Carlos Valdivia Alcántara

Carlos Valdivia Alcántara Eliana Canafoglia

Eliana Canafoglia- 1Instituto de Ciencias Sociales, Humanas y Ambientales, CONICET, Mendoza, Argentina

- 2Cátedra de Metodología de las Ciencias Sociales, Facultad de Ciencias Políticas y Sociales, Universidad Nacional de Cuyo, Mendoza, Argentina

Argentina possesses abundant quartz resources and a solid scientific legacy in nuclear and satellite technologies. However, the country lacks a developed value chain for producing solar-grade silicon. This paper aims to analyze Argentina’s current situation, identify existing capabilities, and assess the obstacles to creating a local silicon industry for photovoltaic applications. A qualitative research approach was used, based on document analysis and triangulation of national and international sources. The study identifies the relevant actors, policies and infrastructure relating to quartz mining, silicon purification and photovoltaic development. Results show that while Argentina has institutional knowledge and quartz reserves—especially in Córdoba and San Luis—it lacks purification facilities, specialized laboratories, and policy coordination. Key institutions like CNEA and INVAP possess technical know-how but are disconnected from productive sectors. The article concludes that Argentina’s integration into the global photovoltaic value chain depends on targeted policies, infrastructure development, and international cooperation. It recommends pilot purification plants, improved material testing capacity, and a national strategy for high-purity silicon.

1 Introduction

The current climate crisis, primarily caused by greenhouse gas emissions from fossil fuel combustion, is deeply intertwined with the development of the modern capitalist system. This emergency has prompted, since the 1970s, a series of institutional agreements aimed at mitigating its consequences. One of the most significant and recent milestones occurred during the 21st Climate Summit in 2015, where the Paris Agreement was signed, followed by the adoption of the UN’s 2030 Agenda in 2016 (Serrani, 2020). These agreements establish a set of binding guidelines for the signatory countries, with the most prominent being the decarbonization of the energy mix through a transition that encourages the adoption and development of renewable energy sources.

Historically, energy transitions have been triggered by technological breakthroughs or the discovery of new primary resources, such as the shift from coal to oil. These transitions have led to profound transformations in infrastructure, institutions, regulations, and consumption patterns - processes that typically unfold over decades. As a result, different energy sources often coexist, and the dominance of one over another varies by country and context (Kern and Markard, 2016). The current transition toward renewable energy shares these characteristics but is distinct in its intentionality: it is being actively driven by international governmental institutions in response to the urgent ecological risks facing the planet (Serrani, 2020). Consequently, this transition is a complex and multidimensional process, marked by significant uncertainty and requiring robust public policies to guide and promote it (Kern and Markard, 2016). The state plays a pivotal role in this process by ensuring that supply meets demand and fostering technological development and innovation at various levels, while also providing targeted incentives to related industries. These actions help to reduce risks and uncertainty (Chang and Andreoni 2020). At the same time, the transition is shaped by conflicting interests and objectives within the process, as well as country-specificities that can either enable or constrain changes (Lazaro and Serrani, 2023).

Among renewable energy sources, solar photovoltaic energy currently stands out as one of the most promising, owing to unique characteristics that set it apart. Globally, solar energy has reached 407 GW, with a total accumulated photovoltaic capacity of 1,581 GWp, representing 5.5% of global electricity generation (Philipps and Warmuth, 2024). This growth is mainly attributable to two factors. First, its high modularity allows for the generation of large amounts of energy through solar farms for mass consumption, as well as the installation of systems in homes and public spaces. Second, constant improvements across all links of its global value chain have significantly reduced the price of solar panels, making it one of the most competitive technologies today, with cost reductions nearing 99% over the past 4 decades. Key improvements in solar panels driving this growth include their efficiency, which in the 1970s was only 6.32%, whereas today most solar modules achieve 22%, and laboratory experiments have achieved efficiencies in the range of 24%–27% using various technologies (Philipps and Warmuth, 2024; International Energy Agency, 2022; Asmelash and Prakash, 2019; Kavlak et al., 2018).

These advancements have been made possible by improvements in crystalline silicon wafer growth methods, optimization of energy consumption and associated processing techniques, the thinning of silicon wafers, and the creation of new architectures based on conventional, advanced, or alternative material solar cells. Additionally, reductions in the price of raw materials for polysilicon production have played a significant contributing factor (International Energy Agency, 2022; Kavlak et al., 2018; Yuan et al., 2024).

All these elements contributed to the global expansion and competitiveness of solar energy up to the early 2000s. Since then, economies of scale and supportive government policies -particularly China’s central role-have driven further cost reductions and enhanced competitiveness (International Energy Agency, 2022). Despite these advances, processed silicon -specifically crystalline silicon (c-Si)- remains the dominant raw material for solar cell production, accounting for 97% of the global market (Philipps and Warmuth, 2024). This silicon is produced through complex processes amid increasing raw material scarcity, rising global demand, and the concentration of development among a few key stakeholders.

Within this global context, this article focuses on the development of the solar-grade silicon value chain in Argentina and the technological advancements associated with this material. Efforts in this country to produce solar-grade silicon date back to the 1970s, led by the Solar Energy Department of the National Atomic Energy Commission (DES - CNEA in Spanish), which has since achieved significant progress in silicon-related technologies. More recently, the development of the RA-10 multipurpose nuclear reactor is expected to facilitate the production of doped silicon, potentially positioning Argentina as a relevant actor in this strategic sector. This study examines the production processes and value chain of solar-grade silicon as a fundamental component of photovoltaic cells. The analysis considers both its potential applications and the structural limitations facing the integration of this material into terrestrial and satellite equipment manufacturing within Argentina’s current political and economic context, providing an in-depth examination of the national and global dynamics shaping the development of this critical technological input.

