Maike Keil

Maike Keil Anna Rohowsky

Anna Rohowsky Julia Offermann

Julia Offermann Martina Ziefle

Martina Ziefle Katrin Arning

Katrin Arning- 1Risk Perception and Communication, RWTH Aachen University, Aachen, Germany

- 2Communication Science, RWTH Aachen University, Aachen, Germany

Introduction: As integral societal actors, companies must engage in corporate sustainability to address climate change and remain competitive. While many factors influencing corporate sustainability have been identified, little research has analyzed them jointly.

Methods: Therefore, this study surveyed corporate sustainability leaders in a mixed-methods approach, utilizing semi-structured interviews (N = 25) and an online survey (N = 108) to assess organizational and individual, leader-related drivers.

Results and discussion: Qualitative results highlighted the importance of leadership in sustainability decisions. Quantitative results showed that perceived corporate sustainability correlated with individual factors (e.g., leaders' environmental behavior), while practical sustainability, measured by the Corporate Sustainability Index, was linked to organizational factors (e.g., company size). Hierarchical multiple regression quantified the relative impact of factors and confirmed leaders' environmental citizenship behavior, company size, and annual revenue as key sustainability predictors. The findings provide valuable guidance for organizations and policymakers to support corporate sustainability transformation by empowering sustainability leaders and smaller organizations.

1 Introduction

Sustainability in all its dimensions—social, ecological, and economic—plays an increasingly significant role in shaping corporate practices (Gawusu et al., 2022). Accordingly, companies are expected to contribute to a sustainable future by implementing changes at multiple levels, from operational processes to strategic decision-making (Meza-Ruiz et al., 2017). While responsibility for these efforts often lies with management, employee engagement is also a key driver for successful implementation (Reilly and Larya, 2018; Orazalin, 2020).

Despite its importance within corporate structures and the substantial increase in scholarly debate over the past two decades, there is no standardized definition of corporate sustainability. While the concept's origin is mainly linked to the Brundtland Report's definition of sustainable development as “development that meets the needs of the present without compromising the ability of future generations to meet their own needs” (Oxford University Press, 1987), scientific perspectives differ regarding its operationalization. Some studies conceptualize corporate sustainability as a three-dimensional construct encompassing social, ecological, and economic dimensions, while others focus primarily on environmental aspects (Montiel and Delgado-Ceballos, 2014; Meuer et al., 2020). This emphasis on the environmental dimension reflects companies' frequent prioritization of environmental sustainability, given its crucial role in combating climate change (Santos, 2011), and their focus on energy efficiency to reduce both carbon emissions and operational costs. The German government's “Efficiency First” approach highlights the importance of energy efficiency as a cost-effective and impactful solution for combating climate change. Companies are encouraged to leverage funding programs and invest in sustainability initiatives to achieve the target of a 30% reduction in primary energy consumption by 2030, relative to 2008 levels (BMWi, 2019). However, such technical measures often overlook broader organizational and individual factors that influence sustainability.

Corporate sustainability is inherently complex, shaped by the interplay of internal organizational factors, individual drivers, and external market-related barriers and enablers (Lozano, 2015). This complexity is further increased by the nature of sustainability research, which spans multiple disciplines but lacks a unified theoretical framework (e.g., Clark and Harley, 2020). Various theoretical perspectives have been employed to conceptualize and explain corporate sustainability. Early research predominantly emphasized the role of external pressures. For instance, institutional theory posits that companies adopt sustainability practices primarily to gain legitimacy by conforming to prevailing social norms, cultural expectations, and regulatory frameworks (Scott, 1992; Jennings and Zandbergen, 1995). In contrast, stakeholder theory (Freeman, 1984) highlights how external pressures arise from specific stakeholder groups—such as customers, investors, and local communities—whose interests managers must consider when formulating corporate strategies toward sustainability (see Montiel and Delgado-Ceballos, 2014 for a Review). Further research has examined how external pressures interact with internal organizational factors to shape corporate environmental strategies. For instance, Delmas and Toffel (2004) have shown that elements such as organizational structure and prior environmental performance moderate how managers perceive and respond to these pressures. Individual-level factors also play a crucial role; for instance, managerial interpretations of environmental issues—as either threats or opportunities—significantly influence the choice of environmental strategy. These individual interpretations, in turn, are shaped by organizational characteristics, including the degree to which environmental issues are legitimized within the firm and the extent of discretionary slack available to managers. However, these earlier theories largely overlooked the integration of psychological factors—such as attitudes and behaviors—which subsequently became a central focus in research on the drivers of corporate sustainability (see Section 2.1).

Although empirical research highlights the complexity of sustainability factors, it often examines them in isolation—focusing solely on organizational or individual factors (e.g., Candrianto et al., 2023). Further, significant shortcomings persist in studies attempting to examine corporate sustainability drivers holistically. Avota et al. (2015) provided a theoretical framework but lacked empirical validation. Lozano qualitatively identified various influencing factors, but later analyses revealed methodological shortcomings in quantifying and linking them directly to a corporate sustainability indicator (Lozano, 2015; Lozano and Von Haartman, 2018).

Moreover, understanding corporate sustainability requires both analyzing measurable outcomes and subjective perceptions. While metrics like carbon footprint reductions are important for evaluating sustainability efforts, perceptions of corporate sustainability reflect how these strategies are implemented and perceived within organizations. Specifically, the perceived relative importance of corporate sustainability shapes the organizational cognitive frame, influencing how managers interpret sustainability issues and develop corresponding organizational capabilities (Grewatsch and Kleindienst, 2018). Further, perceptions of corporate sustainability—i.e., how employees subjectively understand and evaluate a company's green work climate or green shared vision—play a role in shaping pro-environmental behaviors and, consequently, the implementation and success of these strategies (Norton et al., 2014; Latif et al., 2022). Thus, these perceptions shape not only individual behavior but also collective organizational dynamics such as employee commitment, stakeholder trust, and organizational success (e.g., Farooq et al., 2014). By integrating perceptions of organizational sustainability efforts, organizations can better understand the drivers of employee engagement as well as potential barriers to sustainability strategy implementation. However, the way organizational members perceive sustainability and its relevance does not necessarily align with how sustainability measures are implemented in practice, as individual sensemaking may be constrained or overridden by the organization's profit orientation. Hahn and Aragón-Correa (2015) describe this disconnect and emphasize the need to consider both individual- and organizational-level factors when investigating corporate sustainability.

Therefore, this study empirically examines how individual and organizational factors jointly influence corporate sustainability. Specifically, it adopts an internal perspective, analyzing how organizational context-related factors, as well as the attitudes and behaviors of leaders, shape both the perceived relevance of corporate sustainability and its implementation. Given the lack of a unified theoretical framework, it offers an exploratory overview of relevant drivers and quantifies their importance—laying a foundation for future research and offering practical insights for organizations and policymakers.

2 Literature review of corporate sustainability drivers

2.1 Individual-psychological corporate sustainability drivers

Corporate sustainability is driven by employees and managers acting as “change agents” through pro-environmental behavior, yet the psychological drivers of these behaviors are largely unexplored (Biswas et al., 2022; Schaltegger et al., 2024). Although managers have the power to implement sustainability measures (Schaltegger et al., 2024), most research focuses on employees' pro-environmental behaviors and the influence of leadership styles (e.g., Robertson and Carleton, 2018). Research on psychological factors behind employee pro-environmental behavior rarely examines their direct impact on corporate sustainability (Norton et al., 2015).

Environmental attitudes and values shape employees' green behavior and, in turn, corporate sustainability (Norton et al., 2015; Zientara and Zamojska, 2018). (Bhattacharyya and Biswas 2021) showed that the pro-environmental behavior of MBA students as potential future leaders was influenced by their environmental values, attitudes, and norms. Papagiannakis et al. (2014) found that managers' environmental values and attitudes drive the implementation of environmental strategies. These findings underscore the importance of pro-environmental values, beliefs, and norms—defined in this study as “eco-consciousness”—in driving corporate sustainability.

Innovation also plays a key role in sustainability, as environmental innovations reduce environmental footprints and tackle ecological challenges like hazardous substance usage. Since innovation stems from employees' creativity, fostering it is essential for cultivating sustainable organizations (Ramus, 2001; Kao et al., 2021). However, little is known about how managers' innovativeness impacts corporate sustainability. Neessen et al. (2021) link environmental citizenship behavior and intrapreneurship as forms of voluntary innovative behavior.

Managers' environmental awareness is another key factor influencing corporate sustainability. Environmentally aware managers prioritize eco-friendly innovations and green investments (Cao and Chen, 2019; Candrianto et al., 2023). Nevertheless, the impact of managers' environmental awareness remains understudied, and the concept lacks a consistent definition. Candrianto et al. (2023) describe it as a multifaceted construct involving environmental knowledge, affective attitudes, and behavioral intentions to address environmental issues, while Cao and Chen (2019) measured the importance that top management attaches to environmentalism. In this study, environmental sustainability awareness is defined as the individual's cognitive (knowledge) and affective (interest) awareness of corporate sustainability behaviors and their perceived importance for addressing climate issues. Additionally, we distinguish between energy efficiency awareness and sustainability awareness. Notably, energy efficiency awareness has been identified as a key influencing factor on a company's energy consumption patterns and plays a crucial role in shaping their energy culture, which is an essential component of corporate sustainability (Oksman et al., 2021). Analogously, energy efficiency awareness is defined as an individual's cognitive and affective awareness of corporate energy efficiency behaviors and their assessment of climate change impact.

Locus of Control (LoC) is another personality trait linked to pro-environmental behavior, reflecting perceived control over environmental outcomes (Fielding and Head, 2012). Rotter (1966) defines an internal LoC as the belief that one's actions determine outcomes, while an external LoC attributes outcomes to chance or powerful others. In small and medium-sized enterprises (SMEs), managers with internal LoC were more involved in environmental initiatives, believing they could make a positive impact (Williams and Schaefer, 2013).

Employee green behavior and its antecedents have been well-researched and are considered crucial for corporate sustainability. One approach to measuring green behavior is through Organizational Citizenship Behavior for the Environment (OCBE), voluntary pro-environmental behaviors that support environmental management without formal recognition (Boiral, 2009). However, research on OCBE's direct impact on green organizational performance is limited. While (Luu 2020) and Chang et al. (2019) found positive links between OCBE, corporate sustainability performance, and green product development, Keil et al. (2025) reported no such correlation between OCBE and corporate sustainability. However, their small subsample of 14 leaders showed higher OCBE levels and a significant positive correlation with corporate sustainability, unlike employees' OCBE.

