Xiaoshan Cai1

Xiaoshan Cai1 Qing Peng

Qing Peng- 1School of Culture Tourism and Geography, Guangdong University of Finance and Economics, Guangzhou, China

- 2Research Institute of International Service Economy, Guangdong University of Foreign Studies, Guangzhou, China

- 3School of Economics and Business Administration, Chongqing University, Chongqing, China

Regarding the signing of the China–ASEAN Free Trade Agreement (CAFTA) as a quasi-natural experiment, this article uses the difference-in-differences model to examine the pollution emissions of domestic trading enterprises in the face of varying trade openness under international environmental regulations. It is found that trade liberalization will drive domestic trading firms to choose more proactive pollution abatement strategies, namely, the signing of CAFTA facilitates pollution reduction in enterprises trading mainly with CAFTA members. This effect is more significant in non-state-owned enterprises and labor-intensive enterprises. In particular, the effect of becoming a member of CAFTA to facilitate firm-level pollution reduction has a time lag, and its marginal effect tends to expand over time.

Introduction

The earth is experiencing major changes in global and regional climates (Dodd and Douhovnikoff, 2016), and it is predicted that these changes will exert a significant impact on both human well-being and global sustainability (Huang et al., 2021; Cai et al., 2022). Government across the world has formulated and implemented a large number of environmental regulations with different jurisdictions to coordinate the contradiction between domestic economic growth and environmental protection (Liu et al., 2022). Specifically, in the context of free trade and economic globalization, many countries have raised the operating environment standards of their domestic markets, refusing to allow the products that ignore environmental pollution reduction to enter their domestic markets. This kind of international environmental regulation has evolved into an important part of competition rules or environmental barriers that hinder trade liberalization, leading to profound changes in the way enterprises operate.

Confronted with increasingly stringent environment/green trade barriers, there have been many debates on their impacts on international trade. Some studies suggested that due to stricter environmental regulations, the corresponding exports of heavy industries will be reduced (Merican et al., 2007; Cole et al., 2011; Ghani, 2012). Cole et al. (2010) reached a similar conclusion and showed that environmental regulation was an important determinant of Japan’s status as a net importer in non-OECD countries and China. However, another branch of the literature found that environmental regulation does not always have a negative impact on international trade; instead, stricter environmental standards can facilitate the transition to cleaner production processes in developing countries (Arouri et al., 2012).

In view of the existing environmental regulation literature in an open economy, however, it seems that most studies are confined to economic activities, whereas less attention has been paid to enterprises’ environment practices. In fact, in the recent years, developed economies, including countries in the European Union (EU), the United States, and Japan, have been the earliest, most frequent, and strictest countries and regions in adopting environmental regulation measures in the field of international trade, mainly by “improving environmental standards,” “increasing inspection and quarantine items,” and making “changes in technical regulations,” which prompted trading enterprises of developing countries (e.g., China and Vietnam) to continue to implement ISO9000 and other environmental or technology standards of certification. In this background, it is reasonable to infer that not only will trade performance change, but pollution reduction will also be directly affected. Therefore, this article attempts to shed light on the question of how trade liberalization affects the environment practices of trading enterprises in the context of increasingly stringent international environmental regulations.

Under the constraints of the international market for environmental standards, domestic trading enterprises may try to attach green attributes to their products to meet basic transaction conditions and expand their international market share (Bagnoli and Watts, 2003), thus benefiting from more efficient utilization of materials and energy. Furthermore, in the context of responsible consumption, as consumers are willing to pay additional fees for the products of socially responsible enterprises (Kotler and Lee, 2005; Leisinger, 2005; McWilliams et al., 2006), domestic trading enterprises may improve the production environment standards to increase the resolution with similar products and obtain new market segments (such as “green” consumers) (Hart, 1995; Russo and Fouts, 1997; Kramer and Porter, 2011; Oikonomou et al., 2014). Based on the above mechanism, Costantini and Mazzanti (2012) found that EU environmental regulation can promote enterprise innovation and significantly increase exports of various industries. Fernández-Kranz and Santaló (2010) and Flammer (2015) proved that intensification of market competition can improve firm-level environmental performance and that trade liberalization is an important factor in shaping the practice of enterprise emission reduction.

Enterprises respond to trade liberalization by reducing pollution emissions, so that they can stand out in the competition with rivals, which supports the view of the Porter hypothesis.1 However, international environmental policies exert environmental pressure on enterprises. Controlling pollution or updating equipment is bound to occupy the original production management and technological innovation resources, which will have adverse impacts on the productivity and trade competitiveness of enterprises (Copeland and Taylor, 2004). Specifically, in emerging economies with relatively low per capita income (e.g., China, India, and Brazil), consumers are highly price-sensitive, and therefore, trading enterprises’ implementation of a “green” differentiation strategy may become a risky choice (Biswas and Roy, 2015). Bansal and Roth (2000) found that Japanese and British companies only consider environmental protection measures when improving their financial performance. Orsato (2006) showed that the lack of reliable information on product environmental performance is the main obstacle to consumers’ willingness to pay, which weakens the willingness of enterprises to “go green.” Therefore, due to cost pressure considerations and the uncertainty of green consumption awareness of target consumers, domestic trading enterprises may not implement emission reduction in response to international environmental regulation under the free trade system.

Based on the above practical observation and theoretical analysis, this study conducts a quasi-natural experiment in the form of the China–ASEAN Free Trade Agreement (CAFTA), which was signed in 2002 and entered into force in 2005, to empirically test the effect of trade liberalization on the green development of China’s trading enterprises by employing the difference-in-differences (DID) method. We find that China’s trading enterprises respond to higher competitive pressure from trade liberalization by reducing their pollution emissions under the increasingly strict conditions of environmental protection in production and trade. In an auxiliary analysis, this article documents that this effect is stronger for non-state-owned enterprises (non-SOEs) and labor-intensive enterprises. The comparative advantage of developing countries’ products mainly comes from low factor prices, and the international environmental standards aimed at protecting the environment and enhancing social welfare may seriously weaken the international competitiveness of labor-intensive industries, such as electronics, clothing, toys, textiles, and shoes, forcing trading enterprises, especially private enterprises without policy support, to reduce pollution to meet trading standards. Consequently, the survival risk of trading enterprises in developing countries will be increased significantly. From the perspective of dynamic effect, the positive effect of membership of CAFTA on enterprise pollution reduction has a time lag, and its marginal effect shows an expanding trend with the passage of time.

The contributions of this article are as follows. First, while the existing literature primarily examines the policy effects of international environmental regulation on import and export activities (Merican et al., 2007; Cole et al., 2011; Arouri et al., 2012; Ghani, 2012), less attention has been paid to how domestic trading enterprises respond to it in terms of pollution reduction. Second, unlike previous studies that focus on the environmental pollution performance of general enterprises (Duanmu et al., 2018), this article investigates the environmental practices of domestic trading enterprises when facing drastic trade liberalization. Third, this article extends the related research studies (Fernández-Kranz and Santaló, 2010; Flammer, 2015) and considers the issue of enterprises’ pollution reduction in the context of emerging economics or developing countries, improving the applicability and universality of the conclusions of previous research.

The remainder of this article is organized as follows. See the section “Theoretical analysis and research hypothesis” outlines the establishment of an international oligopoly model for theoretical analysis. See the section “Sample and research design” describes the construction of the sample, variable measurement, and research design. The empirical analysis is presented in the section “Empirical results.” Finally, see the section “Conclusion” summarizes the main conclusions.

Theoretical analysis and research hypothesis

Basic model

Following Brander and Spencer (1985) and Wang et al. (2012), we formulate an international duopolistic model composed of one domestic enterprise and one foreign enterprise, indexed by 0 and 1, respectively. Both enterprises export different products to a third country’s market and engage in Cournot players. The linear (inverse) demand function is specified with Pi = 1−qi−γq−i,i = 0,1, where qi denotes the outputs of the firm. We assume that all firms use an identical technology and have increasing marginal cost function: .

