Mark L. Taper

Mark L. Taper Brian Dennis

Brian Dennis Christopher L. Jerde

Christopher L. Jerde- 1Department of Ecology, Montana State University, Bozeman, MT, United States

- 2Department of Biology, University of Florida, Gainesville, FL, United States

- 3Department of Mathematical and Statistical Sciences, University of Alberta, Edmonton, AB, Canada

- 4Department of Fish and Wildlife Sciences, University of Idaho, Moscow, ID, United States

- 5Department of Mathematics and Statistical Science, University of Idaho, Moscow, ID, United States

- 6Marine Science Institute, University of California, Santa Barbara, Santa Barbara, CA, United States

Scientists need to compare the support for models based on observed phenomena. The main goal of the evidential paradigm is to quantify the strength of evidence in the data for a reference model relative to an alternative model. This is done via an evidence function, such as ΔSIC, an estimator of the sample size scaled difference of divergences between the generating mechanism and the competing models. To use evidence, either for decision making or as a guide to the accumulation of knowledge, an understanding of the uncertainty in the evidence is needed. This uncertainty is well characterized by the standard statistical theory of estimation. Unfortunately, the standard theory breaks down if the models are misspecified, as is commonly the case in scientific studies. We develop non-parametric bootstrap methodologies for estimating the sampling distribution of the evidence estimator under model misspecification. This sampling distribution allows us to determine how secure we are in our evidential statement. We characterize this uncertainty in the strength of evidence with two different types of confidence intervals, which we term “global” and “local.” We discuss how evidence uncertainty can be used to improve scientific inference and illustrate this with a reanalysis of the model identification problem in a prominent landscape ecology study using structural equations.

1. Introduction

When a person supposes that he knows, and does not know; this appears to be the great source of all the errors of the intellect.

Plato. The Sophist. 360 B.C.E Translated by Benjamin Jowett

One of the main goals of scientific inference is to delineate and understand the underlying mechanism of a phenomenon of interest. In practice, scientists have several different hypotheses or proposed mechanisms, and want to use the observed data to quantify the strength of evidence for one mechanism over the alternatives. The evidential approach to statistical and scientific inference uses estimates of the difference of the divergences from the true mechanism to the competing mechanisms to quantify the strength of evidence in the observed data for one mechanism over the other. The evidence function is an estimator of the sample size scaled divergence difference between two candidate statistical mechanisms (Lele, 2004a). Importantly, evidence functions can be applied pairwise to multiple models to determine the support for multiple alternative mechanisms.

Dennis et al. (2019) demonstrates that evidential inference makes fewer errors than does the Neyman-Pearson hypothesis testing (NPHT) approach at all but the very smallest sample sizes. This is true if the models being compared are “correctly specified.” Evidential inference is even more strongly favored if the model set is “misspecified” (definitions of correctly specified and misspecified model sets follow below). Unfortunately, Dennis et al. also shows that the probability of error depends on the nature of model misspecification and can be large. Ponciano and Taper (2019) demonstrates that the entire geometry of the model set and unknown generating process influences inference. Lele (2020a) discusses that uncertainty in science can be usefully expressed in multiple fashions. The current paper is written as a unifying response to these three papers and will be most clear if read in conjunction with them. The goal of the current paper is to introduce empirical measures of evidential uncertainty that are both valid and estimable in the presence of model misspecification.

Various papers (Lele, 2004a; Taper and Lele, 2011; Taper and Ponciano, 2016; Jerde et al., 2019) discuss the desiderata that an evidence function should satisfy. In comparing a reference model to an alternative, the log-likelihood ratio (LLR) is the most commonly used evidence function. An evidence function is usually constructed so that if the realized value of the evidence function, the observed evidence, is larger than a pre-specified positive threshold value (kR), we say that data strongly support the reference model. If it is below a negative threshold value (kA) (i.e., closer to negative infinity), data strongly support the alternative model. If the evidence function is in between these two thresholds, data are said to be unable to distinguish between the two models.

A commonly used alternative to the evidential framework, Neyman-Pearson tests, accords a special statistical status to the null model in that the type I error probability is fixed (does not depend on sample size) and the p-value is calculated with only the null model. Consequently, a variety of inferential distortions can famously occur when Neyman-Pearson testing is used for purposes beyond its working specifications (Dennis et al., 2019). By contrast, in the evidential framework no special status is accorded either the reference or alternative model. The designations of reference or alternative serve only to help an analyst understand which model is supported (relative to the other) by positive or negative evidence and do not confer any differences in statistical properties. Royall (1997, 2000) considers the situation where the reference and alternative models are fully specified, that is, there are no parameters with unknown values that need to be estimated from the data. Under the assumption that the reference model is the true generating mechanism, he uses the asymptotic distribution of the LLR to compute the probability of misleading evidence, that is the probability that observed evidence would strongly support the alternative (i.e., wrong) mechanism. He also considers the probability of weak evidence, that is the probability of being unable to distinguish between the two mechanisms. Following the results of Godambe (1960), Lele (2004a) shows that, under regularity conditions, among all evidence functions the LLR is optimal in the sense that the rate at which the probability of strong evidence converges to 1 is the fastest. These error probabilities, especially the probability of weak evidence, are useful for pre-experiment decisions on sample size (Strug et al., 2007) or optimal designing of experiments.

Dennis et al. (2019) recognizes the reality that most models are only approximations and hence the true generating mechanism is likely to be neither the reference nor the alternative model. Following Dennis et al. (2019), we consider a model misspecified if the data distribution it predicts cannot be made to match the distribution of the true generating process by appropriate parameterization. A model set is misspecified if all of its members are misspecified. In practice, the model sets used in science are almost always misspecified to some degree and may be badly misspecified particularly during early exploration of scientific phenomena.

The asymptotic distribution of the LLR under model misspecification (Vuong, 1989; Sayyareh et al., 2011; Dennis et al., 2019) depends on the geometry of the misspecification, that is, how the true generating mechanism and the two competing model spaces relate to each other. In scientific studies, instead of fully specified reference and alternative models, one generally has reference and alternative model spaces, a set of parametric models whose parameters need to be estimated using the observed data. Such a set forms a space because its elements have geometrical relationships such as divergences between them. Dennis et al. (2019) uses the asymptotic distribution of the LLR to compute the error probabilities in comparing model spaces when the true generating model might be outside the specified model spaces. The current paper lists all possible topologies, i.e., configurations, for the generating mechanism and competing model spaces and corresponding asymptotic distributions of the LLR. One important feature of these asymptotic distributions is that the means of these distributions increase toward infinity at rates proportional to sample size, n, whereas the standard deviations increase toward infinity at rates proportional to n1/2, producing tail probabilities (probabilities of misleading evidence) that converge to zero (because the coefficient of variation goes to zero). Thus, in all evidential comparisons using the LLR, as the sample size increases, probability of strong evidence for the best approximating mechanism converges to 1 and all other error probabilities converge to 0 (Dennis et al., 2019).

As discussed by Royall (1997, 2000, 2004), this behavior of the error probabilities is in stark contrast to the classical Neyman-Pearson approach where the probability of type I error remains constant for all sample sizes. The consequence to the applied scientist is that the true generating mechanism is rejected in favor of a misspecified null some fraction of the time regardless of the amount of data collected. Of course, classical statistical inference does not stop at hypothesis testing. It also computes the sampling distribution of the estimator of the effect size. Unlike the probability of type I error in hypothesis testing, as the sample size increases, the sampling distribution does concentrate around the true effect size, thus leading to the correct inference. Royall (2000) and Dennis et al. (2019) obtain this sampling distribution asymptotically. Several excellent papers (Linhart, 1988; Shimodaira, 1998; Ng and Joe, 2016) construct confidence intervals for evidence under model misspecification using the asymptotic theory of White (1982) and Vuong (1989). Our experience in simulations is that the distribution of evidence does not approach its asymptotic form until sample size is quite large (Jerde et al., 2019; Taper et al., 2019).

Again, the goal of this paper is to obtain a fuller understanding of uncertainty in observed evidence under realistic sample sizes by estimating the finite sample sampling distribution of the strength of evidence under model misspecification via non-parametric bootstrap. In an earlier paper, Taper and Lele (2011) had suggested the use of non-parametric bootstrap to understand finite sample uncertainty in observed evidence when the true generating mechanism may be different than the reference and alternative models. This current paper is a detailed exploration of this suggestion.

The non-parametric bootstrap is a computational approach (Hall, 1986, 1987; Efron and Tibshirani, 1993) used to get a finite sample approximation to the sampling distribution of a statistic that is valid under model misspecification. Generally, the sampling distribution of the estimator is far more useful for supporting scientific arguments than is a hypothesis test by itself (Xie and Singh, 2013; Schweder, 2018).

An inferential statement is any statement about the model parameters, form of the underlying mechanism, or a future outcome. An inferential statement becomes a statistical inferential statement only when a measure of uncertainty is attached to it (Cox, 1958). An accessible review of various approaches to quantifying uncertainty in an inferential statement is available in Lele (2020a). The classical frequentist inference uses aleatory probability (frequency of an event under hypothetical infinite replication of experiment) to quantify uncertainty of an inferential statement. To obtain the aleatory uncertainty of an inferential statement, a critical question that needs to be answered is: which experiment/sampling design do we (hypothetically) repeat? Lele (2020a) uses the simple linear regression model to illustrate the distinction between the global (also known as unconditional, pre-data or, pre-experiment) and local (also known as conditional, post-data or, post-experiment) uncertainty. In this paper, we augment that illustration by comparing the differences between global and local uncertainty in mark-recapture analysis and in structural equations.

Although the unconditional/conditional distinction has been in the theoretical statistics literature since Fisher (1936), the difference has not been well understood by ecologists and scientists in general. To the extent that the difference has been recognized at all it has been common to ascribe unconditional inference to frequentists and conditional inference to Bayesians. However, we agree with Goutis and Casella (1995) that: “In any experiment both pre-data inferences and post-data inferences are important, and each can be made within either frequentist or Bayesian paradigms, which perhaps shows that the frequentist/Bayesian distinction is not as fundamental as the pre-data/post-data distinction.”

In the ecological literature, both kinds of intervals have been used, often without an awareness of the distinction. This is a mistake, because the two kinds of intervals answer different scientific questions. In the discussion, we expand on the interpretation of the two intervals.

Here we consider the evidential approach to model selection under model misspecification. As was described in Dennis et al. (2019), the reference and the alternative models are not fully specified. There are parameters with values that need to be estimated and hence the set-up discussed in Royall (1997) must be altered. Because these two competing models may involve different number of parameters, an unmodified LLR is not an appropriate evidence function, and the LLR needs to be penalized for the number of parameters to be estimated (Akaike, 1973). Furthermore, to make the error probabilities of misleading and weak evidence to converge to 0 as sample size increases, we also need to moderate the penalty by a function of the sample size that grows to infinity at a rate between log(log(n)) and n (Nishii, 1988). The appropriate evidence functions for the model selection problem are based on the consistent information criteria (IC) such as the Schwarz’s Information Criterion (SIC)1 (Schwarz, 1978) that incorporates both the sample size and the number of parameters in its penalty term. Inconsistent criteria, such as the Akaike Information Criterion (AIC), tend to overfit at all sample sizes and do not lead to valid evidence functions due to the absence of an augmentation of the penalty by the sample size. Note that despite having a sample size correction, the AICc (Hurvich and Tsai, 1989) is not consistent. Its sample size correction is aimed at correcting small sample bias, not large sample inconsistency. We will return to this point in the discussion.

All of the above measures are based on the Kullback-Leibler divergence. However, one can potentially use any divergence measure and with appropriate (i.e., consistent) sample size and parameter number penalty function, one can create a valid evidence function. The evidence function is, as will be made clear later, a scaled and penalized difference between the estimates of divergences of two models each to the generating process.

In this paper, we show that model selection based on a bootstrap bias corrected information criterion known as the extended information criterion (EIC) (e.g., Kitagawa and Konishi, 2010) is strongly connected to various bias corrections of the profile likelihood (e.g., Pace and Salvan, 2006). We combine these two ideas with the use of a consistent penalty and show that a non-parametric bootstrap approach can be used to obtain finite sample and consistent estimates of global and local uncertainty in the observed strength of evidence for the reference model vis-à-vis the alternative model. The mathematical details are given in Section 4. As a consequence of this development, we will use as our evidence function the mean of a bootstrapped distribution of ΔSICs.

Pace and Salvan (2006) and Kitagawa and Konishi (2010) use the bootstrap only for computing the bias correction factor. In contrast, we also use the entire sampling distribution to obtain valid, finite sample, global and local confidence intervals for the strength of evidence. That is, our confidence intervals will also be based on the quantiles of a bootstrapped distribution of ΔSICs.

These confidence intervals are extremely helpful in drawing scientific conclusions (Tukey, 1960). For example, if most of the sampling distribution is above the threshold, we have not only strong evidence, but it is also very unlikely to be strong by chance. We define such evidence as secure. If the sampling distribution is such that a substantial portion is below the threshold, the observed evidence may be strong, but it cannot be considered secure, and more data may be needed to clarify the situation.