The main objective of this article is to analyze the opportunities and limitations for Argentina to develop a domestic value chain for solar-grade silicon, from quartz extraction to its potential application in photovoltaic technologies. The study particularly focuses on both terrestrial and satellite uses, evaluating the country’s technological capabilities, industrial gaps, and strategic role in the global silicon value chain.

2 Methods

This research follows a qualitative methodological design centered on a comprehensive literature review and documentary analysis. It integrates international and national sources of data, including technical reports, scientific publications, government databases, and expert interviews.

International data focuses on the structure and actors of the global value chain (GVC) of solar-grade silicon, particularly the role of China and other major players. These were collected from the International Energy Agency (IEA), International Trade Centre (ITC), U.S. Geological Survey and BloombergNEF. National data considers geological reports (Argentine Mining Geological Service, SEGEMAR in Spanish, and Ministry of Mining and Energy), statistical production indices (National Statistic Institute, INDEC in Spanish), and institutional documentation from Argentine organizations such as the National Atomic Energy Commission (CNEA in Spanish), INVAP (Investigaciones Aplicadas S.E. in Spanish), and National Commission on Space Activities (CONAE in Spanish).

The methodology involved triangulating historical data with contemporary assessments of technological capacity, production feasibility, and political-economic conditions, with a focus on understanding Argentina’s position in this strategic sector. To ensure robustness, this review applied methodological triangulation by integrating data from academic literature, technical documents, and expert interviews. The inclusion criteria prioritized recent publications (last 10 years), official statistics (e.g., SEGEMAR, INDEC), and peer-reviewed scientific reports (e.g., Gallisky and y Sfragulla 2014). Data were weighted according to their source reliability, level of detail, and relevance to technological and industrial development in Argentina. When discrepancies among sources emerged, a cross-verification approach was used, privileging institutional technical data (CNEA, CONAE) and the guidance of the interviewed experts. This methodological strategy allowed for the construction of a comprehensive picture of the current state and potential of the national solar-grade silicon chain.

3 Results

3.1 Global silicon industry

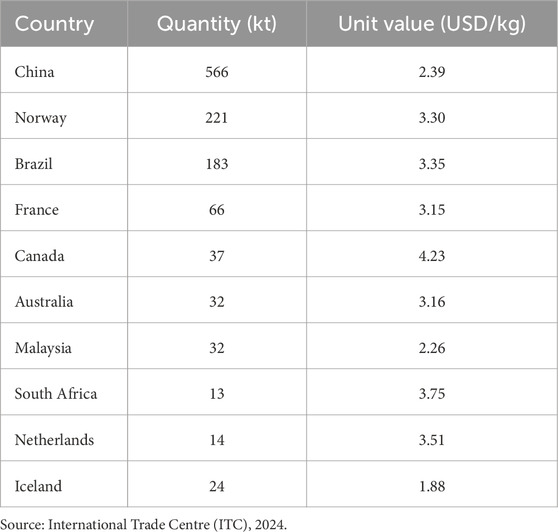

Historically, silicon (Si) has had diverse uses, ranging from optics to construction. However, since World War II, new physical and chemical processes for purifying this element have been developed, making it one of the main components in the electronics, semiconductor, and renewable energy industries due to its chemical, electrical, thermal, and mechanical properties (Vatalis et al., 2015). In the case of the photovoltaic solar industry, high-purity silicon known as solar-grade is required. This is the central element of solar cells and controls approximately 97% of the market (Heidari and Anctil, 2022). While silicon is the second most abundant material on the planet, the type of silicon required for solar cells must meet specific conditions, primarily obtained from quartz mines with high purity levels or through industrial processing Table 1. Considering that deposits of this type of quartz are scarce, it becomes a strategic resource, creating tension between the growth of solar energy and the technical-economic processes necessary for its development (Pan et al., 2022).

Table 1. Main exporting countries of silicon with purity below 99%.

Currently, there are four main types of high-quality quartz: the first has a purity of at least 99.9%, referred to as standard quality (3N); next is medium-quality quartz (4N) with at least 99.99%; followed by high-purity quartz (4N5) with 99.995% or higher; and finally, ultra-high-purity quartz (4N8) with at least 99.998% (Zhang et al., 2023). Achieving this level of purity requires the quartz to have a specific molecular structure, along with the appropriate procedures to eliminate impurities that limit its characteristics. In the case of the photovoltaic solar industry, the most commonly used types of quartz are pegmatite and vein quartz, as their crystallization contains low levels of impurities. This allows for the removal of elements that limit their properties during processing, resulting in high-quality quartz sand.

The main deposits of this type of quartz are scarce and are located in the United States, Australia, Mauritania, Norway, Brazil, and Russia. These countries have the capacity to process this raw material. In the United States, the Spruce Pine mine is located in North Carolina. This mine contains the largest reserves for the production of ultra-highquality quartz, with around 10 million tons, allowing it to control approximately 90% of the market through Unimin Corporation (Wang, 2021; Pan et al., 2022).

3.1.1 Quartz processing for metallurgical-grade silicon (MG-Si)

For the development of solar cells, industrial-grade quartz sand with a purity of at least 95% is required, obtained from natural quartz deposits. Once extracted, the quartz undergoes a crushing process to reduce its size and facilitate subsequent processing. Next, grinding is performed, during which the material is converted into finer particles. Magnetic separation is then applied to extract ferrous elements, followed by the addition of chemical reagents to remove light metals such as aluminum and titanium. Finally, the material is washed with water and dried in ovens or under the sun before being classified according to its size (Zhang et al., 2023).

