Aldo Bazán-Ramírez1*

Aldo Bazán-Ramírez1* Eduardo Hernández-Padilla2

Eduardo Hernández-Padilla2 Ybar Gustavo Palomino-Malpartida3

Ybar Gustavo Palomino-Malpartida3 Wilfredo Bazán-Ramírez4Edwin Félix-Benites1

Wilfredo Bazán-Ramírez4Edwin Félix-Benites1- 1Department of Education and Humanities, Universidad Nacional José María Arguedas, Andahuaylas, Peru

- 2Center for Transdisciplinary Research in Psychology, Universidad Autónoma del Estado de Morelos, Cuernavaca, Mexico

- 3Faculty of Chemical Engineering and Metallurgy, Universidad Nacional de San Cristóbal de Huamanga, Ayacucho, Peru

- 4Faculty of Administrative Sciences, Universidad Nacional Mayor de San Marcos, Lima, Peru

Introduction: The financial literacy and competencies of future citizens are of global interest to educational researchers and behavioral scientists. We investigated the influence of academic achievement, financial literacy and sociodemographic factors on the Peruvian students’ financial competence performance in the Programme for International Student Assessment (PISA) 2022.

Methods: Data from 4,092 students were analyzed using multilevel hierarchical models. Five groups of predictor variables were evaluated: sociodemographics, financial familiarity and experience, financial literacy, support and involvement, and math and reading achievement.

Results: Eight variables had independent significant effects on financial competencies: gender, technological resources and household possessions, attitudes to financial matters, familiarity with financial concepts, school financial education, family support and influence of friends. However, when testing a full multivariate model incorporating all predictor groups, math and reading achievement emerged as the strongest predictors of financial competence, followed by familiarity with financial concepts.

Discussion: The results suggest that the development of financial competencies in Peruvian students is more closely linked to general academic performance in mathematics and reading than to specific financial literacy variables. These findings have significant implications for educational policies and curriculum development, because starting in 2024, economic and financial contents were included in the Peruvian national curriculum.

1 Introduction

Financial competence encompasses knowledge and understanding of financial concepts and risks as well as skills, attitudes, motivation, and self-confidence to make effective decisions in a variety of financial contexts. This knowledge improves the financial well-being of individuals and society and generates active participation in economic life (Chu Cam et al., 2020; Organization for Economic Co-operation and Development (OECD), 2019a). According to the Organization for Economic Cooperation and Development (OECD), to achieve better financial management among citizens, in recent years, “developed and emerging economies have become increasingly aware of the importance of ensuring that their citizens are financially literate” (Organization for Economic Co-operation and Development (OECD), 2019b, p. 120).

Financial literacy has gained importance not only since the global economic crisis of 2008 but also in response to recent events, such as the COVID-19 pandemic, the conflict between Russia and Ukraine, and tensions in the Middle East. These situations have intensified economic instability and accentuate the need for people to be better prepared to manage financial risks. In this area, financial education is key to developing the necessary skills to make informed decisions in an increasingly uncertain and volatile global environment. According to the OECD, financial literacy has become so important that the G20 has actively supported the initiatives of the OECD and the International Network for Financial Education (INFE), promoting financial education at the local and national levels. This is in recognition that a financially literate citizenry is essential for economic stability and resilience in times of crisis.

In a context of substantially virtualized financial services and exchanges, in which people are living longer, there is a belief that greater financial literacy and knowledge among the population will allow people to make better financial decisions and have better morale and greater confidence (Cordero et al., 2022; Rostamkalaei et al., 2024). However, the risks of indebtedness have also increased, as has the poor use of the advantages of virtualized finance. Poor understanding of market volatility, poor handling of technologies, and minimal knowledge and training in finance, especially among the younger population and among the population with a lower socioeconomic level (Bazán-Ramírez et al., 2024; Houle, 2014; Moreno-Herrero et al., 2018a). This situation promoted the interest of various specialists in studying the relationship between literacy and financial education on financial competence (Aprea et al., 2016; Cordero et al., 2022; Moreno-Herrero et al., 2018b). This aligns with findings by Mancone et al. (2024), who emphasized the behavioral impact of structured financial literacy programs among youth, highlighting the critical need for well-designed educational interventions that can effectively bridge the gap between financial knowledge and practical application.

According to the PISA 2022 Assessment and Analysis Framework (Organization for Economic Co-operation and Development (OECD), 2023), financial literacy plays a crucial role in preparing young people to face global economic challenges, enabling them to develop skills to make responsible and informed decisions and adapt to market volatilities. Similarly, Ferrada et al. (2022) highlighted the importance of financial education and its promotion from the initial stage of schooling to achieve the economic inclusion of new citizens in the various spheres of society. Chu Cam et al. (2020) pointed out that Vietnam is one of the countries that does not have a national financial education strategy for citizens; similarly. Tzora et al. (2023) have reported the absence of a curriculum dedicated to personal finance in public schools in Greece. In the case of Peru, as of the 2024 school year, economic and financial education content was included in the National Curriculum for Regular Basic Education (MINEDU, 2024).

Financial literacy for the development of financial skills and knowledge has attracted the interest of educational and economic education specialists and researchers. Amagir et al. (2018) conducted a systematic literature review study on financial literacy education programs for children and adolescents. This review evidences that school-based financial literacy education programs contribute to the improvement of financial knowledge and attitudes of children and adolescents. Studies assessing the intention to practice good financial behavior and studies based on self-reported behavior also had positive effects on financial knowledge, but studies assessing the effects of financial education on the actual financial behavior of children and adolescents are scarce. Similarly, Savard and Cavalcante (2021) gathered in a book the contributions of various educational researchers on the role of mathematics in teaching financial education, emphasizing the concept of financial arithmetic as teaching practices, resources, and the needs of secondary mathematics teachers to incorporate financial concepts in their classes.

Another systematic review analysis by Méndez Prado et al. (2022), on financial education in Latin American and Caribbean countries, from 65 publications selected, from 2016 to 2022. The results reflect that in the region, there is a considerable increase in articles based on financial education because there is greater accessibility to information, especially from young people who have access to Information and Communications Technologies (ICTs). The analysis reveals the evolution of studies on financial education in the Latin American and Caribbean region, with Brazil being the country with the highest number of articles published on the subject. The selected articles emphasize the importance of implementing educational programs that guarantee the economic management of individuals in accordance with their country’s needs.

Based on a bibliometric study of 274 articles published between 1994 and 2022 in the Scopus database, Sagita et al. (2022) found the predominance of the following concepts: applying financial knowledge and understanding financial information and mathematical concepts. The study highlights the need for teachers to know financial literacy terms; it also found evidence of the link between mathematics and financial literacy skills, the application of financial literacy to learning outcomes in mathematics, and the willingness of schools to apply financial literacy through pedagogical projects.

2 Literature review

The development of financial competence can be influenced by psychological factors, attitudes, competencies and personality (interactive styles), family factors, literacy experiences, and previous financial practice. Thus, people’s financial decision-making or avoidance will also be influenced by psychological variables, such as decision or risk attitudes (Beattie et al., 1994). Also, the gender and culture of origin of the students have been included as important predictors of financial literacy (Hornyák, 2018; Preston et al., 2024). Several research studies have been reported on financial competencies and their associated variables.

Hornyák (2018) assessed the financial knowledge of Hungarian high school students using PISA questionnaires and found that differences in financial knowledge and behavior, as well as attitudes toward financial processes, were due to gender, age group and family background. Chu Cam et al. (2020) have proposed strategies to work on financial literacy by designing appropriate educational content in mathematics teaching. Specifically, to develop numeracy, educators can use the context of financial literacy that has a close relationship with students, such as saving, shopping, simple statistics of daily expenses, among other actions, which allows creating a corpus of appropriate situations.