In summary, while various individual drivers of corporate sustainability have been identified, there is still a lack of empirical research linking them to corporate sustainability measured as a multi-criteria construct—rather than relying on narrow indicators like green product management (Candrianto et al., 2023) or green innovation strategy (Cao and Chen, 2019). Moreover, there is a lack of empirical studies focusing on leadership samples to examine how leaders' individual attitudes are related to corporate sustainability (Keil et al., 2025).

2.2 Organizational-contextual drivers

Company size, operationalized either by workforce size or revenue, is positively associated with sustainability practices (e.g., Gallo and Christensen, 2011; Hörisch et al., 2015). Smaller firms face more challenges due to limited financial and human resources and lower public pressure (Uhlaner et al., 2012; Hörisch et al., 2015). Conway (2015) adds that SMEs often judge low-carbon activities as irrelevant to their business operations. In contrast, large firms benefit from greater financial resources (Baah et al., 2021) and technological capabilities (Skordoulis et al., 2020), enabling them to integrate sustainability into core operations, resulting in reduced environmental footprints, improved resource efficiency, and stronger financial performance. By leveraging their scale, these firms can implement advanced supply chain practices, foster innovation in sustainable technologies, and gain competitive advantages in sustainability-oriented markets (e.g., Hermundsdottir and Aspelund, 2022).

Company size and energy consumption showed positive associations with the implementation of energy efficiency in corporate strategies. Large firms can invest in advanced energy management technologies and adopt best practices like real-time energy monitoring systems, renewable energy sources, and energy audits to identify inefficiencies (e.g., Schubert et al., 2021). High-consumption firms are more motivated to cut costs, meet regulations, and respond to stakeholder expectations (Neri et al., 2021; Seroka-Stolka and Fijorek, 2022). These firms are also more likely to implement ISO EN 5000-compliant energy management systems (Löbbe et al., 2019).

Reinvestment of savings from sustainability measures is a critical yet underexplored aspect of corporate sustainability. Sustainable investing is recognized for improving sustainability performance, generating economic benefits (Staub-Bisang, 2015), meeting stakeholder expectations, and supporting market leadership (Esty and Cort, 2020). However, the role of sustainable reinvestment as a driver of corporate sustainability has not been directly studied. The importance of reinvestments becomes evident in research on rebound effects following energy efficiency measures. Sustainable investments do not automatically lead to positive environmental outcomes. For instance, energy efficiency improvements and resulting cost savings can paradoxically lead to increased production or expansion, ultimately raising overall energy demand (Santarius, 2016).

Another relevant factor is the landlord/tenant dilemma, where landlords lack incentives to invest in energy-efficient refurbishments, having no direct benefit from energy cost savings, while tenants hesitate due to short-term occupancy or potential restrictions imposed by lease agreements (Ástmarsson et al., 2013). This issue also affects small industrial firms in Germany, which are less likely to implement energy efficiency measures when renting their premises (Schleich, 2009).

Summarizing so far, corporate sustainability is shaped by a complex interplay of organizational, context-related, and individual-psychological factors. This leads to key research questions: How do organizational and individual factors jointly influence sustainability practices? Which factors play a significant role in explaining corporate sustainability? The next section outlines the mixed-methods approach to analyze the complex dynamics of sustainability adoption.

3 Materials and methods—Qualitative pre-study

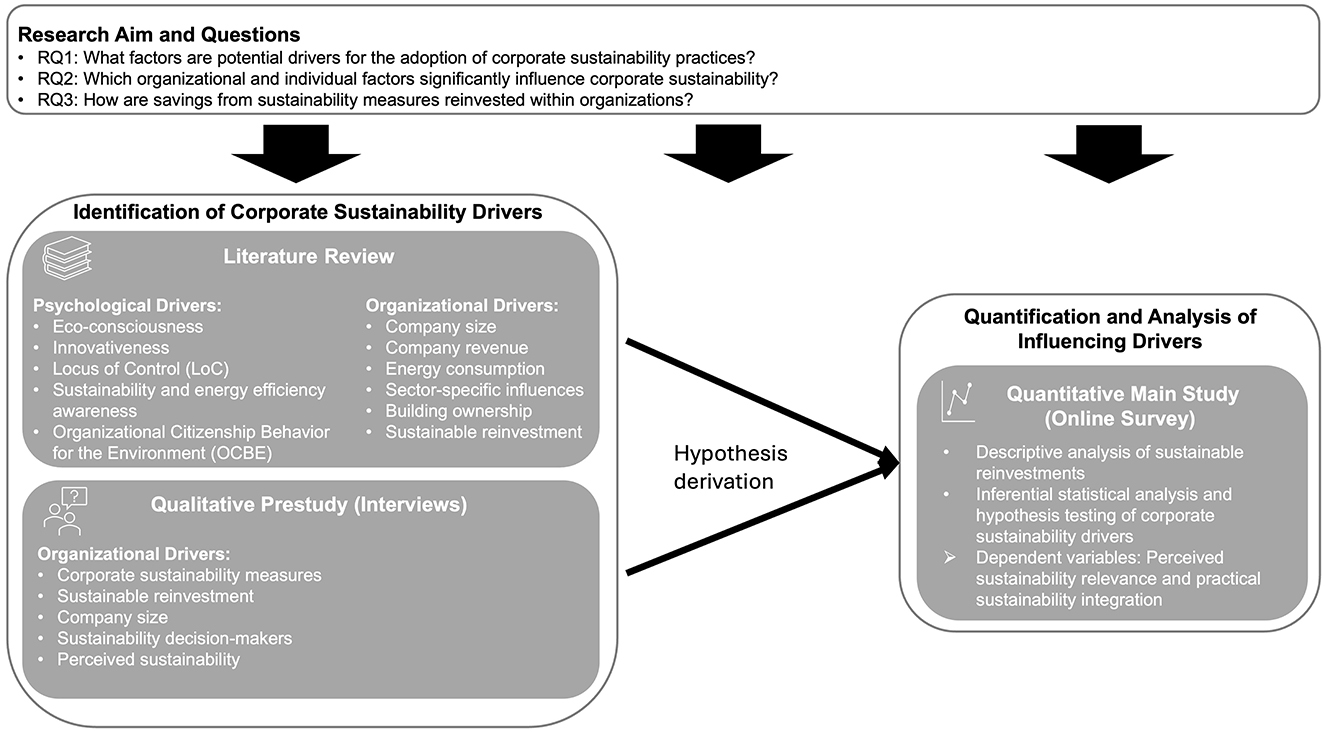

To investigate corporate sustainability drivers, we applied a two-step mixed-methods empirical approach, combining qualitative depth with quantitative generalizability (Creswell and Clark, 2017). First, we conducted a qualitative interview study and literature review to explore and select key drivers of corporate sustainability in German companies. Based on these findings, we formulated hypotheses and analyzed the identified individual-psychological and organizational-contextual drivers through an online survey. Figure 1 illustrates the empirical approach of our study.

Figure 1. Empirical approach for the identification and quantification of corporate sustainability drivers.

This study investigated three key research questions to deepen our understanding of the dynamics influencing corporate sustainability:

• RQ1: What factors are potential drivers for the adoption of corporate sustainability practices?

This question seeks to identify the key factors—psychological and organizational—that drive companies to adopt sustainable practices.

• RQ2: Which organizational and individual factors significantly influence corporate sustainability?

This question seeks to analyze the interplay between organizational and individual factors in shaping the implementation of sustainability measures within companies.

• RQ3: How are savings from sustainability measures reinvested within organizations?

Focusing on the financial dimension of sustainability, this question explores how companies utilize the savings generated from initiatives such as energy-saving measures, contributing to long-term organizational and environmental benefits.

3.1 Qualitative interview study

First, we conducted a qualitative exploration of the current state of corporate sustainability in German companies, focusing on the environmental dimension. This focus was chosen due to its central relevance in corporate sustainability (Santos, 2011) and the respondents' understanding of sustainability, which focused almost exclusively on environmental sustainability, e.g., explicit pro-environmental measures. Semi-structured interviews were conducted with participants from various sectors, company sizes, and roles (Cropley, 2022), aiming to explore the status quo of sustainability practices in companies and to identify factors relevant to a successful implementation of sustainability strategies. The interviews were conducted between November 2022 and February 2023.

The interview guide consisted of four parts, beginning with an introduction to the topic, and questions on demographic information (e.g., age, gender), and company-related information (e.g., company size, position within the company). The second part focused on the company's sustainability strategy, its integration into the overall corporate concept, and specific measures implemented, where applicable.

The third part addressed responsibilities and decision-making processes related to sustainability efforts. The final part explored reinvestments, including resources, targets, and how savings (e.g., time, money) are allocated and monitored.

3.2 Qualitative content analysis

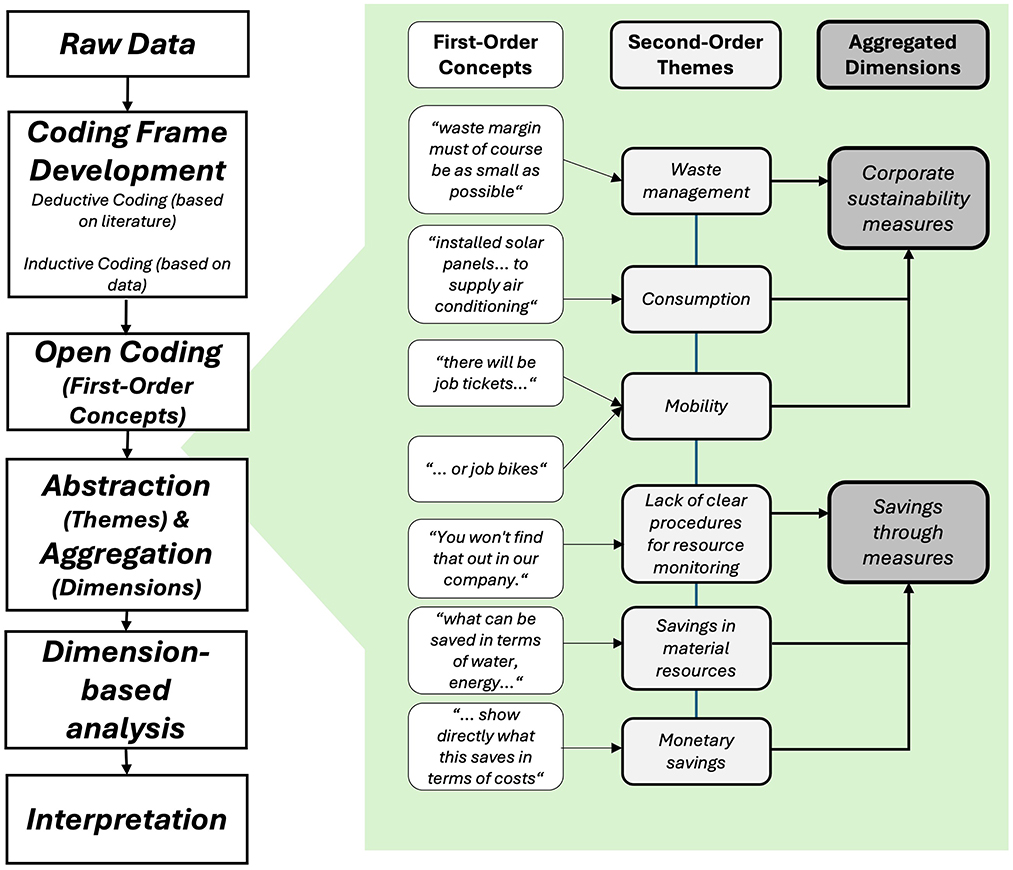

Participants provided informed consent, and all interviews were recorded and transcribed verbatim, ensuring both accuracy and readability, using MAXQDA 2018. A qualitative content analysis according to Mayring (2022) was conducted, chosen for its ability to integrate deductive and inductive categorization within a transparent, replicable framework. Initially, a deductive category system was developed based on the interview guide and prior literature. Subsequently, data were fine-coded inductively, allowing for the refinement and extension of categories where new insights emerged (Ruin, 2017). Coding reliability was ensured through iterative comparison and contextual validation, with multiple category assignments applied where conceptually appropriate. This process enabled a structured yet flexible analysis that contributed to theoretical advancement. The procedure of coding and aggregation of contents is presented in Figure 2.