Hoping to stimulate practicing scientists with the utility of our approach before they encounter the mathematics of our methods, this paper proceeds as follows: In Section 2, we discuss the implications of uncertainty in evidence and the use of sampling distributions of the strength of evidence in drawing scientific conclusions in detail. In Section 3 we apply these ideas in a reanalysis of a prominent ecological experiment analyzed using structural equations models (SEM) and discuss the scientific implications of the uncertainty in the strength of evidence. Section 4 describes the underlying mathematical concepts and the methodology for computing finite sample, global and local sampling distributions of the strength of evidence for model selection. In Section 5, we validate the methodology using simulations for model selection in linear regression. In Section 6, we discuss implications of the uncertainty quantification of the strength of evidence for the pursuance of science and suggest avenues for further research. Section 7 concludes.

2. Scientific Inference Under Evidential Uncertainty

First, we note that simulations as well as the analytical results in Dennis et al. (2019) show that the sampling variability in evidence can be substantial. Hence using empirical evidence without a measure of uncertainty can be dangerous in practice leading to overconfidence, wrong decisions, misleading inferences, and misguided scientific enquiry. Furthermore, under model misspecification, evidence functions, such as the LLR and others become detached from model-based estimates of error probabilities and are just measures of relative plausibility (Barnard, 1949; Fisher, 1922, 1960; Sprott, 2000). Non-parametric confidence intervals on the strength of inference then allow us to reattach our inferences to probability measures, although there is a considerable difference in what those probabilities mean between global and local inference. Before discussing the methodology to quantify global and local uncertainties in evidence and their real-world applications, let us first discuss how the sampling distribution of the strength of evidence could be used to draw scientific conclusions.

Royall (1997) considers three categories of strength of evidence: Strong evidence for a reference model, strong evidence for the alternative model, and weak evidence when the strength of evidence cannot distinguish between the two models. Often in ecological analysis, one finds the strength of evidence that is neither so weak that one feels comfortable saying one cannot distinguish between the models nor so strong that one is willing to stake a reputation on it. Hence, we suggest using five categories for strength of evidence, inserting categories of prognostic evidence for the reference model and prognostic evidence for the alternative. See Box 1 for a more complete discussion.

BOX 1. Categories of strength of evidence.

Often in ecological analysis, one finds evidence that is neither so weak that one feels comfortable saying one cannot distinguish between the models at all nor so strong that one is willing to stake a reputation on it. Thus, to the thresholds kA and kR we add the thresholds ka and kr. Evidence between the thresholds kA and ka and between kr and kR could reasonably be called moderate, but to avoid a clash in abbreviations with the error category of misleading evidence, we will call such evidence prognostic. Now evidence is divided into five categories: strong evidence for the alternative model, prognostic evidence for the alternative model, evidence so weak that it is best to say that neither model is favored, prognostic evidence for the reference model, and strong evidence for the reference model.

(1) Strong evidence for the reference model if the strength of evidence is larger than kR.

(2) Prognostic evidence for the reference model if the strength of evidence is between kr and kR.

(3) Weak evidence favoring neither model if the strength of evidence is between ka and kr.

(4) Prognostic evidence for the alternative model if the strength of evidence is between kA and ka.

(5) Strong evidence for the alternative model if the strength of evidence is less than kA.

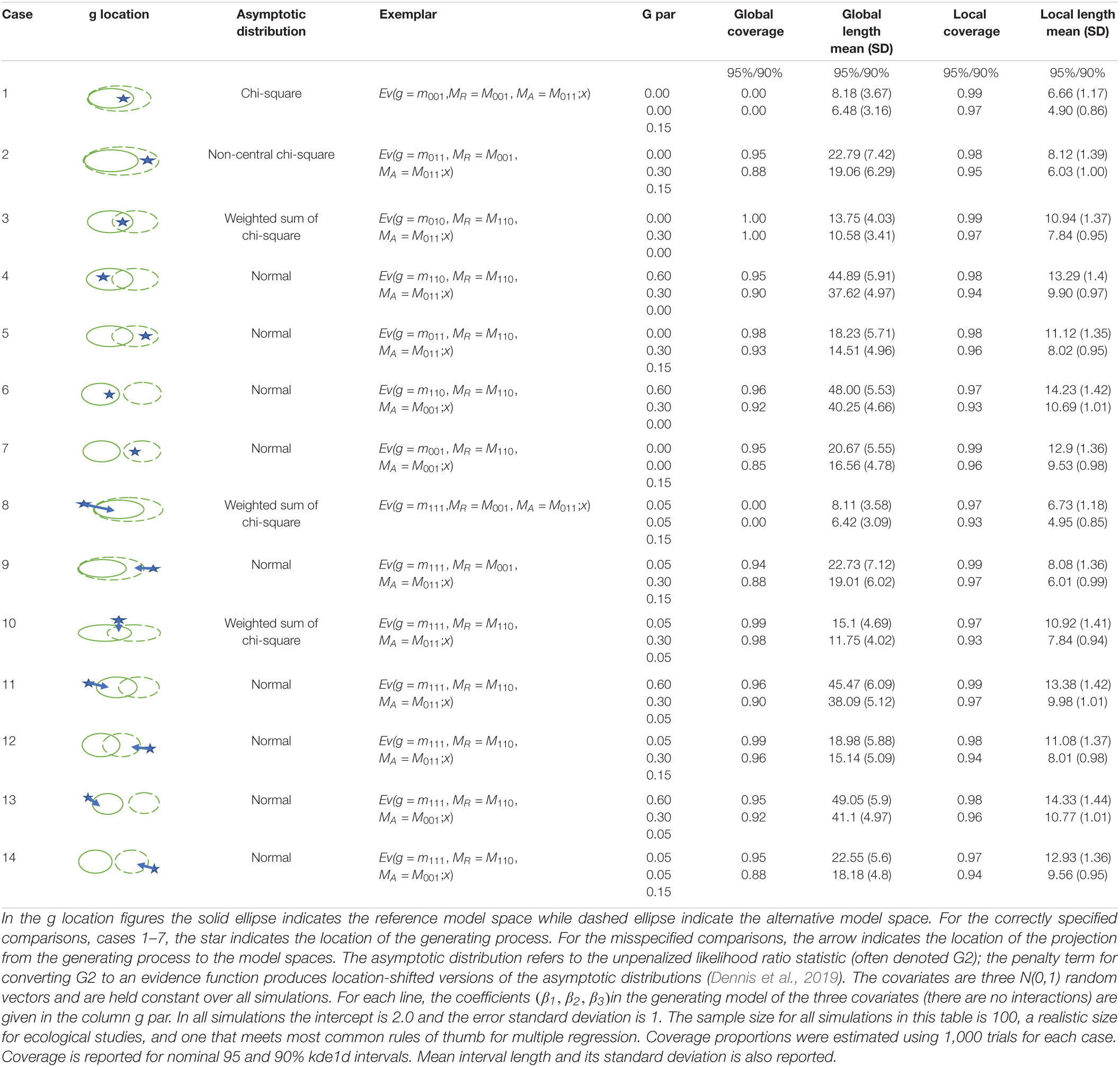

Royall (1997) pointed out that on occasion, one can have strong evidence that one model, say the reference, in your comparison is closer to the generating process than the other, say the alternative, when in fact it is the alternative that is truly closer to the generating process. Royall called such counterfactual evidence “misleading.” With the weaker category of prognostic evidence, it is even more likely that evidence that is counterfactual will be estimated. We designate counterfactual prognostic evidence as “confusing evidence.” With real data, one does not know if strong evidence is in fact misleading, or if prognostic evidence is confusing. However, in design and validation studies, whether analytic or computational, the researcher does know when evidence is misleading or confusing, and these categories are very helpful (see Section 5).

It is important to realize that the sign of evidence only indicates which model is estimated to be closer to the generating process, positive for the reference model and negative for the alternative. Previously in the literature, kA has been set symmetrically to −kR. In specific cases, there could be reason for asymmetry in thresholds, either because of asymmetry in probability models or because of decision cost. For simplicity, we adopt symmetric thresholds with −kp and kp indicating the thresholds between weak evidence and prognostic evidence for the alternative and reference models respectively. Similarly, −kS and kS are the thresholds between prognostic evidence and strong evidence for the alternative and reference models. The boundaries for our categories then become: strong evidence for the alternative = −kS, prognostic evidence for the alternative = −kp, prognostic evidence for the reference = kp, and strong evidence for the reference = kS. Jerde et al. (2019) discuss interpretations for levels of evidence. Following their recommendations, we define kp ≡ 4 and kS ≡ 7.

While we have introduced thresholds, it is important to realize that these are not the absolute accept/reject thresholds of NPHT. They create descriptive categories to help us think, like the names of colors. Light with a wavelength of 521 nm is called a green while that with a wavelength of 519 is called a cyan, but the difference is slight. These thresholds should be thought of “as more what you call guidelines, than actual rules”2 (Bruckheimer and Verbinski, 2003).

We note finally that Dennis et al. (2019) used a reversed direction for the evidence scale, in order to compare more clearly evidence analysis with Neyman-Pearson hypothesis testing. Dennis et al. posed a correspondence between the reference model in evidence analysis and a NPHT null hypothesis, along with a correspondence between the alternative models, to study error properties of the two analysis approaches. It was convenient to define evidence strength for the alternative to increase as the evidence function moved in the positive direction (by simply reversing the difference of SICs) instead of the negative direction. This defined evidence for the alternative model to be in concordance with the direction favoring the alternative hypothesis in NPHT according to the generalized likelihood ratio statistic (G2), allowing easy study of errors with the well-known asymptotic distributions of G2. Either direction for evidence favoring the alternative model can be used provided one stays consistent within an application. In the present paper, it is convenient to adopt the convention described earlier in this box, because errors will be estimated by bootstrapping rather than by asymptotic distributions of G2.

One final difference between Royall’s characterization of the strength of evidence and our characterization is that Royall considered the strength of evidence a ratio of likelihoods. We, on the other hand always consider strength of evidence as differences on a logarithmic scale (see discussion in Barnard, 1949). This ties our conceptualization more closely with information theory and the comparison of divergences.

This seemingly small difference marks large differences between our current understanding and that expressed in Royall (1997). We differ from Royall primarily in two intertwined but distinct issues. The first is the utility and scope of the “likelihood principle” (LP). And the second is the usefulness of measures of “pre-data” and “post-data” uncertainty.

Royall’s (1997) evidence is developed axiomatically from the “likelihood principle” (Birnbaum, 1962). We do not deny the likelihood principle within the context it was originally stated: “We deliberately delimit and idealize the present discussion by considering only models whose adequacy is postulated and is not in question” (Birnbaum, 1962). Unfortunately, this means that the likelihood principle and everything that follows from it is silent on what happens if models are at all misspecified. We agree with Sprott (2000, p. 105) that “Since few scientists would claim that the model and surrounding assumptions are exactly correct, particularly in the latter situation, the domain of scientific application of LP seems extremely narrow.”

We develop evidence as the difference of estimates of the distance of a modeled distribution to the generating process’s distribution. This definition is compatible with model misspecification. Further, as we have previously demonstrated (Lele, 2004a; Taper, 2004; Dennis et al., 2019 in this research topic), under correct model specification, along with both models being simple hypotheses (i.e., no parameters with unknown values), this definition is compatible with the Royall’s likelihood ratio definition of evidence, if one uses the Kullback-Leibler divergence as a distance measure. We also suggest and use distances that are different from KL distance. That negates the likelihood principle in its purest form. For example, design seems to play a role (Lele, 2004a; and our discussion in Section 6).

Royall’s commitment to the likelihood principle entails a stance supporting the irrelevance of uncertainty estimates of evidence based on sample space probabilities, such as pre- and post-data error probabilities. Nevertheless, Royall sets great stock by his argument that you don’t need to worry about the probability of misleading evidence post data, because it will always be small if the LR evidence is large. Royall’s argument falls short when there are parameters with values to be estimated and/or when there is model misspecification. We have previously argued (Taper and Lele, 2011; Dennis et al., 2019) that pre- and post-data measures of uncertainty are useful for scientists to think about. Even in the correct specification case where the (post-data) probability of misleading evidence is bounded by 1/LR, other uncertainty measures are useful for study planning and probing the extent of the results. In the more usual case of model misspecification, estimation of the probability of misleading evidence is not simply a matter of transforming the evidence. We have shown (Dennis et al., 2019) that it also depends on the geometry of the model set and the generating process. Importantly, the probability of misleading evidence is not guaranteed to be small—it can be as large as 0.5. Thus, measures of the uncertainty of evidence are a critical complement to an estimate of evidence. Further, to be useful, such measures must be estimable in the presence of model misspecification. In this work, we show that non-parametric bootstrap greatly expands the options, capabilities and the nature of the inferential problem under which estimating these measures is possible.

We are not alone in our insistence on a measure of uncertainty in evidence. Alan Birnbaum, after being an early advocate of Hacking’s (Hacking, 1965) LR formulation of statistical evidence, strongly repudiated it in Birnbaum (1970, 1972) on the grounds of its lack of confidence measures.

If there has been ‘one rock in a shifting scene’ or general statistical thinking and practice in recent decades, it has not been the likelihood concept, as Edwards suggests, but rather the concept by which confidence limits and hypothesis tests are usually interpreted, which we may call the confidence concept of statistical evidence. This concept is not part of the Neyman-Pearson theory of tests and confidence region estimation, which denies any role to concepts of statistical evidence, as Neyman consistently insists. The confidence concept takes from the Neyman-Pearson approach techniques for systematically appraising and bounding the probabilities (under respective hypotheses) of seriously misleading interpretations of data. (The absence of a comparable property in the likelihood and Bayesian approaches is widely regarded as a decisive inadequacy.) Birnbaum (1970)

We believe that the current paper rehabilitates statistical evidence by coupling it with an estimate of confidence.

