Julia Pargmann

Julia Pargmann Florian Berding

Florian Berding- Department for Vocational Education and Lifelong Learning, Faculty of Education, Institute of Vocational and Business Education, University of Hamburg, Hamburg, Germany

Introduction: Sustainable transformation is critical in the face of today’s challenges, with business at the center of sustainable development. Students in vocational business education need to integrate sustainability into decision-making processes, which are often based on accounting and controlling. These form a significant operational foundation, which is why sustainability should play an essential role here. Teachers need appropriate content knowledge and knowledge of industry needs.

Methods: This study uses a PRISMA-led systematic review and qualitative content analysis to explore the current discourse. The aim is to derive starting points for adequate content knowledge. 79 full texts were analyzed that link sustainability to accounting and/or controlling.

Results: The literature shows a shift towards a comprehensive approach where sustainability permeates legal and profit-orientated operational aspects. Challenges exist in the integration of non-monetary information, with proposed solutions such as social and environmental accounting. Essential competences include sustainability awareness and ethical principles.

Discussion: The study emphasizes the need to integrate sustainability into education and recommends a process-oriented perspective to promote a multidimensional understanding.

1 Introduction

Accounting and controlling are fundamental elements for managing entrepreneurial success and promoting economic thinking (Chiapello, 2009; Preiß and Tramm, 1996). Seifried (2004) pointed out 20 years ago that accounting lessons should be expanded to include more and more controlling elements. Current global developments support this call: traditional accounting is increasingly being questioned, particularly as a result of digitalization (Klein and Küst, 2020; Pargmann et al., 2023). However, little seems to have changed; there is still a need in practice for more comprehensive controlling knowledge that goes beyond accounting and offers deeper insights into the management and control of companies (Schöning et al., 2020). In order to do justice to the operational relevance that accounting and management control have in theory, they must face modern challenges such as sustainability.

The concept of sustainability in accounting and controlling was previously understood to primarily entail the assurance of the company’s long-term viability. However, the advent of integrated non-financial reporting has also prompted a growing recognition of sustainability as a core aspect of accounting and control (Meeh-Bunse and Luer, 2016; Osburg, 2013). Presently, this is predominantly observed in the form of discrete sustainability management and controlling departments, rather than being integrated in a more comprehensive manner (Ghosh et al., 2019; Schaltegger, 2016). The implementation of sustainability efforts also necessitates the presence of suitably qualified employees, who facilitate corporate transformation toward sustainability (e.g., Berding et al., 2020; Bliesner-Steckmann, 2018; Gallagher et al., 2020). For a variety of reasons, not all companies demonstrate a commitment to pursuing sustainability. Some companies cite a lack of expertise, financial resources, or industry interest as reasons for their inaction. Others attempt to disguise unsustainable practices through green marketing and communications. Conversely, other organizations have already transitioned to more environmentally sustainable business models.

Accounting and controlling take on a vital role in vocational business education, as they facilitate students’ comprehension of economic correlations, causal chains and the ramifications of their own economic decisions. This process-oriented approach facilitates the application of knowledge in novel contexts and situations. The curriculum for accounting and controlling typically emphasizes an understanding of double entry bookkeeping as well as with traditional control instruments, such as SWOT analysis and various key performance indicators (KPIs), including return on investment (ROI) and ABC analysis. It is uncommon for students to complete the control cycle, omitting a central component designed to instruct them in the process of making economic decisions (Stütz, 2024). The control cycle is comprised of six steps that enable students to translate the theoretical domain of accounting into practice. The six steps are (1) orientation in the material, (2) translation into the real world, (3) working in the systems of accounting, (4) interpret results, (5) validate solutions and (6) decision making. In an analysis of 2,000 accounting and controlling tasks, Stütz (2024) shows that the last two steps that connect the results back to reality are often omitted. This might be due to a lack of action-orientation. In addition, few didactical concepts exist for the integration of sustainability into accounting and controlling lessons. This points to the issue of missing real world examples of how sustainability can be incorporated into accounting and controlling classes.

In recent years, there has been a notable surge in the number of publications on sustainability in accounting and controlling. In addition to examining the processes of sustainable transformation, these publications also address the competences that employees must possess in order to contribute to these changes. Other current reviews either focused on sustainability in accounting and controlling in general (i.e., Broccardo et al., 2024), on higher education accounting and controlling curricula (i.e., Frizon and Eugénio, 2022) or on sustainability accounting as a separate concept (i.e., Gil-Marín et al., 2022). The present review adds a process-oriented approach that makes the results useable for teaching practices, especially in German vocational education contexts. In order to successfully integrate sustainability into school wide accounting and controlling curricula, educators must first ascertain which types of content are relevant to their students’ vocation and then determine the manner in which these contents are connected to the various competence dimensions. The key problem in this article is the current scope of sustainability in business literature to derive teacher content knowledge.

To shed light on the relevant content knowledge for teachers in vocational accounting and controlling education, a systematic review of n = 79 publications was carried out using PRISMA guidelines (Page et al., 2021) and evaluated using qualitative content analysis (Kuckartz, 2018). Contributions to the following research questions will be made:

1. How is sustainability discussed in accounting and controlling literature? Which tools, processes and practices are relevant in this context?

2. Which sustainability-focused competences are discussed in accounting and controlling research and practice?

The aim of this article is (a) to gain insights into the state of the discussion on sustainability in accounting and controlling literature. Through this we aim to discover which content knowledge teachers who would like to incorporate sustainability into lessons (or sequences) focused on controlling or accounting need. Aim (b) is to derive the sustainability-related professional, methodological and social competence requirements teachers need to foster in their classes. As a result of this critical analysis, we extract implications for accounting and controlling classroom activities.

The remainder of this paper is structured as follows: First, the methodology is presented and the categories for the content analysis are deducted as a backdrop for the critical analysis. Then, the results will be reported, structured by the analytical categories. Lastly, the findings will be discussed and implications for vocational accounting and controlling education will be derived to help both research and practice to sharpen their efforts regarding vocational sustainability education.

2 Materials and methods

When designing this literature review, the preferred reporting items for systematic reviews and meta-analyses (PRISMA) (Page et al., 2021) were used to ensure a replicable search. We developed selection criteria, a consistent search strategy and a framework for data analysis. In the later stages of the analysis, we also performed a qualitative content analysis following Kuckartz (2018) to identify trends. Thus, this review follows PRISMA standards for record identification and retrieval but a qualitative content analysis framework for analysis.

2.1 Search strategy

We searched five electronic databases (Web of Science, PEDOCS, Google Scholar, EBSCO, and WISO) for the years 2000-2022. The databases were chosen because they provide literature from both the technical content side of business education as well as the pedagogical-didactical side. While Web of Science, Google Scholar and EBSCO are well known international databases, WISO and PEDOCS are only established in Germany. Since the German vocational education system has a unique structure that combines workplace learning and vocational schools, the curricula encompass a distinct connection to the current developments in businesses and industries (Fürstenau et al., 2014). To honor this connection, we included the WISO database, which offers more practice-related publications. This matches well with our goal to derive implications for competences, as we get to analyze developments from the industry that are specific to the German market. PEDOCS on the other hand is a database that offers publications from educational science. Internationally, accounting education is mostly a topic for higher education institutions (Kleinberg Neimark, 1996). Since this paper focuses on developing implications for vocational accounting education, it was appropriate to extend our search to databases that focus on educational science and are often published with the German educational system in mind. This makes it easier to connect the implications to the use cases of this paper. PEDOCS has been used in reviews before, such as by Herrmann and Gerlach (2020). Same is true for the WISO database, which was used by Niesen and Houy (2015).

We still searched for both English and German articles to reflect international discussions. Two researchers searched the databases using the same search terms to make aligned decisions on exclusion and inclusion. The search terms were grouped to search for sustainability and controlling/accounting literature as well as literature that includes competence, skills, or knowledge/expertise in this context. Table 1 presents an overview of keywords used. The search included titles, abstracts and full texts.

Table 1. List of Keywords.