Figure 2. Exemplary procedure of coding and aggregation adapted from Gioia et al. (2013).

3.3 Characteristics of the interview participants

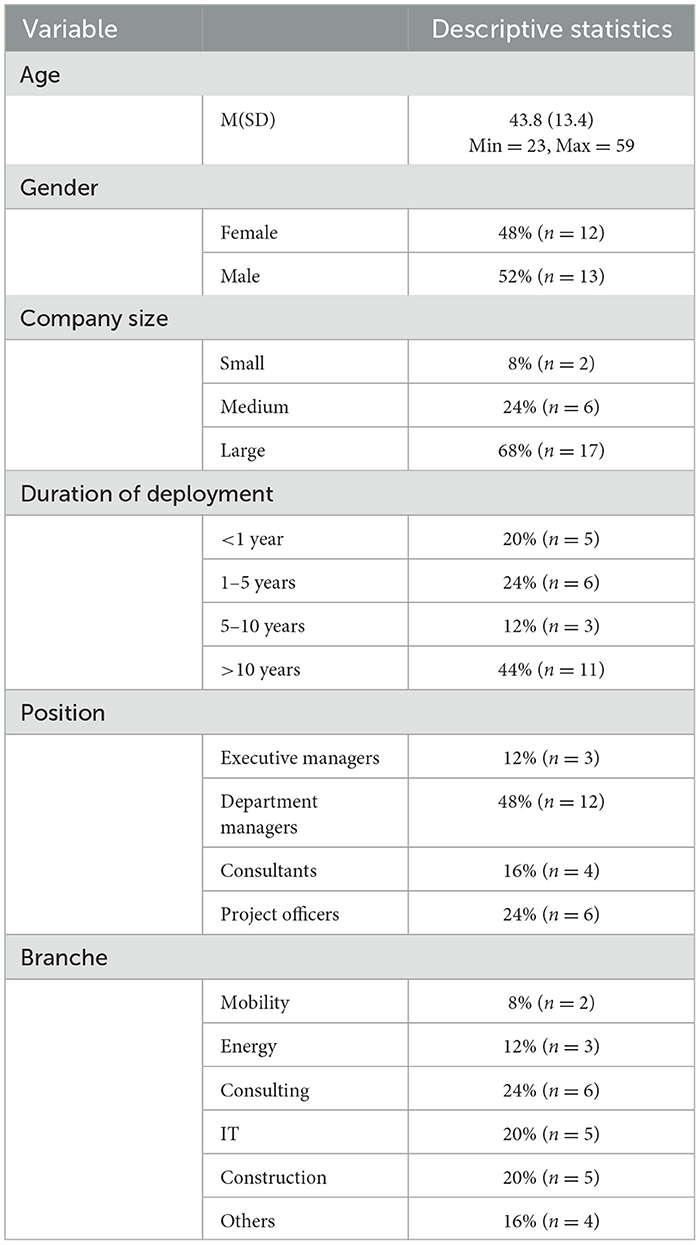

The descriptive statistics referring to the interviewed participants are presented in Table 1. Overall, N = 25 participants (age range: 23–59 years) took part in the interview, evenly split between genders (12 female, 13 male). Most participants worked in companies located in North Rhine-Westphalia in Germany. According to the German Federal Statistical Office, companies are classified as small (up to 49 employees), medium-sized (50–249 employees), and large (more than 250 employees). Most of the participants worked in large companies (n = 17), and fewer in medium-sized (n = 6) or small companies (n = 2). Professional expertise and lengths of stay in the company varied between 3 months to 20 years. Participants came from various industry branches (mobility, energy, consulting, IT, construction) and worked in different positions (executive managers, department managers, consultants, or project officers). All participants reported a high interest in sustainability. Interviews lasted between 30 and 90 minutes.

Table 1. Description of interviewed participants.

4 Results of the qualitative pre-study

4.1 Corporate sustainability measures and sustainable reinvestments

Various corporate sustainability measures were reported to be implemented within the companies, which fall into three main categories: waste management, consumption, and mobility. The category of waste management refers primarily to the separation of waste into plastic, paper, organic, and residual waste, as well as the prevention of waste in production and in general. Pollutant filtration, for example, of water from production, was also classified in this category.

“Of course, you also try to reduce waste and what is necessary for the product always needs a certain margin so that it can be processed and this waste margin must of course be as small as possible.” (Business Development Manager Display, 56)

The second main category on consumption includes measures to reduce resource consumption or sourcing renewable resources, primarily electricity and heating energy. In the area of electricity, respondents stated that they had integrated monitoring systems to accurately track consumption and identify savings. They also eliminated standby modes and reduced the number of monitors in use. Regarding the power source, some respondents reported generating their own electricity from photovoltaic systems on their company roofs.

“For example, they have installed solar panels on the entire roof and, in this sense, they also want to supply the air conditioning in the building with their own electricity, for example.” (Sourcing Site Leader, 59)

Other companies switched their contracts to green electricity.

The third category relates to measures around mobility. Companies frequently provided their employees with job tickets and rail passes for public transport and bicycle leasing opportunities. With regard to business trips, the respondents stated that the vehicle fleets would increasingly consist of e-cars. Some companies also provide their employees with charging stations for their own e-cars. In addition, air travel and car journeys are increasingly replaced by public transport.

“There are no company cars, explicitly, nor will there be. Instead, there will be job tickets. Or job bikes.” (Head of technical operations, 31)

Through the analysis, other overarching categories were identified, but these were given less importance in the interviews than the three previously mentioned. For example, the interviewees stated that sustainability aspects were also taken into account when procuring resources. Care was also taken to ensure that electronic equipment was purchased second-hand rather than new. Respondents also emphasized the importance of material origin, tracing supply chains, and considering the country and region of manufacture (where possible) to reduce transport distances.

Further, respondents were asked whether they knew if the implementation of sustainability measures would result in savings. Most respondents stated that they did not know whether savings would be made. Some reported a lack of clear procedures for resource monitoring. Respondents from companies with monitoring systems reported savings in material resources and monetary savings.

“What we can show if you use different materials; what can be saved in terms of water, energy or other areas that are important for production. That you have less glue, whatever. You can show directly what this saves in terms of costs. What it also saves for the environment.” (Business Development Manager Display, 56)

However, both flew seamlessly into the budget and were used for various other investments or further production.

The reasons for implementing certain sustainability measures varied depending on company size. For small and medium-sized companies (< 249 employees), economic efficiency was the primary concern, as they were focused on ensuring the implemented measures provided an economic advantage without disrupting existing processes. In contrast, for large companies (>249 employees), while the proportion of costs and benefits remained important, idealism was an additional strong driver for implementing sustainability measures. Decision-makers in these companies were motivated by a genuine belief in the importance of contributing to sustainability.

4.2 Sustainability decision-makers and participation

Interviewees reported that the decision to implement a sustainability measure within the company was made by management. Few companies have departments dedicated to sustainability issues staffed by experts. However, in most of the companies surveyed, employees can also participate in the decision-making process. Voluntary employee initiatives independent of company structures discuss sustainability issues and approach the management with suggestions.

“Anyone can contribute ideas, of course. So, if you say there's a company that does the following and that would be interesting for us as a partner or as an investment, then of course you can bring it up. There are also meetings every two weeks, for example, ‘[company] goes sustainable'.” (Consultant, 26)

In some of the companies surveyed, there are also guided working groups initiated by the person responsible within the company. Either selected employees get together or the entire workforce can get involved.

To encourage employee participation, respondents said that companies also provided incentives to get involved. This could take the form of prizes in the form of gift packs or a sum of money to be invested in the specific idea proposed.

The company size appears to influence the nature of sustainability engagement. Respondents from small and medium-sized companies reported a high level of employee involvement in sustainability issues through working groups, without dedicated sustainability positions. In contrast, some large companies have sustainability departments or internal consultants and offer incentives for idea submission.

4.3 Perceived sustainability

The respondents were also asked about their perception of the implementation of sustainability measures in their company. Many respondents stated that they could not recognize in their daily work whether the company acted sustainably. The demands of daily business were so engaging that there was no time to address sustainability issues.

“In my daily work, no, I don't really notice it. As I said, when impulses arise, you try to bring them to the fore or pass them on. But of course, you're always confronted with the practical side of things, primarily a schedule or resources.” (Sourcing Site Leader, 59)

Respondents whose work was directly related to sustainability stated that they felt sustainable through their tasks. Through everyday measures, such as waste separation, the companies' sustainability efforts were visible to all respondents, at least to some extent. All respondents emphasized the extreme importance of sustainability, indicating a strong perceived relevance. One even said that it would be “negligent not to deal with it” (Project officer, 32). Particularly in the corporate context, respondents saw a significant impact of sustainability measures on the environment, attributing this to the company's size, i.e., the number of employees, who could be inspired to adopt sustainability practices.

“Companies, especially large companies with many employees, are big consumers. This means that they have more opportunities to exert influence than an individual.” (Facility Manager, 52)

4.4 Conclusion of qualitative pre-study

Overall, the qualitative pre-study found that the surveyed companies mainly invest in visible sustainability measures, such as mobility and waste management. Employees are aware of these day-to-day measures but generally lack time to engage with the topic further. Nevertheless, employee participation plays a major role in implementing sustainability ideas, especially in large companies. However, the final decision lies with the management.