2.1. Understanding Global and Local Uncertainty in Evidence

Confidence intervals are a mainstay in ecological inference, increasingly and justifiably so (Johnson, 1999; Ponciano et al., 2009; Halsey, 2019; Holland, 2019; Fieberg et al., 2020). They transmit a more complete and interpretable representation of the information in data than do hypothesis tests. A confidence interval is a range of values for a statistic, a function of the data, that is expected to cover (capture, include) an estimation target a given per cent of the time (e.g., 95%) under repetition of a specified hypothetical experiment (Neyman, 1937). The target of an interval is something in nature about which we would like to make an inference such as a population parameter or a function of a parameter.

For evidence, there are both local and global intervals that can be calculated (see Section 4 for details). In order to understand confidence intervals for evidence, it is important to realize that not only are the interval widths different, but that the targets are also different.

The global target is the difference between the divergences of the best possible representations of the two models to the natural generating process. The uncertainty in the global interval includes the sampling uncertainty for the data, model estimation uncertainty given the data, and uncertainty due to model set misspecification.

The local target is the evidence in the observed data for the best possible representation of one model over the best possible representation of the other model. The uncertainty in the local interval represents just the model estimation uncertainties given the observed data, and uncertainty due to model set misspecification.

Global intervals reflect the variation in the estimates if independent experiments are conducted in a manner like the original experiment. The local intervals reflect the informativeness of the specific experimental outcome in hand.

The local interval can capitalize on lucky samples to make precise inferences about the strength of evidence for the reference model relative to the alternative model. On the other hand, with unlucky samples where the parameter estimate may be far from the truth, the local intervals also end up making precise but misleading inferential statements. Global intervals, because they average over all possible datasets, tend to be wider than the local intervals. They are conservative in their uncertainty quantification, making strong inferential statements only cautiously. That does not mean that the global intervals are without use. Scientific results need to be validated by independent replication. A global interval indicates how discrepant the results of a repetition of the experiments could be from the original before contradicting your results and hence protects against the possibility of being contradicted. A worked example of global and local intervals in a mark recapture analysis can be found in Box 2.

BOX 2. Global and local intervals in mark/recapture analysis.

In ecology, where uncertainty in the study systems is ubiquitous, it is common practice to formulate a scientific hypothesis in the form of a simplified probabilistic model of how the data arose. This simplification allows the analysts to focus the inferential process on a typically small set of quantities bearing strong ecological or management importance. Such simplifications are in fact conceptual restrictions on how the data arose and are used to formulate the likelihood function. Multiple uncertainty simplifications/restrictions are incorporated in the form of multiple conditioning layers. Take for instance a simple closed population mark-recapture experiment where in a first visit to a study area, a number of animals of the species of interest are marked and released. In a second visit, a sample of animals from the same population are captured and the number of previously marked animals in that sample recorded. Under that setting, different levels of conditioning restrict more and more the sampling uncertainty while keeping the focus on the same inferential quantity of interest—the total population size. We prefer the terms “global’ and “local” because they evoke the scope of inference that can be addressed by each type of uncertainty. The sampling distribution for global uncertainty is computed using the entire sample space whereas “local” uncertainty is computed using a relevant subset of the sample space (Buehler, 1959).

The key question in global and local inference is what components of your data do you want to be considered fixed (or given) and what components do you want to be considered random (or representative). A completely unconstrained interval is considered global. Intervals with constraints are considered local. An alternative way of approaching this question, which may be clearer for some, is to recognize that a confidence interval represents the variability in hypothetically repeated experiments. When you treat a component as fixed or random, you are specifying different hypothetical experiments. One of the goals of confidence intervals is to define what estimates a skeptic who tries to replicate the experiment might obtain. Different types of experimental conditions that the skeptic might use dictate the choice of the interval.

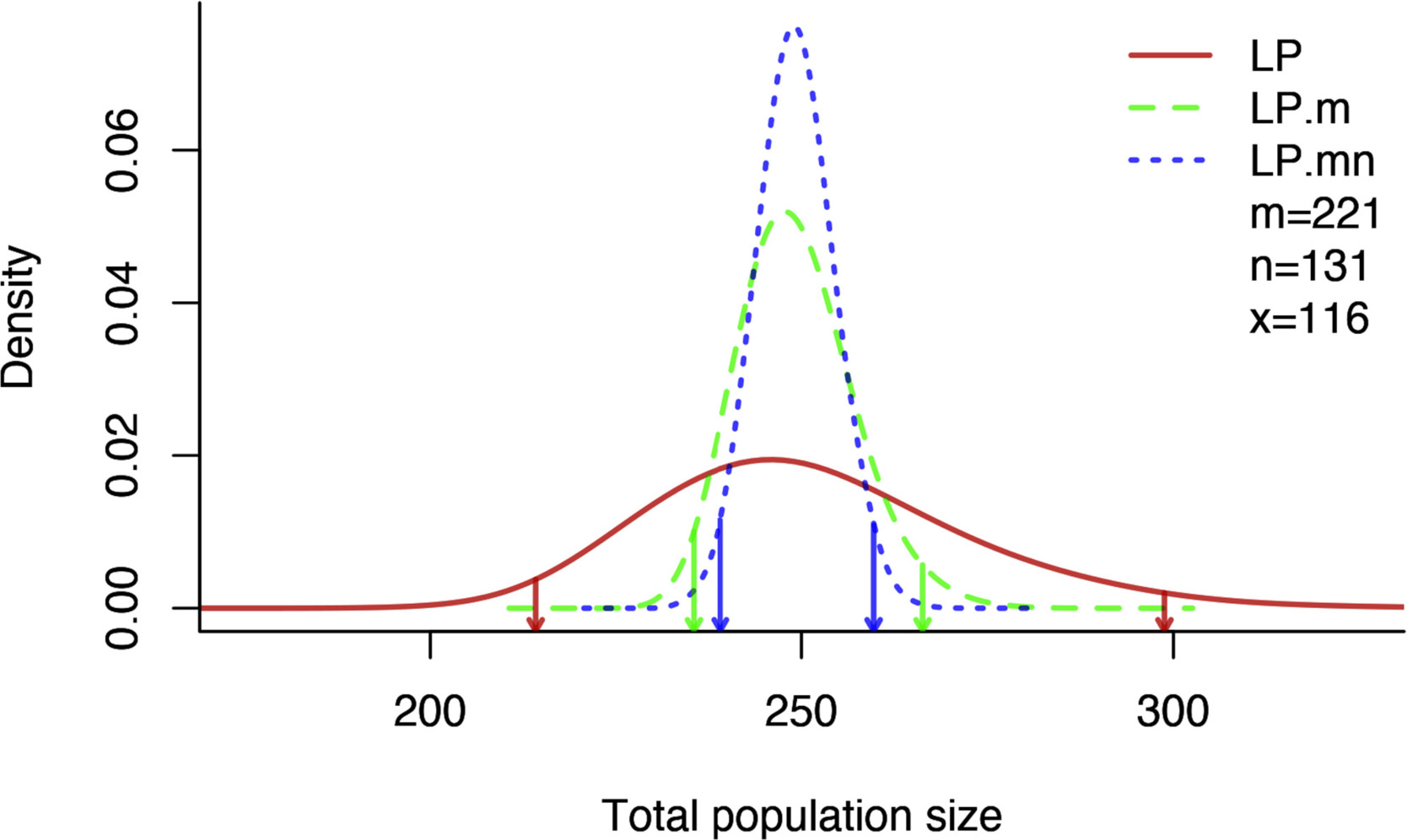

We illustrate the concepts of global and local inference using the familiar problem of population size estimation using the Lincoln-Peterson estimator. We use the data from a published experiment on iguana population density to create a realistic framework along with some R commands to demark the global and local differences clearly in the calculations. The data and a more complete treatment can be found in Powell and Gale (2015).

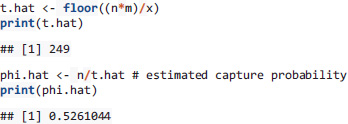

Below is a mark-recapture data set, describing one re-sampling occasion. On day 3 of their experiment 131 individuals, n, are captured and 116, x, of these have previously been marked. Initially (days 0, 1 and 2) m = 221 individuals have been captured, marked and released:

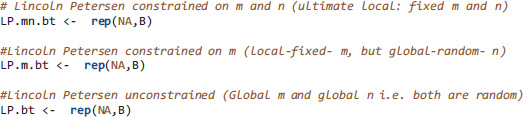

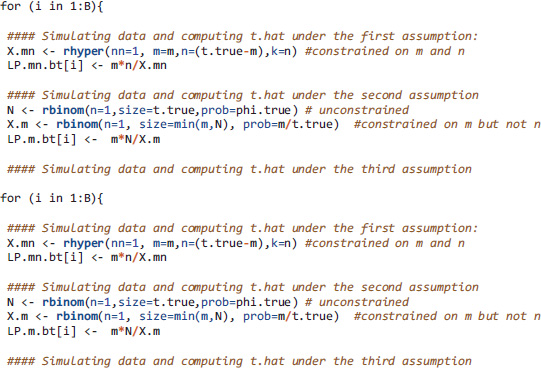

From these data we estimate a total population size using the Lincoln-Petersen estimator. Thus, the target for point and interval estimation is the true population size. As it happens, the same estimator is obtained whether you assume that: (1) Both m and n are fixed. (2) m is considered fixed, but n is not. And (3) Both m and n are considered random.

While the estimate of the total population for these three cases is identical, the uncertainty around it is not. Each set of assumptions fully determines the confidence intervals. We demonstrate this via parametric bootstrap (PB) because of how the levels of randomness enter at each stage is much more perspicuous in the PB code than in the corresponding analytic formulae.

Parametric Bootstrap

Compute the Lincoln-Petersen estimator for the sample at hand as well as the nuisance parameter phi.hat (the capture probability)

Now let’s set our PB simulation parameters to these two estimates:

Next, set the total number of simulations

and then create empty arrays to store the three types of estimates

Finally, just turn the crank on the PB iterations and store them:

It is instructive to look at the sample spaces for these three estimators:

The sample spaces are all possible data sets that the simulations could generate under each of the model assumptions. The sample space for LP.m.bt is nested within that of LP.mn.bt, which is itself nested within the sample space of LP.bt. Clearly, global and local are relative terms. LP.m.bt is local with respect to LP.bt, but global with respect to LP.mn.bt.

The sampling distributions for the three estimators are plotted in the figure below. We now have three different confidence intervals. Which is right? Statistics by itself cannot answer that question. These three intervals represent the uncertainty in the hypothetical repetition of three different experiments. In the type 1 experiment, with m and n constrained, the only thing that can vary experiment to experiment is the number of marked animals in the final day sample.

In type 2, the number of previously marked individuals is constrained but not the final day sample size. The hypothetical experiment is repeated only for the final day; varying numbers of individuals as well as varying numbers of marked animals may be captured on the final day. In type 3, the entire hypothetical experiment is repeated. The number of marked individuals, the number of captured individuals, and the number of marked individuals in the second sample may all vary.

The appropriate interval depends on the kind of uncertainty you are trying to represent. The first interval answers the question: How different the estimators of the total population could be if someone else replicated the experiment such that the total number of marked individuals and total number of captures are identical to your experiment? This can happen in a field survey where the total number of marked animals and total number of captures is fixed by design, a priori. These numbers may depend on the budget the researcher might have for capturing animals for marking and for recapturing.

In some situations, such as camera trap surveys, the total number of marked animals may be fixed by design but the total number of captures, by the nature of the survey technique, is random. The second interval considers this possibility and allows for the randomness in the number of captures to compute the uncertainty in the total population size estimator. In the case of fish surveys, the number of fish caught in the traps or by electrofishing for marking is necessarily random and so is the number of fish in the sample afterwards. In this case, the third interval will be appropriate.

Figure Box 2.1 Sampling distributions and 95% confidence intervals of total population size estimates for three levels of conditioning in Lincoln Peterson estimates. The ML estimate for all three models is 249. The confidence 2.5 and 97.5% limits are indicated by the vertical lines dropped from each curve to the x-axis. The intervals become increasingly shorter as the models (hypothetical experiments) become more constrained. Here, as is generally but not universally the case, the intervals are completely nested.

