Jeaneth Lucía Bastidas-Guerrón1

Jeaneth Lucía Bastidas-Guerrón1 Gisselle Mariuxi Cárdenas-Fierro1

Gisselle Mariuxi Cárdenas-Fierro1 Ana Cristina Mora-Lucero1Freddy Richard Quinde-Sari1

Ana Cristina Mora-Lucero1Freddy Richard Quinde-Sari1 Angel Ramón Sabando-García2

Angel Ramón Sabando-García2 Jenniffer Sobeida Moreira-Choez3*

Jenniffer Sobeida Moreira-Choez3*- 1Facultad de Comercio Internacional, Integración, Administración y Economía Empresarial de la Universidad Politécnica Estatal del Carchi, Tulcán, Ecuador

- 2Departamento de Estadística y Matemática de la Universidad Católica del Ecuador, Sede Santo Domingo de los Colorados, Santo Domingo, Ecuador

- 3Departamento de Matemáticas y Estadísticas de la Facultad de Ciencias Básicas de la Universidad Técnica de Manabí, Portoviejo, Ecuador

Background: Financial literacy has been recognized as a key competency for making in-formed economic decisions, particularly in contexts where access to financial products exceeds the population’s literacy level. However, in Ecuador, persistent gaps remain be-tween formal educational attainment and applied financial knowledge. In this context, the objective of this study was to analyze the relationship between educational level and financial literacy among Ecuadorian students.

Methods: A quantitative approach was adopted, with a descriptive-correlational level, non-experimental type, and cross-sectional design. The sample consisted of 2,021 participants, selected through non-probabilistic convenience sampling. A structured questionnaire of 33 items was administered, distributed across four analytical dimensions. Statistical analysis was performed using SPSS and AMOS, including reliability testing, factorial validity, and structural model fit.

Results: The results revealed that educational level has a significant effect on financial literacy. Individuals with higher education exhibited the highest levels, while those who completed only primary education showed the lowest. Four latent factors were validated: technical knowledge, socioeconomic impact of financial education, practical application of knowledge, and financial self-management.

Conclusion: The correlations between these factors were strong and statistically significant, highlighting the pivotal role of educational level in shaping financial literacy. The proposed model presents a valid and consistent structure, effectively reflecting the relationships between the key variables. These findings emphasize the necessity for tailored and context-specific educational interventions that address the diverse needs of different population segments, thereby enhancing financial literacy across varying educational levels.

1 Introduction

Various studies have demonstrated that financial literacy constitutes an essential competency for the economic and social development of individuals, particularly in con-texts where access to financial services has expanded rapidly without adequate education to support their responsible use (Grohmann et al., 2018; Lusardi, 2019). In Latin America, research by da Silva Souza Caggy et al. (2023); Méndez-Prado et al. (2022) highlights deficiencies in financial literacy levels, even among populations with higher education, reflecting a dis-connect between educational attainment and mastery of financial knowledge and skills. This situation is particularly concerning in the Ecuadorian context, where recent studies have shown that a significant proportion of university students exhibit limitations in planning, budgeting, and making informed decisions about their personal finances (Loza et al., 2023; Méndez-Prado et al., 2022; Tulcanaza-Prieto et al., 2025).

Despite advances in the measurement of financial literacy, significant gaps remain in the national literature. First, there is limited empirical evidence linking financial literacy to key sociodemographic variables such as educational level, using a robust multivariate approach (Rehman and Mia, 2024; Siegfried and Wuttke, 2021). Second, the theoretical models commonly applied often lack rigorous statistical validation and instruments adapted to the Ecuadorian context (Méndez-Prado et al., 2023; Moreira-Choez et al., 2023). Moreover, a limited articulation is observed between academic findings and the formulation of public policies aimed at promoting financial inclusion based on the population’s educational level.

In the Ecuadorian context, the study of financial literacy among students is particularly relevant due to the country’s unique socioeconomic and educational characteristics. Ecuador, a developing nation in Latin America, faces significant disparities in terms of access to quality education and financial services. While recent educational reforms have aimed to address these gaps, financial literacy remains an area that has not been fully integrated into the national curriculum. The diverse socioeconomic backgrounds of students, particularly in rural and marginalized areas, further complicate efforts to provide consistent and effective financial education. As such, analyzing how educational level influences financial literacy in Ecuador provides valuable insights into how the education system can better meet the financial needs of its students and inform more targeted interventions.

Additionally, Ecuador’s economic environment characterized by inflationary fluctuations, changing exchange rates, and high unemployment adds complexity to financial decision-making, especially for students in the process of developing financial knowledge. The findings from this study can offer critical evidence to help design educational interventions that are specifically tailored to the needs of Ecuadorian students, addressing their particular challenges and opportunities. By considering the country’s unique economic and educational context, the research aims to contribute to the creation of more effective policies and practices that foster financial literacy, thereby empowering students to make informed financial decisions and improving their overall financial wellbeing.

Within this context, the following research question is posed: What is the relationship between educational level and financial literacy among Ecuadorian students? This inquiry is pivotal in understanding how various levels of education impact the financial knowledge and behaviors of students within the context of Ecuador’s unique socioeconomic environment. To explore this relationship, the study is framed around the following hypotheses:

H1. There is a significant positive relationship between the educational level and the financial literacy of Ecuadorian students.

H2. Socioeconomic awareness, as influenced by financial education, positively impacts students’ practical application of financial knowledge.

H3. Technical-financial knowledge significantly predicts students’ financial self-management behaviors.

H4. The perception of the socioeconomic impact of financial education is positively correlated with students’ engagement in entrepreneurship and innovation.

To address the research question and test the proposed hypotheses, the study aims to analyze the relationship between educational level and financial literacy among Ecuadorian students, with the purpose of understanding how different educational backgrounds influence students’ financial knowledge, decision-making, and behaviors. This analysis will provide valuable insights into the factors that contribute to financial literacy in a developing context, such as Ecuador, where socio-economic disparities may affect access to financial education.

2 Theoretical foundations

Financial literacy is conceptualized as the set of knowledge, skills, and attitudes necessary to make informed decisions regarding personal financial resource management. This competence involves not only understanding technical concepts but also the ability to apply them effectively in everyday life, with a significant impact on individual and collective economic wellbeing (Akbaş and Seedsman, 2024; Goyal and Kumar, 2021; Mavlutova et al., 2021). In the context of this research, financial literacy will be addressed through four key dimensions that reflect its practical applicability and its relationship with the socioeconomic environment.

Firstly, technical-financial knowledge refers to the understanding of fundamental concepts related to money management, such as saving, investing, credit, insurance, and financial planning (Muthu and Bharathi, 2025; Owuor et al., 2022). This component is essential for individuals to make informed and appropriate financial decisions in various contexts. However, although technical knowledge is crucial, its effectiveness depends on individuals’ ability to apply it practically.

The dimension of the socioeconomic impact of financial education emphasizes how access to financial education can improve individuals’ economic conditions and, consequently, contribute to broader social and economic development (Brüggen et al., 2017; Resham et al., 2024). Previous studies suggest that financial literacy not only improves individuals’ ability to manage finances but also has positive effects on the local economy by reducing vulnerability to economic crises (Katnic et al., 2024; Lusardi and Mitchell, 2014; Matewos et al., 2016).

The practical application of knowledge is another relevant dimension, as it refers to individuals’ ability to use acquired knowledge in real-life situations, such as making decisions about saving, investing, or borrowing (Garg and Singh, 2018; Pang, 2010). Unlike theoretical knowledge, the ability to make correct financial decisions depends on experience and the contextual application of financial principles. Finally, personal financial management refers to the ability to plan and control spending, save adequately, and manage credit, which is a fundamental part of individual financial decision-making (Mieèinskienë et al., 2023; Rodriguez et al., 2024). This dimension is closely linked to economic wellbeing, as proper personal financial management can prevent debt issues and improve long-term financial stability.

3 Materials and methods

This study was framed within a quantitative approach, with a descriptive-correlational level of research, as it aimed to characterize the population based on sociodemographic variables and establish associations between these and the level of financial literacy. The research was non-experimental in nature, since the variables were not intentionally manipulated, and a cross-sectional design was adopted, as data were collected at a single point in time.

The study population consisted of students at different levels of the educational system, as well as individuals engaged in continuing education (CE), with no geographical or age restrictions. This allowed for a broad perspective on financial literacy across various social segments. The sample was composed of 2,021 participants, selected through non-probabilistic convenience sampling. This technique was employed due to the ease of access to participants in both face-to-face and digital settings, which facilitated efficient data collection in diverse contexts.