Although the world’s economic landscape is increasingly moving toward greater trade liberalization, tariffs still exist in most economies to protect domestic industries. Accordingly, it is assumed that a uniform tariff rate t∈(0,1) is imposed on the foreign firm’s output. The profits of two firms are given by:

The production of commodities in both enterprises leads to pollution emissions. However, each enterprise can prevent pollution by adopting abatement measures to achieve the environmental standards of the host country. To simplify the analysis, we assume that only the domestic enterprise has concerns about the problem of emission reduction and chooses to produce environmentally friendly products. Following Goering (2007), the payoff of the domestic enterprise is to maximize the weighted sum of its own profits and the host country’s consumer surplus:

where denotes the host country’s consumer surplus. α∈[0,1]captures the level of pollution reduction or the willingness to provide environmentally friendly products to the host country. Specifically, as α increases, the domestic enterprise makes more effort to meet environmental standards and provide environmentally friendly products in the host country market.

A two-stage game is constructed. In stage 1, the domestic trading enterprise chooses the optimal environmental practice in the host country (α). In stage 2, all the enterprises choose their output levels according to the Cournot equilibrium to maximize their respective objectives. We solve the game through backward induction.

Analytical results

In the last stage of the game, given α and t, the domestic trading enterprise chooses q0 to maximize (2) and the foreign trading enterprise chooses q1 to maximize (1). The first-order conditions are as follows, respectively:

Considering Eqs. 3, 4 simultaneously, we obtain the equilibrium outputs:

Using and , we calculate the following equilibrium outcomes:

Note that requires or ,2 which is assumed in the following discussion. Differentiating and with respect to α , it is easy to see that when the domestic trading enterprise gradually implements relatively positive environmentally responsible strategies in the host country, it will acquire a greater market share than the foreign trading enterprise (,). This result means that the domestic trading enterprise can improve its competitiveness and differentiate itself from the foreign rival, which conforms to economic practical experience that the host country (or consumers) is always willing to import (purchase) products from environmentally responsible enterprises.

In the first stage, given the above equilibrium outcomes, the domestic trading enterprise chooses the optimal level of pollution reduction or the willingness to provide environmentally friendly products to the host country. Following the general oligopoly literature, the objective of the domestic enterprise is to choose α to maximize its own profits. Combined with the derivatives (,), we can obtain only one interior and positive solution:

In general, tariff reductions represent greater trade liberalization. Therefore, to further explore the impact of trade liberalization on the optimal environmental decision-making of domestic trading enterprises, we differentiate α* with respect to t and find . This result shows that α* is the subtractive function of t, that is, with the deepening of trade liberalization, the domestic trading enterprise will adopt more environmentally responsible measures to engage in production activities to cultivate international competitive advantage. Accordingly, we formulate the following research hypothesis:

Hypothesis 1: Under stringent international environmental protection standards, domestic trading enterprises will choose more proactive pollution emission reduction strategies to maintain market competitive advantage. In brief, trade liberalization will drive trading enterprises to reduce pollution emissions.

Sample and research design

The theoretical analysis shows that domestic trading enterprises will choose more proactive pollution abatement strategies to maintain their competitiveness in the international market if there is a tendency toward a more open trading environment. Are these firms really responding in this way? If so, how significant is this effect? To answer these questions, the primary task is to determine how to measure the variation in trade openness. In general, the measure of trade openness tends to be tariffs; however, the change in a country’s tariff policy is discrete in time, the adjustment direction is not uniform, each adjustment involves a wide variety of commodities, and therefore, there are certain difficulties in operation.

With the deepening of China’s economic and trade relations with the world, actively promoting the negotiation of Free Trade Agreements (FTAs) has become an important part of China’s new round of the opening-up strategy. After signing FTAs, the contracting countries often reduce tariffs substantially, or even achieve zero tariffs, which provides us with an exogenous shock to measure the tariff changes. However, by 2018, China had signed 16 FTAs involving 24 countries or regions in Asia, Oceania, Latin America, and Europe, including China–Maldives, China–Georgia, China–Australia, China–South Korea, China–Switzerland, China–Iceland, China–Costa Rica, China–Peru, China–Singapore, China–New Zealand, China–Chile, China–Pakistan, and China–ASEAN. Of these FTAs, only CAFTA is a collective agreement signed by China with a number of developed and developing countries simultaneously, which provides us with more abundant and more general research samples. Therefore, using China’s membership of CAFTA as an opportunity to measure the variation in trade openness,3 this article examines the impact of membership of CAFTA on the domestic firm-level pollution reduction.

Design

In general, the impact of CAFTA on enterprises’ pollution emissions can be assessed by making a horizontal and vertical comparison. Horizontal comparison shows the differences in pollution emissions between firms that trade mainly with CAFTA members and those that do not; however, it ignores the heterogeneity between firms. The latter is a direct comparison of the differences in pollution emissions of enterprises trading mainly with CAFTA members before and after becoming a member of CAFTA; however, it does not take into account the consistency of time trends. Following the general practice in environmental regulation literature (Chen et al., 2018; Wang et al., 2019), we regard the membership of CAFTA as a quasi-natural experiment.4 Due to its application at different enterprises at the same time (trade and non-trade or major and non-major trade), we divide Chinese enterprises into two groups: the treatment group and the control group. The treatment group contains the enterprises significantly affected by membership of CAFTA, and the control group contains the enterprises minimally affected by membership of CAFTA. This allows us to adopt the DID method to explore the effects of varying intensity of trade liberalization caused by becoming a member of CAFTA on firm-level pollution emissions:

where the subscripts i and t represent the enterprise and year, respectively. Yit represents the level of pollution emissions of firm i in year t. To enhance the reliability and robustness of the research results, we choose both water pollution (wastewater) and air pollution (wasteair) as a measure of pollution emissions, expressed as the natural logarithm of the total amount of industrial wastewater/waste gas discharged by enterprises, respectively.

treati is the grouping variable to identity whether enterprise i belongs to the treatment or control group. A total of eleven countries have become the members of CAFTA: China, Malaysia, Indonesia, Thailand, the Philippines, Singapore, Brunei, Vietnam, Laos, Myanmar, and Cambodia. Unlike the previous studies that simply classify the group based on the occurrence of the trade, we aim to distinguish the treatment group from the control group to a greater extent and avoid as far as possible the interactive effects on the control group as a result of becoming a member of CAFTA. If an enterprise’s share of trade (exports or imports) with the above-mentioned countries is larger than the median of that of all enterprises in all years, it trades mainly with CAFTA members and belongs to the treatment group, whereas if an enterprise has neither import nor export trade with the above-mentioned countries, it belongs to the control group.

postt is the time difference variable before and after the signing of CAFTA to recognize the period in which enterprise i is located. Although the relevant agreement between China and ASEAN was formally signed in November 2002, the tax reduction of CAFTA was not initiated until July 2005, which was objectively the point when the agreement came into effect. Therefore, 2005 is adopted as the starting year when China’s membership of CAFTA has an effect on enterprises’ pollution emissions, with postt taking a value of 0 before 2005 and 1 after 2005.

According to the different values assigned to treati and postt, all samples can be divided into the following four groups: the treatment group before the signing of CAFTA (treati=1,postt=0), the treatment group after the signing of CAFTA (treati=1,postt=1), the control group before the signing of CAFTA (treati=0,postt=0), and the control group after the signing of CAFTA (treati=0,). The net policy shock effect, measured by the characterization of the regression coefficient of the interaction term , can be obtained through two different calculations of the above four groups of samples. Thus, is the core explanatory variable, whose regression coefficient β3 >0 means that the pollution emissions of the treatment group increase compared to those of the control group and membership of CAFTA has a negative impact on the enterprise pollution reduction, whereas β3 <0 denotes that the pollution emissions of the treatment group decrease compared to those of the control group and membership of CAFTA has a positive impact on the enterprise pollution reduction.

Following the approach of existing studies (Flammer, 2015; Duanmu et al., 2018), we include control variables as follows: (1) enterprise scale (size), measured as the natural logarithm of its net fixed assets; (2) enterprise age (age), measured by adding 1 to the difference between the year in which the enterprise is located and founded; (3) capital intensity (intz), measured by the ratio of the average balance of net fixed assets to the number of employees; (4) asset-liability ratio (debt), measured by the ratio of total liabilities to total assets; (5) enterprise profitability (profit), measured by the ratio of operating profit to sales revenue; And (6) asset liquidity (liquidity), measured by the ratio of the excess of current assets over current liabilities to current assets. Furthermore, μn and ϑj are industrial effects and regional effects, respectively, and εit is a random disturbance term.