2.2. Interpreting Evidential Uncertainty

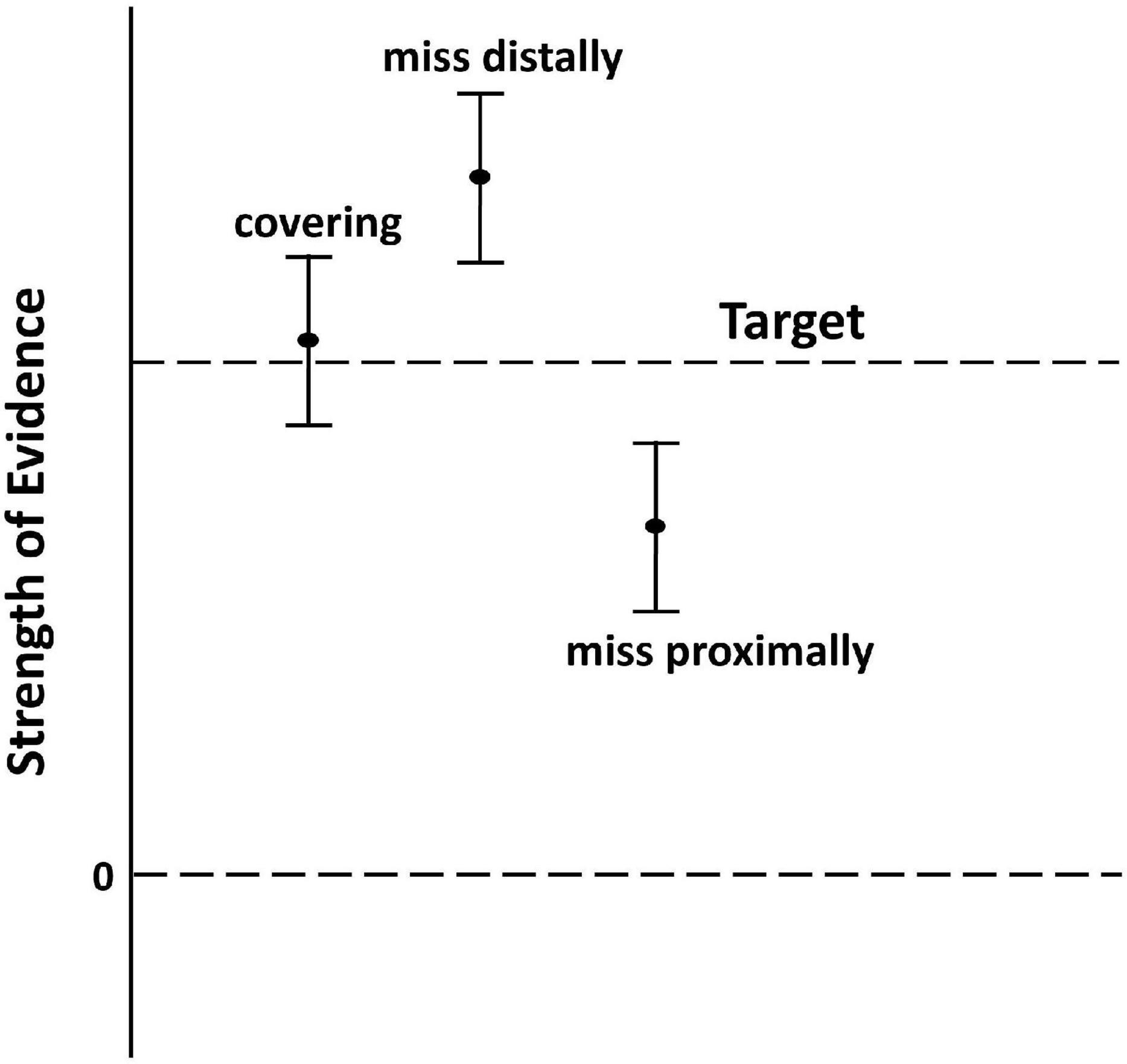

Generally, desirable properties in confidence intervals are proper coverage and given proper coverage, shortness of length (Casella and Berger, 2002). A confidence interval can either cover the target or it can miss it. If the interval fails to cover the target, it can either be entirely above the target (miss high) or entirely below it (miss low) (see Figure 1). It is often, but not always, considered desirable if intervals that miss the target value are distributed equally above and below it. Evidence is one of the cases where an equal distribution of non-coverage is undesirable. In this context missing high is superior to missing low. Both types of intervals misrepresent the confidence one should have in the evidence, but the high miss is at least always indicating a correct assessment while a low miss could be supporting an incorrect assessment. Of course, this is assuming the expected evidence is positive, as in Figure 1, if the expected evidence were negative, the desirability of missing high and low would be reversed. Really, we mean that it is better for the interval to miss its target distally from 0 than to miss proximally to 0. However, in this simulation study the evidential comparisons are arranged so the reference model is always the better model as to keep the language of missing high and low less confusing.

Figure 1. Hypothetical coverage of confidence intervals for evidence. The strength of evidence is the value of an evidence function relating two models and a data set. Typical evidence functions are LLR or the difference of information criterion values, ΔICs. In our worked example (Section 3) we use the Schwarz information criterion. ΔSICRA values greater than 0 indicate support in the data for the reference model relative to the alternative. These values are indicated by dots in the figure. The vertical bars indicate confidence intervals for the strength of evidence. The target for a confidence interval on the strength of evidence is a penalized scaled divergence difference (see Section 4.1), loosely this is the expected evidence. By design, a perfect confidence interval, at say the 95% confidence level, will fail to cover its target 5% of the time. If a confidence interval that misses its target is entirely more distant from 0 than is its target, we say that it misses distally, otherwise we say that it misses proximally. We will also speak of the bound of a confidence interval for evidence that is closest to 0 as the proximal bound.

The categories of evidence introduced in Box 1 suggest useful ways to apply confidence intervals for strength of evidence to scientific inference. Scientifically, the paramount question is: is the evidence veridical (i.e., in agreement with fact) or is it misleading? The intervals we propose estimating can give us confidence in our answer. We propose that if the proximal bound of this confidence interval is distal to kS that it be considered “very secure.” If the proximal bound falls between kS and kp then the evidence should be considered “secure.” Finally, if the proximal bound is proximal to kp or the interval overlaps 0 the evidence is “insecure.”

These three levels of strength of evidence and two levels of security of evidence create six heuristic categories:

1. Strong and very secure (SV): The point estimate of evidence (e.g., ΔSIC) is strong and the lower bound of uncertainty indicates that we have confidence that the target (true evidence) is also strong.

2. Strong and secure (SS): The point estimate of evidence is strong, and we are confident that the true target is at least prognostic. There is very little chance that this evidence is misleading.

3. Strong but insecure (SI): The point estimate of evidence is strong, but we cannot be confident that the target is not weak.

4. Prognostic and secure (PS): The point estimate of evidence is prognostic, and we can be confident that the target is at least prognostic.

5. Prognostic but insecure (PI): The point estimate of evidence is prognostic, but we are not confident that the target is not weak.

6. Weak and insecure (WI): The point estimate of evidence is weak and thus by definition, we are not confident that the target is not weak.

As sample size increases, a majority of the sampling distribution lies above the strong evidence threshold and the probability of obtaining evidence that is not SS diminishes to 0 (Dennis et al., 2019). There is, of course, the pathological case where two models are equally divergent from the true generating process. Were this curiosity ever to occur, then each model would be strongly and securely selected with probability 0.5. It is arguable that, even in such a situation, no error has occurred, as in each case a model closest to the generating process has been selected. Substantial discussion on interpreting statistical evidence when augmented with confidence intervals is given in Box 3.

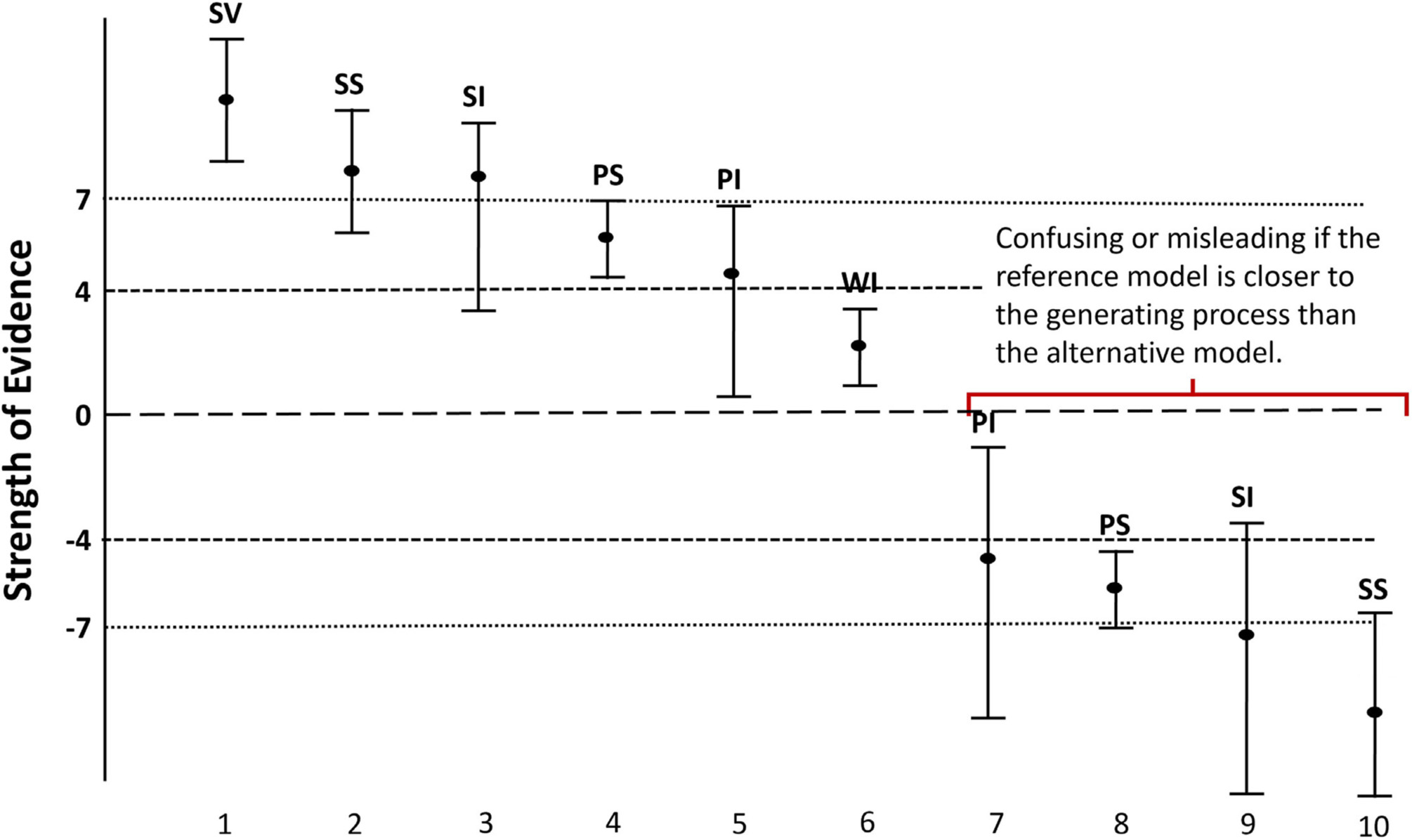

BOX 3. Interpreting evidence using confidence intervals.

Figure Box 3.1 depicts some hypothetical confidence intervals for the strength of evidence. The boundaries for the evidential categories are set as: strong evidence for the alternative = −kS = –7, prognostic evidence for the alternative = −kp = –4, prognostic evidence for the reference = kp = 4, and strong evidence for the reference = kp = 7.

In interval 1, the observed evidence (e.g., ΔSIC), indicated by the filled oval, is strong and the lower bound for the confidence interval is above the strong evidence threshold. This evidence is designated strong and very secure (SV)—the reference model is strongly supported as being closer to the generating process than the alternative and there is almost no chance that sampling variation would upset this identification. In this case, the researcher may reasonably conclude that no further work is needed regarding model identification in this particular model contrast. Possibly, further work may be indicated to improve parameter estimate precision in the identified better model.

In interval 2, the observed evidence is above the strong evidence threshold, and the proximal bound is greater than the prognostic evidence threshold. We call this situation “strong but secure” (SS). This implies that the reference model is strongly supported, and it is unlikely (but plausible) that this is due to sampling variation. Cautious but optimistic interpretation is indicated, and if possible, more data should be collected to confirm the conclusions.

In interval 3, the observed evidence is above the strong evidence threshold, but the proximal bound is less than the prognostic evidence threshold. We call this situation “strong but insecure” (SI). This implies that while the reference model is strongly supported, it is uncertain due to sampling variation. Very cautious interpretation is indicated, and if possible, more data should be collected to confirm the conclusions.

In interval 4, the observed evidence is less than the strong evidence threshold, and the proximal bound is greater than the prognostic evidence threshold. We call this situation “prognostic but secure” (PS). This implies that while the reference model has only moderate support, it is unlikely that this is due to sampling variation. In this case, the distal bound is less than the strong evidence threshold. It is likely that both models explain the data nearly equally well, but with a slight edge to the favored model.

In interval 5, the observed evidence is less than the strong evidence threshold, and the proximal bound is less than the prognostic evidence threshold. We call this situation “prognostic but insecure” (PI). This implies that the reference model has only moderate support and even this may be due to sampling variation. The primary implication is that more data is needed either within the context of the current experiment or by combining these results with the results of other experiments.

In interval 6 the evidence is weak and insecure (WI). The models are not differentiated by the data. The researcher should collect more data in order to identify the models. The researcher should of course recognize that not all data is equally informative and seek data that will distinguish the two models (e.g., Cooper et al., 2008). Another choice that could be made, particularly if large amounts of data have already been collected, is to decide that both models are adequate for the intended purposes (Lindsay, 2004; Markatou and Sofikitou, 2019).

Intervals 7, 8, 9, and 10 are reflections of intervals 5, 4, 3, and 2, only in this case they are misleading. The designation C stands for confusing evidence, which is prognostic evidence for the wrong model. The designation M stands for misleading evidence, which is strong evidence for the wrong model.

Interval 10 is a researcher’s worst case. The evidence is strong, secure and misleading. The researcher should try to avoid this situation both by experimental design (large sample size, treatments or observations that strongly differentiate between the models) and by analytic design (higher strong and marginal evidence thresholds).