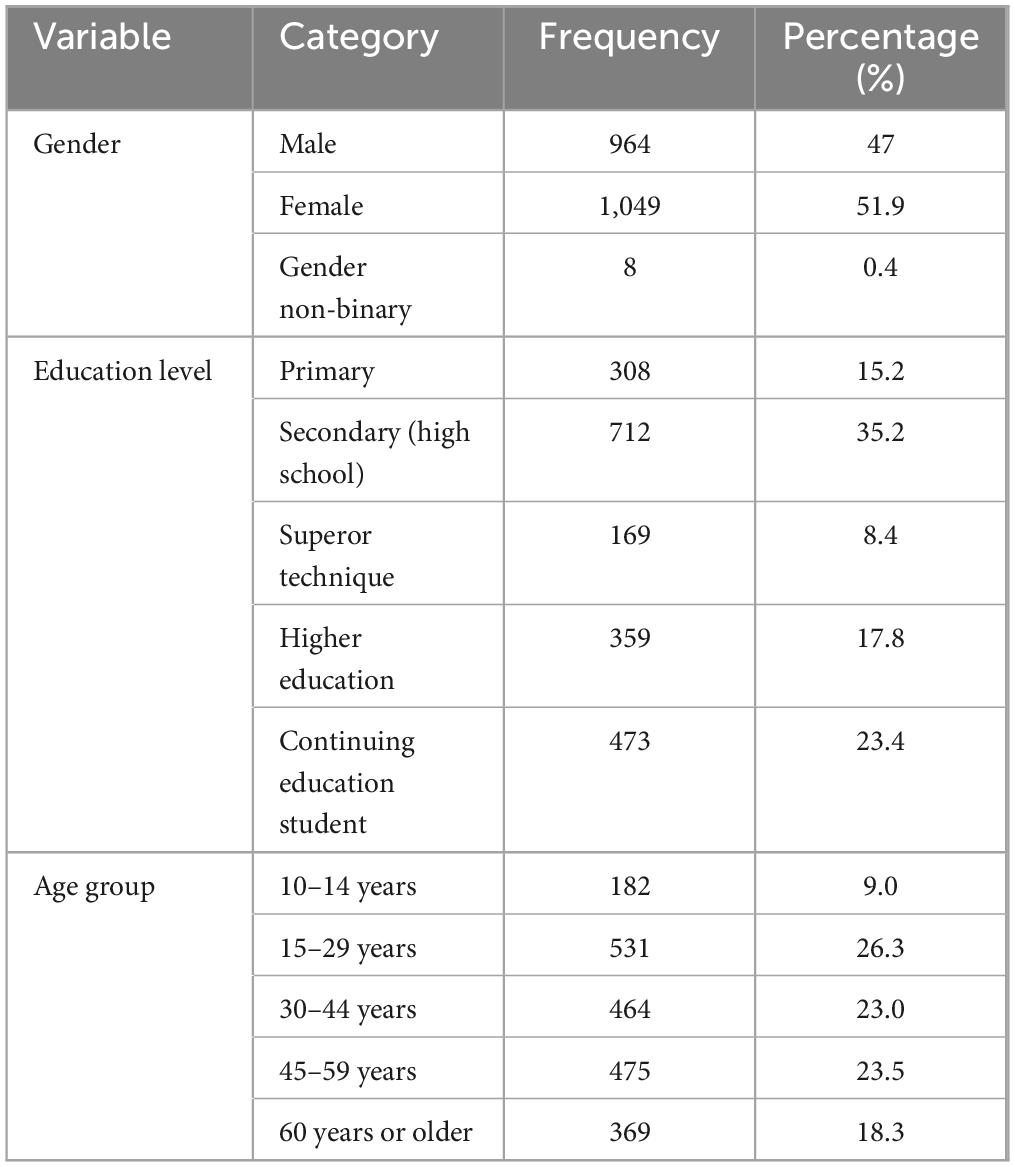

In order to contextualize the characteristics of the sample, Table 1 presents the sociodemographic distribution of the participants according to gender, educational level, and age group. These attributes are relevant for the subsequent analysis, as the specialized literature has highlighted their potential influence on levels of financial competence. The detailed characterization reveals, for instance, a gender balance with a slight female majority, a significant presence of secondary and continuing education students, and a broad representation of individuals within economically active age groups. This internal diversity of the sample strengthens the analytical validity of the study and ensures the relevance of the findings in comparable contexts.

Table 1. Sociodemographic distribution of participants.

The sociodemographic distribution of participants in the study provides key insights into the profile of the sample, which includes several variables that are critical for understanding the factors influencing financial literacy. The gender distribution indicates a gender-balanced sample, with a slight majority of females (51.9%) compared to males (47%), and a minimal representation of non-binary individuals (0.4%). The inclusion of gender as a variable is relevant, as financial literacy may differ across genders due to societal roles, economic opportunities, and access to financial resources. This variable is crucial for understanding the possible disparities in financial behavior and decision-making across different gender groups.

In terms of education level, the sample is primarily composed of individuals with secondary education (35.2%), followed by continuing education students (23.4%) and those with higher education (17.8%). A smaller proportion holds a technical education (8.4%) or primary education (15.2%). This distribution is important because it highlights that the majority of participants have mid-level education or are in the process of professionalizing. This educational background may significantly influence the level of financial literacy, as higher levels of education generally correlate with better financial knowledge and decision-making skills. The relatively lower proportion of participants with technical or primary education may reflect systemic barriers to accessing higher educational opportunities in certain sectors, which could affect their financial literacy levels and overall economic opportunities.

Regarding age, the majority of participants fall within economically active age groups: 26.3% are between 15 and 29 years, 23.5% are between 45 and 59 years, and 23.0% are between 30 and 44 years. These age groups are particularly relevant for analyzing financial literacy, as individuals within these ranges are likely to face responsibilities associated with income generation, saving, investing, and managing debt. Moreover, younger adults are often in the process of acquiring financial knowledge, while middle-aged individuals might already be making significant financial decisions, such as home ownership, retirement planning, and family budgeting. The inclusion of these age categories allows for a deeper understanding of how financial literacy varies across the life cycle and within different stages of financial responsibility.

The data collection technique consisted of administering a structured survey both in person and online, ensuring the participation of individuals with diverse sociodemographic profiles. The instrument used was a 33-item questionnaire distributed across four analytical factors, designed to assess multiple dimensions of financial literacy. These dimensions address key aspects of financial literacy, such as technical-financial knowledge, the practical application of knowledge, the socioeconomic impact of financial education, and personal financial management. The questions were designed to capture both theoretical knowledge and the participants’ ability to apply this knowledge in everyday situations, allowing for a comprehensive and detailed assessment of the students’ financial competencies. The administration of the questionnaire was preceded by informed consent, safeguarding ethical principles of confidentiality, anonymity, and voluntariness.

Additionally, several methodological limitations are recognized that should be considered when interpreting the results. The sample was selected through non-probabilistic convenience sampling, meaning that the findings cannot be generalized to all populations but are limited to the specific group studied. Furthermore, the gender distribution in the sample showed a slight imbalance, with a majority of female participants, which could have influenced the responses obtained.

For statistical analysis, SPSS version 25 was used during the preliminary phase to perform descriptive statistics and assess the internal reliability of the instrument. Subsequently, AMOS version 24 was employed to conduct structural equation modeling (SEM), which allowed for the examination of latent construct structures and the verification of theoretical relationships among the variables included in the proposed model.

At this initial stage, the reliability of the instrument was established using Cronbach’s alpha coefficient (α = 0.972) and McDonald’s Omega index (ω = 0.972), both indicating excellent internal consistency. Thereafter, to validate the construct structure, a two-phase factorial strategy was implemented. First, an exploratory factor analysis (EFA) was conducted to identify the underlying dimensions without imposing prior theoretical assumptions, which enabled the reorganization and refinement of the questionnaire items based on emerging correlation patterns.

Subsequently, a confirmatory factor analysis (CFA) was carried out with the explicit objective of empirically validating the dimensional structure suggested by the EFA. In contrast to the exploratory phase, CFA tested a theoretically grounded measurement model by evaluating factor loadings, error variances, and overall model fit indices. This procedure was essential to confirm that the latent constructs were accurately represented by the observed indicators. In this context, the inclusion of CFA was not a redundant step, but a critical methodological phase prior to the structural analysis. The robustness of the dataset for these techniques was supported by a Kaiser-Meyer-Olkin (KMO) index of 0.976 and a statistically significant Bartlett’s test of sphericity (p < 0.001), confirming sample adequacy for factorial analyses.

Finally, once the measurement model had been validated, SEM was employed to evaluate the hypothesized relationships among latent constructs. The resulting model fit indices were satisfactory (CFI = 0.929; RMSEA = 0.073), thereby confirming both the validity of the structural model and the theoretical soundness of the framework. Therefore, the application of CFA was not a remnant of a previous draft but an integral part of the methodological approach, aimed at ensuring the psychometric quality of the instrument before testing structural hypotheses within the overall model.

4 Results and discussion

This section presents the results obtained from the statistical analysis of the data, aimed at determining the influence of educational level on participants’ financial literacy. To this end, an inter-subject effects test was applied to identify whether statistically significant differences existed among educational groups with respect to their reported levels of financial literacy.

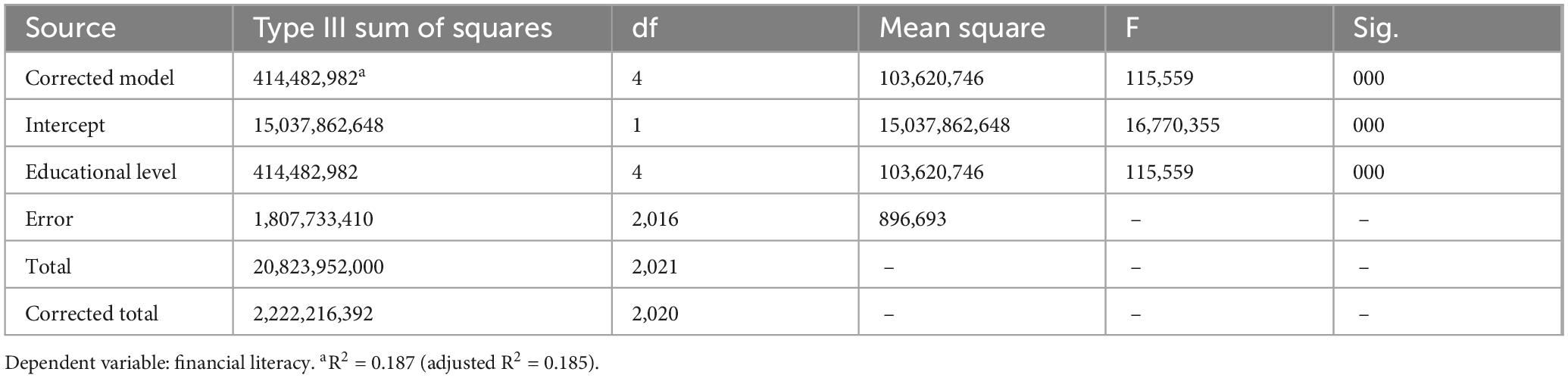

Table 2 below summarizes the results of the one-way analysis of variance (ANOVA), in which educational level was considered the independent variable and financial literacy the dependent variable. The table reports values for the sum of squares, degrees of freedom, mean square, F statistic, and the significance level associated with each source of variation.

Table 2. Analysis of variance: effects of educational level on financial literacy.