2.2 Article selection criteria

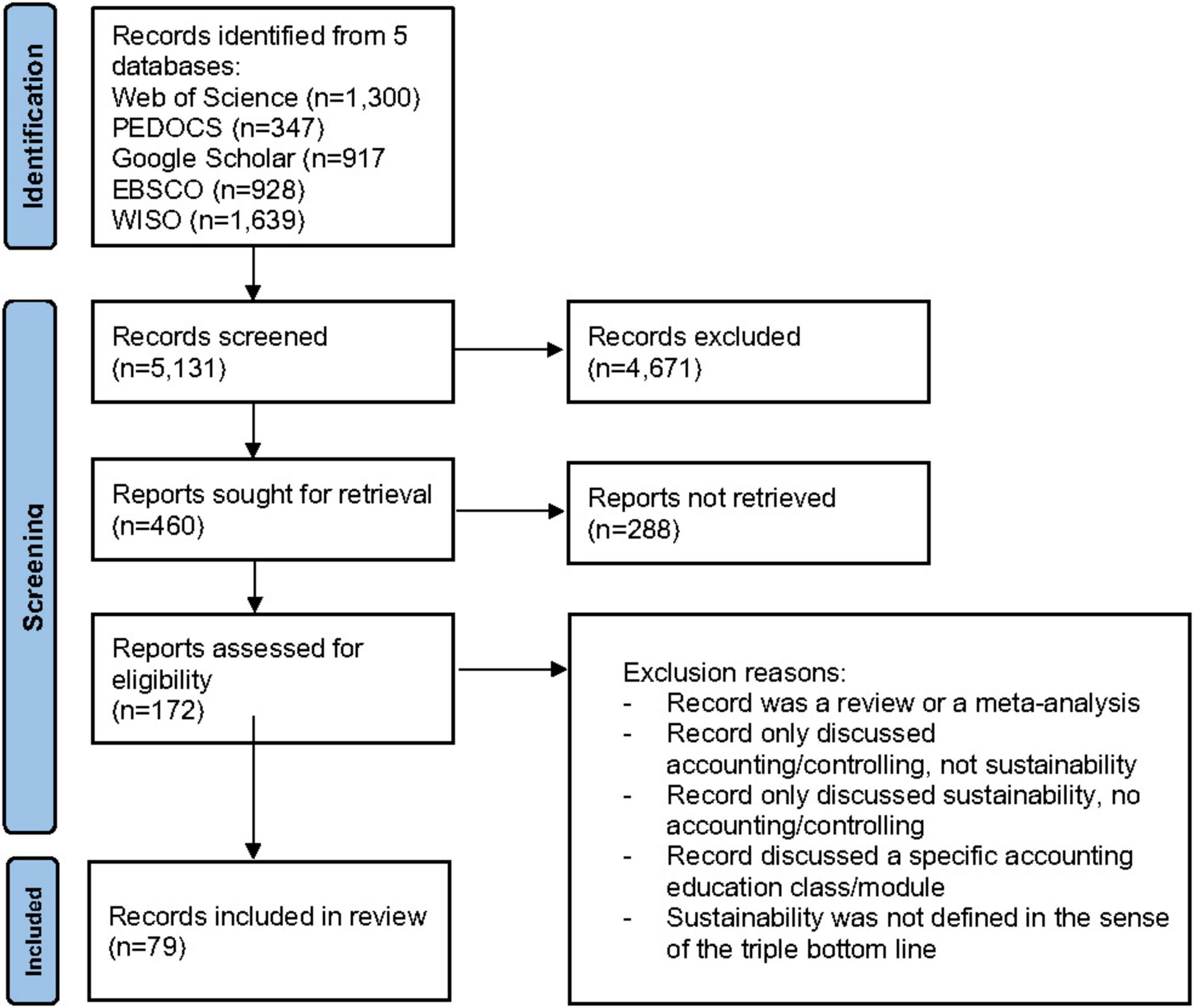

To identify as many suitable articles as possible, we determined the following selection criteria. Articles were excluded if they did not connect sustainability and controlling/accounting. Publications about accounting and controlling classes in higher education or case studies on higher education were also excluded, even if they had a distinct sustainability focus. Additionally, the screening excluded all publications which did not use a suitable definition of sustainability, i.e., in the sense of longevity. The review only includes original research or reports from practice (gray literature, book chapters, and working papers), no literature reviews or meta-analyses. The search strategy yielded 5,131 records for screening of which 4,671 were excluded right away as they did not connect the two perspectives of sustainability and controlling/accounting. We derived a total of n = 79 full texts for coding. Figure 1 shows the PRISMA flow diagram for this paper. A detailed list of the publications can be found in Supplementary Appendix A.

Figure 1. PRISMA flow diagram.

2.3 Qualitative content analysis

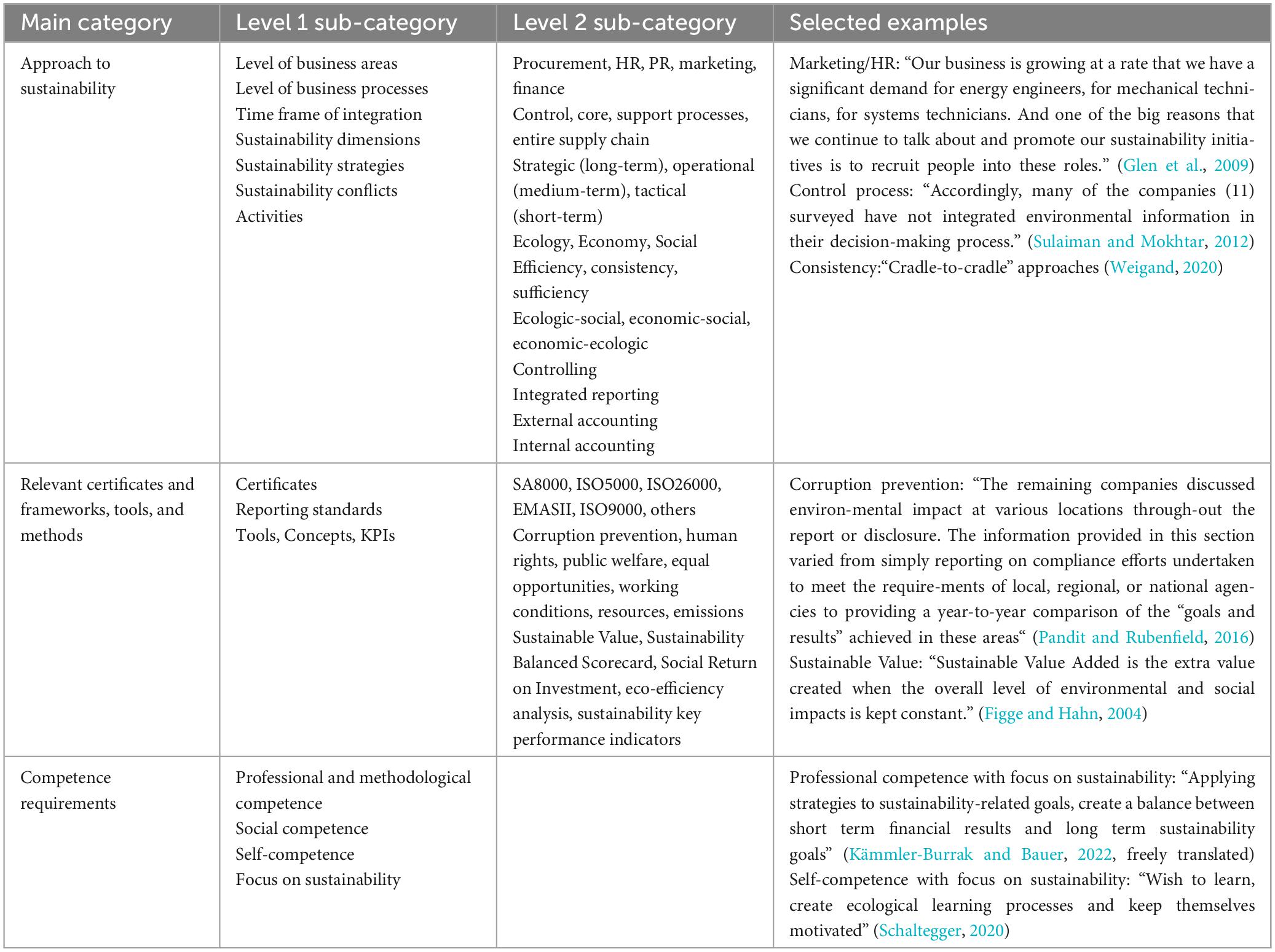

To gain structured insight into the topic, we performed a qualitative content analysis using inductive and deductive categories. The coding manual was developed using guidelines for qualitative content analysis (Kuckartz, 2018) and was carried out using the software MaxQDA (Release version 22.8.0). The full texts were coded using the analytical framework (Table 2). After baseline coding for alignment, the remainder was coded in pairs with regular discussion regarding inconsistencies.

Table 2. Analytical framework with sub-categories.

Most of the analytical framework was developed deductively, as the purpose of this paper is not to create a new systemization but rather to see how far the discourse on sustainability in controlling and accounting has progressed. The following categories were developed to enable a critical analysis:

• Approaches toward sustainability, sustainability dimensions, strategies, and conflicts: To identify where corporate sustainability efforts are located and how well companies have integrated sustainability into their supply chain, the approaches toward sustainability were coded by the relevant business process. The differentiation between controlling, core and support processes helps match sustainability contents with accounting and controlling activities (Gadatsch, 2017). The areas of activities were added because not every company, especially not small- and medium-sized enterprises (SME), are organized in a process-oriented manner (Wöhe et al., 2020). Here, sustainability efforts are closely intertwined between different areas of the business. The last three categories were included to develop an understanding of how companies conceptualize their sustainability efforts, how they define them and how long-term they think about the topic (Perridon et al., 2017). The most common definition of sustainability is a balance between the ecological, social, and economic dimensions (Schmidt, 2012) and a sustainable development requires a transformation that stops the exploitation of resources (World Commission on Environment and Development, 1987). Generally, sustainability efforts can follow one of three strategies: efficiency, consistency or sufficiency. Each of these strategies has its own risks and benefits and their implementation largely depends on the business model. In consequence, there are some conflicts that can be derived from the triple bottom line and the sustainability strategies, i.e., rebound effects. As these also affect controlling and accounting, they were included. We also inductively coded the motivation of companies to become more sustainable.

• Sustainability reporting, certificates, frameworks, tools and methods: Corporate sustainability efforts usually include some notion of corporate social responsibility and thus integrated reporting. Due to legislative developments, companies registered in the European Union that exceed the size of 500 employees and are of public interest are now obligated to report on their efforts in a suitable way, regulations for other enterprises are to follow in the coming years (European Union, 2022). For the purpose of this paper, it is of interest to identify reporting standards and certificates in which businesses have a particular interest in (Scholz and Pastoors, 2018). As we focus on controlling and accounting, the “tools and methods” category also includes key performance indicators (KPIs) used by companies. This is especially interesting because in vocational business education in Germany, the curricula use KPIs as means to illustrate impact relationships to students.

• Competences: In the German-speaking countries, the promotion of action competence is a crucial part of vocational education programs. This concept depicts the ability to solve occupational tasks successfully and to execute routine and non-routine activities. Typically, frameworks distinguish between professional, social and self-competences, with methodological and technological competences as interdisciplinary dimensions (Roth, 1971; Winther and Achtenhagen, 2008). Thus, we included the sub-category of “Focus on sustainability” to each competence dimension.

3 Results

3.1 The sample

Out of the 79 publications, 25 were journal articles, 33 were magazines, whitepapers or grey literature, three were conference proceedings, 15 were book chapters and three were monographs. Regarding the publishing years, three peaks can be identified in the years 2011, 2016 and in 2020/2021. Nineteen publications are from the period between 2001 and 2011, 60 were published between 2012 and 2022. Language-wise, most publications (n = 55) are German, the remainder (n = 24) are English. The specific characteristics of each publication are provided in the Supplementary material.

The next section presents the results for each of the main categories.