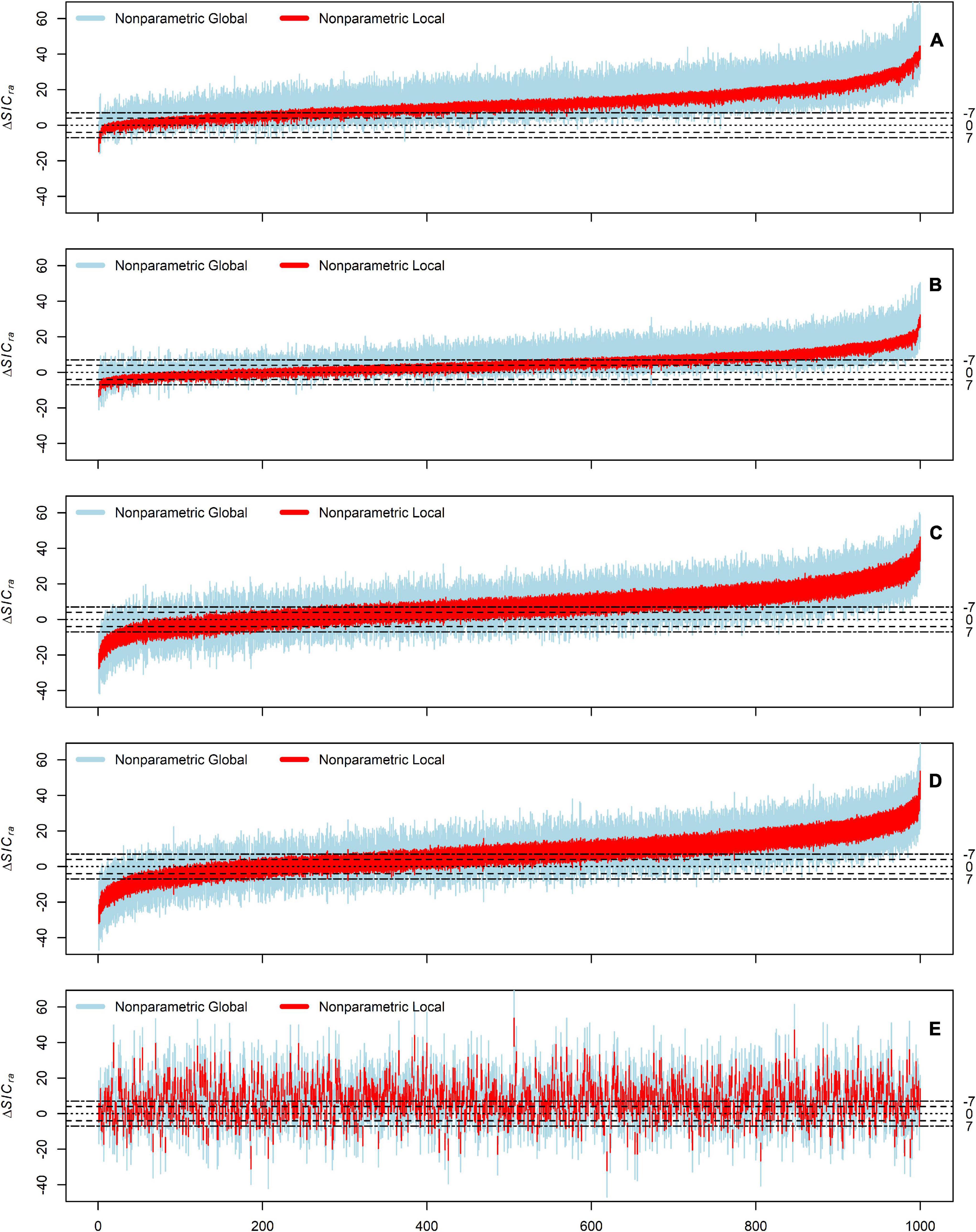

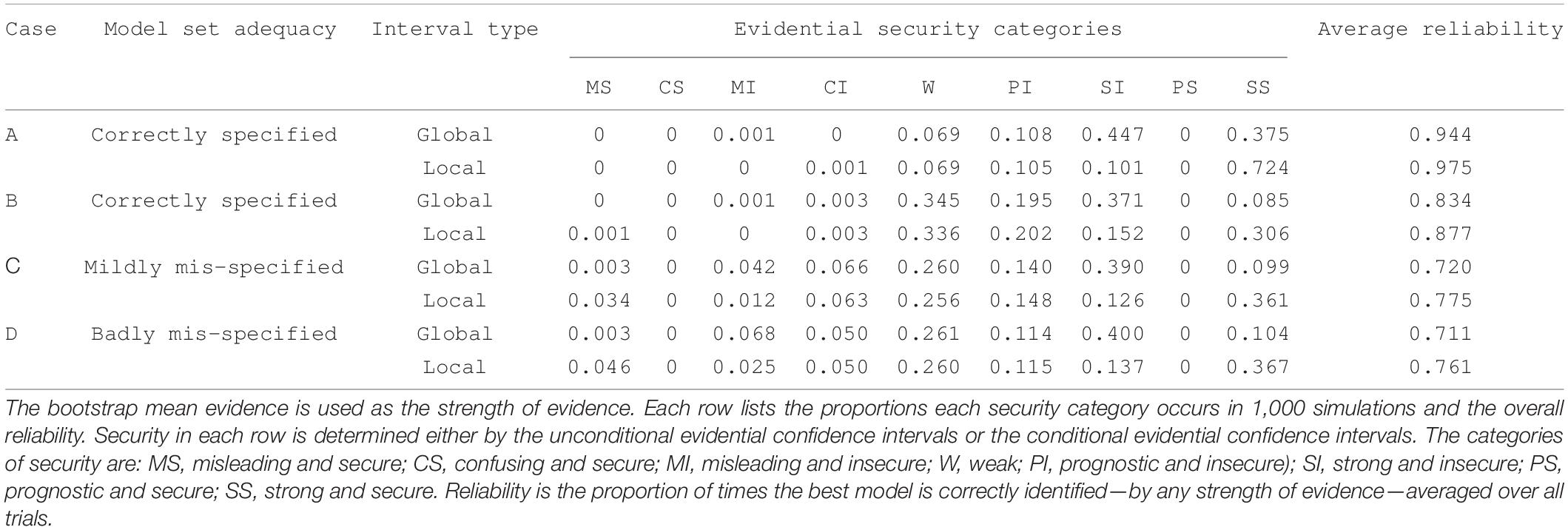

In practice, we do not know if the evidence is misleading or not. For this discussion, we consider “negative” evidence as misleading but in fact, it only indicates that it supports the alternative model—unless one knows the location of the generating process (see Ponciano and Taper, 2019). Simulations (Section 5.2 and Taper et al., 2019) show that for global evidence strong but secure misleading evidence occurs very rarely—regardless of whether the model set is correctly specified or misspecified. For local evidence if the model set is correctly specified, secure misleading evidence is exceedingly rare. However, under model misspecification secure misleading evidence occurs more frequently, although it is still not common. We present an explicit comparison of global and local inference under correctly specified and misspecified models in Section 5.2.

3. Example: Uncertainty in a Structural Equations Models Analysis of Post-Fire Recovery of Plant Diversity

To probe the effectiveness of bootstrapping evidence in realistically complex problems, we revisit the classic analysis of Grace and Keeley (2006). These authors used structural equation modeling to study the impact of landscape, environment, and community factors on the recovery after fire of shrubland plant diversity.

A recent article on developing causal models (Grace and Irvine, 2020) revisits the 2006 study and takes a more moderate stance than the original paper: “Subsequent SEM studies (Keeley et al., 2008) have enhanced our confidence in the general inferences drawn from the original study. That said, we would not claim that all our parameter values are unbiased causal estimates without further evidence to support such inferences.” We believe that had Grace and Keeley had the tools for estimating the two kinds of evidential uncertainties we have developed here a much more nuanced understanding could have been gained—even from the original data—as to which paths were likely to be supported by future work and which were potentially non-replicable.

3.1 Example Choice

There are reasons why SEM is growing in influence in environmental informatics, ecology and evolution. First, SEM allows for legitimate causal inference in situations both in observational studies (Grace, 2008; Bollen and Pearl, 2013; Grace and Irvine, 2020) and where experimental manipulation has been performed (Grace et al., 2009; Breitsohl, 2019). In fact, path analysis, the precursor to SEM, was first developed by Sewall Wright (1934) to expose causal effects to statistical inference. Second, because it is designed for estimation of a network of causal effects, SEM is well suited for analyses of the complex patterns of influence often found in environmental science, ecology and evolution (e.g., Grace and Pugesek, 1997). Third, SEM recognizes that many observables may be recorded with measurement error (Bollen, 1989). The ability to incorporate measurement error in an analysis eliminates an important source of bias that has plagued environmental science, ecology and evolution (Taper and Marquet, 1996; Cheng and Van Ness, 1999). Implicit in the incorporation of measurement error is the ability to consider latent variables (i.e., unobserved, and potentially unobservable variables) (Grace and Bollen, 2008; Grace et al., 2010). Fourth, causal paths and latent variables allow linking scientific theory and statistical analysis in a particularly perspicuous fashion (Grace and Bollen, 2008; Grace et al., 2010; Laughlin and Grace, 2019). Because of these beneficial features, SEM is being utilized in growing number of applications in environmental informatics, ecology and evolution. The explosive growth of SEM in ecology is documented in Laughlin and Grace (2019).

Despite its many advantages for scientific thinking, SEM does present some inferential difficulties (Tomarken and Waller, 2003). Information can flow between variables by multiple pathways. As a consequence, the fit of alternative models and therefore the evidence between them can vary considerably with small changes in the configurations of the data. This uncertainty in evidence needs to be quantified.

A final reason for the choice of the Grace and Keeley example is the excellence of the original study. The observations were collected under the direction of Jon Keeley, while the analysis was conducted by James Grace. Jon Keeley is a very experienced empirical ecologist, while Grace has been a leading proponent the application of SEM to ecological systems. Both are scientists of great distinction. We do not seek to cavil at pedestrian research but look to see what bootstrapping of evidence can add to a well done scientific analysis.

3.2. Example Description

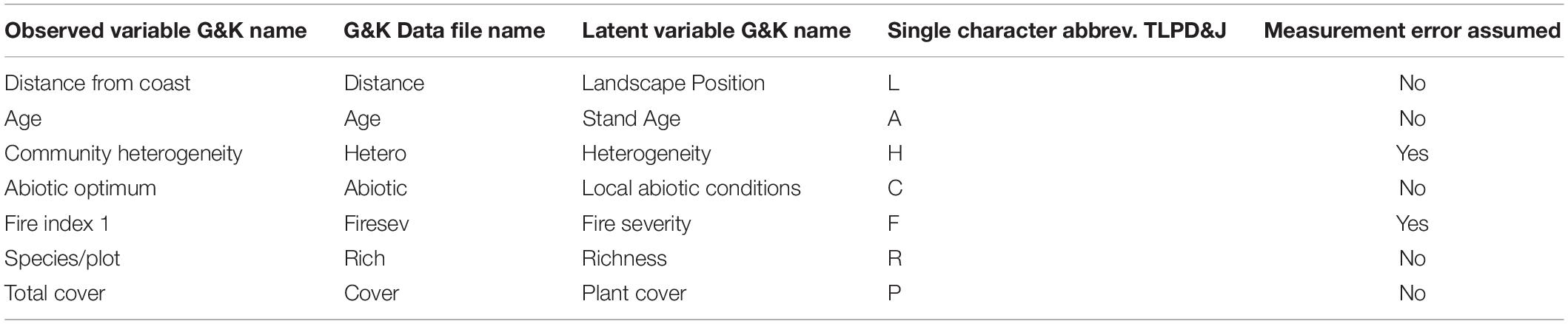

Keeley et al. (2005) and Grace and Keeley (2006) describe the data collection in detail. In brief, 90 sites in southern California were surveyed for 5 years following wildfire. Seven variables were observed indicating 7 latent variables (see Table 1). Variables were transformed to generate approximate linear homoscedastic relationships.

Table 1. Descriptions of variables from Grace and Keeley (2006).

3.3. Model Naming Conventions

We will use a model naming convention that indicates latent variable regression structure. The single character abbreviation for a variable will be followed by “.” and then by the abbreviations for the variables it is regressed on. Regressions with different response variables will be separated by “_.”