5 Materials and methods—Quantitative main study

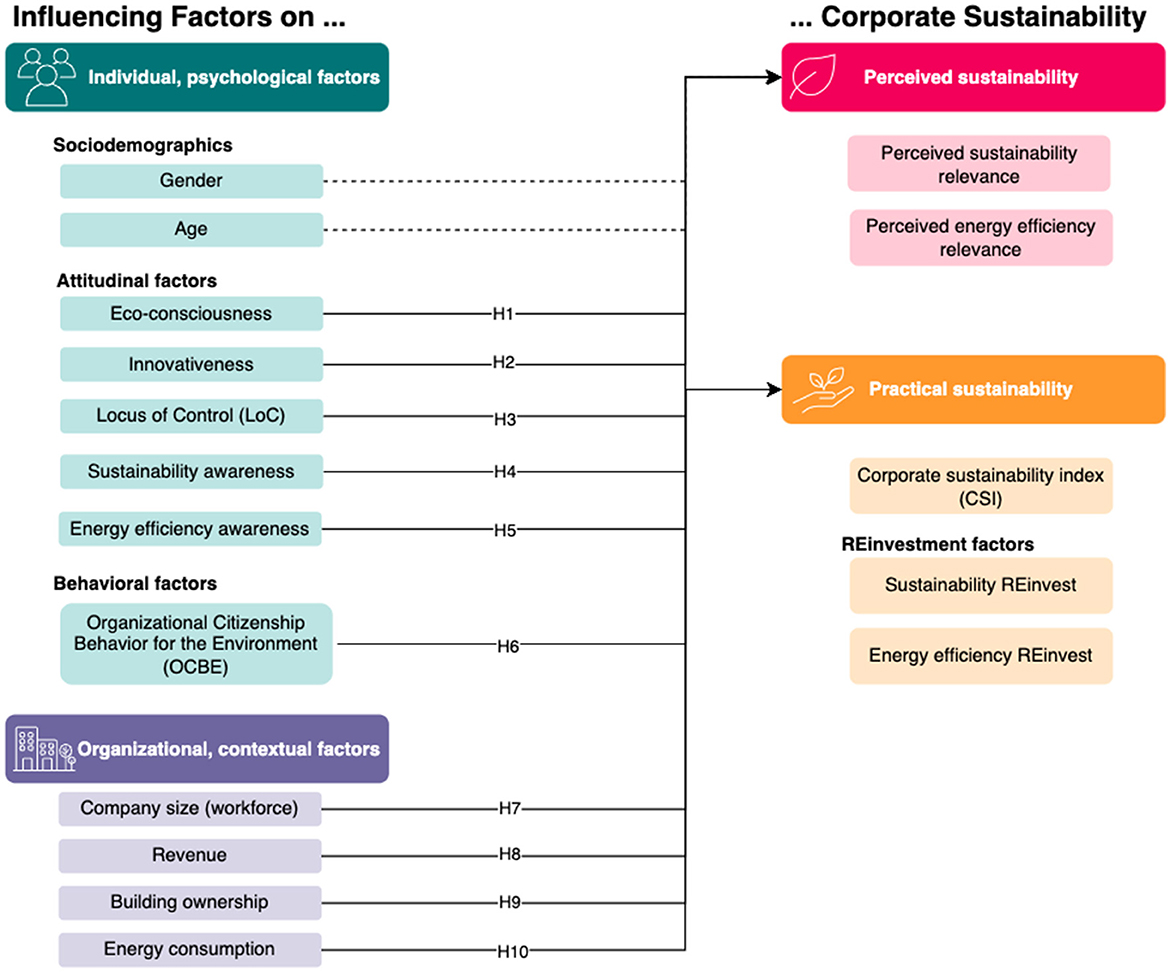

Building on the findings of the qualitative study, the subsequent step involved quantifying the identified sustainability measures and analyzing potential explanatory and influencing factors. The quantitative analysis focused on managers as key decision-makers regarding sustainability within companies, a role highlighted by both the existing literature and our qualitative pre-study. To assess corporate sustainability, we distinguish between perceived sustainability, reflecting a company's ideological commitment to sustainability, and practical sustainability, representing the tangible sustainability measures and policies implemented. This distinction is intended to address the disconnect described in the literature, whereby sustainability issues are widely recognized as relevant within companies, yet are not implemented in a manner that reflects their perceived importance (Hahn and Aragón-Correa, 2015). The following section will detail both constructs and their underlying variables. Figure 3 provides an overview of the analyzed influencing factors and the underlying hypotheses for the statistical analysis.

Figure 3. Analyzed factors and underlying hypotheses of the statistical analysis.

The sociodemographic variables age and gender were employed as control variables in the subsequent hierarchical regression. The selection of attitudinal, behavioral, and organizational-contextual factors was informed by their relevance in the reviewed literature and the qualitative interview pre-study. For individual-level factors, we focused on those identified as particularly salient leader characteristics. The final set of factors was validated through discussions within the interdisciplinary research team of the overarching ENRI project (ENRI–Decision Factors for Sustainable Reinvestments in Companies). Given that the qualitative pre-study indicated that reinvestments in sustainability and energy efficiency are rarely measurable due to insufficient monitoring, the two reinvestment factors will be examined descriptively. Consequently, the hypothesis testing of the relationship between individual and organizational variables will focus on the Corporate Sustainability Index (CSI) as the target variable for practical sustainability. A detailed explanation of the construction of this variable is provided in the statistical analysis section.

5.1 Quantitative survey structure and variables

To investigate the relationships between individual, organizational, and corporate sustainability factors, we conducted a quantitative online study using Qualtrics software (Version June 2023; © 2023 Qualtrics, Provo, UT). All measurement constructs and items were sourced from either validated scales found in the literature or our interview pre-study and other previous research. All scales were translated into German unless a translation was already available. Further, we assessed multi-item constructs using six-point Likert scales (1 = “strongly disagree”; 6 = “totally agree”). The questionnaire was structured as follows:

In the introduction, subjects were provided with a thematic overview of the significance of sustainability and energy efficiency within the corporate domain.

In the subsequent sections, individual factors were examined, beginning with sociodemographics (age, gender, education). To enhance accessibility for an international audience, the qualifications from the German education system were classified into low, medium, and high educational attainment based on the International Standard Classification of Education (ISCED). The respondents' age was surveyed in age groups (18–25, 26–35, 36–45, 46–55, 56–65, 66–75, 76–85 years) to further facilitate their anonymity.

Following this, attitudinal factors were assessed, including participants' eco-consciousness using an instrument by Geiger and Holzhauer (2020; eight items, e.g., “We need to find ways to live well independently of economic growth”), and their innovativeness using five items by Klöckner and Nayum (2017; e.g., “I enjoy trying new ideas”). Locus of Control (LoC) was measured with four items by Kovaleva et al. (2014; e.g., “If I work hard, I will succeed”). To assess leaders' pro-environmental behaviors, we used the Organizational Citizenship Behavior for the Environment (OCBE) scale by Boiral and Paillé (2012; nine items, e.g., “I voluntarily carry out environmental actions and initiatives in my daily work activities”).

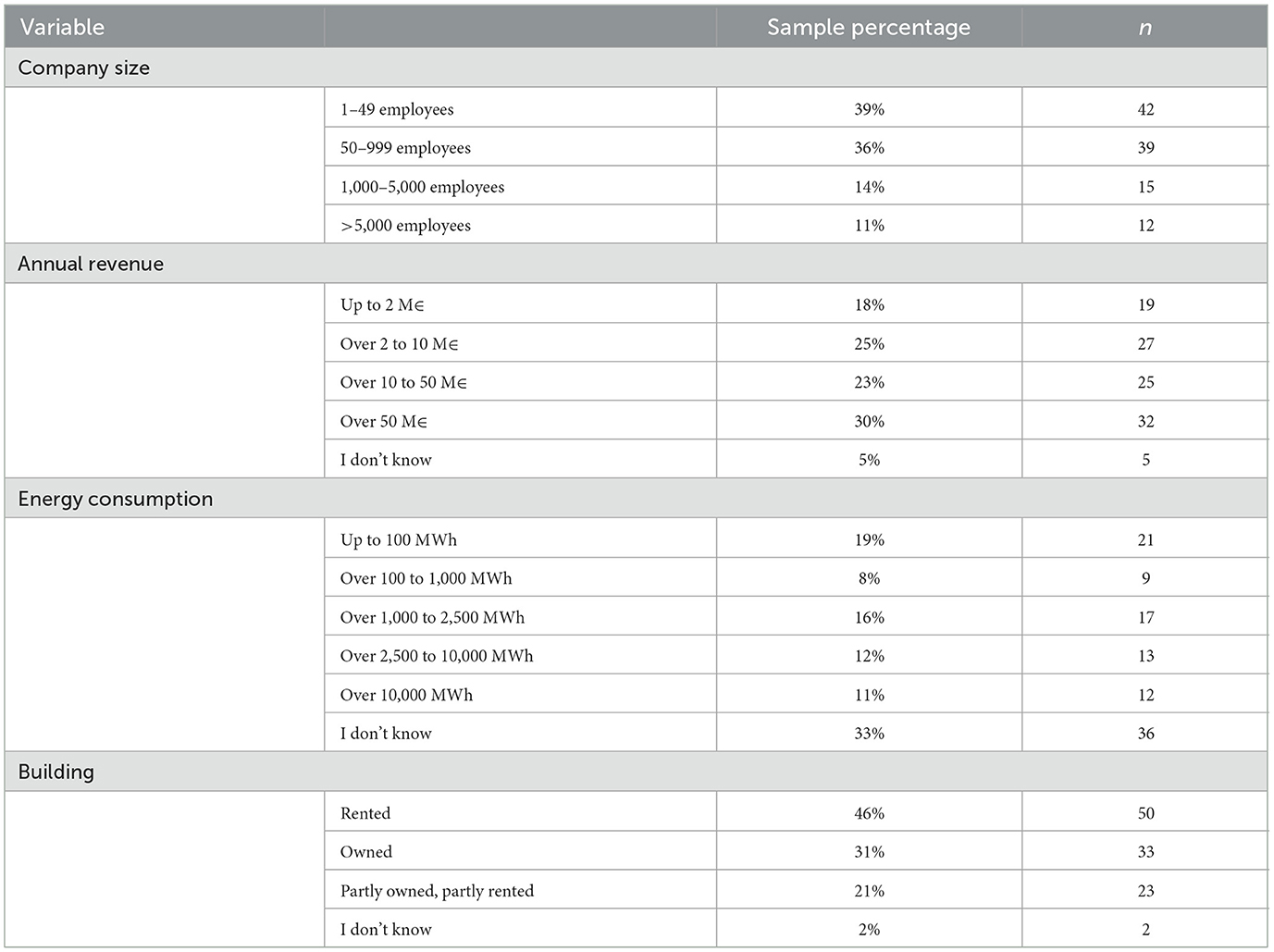

In the following sections, the thematic focus shifts to the organizational context. Participants were asked to provide the basic key data of their respective companies: sector, company size (number of employees), annual revenue, energy consumption, and building type (rented, owned, or partly owned and rented). An additional “I don't know” option was provided.