3.2 Content analysis results

3.2.1 Approaches toward sustainability

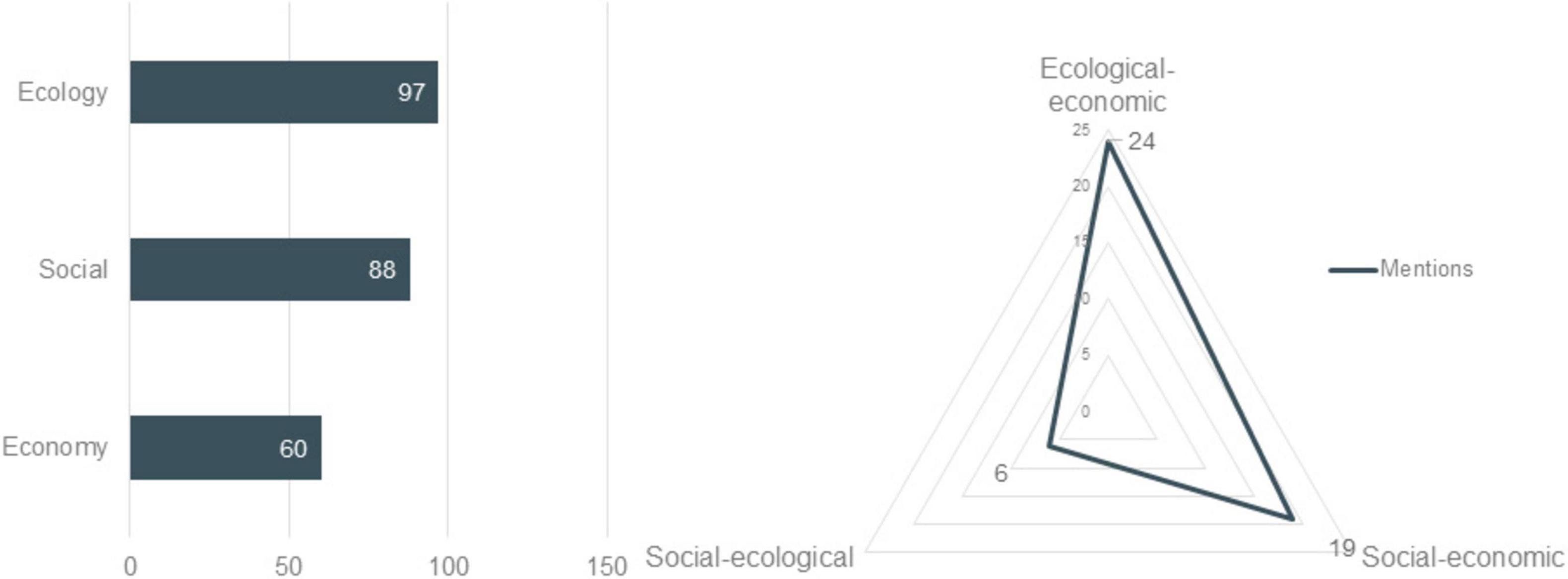

Few texts focus on the economic dimension of the triple bottom line (Figure 2, left). Instead, the ecological dimension is discussed most frequently, followed by the social dimension. The right side of Figure 2 shows that conflicts between the social and ecological dimension seem to be less important, as conflicts between economic and ecological decisions and economic and social decisions dominate.

Figure 2. Dimensions of the triple bottom line mentioned (left) and conflicts arising (right).

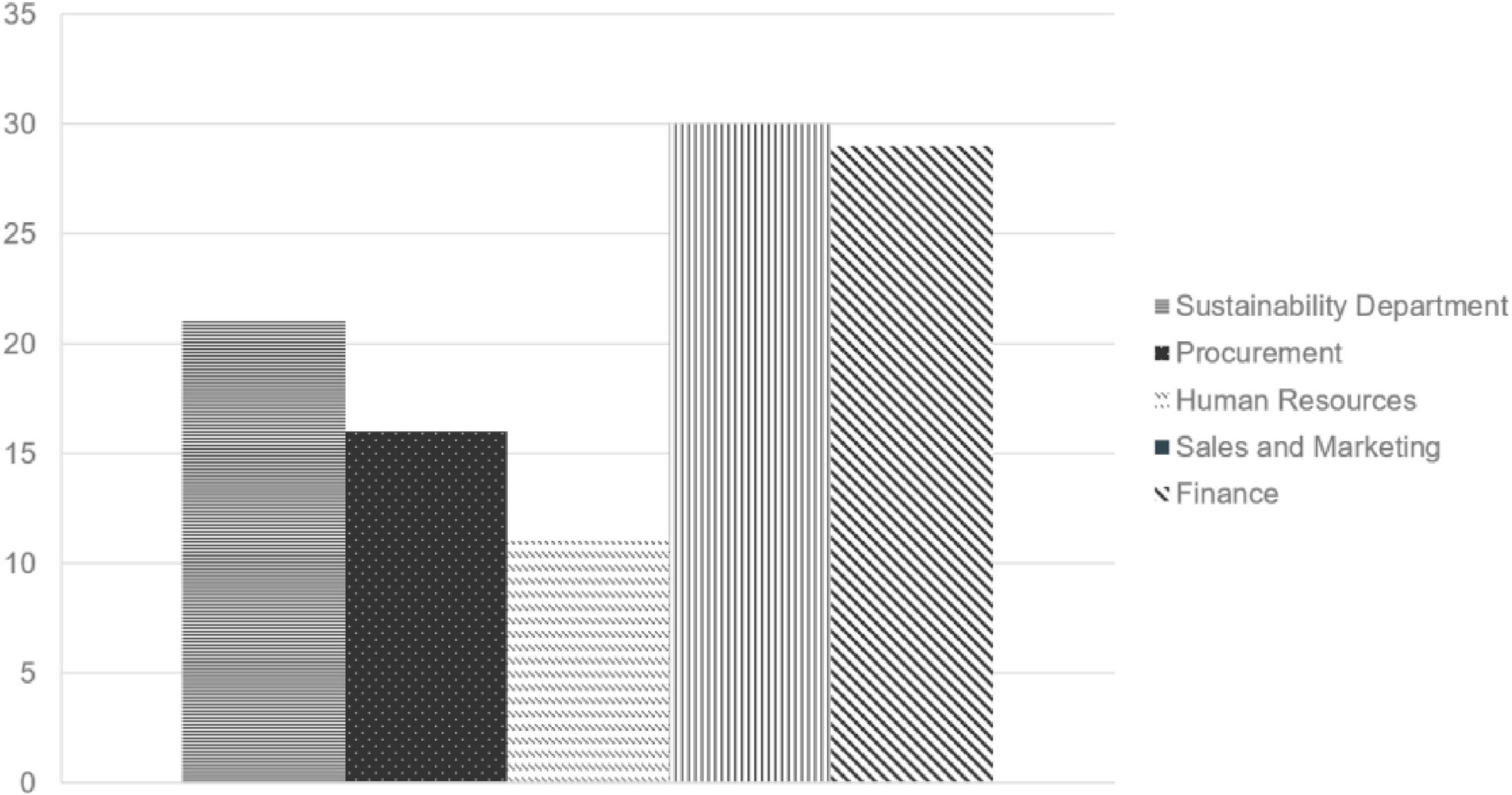

In the material, the departments most frequently discussed to be responsible for integrating sustainability into practice were sales and marketing, finance and the sustainability department (Figure 3). Less frequently, procurement and HR were mentioned.

Figure 3. Integration of sustainability on a departmental level (frequency of mentions).

The sustainability department was mentioned as a possible point of interaction with controlling/accounting because they aggregate corporate information from different areas of the business, generating an overview of environmental, social, and economic sustainability progress (Isensee and Michel, 2011). However, the degree of cooperation between the interfaces varies. While not all businesses have a sustainability department, those that do usually are the main locus of sustainability information for all other business areas (Michel et al., 2014). In contrast, employees in controlling and accounting do not see themselves as relevant stakeholders of the sustainability department and rarely keep up with their developments, unless they have a personal interest in the topic (Kämmler-Burrak and Bauer, 2022; Stehle and Stelkens, 2018).

In procurement, the sustainability efforts that are connected to controlling and accounting usually focus on the corporate supply chain’s emissions and resource consumption (Ferreira et al., 2010; Glanze, 2022; Krause, 2016). However, some publications mention progress in the sense of design for sustainability, procurement for sustainability or the development of more efficient and environmentally friendly means of production (Greiling and Ther, 2010; Isensee and Michel, 2011; Schaltegger, 2020; Schaltegger and Zvezdov, 2011).

Sustainability in HR mostly focuses on the social dimension through employee development and training, as well as the controlling of employee KPIs (Greiling and Ther, 2010; Weber et al., 2010). They are a stakeholder of the sustainability department because for an increasing number of potential employees, a company’s sustainability efforts are relevant in the application process. HR needs sustainability information to market the roles to applicants (Braun, 2019). It is also in the company’s interest that employees act in line with corporate strategy. This extends to sustainability-specific aspects. It is therefore necessary for HR to also offer further training in this area in cooperation with the sustainability department (Lacy et al., 2009). Regarding controlling, HR also records data relevant to the social dimension of sustainability, such as absence and sickness rates, workplace incidents and personal development hours, amongst others (Schwarzmaier, 2015).

The development of an “honest” marketing mix dominates the codings in the field of sales and marketing (Gebauer, 2013; Schaltegger and Zvezdov, 2011; Schwarzmaier, 2013). Braun (2019) even calls some CSR reports a mere marketing tool that is used strategically as a means of corporate communications. These reports provide little value to stakeholders as they lack substance (Gaggl, 2021). To enforce truly sustainable marketing efforts, reporting should be seen as an opportunity to realize the corporate sustainability strategy, i.e., by commenting on internal sustainability efforts and failures (Schwarzmaier, 2013; Weigand, 2020).

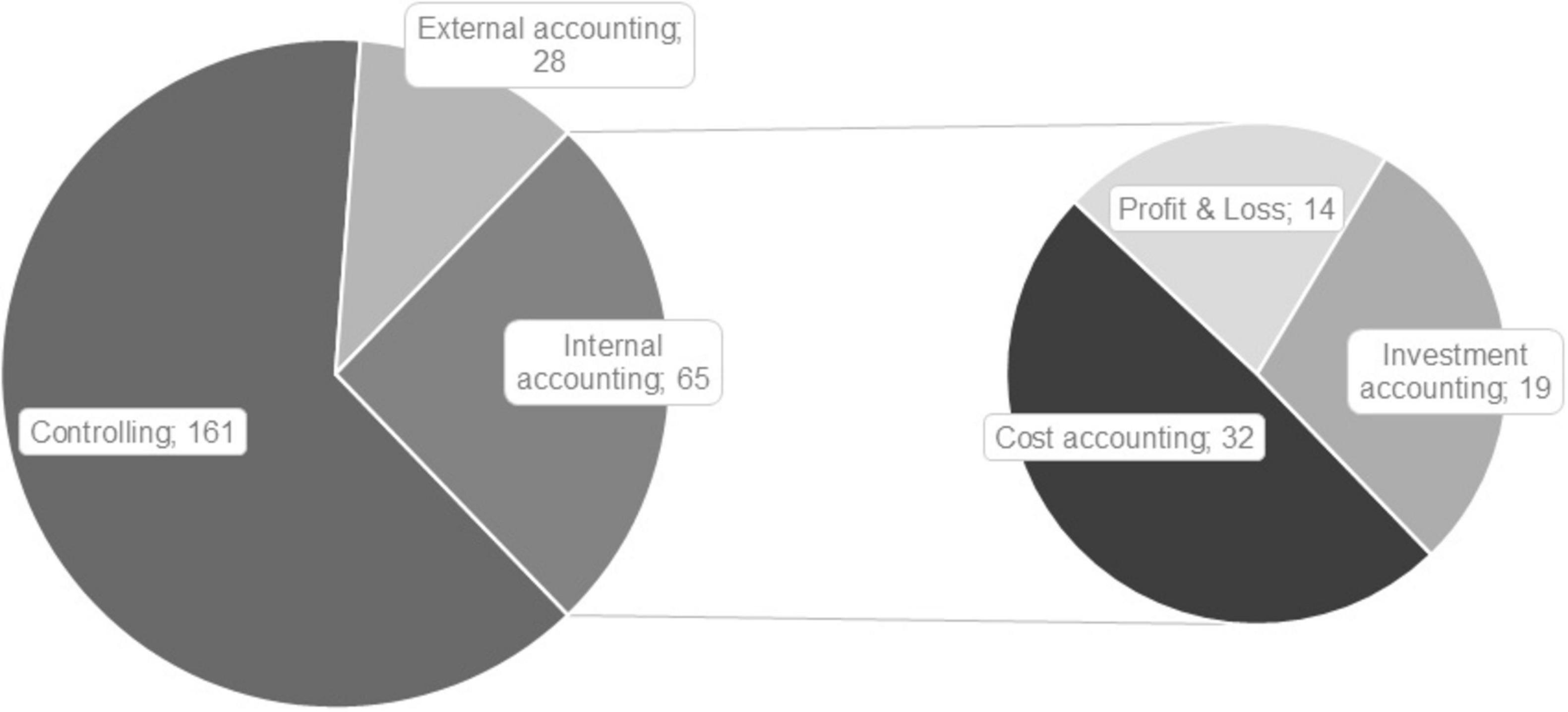

In the finance department, most codings relate to the area of controlling (Figure 4). These were coded whenever the area was mentioned in a sustainability context. The other areas like external and internal accounting (the latter represented by the different areas of cost accounting and investment accounting) were mentioned far less frequently, although explicitly included in the search terms (Table 1).