Once the processed quartz sand is obtained, metallurgical-grade silicon (MG-Si) is produced with a minimum purity of 99%. At this stage, remaining impurities such as iron (Fe), aluminum (Al), phosphorus (P), and other elements are removed. Subsequently, the silicon is refined to achieve the purity levels required by the solar industry, which range from 99.99% (4N) to 99.9999% (6N) (Pan et al., 2022). This process is critical because the purity level of the silicon determines the efficiency of the solar cells (Safarian et al., 2012).

To obtain metallurgical-grade silicon, industrial-grade quartz must be processed through carbothermal reduction in an electric arc furnace at temperatures ranging from 1780 °C to 2000 °C. The process involves crushing the quartz and mixing it with a reducing agent, such as coal or petroleum coke, along with wood chips to enhance the reaction. Once the mixture is prepared, it is placed in the furnace at high temperatures. The chemical reaction produces silicon with a purity of between 98% and 99%, along with carbon monoxide. The denser silicon settles at the bottom of the furnace, exits through a tap hole, and is collected in refractory molds or trays to cool (Safarian et al., 2012).

3.1.2 Quartz processing for solar grade silicon

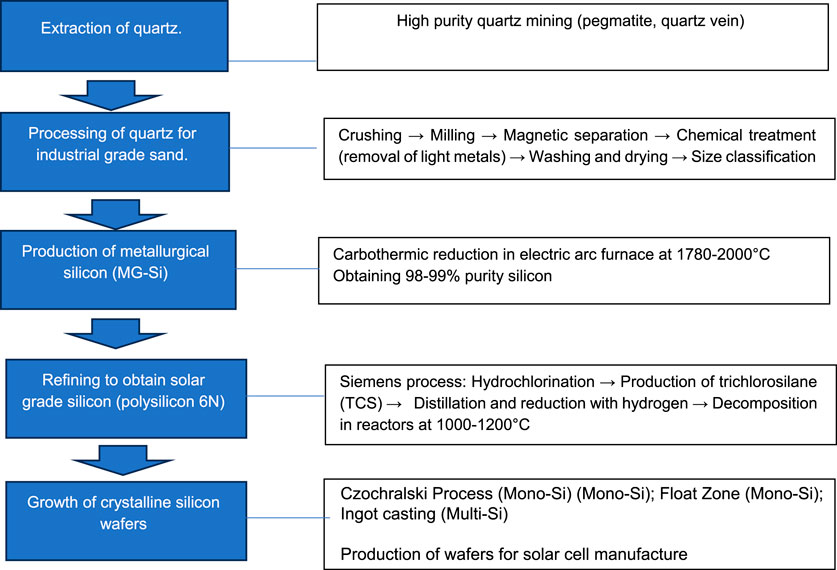

Due to the stringent specifications needed to obtain 6N solar-grade polysilicon (Figure 1), its production involves highly intensive energy and industrial processes. To achieve this necessary level of purification, there are currently several methods aimed at improving the efficiency and cost of the procedures. The most widely used method is the Siemens process, which involves the hydrochlorination of silicon at temperatures close to 300 °C to produce trichlorosilane (TCS). Once obtained, it is distilled and reduced with hydrogen (H) to produce pure trichlorosilane, which is then decomposed in reactors at temperatures near 1000 °C-1200 °C. This stage breaks down the TCS, releasing pure solid silicon and forming high-purity polycrystalline silicon. This method requires a significant amount of energy, approximately 50–75 kWh/kg; therefore, only a few stakeholders in the world are capable of producing this type of silicon at industrial levels (Míguez Novoa et al., 2024; Safarian et al., 2012).

Figure 1. Process for solar-grade silicon production. Source: Elaboration base on Míguez Novoa et al. (2024), Safarian, et al. (2012).

The characteristics of this method have promoted alternative forms of silicon purification, either by price or lower complexity. These alternatives include replacing TCS with other compounds such as silane (SiH4), distilling metallurgical silicon into volatile forms of the element, or using mechanical methods focused on removing specific elements such as phosphorus (P) or boron (B). There are also methods that remove impurities through plasma or chemical refining using various types of acids or chlorine (Lan, 2024; Safarian et al., 2012). Once polycrystalline silicon is obtained, three main methods are primarily used to grow it into wafers to obtain crystalline silicon (c-Si), either monocrystalline (Mono-Si) or multicrystalline (Multi-Si), which are then used to create solar cells. The first method is the Czochralski (CZ) process, which produces Mono-Si; there is also the floating zone (FZ) method, and finally, the ingot casting or melt method, which produces Multi-Si (Ranjan et al., 2011; Ciftja et al., 2008).