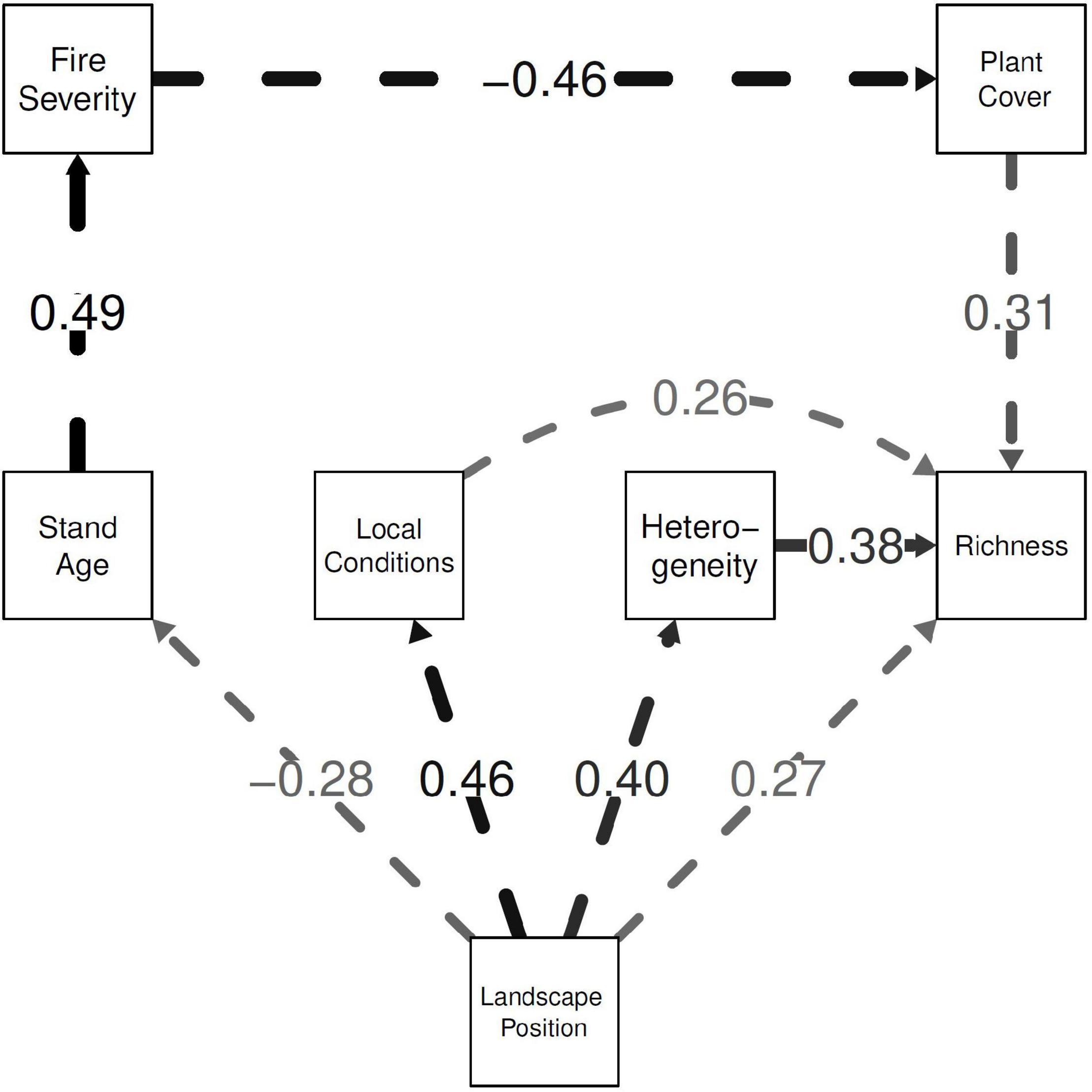

If a latent is isolated, that is it is neither a response nor a predictor in any regression in the model, its character would be entered in the model name but not followed by a “.” We don’t consider any such models, because we are picking up the Grace and Keeley reanalysis mid-stream, after they eliminated a variable called “Community Type” from their analysis. Alphabetical order will be imposed so that a path model uniquely determines a name. Thus the Grace and Keeley best model can be named: “A.L_C.L_F.A_H.L_P.F_R.CHLP” (see Figure 2 and Table 1).

Figure 2. The estimated final, simplified model explaining plant diversity. Arrows indicate causal influences. The standardized coefficients are indicated by path labels and widths. Weak paths with coefficients of magnitude less than 0.30 are shown in gray.

3.4. Example Reanalysis

Dr. Grace kindly provided the original data set and his original code (written using R package lavaan). In our reanalysis we use the R package lava (version 1.6.7). The estimates of the standardized coefficients from the two packages agree to at least the 5 decimal places reported by lava. Grace and Keeley determine their best model based on several factors including theoretical background, chi-square model adequacy tests, generalized likelihood ratio tests between nested models, and inspection of deviations between observed and model implied covariances. Grace and Keeley note the consistency of their model identification with identification based on information criterion.

The strong theoretical relationship between ΔICs, the difference of information criterion values, and the likelihood ratio test statistic has been noted before (e.g., Burnham and Anderson, 2002; Lele and Taper, 2012; Taper and Ponciano, 2016). What differs between the approaches are the assumptions and warrants that tie the statistics to scientific inference. These differences can lead to substantive differences in inference from the same data and essentially the same statistic. With a NP test you inference is a categorical accept or reject if your p-value is 0.051, just the wrong side of alpha of 0.05 your reject. If you have a ΔIC of 6.9, you don’t reject it instead you give a more elaborate discussion: “Well the evidence doesn’t quite reach our arbitrary strong evidence threshold, but it is very strong prognostic evidence.” We will return to this in the discussion (see also Box 1). Here we focus on the impact of uncertainty in evidence for one model over another given the data on reasonable scientific inference.

3.4.1. Models Considered

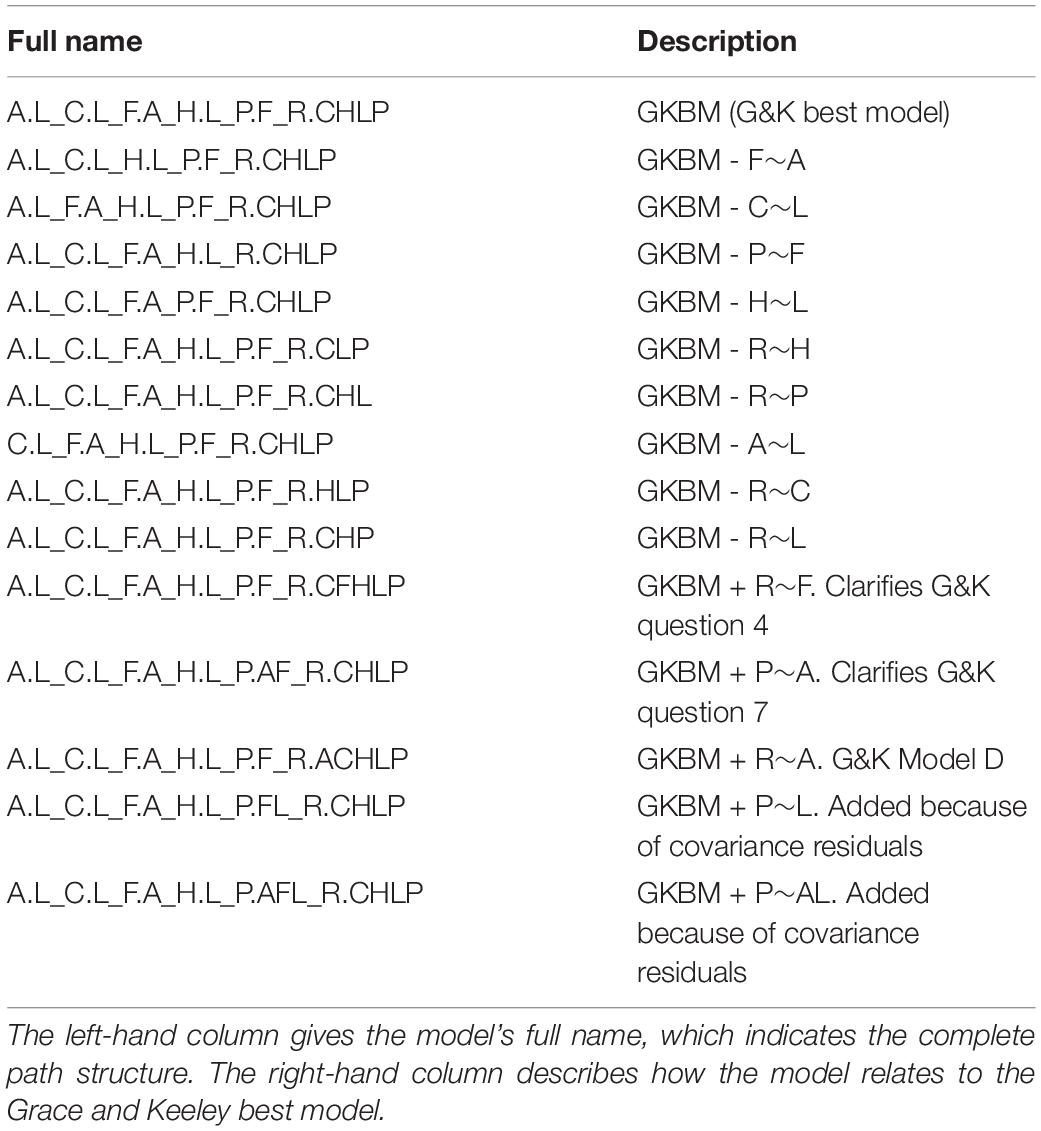

Statistical evidence, at least defining the term as in the Royall (1997), Lele (2004a), Taper and Ponciano (2016), and Brittan and Bandyopadhyay (2019) tradition, is not unary, but binary: It measures the support (Edwards, 1992) for one model over another model that is given by data. The models we compare are listed in Table 2.

Table 2. Models compared in our reanalysis of the Grace and Keeley (2006) structural equation analysis of diversity recovery after fire.

The first model is the Grace and Keeley best model (GKBM). The next 9 models are deletion models that each differ from the best model by the absence of a single path. These models are listed in order (strongest to weakest) of the strength of the effect in the best model (as measured by the coefficient z-statistic). Comparison of each of these models with the GKBM will probe the question of whether the deleted path belongs in “best model.” The last 5 models are addition models that each differ from the GKBM by the presence of 1 or 2 paths. Comparison of each of the addition models with the GKBM probes the question of whether that/those paths should be included in a “best model.”