Figure 4. Coding distribution across different accounting and controlling departments with an overview on the left and a zoom into internal accounting on the right.

Most texts did not discuss new sustainability-oriented instruments for controlling but rather applied traditional tools to the new context (Wellbrock et al., 2020). Some traditional tools that are mentioned are ecology-oriented SWOT analysis, portfolio analysis, ABC-scoring, eco-efficiency indicators or ecological life cycle assessments (Greiling and Ther, 2010). Some publications specify controlling tools that are unique to the issue of sustainability, for example the “sustainable value” or the “sustainability balanced scorecard” (Figge and Hahn, 2004; Gaggl, 2021; Heimel and Momberg, 2021; Hubbard, 2009; Wellbrock et al., 2020). Fischer et al. (2010) and Michel et al. (2014) highlight the need of new KPIs that include the triple bottom line approach. Thus, new KPI systems need to be developed to ensure number-based reporting (Lühn et al., 2022). According to Aras and Crowther (2009) and Rönz and Ryba (2012) however, companies need guidance to develop these KPIs, as many sustainability aspects are difficult to quantify for accounting purposes.

Some publications discuss the connection between controlling and CSR departments, as both collect relevant data that requires profound sustainability expertise (Rönz and Ryba, 2012). Since most controlling employees are not sustainability experts, cooperation is needed to successfully develop and control the corporate sustainability strategy (Endenich and Trapp, 2019).

In both external and internal accounting, sustainability aspects were mostly discussed as supplemental to the regulations companies already follow (Günther and Stechemesser, 2011; Sulaiman and Mokhtar, 2012). In external accounting, most codings related to hardships that sustainable companies face when it comes to financial accounting and reporting. Sulaiman and Mokhtar (2012) specify that professional accounting bodies should require monetary information to be reported in the CSR reports, because only this will motivate companies to be serious about the integration of environmental issues into their accounting and control systems. Schwarzmaier (2015) adds that companies that report in Germany can use accounting instruments such as social balance sheets in addition to the traditional management reports. In cost accounting, it is an option to internalize costs, e.g., CO2 compensation. Some companies go a step further and prepare an ecology-oriented profit and loss statement that internalizes effects on ecology and values them at an internal cost rate (Michel et al., 2014).

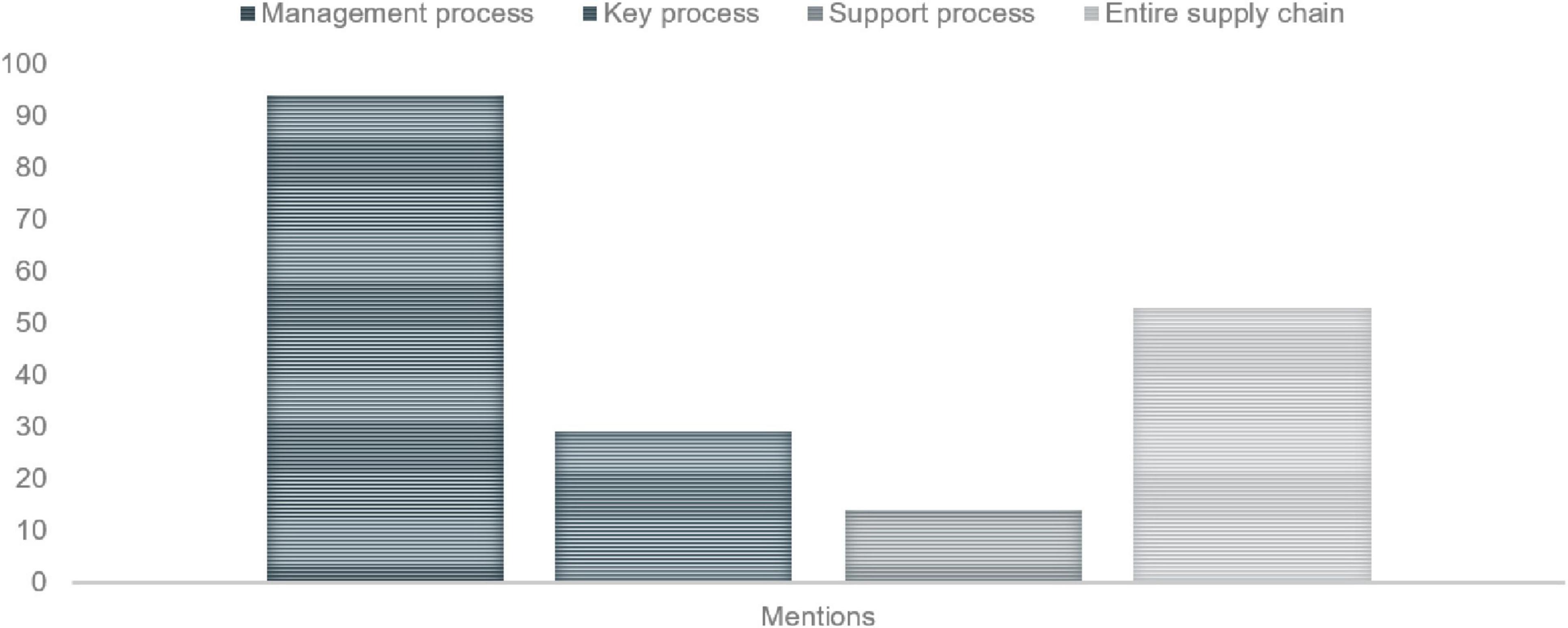

In addition to sustainability efforts on a departmental level, some aspects affect some or all parts of a business’ supply chain. The results for this category are presented in Figure 5. Most frequently, management and control processes as well as the entire supply chain were coded. Key and support processes were not coded as often.

Figure 5. Distribution of codings across different business processes.

Publications that discuss sustainability in management processes suggest that the topic can be integrated in multiple directions (Lacy et al., 2009; Olbert-Bock et al., 2015; Stehle and Stelkens, 2018). Sustainability should be integrated both top-down and bottom-up by engaging in continuous stakeholder dialogue. However, a significant amount of data is needed for adequate sustainability performance management within these processes. Another option is to incentivize sustainable decision-making (Schäffer, 2022). Additionally, non-financial information should be as relevant in management decisions as financial information and thus discussed as such in corresponding contexts (Sulaiman and Mokhtar, 2012). Some publications also discuss key processes such as production, logistics and procurement as appropriate options to promote sustainability (Ferreira et al., 2010; Fischer et al., 2010; Weber et al., 2010). This could be the reduction of scrap products and materials, resource and energy consumption, as well as the extension of product life. In support processes, sustainability takes on the form of employee habit change and the sustainability of the company itself (Krause, 2016; Weigand, 2020). This extends to aspects such as using recycled printing paper (or not printing at all), being conscious of cloud data and server energy usage, recycling in-house, using regenerative energy to power production sites and offices and donating to charity. Publications discussing a company’s entire supply chain mostly focus on the social dimension of sustainability by describing the impact on local labor laws and even environmental protection laws at production sites (Gaggl, 2021; Hubbard, 2009; Klute-Wenig and Refflinghaus, 2015; Rodriguez-Olalla and Aviles-Palacios, 2017; Schulz, 2014).

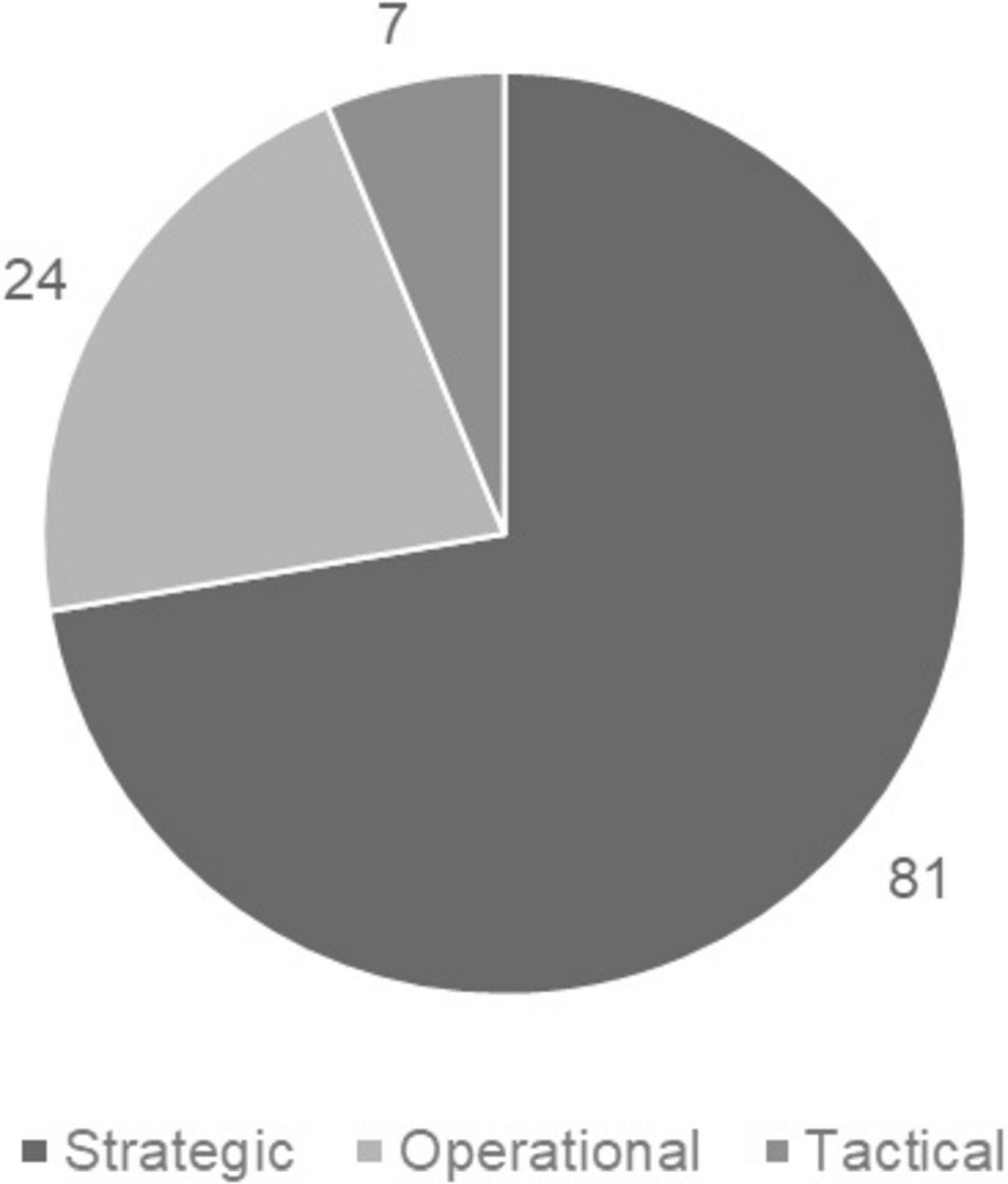

Additionally, most texts discuss a strategic integration of sustainability (n = 81 codings). Operative and tactical timeframes are mentioned less often (Figure 6).