Kolachev et al. (2021) studied financial literacy factors in Russian schoolchildren and found strong positive associations between family and school socioeconomic levels with financial literacy. Liu et al. (2021) reported the effect of behavioral patterns (self-control, optimism, herding, and loss aversion) on financial inclusion in a sample of Pakistani families, mediated by financial literacy, which was shown to have a significant moderating effect on the relationship between behavioral (psychological) factors and financial inclusion. The relationship between financial literacy and psychological aspects, such as entrepreneurial behavior and saving behavior, has also been raised (Alshebami and Al Marri, 2022).

Even societies with a higher socioeconomic level have considered the importance of influencing the financial literacy of their young people. For example, Silinskas et al. (2021) pointed out that Finnish adolescents should acquire basic knowledge of financial education as early as secondary school so that, in adulthood, they can make appropriate decisions about complex and highly volatile situations. Thus, being financially competent will depend on variables, such as having gone through financial literacy processes (school or out-of-school financial education); developing attitudes and interactive styles based on experiences in the family, school, and community; the socioeconomic and cultural educational level of the families of origin and the schools attended, as well as access, knowledge, and management of technological resources.

Amirullah et al. (2022) have pointed out that financial education and mathematics education are closely linked; therefore, a significant number of educational institutions and universities have included, within their curricula, subjects on financial planning because being educated and knowing about finances from basic education helps to make better decisions in their lives. On the other hand, Cavalcante and Huang (2022), based on the analysis of curricular policies, school textbooks, and a survey of 60 in-service teachers, found little curricular content on financial education and financial literacy, and that, in the collection of school textbooks, few exercises related to financial tasks are also included. Cavalcante and Savard (2022) have further elaborated that particularly in times of crisis, mathematics education must address the immediate needs of society and contribute to overcoming societal challenges because the rise of complex technologies, the climate crisis, and the financing of essential commodity items pose challenges that require mathematics education to be responsive and adaptive. The authors reiterate the importance of financial arithmetic in teaching mathematics in a way that helps individuals and communities produce and manage resources in three dimensions: contextual, conceptual, and systemic.

According to Khusaini et al.’s (2022) study in Indonesia, socioeconomic status significantly predicted financial literacy performance, but financial education and gender were not significant predictors. The authors highlighted that the high socioeconomic status of the student body fosters higher financial skills and competencies, family literacy experience, better financial planning, and family decision-making. On the other hand, Mihalcova et al. (2020), with a sample of students from fifteen countries that participated in the PISA 2015 assessment, conducted a comparative analysis using cluster analysis, placing Peru together with Brazil in the fourth and last group in hierarchical order. The results revealed that all participants achieved similar results in financial literacy and that the education provided lacked a sense of market performance, which has generated permanent rejection by employers.

Kusumawati et al. (2023) conducted an experimental study with a social arithmetic learning instructional design through the mathematics-based Islamic financial literacy framework for Islamic schools. They succeeded in developing learning mechanisms to foster and strengthen numeracy and Islamic financial literacy skills with multiple exercises on Islamic financial aspects as mathematics extension work. To develop this task, the researchers considered three experts and six students from an Islamic high school as a study sample. The former is to analyze and plan the extension school works within social and financial arithmetic, while the students can develop with relevance these proposed tasks. As a result, they show that mathematics helps considerably to improve the ability of Islamic students to develop financial literacy.

Tzora et al. (2023) administered an online questionnaire on financial literacy, financial behavior, and attitudes to 3,028 15-year-old students from 96 schools in Greece. Among the most important results are that 31.7% of the students scored above the 70% threshold, and girls have 14.5% less financial capability. Students’ performance in school is positively related to financial capability, and the crisis has induced financial constraints in their households. The contribution of the Tzora et al.’s (2023) study was to highlight family and cultural capital aspects as variables associated with financial literacy and education, for example, parents’ years of education were positively related to financial capability; crisis-induced financial constraints are positively related to financial capability; a higher amount of pocket money exerts a negative impact on financial knowledge and behavior scores.

Silinskas et al. (2023) investigated the effect of school environment and family environment on financial confidence in developing financial literacy skills of adolescents in Finland, who participated in the PISA 2018 test. The results evidence that financial education at school positively predicted adolescents’ confidence in using financial and digital services. Similarly, financial education in schools and families indirectly predicted students’ financial literacy, mediated by students’ confidence in using digital financial services. They also found that older adolescents were more exposed to financial education at school and in families, while adolescents from wealthier families and female students, relative to their male counterparts, were exposed to more frequent discussion of financial matters with their parents at home. It was further found that higher parental education in the family was related to higher financial literacy but not to higher financial confidence, while family wealth was related to higher financial confidence, but not to financial literacy.

Oberrauch et al. (2025) analyzed the effect of various predictor variables of financial literacy in 2012, 2015, 2018, and 2022 assessments of countries participating in the PISA financial literacy assessments. Their results show that in all four PISA assessments, immigrant origin, parents’ highest occupational status, and student gender significantly influenced financial literacy scores. Additionally, math and reading performance are strong predictors of financial literacy.

In the Latin American context, Carvalho and Carlo (2021) developed research with results of Brazilian students in PISA 2015, with the purpose of comparatively analyzing the performance of Brazilian schoolchildren in relation to the level of financial education. It was found that 61.98% of Brazilian students claim not to have learned how to manage their money at school. Of these, 75% of them, grouped according to the level of financial competence, were classified in the two worst positions, 53% of them being classified in the group with the lowest performance. Furthermore, when considering the percentage of schoolchildren at each level, it was found that Brazilian students had the worst performance in terms of financial literacy compared to students from the 15 countries that evaluated financial competence in PISA 2015. On the other hand, Reisdorfer Da Silva et al. (2024), using the database of Brazilian students in PISA 2018, found that males and those with a higher socioeconomic level obtained better results in financial literacy. Similarly, they reported significant effects on achievement in financial competence of variables such as having taken specific classes at school on the subject, having access to books at home, liking to compete, earning money in some way, and making autonomous decisions about how to spend it.

In contrast, Bazán-Ramírez et al. (2024) taking the database of Peruvian students who took the 2018 PISA test, found that achievement in financial competencies in PISA 2018 was best predicted by achievement in mathematics, followed by achievement in reading and third by financial education received, once the effect of the school mean of the socioeconomic and cultural status index was controlled for. Also, the authors reported that confidence about financial subjects and topics had a partial effect, but that family involvement in financial literacy had no effect on achievement in financial competence.

Considering the data available from the PISA 2022 application of Peruvian students, the present study sought to answer the research question: How do variables of academic achievement in math and reading, financial literacy and experience, and sociodemographic variables influence achievement in financial competence among Peruvian adolescents in the PISA 2022 application? The objective of this study was to determine the differential effect, through multilevel models, of sociodemographic variables, financial familiarity and experience, financial literacy, support and involvement, and achievement in math and reading, on the achievement of financial competencies in Peruvian students in PISA 2022.

3 Method

3.1 Design and participants

A retrospective cross-sectional design with secondary data analysis was used with results from 4,092 Peruvian students, from 336 schools, who participated in the PISA test of financial competencies in the year 2022. The sample was selected through a two-level stratified procedure and is nationally representative. The databases are freely accessible and were obtained from the PISA 2022 Database | OECD (Organization for Economic Co-operation and Development (OECD), 2024). This is the sixth time that Peru, which is not part of the OECD countries, has participated in PISA, and the third time that it has also obtained results in financial competence. Notably, 50.3% of Peruvian students who participated in this application were female.