3.1.3 The main actors in the global solar-grade silicon sector

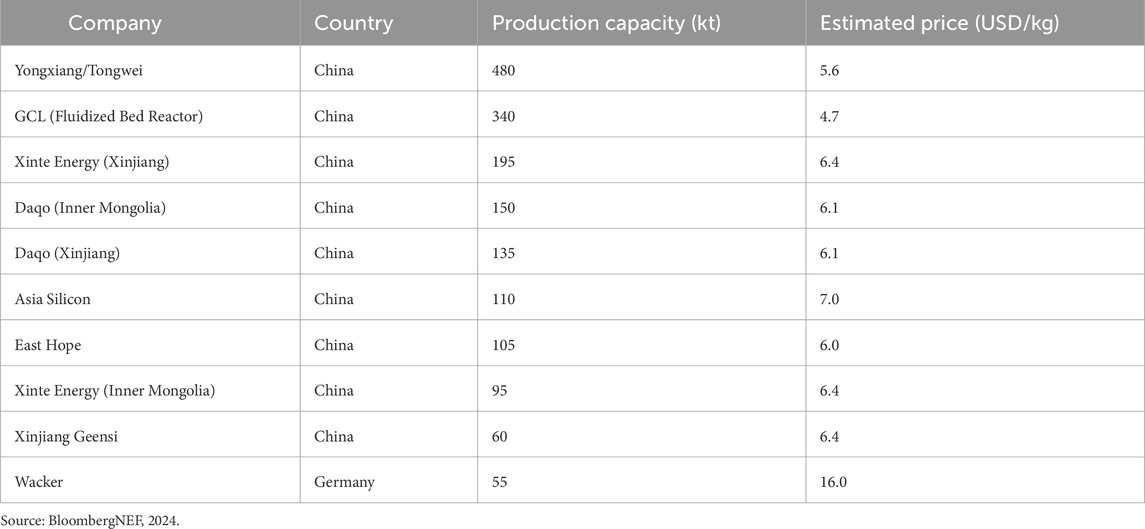

China produces nearly 80% of the solar-grade polysilicon used in the creation of solar modules. In the coming years, this demand is expected to grow significantly alongside solar energy (Heidari and Anctil, 2022). In this regard, only a few countries can achieve this scale, with China being the leading producer of metallurgical silicon: it produces approximately 6 million metric tons of this material, controlling about 70% of the global market for this type of silicon (Table 2). Russia and Brazil follow, with productions of 640,000 and 400,000 metric tons, respectively (U.S. Geological Survey, 2023). Most of the production is used domestically, while around 10% is exported. Although China dominates the MG-Si market, its main weakness lies in the lack of large deposits of high-quality quartz.

Table 2. Top 10 global solar-grade silicon producers in 2024.

Nowadays, Mono-Si is the dominant technology for manufacturing solar cells (IEA, 2022; Philipps and Warmuth, 2024), thanks to improvements in production processes that have led to a reduction in the price (Lan, 2024; Ovaitt, Mirletz, Seetharaman & Barnes, 2022; Kavlak et al., 2024). China has made significant advances in this processes and the scale of production to do so. However, much of the material is imported from countries such as Australia, Cambodia, Malaysia, Vietnam, and Pakistan (Wang, 2021; Zhang et al., 2023). Adding to this, the economic sanctions imposed on China by the United States and the European Union could further complicate this link in the photovoltaic solar value chain (Golub, 2019; Lüke and Pölher, 2025).