Next, we surveyed the position demographics, including participants' area of occupation, job title, and years of work experience.

To evaluate corporate sustainability factors, participants were asked whether their companies had implemented sustainability measures in 14 potential areas (e.g., energy procurement, CO2 compensation), derived from our qualitative pre-study. Additionally, we adapted the Corporate Environmental Policies Scale by Ramus and Steger (2000) and included 12 items to assess the integration of sustainability within the organizational policy framework (e.g., “My company publishes an environmental policy”). The respondents were presented with three answer options—“yes”, “no”, and “I don't know”—for both questions. The reinvestment phase of corporate sustainability was assessed using six self-designed items derived from the qualitative study. These items aimed to gauge whether sustainability and energy efficiency measures and investments were monitored, evaluated, and subsequently reinvested into advancing sustainability endeavors (e.g., “My company monitors the impact of sustainability measures and investments”). Lastly, participants were asked to rate the perceived importance of sustainability and energy efficiency within their companies (1 = “not at all important”; 6 = “very important”).

Finally, we measured the participants' sustainability and energy efficiency awareness as another attitudinal factor. We evaluated awareness using three self-formulated items to measure interest, self-perceived knowledge, and assessment of climate effectiveness regarding corporate sustainability and energy efficiency measures, respectively (e.g., “Companies that invest in sustainability/energy efficiency contribute significantly to climate change mitigation”).

The questionnaire was pretested for comprehensibility and approved by the university ethics committee.

5.2 Statistical analysis

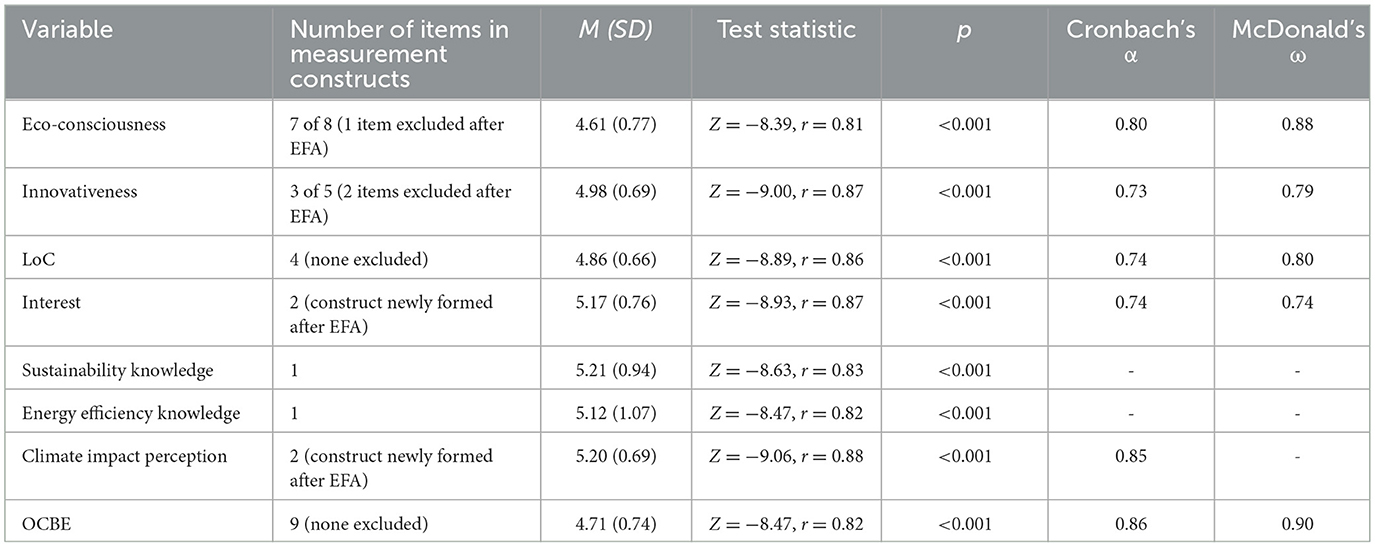

Data analyses were conducted in R Studio Version 2022.12.0+353. To assess the internal consistency of the constructs, Cronbach's alpha and McDonald's omega values were computed, and exploratory factor analysis (EFA) was conducted. The analysis revealed that scale reliability could be enhanced by removing one item of eco consciousness (α = 0.8) and two items of innovativeness (α = 0.73). Additionally, EFA indicated that the original assumption of combining the three factors (knowledge, interest, and assessment of climate effectiveness) into one awareness construct was not supported. Instead, interest in sustainability and energy efficiency were merged into a single “interest” construct (α = 0.74), while the effectiveness items were combined into a construct labeled “climate impact perception” (α = 0.85). Sustainability knowledge and energy efficiency knowledge formed separate 1-item constructs.

The measured corporate sustainability factors were divided into two groups, forming the target variables for the study: First, perceived sustainability, reflecting the ideological stance toward sustainability within the company, was operationalized through the two variables perceived sustainability relevance and perceived energy efficiency relevance. Secondly, practical sustainability was evaluated through the implementation of sustainability measures and corporate environmental policies. As in the study by Keil et al. (2025), we combined sustainability measures and corporate environmental policies into an additive index, the Corporate Sustainability Index (CSI, 26 items). Thus, the CSI reflects both tangible sustainability initiatives and the degree to which sustainability is systematically and politically embedded in companies, thereby providing a means to analyze correlations with practical sustainability efforts. It is important to note that the methodological approach of measuring practical sustainability via an online survey reflects the respondents' perceptions of integrated measures and policies. However, given their positions as sustainability decision-makers, it is assumed that the respondents provided realistic evaluations of the implementation of these measures and policies. Therefore, we classify the CSI and the sustainability and energy efficiency reinvestment factors as practical sustainability variables, reflecting the participants' evaluation of specific measures. Conversely, we categorize perceived relevancies as perceived sustainability factors, as they represent a less tangible assessment of the overall organizational climate regarding sustainability.

Appropriate parametric and non-parametric test procedures (e.g., ANOVAs, Spearman's rank correlation) were performed for inferential statistical analysis. We conducted hierarchical multiple regression analysis to investigate how the dependent variable varies with the incremental addition of each independent variable. This methodological approach facilitates the computation of the unique influence of a predictor while simultaneously controlling for the effects of other (control) variables (Jeong and Jung, 2016). Prior to the regression analysis, we verified assumptions of linearity, multicollinearity, normality of residuals, homoscedasticity, and independence of errors. Categorical variables were dummy-coded, using as reference levels either the group representing the majority of respondents or, for ordinal variables, the lowest-ranked cohort, such as companies with the lowest energy consumption.

5.3 Characteristics of the survey participants

This study targeted individuals responsible for decisions related to sustainability and energy efficiency investments within their companies. To reach this specific demographic, a market research institute was commissioned with the acquisition and remuneration of suitable respondents. To verify the authenticity of respondents as decision-makers responsible for determining sustainability measures and investments in their respective companies, potential respondents from the panel were first invited to complete a screening survey. Stringent screening criteria were applied to identify sustainability decision-makers: eligible participants were required to (a) have financial responsibility; (b) be professionally involved—at least in part—in sustainability-related activities in their company; (c) influence sustainability-related decisions, either as sole decision-makers, as members of a decision-making team, or as someone preparing the decision. Additionally, (d) individuals whose companies had not yet integrated sustainability as an organizational objective were excluded, as no relevant decision-making processes would be present in such cases.

The study was conducted in Germany in 2023. Incomplete data sets and participants with rapid response patterns were excluded to maintain data integrity. Additionally, respondents who made contradictory statements were excluded from the study. The final sample comprised N = 108 participants, with a gender distribution of 61% male (n = 66) and 39% female (n = 42) participants. The majority of respondents were aged 26–35 years (n = 25, 23%), 36–45 years (n = 37, 34%) or 46–55 years (n = 32, 30%). Approximately one-third of participants held business management or leadership positions (n = 35, 32%), while 14% (n = 15) were specifically designated to sustainability management roles. For detailed information about the companies where the surveyed decision-makers were employed, refer to Table 2.

Table 2. Description of organizational key data.

6 Results of the quantitative main study

6.1 Descriptive analysis of individual and corporate sustainability factors

Considering attitudinal factors, the sustainability decision-makers exhibited high levels of eco-consciousness (M = 4.61, SD = 0.77), innovativeness (M = 4.98, SD = 0.69), and Locus of Control (LoC: M = 4.86, SD = 0.66). They also showed strong interest in sustainability and energy efficiency (M = 5.17, SD = 0.76). On average, they were knowledgeable about sustainability (M = 5.21, SD = 0.94) and energy efficiency measures (M = 5.12, SD = 1.07). The elevated mean score for climate impact perception (M = 5.20, SD = 0.69) indicated that decision-makers viewed these measures as effective in addressing climate concerns. Regarding behavior, decision-makers displayed heightened Organizational Citizenship Behavior for the Environment (OCBE: M = 4.71, SD = 0.74). All attitudinal factor means were left-skewed and deviated significantly from the scale mean of 3.5 (see Table 3).

Table 3. Values for the descriptive analysis of individual factors (M = Median, SD = Standard Deviation, Test statistic for one-sample Wilcoxon signed rank test).

Regarding the perceived sustainability factors, respondents evaluated sustainability issues within their company as “important,” shown by high perceived sustainability (M = 4.71, SD = 0.84, Z = −8.39, p = < 0.001, r = 0.81) and energy efficiency relevancies (M = 4.71, SD = 0.84, Z = −8.55, p < 0.001, r = 0.82). The Corporate Sustainability Index (CSI), as the practical sustainability factor, ranged from 5 to 26 with a mean of M = 17.27 (SD = 4.37). This indicates that, on average, the companies surveyed have already implemented a range of measures and policies in the domain of sustainability.

6.2 Individual factor correlations

The analysis of bivariate correlations between the individual factors of sustainability decision-makers and corporate sustainability showed that sustainability relevance was positively and significantly associated with almost all measured decision-makers' attitudes (see Table 4): a strong association was found for sustainability relevance and decision-makers' citizenship behavior for the environment (OCBE, rs = 0.54, p < 0.001). Interest in sustainability and energy efficiency was moderately correlated with sustainability relevance (rs = 0.44, p < 0.001). The remaining factors demonstrated weak correlations, except for Locus of Control (LoC), which was not associated with sustainability relevance (rs = 0.09, p = 0.184, n.s.).