3.2 Variables

The dependent variable (variable to be predicted) was overall achievement in financial competence. The 10 plausible values were used at which PISA reports the overall scores in an assessed competency (PV1FLIT to PV10FLIT). Similarly, the sample weights of the participants were used to obtain results that can be generalized to the Peruvian national level.

3.3 Procedure

3.3.1 Multilevel hierarchical modeling

In order to analyze the effects of the independent variables considered in this study, which are presented later, seven hierarchical multilevel analysis models (HLM), for which the statistical package HLM® (Raudenbush et al., 2019) was used, were carried out in seven different models where the dependent variable was performance in financial achievement. It is important to note that, during the analyses, the 10 plausible values of financial competence were considered as previously mentioned, and the use of the sample weights of the individuals seems to improve the performance of the HLM analysis. By using the aforementioned information, it allows estimating the correct relationships within the level of the students’ variables, eliminating the biases of the segregation of the stated variables, in addition to allowing greater heterogeneity in hypotheses, and being able to compare the random or fixed effects of the variables; as well as obtaining the estimation of the standard errors derived from the group effects, including the variance components (Tat et al., 2019).

The predictor variables, used in the different multilevel models, were grouped into five factors and were structured as follows:

3.3.1.1 Factor 1. Sociodemographic factors

3.3.1.1.1 School type

Type of school support: public or private.

3.3.1.1.2 Student (standardized) gender (gender)

This is a standardized nominal variable that identifies the gender to which the respondent belongs; for the present study, the reference value used was male (with a code of 0), while for female students, a code with a value of 1 was used.

3.3.1.1.3 ICT resources (weighted likelihood estimates (WLE))—(ICTRES)

This index is based on the availability of 11 ICT resources in your home (e.g., screens, desktop computer, laptop or notebook, Internet access, tablets, e-book readers, cell phones with Internet access, among others).

3.3.1.1.4 Home possessions (WLE)—(HOMEPOS)

It is the number of home possessions, including considering household books and items specific to the respondent’s country of origin. Unlike the PISA 2018 application (Organization for Economic Co-operation and Development (OECD), 2023), which considered 16 items, this time 31 items were considered, among which four country/economy-specific items were included, as well as how many e-books and digital devices with screens were possessed at home.

3.3.1.1.5 Index of economic, social, and cultural status

The index of economic, social, and cultural status (ESCS) is a composite variable composed of the scores of three simple and composite variables: the highest parental educational level of both parents (PAREDINT), the highest occupational status of either parent (HISEI) and the number of household possessions from a list of items asked (HOMEPOS). The school average of the index of economic, social, and cultural status (MESCS) was also included based on the index of economic, social, and cultural status (ESCS).

3.3.1.2 Factor 2. Financial familiarity (experience)

3.3.1.2.1 Access to money and financial products, sources of money (WLE)—(ACCESSFP)

It is an index composed of seven items that indicate the frequency with which students indicate the sources and periodicity from which their money comes. The response options are presented on a Likert scale.

3.3.1.2.2 Access to money and financial products, financial activities (WLE)—(ACCESSFA)

It is an index made up of 11 items in which students report the frequency with which they completed different financial activities. The response options are based on a Likert scale.

3.3.1.2.3 Attitudes toward and confidence about financial matters (WLE)—(ATTCONFM)

There are seven items that indicate the degree of agreement of the students about their attitudes and confidence about financial matters. The response options are a Likert scale.

3.3.1.3 Factor 3. Financial literacy

3.3.1.3.1 Familiarity with concepts of finance (FCFMLRTY)

It is an index of the sum of 16 items on the students’ self-reported familiarity with a set of financial topics and/or concepts of finance. The response options were 1 if the student reported having some knowledge and 0 if not.

3.3.1.3.2 Financial education in school lessons (WLE)—(FLSCHOOL)

It is an index composed of six indicators referring to grades (in PISA 2018, there were only five), which students attribute to the frequency with which, in school lessons, they had financial tasks and activities. Financial education in school lessons, multiple subjects (WLE)—(FLMULTSB). These are students’ responses to questions about the educational lessons (mathematics, economics or business, etc.) in which they addressed financial topics. The index is composed of seven items with Yes or No response options.

3.3.1.3.3 Confidence about financial matters (WLE)—(FLCONFIN)

It is an index constructed based on the students’ scores regarding their confidence in different financial matters. The scale consists of six items with Likert-scale response options.

3.3.1.3.4 Confidence about financial matters using digital devices (WLE)—(FLCONICT)

Based on students’ responses to five items, with Likert-scale response options, regarding the performance of various financial tasks using electronic devices.

3.3.1.4 Factor 4. Support and involvement

3.3.1.4.1 Family support (WLE)—(FAMSUP)

This index is composed of ratings of students’ perceptions of the frequency and consistency with which parents and other family members engaged in supportive behaviors directed toward the student’s school activities. The index is comprised of 10 indicators on this topic.

3.3.1.4.2 Parental involvement in matters of FL (WLE)—(FLFAMILY)

These are students’ responses to questions about the frequency with which they discuss various financial issues with their parents. It is an index composed of seven items.

3.3.1.4.3 Friends’ influence on financial matters (WLE)—(FRINFLFM)

It is an index formed from students’ responses on their degree of agreement with various statements about their friends’ influence on financial decisions.

3.3.1.5 Factor 5. Academic achievement in PISA 2022

3.3.1.5.1 Mathematics achievement (mathematical literacy)—(MATH)

The average of the 10 estimated plausible values for each student in overall mathematics proficiency.

3.3.1.5.2 Reading literacy achievement (READ)

The average of the 10 plausible estimates for each student on the overall reading literacy proficiency.

It should be noted that the WLE indicates that the index scores have been standardized in their construction and are known as WLE. These indices were constructed to have a mean of 0 and a standard deviation of 1 for all countries that participated in the implementation of PISA 2022 (Organization for Economic Co-operation and Development (OECD), 2024).

3.4 Data analysis

Standardized value indices were taken for the variables involved, and the WLE ESCS index for most of the predictor variables of financial competence. Descriptive data analysis was performed with these values, and a matrix of bivariate correlations between the variables involved was used (Pearson’s correlation was used). On the other hand, to analyze the differential effect of the variables included as predictors of financial achievement, seven multilevel hierarchical models were tested as follows:

Model 1 included three sociodemographic predictors of financial competence: V1, student (standardized) gender; V2, ICT resources (WLE); V3, home possessions (WLE); and V4. Index of economic, social, and cultural status (ESCS).

Model 2, financial familiarity (experience), considered three predictor variables of financial achievement: V5, access to money and financial products, sources of money (WLE); V6, access to money and financial products, financial activities (WLE); V7, attitudes toward and confidence about financial matters (WLE).

Model 3, Fifnancial literacy, incorporated five predictor variables: V8, familiarity with concepts of finance; V9, financial education in school lessons (WLE); V10, financial education in school lessons, multiple subjects (WLE); V11, confidence about financial matters (WLE); V12, confidence about financial matters using digital devices (WLE).

Model 4, support and involvement, included three variables: V13, family support (WLE); V14, parental involvement in matters of FL (WLE); and V15, friends’ influence on financial matters (WLE).

Model 5, academic achievement in PISA 2022, included two competencies: V16, mathematical literacy, and V17, reading literacy.

Model 6, the general model without competencies, included all the predictor variables of financial achievement at the same time, except for the two competency variables.

Model 7 included all the predictor variables of financial achievement simultaneously.