Figure 6. Mentioned timeframe for sustainable transformation.

3.2.2 Sustainability reporting, certificates, frameworks, tools, and methods

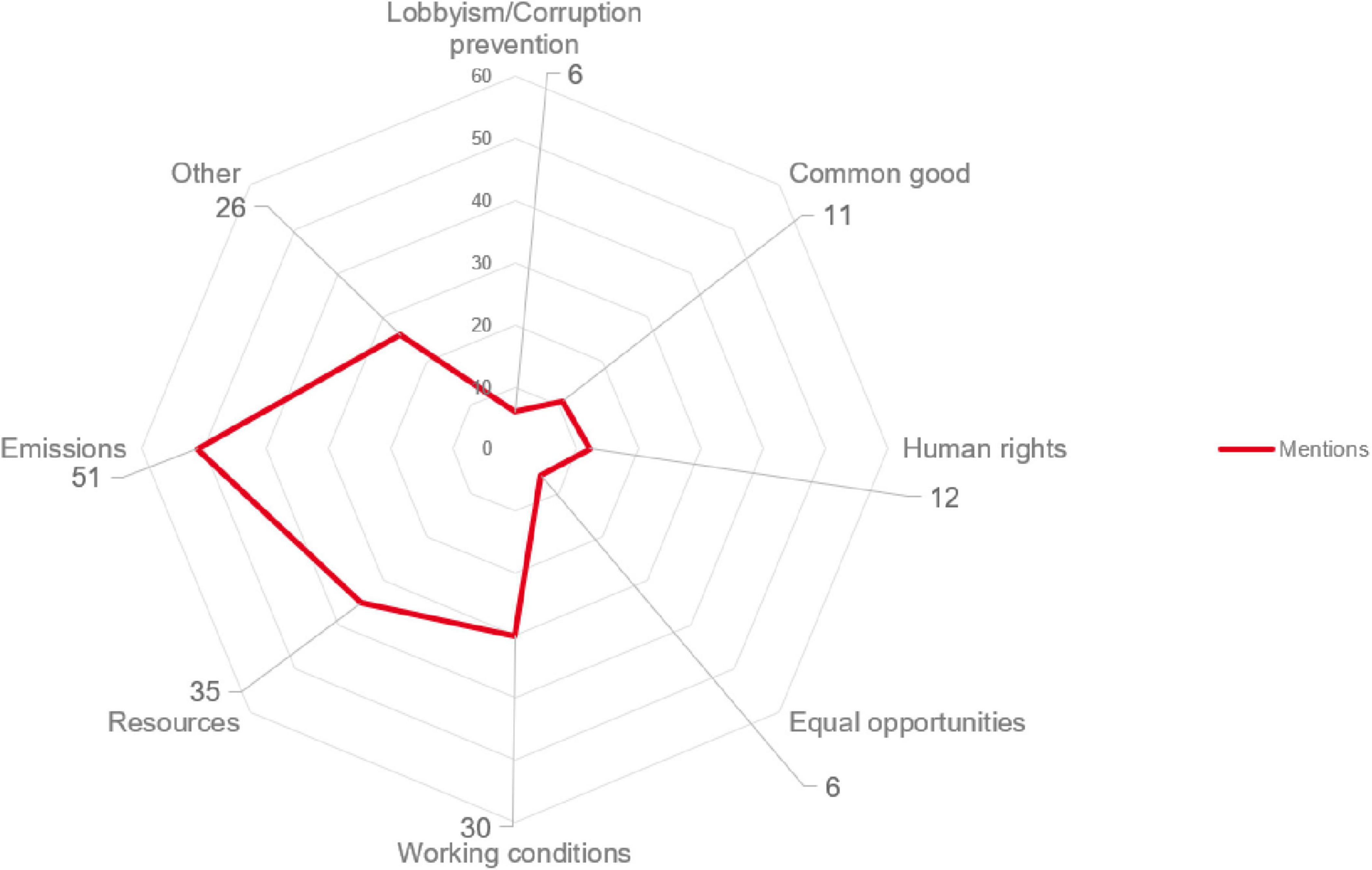

Regarding the non-financial data that companies reported on, a few trends can be identified in the publications (Figure 7). Most publications mention that companies use the GRI standards and focus on emissions, the exploitation of resources and work conditions (Gawenko et al., 2020; Pandit and Rubenfield, 2016; Rönz and Ryba, 2012; Weber et al., 2010). Less emphasis is put on creating equal opportunities, keeping human rights or fighting lobbyism and corruption (Schier and Bonnländer, 2018; Schmitz, 2021).

Figure 7. CSR reporting items mentioned by publications.

The tools that are mentioned in controlling and accounting codings go beyond more general calculations like KPIs with (n = 19) and without a sustainability focus (SKPI, n = 16) to more specific ones, such as eco efficiency analysis (n = 3), social return on investment (SROI, n = 2), sustainability balanced scorecard (SBSC, n = 19) and sustainable value (n = 9). The SBSC was frequently discussed from a goal-setting perspective, thus more useful as a starting point.

The general KPIs mentioned were rather specific control systems like economic value added (EVA) and total return on investment (Lux and Olbert-Bock, 2016; Schulze and Thomas, 2012; Schwarzmaier, 2013). Newer publications suggested SKPIs such as the recording of CO2 emissions, circular transition indicators or sustainable value added (Gaggl, 2021; Kämmler-Burrak and Bauer, 2022; Lühn et al., 2022). Additionally, newer publications also stressed the issue of data availability and standardization (Kämmler-Burrak and Bauer, 2022). In recent years, there has been an influx of KPIs and tools in sustainability controlling and accounting, most of which companies have developed themselves through benchmarking (Heimel and Momberg, 2021; Rönz and Ryba, 2012).

3.2.3 Competences

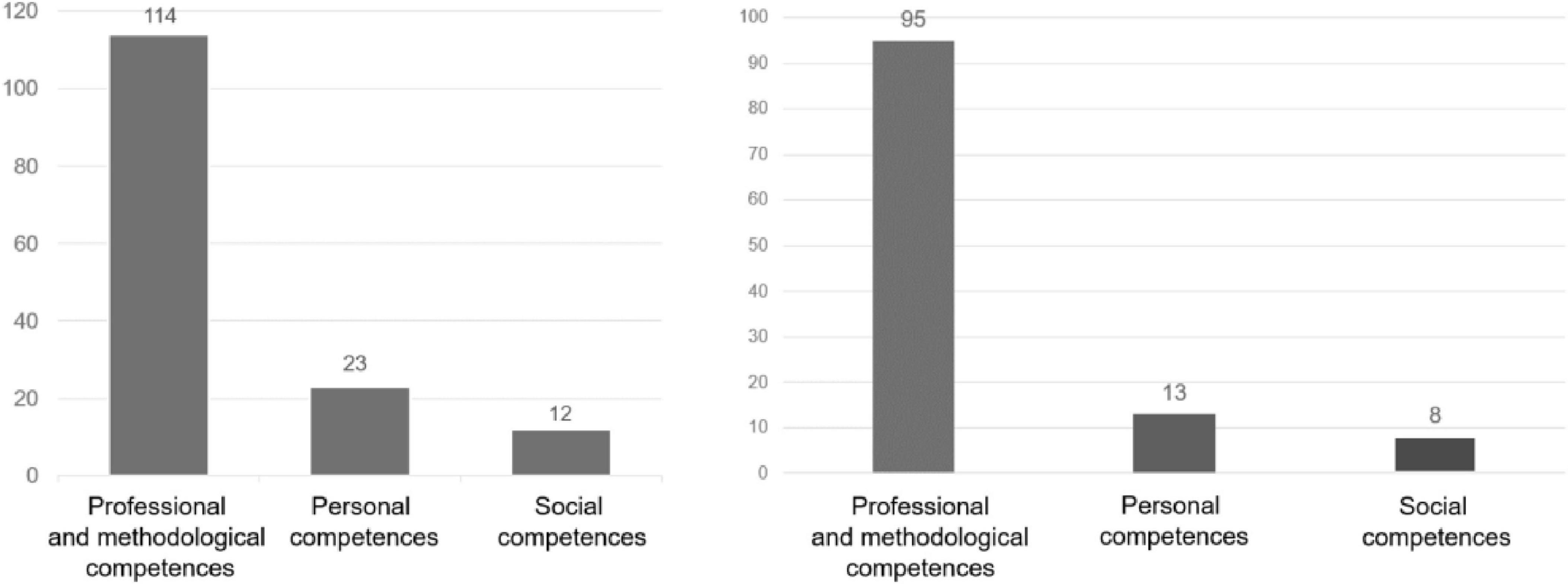

The competences discussed in the texts were presented in a general manner or with a focus on sustainability, since some competences are easily adaptable for different contexts (e.g., researching alternatives for products or developing new strategies), whereas others are only needed in specific sustainability-focused situations (e.g., the calculation of CO2 emissions or the corporate carbon footprint). In the n = 79 publications, professional and methodological competences were discussed the most frequently (Figure 8, left), social competences the least.

Figure 8. Distribution of the mentioned competence dimensions as a total (left) and with a sustainability focus (right).