3.2 Argentine silicon production

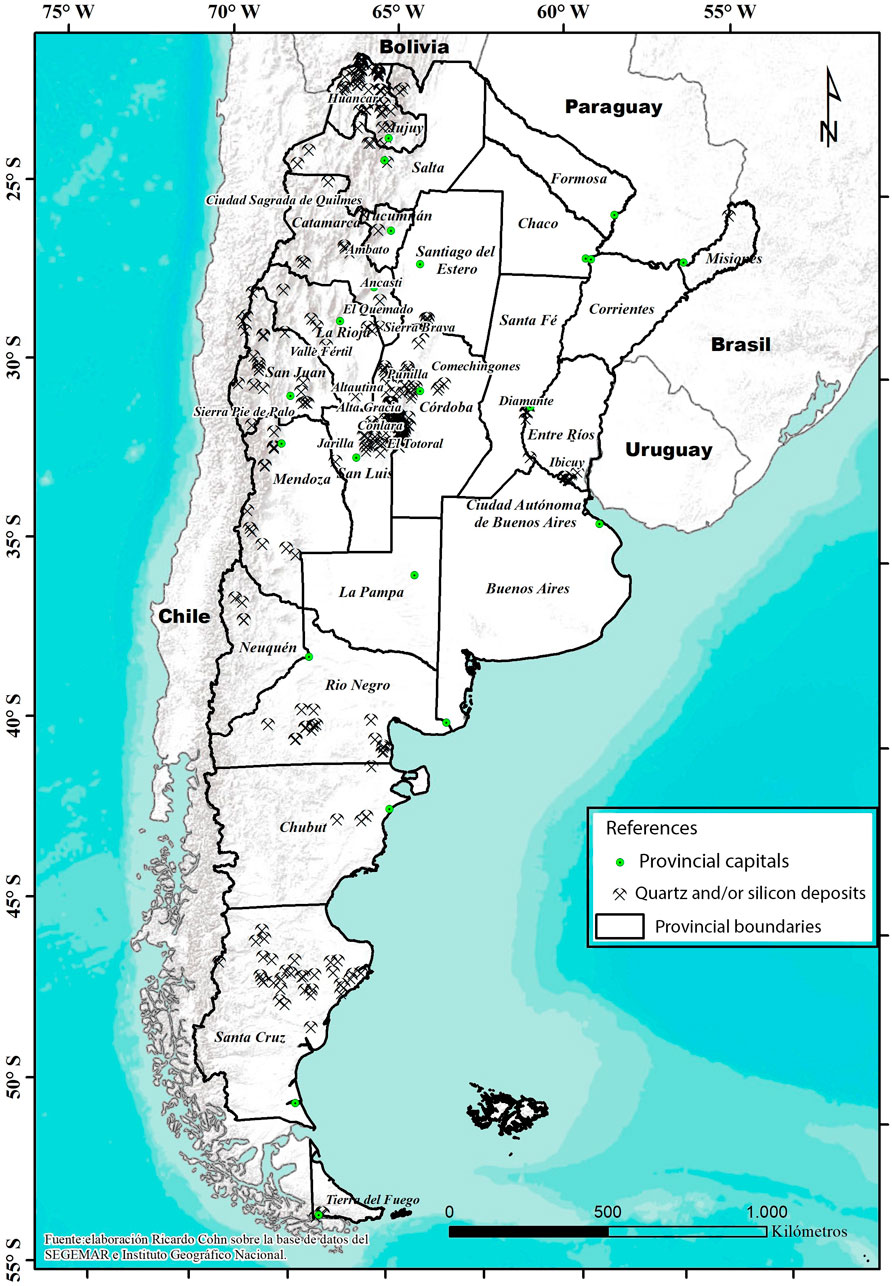

In Argentina, main quartz deposits are located in the Sierras Pampeanas region, which spans the provinces of Catamarca, Córdoba, La Rioja, San Juan, San Luis, Santiago del Estero, and Tucumán (Figure 2). The geographical characteristics of this region result in a large amount of granitic pegmatite relatively small in size (Gozalvez et al., 2004; Galliski et al., 2022).

Figure 2. Quartz and/or Silica-Bearing Mineral Deposits–Republic of Argentina. Source: SEGEMAR.

Different types of pegmatites can be found in Córdoba. Among the most important areas are Altautina, Alta Gracia, Punilla, and Comechingones, where both the types of mines and the quality of the quartz vary significantly (Galliski and y Sfragulla, 2014). In the province of La Rioja, the Sierra Brava area contains open-pit mines that operate on an artisanal scale with low productivity. In San Juan, the Valle Fértil and Sierra Pie de Palo regions host mines with varying productivity levels. Meanwhile, San Luis has two significant zones—Totoral and Conlara—both featuring high-productivity open-pit mines due to the presence of other valuable minerals (Galliski et al., 2022). In Catamarca, Salta, and Tucumán, the main deposits are located in the Ambato, Ancasti, El Quemado, and Quilmes areas. These are open-pit mines whose exploitation began in the mid-20th century and are characterized by low to medium productivity.

Another source of quartz is silica sand, which consists of naturally refined sediments. The main deposits of silica sand are found in Entre Ríos (Diamante and Ibicuy regions), along the Jarilla River in San Luis, in Chubut, and in the Huancar Chico area of Jujuy (Gozalvez et al., 2004; Ministerio de Energía y Minería, 2017).

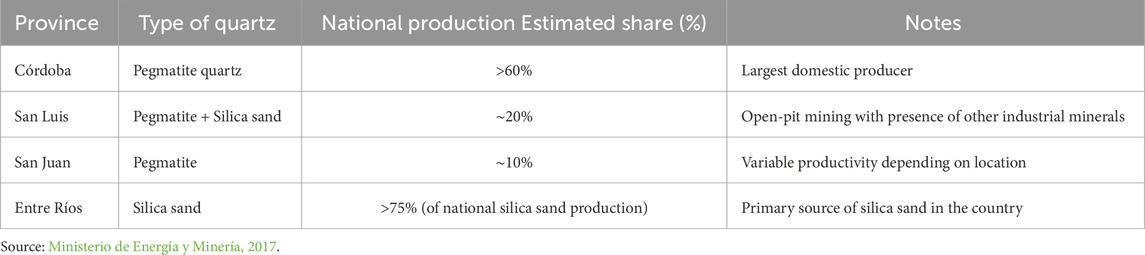

The province that produces the most quartz in the country is Córdoba, accounting for over 60% of national production (Table 3). San Luis ranks second with approximately 20%, followed by San Juan with around 10%. In the case of silica sand, the largest producer is the province of Entre Ríos, with over 75% of national production, followed by Chubut and San Luis. Regarding the destination of quartz, most of it is directed toward the domestic market (Ministerio de Energía y Minería, 2017). Quartz is used in the production of ferrosilicon, in the glass and refractory industries, and as an abrasive material. In 1980, there were approximately 160 producers (Catalano, 2004).

Table 3. Key quartz-producing provinces in Argentina and estimated production share.

The majority of raw quartz production is directed toward various industrial sectors, with grinding accounting for approximately 80%, followed by the glass, chemical, ceramic, and electronics industries. This indicates that most producers extract quartz but do not process it further. In the case of processed quartz, the majority is destined for the metallurgical industry (approximately 50%), followed by the glass industry (30%) and the electronics sector (around 10%) (Ministerio de Energía y Minería, 2017).

According to data from June 2024, the production of non-metallic minerals has declined compared to previous years. At the national level, quartz production has decreased by approximately 25% compared to 2016 levels. Similarly, silica sand extraction has dropped by about 10% (Instituto Nacional de Estadística y Censos, 2024).

3.3 Technological developments with crystalline silicon

The development of crystalline silicon technologies in Argentina, while still limited in scope (with little or no linkages between sectors for the production of high-purity silicon), includes several notable milestones. One of the most prominent efforts is led by the Solar Energy Department (DES) at the National Atomic Energy Commission (CNEA), which began researching and developing monocrystalline silicon in the late 1970s (Bolzi, 2018). This initiative resulted in the creation of Argentina’s first wafer production lab in 1986 in collaboration with INVAP, utilizing the Czochralski process to reach the necessary purity levels for electronics and photovoltaic applications.