The analysis of variance (ANOVA) revealed that educational level exerts a statistically significant effect on financial literacy, as reflected by the F statistic = 115.559 and a significance level of p < 0.001. This result confirms that there are meaningful differences in financial literacy across the different levels of educational attainment, indicating that academic formation plays a relevant role in explaining the variability observed in financial knowledge. Furthermore, the coefficient of determination (R2 = 0.187; adjusted R2 = 0.185) shows that approximately 18.7% of the variance in financial literacy scores is attributable to differences in educational level. Although this represents a moderate effect, it is consistent and statistically robust, supporting the hypothesis that formal education contributes substantially to individuals’ financial competencies.

These findings are aligned with previous empirical evidence. Jugnandan and Willows (2023) highlight that individuals with higher levels of academic achievement tend to demonstrate a stronger command of essential financial principles, enabling more informed and sustainable financial decision-making. Similarly, Mindra and Moya (2017) argue that formal education enhances financial behavior by fostering critical attitudes and practices. In line with this, Gerrans and Heaney (2019) found that individuals with tertiary education exhibit significantly better outcomes in financial planning, savings, and credit use.

Table 3 presents the mean comparison of financial literacy scores across different educational levels, using the Tukey HSD post hoc test to identify significant differences between groups. The table shows the mean differences, standard errors, significance values, and confidence intervals for each pairwise comparison. These results highlight the impact of educational attainment on financial literacy, with higher education levels associated with greater financial knowledge.

Table 3. Mean comparison of financial literacy by educational level.

The data presented in Table 3 highlights the significant differences in financial literacy scores across various educational levels, demonstrating a clear trend: as educational attainment increases, so does financial literacy. This pattern suggests that education plays a critical role in equipping individuals with the necessary knowledge and skills to make informed financial decisions. It is widely recognized that higher education fosters a deeper understanding of complex financial concepts, which could explain the differences observed in this study. The observed progression in financial literacy is consistent with the findings of previous studies, such as those by Silva et al. (2017), who emphasized the positive correlation between educational level and financial knowledge, suggesting that higher levels of formal education lead to better financial planning and decision-making.

Specifically, individuals with primary education had the lowest financial literacy scores (74.2955), whereas those with higher education achieved the highest (116.4847). This significant gap between the two groups underscores the impact of education on financial knowledge and behavior. The Tukey HSD post hoc test showed that all educational categories were significantly different from each other, with the largest difference observed between primary education and higher education (42.1892), which was statistically significant (p < 0.000). This finding suggests that educational attainment is not only associated with financial literacy but also plays a substantial role in narrowing or widening the knowledge gap between individuals from different educational backgrounds.

The pairwise comparisons provided by the Tukey test further clarify the specific differences between the educational groups. These comparisons offer a more precise understanding of how financial literacy varies across educational levels. The results reinforce previous literature, such as that of Johan et al. (2021), who found that individuals with higher educational attainment are more likely to engage in behaviors such as saving, investing, and managing credit effectively. The clear differences between educational groups in this study support the notion that formal education is a key driver of financial knowledge and decision-making capabilities.

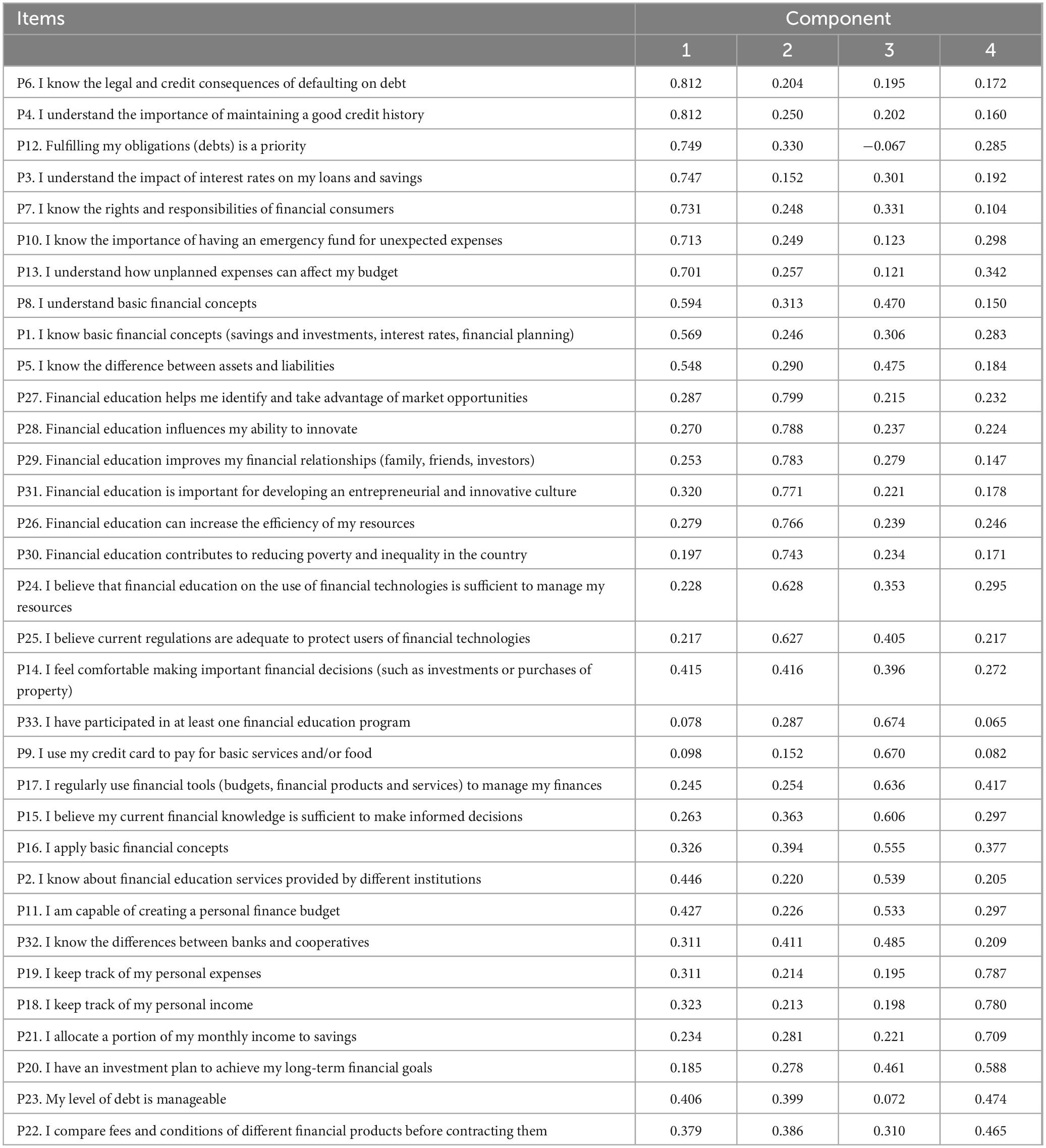

Exploratory factor analysis allows for the identification of latent dimensions that structure a set of items related to financial literacy. This statistical procedure aims to group items based on shared patterns of variability, reducing data complexity and facilitating the theoretical interpretation of the factors. Table 4 below presents the factor loadings of 33 items distributed across four main components, obtained through the principal components method with rotation. It is important to note that non-orthogonal rotation was applied, which enabled the conceptual grouping of the items while allowing for the factors to be correlated, thereby providing a more flexible and realistic model for interpreting financial literacy dimensions.

Table 4. Factor components of financial literacy.

The interpretation of the table reveals that Component 1 groups items associated with technical financial knowledge, particularly those related to credit obligations, interest rates, consumer financial rights, and fundamental concepts such as assets, liabilities, and financial planning. This factor can be conceptualized as instrumental financial literacy, as it encompasses the essential knowledge required for informed economic decision-making. This finding is consistent with the work of Luèiæ et al. (2023), who emphasize that understanding fundamental financial concepts is the foundation for rational financial behaviors, including spending, saving, and investing. Without this foundational knowledge, individuals may struggle to navigate complex financial decisions, potentially resulting in suboptimal financial outcomes.

Component 2 groups items related to the perception of the impact of financial education on broad social and economic dimensions, such as innovation, entrepreneurship, inequality reduction, and resource optimization. This factor can be interpreted as socioeconomic awareness of financial education, reflecting an understanding of its structural value. Financial education goes beyond personal financial management and contributes to sustainable development and social inclusion. For example, it can foster entrepreneurship by providing individuals with the knowledge to identify market opportunities, efficiently manage resources, and build sustainable businesses. In rural or marginalized communities, this can lead to the creation of small businesses, job opportunities, and greater economic mobility. Furthermore, financial education plays a crucial role in inequality reduction by empowering underserved populations, such as low-income individuals or women, to access and effectively utilize financial services. This leads to improved financial security and a reduction in socioeconomic disparities. In addition, resource optimization through financial education enables individuals to make informed decisions about saving, investing, and budgeting, enhancing personal wealth and contributing to overall societal prosperity. Thus, financial literacy not only enhances individual financial wellbeing but also promotes broader social inclusion, fostering a more equitable and sustainable society. In line with Cebrián and Junyent (2015), it is evident that financial literacy is a powerful tool for social transformation, as it equips individuals with the skills needed to engage fully in economic activities and improve their quality of life.

Component 3, in contrast, encompasses items related to the use and practical application of financial tools, such as budgeting, the use of financial services, credit card management, and participation in financial education programs. This factor can be interpreted as functional financial behavior, which represents the level of practical engagement in managing personal finances. This dimension has been highlighted by Weerasinghe et al. (2025), who assert that observable behaviors, rather than theoretical knowledge alone, are more immediate predictors of financial stability. Individuals who actively apply financial tools and participate in financial education programs are more likely to manage their finances effectively, leading to greater economic stability and resilience.