Table 4. Bivariate correlations between perceived corporate sustainability factors and individual factors.

A similar pattern emerged concerning energy efficiency relevance. Again, OCBE exhibited the highest correlation (rs = 0.41, p < 0.001), followed by interest (rs = 0.37, p < 0.001), although both correlations were moderate and less pronounced compared to sustainability relevance. Once again, the remaining individual factors were weakly related to energy efficiency relevance, except for eco-consciousness, which demonstrated no significant correlation (rs = 0.15, p = 0.064, n.s.). In contrast to sustainability relevance, LoC was weakly related to energy efficiency relevance (rs = 0.17, p < 0.05).

In the next step, we calculated bivariate correlations between the CSI and individual factors to examine the relationship between sustainability implementation within companies and the attitudes of decision-makers (see Table 5). OCBE (rs = 0.32, p < 0.001), sustainability and energy efficiency interest (rs = 0.20, p < 0.05) were significantly positively related to CSI. However, leaders' eco-consciousness, innovativeness, Locus of Control, their sustainability and energy efficiency knowledge, as well as climate impact perception were not correlated with CSI as the practical sustainability factor. These findings suggest that while decision-makers' attitudes were linked to the perceived importance of sustainability and energy efficiency within their organizations, their association with the practical implementation of corporate sustainability was weaker and limited to two individual factors.

Table 5. Bivariate correlations between practical corporate sustainability factor and individual factors.

6.3 Organizational factors

6.3.1 Company size

Our analysis revealed no statistically significant association between company size and the perceived relevance of sustainability [H(3) = 1.20, p = 0.752, n.s.] or energy efficiency [H(3) = 1.75, p = 0.627, n.s.] within the corporate landscape.

In terms of practical sustainability, the ANOVA revealed a significant effect of company size on CSI [F(3, 104) = 13.43, p < 0.001]. Post-Hoc tests further showed that small businesses with up to 49 employees (n = 42, M = 14.88, SD = 3.94) had the lowest CSI scores and differed significantly from all other companies with a larger workforce. Companies with 50 to 999 employees (n = 39, M = 17.44, SD = 4.19) showed no significant deviation from the subsequent largest group of companies with 1,000 to 5,000 employees (n = 15, M = 20.33, SD = 3.09), but did exhibit a significant deviation from the largest enterprises with more than 5,000 employees (n = 12, M = 21.25, SD = 1.86). The two groups of the largest companies with more than 1,000 and 5,000 employees, respectively, did not differ significantly in terms of CSI.

6.3.2 Annual revenue

The revenue groups did not differ significantly with regard to either sustainability relevance [H(3) = 2.19, p = 0.534, n.s.] or energy efficiency relevance [H(3) = 2.92, p = 0.820, n.s.].

Contrary, the analysis demonstrated a significant influence of annual revenue on CSI [F(3, 99) = 20.11, p < 0.001]. When comparing the revenue groups, all groups differed significantly from each other except for companies with a turnover of up to ∈2 million (n = 19, M = 13.84, SD = 1.95) and over ∈2 to ∈10 million (n = 27, M = 15.04, SD = 4.56). The two remaining groups, comprising companies with revenues ranging from over ∈10 to ∈50 million (n = 35, M = 18.12, SD = 3.38) and exceeding ∈50 million (n = 32, M = 20.62, SD = 3.23), exhibited even higher CSI values on average. This observation suggests a positive association between higher annual turnover and enhanced corporate sustainability.

6.3.3 Building type

We compared companies who either have rented (n = 50) or owned (n = 33) their company buildings. Companies leasing (M = 4.68, SD = 0.96) their buildings showed no differences compared to those owning (M = 4.76, SD = 0.79) their premises regarding sustainability relevance (W = 787, p = 0.704, n.s.). We found similar results regarding the perceived relevance of energy efficiency, which also did not vary significantly (W = 716, p = 0.261) between tenants (M = 4.64, SD = 0.90) and owners (M = 4.85, SD = 0.71).

Finally, the mean CSI scores for companies with rented (M = 16.14, SD = 4.63) or owned (M = 17.73, SD = 4.05) buildings were comparably high, indicating no significant difference between the two groups [t(81) = −1.61, p = 0.112, n.s.].

6.3.4 Energy consumption

Similar to the factors previously examined, there was no significant difference in the perceived relevance of sustainability [H(4) = 3.881, p = 0.422, n.s.] and energy efficiency [H(4) = 2.806, p = 0.591, n.s.] in companies with different energy demands.

For the Corporate Sustainability Index, the ANOVA indicated a significant effect of companies' energy consumption on CSI scores [F(3, 67) = 5.68, p < 0.001]. However, post-hoc tests showed that only companies with the lowest annual energy consumption of up to 100 MWh (n = 21, M = 14.57, SD = 4.07) exhibited significant differences from groups with the highest energy consumption, specifically those consuming 2,500–10,000 MWh (n = 13, M = 20.31, SD = 3.01) and over 10,000 MWh (n = 12, M = 19.58, SD = 4.50).

In summary, our analyses showed that the relevance attributed to sustainability and energy efficiency in companies remains consistent across various organizational factors. However, company size, annual turnover, and electricity consumption significantly impact practical sustainability, as measured by the Corporate Sustainability Index. Notably, smaller companies with lower annual turnover and energy consumption typically diverge from larger companies with higher turnover and energy consumption.

6.4 Hierarchical multiple regression analysis on CSI

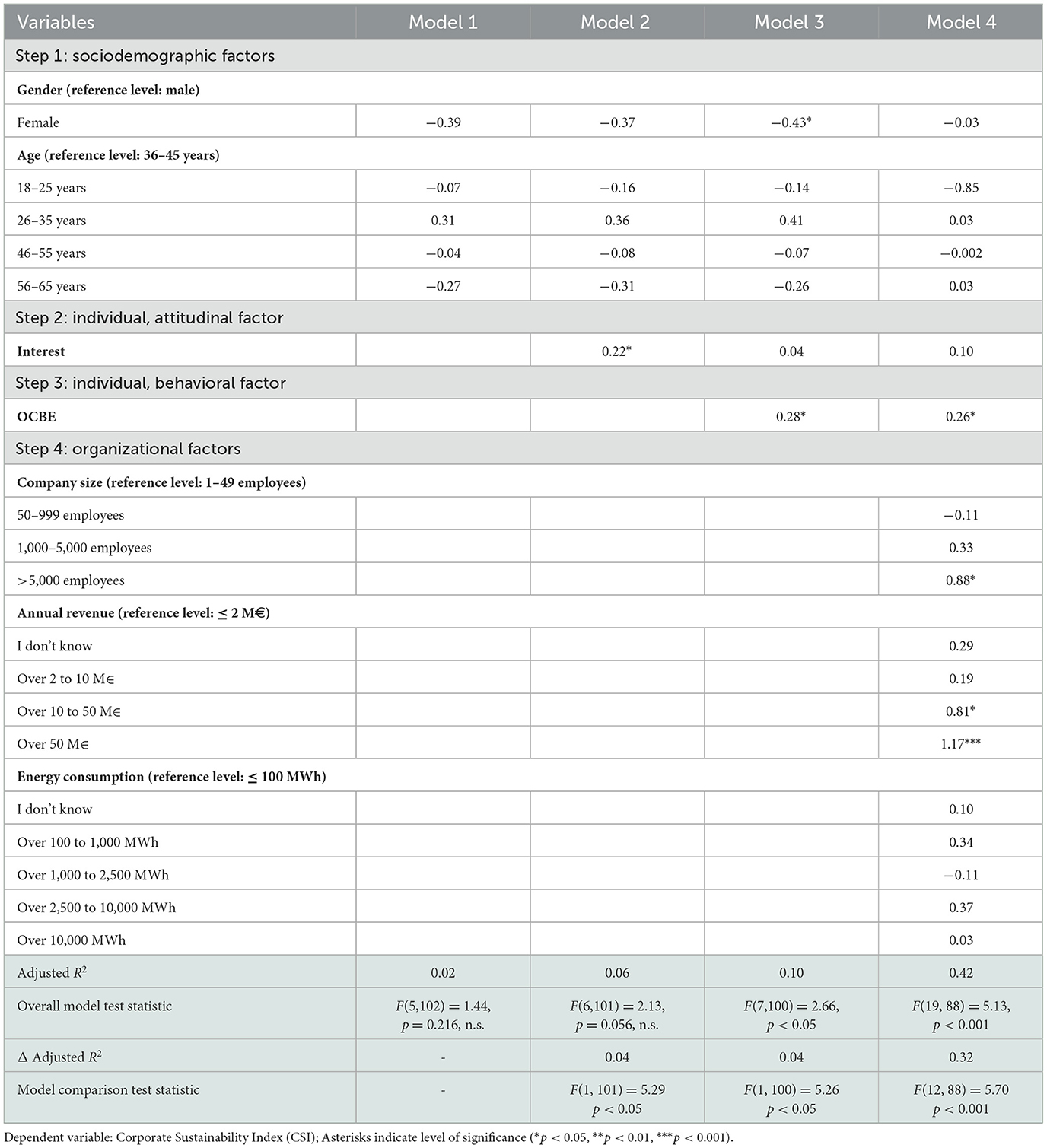

To better understand the factors influencing the Corporate Sustainability Index (CSI), we conducted a hierarchical multiple regression analysis. The CSI was set as the dependent variable, representing practical sustainability implementation within companies, to generate actionable insights to advance corporate sustainability efforts. Guided by the underlying hypotheses presented in the research model, the regression analysis was structured into four models. Predictors identified as relevant in the preceding correlational analysis were systematically introduced in successive steps, enabling a comprehensive evaluation of their individual and combined contributions to corporate sustainability outcomes.

• Step 1: Inclusion of gender and age as sociodemographics to control their potential influence in the subsequent steps.

• Step 2: Interest was added as the only individual attitudinal factor significantly correlating with CSI.

• Step 3: OCBE was added as the only individual behavioral factor significantly correlating with CSI.

• Step 4: Inclusion of organizational factors (company size, annual revenue and energy consumption), which were found to be associated with CSI. Because categorical, non-dichotomous variables cannot be included directly in regression analysis, all organizational factors were dummy-coded. Reference levels can be seen in Table 6.

Table 6. Results of hierarchical regression analysis on the prediction of the Corporate Sustainability Index showing β-values for all predictors and model test statistics.