Sample

The sample for this article is mainly taken from the Database of Chinese Industrial Firms and the Database of Chinese Customs Firms from 2000 to 2009. A different treatment for the two databases is designed to improve the accuracy of this empirical study, processing the monthly data of products on the Database of Chinese Customs Firms by adding it to annual data. Moreover, the following treatments are carried out on the Database of Chinese Industrial Firms consecutively. First, samples with fewer than eight employees are excluded based on the experiences of Brandt et al. (2012) and Yu (2014). Second, samples that do not conform to objective facts and have excess missing data and outliers (e.g., total output less than zero) are excluded. Third, samples that are not in correspondence with the accounting standards (e.g., total assets less than current assets or fixed assets) are not available. In addition, we exclude samples with errors and omissions in their original records (e.g., the enterprise has been operating for less than 1 month or more than 12 months).

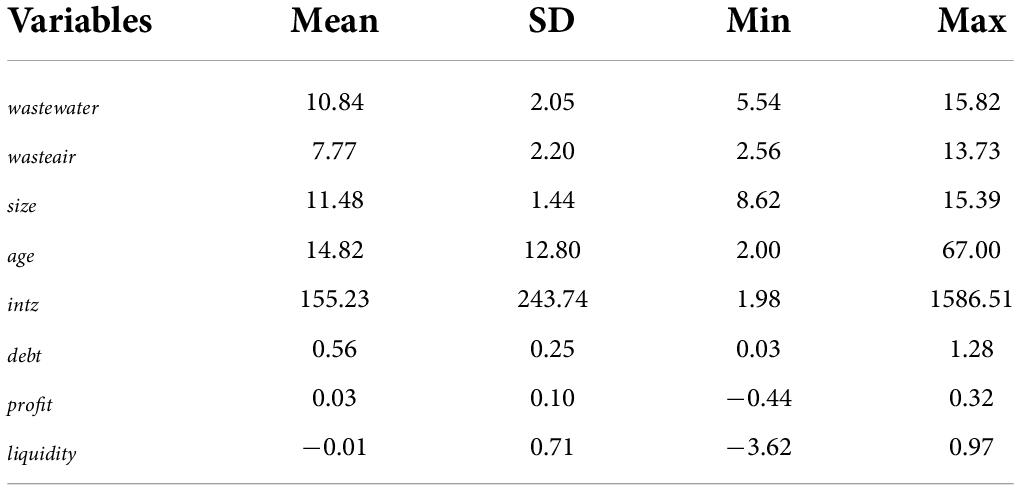

Due to the difference in the coding system between the Database of Chinese Industrial Firms and the Database of Chinese Customs Firms – the former has a 10-digit legal person code and the latter has a 9-digit code – this article draws on Yu and Tian’s (2012) article to combine enterprises with the same name and year in these two databases while excluding samples that do not record industrial wastewater (waste gas) emissions. Based this, enterprises that exited the market before 2005 and those that entered the market after 2005 will be excluded to ensure that all firms we choose are still in operation in the policy year of 2005. Continuous variables used in the regressions are winsorized at 1% to mitigate the possible effects of outliers, resulting in 33,229 initial observations. Descriptive statistics for the main variables are shown in Table 1.

Table 1. Descriptive statistics of variables.

