soc. Responsib. Environ. Manag. 27, 1958–1971. doi: 10.1002/csr.1939

Raza, A., Rather, R., Iqbal, M. K., and Bhutta, U. (2020). An assessment of corporate social responsibility on customer company identification and loyalty in banking industry: a PLS-SEM analysis. Manag. Res. Rev. doi: 10.1108/mrr-08-2019-0341

Riza, F., and Santoso, R. A. (2023). The Influence of Relationship Marketing on Loyalty with Mediation of Customer Trust at PT. Bank Rakyat Indonesia (Persero) Tbk Krian Branch Office. Dinasti International Journal of Economics, Finance \u0026amp; Accounting (DIJEFA), 4.

Sanchez-Franco, M. J. (2009). The moderating effects of involvement on the relationships between satisfaction, trust and commitment in e-banking. J. Interact. Mark. 23, 247–258. doi: 10.1016/j.intmar.2009.04.007

Sharma, A., Fadahunsi, A., Abbas, H., and Pathak, V. K. (2022). A multi-analytic approach to predict social media marketing influence on consumer purchase intention. J. Indian Bus. Res. 14, 125–149. doi: 10.1108/JIBR-08-2021-0313

Singh, J. J., Iglesias, O., and Batista-Foguet, J. M. (2012). Does having an ethical brand matter? The influence of consumer perceived ethicality on trust, affect and loyalty. J. Bus. Ethics 111, 541–549. doi: 10.1007/s10551-012-1216-7

Siqueira, J. R., Peña, N. G., ter Horst, E., and Molina, G. (2019). Spreading the word: how customer experience in a traditional retail setting influences consumer traditional and electronic word-of-mouth intention. Electron. Commer. Res. Appl. 37:100870. doi: 10.1016/j.elerap.2019.100870

Siqueira, J. R., ter Horst, E., Molina, G., Losada, M., and Mateus, M. A. (2020). A Bayesian examination of the relationship of internal and external touchpoints in the customer experience process across various service environments. J. Retail. Consum. Serv. 53:102009. doi: 10.1016/j.jretconser.2019.102009

Skarmeas, D., and Leonidou, C. N. (2013). When consumers doubt, watch out! The role of CSR skepticism. J. Bus. Res. 66, 1831–1838. doi: 10.1016/j.jbusres.2013.02.004

Statista (2022). Coronavirus: impact on the global economy. Statista. Available online at: http://www.statista.com/study/71343/economic-impact-of-the-coronavirus-covid-19-pandemic/ (Accessed February 15, 2022).

Taliento, M., and Netti, A. (2020). Corporate social/environmental responsibility and value creation: reflections on a modern business management paradigm. Bus. Ethics Leadersh. doi: 10.21272/BEL.4(4).123-131.2020

Teah, K., Phau, I., and Sung, B. (2023). CSR commitment and consumer situational scepticism of luxury brands: antecedents, moderator and outcomes. Int. J. Ethics Syst. doi: 10.1108/ijoes-06-2023-0141

Tirado, D. M., Vidal-Meliá, L., Cardiff, J., and Quille, K. (2023). Vulnerable customers’ perception of corporate social responsibility in the banking sector in a post-crisis context. Int. J. Bank Mark. doi: 10.1108/ijbm-03-2023-0162

Wagner, T., Korschun, D., and Troebs, C.-C. (2020). Deconstructing corporate hypocrisy: a delineation of its behavioral, moral, and attributional facets. J. Bus. Res. 114, 385–394. doi: 10.1016/j.jbusres.2019.07.041

Wagner, T., Lutz, R. J., and Weitz, B. A. (2009). Corporate hypocrisy: overcoming the threat of inconsistent corporate social responsibility perceptions. J. Mark. 73, 77–91. doi: 10.1509/jmkg.73.6.77

Wang, Z., Liu, X., Zhang, L., Wang, C., and Liu, R. (2022). Effect of matching between the adopted corporate response strategy and the type of hypocrisy manifestation on consumer behavior: mediating role of negative emotions. Front. Psychol. 13, 1–20. doi: 10.3389/fpsyg.2022.831197

Xie, C., Bagozzi, R., and Grønhaug, K. (2019). The impact of corporate social responsibility on consumer brand advocacy: the role of moral emotions, attitudes, and individual differences. J. Bus. Res. 95, 514–530. doi: 10.1016/J.JBUSRES.2018.07.043

Zasuwa, G., and Stefańska, M. (2023). How do CSI and CSR perceptions affect word of mouth recommendations? The role of trust, distrust, and moral norms. Corp. Commun. Int. J. 28, 905–923. doi: 10.1108/CCIJ-11-2022-0139

Zhang, D., Mahmood, A., Ariza-Montes, A., Vega-Muñoz, A., Ahmad, N., Han, H., et al. (2021). Exploring the impact of corporate social responsibility communication through social media on banking customer E-WOM and loyalty in times of crisis. Int. J. Environ. Res. Public Health 18:4739. doi: 10.3390/ijerph18094739

Keywords: CSR motives, corporate hypocrisy, CSR skepticism, CSR beliefs, attitudes, commitment

Citation: Peña-García N, Losada-Otálora M and ter Horst E (2025) The effect of CSR beliefs among bank customers during difficult economic times. Front. Commun. 10:1538309. doi: 10.3389/fcomm.2025.1538309

Edited by:

Naser Valaei, Liverpool John Moores University, United KingdomReviewed by:

Nada Nasr, Bentley University, United StatesCarmen Adina Pastiu, 1 Decembrie 1918 University, Romania

Copyright © 2025 Peña-García, Losada-Otálora and ter Horst. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Nathalie Peña-García, bmF0aGFsaWUucGVuYUBjZXNhLmVkdS5jbw==