Finally, Component 4 integrates items related to income and expenditure management, savings, and long-term financial planning, thereby reflecting a personal financial self-management dimension. This aspect operationalizes the individual’s ability to organize household finances and achieve financial goals, ensuring long-term economic security. Studies, such as those conducted by Festa and Knotts (2021), support this interpretation by demonstrating that competencies in financial self-management are positively associated with higher levels of economic wellbeing and a reduced risk of problematic indebtedness. Effective personal financial management not only contributes to financial stability but also mitigates the risks associated with over indebtedness, fostering a more secure and prosperous future for individuals and their families.

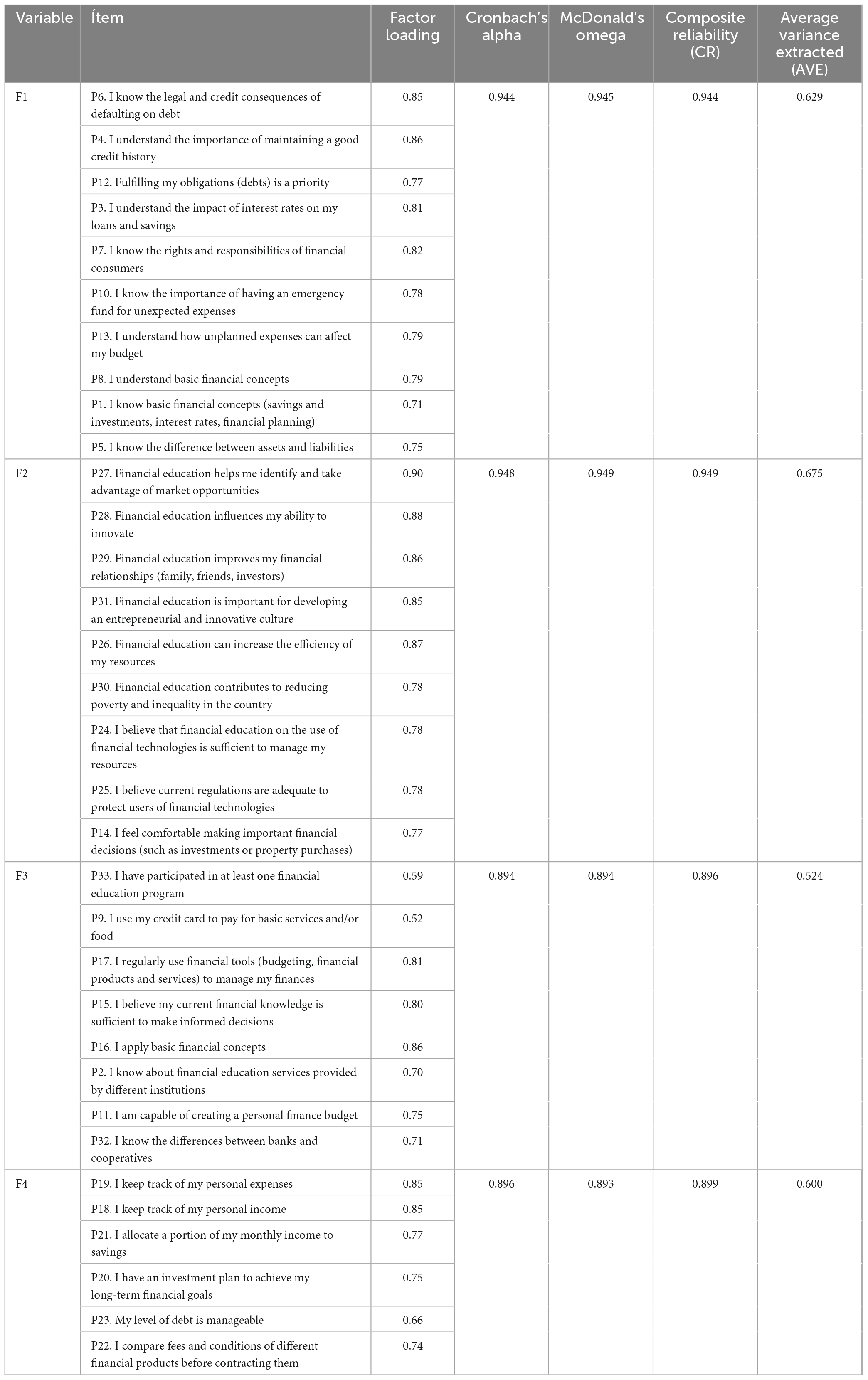

The assessment of the psychometric quality of measurement instruments is essential in studies on financial competencies, as it ensures the validity and reliability of conclusions derived from the data. In this context, analyses of internal consistency and convergent validity were applied to the factors derived from the financial literacy model. Table 5 presents the reliability and validity indicators for the four identified factors, reporting standardized factor loadings, Cronbach’s alpha coefficient, McDonald’s omega, composite reliability (CR), and average variance extracted (AVE).

Table 5. Reliability and validity indicators of the financial literacy factors.

For Factor 1, associated with technical and conceptual financial knowledge, all items showed factor loadings above 0.70. Cronbach’s alpha was 0.944 and McDonald’s omega was 0.945, indicating high internal consistency. The composite reliability was 0.944 and the average variance extracted (AVE) reached 0.629, exceeding the thresholds recommended by Hafeez et al. (2022), who suggest that AVE values above 0.50 and CR values above 0.70 provide evidence of adequate convergent validity. These results reflect a robust structure for measuring essential knowledge related to responsible credit use, financial planning, and understanding of basic financial concepts.

Regarding Factor 2, related to the perception of the social and economic impact of financial education, high loadings were observed across all items, with values exceeding 0.85. Cronbach’s alpha was 0.948 and McDonald’s omega reached 0.949, indicating excellent reliability. Additionally, the composite reliability was 0.949 and the AVE was 0.675. These results are consistent with studies such as Kyeyune and Ntayi (2025), who emphasize that financial education not only strengthens individual decision-making but also fosters the development of competencies that influence the social, professional, and productive spheres.

With respect to Factor 3, which groups the practical application of financial knowledge, satisfactory indicators were also reported. Both Cronbach’s alpha and McDonald’s omega were 0.894, while the composite reliability reached 0.896 and the AVE was 0.524. Although some items presented slightly lower loadings (e.g., items P9 and P33), the overall values remained within acceptable parameters. These findings suggest that the construct measured has a solid structure for representing everyday financial behavior, in line with García-Mata and Zerón-Félix (2022), who argue that the practical application of financial knowledge constitutes a critical dimension of sustainable financial wellbeing.

Finally, Factor 4, associated with financial self-management and resource control, also showed high levels of reliability: Cronbach’s alpha was 0.896, McDonald’s omega was 0.893, composite reliability was 0.899, and AVE reached 0.600. Factor loadings were high across all items, particularly those related to saving, planning, and managing income and expenditures. These results support the findings of Kasoga and Tegambwage (2024), who emphasize that conscious control of personal finances represents a key skill to avoid excessive debt and promote long-term economic stability.

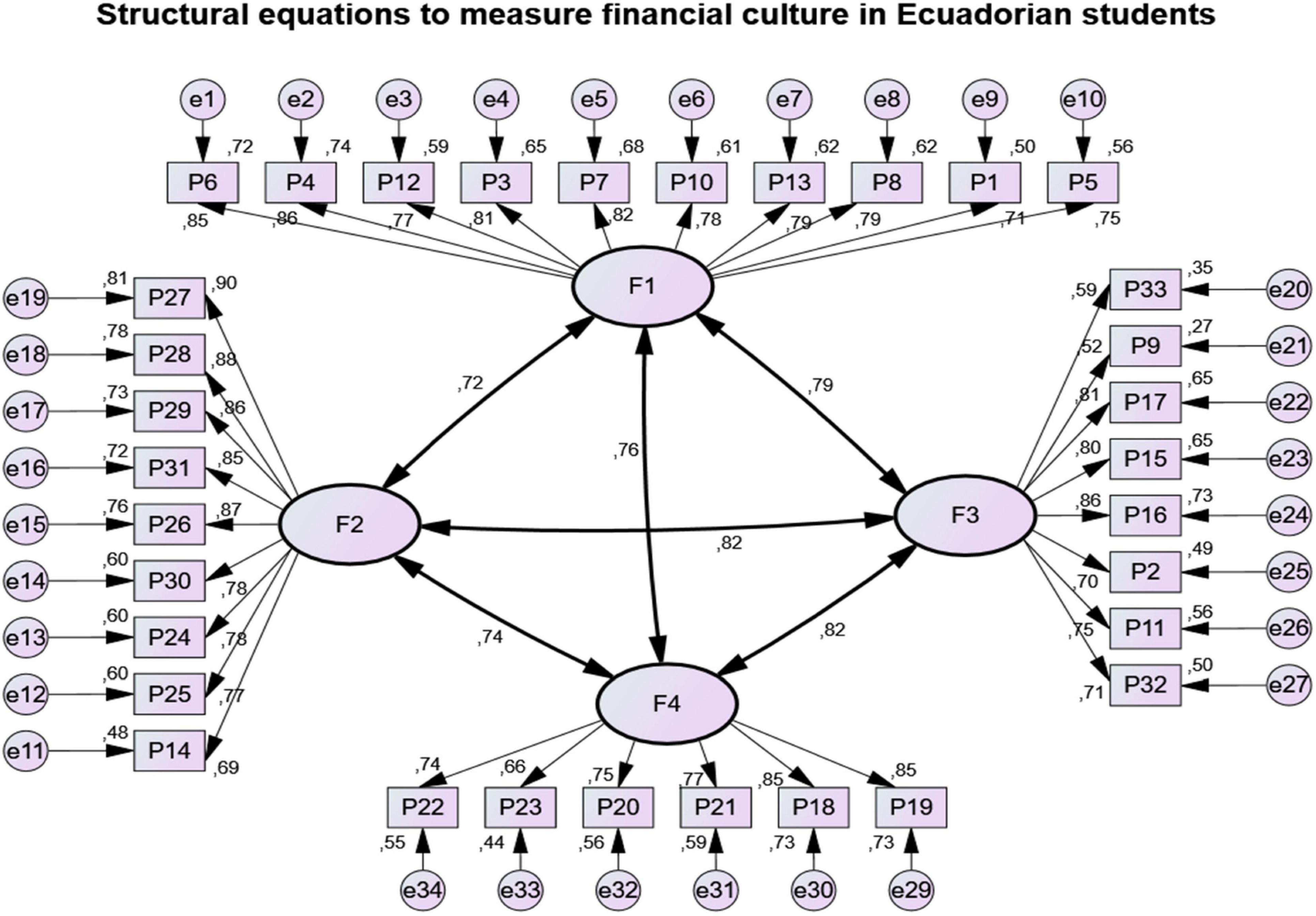

Figure 1 below presents the structural model estimated based on the empirical data collected. This model establishes relationships between the identified latent factors (F1 to F4) and their corresponding observed indicators, as well as the correlations among the factors. Each component was modeled based on the validated items from the previous exploratory factor analysis, allowing for an assessment of model fit quality and the significance of the estimated paths.