Roughly 83% of the codings for professional and methodological competences are connected to sustainability in some way. In contrast, only 56% of personal competences and 66% of social competences can be connected to sustainability (Figure 8, right) (Hoekstra, 2020; Kämmler-Burrak and Bauer, 2022; Sneidere and Bumane, 2019; Tsiligiris and Bowyer, 2021).

Results from the professional and methodological dimension can be clustered into three key aspects: (1) sustainability knowledge, (2) knowledge about tools and KPIs, and (3) data and interface management. The first aspect touches on the development of professional knowledge about sustainability. Employees in controlling and accounting need to identify intersections between their area of expertise and potential sustainability aspects to analyze information potentially relevant for sustainability controlling processes (Gaggl, 2021). It is not required for them to become sustainability experts, but there is nuance: employees in controlling and accounting should be open to include sustainability-oriented tools and processes into their repertoire and be available to take on learning opportunities (Lühn et al., 2022; Schulz, 2014; Stehle and Stelkens, 2018). Especially the methodological skill can be developed to include the transformation of ecological and social effects into financial units (Weber et al., 2010). To aid this, companies need to train controllers as additional “sustainability managers” by developing their general skill of preparing management information (Schulz, 2014; Schulze and Thomas, 2012). Lastly, these employees need to be able to communicate the performance of management accounting reports or other regular external reporting and realize their value for controlling processes (Weber et al., 2010).

Regarding the second aspect, publications mention three relevant perspectives. Those concepts that are currently used need to be reevaluated for their suitability regarding a sustainable transformation. Thus, employees need to be able to measure, analyze, report, and evaluate financial data to quantify non-financial information, i.e., by adapting existing KPIs and/or tools (Clarke and O’Neill, 2005). In doing so, they need to apply legal frameworks and keep up with industry standards and best practices. When adaptation is not an option, new concepts need to be developed by defining new relevant KPIs that gather the corporate environmental and social impacts (Stehle and Stelkens, 2018). Necessary competences include benchmarking, risk analysis, stakeholder surveys and external ratings (Kämmler-Burrak and Bauer, 2022). When finally, all tools are up to date, they need to be competent in the use of the new tools, thus broadening their competences in measuring sustainability-relevant information (Hartmann et al., 2016). Then, employees should consider the fit with the corporate sustainability strategy and control accordingly. This might require new workflows (Schulze and Thomas, 2012).

The last aspect, data and interface management, considers the support of other potentially relevant departments and processes. Not all information relevant to sustainability is aggregated in a single department. Thus, departmental cooperation is required. Some publications suggest collaboration between the sustainability experts and those employees who now need to include sustainability in their activities (Fischer et al., 2010; Isensee and Michel, 2011). This can be done through an additional or integrated sustainability department. This reduces specialized technical knowledge that employees in controlling and accounting need to develop (Schaltegger, 2020).

Regarding social competences, publications primarily focus on cooperation, collaboration and communication. Employees are required to use high-quality data as a basis and keep it up to date by collaborating with other departments through empathy and initiative (Gebauer, 2013; Schubert and Gerhardt, 2021). This extends to the collection of relevant data from other departments, including the sustainability department (Fischer et al., 2010).

The personal competences can be divided into ethical guidelines and respecting values as well as identifying complexities and being willing to learn. Regardless of their personal opinion on sustainability, employees need to respect company values and guidelines in their recommendations (Walinska and Dobroszek, 2021) and produce comparable, reliable and consistent data and reports (Arora et al., 2022). Additionally, they need to put problems into larger contexts and derive implications for their actions (D’Amato et al., 2009).

The competence requirements clearly show that controllers need to expand their existing competences: a certain level of sustainability knowledge is required as well as the ability to navigate sustainability-oriented tools and key figures by adapting them or developing new ones. Data management is also important, as non-financial data may need to be transformed or communicated. Since sustainability data occurs everywhere in the company, controllers also have to manage interfaces. Overall, controllers do not need to be experts, but they do need to cooperate.

4 Discussion

4.1 Sustainability in the occupational reality of employees in controlling and accounting

The exploration of sustainability in accounting and controlling literature reveals a dynamic shift from a traditional perspective, which primarily aimed at securing the long-term existence of companies, to an integrated approach aligned with the three-pillar model. Notably, sustainability discussions have expanded beyond separate sustainability management and controlling departments, indicating a need for a more integrative approach within organizations. The literature highlights the challenges faced by companies, including a lack of expertise, financial resources, and industry interest, emphasizing the multifaceted nature of sustainability integration. Relevant tools and processes in controlling predominantly focus on KPIs, cost management, and sustainability KPIs, underscoring the need for a comprehensive understanding of both financial and non-financial aspects. Furthermore, the literature suggests the importance of sustainability-oriented information and tools that integrate sustainability into mainstream controlling processes rather than segregating it into a distinct sustainability controlling function.

The identified integration of sustainability initiatives spans across various organizational levels, ranging from dedicated sustainability departments to functions within sales, marketing, PR, and finance, here most often it is sustainability controlling. The predominant motivations driving this integration are legal compliance and profit optimization. The strategic implementation of sustainability measures is dominated by the economic dimension, emphasizing the prevalence of economic goal conflicts. The ecological dimension is affected through the reduction of emissions and resources, while the social dimension mostly considers working conditions, often interconnected with legal obligations such as labor laws.

The primary objective of controlling activities is to monitor and evaluate key performance indicators (KPIs) with and without a sustainability focus, and to assess their relationship with cost management. It is notable that there is an emphasis on capturing sustainability-relevant management information across the entire company. This is to be achieved by utilizing tools that consider sustainability holistically, rather than relying on separate sustainability controlling entities. In the domain of accounting, there are a number of challenges to be overcome. These include the incorporation of non-monetary information, such as the accrual of financial information, and the external reporting of non-financial aspects. A number of proposed solutions have been put forward. These include the amortization of costs through funds, the utilization of social balance sheets, or environmental investment calculations as complementary tools alongside traditional instruments like the income statement.

The discussion on sustainability-focused competences in accounting and controlling research and practice underscores the critical role of accounting and controlling in VET in driving corporate transformation toward sustainability. Students require general competences such as sustainability-related learning readiness, collaboration, identification, and adaptation of relevant tools and KPIs, understanding and addressing complexities and conflicts, and weighing ethical principles. The literature suggests that even in organizations with dedicated sustainability departments, controllers need to possess sustainability-related competences, indicating the pervasive nature of sustainability across different facets of business operations.

The identified competences extend beyond technical proficiency to include sustainability-related learning readiness, collaboration, and cooperation. Professionals need to identify and potentially develop or adapt relevant tools and metrics, recognizing the evolving nature of sustainability metrics. The literature focuses on the importance of understanding complexities and conflicts to enable students to propose viable solutions as change agents. In addition, personal competence should balance personal and organizational (ethical) principles, which are both crucial for navigating sustainability decision-making.

Synthesizing these insights, the literature points toward a paradigm shift in organizational practices, where sustainability is a strategic imperative while considering economic implications. The competences highlighted serve as a starting point to develop critical implications for vocational education. These indicate the need for a comprehensive and dynamic curriculum that not only imparts technical knowledge but cultivates a holistic perspective on the complexities and ethical dimensions of sustainable decision-making as change agents.

4.2 Implications for teacher content knowledge and curriculum design

Combining the results described above and the central arguments from the discussion with the critical perspective on sustainability in accounting and controlling developed in the introduction, the following implications should be considered to include a sustainability-forward approach in accounting and controlling lessons:

• The integration of sustainability in learning scenarios to connect the increasing relevance of sustainability in decision-making processes. Instead of a selective approach, teachers need to view sustainability in controlling as an intersectional topic that affects students in multiple dimensions.

• Connecting to this, educators need to be aware of alternative controlling and accounting tools and KPIs that they can add to their repertoire. They need to be able to research relevant additions to the school-wide curriculum and integrate them into learning scenarios. In this context, controlling educators should also consider the importance of non-financial KPIs and their potential for learning opportunities as they may aid to illustrate conflicts and foster valuable learning opportunities as they connect the dimensions of economics, business management and legal.

• Educators should include the premise of economic sustainability as the primary goal to employ sustainability conflicts in a didactically beneficial manner, rather than to make the students feel demotivated. Students will need to develop a set of competences that helps them drive organizational change as part of their vocational action competence. For this, it might be helpful to discuss alternatives and best practice examples.

• A deepened business process orientation that focuses on management processes to enable students to take on a multidimensional approach. German vocational business education is, in theory, inherently process-oriented; thus, the development of sustainability integrated processes may uncover potential starting points for lesson planning. When discussing the entire supply chain, sustainability-oriented aspects need to be considered to depict the corporate situation holistically. In addition, discussing business processes helps illustrate conflicts between sustainability dimensions because it illustrates cause-and-effect chains.

4.3 Limitations

There are some limitations to this review that need to be discussed. Although with PRISMA, we used a standardized strategy, we cannot control “intelligent” search algorithms that use geolocalization (particularly with Google Scholar) and smart indexing. This might also explain the uneven language distribution. Although we searched for the same keywords in English and German, we retrieved more German than English publications. We prioritized publications that would give us insights into relevant content knowledge for vocational business education and, more specifically, the area of accounting and controlling. It is very likely that we missed publications that showcase sustainability efforts but do not do so in the context of accounting and controlling. Additionally, no case studies about higher education contexts were included as we focused on developments in the relevant academic field. These two aspects might have limited the scope of the papers that we analyzed. Another limitation is the uneven distribution of controlling and accounting. Controlling literature was predominant as external accounting often faces legal constraints. Thus, we naturally identified more implications for this area. In addition, there is another content-related limitation as in German concepts, controlling only comprises internal accounting and is decision-oriented, whereas internationally, a more integrated approach is common (Beckers, 2010). Thus, the data basis controllers use is different. These variations have grown historically and hence contributed to different views on the roles of controllers. Through this we might have unintentionally excluded papers using different vocabulary than us. As a consequence, this literature review is neither exhaustive nor representative for the discourse but rather serves as a starting point for discussions about relevant teacher content knowledge.

5 Conclusion

This research paper sheds light on the role of sustainability in accounting and controlling, with a particular emphasis on its implications for vocational education. The study provides valuable insights into how sustainability is discussed in accounting and controlling literature and the competences essential for practitioners in this field:

In the context of vocational education, the study proposes implications for accounting and controlling teachers. It advocates for the integration of sustainability into learning scenarios to align with the increasing relevance of sustainability in decision-making processes. The paper emphasizes the need for teachers to be aware of alternative tools and KPIs, fostering a proactive approach to researching and integrating relevant additions into the curriculum. Additionally, ethical considerations are highlighted, acknowledging the potential dissonance between personal values and corporate practices that students may encounter in their future careers. The study encourages a deepened business process orientation to enable students to take on a multidimensional approach and emphasizes the development of sustainable controlling and accounting action competences. In essence, the research not only contributes to understanding where companies are currently at regarding sustainability in accounting and controlling literature but also provides practical guidance for vocational education, urging educators to adapt their approaches to equip students with the necessary competences for a future where sustainability is integral to corporate decision-making. The implications drawn from this research paper hold particular relevance within the context of the vocational education system in Germany. German vocational business education has long been renowned for its emphasis on practical training and its early and thorough integration into the workforce. As the study highlights the topic’s increasing importance, it becomes imperative to consider how these findings can be effectively incorporated into research for accounting and controlling didactics in vocational business education. New concepts need to be developed, trialed and established to develop the fitting content knowledge.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Author contributions

JP: Conceptualization, Data curation, Formal analysis, Methodology, Visualization, Writing – original draft. FB: Conceptualization, Supervision, Writing – review & editing.