Throughout the 1990s, DES-CNEA advanced the production of photovoltaic cells, installing diffusion/oxidation furnaces and developing sensors and cells for space and meteorological missions (Tamasi et al., 2021). This included setting national standards for solar energy systems alongside IRAM (Argentine Institute of Standardization).

In 2001, the first photovoltaic module composed of 36 interconnected cells was produced and used to power a solar cooker tracking system (Martínez Bogado, 2011). The space sector marked another major application: monocrystalline silicon solar cells developed at CNEA were tested onboard the SAC-A satellite (1998) and later used in SAC-D (2011), which featured panels jointly manufactured with INVAP. The SAOCOM one series also utilized solar sensors and modules with thousands of interconnected cells (Godfrin, 2021).

These developments fostered expertise in the simulation, fabrication, and optimization of silicon-based devices, including solar sensors and anti-reflective coatings. In parallel, the upcoming RA-10 Multipurpose Reactor (Cintas, 2014; Deza 2024) is poised to produce doped silicon via neutron transmutation, placing Argentina among the few global suppliers of this high-value material for the semiconductor industry.

3.3.1 Projects and opportunities

Argentina holds potential to further develop its silicon industry. The country possesses significant quartz resources, especially in Córdoba, San Luis, La Rioja, and San Juan, which historically supplied material for metallurgical-grade silicon production. A notable case was Electrometalúrgica Andina, which produced silicon by blending quartz from different provinces.

The RA-10 reactor represents a major opportunity. With a projected capacity of 80 tons of doped silicon annually, the country could meet part of the international demand for semiconductors—an industry worth over $700 billion globally. This would open doors for local value creation and strategic insertion into global supply chains.

Other initiatives, such as collaborations between DES-CNEA, INVAP, and CONAE, along with international partners like Unicamp and NASA, underscore Argentina’s capability to produce solar sensors and related components for both space and terrestrial use. These partnerships demonstrate the potential for technology transfer into broader photovoltaic applications.

3.3.2 Challenges and limitations

The development of a complete domestic value chain for high-purity silicon faces several obstacles. Quartz reserves often lack the necessary purity for solar applications, and local facilities are not equipped to conduct the advanced chemical analyses required to assess their suitability. Testing must be outsourced to labs in countries like Germany or Norway, increasing costs significantly.

Additionally, there is no large-scale infrastructure for the purification of quartz into metallurgical- or solar-grade silicon. This limits scalability and prevents the consolidation of local manufacturing. Technological developments remain largely confined to specialized institutions and do not yet extend into broader industrial production.

China’s dominance in the silicon market, driven by its scale, low costs, and state support, presents another hurdle. It makes domestic cell manufacturing economically unviable without strong public policy and investment.

Finally, recent solar cell manufacturing projects in Argentina have suffered from a lack of institutional and financial support. Some initiatives, like those by CONAE, have succeeded in producing monocrystalline silicon components, but others remain incomplete or operate sporadically, with craft equipment and for specific purposes.

4 Conclusion

This article examined the current status and potential of Argentina to develop a domestic value chain for solar-grade silicon. The main findings indicate that, although the country possesses significant geological resources - especially quartz deposits in provinces such as Córdoba and San Luis- and has accumulated substantial scientific and technical expertise over decades, particularly through institutions like CNEA and INVAP, these assets remain largely disconnected from an industrial framework capable of processing the material to the purity levels required for photovoltaic applications.

Currently, Argentina lacks the infrastructure to purify quartz to 4N or 6N levels, and high-purity testing still depends on foreign laboratories. While the RA-10 reactor could position the country as a potential future supplier of doped silicon for semiconductor applications, the absence of intermediate-scale processing facilities constrains efforts to establish a fully integrated value chain. Consequently, most quartz continues to be utilized in low value-added sectors such as grinding and glass manufacturing, rather than in higher-technology applications.

A key contribution of this work is the mapping of existing capacities and limitations within the national silicon value chain, linking historical developments -such as wafer and photovoltaic cell production in the 1980s and 1990s-with more recent advances in the space sector. Based on this comprehensive overview, several strategic lines of action are proposed:

• From a policy perspective, it is essential to promote the installation of pilot purification plants and support research infrastructure capable of analyzing quartz and silicon purity.

• From an industrial standpoint, it is necessary to foster coordination in order to align ongoing developments in the satellite and nuclear sectors with broader photovoltaic applications.

• In terms of research, consolidating and expanding institutional capabilities that already exist could provide a foundation to scale these technologies.

At an international level, cooperating with countries that have developed purification technologies and quality standards, such as Germany and Norway, would reduce the learning curve and enable Argentina to integrate more effectively into the global value chain.

Furthermore, any attempt to develop this sector must consider the social and environmental implications of expanding quartz extraction and processing, particularly in provinces that are ecologically sensitive or have limited institutional oversight.

Argentina’s participation in the global solar industry will ultimately depend on its ability to turn its scientific knowledge and mineral resources into strategic production capabilities through long-term planning and targeted industrial policy.

Data availability statement

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding authors.

Author contributions

CV: Writing – review and editing, Formal Analysis, Validation, Resources, Visualization, Funding acquisition, Writing – original draft, Project administration, Investigation, Methodology, Data curation, Supervision, Conceptualization, Software. EC: Methodology, Data curation, Investigation, Validation, Conceptualization, Writing – review and editing, Supervision, Visualization, Writing – original draft, Formal Analysis, Software, Project administration, Funding acquisition, Resources.