Figure 1. Standardized structural equation model for measuring financial literacy. It shows the relationships between latent constructs (F1: technical-financial knowledge, F2: perception of the socioeconomic impact of financial education, F3: practical application of knowledge, F4: personal financial self-management) and their respective observed items (P). Arrows indicate standardized factor loadings and regression coefficients among latent factors, all statistically significant. Measurement errors (e) are associated with each observed variable.

The figure represents the relationship between the four latent variables (F1 to F4) and their observed indicators, as well as the correlations among factors. Factor 1 (F1), associated with technical-financial knowledge, shows high standardized loadings (= 0.71) across all items, supporting its internal consistency. This factor is significantly related to Factor 2 (F2), which measures awareness of the social impact of financial education (r = 0.72), suggesting that a solid foundation in technical knowledge is associated with a greater perception of the social utility of financial literacy. This finding is consistent with Lontchi et al. (2022), who argue that understanding basic financial concepts enhances both economic autonomy and responsible participation in the financial environment.

Factor 3 (F3) reflects the practical application of financial knowledge. Factor loadings in this component are consistent (ranging from 0.52 to 0.86), indicating a well-defined structure. The relationship between F3 and both F1 (r = 0.79) and F2 (r = 0.84) demonstrates that the implementation of financial concepts depends on both knowledge and the contextual appreciation of financial education. Murari (2019) states that financial literacy should be assessed not only by knowledge acquisition but also by its behavioral impact, including everyday financial decisions such as saving, credit use, and budgeting.

In turn, Factor 4 (F4) encompasses indicators related to personal financial management, such as income control, savings, and planning. The relationships between F4 and the other factors are all statistically significant (r = 0.74), suggesting that financial self-management is holistically influenced by knowledge, perception, and practice. This finding aligns with Kiesnere and Baumgartner (2019), who affirm that the combination of technical knowledge, a positive attitude, and practical experience increases the likelihood of efficient and sustainable financial management.

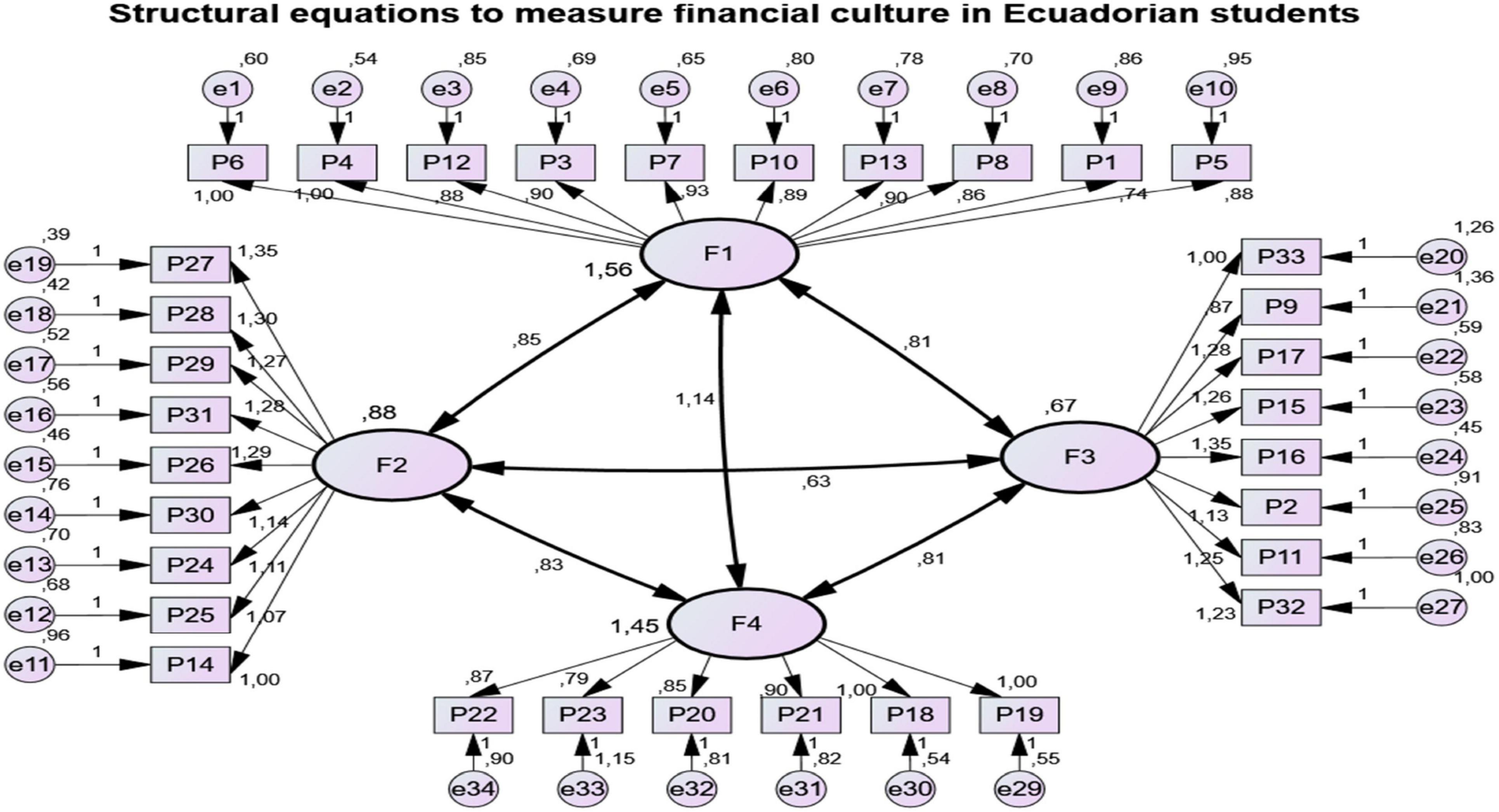

Figure 2 below graphically presents the structural model of financial literacy. This diagram displays the direct relationships between the four latent factors and their corresponding observed variables. It also highlights significant correlations among the latent components, thus emphasizing the interdependence of the dimensions within the construct under analysis.

Figure 2. Unstandardized structural model of financial literacy: relationships between latent factors and observed indicators. It shows the relationships between latent factors (F1: technical-financial knowledge, F2: perception of the socioeconomic impact of financial education, F3: practical application of knowledge, and F4: personal financial self-management) and their respective observed indicators. All depicted paths are statistically significant (p < 0.001), and standardized coefficients are shown along the arrows.

Figure 2 displays high unstandardized factor loadings across all items, particularly those associated with Factor F1, related to basic financial knowledge and credit obligations, with loadings ranging between 0.74 and 0.93. In this context, values greater than one may be interpreted as indicators of stronger predictive capacity within the multivariate model, without compromising the validity of the analysis. This supports the conclusion that the first factor exhibits adequate internal consistency, reinforcing its relevance as a central axis of the theoretical construct. These findings confirm that mastering fundamental financial concepts is essential for efficient and informed personal economic management (Engelbrecht, 2014; Gallery et al., 2011).

Regarding Factor F2, which measures perceptions of the socioeconomic impact of financial education, the figure shows high factor loadings, especially for items related to market opportunities, innovation, and entrepreneurship. This configuration highlights the importance individuals attribute to the transformative and social impact of financial education, correlating strongly with the first factor (F1 = 0.85). Consistent with findings from several studies, financial literacy is increasingly recognized as extending beyond the individual dimension, having meaningful implications for economic and social development (Engelbrecht, 2014; Glory et al., 2024; Lusardi and Messy, 2023).

As for latent Factor F3, linked to the everyday practical application of financial knowledge, factor loadings ranged from 0.52 to 0.86, reflecting an adequate level of consistency. This result indicates that, beyond theoretical knowledge, the practical application of financial concepts in daily life constitutes a critical component of financial literacy. Goyal and Kumar (2021) argue that sound financial literacy must be grounded not only in technical knowledge but also in the ability to translate such knowledge into practical, informed, and responsible decisions.

Finally, latent Factor F4, associated with financial self-management, includes elements related to personal income and expenditure control, systematic saving, and long-term financial decision-making. This dimension shows high factor loadings (between 0.66 and 0.85), confirming its robustness and relevance as both an independent and complementary factor within the model. These findings are consistent with previous research, which has demonstrated that effective self-management and strategic planning in personal finances are strong predictors of financial wellbeing (Palmer et al., 2021).