3.4.2. Example Reanalysis Results

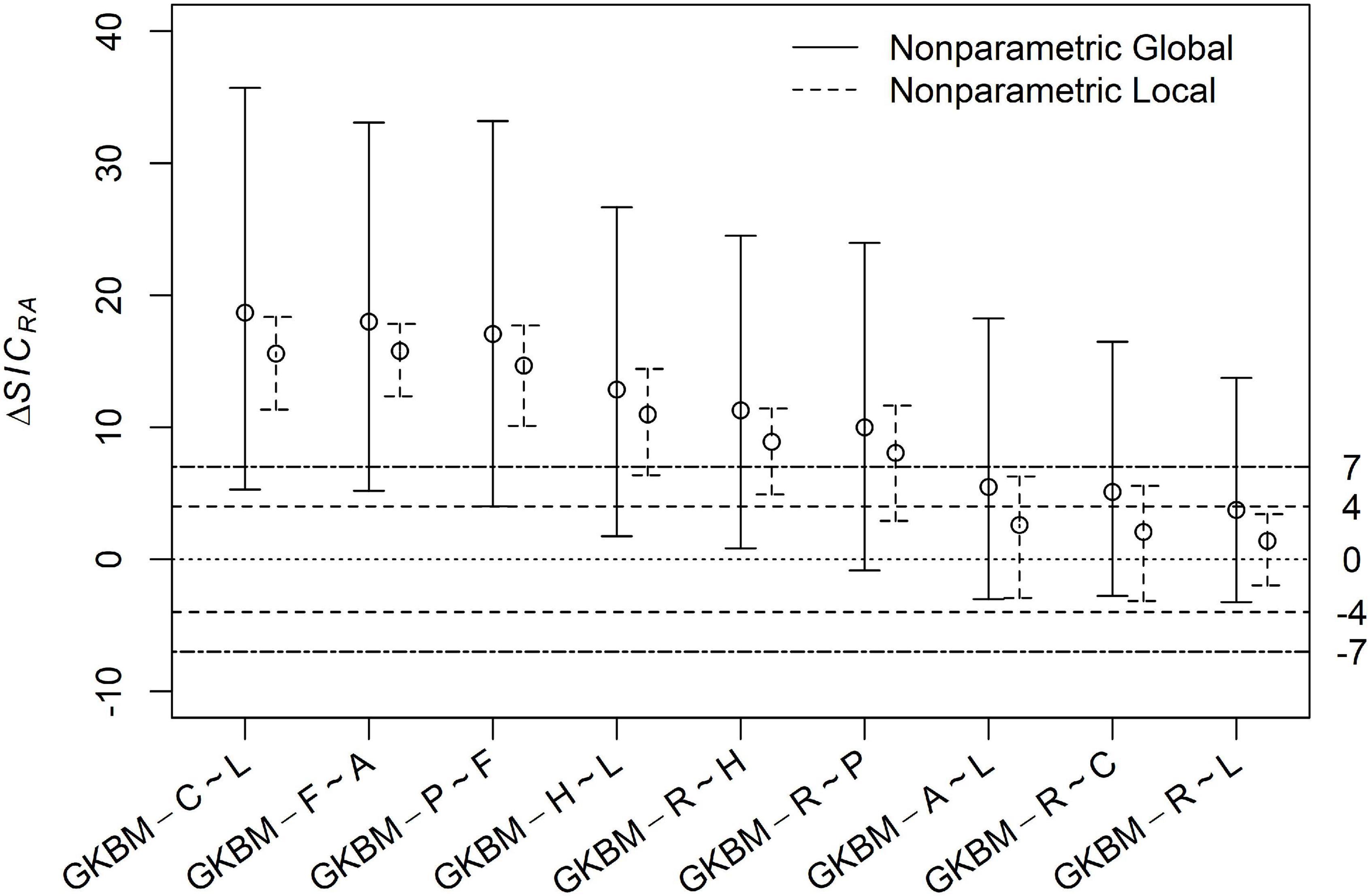

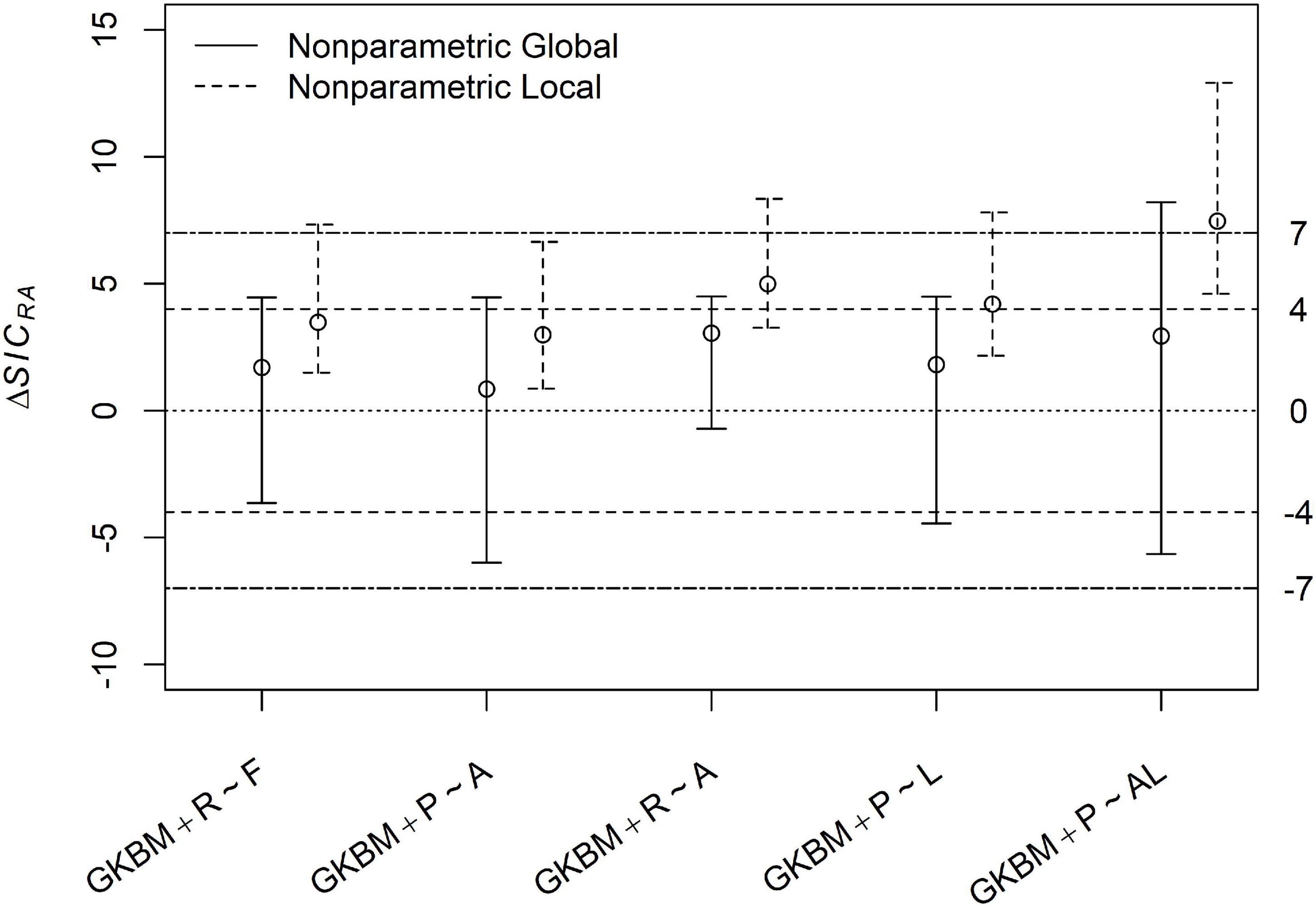

The results of our reanalysis are presented in Figure 3, which plots the evidence (ΔSIC) and its uncertainty for the GKBM relative to each of the deletion models, and Figure 4, which shows GKBM evidence and uncertainty relative to the addition models.

Figure 3. Evidential uncertainty intervals comparing the Grace and Keeley best model with 9 models, each that deletes one of the paths in the GKBM. For each model comparison, the open circle indicates the observed evidence, the solid error bar indicates the global uncertainty, the dashed error bars show the local uncertainty. These are approximate 90% confidence intervals based on 4000 non-parametric bootstraps. The strong evidence thresholds are indicated by dot-dash horizontal limit lines at 7 and -7, while the prognostic evidence thresholds are indicated at dashed limit lines at 4 and -4. Positive values of the ΔSICRA indicate evidence for the GKBM, as the reference model, relative to the alternative model, while negative values indicate evidence for the alternative model relative to the GKBM. The separatrix between these two regions is the dotted horizontal limit at 0.

Figure 4. Evidential uncertainty intervals comparing the Grace and Keeley best model with 5 models, each that adds one or two paths to the GKBM.

The first three model comparisons are rock solid. They all have strong and secure global evidence and strong and very secure local evidence. Not only does this data set strongly favor including these three paths, but replication of the experiment—in the same environment—will almost always reach the same conclusion.

The next two comparisons (GKBM - H∼L and GKBM - R∼H) both have strong and secure local evidence for including their paths, but globally, they are insecure. We have good reason to believe that these paths represent real causal effects, but need to advise researchers seeking to replicate this experiment to increase sample size to avoid equivocal results.

Then a comparison (GKBM - R∼P) with evidence, both global and local, that is strong but insecure. Here the global interval crosses the 0 line. Researchers should consider the possibility that the path may be weaker than estimated or may be non-existent.

The next two comparisons have barely prognostic evidence for their paths, but are insecure both globally and locally, with intervals that substantially overlap the line separating evidence for one model versus evidence for the other. The final comparison has positive but weak evidence for inclusion of the path. It is by definition insecure. The local evidence interval falls entirely between the two prognostic evidence thresholds. There is evidence for the path, but it is just a bit more than a toss-up.

Whether or not the last 3 paths should be included in a model is a judgment call for the reporting researchers based on the costs both practical and intellectual of including false paths or omitting true paths. For these deletion paths, a nudge might be given toward including them because the evidence favors the more complex model despite the SIC evidence function being used having a slight bias at small sample size toward compact models.

All five addition models have global evidence that is weak and insecure but that leans toward the more compact GKBM. However, all the global intervals overlap the separatrix at 0, and three of the intervals even overlap the marginal evidence thresholds for including the paths. The local evidence shifts slightly further toward the GKBM.

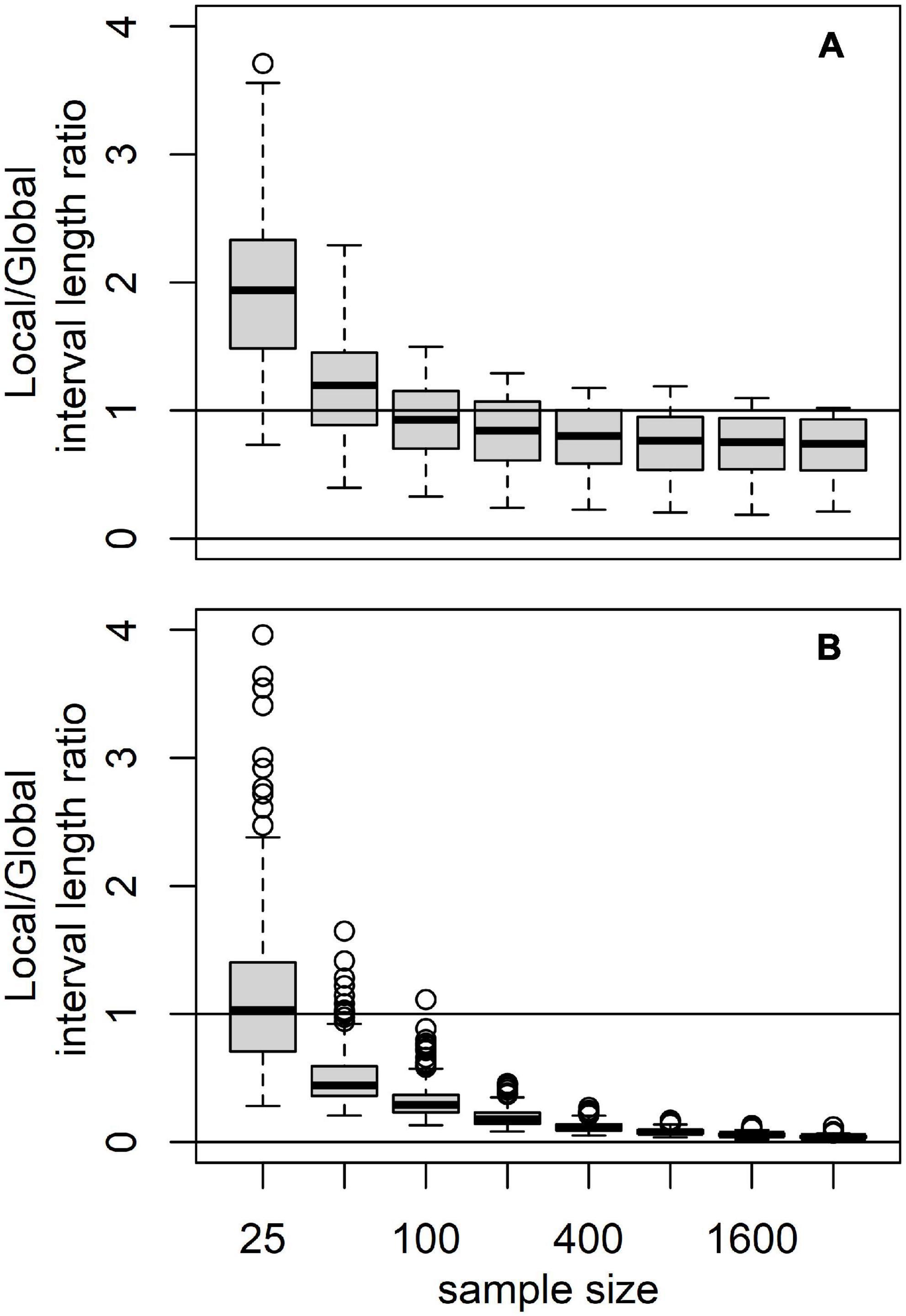

At this sample size, there is no compelling statistical reason to include any of the addition paths in the “best model,” but there is also no compelling statistical reason not to. The slight tilt toward the GKBM may represent nothing more that the SIC bias toward compact models. It is very hard statistically to distinguish between the true absence of a path and the presence of a weak path. It would take a sample size of more than 1,000 for there to be an expectation of global strong and secure SIC evidence for the absence of a path even if it was truly absent. On the other hand, because the coefficient of variation of local evidence declines at a much faster rate than that of global evidence (n–1 versus n–1/2) even a modest increase in sample size may allow local identification of weak effects. In the case of the Grace and Keeley example the breadth of the conditional intervals indicates that the sample size is marginal in a statistical sense—despite the Herculean effort represented.

Models are single entities, but they are entities built from components. In our experience, a great deal of insight into how components function in models can be found by estimating the evidence for a model including the component relative to the same model without that component. In all 14 model comparisons, the weight of evidence tilts toward the GKBM. We agree with Grace and Keeley that A.L_C.L_F.A_H.L_P.F_R.CHLP is the “best model” (at least out of those considered) to describe the structural relationships in this data set. Grace and Keeley chose in 2006 to interpret the empirical results of their study narrowly. “Ultimately, results and interpretations presented in this paper are based on the model judged to be the best representation of the data” (Grace and Keeley, 2006). Here we do disagree with Grace and Keeley. Our analysis has shown that even within a small list of a priori models, drawn from their own back-ground theory, there are multiple plausible models whose interpretation should be considered. To interpret only a single best model is like choosing to use only a parameter point estimate without considering its uncertainty. It is simple, but over-confidence can be generated.

4. Mathematical Development

In this section, we develop the statistical justification and estimation algorithms for the confidence intervals for evidence that we use in this paper. A reader satisfied with a simulation-based justification could skip to Section 5, at least on first reading.

Different statistical divergences could be used to construct model adequacy measures and thus evidence functions (see Lele, 2004a; Markatou and Sofikitou, 2019). Each will have its own properties, and each could be useful in different circumstances. In this paper we focus on the Kullback-Leibler divergence (KLD) as it leads to the information criteria, evidence functions already in common use. The treatment of uncertainty for other divergences and evidence functions should parallel that for the KLD. The mathematical notation, definitions, and assumptions used in our treatment are given in Box 4.

BOX 4. Mathematical notations, definitions, and assumptions.

The notation in this box is more verbose than commonly used to allow the reader to track fine distinctions among generating process, distribution estimators, estimated distributions for a particular sample, true parameters, parameter estimators and parameter estimates given a particular sample.

(1) Data are assumed to be suitable for non-parametric bootstrapping. For this paper we further assume that the data are independently and identically distributed (i.i.d.).

(2) Probability density function (pdf) or probability mass function (pmf) representing the true generating mechanism is denoted g(.). Its cumulative distribution function (cdf) is denoted as Fg(⋅).

(3) Observed data: , where n denotes the sample size.

(4) Random variables: .

(5) The pdfs/pmfs for reference (R) and alternative (A) models are denoted by mR(.) and mA(.), respectively. For example, mR is N(μ = 5, σ = 1). Note, these are fully specified models.

(6) If the reference and alternative model are not fully specified, then they represent model spaces denoted MR and MA respectively. In that case each of MR and MA is a collection of models. For example, MR = N(μ, σ)) with μ in (−∞, ∞) and σ in (0, ∞).

(7) is the empirical estimator of the cdf of g(.) for a random vector of length n. Here I(A) is the indicator function for event A. Denote a corresponding numerically smoothed density as .

(8) , the empirical estimate of the cdf of g(.) for an observed vector of length n. Denote a corresponding numerically smoothed density as .