Empirical results

Parallel trend test

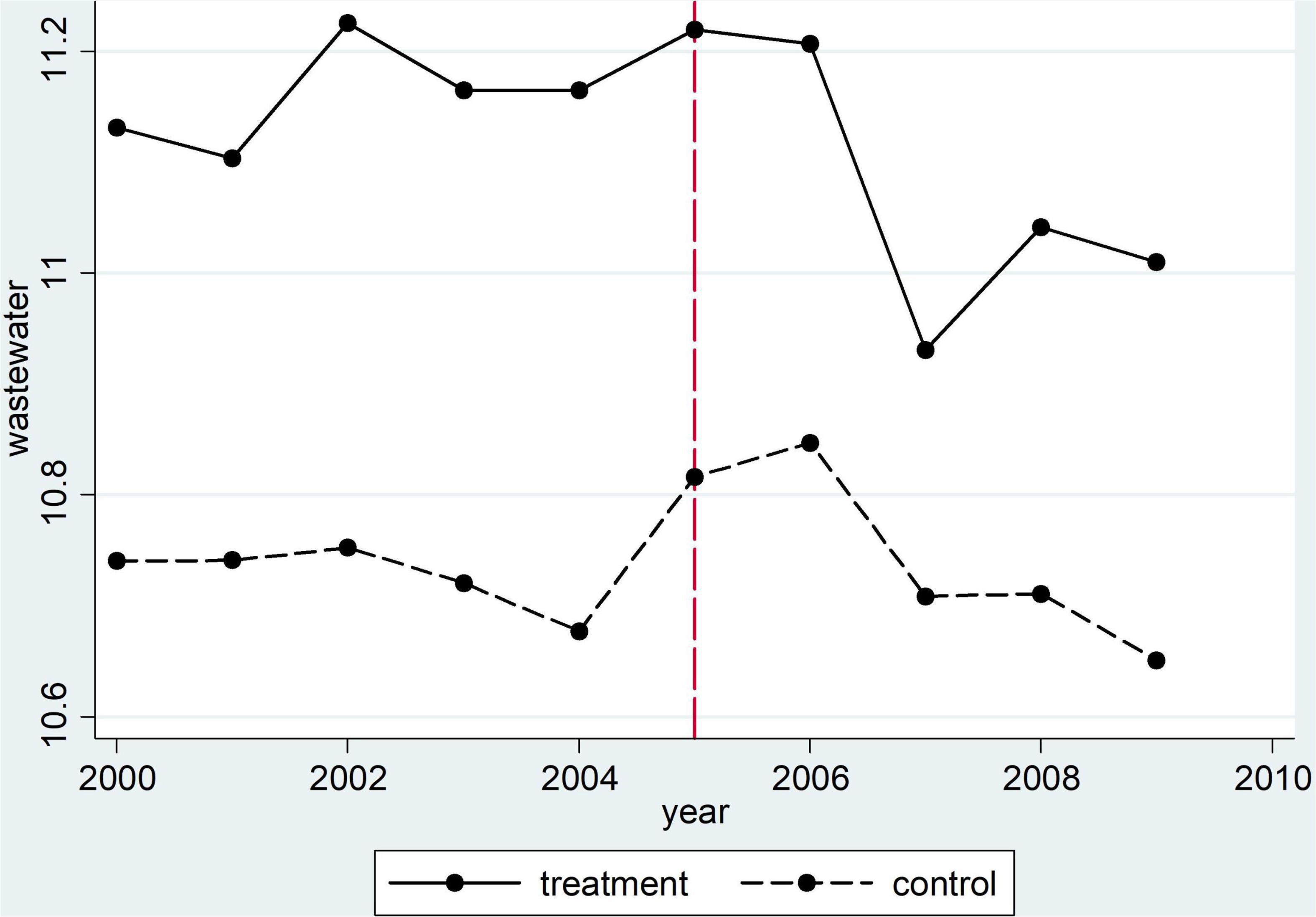

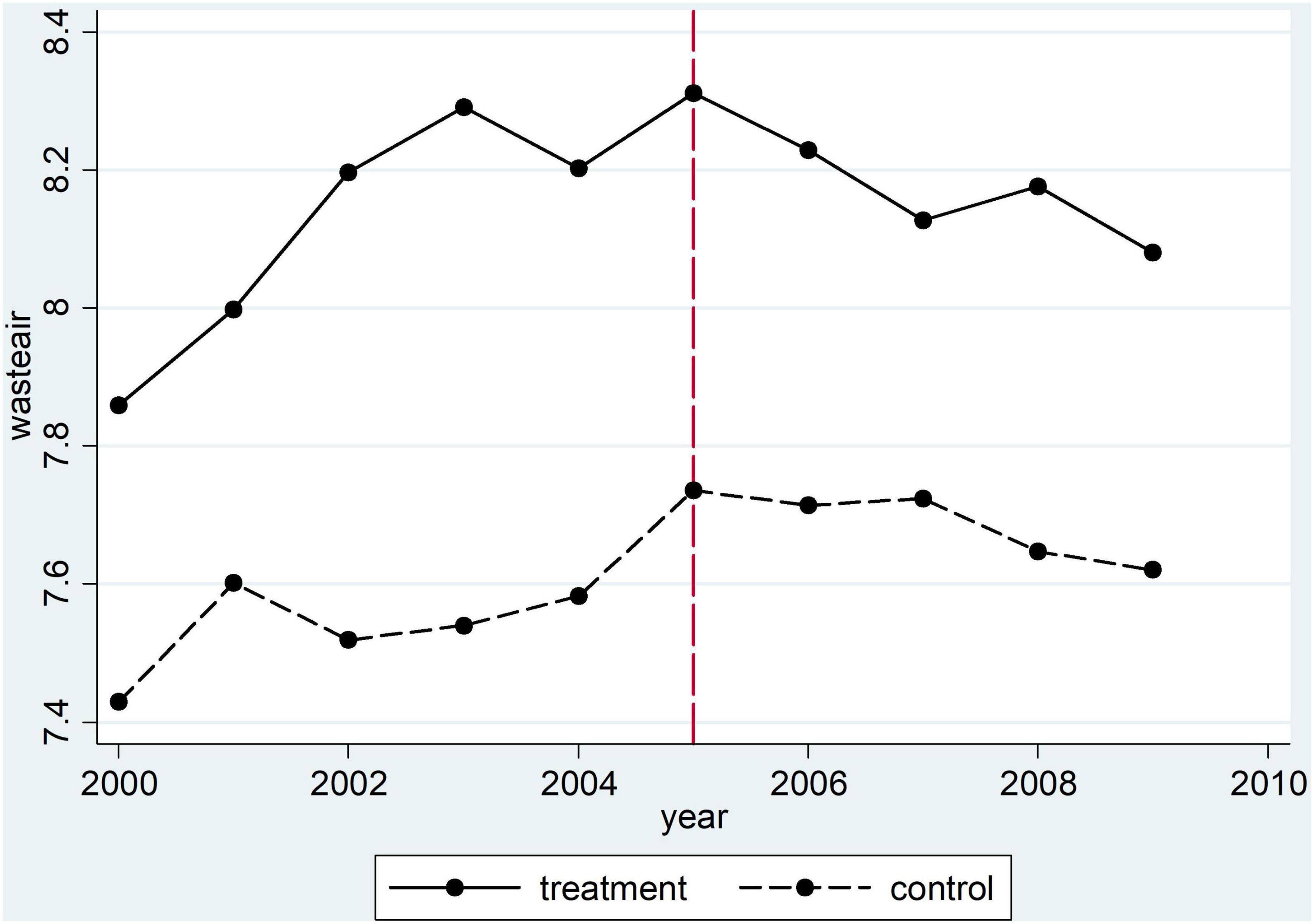

The DID method is valid on the premise of meeting the parallel trends assumption that the growth rate of the dependent variable should be consistent in the treatment and control groups before and after treatment. Figures 1, 2 show that the total industrial wastewater (waste gas) emissions of the treatment and control groups maintain a highly similar trend prior to China becoming a member of CAFTA, both being on a slow rise. After China became a member of CAFTA, the trends in the two groups diverge significantly. In terms of total industrial wastewater discharge, the curve for the control group rises slowly and then falls, whereas that of the treatment group remains virtually constant at first and then plunges. For total industrial waste gas emissions, both groups show a continuing downward trend, with a larger decline in the treatment group. The above findings prove that the DID model meets the prerequisites of the common trend assumption in temporal trends.

Figure 1. Parallel trend of wastewater.

Figure 2. Parallel trend of wasteair.

Baseline regression results

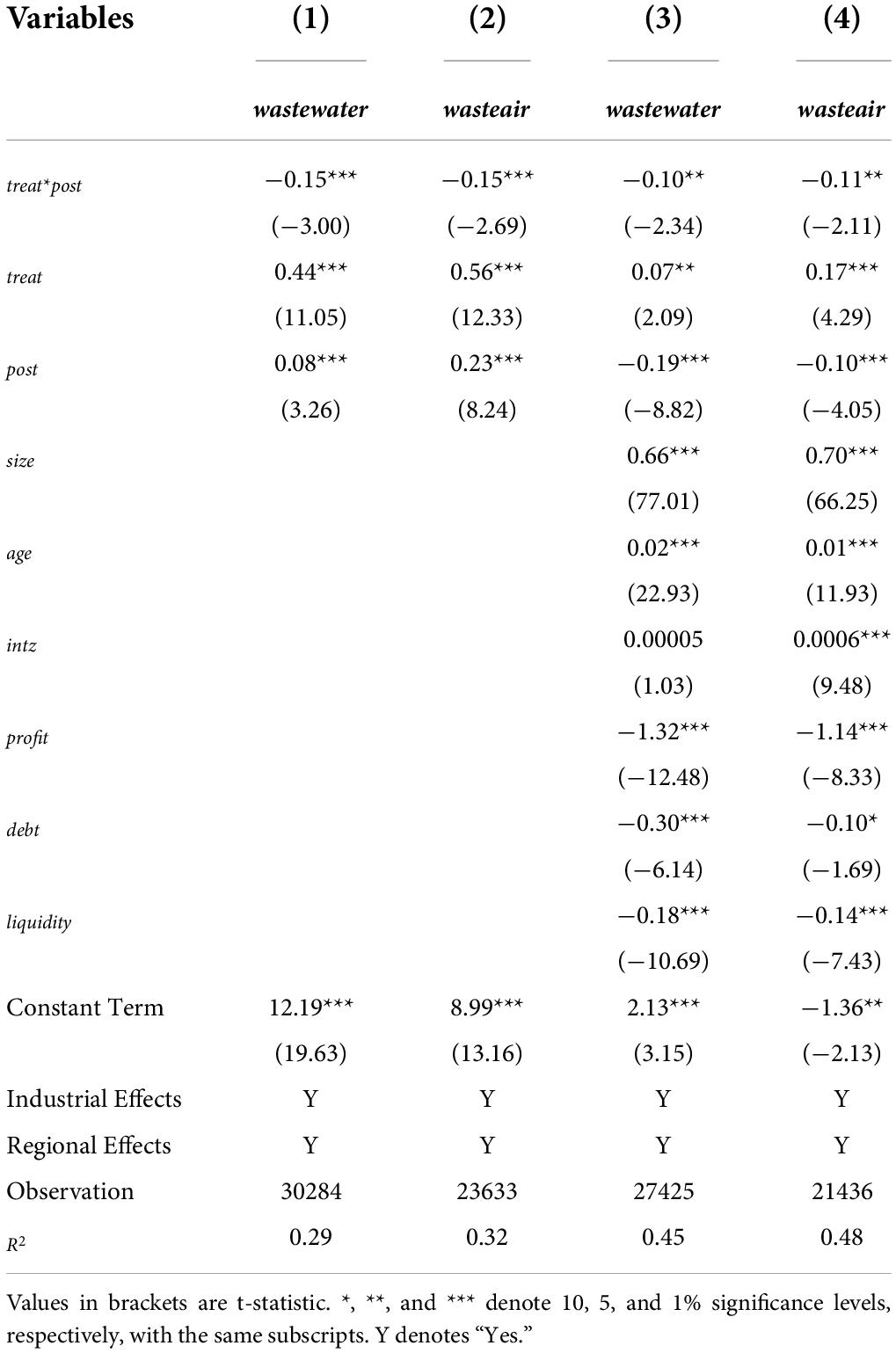

The baseline regression results regarding the effect of membership of CAFTA on enterprise pollution emissions are presented in Table 2. As shown in columns (1) and (2), the coefficients of treat*post are significant and negative. After adding control variables in columns (3) and (4), the coefficients are still significantly negative. This indicates that the total industrial wastewater (waste gas) emissions of enterprises that trade mainly with CAFTA members decreased more significantly after China becomes a member of CAFTA, signifying that CAFTA strongly encourages trading enterprises to work on pollution control and compete in international markets with products and services that are highly socially responsible. Thus, hypothesis 1 is valid.

Table 2. Baseline regression results.

Regarding the control variables, the regression coefficients of size, age, and intz are positive, and most of them pass the 1% significance test, which indicates that the enterprise emits more pollution with larger size, longer survival, and higher capital intensity. This may be related to the corporation organizational inertia. The regression coefficients of profit, debt, and liquidity are negative, and most of them pass the 1% significance test. This suggests that the enterprise emits less pollution with greater profitability and liquidity. The findings are in line with those of previous research indicating that successful pollution control relies on good financial performance. In particular, enterprise pollution emissions decrease with the increase in debt to total assets ratio, probably due to the fact that the enterprise purchases major equipment for pollution control, which generally raises the gearing overall but also achieves pollution reduction.