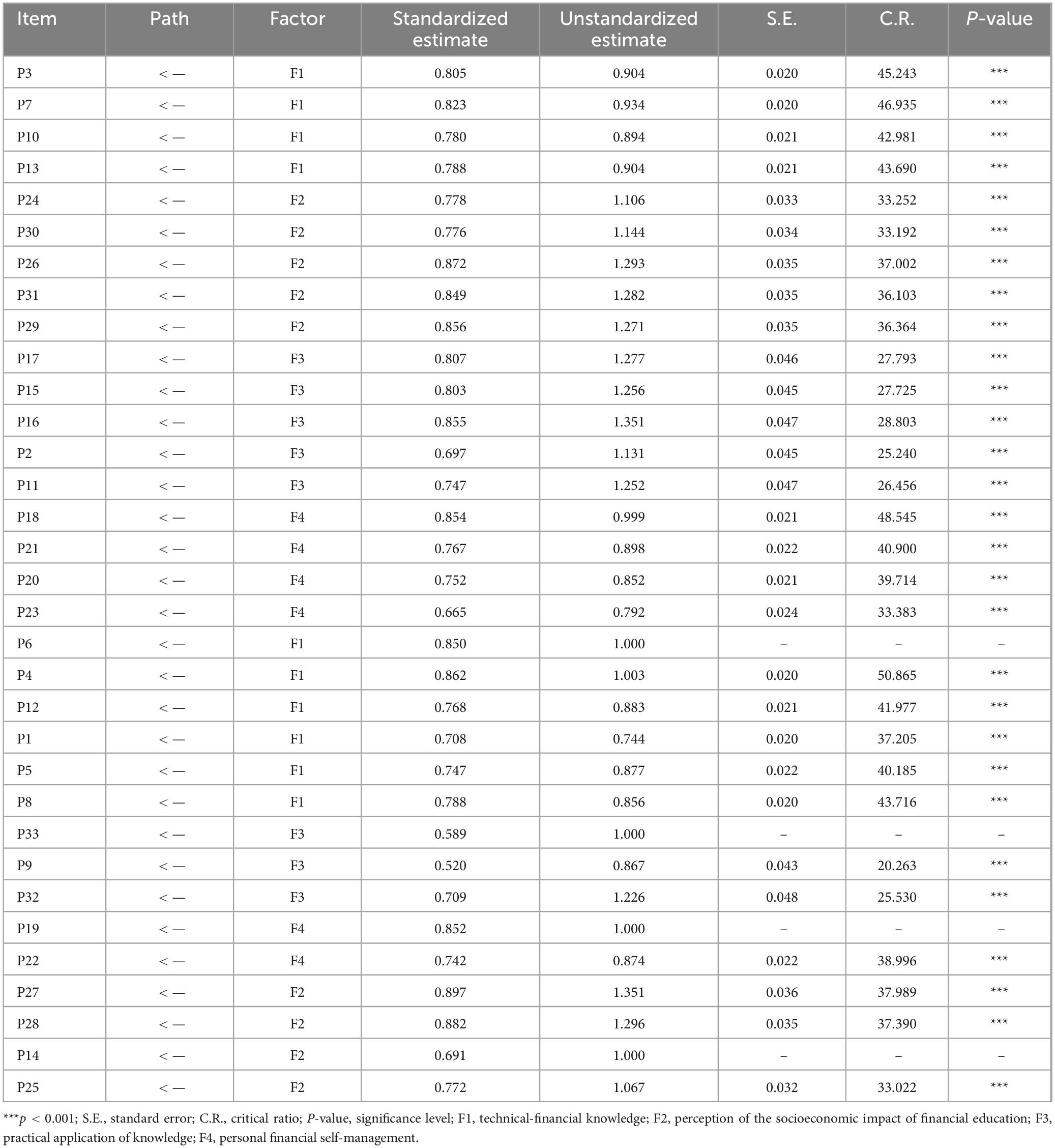

Table 6 below presents the results of the estimated structural model. This table summarizes the relationships between latent factors and their respective indicators, organized by dimension, and reports standardized and unstandardized estimates, standard errors, critical values, and significance levels. Only items with highly significant values (p < 0.001) are included, thereby supporting the robustness of the proposed model.

Table 6. Results of the structural model of financial literacy.

Regarding Factor 1, which represents technical-financial knowledge, all standardized estimates exceeded 0.70, with particularly high values for item P4 (0.862) and item P6 (0.850). These results suggest a strong conceptual loading on this factor, confirming that participants demonstrate a high degree of familiarity with topics such as credit history, interest rates, and financial consumer rights. This finding aligns with the work of Cwynar et al. (2019), who assert that technical knowledge is a central component of financial literacy and a key predictor of healthy financial behaviors.

Factor 2, related to the perception of the socioeconomic impact of financial education, shows even higher standardized loadings, such as P27 (0.897) and P28 (0.882). These results reflect a strong association between this construct and participants’ awareness of the role that financial education plays in processes such as innovation, inequality reduction, and economic development. This empirical evidence is consistent with the findings of Menberu (2024), who argue that a critical and transformative perspective on financial education enhances social participation and informed decision-making.

Regarding Factor 3, focused on the practical application of financial knowledge, loadings range from 0.520 (P9) to 0.855 (P16). Although some items exhibit moderate loadings, such as P33 (0.589), the majority fall within an acceptable range. The relationship between this factor and its indicators reveals that individuals not only possess financial knowledge but also apply it in their daily lives through budgeting, the use of financial products, and financial planning. Stolper and Walter (2017) emphasize that such practical application is essential for translating knowledge into responsible financial behavior, reinforcing the importance of this component within the model.

As for Factor 4, related to financial self-management, high standardized loadings are also reported, notably for P18 (0.854) and P19 (0.852), both of which pertain to income and expense control. These loadings reflect the internalization of personal financial management habits such as planned saving, investment, and debt assessment. Isler et al. (2022) argue that these skills though often underestimated are fundamental for achieving long-term financial stability and wellbeing, and should be actively promoted within educational programs.

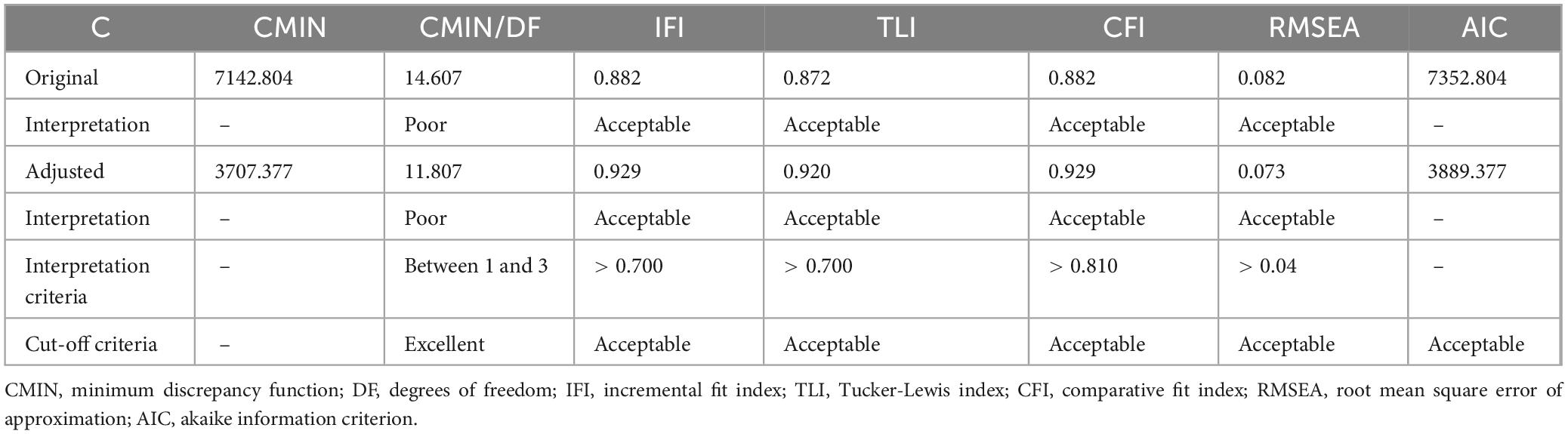

Table 7 below presents a comparison between the original structural model and its adjusted version, based on the main fit indices. This table allows for the evaluation of improvements obtained after the adjustments, considering standard criteria for assessing model acceptability.

Table 7. Fit indices of the original and adjusted structural model of financial literacy.

The results indicate that the original model presented a CMIN value of 7142.804 with a CMIN/DF ratio of 14.607, which far exceeds the recommended threshold of 3. This value suggests a poor model fit. However, the incremental indices (IFI = 0.882; TLI = 0.872; CFI = 0.882) fall within the acceptable range (> 0.80), while the RMSEA = 0.082 is considered adequate, though not optimal. These values suggest that while the initial model had a theoretically solid structure, it required adjustments to improve its empirical fit. This situation is common in models with a large number of indicators, as noted by Hein et al. (2021), who warn that model complexity may negatively affect parsimony without necessarily compromising structural validity.

After making the necessary adjustments, the refined model showed a substantial improvement. The CMIN value decreased to 3707.377, and although the CMIN/DF ratio remained high (11.807), the incremental indices improved: IFI and CFI reached 0.929, while TLI increased to 0.920. Additionally, the RMSEA decreased to 0.073, a value considered acceptable in complex models with large samples. A significant reduction in AIC was also observed (from 7352.804 to 3889.377), indicating improved model efficiency and a higher probability of replicability. In this context, Amare et al. (2024) assert that targeted modifications can optimize model fit without compromising theoretical structure, as long as conceptual coherence is maintained.