(9) The KLD between two specified continuous models, where the reference model is mR is K(mR, mA) = ∫(log(mR(x)) − log(mA(x)))mR(x)dx. In general, for any two models (discrete, continuous or piecewise continuous) we write K(m1, m2) = ∫(log(m1(x)) − log(m2(x)))dFm1(x).

(10) The KLD orthogonal projection of a probability distribution, such as a fully specified model, s(.) onto a model space M is (see Figure 3 in Ponciano and Taper, 2019). This model is the closest approximation to s(.) in the model space M.

(11) If . If the generating process is in either MR or MA that is if either g(.) ∈ MR or g(.) ∈ MA then the model set {MR, MA} is considered correctly specified, as in the foundations of much classical statistics (e.g., Neyman and Pearson, 1933; Wilks, 1938; Wald, 1943).

(12) The log-likelihood function for the observed data, , under g(.) is

The log-likelihood function for the observed data under a model m(.) is . is the model with parameter values that maximizes .

(13) Conceptually, is the same model as . The first notation is more familiar, the second emphasizes that the maximum likelihood model is a projection of the model to the empirical density. Asymptotically these estimates will be identical, but there will be slight numerical differences at finite sample size due to the smoothing in .

(14) The KLD estimator of the divergence of a model, m, from the generating process, g is given as

where Sĝn,X,ĝn,X is the neg-self-entropy of the generating process and Sgn,X,m is the neg-cross-entropy from the generating process to the model m. Note, an estimator is the function of a random variable (i.e., ) that returns an estimate for a particular realization of the random variable.

(15) The KLD estimate of the divergence of a model, m, from the generating process, g:

.

where is the neg-self-entropy of the empirical distribution.

(16) The KLD projection estimator of the divergence of a model space, M, from the generating process, g:

(17) The KLD projection estimate of the divergence of a model space, M, from the generating process, g:

(18) One estimate for is , see discussion in definition (13). Bias correction for this estimate is the goal of information criteria. We employ the consistent family of bias correction terms cnp, where cn is a function of n growing strictly between loglog(n) and n. And, p is the parametric dimension of M (Nishii, 1988).

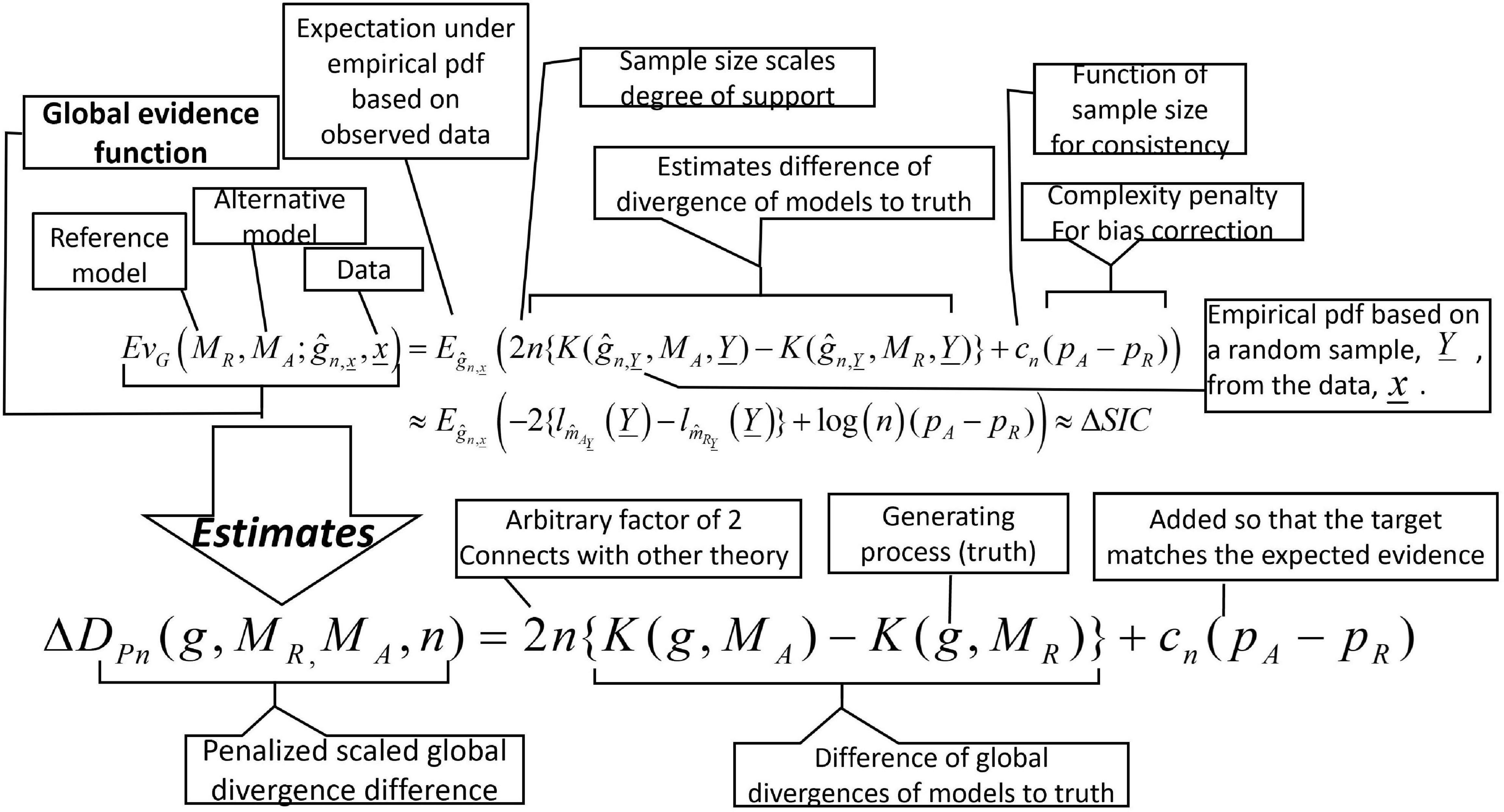

(19) The global penalized scaled divergence difference target: ΔDPn(g, MR,MA, n) = 2n{K(g, MA)−K(g, MR)} + cn(pA−pR) (see definition 16). The target is the quantity for which we attempt to find both a central estimate and an uncertainty measure (see discussion in Section 4.1). Note that for fully specified model comparisons, the penalty term is 0, and ΔDPn(g, mR, mA, n) = 2n{K(g, mA)−K(g, mR)}

(20) The local penalized scaled divergence difference target, (see definition 17).

(21) The global penalized divergence difference estimator, . Note that inside the expectation is a random vector drawn from .

(22) The local penalized divergence difference estimator, . Note that inside the expectation is a random vector drawn from .

(23) The global evidence estimate, . Note that inside the expectation is a random vector drawn from and that the maximum likelihood estimate, , has been substituted for (see definitions 13 and 18). Both the estimated models and the data from which the likelihoods are calculated are random. Thus, variation in EvG is due to both variation in and to variation in the estimates of . Non-parametric bootstrap will be used to estimate the expectation and its uncertainty estimation and for further bias reduction. Positive values for evidence indicate that the reference model is supported over the alternative model (see discussion Box 1).

(24) The local evidence estimate, Note that inside the expectation is a random vector drawn from and that the maximum likelihood estimate, , has been substituted for (see definition 18). Here the estimated models are random, but the data from which the likelihoods are calculated are fixed. Thus, variation in EvL is due only to variation in the estimates of . Non-parametric bootstrap will be used to estimate the expectation and its uncertainty estimation and for further bias reduction. Positive values for evidence indicate that the reference model is supported over the alternative model (see discussion Box 1).

(25) The raw evidence, . Note that no bootstrapping is done nor expectation taken. This is an information criterion as generally used.

Commonly, either confidence or credible intervals are used to quantify uncertainty in parameter estimates. A very general method of constructing confidence intervals is hypothesis test inversion (Casella and Berger, 2002). If your test is a generalized likelihood ratio test then the set is an approximate 100(1−α)% confidence interval if θ is of dimension 1 or confidence region if θ is of dimension > 1 (Pawitan, 2001).

If one is interested in inference on a subset of the parameters in a multidimensional parameter vector θ, one can partition the parameter vector as θ = [γ, λ], where γ is a vector of the parameters of interest, often of dimension 1, and λ is a vector of all the other parameters. A profile log-likelihood (for a given γ) can be calculated as , that is by maximizing over λ. It is argued (Cox and Reid, 1987) that maximization of the profile likelihood leads to inconsistent estimators of the parameters of interest because it does not appropriately penalize for the cost of the estimation of the incidental parameters. Various bias corrections or penalty terms for the profile likelihood have been suggested (Pace and Salvan, 2006).

The connection between profile likelihood and model selection becomes obvious if one considers that the parameter of interest could be nothing more than an index for the models considered. In Box 5 we use this connection to develop and justify global and local uncertainty in the evidence for one model over another. We point out that these penalties for parameter estimation are similar to the penalties employed in information criteria. A general parametric bootstrap approach to calculating an approximate penalty for the profile likelihood is described in Pace and Salvan (2006).

BOX 5. Adjusted profile likelihood for model selection inference.

Readers can see Meeker and Escobar (1995) for a brief introduction to profile likelihood in the context of confidence interval construction and Pierce and Bellio (2017) for a substantial review of practical likelihood adjustments. A gentle introduction to model selection through information criteria can be found in Anderson (2008), with more technically robust discussions in Burnham and Anderson (2002) or Konishi and Kitagawa (2008).

A general parametric bootstrap approach to calculating an approximate penalty for the profile likelihood is described in Pace and Salvan (2006) and outlined below.

Let Mφ, φ = 1, 2, …, S denote S distinct model spaces. The goal of model selection is to use the data to select the best model space. The form of the best model space is used to draw various statistical and scientific inferences about the generating mechanism.

First, we show that model selection procedure can be looked upon as a profile likelihood estimation procedure. Let denote the parameters for the respective model spaces (M1, M2, …, MS). Denote the dimension of by pφ.

A universal model space, that is simply a union of the model spaces, may be written as . In this notation, indicates the parametric form of the probability model in the first model space, say LogNormal(μ, σ2), denotes the parametric form of the probability model in the second model space, say Gamma(μ, ϕ), and so on. The parameter φ, which is a discrete parameter, is simply an index for the model space. Thus, model selection can be viewed as selecting a particular value of φ. In model selection problem, the index parameter φ is of interest and model parameters are the incidental parameters. The profile likelihood of the index parameter φ can be written as: .

In the familiar example of the maximum likelihood estimator of the variance σ2 in the multiple linear regression model Yi = β0 + β1X1i + β2X2i + … + βpXpi + εi where εi ∼ N(0, σ2) independent, . This is a biased estimator and bias is pronounced when the number of covariates is large. A bias corrected profile likelihood yields the usual unbiased estimator with the divisor (n−p−1), instead of n. We lose (p + 1) degrees of freedom because we spend some of the information in the data to estimate the nuisance parameters .

We describe the Pace-Salvan approach for the general profile likelihood case where the parameter of interest may or may not be discrete. To reflect this generality, for the description of the Pace-Salvan approach, we make a slight change in the notation. We use γ for the parameter of interest, λ for the incidental parameters and h(.) denotes the parametric probability function presumed to be the data generating mechanism.

Let X∼h(., γ, λ). Let the parameter of interest, γ, be of dimension 1 and the nuisance parameter λ be a vector of any dimension that does not depend on the sample size. Let be a random sample of size n from h(., γ, λ). The log-profile likelihood for γ is defined as .

Model selection based on the maximum of this profile likelihood would correspond to selecting the model space that maximizes the log-likelihood but without any penalty for the number of parameters in the model. This procedure is known to lead to what is termed an inconsistent model selection procedure. The reason for the inconsistency is that this profile likelihood is a biased estimator of the expected Kullback-Leibler divergence (Akaike, 1973; see discussion in Ponciano and Taper, 2019). The inconsistency of and the bias correction used in information-based model selection bears strong similarity to the inconsistency and bias correction in the profile likelihood estimators (e.g., Severini, 2000; Pace and Salvan, 2006) suggested in a very different context.

Following Pace and Salvan (2006), the adjusted profile likelihood, adjusted for the effects of estimation of the nuisance parameter λ, can be computed, assuming the presumed model is the true generating mechanism, using parametric bootstrap as follows:

(1) Estimate the full parameter vector .

(2) For each bootstrap iteration b ∈ {1, ⋯, B}

(a) Generate a random sample of size n from denoted by .

(b) For these new data and for a fixed value of γ, obtain by .

(3) Compute the simulation adjusted profile likelihood as: . We point out specifically that the likelihood is evaluated for the original data but with the parameters that are estimated using the bootstrap data.

Pace and Salvan (2006) suggest using , instead of to conduct statistical inference for γ, the parameter of interest. Most importantly, they use sophisticated mathematics to show that the adjustment achieved by is locally (conditionally, post-data, post-experiment) appropriate. Note that following Efron and Tibshirani (1993) description of bootstrap bias correction, one may use . It follows from the results in Section 3.4 of Pace and Salvan (2006) that these two versions are equivalent up to O(n−1) and that the difference between these central estimates is small compared to the uncertainty. We use the mean of the bootstrap distribution as our central estimate to be consistent with both Pace and Salvan (2006) and Kitagawa and Konishi (2010). There is reason to believe that the median of the bootstrap distribution might have superior theoretical properties (De Blasi and Schweder, 2018), but we will pursue this in another paper.