4 Results

This article analyzed the relationships between 17 predictor variables of student level and two school variables, in seven multilevel models, and achievement in financial competence. Table 1 shows the descriptive values of the predictor variables and financial competence. First, the percentage values of the number of participants by sex are shown. Similarly, it is observed that there are no significant differences between the percentage of female students (50.3%) and 49.7% of male students (which was the reference value for this variable).

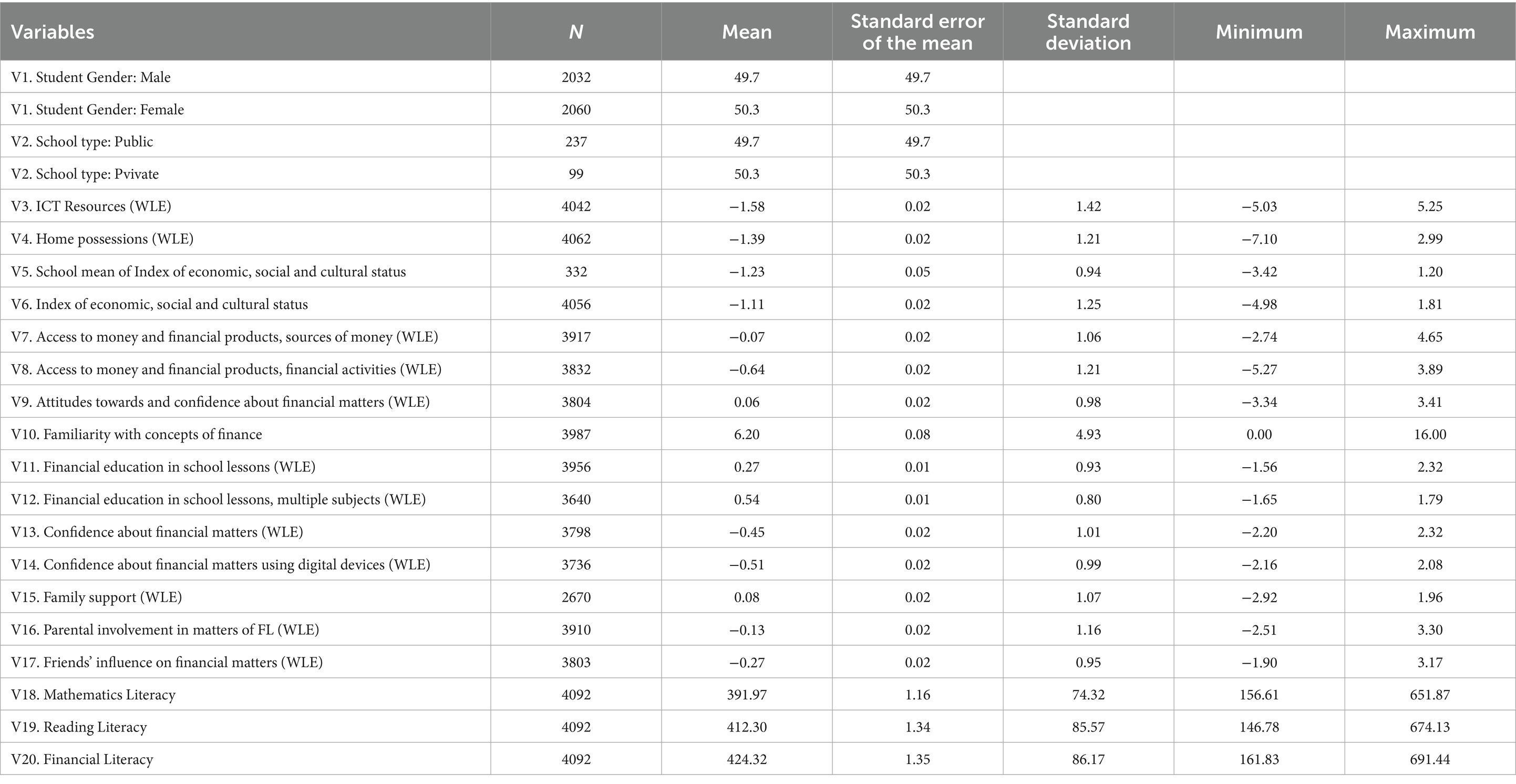

Table 1. Descriptive statistics of the variables included in the study.

The other part of the table indicates the number of participants, the average obtained for each of the composite variables, the standard error of the mean, its standard deviation, and the minimum and maximum values reached by each variable. It should be remembered that the sample is made up of 4,092 participants, and the number of responses for each variable is less than this value, with the exception of the results in mathematics, reading, and financial literacy, where the number of respondents is equal to the total sample. The lowest value of respondents (2670) is in the family support variable. In the rest of the variables, the number of responses ranged between 3,640 and 4,062. The mean value of each variable established by the OECD is 0 and the standard deviation is 1; however, in the present study the means obtained in the different variables differ from the established mean: eight variables have values below the mean (ICT resources, home possessions, index of economic, social, and cultural status, access to money and financial products, sources of money, confidence about financial matters, parental involvement in matters of FL, Friends’ influence on financial matters). In addition to a constructed variable (school mean of index of economic, social, and cultural status), also with a mean below 0.

Also, five variables were included whose means were above 0 (attitudes toward and confidence about financial matters, familiarity with concepts of finance, financial education in school lessons, financial education in school lessons, multiple subjects, and family support). In these variables, the standard error of the mean ranges between 0.01 and 0.08. Regarding the predictor variables, mathematics literacy and reading literacy have values below the established mean (391.97 and 412.30, respectively). Similarly, the variable to be predicted, financial literacy, also has a value below the mean (424.32). For these three variables, the standard error of the mean ranges between 1.16 and 1.35.

The dispersion measures of the predictor variables show a marked heterogeneity both in the standard deviation and in the minimum and maximum values. For the composite variables, the standard deviation ranged from 0.80 to 4.93; whereas, for the proficiency variables, there is greater homogeneity with standard deviation ranging from 74.32 (mathematics literacy) to 86.17 (financial literacy). Finally, the minimum and maximum values for the predictor variables establish differences between them that range from scores with a difference of two to 16 points; while, in the competency variables, the differences in scores reach approximately 531 points between the minimum and maximum values (financial literacy).