The initial model, containing only sociodemographic factors, explained 2% of CSI variance and was statistically insignificant (adjusted R2 = 0.02). Incorporating interest as an attitudinal factor in Model 2 increased explained variance by 4% up to 6%, yet Model 2 (adjusted R2 = 0.06) remained statistically insignificant. The inclusion of OCBE in step 3 further elevated explained variance by 4% (Model 3, adjusted R2 = 0.10). Finally, adding organizational factors in Model 4 (adjusted R2 = 0.42) resulted in the most substantial enhancement, increasing explained variance by 32% up to 42%.

Since Model 4 offered the most accurate prediction of corporate sustainability, it is analyzed in detail. For a comprehensive overview, Table 6 presents the beta coefficients for all models and variables. The sociodemographic variables were not significant, indicating that neither decision-makers' gender nor age was associated with their company's corporate sustainability. While interest did not demonstrate significant predictive value, OCBE, as a behavioral individual factor, emerged as a significant predictor (β = 0.26, p < 0.05), indicating that decision-makers who exhibit strong environmental citizenship behavior positively influence corporate sustainability performance. Among the organizational factors, a significant difference was found for the largest enterprises with over 5,000 employees, which showed higher CSI levels compared to the reference group (1–49 employees; β = 0.89, p < 0.05). The analysis did not reveal significant predictive power for the two smaller company groups, those with 50–999 employees and those with 1,000 to 5,000 employees, when compared to the reference group. These findings suggest that the size of companies within these ranges did not exert a notable influence on the outcome variable. The analysis of company revenue revealed two significant predictors of CSI compared to the reference group (≤ 2 M∈): companies with revenues ranging from over ∈10 to ∈50 million (β = 0.81, p < 0.05), and those exceeding ∈50 million (β = 1.17, p < 0.001). The revenue group with over ∈2 to ∈10 million and the group where respondents indicated that they “don't know” their company's revenue were both not significant predictors in Model 4. Energy consumption groups were not identified as significant predictors for CSI, indicating that a higher energy consumption—compared to the reference level ≤ 100 MWh—does not significantly impact corporate sustainability.

6.5 Descriptive analysis of energy-efficiency-reinvestments

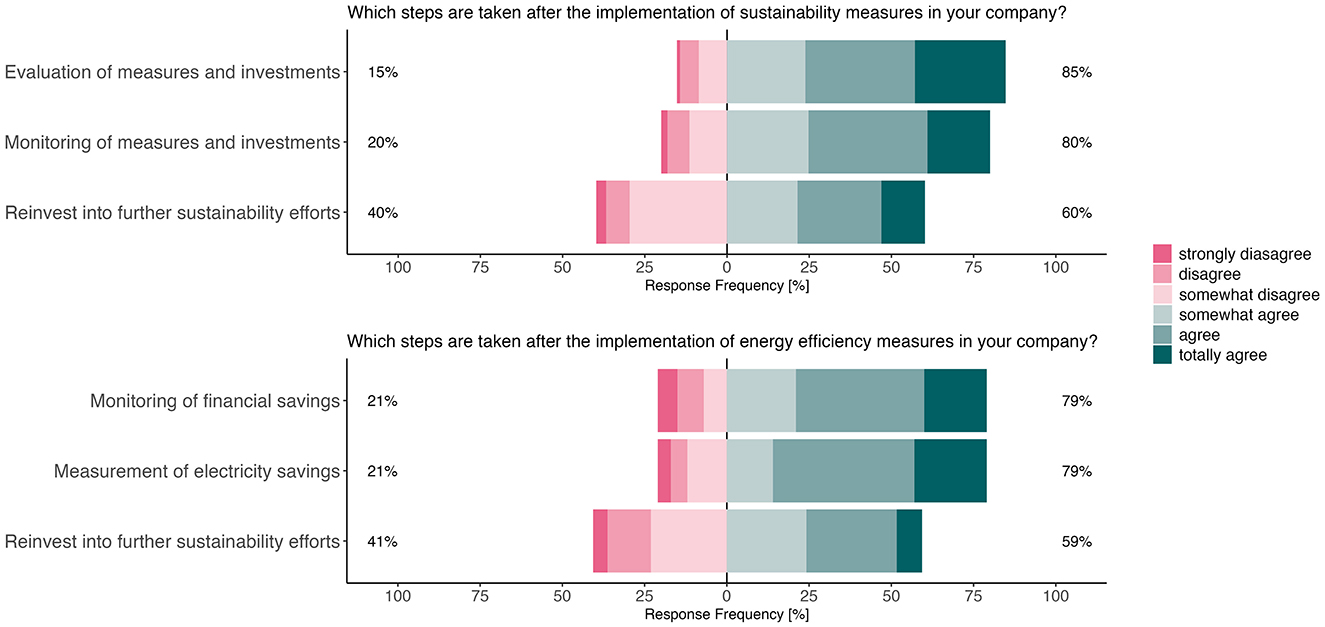

The implementation of sustainability and energy efficiency measures marks an important first step toward corporate sustainability. However, these efforts must be accompanied by rigorous monitoring and strategic reinvestments to mitigate potential long-term rebound effects and ensure sustained impact.

Following the implementation of sustainability measures and investments, 85% of respondents reported that their companies evaluate the measures taken (M = 4.66, SD = 1.19), and 80% indicated that their organizations actively monitor the impact of these measures (M = 4.44, SD = 1.22). Despite this, only 60% of companies reinvest savings from sustainability measures into further sustainability initiatives (M = 3.99, SD = 1.29), highlighting a potential gap between implementation and reinvestment practices. A similar pattern was observed for the energy efficiency measures and investments taken. Among the companies surveyed, 79% reported monitoring electricity (M = 4.53, SD = 1.31) and monetary savings (M = 4.36, SD = 1.4) from energy efficiency investments, while just 59% reinvested these savings into additional sustainability efforts (M = 3.8, SD = 1.31). Figure 4 provides a detailed breakdown of the response frequencies for monitoring and reinvesting practices.

Figure 4. State of reinvestment phase regarding sustainability and energy efficiency (n = 91–105, “I don't know” excluded).

7 Discussion and implications

Understanding the organizational and individual drivers of corporate sustainability is crucial for advancing sustainable development within organizations. By applying a two-step empirical approach, we first qualitatively explored relevant factors of corporate sustainability from an employee perspective. Second, we quantified their significance and investigated their respective impact on sustainability performance based on the Corporate Sustainability Index (CSI). While previous research has primarily focused on analyzing the influence of various sustainability drivers in isolation, this study takes a comprehensive approach by examining their combined effects to assess their relative impact.

7.1 Perception and practical implementation of sustainability in companies

The findings indicate that sustainability and energy efficiency are perceived as highly relevant across German companies, reflecting growing awareness of corporate responsibility. However, a notable discrepancy was observed between the widely acknowledged importance of corporate sustainability and its practical incorporation. Despite widespread recognition of corporate sustainability's importance, participants reported limited integration into daily routines, empirically confirming the disconnect between sustainability perception and practice (Hahn and Aragón-Correa, 2015). This discrepancy—reflected in medium average CSI scores—suggests that while progress exists, potential remains to strengthen sustainability measures and implementation. The gap underscores the need for better strategic and operational alignment to translate perceived relevance into measurable practice (e.g., Manninen and Huiskonen, 2022).

One possible explanation for this disparity is the green attitude-behavior gap (ElHaffar et al., 2020), which describes the discrepancy between individuals' green attitudes and their actual actions, often influenced by contextual barriers or a lack of supporting mechanisms. While extensively studied in the context of private green behaviors, it has received limited attention so far in organizational contexts. Bekmeier-Feuerhahn et al. (2017) acknowledged this research gap, proposing that targeted corporate social responsibility communication could enhance employees' subjective norms and perceived behavioral control, thereby fostering the alignment of their attitudes with pro-environmental behaviors. While their study was based on theoretical perspectives, this study provided empirical evidence of the attitude-behavior gap in an organizational context, highlighting the divergence between perceived and practical corporate sustainability. This gap underscores the influence of both individual-psychological and organizational factors in shaping sustainability outcomes (Joshi and Rahman, 2015; Jusuf and Nuttavuthisit, 2023).

An important contribution of this study is the refinement of the Corporate Sustainability Index (CSI), which measures employees' perceptions regarding the practical implementation of sustainability measures and policies (Keil et al., 2025). Although the CSI has been described as a “practical sustainability” indicator, it remains a reflection of decision makers' perceptions of the practical implementation of specific sustainability measures. The CSI bridges a critical gap in existing tools that often emphasize objective sustainability outcomes, such as environmental performance indicators (e.g., carbon footprints or energy consumption), without considering how sustainability efforts are interpreted by employees. Existing frameworks like the Global Reporting Initiative and ISO 14001 certification provide standardized approaches to assess and report environmental sustainability, yet they do not account for subjective evaluations, which are crucial for fostering employee engagement and aligning organizational culture with sustainability goals (e.g., Herremans and Nazari, 2016; Lozano, 2020). The CSI offers a complementary perspective by providing insights into how well organizations integrate their sustainability efforts into workplace practices and how these efforts resonate with their workforce. Future research should extend the CSI framework by exploring its relationship with objective sustainability measures to examine whether perceived and objective sustainability efforts align or diverge. Understanding this alignment is critical for identifying potential gaps in organizational sustainability communication and implementation.

7.2 Individual and organizational impact factors on corporate sustainability

This study aimed to identify (RQ1) and analyze (RQ2) how organizational and individual-psychological factors jointly influence corporate sustainability. Findings show that individual factors, such as Organizational Citizenship Behavior for the Environment (OCBE), strongly influenced perceived sustainability, while organizational factors, such as company size and revenue, drove the practical implementation of sustainability measures. This highlights the need for integrated strategies that align employee engagement with corporate goals, as both levels interact to shape sustainability outcomes (e.g., Lozano, 2015; Florez-Jimenez et al., 2024).

Among the individual factors, OCBE was a significant predictor of corporate sustainability, underscoring the need for organizations to cultivate a culture that encourages proactive sustainability behaviors. Consistent with previous research, OCBE was associated with pro-environmental actions that support organizational sustainability outcomes (e.g., Boiral et al., 2015). Notably, OCBE was the only significant individual-level predictor of corporate sustainability among leaders, while their personal pro-environmental attitudes showed no direct effect. However, individual attitudes may still influence outcomes indirectly through OCBE (Bhattacharyya and Biswas, 2021). Leaders with strong pro-environmental attitudes may perceive sustainability as more relevant within their organizations, motivating them to promote sustainability initiatives through their behavior (Cheema et al., 2020). Future research should use structural equation modeling to analyze the pathways through which individual attitudes and OCBE interact. To support managers in their role as sustainability leaders, companies can support and train them to further enhance their OCBE and other leadership practices facilitating sustainability, e.g., green transformational leadership (Liu and Yu, 2023). Still, Löbbe et al. (2019) highlight that for effective integration of sustainability, particularly in energy efficiency, managers must not only initiate and organize measures, but also raise awareness and decentralize responsibility, thereby combining top-down and bottom-up approaches.