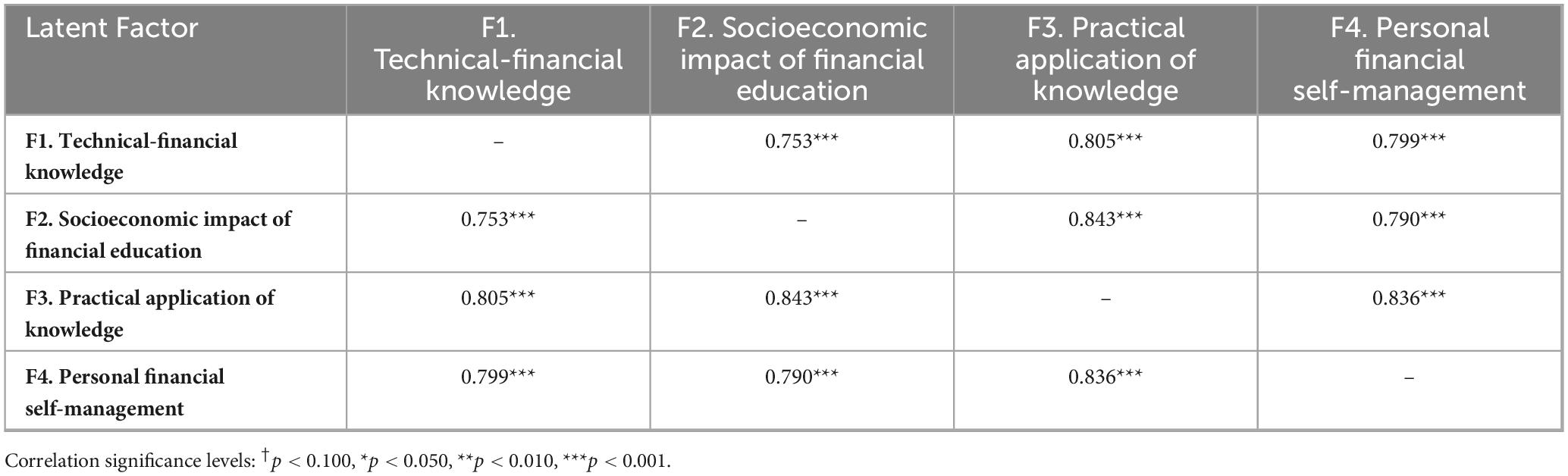

Table 8 presents the correlations among the four latent factors of the financial literacy model: technical-financial knowledge (F1), perception of the socioeconomic impact of financial education (F2), practical application of financial knowledge (F3), and personal financial self-management (F4). All reported correlations are positive, high, and statistically significant, supporting the interdependence of the analyzed dimensions.

Table 8. Correlations among the latent factors of the financial literacy model.

The results show a correlation of 0.753 between F1 and F2, indicating that a higher level of financial knowledge is associated with a stronger perception of the social value of financial education. This relationship suggests that individuals who understand technical concepts are more likely to recognize financial education as a tool for inclusion and transformation. This finding aligns with Marron (2014), who argues that financial literacy not only improves individual resource management but also fosters an economically informed and socially engaged citizenry.

Additionally, the correlation between F1 and F3 was 0.805, revealing that technical financial knowledge is closely linked to its practical application. In other words, those who master fundamental financial concepts tend to implement this knowledge in their everyday decisions. This result is supported by Dao et al. (2024), who assert that financial literacy only yields tangible benefits when it is connected to observable behaviors such as saving, planning, or responsible credit use.

As for the relationship between F2 and F3, the correlation reached 0.843, indicating an even stronger association. This reflects that awareness of the socioeconomic relevance of financial education not only promotes positive attitudes but also encourages functional financial practices. Such a link has been highlighted by Kumar et al. (2023), who point out that a broad and informed view of financial education enhances autonomous and sustainable decision-making, especially among youth and vulnerable populations.

Finally, Factor 4 (financial self-management) showed high correlations with F1 (0.799), F2 (0.790), and F3 (0.836). This confirms that effective management of income, expenses, savings, and investments does not occur in isolation but results from an integrated process involving knowledge, contextual perception, and action. Braßler and Sprenger (2021) agree that the development of financial competencies requires a holistic approach that includes knowledge, skills, attitudes, and values, as only such integration can foster sustainable financial behaviors.

5 Conclusion

The present study aimed to analyze the relationship between educational level and financial literacy, considering that academic training may significantly influence the development of financial competencies. To this end, a structural model was designed to identify the latent dimensions of the construct and empirically evaluate the strength of these relationships. The stated objective was successfully achieved, and the research question was answered based on robust statistical evidence.

The results confirmed that there is a significant difference in financial literacy levels according to the level of education attained. Individuals with higher education presented the highest scores, while the lowest levels corresponded to those with only primary education. Additionally, the structural model revealed four fundamental dimensions: technical-financial knowledge, perception of the social impact of financial education, practical application of knowledge, and financial self-management. The correlations among these factors were high, demonstrating the multidimensional and interrelated nature of the construct.

Regarding the psychometric quality of the instrument, the analyses showed high levels of reliability and validity, which support the relevance of the proposed model. Nevertheless, certain limitations should be acknowledged. The sample was selected through non-probabilistic convenience sampling, which limits the generalizability of the findings. Furthermore, the gender distribution was not fully balanced, which could influence certain response patterns.

As a future direction, it is recommended to include additional contextual variables such as occupation, monthly income, or family environment, which could enrich the analysis. Longitudinal studies are also suggested to observe changes over time and assess the impact of specific training programs on financial literacy. In conclusion, the results provide a solid foundation for future research and constitute a valuable input for the formulation of educational strategies aimed at improving financial literacy across different population sectors.

Data availability statement

The original contributions presented in this study are included in this article/supplementary material, further inquiries can be directed to the corresponding author.

Ethics statement

Written informed consent was obtained from the minor(s)’ legal guardian/next of kin for the publication of any potentially identifiable images or data included in this article.

Author contributions

JB-G: Data curation, Writing – review and editing, Investigation, Writing – original draft, Conceptualization. GC-F: Writing – original draft, Formal Analysis, Writing – review and editing, Investigation, Data curation, Conceptualization. AM-L: Methodology, Writing – original draft, Investigation, Visualization, Data curation, Writing – review and editing. FQ-S: Supervision, Writing – original draft, Writing – review and editing, Investigation, Formal Analysis, Conceptualization, Data curation. AS-G: Visualization, Writing – original draft, Formal Analysis, Resources, Writing – review and editing, Project administration, Data curation, Methodology, Validation, Software. JM-C: Methodology, Writing – original draft, Software, Conceptualization, Investigation, Visualization, Supervision, Writing – review and editing, Validation, Project administration, Formal Analysis.

Funding

The author(s) declare that no financial support was received for the research and/or publication of this article.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Generative AI statement

The authors declare that no Generative AI was used in the creation of this manuscript.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Akbaş, M. Ç, and Seedsman, T. (2024). Financial literacy as part of empowerment education for later life: A spectrum of perspectives, challenges and implications for individuals, educators and policymakers in the modern digital economy. Economics 18, 1–14. doi: 10.1515/econ-2022-0097

Amare, T., Singh, B., Kabeta, G., Jiru, M. G., and Lemu, H. G. (2024). Structural equation modeling of relationships among lean operational, financial performance, and customer satisfaction. Indian J. Sci. Technol. 17, 1606–1620. doi: 10.17485/IJST/v17i15.3016

Braßler, M., and Sprenger, S. (2021). Fostering sustainability knowledge, attitudes, and behaviours through a tutor-supported interdisciplinary course in education for sustainable development. Sustainability 13:3494. doi: 10.3390/su13063494

Brüggen, E. C., Hogreve, J., Holmlund, M., Kabadayi, S., and Löfgren, M. (2017). Financial well-being: A conceptualization and research agenda. J. Bus. Res. 79, 228–237. doi: 10.1016/j.jbusres.2017.03.013

Cebrián, G., and Junyent, M. (2015). Competencies in education for sustainable development: Exploring the student teachers’ views. Sustainability 7, 2768–2786. doi: 10.3390/su7032768

Cwynar, A., Cwynar, W., Baryła-Matejczuk, M., and Betancort, M. (2019). Sustainable debt behaviour and well-being of young adults: The role of parental financial socialisation process. Sustainability 11:7210. doi: 10.3390/su11247210

da Silva Souza Caggy, R. C., Xavier Torreblanca, J., and Siano, C. (2023). Educación y cultura financiera en estudiantes universitarios: Un estudio de caso en una Universidad Privada de Argentina. Rev. Formadores 16, 6–21. doi: 10.25194/rf.v16i2.1732

Dao, D.-H., Pham, D.-H., and Nguyen, N.-D. (2024). Assessment of the factors impacting the financial management skills among university students: The moderating effect of financial education. Pak. J. Life Soc. Sci. 22, 5694–5708. doi: 10.57239/PJLSS-2024-22.1.00420

Engelbrecht, L. (2014). The scope of financial literacy education: A poverty alleviation tool in social work? Soc. Work 44, 252–262. doi: 10.15270/44-3-239

Festa, M. M., and Knotts, K. G. (2021). Self-leadership, financial self-efficacy, and student loan debt. J. Financial Counseling Plann. 32, 242–251. doi: 10.1891/JFCP-18-00054

Gallery, N., Gallery, G., Brown, K., Furneaux, C., and Palm, C. (2011). Financial literacy and pension investment decisions. Financial Accountability Manag. 27, 286–307. doi: 10.1111/j.1468-0408.2011.00526.x

García-Mata, O., and Zerón-Félix, M. (2022). A review of the theoretical foundations of financial well-being. Int. Rev. Econ. 69, 145–176. doi: 10.1007/s12232-022-00389-1

Garg, N., and Singh, S. (2018). Financial literacy among youth. Int. J. Soc. Econ. 45, 173–186. doi: 10.1108/IJSE-11-2016-0303

Gerrans, P., and Heaney, R. (2019). The impact of undergraduate personal finance education on individual financial literacy, attitudes and intentions. Accounting Finance 59, 177–217. doi: 10.1111/acfi.12247

Glory, U., Ndubuisi, L., Ifeyinwa, F., Onyeka, F., Odunayo, A., and Kehinde, F. (2024). Financial literacy and community empowerment: A review of volunteer accounting initiatives in low-income areas. Int. J. Sci. Res. Archive 11, 975–985. doi: 10.30574/ijsra.2024.11.1.0135

Goyal, K., and Kumar, S. (2021). Financial literacy: A systematic review and bibliometric analysis. Int. J. Consumer Stud. 45, 80–105. doi: 10.1111/ijcs.12605

Grohmann, A., Klühs, T., and Menkhoff, L. (2018). Does financial literacy improve financial inclusion? Cross country evidence. World Dev. 111, 84–96. doi: 10.1016/j.worlddev.2018.06.020

Hafeez, F., Ullah Sheikh, U., Mas’ud, A. A., Al-Shammari, S., Hamid, M., and Azhar, A. (2022). Application of the theory of planned behavior in autonomous vehicle-pedestrian interaction. Appl. Sci. 12:2574. doi: 10.3390/app12052574