Funding

The author(s) declare that no financial support was received for the research and/or publication of this article.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Generative AI statement

The authors declare that no Generative AI was used in the creation of this manuscript.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Supplementary material

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/feduc.2025.1519350/full#supplementary-material

References

Aras, G., and Crowther, D. (2009). Corporate sustainability reporting: A study in disingenuity? J. Bus. Ethics 87, 279–288. doi: 10.1007/s10551-008-9806-0

Arora, M. P., Lodhia, S., and Stone, G. (2022). Enablers and barriers to the involvement of accountants in integrated reporting. Meditari Account. Res. 30, 676–709. doi: 10.1108/MEDAR-11-2020-1102

Berding, F., Slopinski, A., and Frerichs, R. (2020). Auszubildende als zukünftige change agents for sustainable innovations. Betriebswirtschaftliche Forschung und Praxis 72, 313–337.

Bliesner-Steckmann, A. (2018). Handlungstheoretisch fundierte Didaktik nachhaltiger Berufsbildung. Springer Fachmedien Wiesbaden. doi: 10.1007/978-3-658-19741-4

Braun, S. (2019). Nachhaltigkeitsberichterstattung: Im Spannungsfeld unterschiedlicher Anforderungen und Interessen. Ökologisches Wirtschaften 33, 22–24. doi: 10.14512/OEW340222

Broccardo, L., Giordino, D., Yaqub, M. Z., and Alshibani, S. (2024). Implementing sustainability: What role do knowledge management and management accounting play? Agenda for environmentally friendly businesses. Corporate Soc. Responsibil. Environ. Manag. 32, 383–403. doi: 10.1002/csr.2936

Chiapello, E. (2009). “Die Konstruktion der Wirtschaft durch das Rechnungswesen,” in Diskurs und Ökonomie: Diskursanalytische Perspektiven auf Märkte und Organisationen, eds R. Diaz-Bone and G. Krell (Wiesbaden: VS), 125–149. doi: 10.1007/978-3-531-91914-0_6

Clarke, K., and O’Neill, S. (2005). Is the Environmental Professional an Accountant? Greener Management International. Austin: Greenleaf Publishing, 111–124. doi: 10.9774/GLEAF.3062.2005.sp.00011

D’Amato, A., Roome, N., and Lenssen, G. (2009). Toward an integrated model of leadership for corporate responsibility and sustainable development: A process model of corporate responsibility beyond management innovation. Corporate Governance Int. J. Effect. Board Performance 9, 421–434. doi: 10.1108/14720700910984972

Endenich, C., and Trapp, R. (2019). “Nachhaltigkeitscontrolling in Klein- und Mittelunternehmen,” in Controlling – Aktuelle Entwicklungen und Herausforderungen: Digitalisierung, Nachhaltigkeit und Spezialaspekte, eds B. Feldbauer-Durstmüller and S. Mayr (Wiesbaden: Springer Fachmedien Wiesbaden), 229–246. doi: 10.1007/978-3-658-27723-9_10

European Union. (2022). Directive (EU) 2022/2464 of the European Parliament and of the Council. Brussels: European Union.

Ferreira, A., Moulang, C., and Hendro, B. (2010). Environmental management accounting and innovation: An exploratory analysis. Account. Auditing Accountability J. 23, 920–948. doi: 10.1108/09513571011080180

Figge, F., and Hahn, T. (2004). Sustainable value added—Measuring corporate contributions to sustainability beyond eco-efficiency. Ecol. Econ. 48, 173–187. doi: 10.1016/j.ecolecon.2003.08.005

Fischer, T. M., Huber, R., and Sawczyn, A. (2010). Nachhaltige unternehmensführung als herausforderung für das controlling. CON 22, 222–230. doi: 10.15358/0935-0381-2010-4-5-222

Frizon, J., and Eugénio, T. (2022). Recent developments on research in sustainability in higher education management and accounting areas. Int. J. Manag. Educ. 20:100709. doi: 10.1016/j.ijme.2022.100709

Fürstenau, B., Pilz, M., and Gonon, P. (2014). “The dual system of vocational education and training in Germany – What can be learnt about education for (other) professions,” in International Handbook of Research in Professional and Practice-based Learning, eds S. Billett, C. Harteis, and H. Gruber (Wiesbaden: Springer), 427–460. doi: 10.1007/978-94-017-8902-8_16

Gadatsch, A. (2017). Grundkurs Geschäftsprozess-Management: Analyse, Modellierung, Optimierung und Controlling von Prozessen. Wiesbaden: Springer Vieweg. doi: 10.1007/978-3-658-17179-7

Gaggl, P. (2021). “Nachhaltigkeitscontrolling: Wie nichtfinanzielle informationen zum werttreiber werden,” in Funktions-Controlling: Praxishandbuch für Unternehmen, Non-Profit-Organisationen und die öffentliche Verwaltung, eds R. Eschenbach, J. Baumüller, and H. Siller (Wiesbaden: Springer Fachmedien Wiesbaden), 327–364. doi: 10.1007/978-3-658-33118-4_13

Gallagher, V. C., Porter, T. H., and Gallagher, K. P. (2020). Sustainability change agents: Leveraging political skill and reputation. J. Organ. Change Manage. 33, 181–195. doi: 10.1108/JOCM-01-2018-0031

Gawenko, W., Richter, F., Hinz, M., and Götze, U. (2020). Interne ansätze zur nachhaltigkeitsbewertung in der externen berichterstattung. Konzeptionelle und empirische analyse der DAX-unternehmen. Nomos Verlagsgesellschaft 74, 264–284. doi: 10.5771/0042-059X-2020-3-264

Gebauer, J. (2013). Die zukunft der nachhaltigkeitsberichterstattung III und IV/IV: Glaubwürdigkeit können nur die unternehmen selbst herstellen. Ökologisches Wirtschaften 28, 8–9. doi: 10.14512/oew.v28i1.1247

Ghosh, B., Herzig, C., and Mangena, M. (2019). Controlling for sustainability strategies: Findings from research and directions for the future. J. Manage. Control 5–24. doi: 10.1007/s00187-019-00279-8

Gil-Marín, M., Vega-Muñoz, A., Contreras-Barraza, N., Salazar-Sepúlveda, G., Vera-Ruiz, S., and Losada, A. V. (2022). Sustainability accounting studies: A metasynthesis. Sustainability 14:9533. doi: 10.3390/su14159533

Glanze, E. (2022). Kompass für green change: Das reifegradmodell des betrieblichen nachhaltigkeitsmanagements. OrganisationsEntwicklung 3, 103–107.

Glen, J., Hilson, C., and Lowitt, E. (2009). The emergence of green talent. Bus. Strategy Rev. 20, 52–56. doi: 10.1111/j.1467-8616.2009.00631.x

Greiling, D., and Ther, D. (2010). “Leistungsfähigkeit des sustainable value-ansatzes als instrument des sustainability controlling,” in Corporate Sustainability: Der Beitrag von Unternehmen zu einer nachhaltigen Entwicklung in Wirtschaft und Gesellschaft, ed. H. K. Prammer (Wiesbaden: Gabler), 37–68. doi: 10.1007/978-3-8349-8991-8_3

Günther, E., and Stechemesser, K. (2011). Instrumente des green controllings: Ein blick zurück, ein blick nach vorn. Controlling 23, 417–423. doi: 10.15358/0935-0381-2011-8-9-417

Hartmann, F., Maas, K., and Perego, P. (2016). “Den wald vor lauter Bäumen nicht sehen: Controller auf der Suche nach Nachhaltigkeit,” in CSR und Controlling: Unternehmerische Verantwortung als Gestaltungsaufgabe des Controlling, eds E. Günther and K.-H. Steinke (Berlin: Springer Berlin Heidelberg), 71–82. doi: 10.1007/978-3-662-47702-1_5

Heimel, J., and Momberg, M. (2021). “Sustainable finance: Nachhaltigkeitscontrolling zur Steuerung des sozialen und ökologischen Wirtschaftens von Unternehmen,” in Nachhaltiger Konsum: Best Practices aus Wissenschaft, Unternehmenspraxis, Gesellschaft, Verwaltung und Politik, eds W. Wellbrock and D. Ludin (Wiesbaden: Springer Fachmedien Wiesbaden), 83–106. doi: 10.1007/978-3-658-33353-9_6

Herrmann, C., and Gerlach, E. (2020). Unterrichtsqualität im fach sport – Ein Überblicksbeitrag zum Forschungsstand in Theorie und Empirie. Unterrichtswissenschaft 48, 361–384. doi: 10.1007/s42010-020-00080-w

Hoekstra, R. (2020). SNA and beyond: Towards a broader accounting framework that links the SNA, SDGs and other global initiatives. Stat. J. IAOS 36, 657–675. doi: 10.3233/SJI-200653

Hubbard, G. (2009). Measuring organizational performance: beyond the triple bottom line. Bus. Strategy Environ. 18, 177–191. doi: 10.1002/bse.564

Isensee, J., and Michel, U. (2011). Green controlling - Die Rolle des controllers und aktuelle entwicklungen in der praxis. Controlling 23, 436–442. doi: 10.15358/0935-0381-2011-8-9-436

Kämmler-Burrak, A., and Bauer, R. (2022). Nachhaltigkeit wird standardaufgabe im controlling. Controller Magazin 1, 24–29.

Klein, J., and Küst, C. (2020). “Wie die digitalisierung im rechnungswesen die Aufgaben und Anforderungen an die Mitarbeiter/-innen verändert,” in Moderner Rechnungswesenunterricht 2020: Status quo und Entwicklungen aus wissenschaftlicher und praktischer Perspektive, eds F. Berding, H. Jahncke, and A. Slopinski (Wiesbaden: Springer VS), 83–97. doi: 10.1007/978-3-658-31146-9_5

Kleinberg Neimark, M. (1996). Caught in the squeeze: An essay on higher education in accounting. Crit. Perspect. Account. 7, 1–11. doi: 10.1006/cpac.1996.0001

Klute-Wenig, S., and Refflinghaus, R. (2015). Integrating sustainability aspects into an integrated management system. TQM J. 27, 303–315. doi: 10.1108/TQM-12-2013-0128

Krause, H.-U. (2016). Controlling-Kennzahlen für ein nachhaltiges Management: Ein umfassendes Kompendium kompakt erklärter Key Performance Indicators. Berlin: De Gruyter. doi: 10.1515/9783110460636

Kuckartz, U. (2018). Qualitative Inhaltsanalyse. Methoden, Praxis, Computerunterstützung. Weinheim: Beltz.