Other individual factors, such as eco-consciousness and sustainability knowledge, showed limited relations with corporate sustainability. Eco-consciousness was associated with the perceived relevance of sustainability but did not significantly impact practical implementation, suggesting that without organizational support, eco-conscious individuals may lack the necessary resources to translate their attitudes into behaviors (e.g., Norton et al., 2015). Although prior studies highlighted sustainability knowledge as a significant predictor of eco-friendly leadership and corporate sustainability advancements (e.g., Candrianto et al., 2023), it was not significantly related to practical outcomes in this study. This finding suggests that in organizational contexts, external factors such as prevailing organizational norms and available resources may exert a more critical influence on sustainability actions than individual dispositions. Future research could examine how targeted interventions help translate individual knowledge into actionable sustainability efforts.

Organizational factors, particularly company size and revenue, were identified as key drivers of practical sustainability implementation. Larger companies with higher revenues demonstrated greater CSI scores, likely due to greater resources and stakeholder pressure, aligning with prior research indicating that smaller companies often face resource constraints and lack the economies of scale needed to implement comprehensive sustainability measures (Uhlaner et al., 2012; Hörisch et al., 2015). Larger organizations, conversely, can leverage sustainability initiatives as a competitive advantage, enhancing their market reputation and operational efficiency (Hermundsdottir and Aspelund, 2022). To support SMEs, policymakers should consider appropriate regulations, tax incentives, or other subsidies to help overcome resource limitations (Bakos et al., 2020). To address the perceived lack of emphasis on sustainability compared to economic efficiency among SMEs, local governments could play a crucial role in facilitating and supporting regional networks. These networks would serve as platforms for SMEs to exchange experiences, share success stories—such as sustainability measures with economic benefits—and disseminate examples of best practices in sustainability and energy efficiency (Conway, 2015). Contrary to existing literature, energy consumption was not a significant predictor of corporate sustainability in this study. This may suggest that companies with higher energy consumption focus on improving energy efficiency rather than adopting broader sustainability initiatives, such as carbon offsetting or supply chain decarbonization—consistent with findings indicating the prioritization of energy efficiency in energy-intensive industries (e.g., Khan et al., 2021).

Overall, the findings underscore a critical gap between the recognition of sustainability's importance and its practical implementation within organizations. While companies increasingly acknowledge the relevance of sustainability, translating this awareness into tangible actions remains a significant challenge. The CSI predictors from the regression analysis suggest possible strategies to enhance practical sustainability. Our findings align with Keil et al. (2025), showing that managers can positively influence sustainability through their proactive citizenship behavior. This underscores their critical role in driving corporate sustainability, as they have the authority to implement sustainability measures and investments (Schaltegger et al., 2024). Considering organizational factors, large enterprises with a high annual turnover scored highest on the CSI, confirming previous research stating that SMEs struggle more with sustainability implementation (e.g., Uhlaner et al., 2012).

7.3 Sustainability and reinvestment practices

One goal of the study was to examine whether companies monitor savings from sustainability and energy efficiency measures and reinvest them into subsequent sustainability initiatives (RQ3). Findings from the qualitative pre-study suggested that monitoring was either not implemented in most companies or unknown to the respondents. In cases where monitoring measures were reported, savings were typically redirected to the general budget, potentially facilitating rebound effects. The rebound effect refers to the phenomenon where the expected savings from an investment are partially offset or negated due to behavioral or systemic responses. For example, after investing in energy efficiency measures, companies may experience less-than-expected reductions in energy consumption due to increased production or other compensatory behaviors (Peters and Dütschke, 2016; Santarius and Soland, 2018). Growth-induced rebound effects are particularly prevalent in corporate settings, as enhanced efficiency often leads to expanded production to gain competitive advantages (Berner et al., 2022). In contrast to the qualitative findings, the quantitative study revealed that the majority of companies monitored and evaluated sustainability and energy efficiency measures. A significant proportion of organizations indicated that they reinvest savings from these measures into further sustainability initiatives. However, reinvestment practices garnered the lowest level of agreement, indicating room for improvement in systematically channeling savings back into sustainability efforts. This also contradicts previous research, which found a lack of monitoring and goal-setting regarding low-carbon activities in SMEs (Conway, 2015). The divergent findings between the qualitative and quantitative studies underscore a need for further investigation into the underlying barriers and facilitators of effective reinvestment strategies. For instance, variations in company size, industry, or organizational culture may contribute to these differences. Additionally, perceived versus actual practices in monitoring and reinvestment require closer examination, as the gap between organizational intentions and implementation could explain some of the divergence.

8 Limitations and future research

Our two-step empirical approach provided comprehensive insights into corporate sustainability drivers. First, we exploratively identified relevant factors, followed by quantitative weighting and analysis. Despite these strengths, some methodological and content-related limitations should be considered.

While the qualitative interview study sample includes participants from a wide range of ages, industries, seniority levels, and job functions, supporting thematic richness and contextual depth, we acknowledge that certain perspectives may still be underrepresented. For example, voices from small companies or especially non-Western cultural settings were less prominent in our data. We recommend that future research explore these contexts further to broaden the applicability and nuance of the findings. Further, the thematic saturation is worth reflecting: to assess thematic saturation, we followed an iterative coding process in which interview data were continuously analyzed alongside data collection. Saturation was considered reached when additional interviews yielded no substantially new codes or themes. This point was observed after approximately 22 interviews, with the remaining three interviews confirming the consistency of the coding frame and the stability of conceptual categories.

For the sampling of the quantitative study, future studies should try to reach larger samples to deepen the insights and the understanding of influencing parameters on corporate sustainability. Since this study targeted sustainability decision-makers, evaluating the sample's representativeness for this group is challenging. Further research is required to determine the sample's balance. However, acquiring specific samples, as in the present study with its extensive screening criteria, requires significant time and resources. Consequently, this study offers valuable insights into corporate sustainability research by taking into account the individual-psychological characteristics of sustainability decision-makers and providing initial insights from this point of view. Although a substantial proportion of the variance in the CSI could be explained by the selected factors, the model may have been further improved by including additional influencing variables. While the selection of factors was based on both the literature review and the qualitative pre-study, it was not feasible to incorporate all factors identified as potentially relevant. Notably, these include organizational-contextual variables such as corporate culture and values (e.g., respect and fairness, accountability), structural characteristics (e.g., hierarchy, formalization), and a range of external factors, including reputation, customer expectations, regulatory requirements, and legislation (Avota et al., 2015; Keil et al., 2025; Lozano, 2015). However, this study deliberately focused on individual-psychological factors and organizational-contextual aspects, rather than external drivers as emphasized in institutional or stakeholder theories. Moreover, the number of factors was limited to ensure the feasibility of the survey in terms of length and cognitive load for respondents, as well as to maintain sufficient statistical power in the multiple regression analysis given the limited sample size. Additionally, future research could employ methodological approaches, e.g., cluster analysis, to uncover patterns of companies and deepen the understanding of influencing factors.

A further limitation is the focus on German companies, offering a single-country perspective that may restrict the generalizability and transferability of the findings to an international context. According to institutional theory, external situational factors, including specific social and cultural expectations and regulatory conditions, play a pivotal role in shaping entrepreneurial actions (Scott, 1992). In this regard, Miska et al. (2018) identified cultural traits and practices that influence corporate sustainability. These included future orientation, gender egalitarianism, uncertainty avoidance, and power distance practices, which acted as positive drivers. Conversely, performance orientation acted as a barrier. They further found that these cultural traits are not confined to country boundaries but rather apply to clusters of countries with similar cultures. While this suggests that our findings are potentially applicable to countries with cultures similar to Germany's, it also underscores the need for comparative studies of corporate sustainability measures and their drivers across diverse cultural contexts. Additionally, situational conditions may influence the identified sustainability drivers. For instance, Lee et al. (2018) demonstrated that Chinese employees exhibited lower organizational citizenship behavior compared to U.S. employees, which could affect corporate sustainability efforts. The authors suggest that this discrepancy may stem from perceptions among Chinese employees that their engagement would not have a significant impact, which could be linked to differing hierarchical structures and power distances in the U.S. and China. Lastly, existing regulations and legislation pose another critical situational driver (Lozano and Von Haartman, 2018) that varies across countries and cultures within different political frameworks that could be integrated into further studies.

Finally, the conflicting findings of the qualitative and quantitative studies regarding the reinvestment of savings from sustainability and energy efficiency measures may indicate a need for further refinement of the measurement of the reinvestment phase. This would be particularly relevant for studies investigating the phenomenon of rebound effects.

9 Conclusion

This study successfully identifies and addresses several critical gaps in corporate sustainability research, contributing significantly to its advancement. We adopted a sequential mixed-methods design, in which the qualitative pre-study provided a vital foundation for the subsequent quantitative phase, examining a diverse range of corporate sustainability drivers collectively. Insights from the qualitative interviews informed the selection and refinement of key constructs, ensuring contextual relevance by emphasizing the role of leaders in corporate sustainability and revealing reinvestment as a significant area of research that had been left unexplored. The subsequent quantitative analysis enabled these constructs to be systematically tested and validated across a broader sample, thereby complementing and extending the exploratory findings. Together, these two approaches provide a more comprehensive understanding of the phenomena in question and strengthen the robustness of our conclusions. This comprehensive analysis not only enhances our understanding but also lays the groundwork for developing a unified theoretical framework. By conducting a sample comprising leaders who serve as sustainability decision-makers, we were able to capture their perceptions and assess their influence on corporate sustainability, thereby highlighting their essential role as vital change agents within organizations.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Ethics statement

The studies involving humans were approved by the Ethics Committee of RWTH Aachen University under the application number 2023_06_FB7_RWTH Aachen. The studies were conducted in accordance with the local legislation and institutional requirements. The participants provided their written informed consent to participate in this study.

Author contributions

MK: Visualization, Data curation, Validation, Methodology, Conceptualization, Project administration, Supervision, Investigation, Writing – review & editing, Writing – original draft, Formal analysis. AR: Investigation, Writing – review & editing, Data curation, Writing – original draft, Conceptualization, Validation, Formal analysis. JO: Formal analysis, Investigation, Writing – review & editing, Data curation, Validation, Conceptualization, Writing – original draft, Visualization. MZ: Resources, Conceptualization, Writing – review & editing, Supervision, Funding acquisition, Methodology, Writing – original draft. KA: Resources, Writing – original draft, Project administration, Writing – review & editing, Conceptualization, Funding acquisition, Supervision, Methodology.

Funding