Heterogeneity analysis

Enterprises with different ownership types

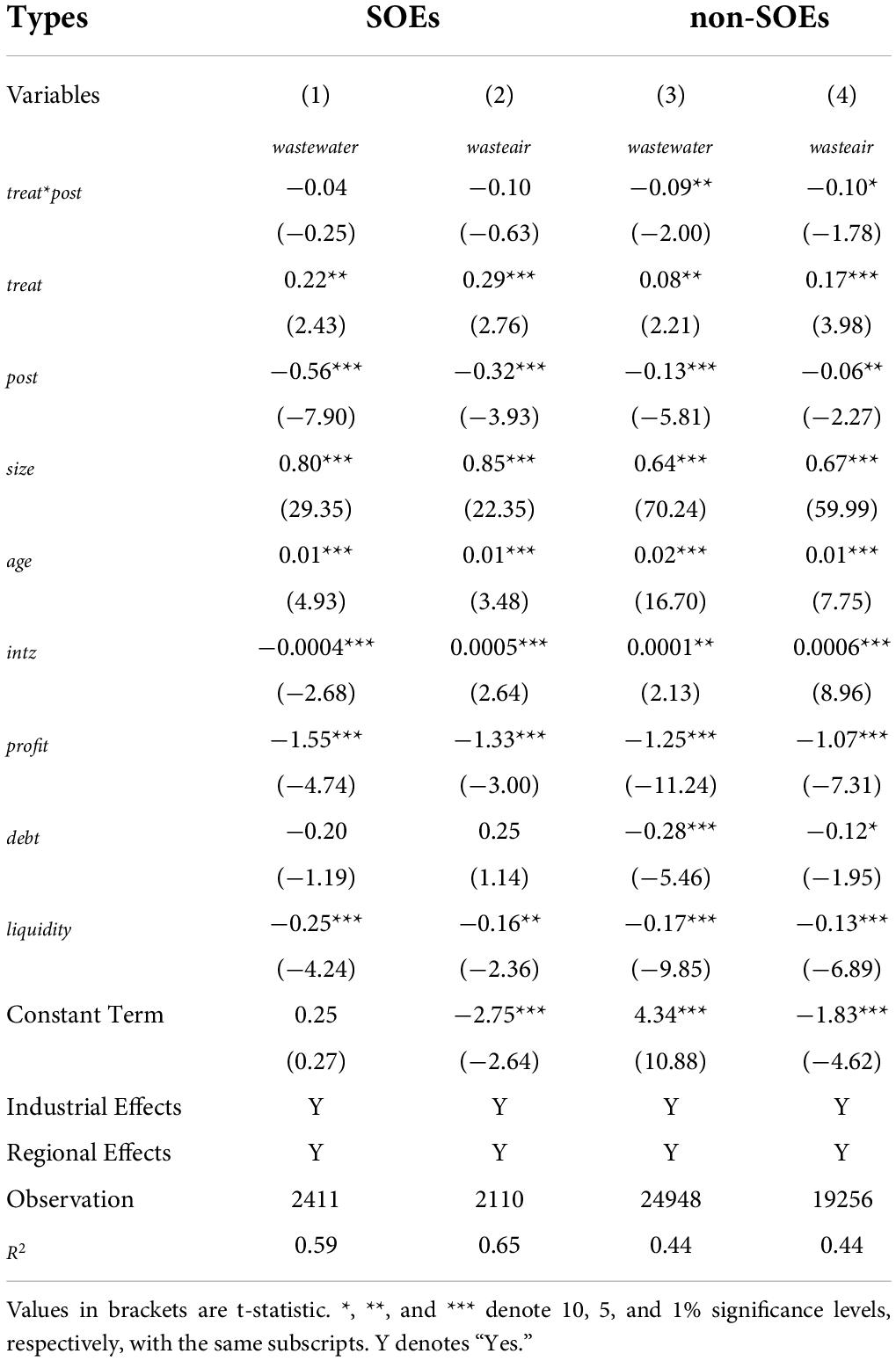

There are differences between SOEs and non-SOEs in terms of their business objectives,s, clearly subjected to government intervention, are inherently required to assume social responsibilities, external environment, and operating method. Due to the special political and social attributes, SOEs, clearly subjected to government intervention, are inherently required to assume social responsibilities, such as environmental cleanup. Therefore,s, clearly subjected to government intervention, are inherently required to assume social responsibilities, the pollution emission of non-SOEs may be more influenced by market mechanisms than that of SOEs. Accordingly, we divide all the enterprises into SOEs and non-SOEs to assess the impact of membership of CAFTA on the pollution reduction of enterprises with different ownership types. The estimation results are shown in Table 3, where columns (1) and (2) are regression results for the SOEs and columns (3) and (4) are those for the non-SOEs.

Table 3. Regression results of subsamples by enterprise ownership.

We found that the estimated coefficients of the interaction terms, treat*post, in columns (1) and (2) are negative but statistically insignificant while those in columns (3) and (4) are negative and pass the 5 and 10% significance tests, respectively. It can be concluded that the estimation results of non-SOEs are more consistent with the whole sample than those of SOEs and that membership of CAFTA leads to greater improvement in non-SOEs’ pollution reduction. This is also in line with the current situation of Chinese enterprises. Compared to SOEs, naturally profit-seeking non-SOEs are more likely to follow the market mechanism and adjust their production and operation despite facing intense pressure from stakeholders and improve their pollution control to maintain or enhance their competitiveness in an increasingly fierce game. Even if China has greater openness, the competitive advantage of SOEs, which dominate national economic development and safeguard people’s well-being, will not decline sharply in the near future since they are monopolies or oligopolies. In particular, SOEs have been driven by the government to improve their pollution control, and the higher openness by becoming a member of CAFTA may have not led to obvious stimulation or pressure on them.