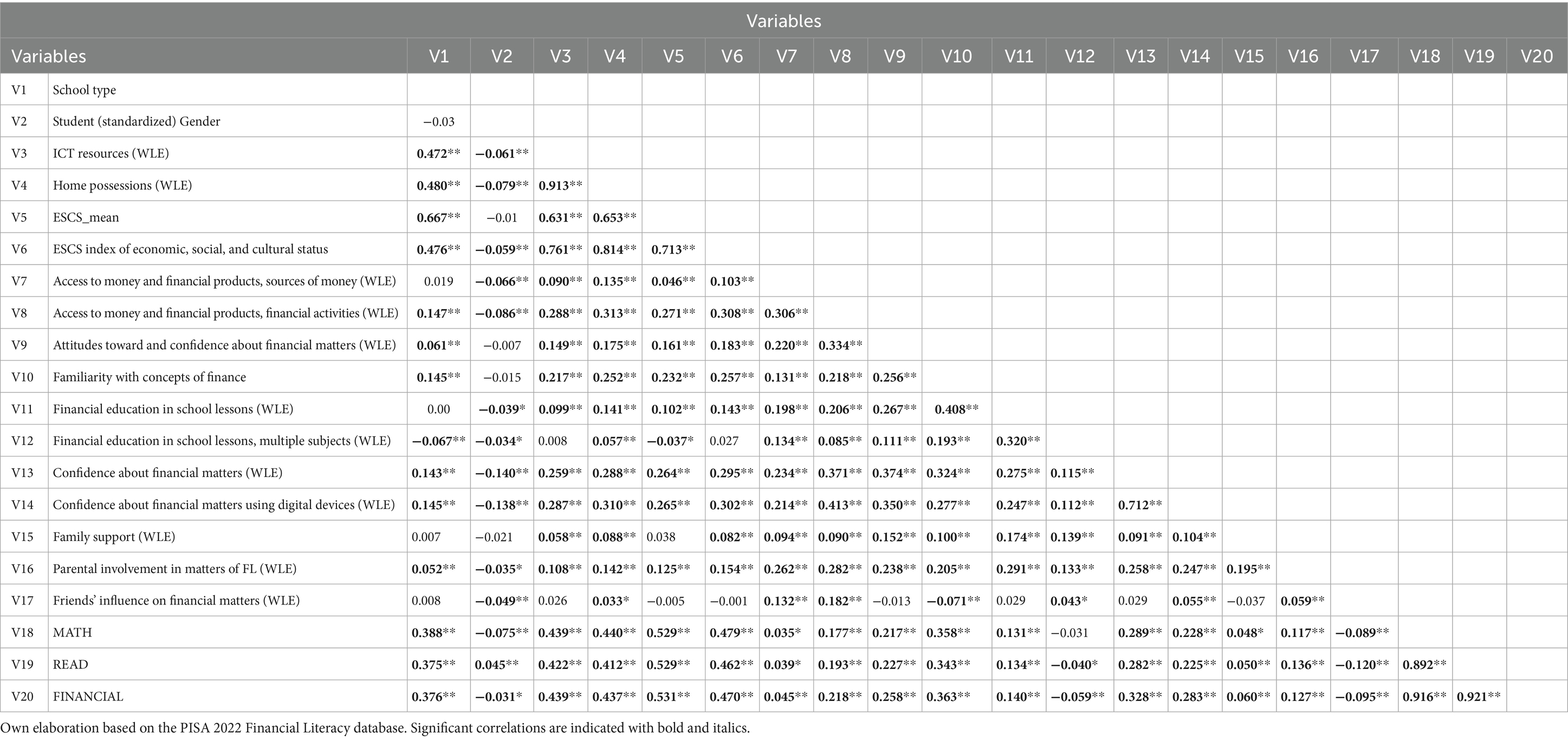

Table 2 shows the correlations between the variables considered in this study. The table shows the Pearson bivariate correlation coefficients. It can also be seen that most of the variables have significant and positive correlations, with the exception of gender, which correlates negatively with almost all the variables (except for reading literacy). There is a wide heterogeneity among the correlation coefficients, ranging from 0.04 (although minimal, it is statistically significant due to the number of cases) to values as high as 0.92 (correlation coefficients among the competencies). On this last point, it should be noted that, except for the high coefficients between competencies, the variables’ index of economic, social, and cultural status (ESCS) and home possessions are the ones with the highest number of significant and positive correlations with the rest of the variables used in this study. The value of their correlations is between 0.81 and 0.03 for the index of economic, social, and cultural status (ESCS); on the other hand, for the variable home possessions, the correlation values are in the range of 0.96 and 0.06.

Table 2. Correlation matrix between study variables.

Of the variables considered to evaluate financial experience, access to money and financial products, sources of money; access to money and financial products, financial activities; and attitudes toward and confidence about financial matters, have positive and significant correlations with the sociodemographic variables ranging from 0.09 to 0.31, although they have a negative association with the variable gender, with the exception of the third variable which does not have a significant relationship. Among the same variables, the correlations are positive and significant, although of low magnitude (0.22 to 0.33). With respect to the remaining variables, the associations, although positive and significant, are very low to medium (0.03 to 0.37). The variables on financial literacy, familiarity with concepts of finance, financial education in school lessons, financial education in school lessons, multiple subjects, confidence about financial matters, and, confidence about financial matters using digital devices, in their great majority have positive and significant relationships with the rest of the variables (associations ranging from 0.04 to 0.41); but they also have statistically significant negative correlations, which are very low with others such as financial education in school lessons and multiple subjects that are negatively associated with achievement in reading and financial literacy, −0.04 and −0.06, respectively.

Similar results were also found for the support and involvement variables: family support, parental involvement in matters of FL, and Friends’ influence on financial matters. The vast majority of the positive associations were low (0.03–0.29), although negative relationships were also obtained (−0.07 to −0.04). Finally, achievement in mathematics, reading, and financial literacy shows a wide heterogeneity in the correlations with the previously mentioned variables. Medium correlations, approximately 0.47, were obtained with sociodemographic variables, while with the rest of the variables referring to financial literacy, the associations were of varying magnitude and direction.