Lacy, P., Arnott, J., and Lowitt, E. (2009). The challenge of integrating sustainability into talent and organization strategies: Investing in the knowledge, skills and attitudes to achieve high performance. Corporate Governance Int. J. Effect. Board Performance 9, 1–0. doi: 10.1108/14720700910985025

Lühn, M., Nuzum, A.-K., Petersen, H., and Schaltegger, S. (2022). Controller und nachhaltigkeit im kontext neuer berichterstattungspflichten. Rethinking Finance 1, 25–33.

Lux, W., and Olbert-Bock, S. (2016). Strategisches controlling als teil des sustainability performance managements - auch für KMU. Controller Magazin 5, 4–12.

Meeh-Bunse, G., and Luer, K. (2016). Zur Abbildung der Nachhaltigkeit im Rechnungswesen - ein Bezugsrahmen und Operationalisierungsvorschläge für den Mittelstand unter einer sich wandelnden Ethik. Współczesne Problemy Ekonomiczne 12, 103–113. doi: 10.18276/wpe.2016.12-09

Michel, U., Isensee, J., and Stehle, A. (2014). “Sustainability controlling: Planung, steuerung und kontrolle der realisierung der nachhaltigkeitsstrategie,” in CSR und Finance, eds T. Schulz and S. Bergius (Berlin: Springer Berlin Heidelberg), 97–112. doi: 10.1007/978-3-642-54882-6_6

Niesen, T., and Houy, C. (2015). “Zur Nutzung von Techniken der Natürlichen Sprachverarbeitung für die Bestimmung von Prozessmodellähnlichkeiten – Review und Konzeptentwicklung,” in Wirtschaftsinformatik Proceedings, eds O. Thomas and F. Teuteberg 1829–1843.

Olbert-Bock, S., Bussmann, C., Lux, W., and Garrels, S. (2015). Nachhaltigkeitsmanagement erfolgreich im Unternehmen professionalisieren. IM+io Fachmagazin 3, 50–57.

Osburg, T. (2013). Soziale innovationen und csr. Chancen für controlling. Controll. Manage. Rev. 57, 18–25. doi: 10.1365/s12176-013-0777-3

Page, M. J., McKenzie, J. E., Bossuyt, P. M., Boutron, I., Hoffmann, T. C., Mulrow, C. D., et al. (2021). The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. Syst. Rev. 10:89. doi: 10.1186/s13643-021-01626-4

Pandit, G. M., and Rubenfield, A. J. (2016). The current state of sustainability reporting by smaller S&P 500 companies. CPA J. 86, 52–57.

Pargmann, J., Riebenbauer, E., Flick-Holtsch, D., and Berding, F. (2023). Digitalisation in accounting: A systematic literature review of activities and implications for competences. Empirical Res. Vocat. Educ. Training 15:1. doi: 10.1186/s40461-023-00141-1

Perridon, L., Rathgeber, A. W., and Steiner, M. (2017). Finanzwirtschaft der Unternehmung. Munchen: Verlag Franz Vahlen. doi: 10.15358/9783800652686

Preiß, P., and Tramm, T. (1996). “Die göttinger unterrichtskonzeption des wirtschaftsinstrumentellen rechnungswesens,” in Rechnungswesenunterricht und ökonomisches Denken, eds P. Preiß and T. Tramm (Wiesbaden: Gabler), 222–323. doi: 10.1007/978-3-322-96343-7_8

Rodriguez-Olalla, A., and Aviles-Palacios, C. (2017). Integrating sustainability in organisations: An activity-based sustainability model. Sustainability 9:1072. doi: 10.3390/su9061072

Rönz, M., and Ryba, M. (2012). Kennzahlen in nachhaltigkeitsberichten. Controller Magazin Heft 5, 87–91.

Roth, H. (1971). Pädagogische Anthropologie, Band 2. Entwicklung und Erziehung. Grundlagen einer Entwicklungspädagogik. Hannover: Jahr.

Schäffer, U. (2022). Nachhaltigkeit und controlling: Ein aufruf zum handeln. Controller Magazin 1, 6–10.

Schaltegger, S. (2016). CSR, nachhaltigkeit und controlling – Zwischen Praxislücke und forschungskonzepten. CSR Controll. 55–69. doi: 10.1007/978-3-662-47702-1_4

Schaltegger, S. (2020). Nachhaltigkeit als treiber des unternehmenserfolgs: Ein mehrperspektivischer controllingansatz. Rethinking Finance 2, 34–39.

Schaltegger, S., and Zvezdov, D. (2011). Konzeption und praxis des nachhaltigkeitscontrollings. Controlling 23, 430–435. doi: 10.15358/0935-0381-2011-8-9-430

Schier, M., and Bonnländer, A. (2018). Nachhaltigkeit als teil der geschäftsstrategie. Die Bank 3, 38–41. doi: 10.15358/0935-0381-2011-8-9-430

Schmidt, O. (2012). Von den wurzeln der nachhaltigkeit: Vor drei jahrhunderten erfand die forstwirtschaft das prinzip der nachhaltigkeit. LWF aktuell 50–51.

Schmitz, H. (2021). GRI-Nachhaltigkeitskennzahlen für das controlling im mittelstand. Controller Magazin 5, 60–61.

Scholz, U., and Pastoors, S. (2018). “Betriebliche nachhaltigkeit,” in Praxishandbuch Nachhaltige Produktentwicklung, eds U. Scholz, S. Pastoors, J. H. Becker, D. Hofmann, and R. van Dun (Berlin: Springer Berlin Heidelberg), 11–21. doi: 10.1007/978-3-662-57320-4_2

Schöning, S., Mendel, V., and Köse, A. (2020). Mit neuen Controller-Kompetenzen in die Zukunft. Control Manag. Rev. 64, 58–63. doi: 10.1007/s12176-019-0073-y

Schubert, R., and Gerhardt, N. (2021). Praxisanforderungen mittelständischer Unternehmen an Controlling-Nachwuchskräfte. Controller Magazin 2, 31–35.

Schulz, T. (2014). “CFO-Agenda: Gute gründe, nachhaltigkeit auf die tagesordnung zu setzen,” in CSR und Finance, eds T. Schulz and S. Bergius (Berlin: Springer Berlin Heidelberg), 3–34. doi: 10.1007/978-3-642-54882-6_1

Schulze, M., and Thomas, S. (2012). Strategisches nachhaltigkeits-controlling bei der deutschen telekom AG corporate responsibility key performance-indikatoren. Controller Magazin 58–63.

Schwarzmaier, U. (2013). Entwicklungstendenzen des controllings unter besonderer Berücksichtigung der Veränderungen durch die Nachhaltigkeitsdiskussion. Controller Magazin 4, 29–36.

Schwarzmaier, U. (2015). Die Rolle des Controllings im Sustainable Management. Der Betriebswirt. Berlin: Duncker & Humblot GmbH, 22–27. doi: 10.3790/dbw.56.2.22

Seifried, J. (2004). Fachdidaktische Variationen in einer Selbstorganisationsoffenen Lernumgebung. [Dissertation]. Wiesbaden: Dt. Univ.-Verl. doi: 10.1007/978-3-322-81139-4

Sneidere, R., and Bumane, I. (2019). “The challenges for the profession of accountant in the changing global economic environment,” in New challenges of economic and business development 2019, ed. Faculty of Business, Management and Economics (University of Latvia), 761–771.

Stehle, A., and Stelkens, V. (2018). Green Controlling - eine Aufgabe für Controller und Nachhaltigkeitsexperten! Controller Magazin 5, 4–10.

Stütz, S. (2024). Charakteristika von Aufgaben in der Domäne Rechnungswesen. Wiesbaden: Springer Fachmedien Wiesbaden. doi: 10.1007/978-3-658-44498-3

Sulaiman, M., and Mokhtar, N. (2012). Ensuring sustainability: A preliminary study of environmental management accounting in Malaysia. Int. J. Bus. Manag. Sci. 5, 85–102.

Tsiligiris, V., and Bowyer, D. (2021). Exploring the impact of 4IR on skills and personal qualities for future accountants: A proposed conceptual framework for university accounting education. Accounting Educ. 30, 621–649. doi: 10.1080/09639284.2021.1938616

Walinska, E., and Dobroszek, J. (2021). The functional controller for sustainable and value chain management: Fashion or need? A sample of job advertisements in the COVID-19 period. Sustainability 13:7139. doi: 10.3390/su13137139

Weber, J., Georg, J., and Janke, R. (2010). Nachhaltigkeit: Relevant für das controlling? Controlling Manag. 54, 395–400. doi: 10.1007/s12176-010-0101-4

Weigand, H. (2020). “Green Marketing - nachhaltig erfolgreich,” in Die 10 wichtigsten Zukunftsthemen im Marketing: Buzzwords die Bleiben, ed. M. Stumpf (Breisgau: Haufe-Lexware GmbH & Co. KG), 47–69.

Wellbrock, W., Ludin, D., and Krauter, S. (2020). Nachhaltigkeitscontrolling: Instrumente und Kennzahlen für die strategische und operative Unternehmensführung. Wiesbaden: Springer Fachmedien Wiesbaden. doi: 10.1007/978-3-658-30700-4

Winther, E., and Achtenhagen, F. (2008). Kompetenzstrukturmodell für die kaufmännische Bildung. zbw 104, 511–538. doi: 10.25162/zbw-2008-0028

Wöhe, G., Döring, U., and Brösel, G. (2020). Einführung in die allgemeine Betriebswirtschaftslehre. München: Verlag Franz Vahlen.

Keywords: sustainability, accounting, controlling, content knowledge, review

Citation: Pargmann J and Berding F (2025) Sustainability content knowledge for teachers in accounting and controlling: a systematic literature review on industry approaches, practices and desired competences. Front. Educ. 10:1519350. doi: 10.3389/feduc.2025.1519350

Received: 29 October 2024; Accepted: 01 May 2025;

Published: 27 May 2025.

Edited by:

Anna-Franziska Kähler, Leuphana University Lüneburg, GermanyReviewed by:

Alfiya R. Masalimova, Kazan Federal University, RussiaMustika Handayani, Indonesia University of Education, Indonesia

Copyright © 2025 Pargmann and Berding. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Julia Pargmann, anVsaWEucGFyZ21hbm5AdW5pLWhhbWJ1cmcuZGU=