Enterprises in different industries

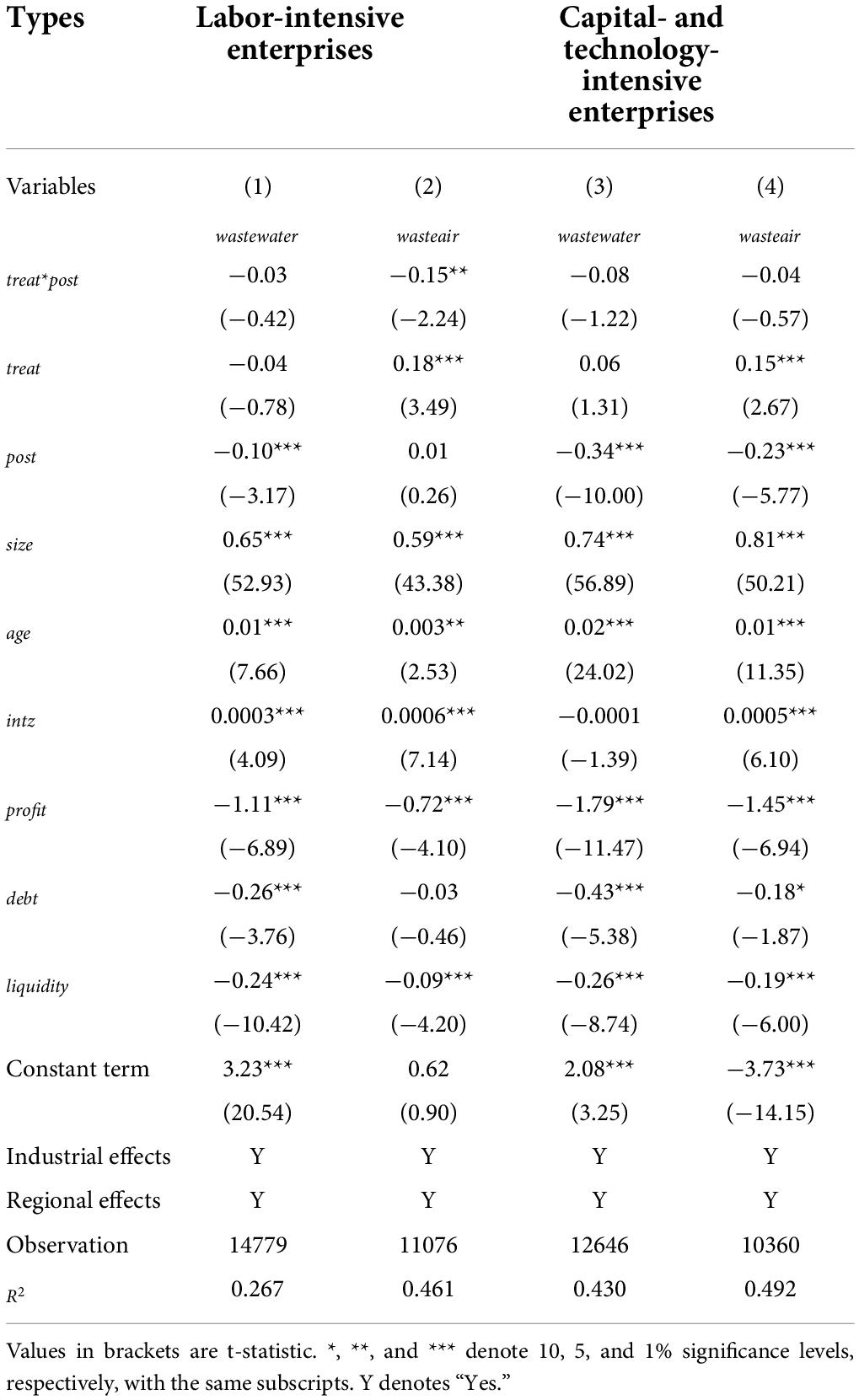

Given the factor intensity of different industries, this article classifies all the enterprises into labor-intensive enterprises and capital- and technology-intensive enterprises to discuss the impact of membership of CAFTA on pollution reduction in different industries.5 The results are shown in Table 4, where columns (1) and (2) are regression results for the labor-intensive enterprises and columns (3) and (4) are those for the capital- and technology-intensive enterprises. We found that the regressions for the subsamples by industry yield negative coefficients for the interaction terms, but only the samples of labor-intensive enterprises with total industrial wasteair emissions as the explained variable pass the 5% significance test. This suggests that China’s membership of CAFTA helps labor-intensive enterprises with pollution control of waste gas to a greater extent than capital- and technology-intensive enterprises. On the one hand, the products that China sells to ASEAN countries are mainly low-price labor-intensive products, such as clothing textiles, fresh oil, frozen fish, and other kinds of agroforestry by-products, so membership of CAFTA has a greater influence on the labor-intensive industries. On the other hand, most of the research samples are from manufacturing sectors, where most capital- and technology-intensive enterprises, still at the startup stage in China, are classified as energy-intensive industries where there is a threshold for environmental investment and a higher cost of pollution control than for labor-intensive enterprises. This huge cost may deter these enterprises even though CAFTA has increased international competition.

Table 4. Regression results of subsamples by industry.

Dynamic marginal effects

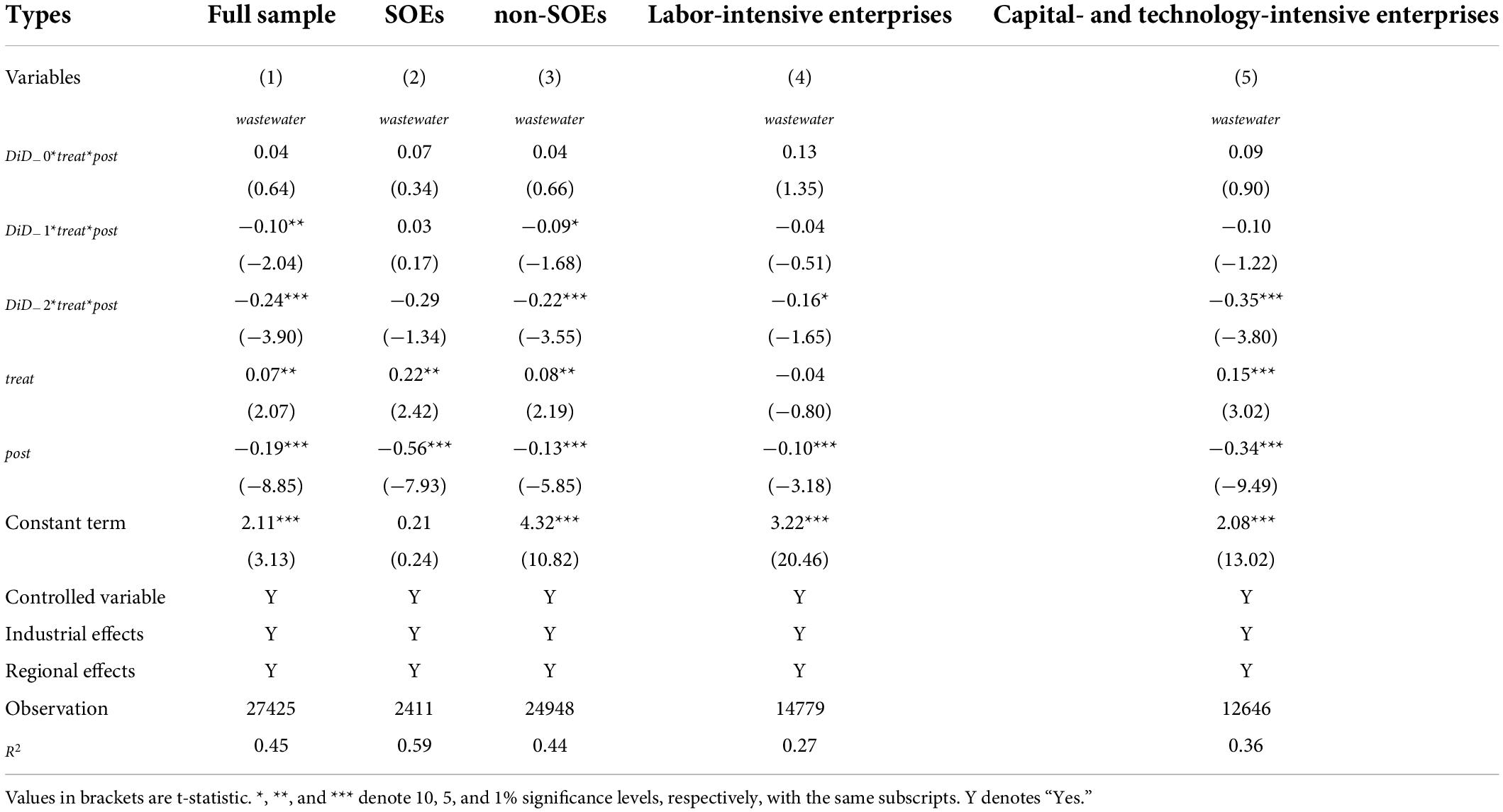

Since the variable post is assigned a value of 1 in 2005 and beyond, the baseline regression measures the difference in the average level of enterprise emissions before and after China became a member of CAFTA (2000–2004 and 2006–2009), which does not reflect whether there is a time lag and stability in the effect of this public policy. Accordingly, Eq. 8 is extended with a triple interaction term comprising the time dummy variable and treat*post:

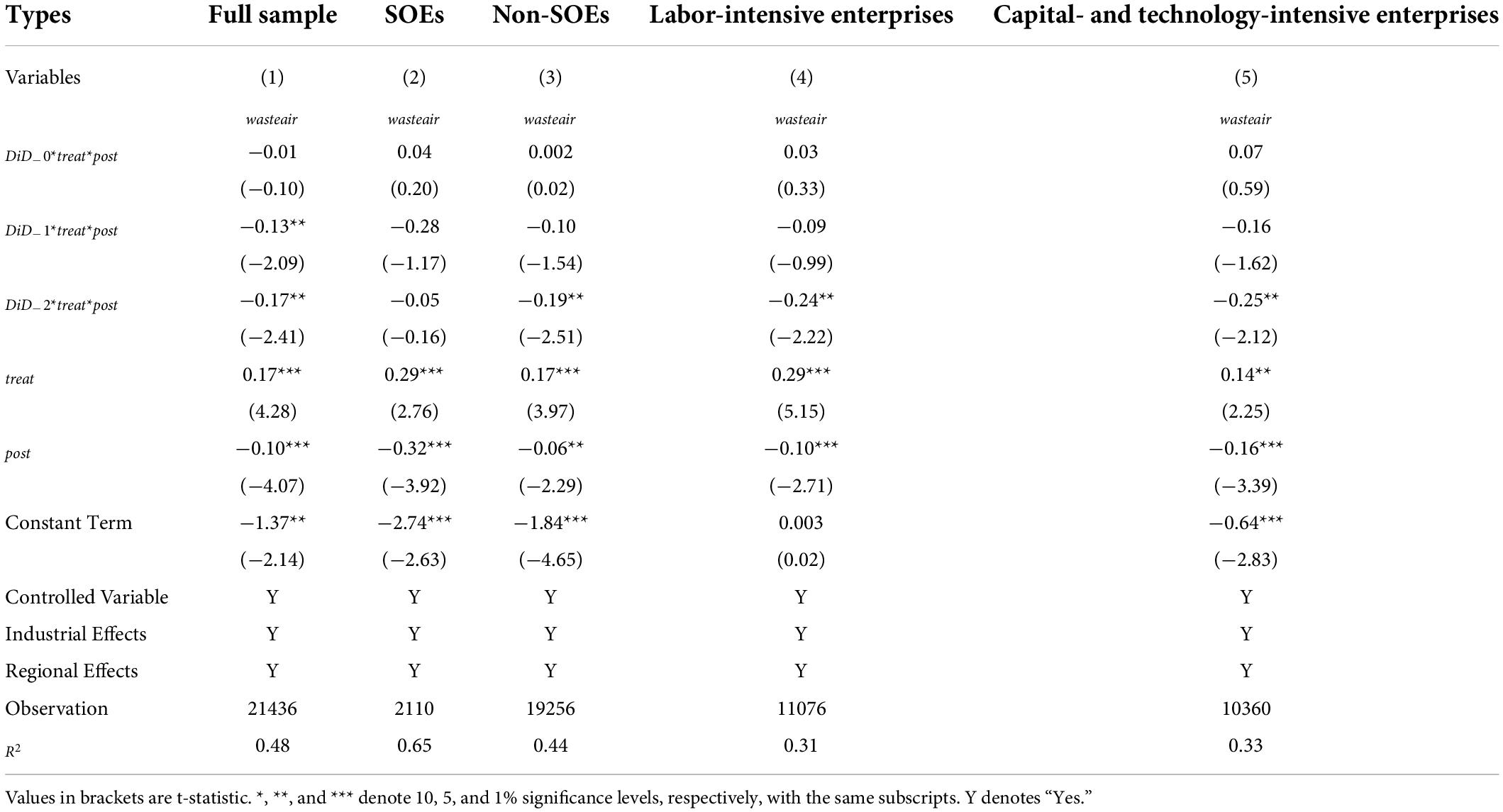

where DiD−τ is the dummy variable for the year during the period after China became a member of CAFTA, and DiD−τ is assigned a value of 1 when the firm is in period τ, otherwise a value of 0. In this article, the current period of China’s membership CAFTA (namely, in 2005) is considered to be in period 0, the first 2 years after China became a member of CAFTA are seen as being in period 1, and the second 2 years are considered to be in period 2. The estimated coefficient ατ is the key subject of examination for the dynamic marginal effects in period τ. The regression results with total industrial wastewater discharge and wasteair emissions as explanatory variables are reported in Tables 5, 6, respectively. For the full sample in column (1), none of the coefficients of the triple interaction term DiD−0*treat*post is significant, whereas both coefficients of DiD−1*treat*post and DiD−2*treat*post are significantly negative, and the absolute value of the latter is greater than that of the former. This proves that it does not work well on industrial wastewater (waste gas) reduction of enterprises in the period when CAFTA has just come into force, but gradually improves during periods 1 and 2, that is, there is a time lag in the effect of China becoming a member of CAFTA on enterprises’ pollution reduction, and the marginal effect tends to expand over time.

Table 5. Dynamic marginal effects of total industrial wastewater emissions.

Table 6. Dynamic marginal effects of total industrial wasteair emissions.

A closer look at the samples grouped by ownership reveals significant differences in the dynamic marginal effects between SOEs and non-SOEs. Shown as the regression results for the samples from SOEs in column (2) that are consistent with the previous findings, the estimated coefficients of DiD−τ*treat*post are statistically insignificant, indicating that there is no significant effect of China becoming a member of CAFTA on pollution reduction by SOEs. Furthermore, the regression results in column (3) for the non-SOEs sample show that they are positive, negative, and negative, respectively, and the significance and absolute value increase period by period. This suggests that the dynamic marginal effects of the samples of non-SOEs are essentially the same as those of the whole sample, that is, there is a time lag in the contribution of CAFTA to pollution abatement by non-SOEs and, similarly, the marginal effect exhibits an expanding tendency over time.

In terms of the samples grouped by industry, we found that the dynamic marginal effects of labor-intensive enterprises are largely in parallel with those of capital- and technology-intensive enterprises. The estimated coefficients of DiD−τ*treat*post are shown as positive, negative, and negative, and they only pass the 5% significance test in period 2, indicating that there is a time lag of about 3–4 years in the effect of China becoming a member of CAFTA on the pollution reduction of enterprises in different industries.

Conclusion

International environmental regulation has evolved into a kind of “blue trade barrier,” which has become an important part of the competition rules in the international market. This article considers China becoming a member of CAFTA as a quasi-natural experiment and investigates the impact of trade openness on pollution abatement by enterprises with the DID method. We found that under international environmental regulation, the pollution abatement strategies of domestic trading firms are subjected to significant constraints from the international environment. Market competition intensifies in an increasingly open trading environment, and domestic trading enterprises will be proactive in strengthening pollution control in an effort to remain competitive in the host country. The empirical analysis reveals that enterprises trading mainly with CAFTA members are generally encouraged to reduce their pollution emissions after China became a member of CAFTA. China becoming a member of CAFTA motivates non-SOEs to fight pollution; however, it is not significant to SOEs. For the samples divided based on the capital intensity, it has a more significant positive effect on pollution reduction for labor-intensive enterprises than capital- and technology-intensive enterprises. In addition, there is a time lag in the effect of China becoming a member CAFTA on enterprises’ pollution reduction and a tendency for its marginal effect to expand over time, especially in the samples of non-SOEs.

At a time when the global environment is deteriorating, it is often used as a trading condition by multinational corporations to meet certain environmental standards. The conclusions of this article suggest that domestic trading enterprises should adopt proactive strategies, differentiating themselves from rivals through pollution control. By fully understanding the environmental culture of target countries, regions, and economies and weighing the cost of pollution control and the benefits of competition, efforts could be made to merge into economic globalization. It is better to continue transforming and upgrading the manufacturing process flow and remain in alignment with international standards to enhance the competitive advantages of their products, as well as using relatively cleaner energy.

Data availability statement

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

Author contributions

XC, QL, and QP contributed to the conception and design of the study. XC and QL organized the database and performed the statistical analysis. XC and QP wrote the first draft of the manuscript. All authors contributed to manuscript revision, read, and approved the submitted version.

Funding

This study was funded by the Philosophy and Social Science Planning Project of Guangdong Province (GD21CGL26 and GD20XYJ07) and the Guangdong Basic and Applied Basic Research Foundation (2021A1515110226).

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Footnotes

- ^ Porter and Van der Linde (1995) proposed that well-designed environmental regulations can protect the environment and accelerate technology innovation, offsetting compliance costs, which is known as the Porter hypothesis.

- ^ ,

- ^ As a new round of opening-up strategy, the negotiation of Free Trade Agreements (FTAs) is always accompanied by the reduction both for tariff and non-tariff barriers among the contracting parties. Thus, it is reasonable to choose the accession to FTA as a proxy for gauging trade openness, and compared with tariff, this measure is more comprehensive and extensive.

- ^ A quasi-natural experiment means that experimental treatment level is completely independent of individual characteristics or other factors that might affect the results of the experiment, thus largely avoiding omitted variable bias and endogeneity bias. Hence, compared with traditional OLS or panel fixed effect estimation, DID model can better identify the causal effect between explained variable and explanatory variable.