Funding

The author(s) declare that no financial support was received for the research and/or publication of this article.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Generative AI statement

The author(s) declare that no Generative AI was used in the creation of this manuscript.

Any alternative text (alt text) provided alongside figures in this article has been generated by Frontiers with the support of artificial intelligence and reasonable efforts have been made to ensure accuracy, including review by the authors wherever possible. If you identify any issues, please contact us.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Abbreviations

CGV, Global value chain; C-Si, Crystalline silicon; DES - CNEA, Solar Energy Department of the National Atomic Energy Commission; CNEA, National Atomic Energy Commission; CONAE, National Commission on Space Activities; H, Hydrogen; IEA, International Energy Agency; INDEC, National Institute of Statistics and Census; INVAP, Investigaciones Aplicadas S.E.; ITC, International Trade Centre; MG-Si, Metallurgical-Grade Silicon; SEGEMAR, Argentine Mining Geological Service; TCS, Trichlorosilane TCS; UN, United Nations Organization.

References

Asmelash, E., and Prakash, G. (2019). “Future of solar Photovoltaic: deployment, investment, technology, grid integration and socio-economic aspects,”Int. Renew. Energy Agency, 1–73. Available online at: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2019/Nov/IRENA_Future_of_Solar_PV_2019.pdf.

Bolzi, C. (2018). “Paneles y sensores solares espaciales,” in Serie: hojitas de conocimiento Nº 27 CIENCIA. IEDS - CNEA. Available online at: https://nuclea.cnea.gob.ar/bitstreams/bf79d90c-9ab7-4295-9c2e261bcdc4a7fd/download.

Catalano, E. (2004). “Antecedentes y Estructura Histórica de la Minería Argentina. En Historia de la Minería Argentina. En Historia de la Minería Argentina. Buenos Aires, Argentina: Tomo I. SEGEMAR.

Chang, H., and Andreoni, A. (2020). Industrial policy in the 21st century. Dev. Change, Int. Inst. Soc. Stud. 51 (2), 324–351. doi:10.1111/dech.12570

Ciftja, A., Engh, T. A., and Tangstad, M. (2008). Refining and recycling of silicon: a review. Trondheim, Norway: Norwegian University of Science and Technology. Available online at: https://ntnuopen.ntnu.no/ntnu-xmlui/handle/11250/244462.

Cintas, A. (2014). “Silicon doping process at the RA10,”XLI Annu. Meet. Argentine Assoc. Nucl. Technol. (AATN 2014). Buenos Aires, Argentina: AATN, 7–7.

Deza, N. (2024). ¿Qué es el dopaje de silicio, el nuevo servicio del reactor RA-10 que podría posicionar al país en la industria electrónica? EconoJournal. Available online at: https://econojournal.com.ar/2024/08/dopaje-de-silicio-servicio-reactor-ra-10-industriaelectronica/.

Galliski, M., and y Sfragulla, J. (2014). Las pegmatitas graníticas de las Sierras de Córdoba. Relatorio del XIX Congreso Geológico Argentino - Córdoba. Available online at: https://bicyt.conicet.gov.ar/fichas/produccion/en/2720121.

Galliski, M. Á., Márquez-Zavalía, M. F., Roda-Robles, E., and von Quadt, A. (2022). The LiBearing pegmatites from the pampean pegmatite province, Argentina: metallogenesis and resources. Minerals 12, 841. doi:10.3390/min12070841

Godfrin, E. M. (2021). Misiones satelitales SAOCOM 1: análisis del funcionamiento de los paneles solares en órbita. Energías Renov. Y Medio Ambiente 47, 1–9. Available online at: https://portalderevistas.unsa.edu.ar/index.php/erma/article/view/2844.

Golub, P. (2019). Entre Estados Unidos y China, una guerra más geopolítica que comercial. París, Francia: Le monde diplomatique. Available online at: https://mondiplo.com/entre-estadosunidos-y-china-una-guerra-mas.

Gozalvez, M. R., Herrmann, C. J., and Zappettini, E. O. (2004). Minerales Industriales de la República Argentina. SEGEMAR. Available online at: http://repositorio.segemar.gov.ar/308849217/2747.

Heidari, S. M., and Anctil, A. (2022). Country-specific carbon footprint and cumulative energy demand of metallurgical grade silicon production for silicon photovoltaics. Resour. Conserv. Recycl. 180, 106171. doi:10.1016/j.resconrec.2022.106171

Instituto Nacional de Estadística y Censos (INDEC) (2024). Índice de producción industrial minero. Junio de 2024. Informes técnicos, 8(172). Ind. minera 2 (8). ISSN 2545-6636.

International Energy Agency (2022). Special report on solar PV global supply chains. París, Francia: OECD Publishing. Available online at: https://www.iea.org/reports/solar-pv-global-supply-chains.

Kavlak, G., McNerney, J., and Trancik, J. E. (2018). Evaluating the causes of cost reduction in photovoltaic modules. Energy policy 123, 700–710. doi:10.1016/j.enpol.2018.08.015

Kavlak, G., Klemun, M. M., Kamat, A., Smith, B., Margolis, R., and Trancik, J. E. (2024). Nature of innovations affecting photovoltaic system costs. SSRN J. doi:10.2139/ssrn.4695169

Kern, F., and Markard, J. (2016). “Analysing energy transitions: combining insights from transition studies and international political economy,” in The Palgrave handbook of the international political economy of energy, 291–318.