Hein, G., Gamer, M., Gall, D., Gründahl, M., Domschke, K., Andreatta, M., et al. (2021). Social cognitive factors outweigh negative emotionality in predicting COVID-19 related safety behaviors. Prevent. Med. Rep. 24:101559. doi: 10.1016/j.pmedr.2021.101559

Isler, O., Rojas, A., and Dulleck, U. (2022). Easy to shove, difficult to show: Effect of educative and default nudges on financial self-management. J. Behav. Exp. Finance 34:100639. doi: 10.1016/j.jbef.2022.100639

Johan, I., Rowlingson, K., and Appleyard, L. (2021). The effect of personal finance education on the financial knowledge, attitudes and behaviour of university students in Indonesia. J. Fam. Econ. Issues 42, 351–367. doi: 10.1007/s10834-020-09721-9

Jugnandan, S., and Willows, G. D. (2023). Towards an integrated debiasing framework for consumer financial decisions: A reflection on debiasing research. Int. J. Consum. Stud. 47, 1544–1560. doi: 10.1111/ijcs.12935

Kasoga, P. S., and Tegambwage, A. G. (2024). The effect of attitudes towards money on over-indebtedness among microfinance institutions’ customers in Tanzania. Appl. Res. Quality Life 19, 1365–1384. doi: 10.1007/s11482-024-10294-0

Katnic, I., Katnic, M., Orlandic, M., Radunovic, M., and Mugosa, I. (2024). Understanding the role of financial literacy in enhancing economic stability and resilience in montenegro: A data-driven approach. Sustainability 16:11065. doi: 10.3390/su162411065

Kiesnere, A. L., and Baumgartner, R. J. (2019). Sustainability management in practice: Organizational change for sustainability in smaller large-sized companies in Austria. Sustainability 11:572. doi: 10.3390/su11030572

Kumar, P., Pillai, R., Kumar, N., and Tabash, M. I. (2023). The interplay of skills, digital financial literacy, capability, and autonomy in financial decision making and well-being. Borsa Istanbul Rev. 23, 169–183. doi: 10.1016/j.bir.2022.09.012

Kyeyune, G. N., and Ntayi, J. M. (2025). Empowering rural communities: The role of financial literacy and management in sustainable development. Front. Hum. Dyn. 6:1424126. doi: 10.3389/fhumd.2024.1424126

Lontchi, C. B., Yang, B., and Su, Y. (2022). The mediating effect of financial literacy and the moderating role of social capital in the relationship between financial inclusion and sustainable development in cameroon. Sustainability 14:15093. doi: 10.3390/su142215093

Loza, R., Romaní, G., Castañeda, W., and Arias, G. (2023). Influence of skills and knowledge on the financial attitude of university students. Tec Empresarial 18, 65–83. doi: 10.18845/te.v18i1.7002

Luèiæ, A., Barbiæ, D., and Uzelac, M. (2023). Theoretical underpinnings of consumers’ financial capability research. Int. J. Consum. Stud. 47, 373–399. doi: 10.1111/ijcs.12778

Lusardi, A. (2019). Financial literacy and the need for financial education: Evidence and implications. Swiss J. Econ. Stat. 155:1. doi: 10.1186/s41937-019-0027-5

Lusardi, A., and Messy, F.-A. (2023). The importance of financial literacy and its impact on financial wellbeing. J. Financial Literacy Wellbeing 1, 1–11. doi: 10.1017/flw.2023.8

Lusardi, A., and Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. J. Econ. Literature 52, 5–44. doi: 10.1257/jel.52.1.5

Marron, D. (2014). “Informed, educated and more confident”: Financial capability and the problematization of personal finance consumption. Consumpt. Mark. Cult. 17, 491–511. doi: 10.1080/10253866.2013.849590

Matewos, K. R., Navkiranjit, K. D., and Jasmindeep, K. (2016). Financial literacy for developing countries in Africa: A review of concept, significance and research opportunities. J. African Stud. Dev. 8, 1–12. doi: 10.5897/JASD2015.0331

Mavlutova, I., Fomins, A., Spilbergs, A., Atstaja, D., and Brizga, J. (2021). Opportunities to increase financial well-being by investing in environmental, social and governance with respect to improving financial literacy under COVID-19: The case of latvia. Sustainability 14:339. doi: 10.3390/su14010339

Menberu, A. W. (2024). Technology-mediated financial education in developing countries: A systematic literature review. Cogent Bus. Manag. 11, 2294879–2294229. doi: 10.1080/23311975.2023.2294879

Méndez-Prado, S. M., Chiluiza, K., Everaert, P., and Valcke, M. (2022). Design and evaluation among young adults of a financial literacy scale focused on key financial decisions. Educ. Sci. 12:460. doi: 10.3390/educsci12070460

Méndez-Prado, S. M., Rodriguez, V., Peralta-Rizzo, K., Everaert, P., and Valcke, M. (2023). An assessment tool to identify the financial literacy level of financial education programs participants’ executed by ecuadorian financial institutions. Sustainability 15:996. doi: 10.3390/su15020996

Mieèinskienë, A., Stankevièienë, J., Jurevièienë, D., Taujanskaitë, K., Danilevièienë, I., and Gudelytë-Žilinskienë, L. (2023). The role of financial intelligence quotient and financial literacy for paving a path towards financial well-being. J. Bus. Econ. Manag. 24, 901–922. doi: 10.3846/jbem.2023.20648

Mindra, R., and Moya, M. (2017). Financial self-efficacy: A mediator in advancing financial inclusion. Equality Diversity Inclusion Int. J. 36, 128–149. doi: 10.1108/EDI-05-2016-0040

Moreira-Choez, J. S., Arteaga, K. C. C., Benavides-Lara, R. M., Gutierrez, M. T. V., Herrera, M. K. G., and Lamus, et al. (2023). The synergy between financial education, economic well-being, and financial stress: An analysis of interconnections and reciprocal effects. J. Educ. Soc. Res. 13:283. doi: 10.36941/jesr-2023-0164

Murari, K. (2019). Managing household finance: An assessment of financial knowledge and behaviour of rural households. J. Rural Dev. 38, 705. doi: 10.25175/jrd/2019/v38/i4/150768

Muthu, L. R., and Bharathi, M. A. (2025). “Enhanced human growth through technical financial literacy,” in Resource Management in Advanced Wireless Networks, eds A. Suresh, J. Ramkumar, and M. Baskar (Hoboken, NJ: Wiley), 291–304. doi: 10.1002/9781119827603.ch14

Owuor, E., Shockley, McCarthy, K., and Kagotho, N. (2022). Financial capability and asset building curriculum for social work students in the kenyan technical and vocational training education system. Glob. Soc. Welfare 10, 71–82. doi: 10.1007/s40609-022-00240-z

Palmer, L., Richardson, E. W., Goetz, J., Futris, T. G., Gale, J., and DeMeester, K. (2021). Financial self-efficacy: Mediating the association between self-regulation and financial management behaviors. J. Financial Counseling Plann. 32, 535–549. doi: 10.1891/JFCP-19-00092

Pang, M. F. (2010). Boosting financial literacy: Benefits from learning study. Instructional Sci. 38, 659–677. doi: 10.1007/s11251-009-9094-9

Rehman, K., and Mia, M. A. (2024). Determinants of financial literacy: A systematic review and future research directions. Future Bus. J. 10:75. doi: 10.1186/s43093-024-00365-x

Resham, I., Muhammad, A., Shamim, A., and Stephanie, E. (2024). Empowering sustainable development: The role of financial literacy and social capital in bridging financial inclusion in developing nations. J. Innov. Res. Manag. Sci. 5, 61–80. doi: 10.62270/jirms.v5i2.79

Rodriguez, J. M., Rodriguez, G. A., and Palallos, L. (2024). The financial planning activities of grade-12 students on their financial management in PCU: Basis for creating a financial management plan. Int. J. Res. Publications 153:10.47119. doi: 10.47119/IJRP1001531720247007

Siegfried, C., and Wuttke, E. (2021). What influences the financial literacy of young adults? A combined analysis of socio-demographic characteristics and delay of gratification. Front. Psychol. 12:663254. doi: 10.3389/fpsyg.2021.663254

Silva, T. P., Magro, C. B. D., Gorla, M. C., and Nakamura, W. T. (2017). Financial education level of high school students and its economic reflections. Rev. Adm. 52, 285–303. doi: 10.1016/j.rausp.2016.12.010

Stolper, O. A., and Walter, A. (2017). Financial literacy, financial advice, and financial behavior. J. Bus. Econ. 87, 581–643. doi: 10.1007/s11573-017-0853-9

Tulcanaza-Prieto, A. B., Cortez-Ordoñez, A., Rivera, J., and Lee, C. W. (2025). Is digital literacy a moderator variable in the relationship between financial literacy, financial inclusion, and financial well-being in the ecuadorian context? Sustainability 17:2476. doi: 10.3390/su17062476

Keywords: financial literacy, educational level, educational assessment, consumer behavior, economic culture, higher education, socioeconomic factors, financial decision-making

Citation: Bastidas-Guerrón JL, Cárdenas-Fierro GM, Mora-Lucero AC, Quinde-Sari FR, Sabando-García AR and Moreira-Choez JS (2025) Financial literacy and educational level in Ecuadorian students: a structural analysis. Front. Educ. 10:1596635. doi: 10.3389/feduc.2025.1596635

Received: 19 March 2025; Accepted: 14 April 2025;

Published: 09 May 2025.

Edited by:

Abubaker Qutieshat, Oman Dental College, OmanReviewed by:

Gavin Revie, Bezalel Education, United KingdomMaryam Al Riyami, Oman Dental College, Oman

Copyright © 2025 Bastidas-Guerrón, Cárdenas-Fierro, Mora-Lucero, Quinde-Sari, Sabando-García and Moreira-Choez. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Jenniffer Sobeida Moreira-Choez, amVubmlmZmVyLm1vcmVpcmFAdXRtLmVkdS5lYw==