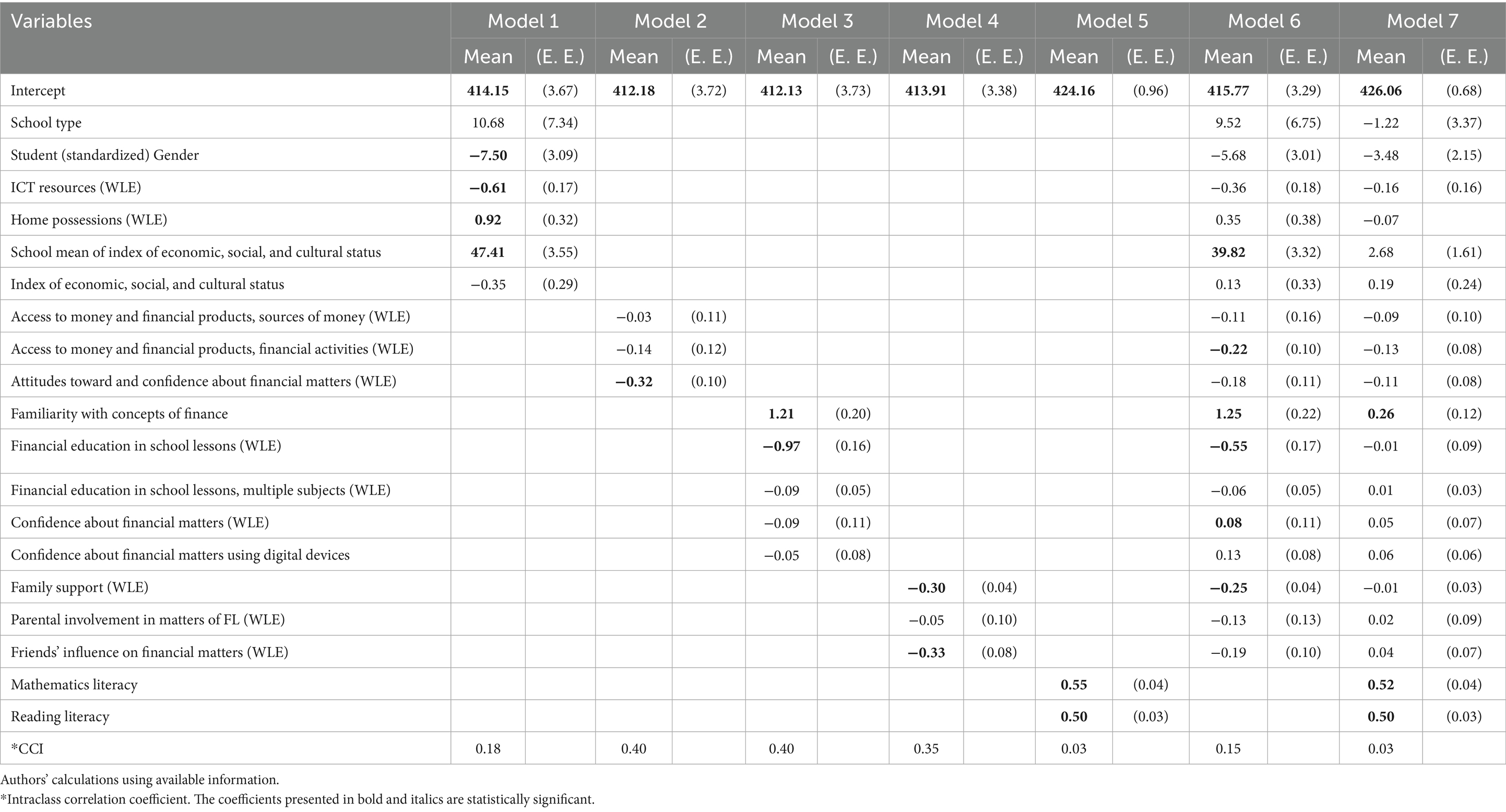

The results of the multilevel analysis of the influence of the different sociodemographic, financial and achievement variables on financial literacy are shown in Table 3. This table shows the seven models suggested to be analyzed in the study proposal; the elements presented are the means obtained for the 10 plausible values of financial literacy, together with their standardized errors resulting from their estimation (S. E.). Similarly, the coefficients of each variable (the contribution to the achievement obtained in financial competence) are shown, together with their standardized errors; and, finally, the intraclass correlation coefficient (ICC), which explains the variability of the respondents that remains to be explained.

Table 3. Hierarchical multilevel regression models.

In general terms, in each of the different models, it can be seen that the effects of the sociodemographic and some financial variables have a positive or negative influence on financial competence, but such influences are small, as will be seen below. The sociodemographic variable with the greatest influence in Model 1 was gender (−8.09 points); while the rest of the variables, such as financial experience, financial literacy, and support and involvement of family and friends, have marginal positive or negative contributions under one point, which means that they have little contribution to achievement in financial competence.

More specifically, in Model 1, the sociodemographic variables that influenced financial competence were, in addition to the aforementioned gender, ICT resources and home possessions (−0.62 and 0.87, respectively); the CCI obtained in this model is 0.41. In Model 2, financial experience, only attitudes toward and confidence about financial matters had a significant impact on the dependent variable (−0.32); in this model, the CCI had a marginal decrease, 0.40. The variables familiarity with concepts of finance (1.21) and financial education in school lessons (−0.97) are those that influenced achievement in Model 3; in this same model, the CCI obtained was equal to that of the previous model (0.40). For Model 4, support and involvement, only the variables family support and Friends’ influence on financial matters exerted changes in the dependent variable (−0.30 and −0.33, in that order); the CCI of this model was reduced to 0.35. The academic achievement in PISA 2022, Model 5, both mathematical and reading literacy worked favorably on achievement (0.55 and 0.50, respectively); in this model, the CCI showed a dramatic reduction (0.03). In the general model without competencies, the variables that influenced financial competence were access to money and financial products, financial activities (−0.24); familiarity with concepts of finance (1.28); financial education in school lessons (−0.58); and, family support (−0.29); the CCI value obtained was 0.35. Finally, in Model 7, which included all the variables, only familiarity with concepts of finance (0.26), mathematical literacy (0.53) and reading literacy (0.51) showed significant effects on financial competence. In this model, the CCI obtained was 0.03.

5 Discussion

The results obtained in this study, using seven-level models, showed the differential effect of five groups of variables on the achievement in financial competencies of Peruvian students in PISA 2022: Sociodemographics, financial familiarity and experience, financial literacy, support and involvement, and achievement in math and reading. In the first four independent multilevel regression models tested, out of 19 manifest variables, significant effects on financial competencies were found for only nine of them. Of the sociodemographic variables, gender and ICT resources, both negatively, and home possessions, positively. Regarding financial familiarity and experience, only attitudes toward and confidence in financial matters are negative. From financial literacy, only familiarity with concepts of finance, positively, and financial education in school lessons, negatively, were significant predictors of financial achievement. Similarly, from the Support and involvement group, two variables with low but significant coefficients negatively predicted achievement in financial competence: family support and friends’ influence on financial matters.

Regarding the effect of sociodemographic variables, the results of this study confirm previously reported findings. For example, the effect of gender on financial knowledge in more restricted predictive models (Bazán-Ramírez et al., 2024; Hornyák, 2018; Preston et al., 2024). Similarly, the effect of some indicators of family socioeconomic status, such as household possessions and technological resources, has also been reported as a significant predictor of financial skills and competencies (Khusaini et al., 2022; Kolachev et al., 2021). Regarding the little effect of financial familiarity and experience on financial competence, other studies have also reported moderate or indirect prediction. For example, attitudes toward financial processes have been associated with financial competencies (Hornyák, 2018), and family experience of financial literacy (Khusaini et al., 2022; Silinskas et al., 2023).

Regarding financial literacy, the results of the direct effect of both familiarity with concepts of finance and financial education in school lessons, coincide with what has been pointed out in other studies (Carvalho and Carlo, 2021; Chu Cam et al., 2020; Liu et al., 2021), and the importance of promoting and developing financial literacy practices in the classroom in the school context is highlighted (Cavalcante and Huang, 2022; Cavalcante and Savard, 2022). These findings align with Mancone et al. (2024), who emphasized the behavioral impact of structured financial literacy programs among youth, demonstrating that well-designed educational interventions can effectively translate financial knowledge into practical competencies. On the other hand, parental support as a predictor of financial behavior or knowledge has been scarcely investigated. In our study, its effect is moderate but significant in a negative way on financial competence, only in the specific model (Model 4) and in Model 6 (general), when the two achievement competencies (in math and reading) were not included as drafters. Similarly, in another context, it has been reported that family support does not strengthen the effect of financial literacy on students’ investment intentions in Indonesia (Widagdo and Roz, 2022).

Although these eight variables were shown to be significant predictors of academic achievement in financial competencies, the effect of these variables was reduced when more complex, comprehensive models were tested, especially when the seventeen predictor variables of academic achievement were included in the seventh multilevel hierarchical model. In this comprehensive model, mathematics achievement, followed by reading achievement (mathematics literacy and reading literacy), significantly and positively predicted, with regression coefficients greater than 0.50; financial literacy achievement in PISA 2022, and to a lesser extent, familiarity with concepts of finance, also positively and significantly predicted financial literacy achievement.

The effect of mathematics achievement on financial competency achievement in PISA assessments has been reported in the case of Peru, with data from the 2018 assessments by Bazán-Ramírez et al. (2024) and the effect of reading achievement on financial competency. This association between mathematical learning and achievement with financial competence has also been noted by Amirullah et al. (2022) and Chu Cam et al. (2020). Similarly, Kusumawati et al. (2023) experimentally evidenced that learning and mastering mathematics lead to improved financial literacy.

A paradoxical aspect of the results is that, contrary to what was reported by secondary analyses of assessment results in financial competence in the PISA 2018 assessment, in which the variable financial education in school lessons had a significant effect on achievement in financial competence (Bazán-Ramírez et al., 2024; Carvalho and Carlo, 2021; Silinskas et al., 2023). In the present study, with data from PISA 2022, the variable financial education in school lessons had no significant effect, unlike the variable familiarity with concepts of finance. Similarly, Silinskas et al. (2021) reported a significant and positive association between financial education in school and financial competence.