Lan, C. W. (2024). Twenty years crystal growth of solar silicon: my serendipity journey. J. Cryst. Growth 626, 127480. doi:10.1016/j.jcrysgro.2023.127480

Lazaro, L., and Serrani, E. (2023). “Energy transitions in Latin America. The tough route to sustainable development,”. Cham: Springer. (coords). doi:10.1007/978-3-031-37476-0

Lüke, V., and Pölher, B. (2025). The EU’s 15th sanctions package - renewed focus on Sanctions Evasion. London, United Kingdom: Clyde&CO. Available online at: https://www.clydeco.com/en/insights/2025/01/eu-15th-sanctions-package.

Martínez Bogado, M. (2011). Materiales y materias primas. Silicio. Guía Didáctica. Instituto Nacional de Educación Tecnológica. Ministerio de Educación. CABA.

Míguez Novoa, J. M., Hoffmann, V., Forniés, E., Mendez, L., Tojeiro, M., Ruiz, F., et al. (2024). Production of upgraded metallurgical-grade silicon for a low-cost, high-efficiency, and reliable PV technology. Front. Photonics 5, 1331030. doi:10.3389/fphot.2024.1331030

Ministerio de Energía y Minería (2017). “Panorama de Mercado de Rocas y Minerales Industriales. Cuarzo,” in Año 1 N°1 Marzo 2017.

Ovaitt, S., Mirletz, H., Seetharaman, S., and Barnes, T. (2022). PV in the circular economy, a dynamic framework analyzing technology evolution and reliability impacts. Iscience 25 (1), 103488. doi:10.1016/j.isci.2021.103488

Pan, X., Li, S., Li, Y., Guo, P., Zhao, X., and Cai, Y. (2022). Resource, characteristic, purification and application of quartz: a review. Miner. Eng. 183, 107600. doi:10.1016/j.mineng.2022.107600

Philipps, S., and Warmuth, W. (2024). Photovoltaics report. Fraunhofer Institute for solar energy systems. ISE with Support of PSE. July 29; Freiburg, Germany. Available online at: https://www.ise.fraunhofer.de/content/dam/ise/de/documents/publications/studies/Photovoltaics-Report.pdf.

Ranjan, S., Balaji, S., Panella, R. A., and Ydstie, B. E. (2011). Silicon solar cell production. Comput. & Chem. Eng. 35 (8), 1439–1453. doi:10.1016/j.compchemeng.2011.04.017

Safarian, J., Tranell, G., and Tangstad, M. (2012). Processes for upgrading metallurgical grade silicon to solar grade silicon. Energy Procedia 20, 88–97. doi:10.1016/j.egypro.2012.03.011

Serrani, E. (2020). Latin America: Towards a multidisciplinary agenda to analyze energy transitions in Latin America, in Energy and Sustainable Development. Energy Transitions in Latin America . Editors E. Canafoglia. Buenos Aires, Argentina: CLACSO, 112–135. Available online at: https://www.clacso.org/boletin-2-energia-y-desarrollo-sustentable/.

Tamasi, M., Martínez Bogado, M., Bolzi, C., Díaz Salazar, M., Fernández Vázquez, J., Kondratiuk, N. Y., et al. (2021). Desarrollo de Sensores Fotovoltaicos de Radiación Solar para Aplicaciones Terrestres y Espaciales. RADI Rev. Argent. Ing. Año 9 N 17, 98–105. Available online at: https://ri.conicet.gov.ar/bitstream/handle/11336/182010/CONICET_Digital_Nro.8c67aa1f-2741-4d70-a745-2288902fab45_L.pdf?sequence=5&isAllowed=y.

U.S. Geological Survey (2023). Mineral commodity summaries 2023. Reston, VA, United States: U.S. Geological Survey, 210. doi:10.3133/mcs2023

Vatalis, K. I., Charalambides, G., and Benetis, N. P. (2015). Market of high purity quartz innovative applications. Procedia Econ. Finance 24, 734–742. doi:10.1016/S2212-5671(15)00688-7

Wang, J.-yi (2021). Global high purity quartz deposits: resources distribution and exploitation status. Acta Petrologica Mineralogica 40 (1), 131–141. Available online at: http://caod.oriprobe.com/issues/2021517/toc.htm.

Yuan, L., Farina, A., and Anctil, A. (2024). How will manufacturing capacity additions in China and North America affect the carbon footprint of silicon photovoltaics? Sustain. Prod. Consum. 49, 236–248. doi:10.1016/j.spc.2024.06.014

Keywords: CPV industry, silicon, technological development analysis, Argentina, solar energy, limitatation

Citation: Valdivia Alcántara C and Canafoglia E (2025) Technological opportunities for the PV industry in Argentina: satellite and terrestrial developments. Front. Energy Res. 13:1610359. doi: 10.3389/fenrg.2025.1610359

Received: 11 April 2025; Accepted: 04 August 2025;

Published: 01 September 2025.

Edited by:

Osvaldo Rodríguez-Hernández, National Autonomous University of Mexico, MexicoReviewed by:

Geydy Luz Gutiérrez Urueta, Autonomous University of San Luis Potosí, MexicoMonika Božiková, Slovak University of Agriculture in Nitra, Slovakia

Dani Rusirawan, Institut Teknologi Nasional, Indonesia

Copyright © 2025 Valdivia Alcántara and Canafoglia. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Carlos Valdivia Alcántara, Y3ZhbGRpdmlhQG1lbmRvemEtY29uaWNldC5nb2IuYXI=; Eliana Canafoglia, ZWNhbmFmb2dsaWFAbWVuZG96YS1jb25pY2V0LmdvYi5hcg==