- ^ According to the three-digit industry codes in the Database of Chinese Industrial Firms, capital- and technology-intensive enterprises include the petroleum processing and coking, and nuclear fuel processing industry; non-metallic mineral products industry; ferrous metal smelting and rolling processing industry; non-ferrous metal smelting and rolling processing industry; metal products industry; general equipment manufacturing; special equipment manufacturing; transportation equipment manufacturing; electrical machinery and equipment manufacturing; instrumental, cultural and official machinery manufacturing; chemical fiber manufacturing; pharmaceutical manufacturing; and chemical raw materials and chemical products manufacturing. The remainder are labor-intensive enterprises.

References

Arouri, M. E. H., Caporale, G. M., Rault, C., Sova, R., and Sova, A. (2012). Environmental regulation and competitiveness: evidence from Romania. Ecol. Econ. 81, 130–139. doi: 10.1016/j.ecolecon.2012.07.001

Bagnoli, M., and Watts, S. G. (2003). Selling to socially responsible consumers: competition and the private provision of public goods. J. Econ. Manag. Strategy 12, 419–445. doi: 10.1111/j.1430-9134.2003.00419.x

Bansal, P., and Roth, K. (2000). Why companies go green: a model of ecological responsiveness. Acad. Manag. J. 43, 717–736. doi: 10.5465/1556363

Biswas, A., and Roy, M. (2015). Green products: an exploratory study on the consumer behaviour in emerging economies of the east. J. Clean. Prod. 87, 463–468. doi: 10.1016/j.jclepro.2014.09.075

Brandt, L., Van Biesebroeck, J., and Zhang, Y. (2012). Creative Accounting or Creative Destruction? Firm-level Productivity Growth in Chinese Manufacturing. J. Dev. Econ. 97, 339–351. doi: 10.1016/j.jdeveco.2011.02.002

Brander, J. A., and Spencer, B. J. (1985). Export subsidies and international market share rivalry. J. Int. Econ. 18, 83–100. doi: 10.1016/0022-1996(85)90006-6

Cai, F. F., Yin, K. D., and Hao, M. Y. (2022). COVID-19 pandemic, air quality and PM2.5 reduction-induced health benefit: a comparative study for three significant periods in Beijing. Front. Ecol. Evol. 10:885955. doi: 10.3389/fevo.2022.885955

Chen, Y. J., Li, P., and Lu, Y. (2018). Career concerns and multitasking local bureaucrats: evidence of a target-based performance evaluation system in china. J. Dev. Econ. 133, 84–101. doi: 10.1016/j.jdeveco.2018.02.001

Cole, M. A., Elliott, R. J., and Okubo, T. (2010). Trade, environmental regulations and industrial mobility: an industry-level study of Japan. Ecol. Econ. 69, 1995–2002. doi: 10.1016/j.ecolecon.2010.05.015

Cole, M. A., Elliott, R. J., and Zhang, J. (2011). Growth, foreign direct investment, and the environment: evidence from Chinese cities. J. Regional Sci. 51, 121–138. doi: 10.1111/j.1467-9787.2010.00674.x

Copeland, B. R., and Taylor, M. S. (2004). Trade, growth, and the environment. J. Econ. Literature 42, 7–71. doi: 10.1257/002205104773558047

Costantini, V., and Mazzanti, M. (2012). On the green and innovative side of trade competitiveness? The impact of environmental policies and innovation on EU exports. Res. Policy 41, 132–153. doi: 10.1016/j.respol.2011.08.004

Dodd, R. S., and Douhovnikoff, V. (2016). Adjusting to global change through clonal growth and epigenetic variation. Front. Ecol. Evol. 4:86. doi: 10.3389/fevo.2016.00086

Duanmu, J. L., Bu, M., and Pittman, R. (2018). Does market competition dampen environmental performance? Evidence from China. Strategic Manag. J. 39, 3006–3030. doi: 10.1002/smj.2948

Fernández-Kranz, D., and Santaló, J. (2010). When necessity becomes a virtue: the effect of product market competition on corporate social responsibility. J. Econ. Manag. Strategy 19, 453–487. doi: 10.1111/j.1530-9134.2010.00258.x

Flammer, C. (2015). Does product market competition foster corporate social responsibility? Evidence from trade liberalization. Strategic Manag. J. 36, 1469–1485. doi: 10.1002/smj.2307

Ghani, G. M. (2012). Does trade liberalization effect energy consumption? Energy Policy 43, 285–290. doi: 10.1016/j.enpol.2012.01.005

Goering, G. E. (2007). The strategic use of managerial incentive in a non-profit firm mixed duopoly. Manager. Decis. Econ. 28, 83–91. doi: 10.1002/mde.1307

Hart, S. L. (1995). A natural-resource-based view of the firm. Acad. Manag. Rev. 20, 986–1014. doi: 10.2307/258963

Huang, C., Li, X. F., and You, Z. (2021). The impacts of urban manufacturing agglomeration on the quality of water ecological environment downstream of the three gorges dam. Front. Ecol. Evol. 8:612883. doi: 10.3389/fevo.2020.612883

Kotler, P., and Lee, N. (2005). Best of breed: when it comes to gaining a market edge while supporting a social cause, “Corporate Social Marketing” leads the pack. Soc. Market. Q. 11, 91–103. doi: 10.1080/15245000500414480

Kramer, M. R., and Porter, M. (2011). Creating shared value. Harvard Bus. Rev. 89, 62–77. doi: 10.1007/978-94-024-1144-7_16

Leisinger, K. M. (2005). The corporate social responsibility of the pharmaceutical industry: idealism without illusion and realism without resignation. Bus. Ethics Q. 15, 577–594. doi: 10.5840/beq200515440

Liu, B. L., Wang, J. X., Li, R. Y. M., Peng, L., and Mi, L. L. (2022). Achieving carbon neutrality -The role of heterogeneous environmental regulations on urban green innovation. Front. Ecol. Evol. 10:923354. doi: 10.3389/fevo.2022.923354

McWilliams, A., Siegel, D. S., and Wright, P. M. (2006). Corporate social responsibility: strategic implications. J. Manag. Stud. 43, 1–18. doi: 10.1111/j.1467-6486.2006.00580.x

Merican, Y., Yusop, Z., Noor, Z. M., and Hook, L. S. (2007). Foreign direct investment and the pollution in five ASEAN nations. Int. J. Econ. Manag. 1, 245–261.

Oikonomou, I., Brooks, C., and Pavelin, S. (2014). The effects of corporate social performance on the cost of corporate debt and credit ratings. Financ. Rev. 49, 49–75. doi: 10.1111/fire.12025

Orsato, R. J. (2006). Competitive environmental strategies: when does it pay to be green? California Manag. Rev. 48, 127–143. doi: 10.2307/41166341

Porter, M. E., and Van der Linde, C. (1995). Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 9, 97–118. doi: 10.1257/jep.9.4.97

Russo, M. V., and Fouts, P. A. (1997). A resource-based perspective on corporate environmental performance and profitability. Acad. Manag. J. 40, 534–559. doi: 10.5465/257052

Wang, K., Yin, H., and Chen, Y. (2019). The effect of environmental regulation on air quality: a study of new ambient air quality standards in China. J. Clean. Prod. 215, 268–279. doi: 10.1016/j.jclepro.2019.01.061

Wang, L. F. S., Wang, Y. C., and Zhao, L. (2012). Tariff policy and welfare in an international duopoly with consumer-friendly initiative. Bull. Econ. Res. 64, 56–64. doi: 10.1111/j.1467-8586.2010.00382.x

Yu, M. (2014). Processing trade, tariff reductions and firm productivity: evidence from Chinese firms. Econ. J. 125, 943–988. doi: 10.1111/ecoj.12127

Keywords: trade liberalization, environmental regulation, pollution emissions, CAFTA, difference-in-differences method

Citation: Cai X, Liu Q and Peng Q (2022) International environmental regulation, trade liberalization, and enterprise pollution reduction: Evidence from China. Front. Ecol. Evol. 10:965484. doi: 10.3389/fevo.2022.965484

Received: 09 June 2022; Accepted: 06 July 2022;

Published: 01 August 2022.

Edited by:

Di Bu, Macquarie University, AustraliaReviewed by:

Jie Tian, Chongqing Technology and Business University, ChinaDi Gao, Southwestern University of Finance and Economics, China

Copyright © 2022 Cai, Liu and Peng. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Qing Peng, cGVuZ3FpbmdfaGlAMTYzLmNvbQ==