A first possible explanation is that, in the present study, up to three disaggregated variables of financial education in school lessons were considered, and one of them was familiarity with concepts of finance. A second explanation could be that familiarity with concepts of finance could also come from classroom experiences, since financial education and mathematics education can be worked on simultaneously in school (Amirullah et al., 2022; Chu Cam et al., 2020). Either way, these results could suggest that Peruvian students are not developing their financial competencies and skills in the context of financial education itself (Carvalho and Carlo, 2021).

Finally, and considering as an important limitation in this study, perhaps by means of structural regression models the influence of financial education on financial competence, mediated by other variables that were included in the present multilevel hierarchical model, could be better assessed, as they have been studied in secondary analyses of financial competence in the PISA 2018 test (Bazán-Ramírez et al., 2024; Silinskas et al., 2021, 2023). This study is limited by its reliance on cross-sectional, self-reported data from PISA, which may not capture deeper behavioral patterns or changes over time. Additionally, the indirect measurement of financial literacy constructs and the exclusion of school-level variables in some models may limit the generalizability of findings. This remains a pending task for other studies on the results in PISA 2022 regarding financial achievement.

The results of this study have important theoretical as well as practical implications. At the theoretical level, the strong effect of math and reading achievement (>0.50) on financial competence suggests that financial skills build on fundamental academic competencies, rather than developing in isolation. This challenges approaches that treat financial literacy as a stand-alone domain. On a practical level, these findings are especially relevant for the implementation of the new Peruvian financial education curriculum in 2024, suggesting that educational interventions would be more effective if they explicitly integrate the development of financial competencies with the teaching of mathematics and reading comprehension, rather than addressing them as separate subjects. Furthermore, the loss of significance of sociodemographic variables in the comprehensive model suggests that improvements in academic achievement could help reduce socioeconomic gaps in the development of financial competencies.

6 Conclusion

Academic achievement in the PISA 2022 assessment of Peruvian adolescents’ financial competencies is primarily determined by academic performance in mathematics and reading, followed by familiarity with financial concepts. This conclusion is derived from the results of the full hierarchical model of a total of seven variables to explain the financial competence of Peruvian students, including a total of 17 predictor variables. The results of this study challenge the idea that financial education can be developed in isolation and rather underscore the need to strategically integrate it into the school curriculum.

These results highlight the importance of further strengthening the promotion and development of financial literacy in schools, especially as part of mathematics and communication courses, and including aspects of citizenship and interculturality, for the country’s public education policy. From an educational policy perspective, these results demand a curricular reconfiguration that overcomes the fragmentation of financial content. The recent inclusion of economic and financial education in the Peruvian national curriculum, starting in 2024, represents a decisive opportunity to link this learning with already developed skills in mathematics and reading comprehension. Similarly, for this curricular incorporation to have a real impact on Peruvian education, a continuing teacher training policy is also required, preparing teachers to address financial education from an interdisciplinary perspective contextualized to the socioeconomic realities of students.

A second relevant point is that familiarity with financial terminology is associated with mathematical and reading skills and is a good predictor of financial literacy. Students can develop financial literacy when they approach or practice financial concepts. This implies that theoretical knowledge can complement, but not replace, the cognitive skills essential for making informed economic decisions. These financial concepts and practices should be incorporated into the national curriculum as transversal or life skills, starting in primary education.

A third aspect worth highlighting is the impact of the school mean of index on Peruvian students’ financial literacy in PISA 2022. The student’s socioeconomic index and educational and cultural status have a significant effect on financial literacy achievement only at the school level, not at the individual level. That is, their impact on financial achievement is significant when the school-wide index includes socioeconomic and cultural status. Furthermore, its effect on financial literacy is highly significant only when academic achievement in mathematics and reading achievement were excluded as predictors of financial literacy.

Data availability statement

Publicly available datasets were analyzed in this study. This data can be found at: https://www.oecd.org/en/data/datasets/pisa-2022-database.html, PISA 2022 Database | OECD.

Ethics statement

Ethical review and approval was not required for the study on human participants in accordance with the local legislation and institutional requirements. Written informed consent from the participants or participants legal guardian/next of kin was not required to participate in this study in accordance with the national legislation and the institutional requirements.

Author contributions

AB-R: Conceptualization, Data curation, Formal analysis, Investigation, Methodology, Resources, Software, Supervision, Validation, Visualization, Writing – original draft, Writing – review & editing. EH-P: Formal analysis, Investigation, Methodology, Validation, Writing – original draft, Writing – review & editing. YP-M: Data curation, Supervision, Validation, Visualization, Writing – review & editing. WB-R: Data curation, Methodology, Validation, Writing – original draft, Writing – review & editing. EF-B: Investigation, Methodology, Supervision, Validation, Writing – original draft, Writing – review & editing.

Funding

The author(s) declare that financial support was received for the research and/or publication of this article. This research was carried out with the authors’ own resources.

Conflict of interest

The authors declare that this research was conducted in the absence of any commercial or financial relationships that could be construed as a possible conflict of interest.

Generative AI statement

The authors declare that no Gen AI was used in the creation of this manuscript.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Alshebami, A. S., and Al Marri, S. H. (2022). The impact of financial literacy on entrepreneurial intention: the mediating role of saving behavior. Front. Psychol. 13:911605. doi: 10.3389/fpsyg.2022.911605

Amagir, A., Groot, W., Maassen van den Brink, H., and Wilschut, A. (2018). A review of financial-literacy education programs for children and adolescents. Citizsh. Soc. Econ. Educ. 17, 56–80. doi: 10.1177/2047173417719555

Amirullah, A., Malela, N. M., and Biori, H. (2022). Financial numeracy in mathematics education: research and practice. Can. J. Sci. Math. Techn. Educ. 22, 481–484. doi: 10.1007/s42330-022-00215-4

Aprea, C., Wuttke, E., Breuer, K., Koh, N. K., Davies, P., Greimel-Fuhrmann, B., et al. (2016). International handbook of financial literacy. Singapore: Springer.

Bazán-Ramírez, A., Bazán-Ramírez, W., Hernández-Padilla, E., Félix-Benites, E., and Quispe-Morales, R. (2024). Efectos de variables familiares, socioeconómicas y de logro, sobre competencia financiera de estudiantes peruanos en PISA 2018 [Effects of family, socioeconomic and academic achievement variables on the financial competence of Peruvian students in PISA 2018]. Rev. Argent. Cienc. Comport. 16, 104–119. doi: 10.32348/1852.4206.v16.n1.44600

Beattie, J., Baron, J., Hershey, J. C., and Spranca, M. D. (1994). Psychological determinants of decision attitude. J. Behav. Decis. Mak. 7, 129–144. doi: 10.1002/bdm.3960070206

Carvalho, F. L., and Carlo, M. I. S. (2021). Letramento Financeiro dos Estudantes Brasileiros: análise do PISA 2015 [financial literacy of brazilian students: PISA 2015 analysis]. Rev. Adm. Unimep 19, 1–23.

Cavalcante, A., and Huang, H. (2022). Understanding Chinese students' success in the PISA financial literacy: a praxeological analysis of financial numeracy. Asian J Math. Educ. 1, 66–94. doi: 10.1177/27527263221091304

Cavalcante, A., and Savard, A. (2022). Understanding our world in a time of crisis: mathematics education pedagogy toward financial numeracy. J Honai Math 5, 109–126. doi: 10.30862/jhm.v5i2.261

Chu Cam, T., Nguyen Tien, D., and Vu Anh, T. (2020). A role of consumer and financial literacy context in numeracy education for junior high school students. J. Sci. Educ. Sci 65, 176–189. doi: 10.18173/2354-1075.2020-0122

Cordero, J. M., Gil-Izquierdo, M., and Pedraja-Chaparro, F. (2022). Financial education and student financial literacy: a cross-country analysis using PISA 2012 data. Soc. Sci. J. 59, 15–33. doi: 10.1016/j.soscij.2019.07.011

Ferrada, C., Díaz-Levicoy, D., Puraivan, E., and Lizana, A. (2022). Systematic review on financial education in the primary educational context. Rev. Lasallista Investig. 19, 21–51. doi: 10.22507/RLI.V19N1A2

Hornyák, A. (2018). Components of financial literacy of young people. Acta Univ. Sapientiae Econ. Bus. 6, 5–19. doi: 10.1515/auseb-2018-0001

Houle, J. N. (2014). A generation indebted: young adult debt across three cohorts. Soc. Probl. 61, 448–465. doi: 10.1525/sp.2014.12110

Khusaini, K., Mardisentosa, B., Bastian, A. F., Taufik, R., and Widiawati, W. (2022). The impact of financial education and socioeconomic status on the undergraduate students’ financial literacy. Media Ekonomi Dan Manajemen 27:55. doi: 10.24856/mem.v27i01.2385

Kolachev, N. I., Rutkovskaya, E. L., Kovaleva, G. S., and Polovnikova, A. V. (2021). Predictors of Russian students' financial literacy: the PISA 2018 results. Vopr Obrazovaniya-ED 4, 166–186. doi: 10.17323/1814-9545-2021-4-166-186

Kusumawati, I. B., Fachrudin, A. D., and Putri, R. I. I. (2023). Infusing Islamic financial literacy in mathematics education for Islamic school. J. Math. Educ. 14, 19–34. doi: 10.22342/jme.v14i1.pp19-34

Liu, S., Gao, L., Latif, K., Dar, A. A., Zia-UR-Rehman, M., and Baig, S. A. (2021). The behavioral role of digital economy adaptation in sustainable financial literacy and financial inclusion. Front. Psychol. 12:742118. doi: 10.3389/fpsyg.2021.742118

Mancone, S., Tosti, B., Corrado, S., Spica, G., Zanon, A., and Diotaiuti, P. (2024). Youth, money, and behavior: the impact of financial literacy programs. Front. Educ. 9:1397060. doi: 10.3389/feduc.2024.1397060

Méndez Prado, S. M., Zambrano Franco, M. J., Zambrano Zapata, S. G., Chiluiza García, K. M., Everaert, P., and Valcke, M. (2022). A systematic review of financial literacy research in Latin America and the Caribbean. Sustain. For. 14:3814. doi: 10.3390/su14073814

Mihalcova, B., Gallo, P., and Lukac, J. (2020). Management of innovations in finance education: cluster analysis for OECD countries. Marketing Management Innovations 1, 235–244. doi: 10.21272/mmi.2020.1-19

MINEDU (2024). Educación económica y financiera: documento de soporte para docentes de Educación Primaria y Secundaria (Ciencias Sociales) [Economic and financial education. Support document for teachers of primary and secondary education (social sciences)]. Lima: MINEDU. Available online at: https://hdl.handle.net/20.500.12799/10368

Moreno-Herrero, D., Salas-Velasco, M., and Sánchez-Campillo, J. (2018a). Factors that influence the level of financial literacy among young people: the role of parental engagement and students' experiences with money matters. Child Youth Serv. Rev. 95, 334–351. doi: 10.1016/j.childyouth.2018.10.042

Moreno-Herrero, D., Salas-Velasco, M., and Sánchez-Campillo, J. (2018b). The knowledge and skills that are essential to make financial decisions: first results from PISA 2012. Finanz Archiv 74, 293–339. doi: 10.1628/fa-2018-0009

Oberrauch, L., Kaiser, T., and Lusardi, A. (2025). Assessing financial literacy among the young. J. Financ. Lit. Wellbeing 2:1:1. doi: 10.1017/flw.2024.17

Organization for Economic Co-operation and Development (OECD) (2019a). “PISA 2018 financial literacy framework” in PISA 2018, assessment and analytical framework (Paris, France), 119–164. doi: 10.1787/a1fad77c-en4

Organization for Economic Co-operation and Development (OECD) (2019b). PISA 2018 assessment and analytical framework. Paris, France: OECD Publishing.

Organization for Economic Co-operation and Development (OECD) (2023). PISA 2022 assessment and analytical framework, PISA. Paris, France: OECD Publishing.

Organization for Economic Co-operation and Development (OECD) (2024). PISA 2022 technical report, PISA. Paris, France: OECD Publishing.

Preston, A., Qiu, L., and Wright, R. E. (2024). Understanding the gender gap in financial literacy: the role of culture. J. Consum. Aff. 58, 146–176. doi: 10.1111/joca.12517

Raudenbush, S. W., Bryk, A. S., Cheong, Y. F., and Congdon, R. (2019). HLM 8 for Windows [Computer software]. Skokie, IL: Scientific Software International, Inc.

Reisdorfer Da Silva, R. C., Freitas, C. A., Becker, K. L., Casagrande, D. L., and Cassola, N. M. (2024). Analysis of factors influencing the financial education of Brazilian school students. Int J Bus Manag. 26, 46–52.

Rostamkalaei, A., Riding, A., and Saridakis, G. (2024). Does financial knowledge affect borrower discouragement among various social categories? Evidence from the United States. J. Consum. Aff. 1–31. doi: 10.1111/joca.12612

Sagita, L., Putri, R. I. I., and Prahmana, R. C. I. (2022). Promising research studies between mathematics literacy and financial literacy through project-based learning. J. Math. Educ. 13, 753–772. doi: 10.22342/jme.v13i4.pp753-772

Savard, A., and Cavalcante, A. (2021). Financial numeracy in mathematics education: research and practice. Cham: Springer International Publishing.

Silinskas, G., Ahonen, A. K., and Wilska, T. A. (2021). Financial literacy among Finnish adolescents in PISA 2018: the role of financial learning and dispositional factors. Large-Scale Assess E. 9. doi: 10.1186/S40536-021-00118-0

Silinskas, G., Ahonen, A. K., and Wilska, T. A. (2023). School and family environments promote adolescents' financial confidence: indirect paths to financial literacy skills in Finnish PISA 2018. J. Consum. Aff. 57, 593–618. doi: 10.1111/joca.12513

Tat, O., Koyuncu, I., and Gelbal, S. (2019). The influence of using plausible values and survey weights on multiple regression and hierarchical linear model parameters. J Meas Eval Educ Psy. 10, 235–248. doi: 10.21031/epod.486999

Tzora, V. A., Philippas, N. D., and Panos, G. A. (2023). The financial capability of 15-year-olds in Greece. Econ. Lett. 225:111044. doi: 10.1016/j.econlet.2023.111044

Keywords: competencies, achievement, financial, literacy, PISA 2022, Peruvian students, experience

Citation: Bazán-Ramírez A, Hernández-Padilla E, Palomino-Malpartida YG, Bazán-Ramírez W and Félix-Benites E (2025) Predictors of financial competence of Peruvian high school students in PISA 2022. Front. Educ. 10:1563131. doi: 10.3389/feduc.2025.1563131

Edited by:

Stefania Mancone, University of Cassino, ItalyReviewed by:

Francesco Di Prinzio, University of Salerno, ItalyIvonne Carosi Arcangeli, University of Salerno, Italy

Copyright © 2025 Bazán-Ramírez, Hernández-Padilla, Palomino-Malpartida, Bazán-Ramírez and Félix-Benites. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Aldo Bazán-Ramírez, YWJhemFucmFtaXJlekBnbWFpbC5jb20=