Alex Badgett1†

Alex Badgett1† Mark F. Ruth1†*

Mark F. Ruth1†* Colby Smith1†

Colby Smith1† Martin Keller1

Martin Keller1 Julia Terrapon-Pfaff2†

Julia Terrapon-Pfaff2† Peter Viebahn2†*

Peter Viebahn2†* Thomas Pregger3†

Thomas Pregger3† Nathalie Monnerie4†

Nathalie Monnerie4†- 1National Renewable Energy Laboratory (NREL), Golden, CO, United States

- 2Wuppertal Institute for Climate, Environment and Energy, Research Division Future Energy and Industry Systems, Wuppertal, Germany

- 3German Aerospace Center (DLR), Institute of Networked Energy Systems, Stuttgart, Germany

- 4German Aerospace Center (DLR), Institute of Future Fuels, Cologne, Germany

Scientific literature and the energy policies of many countries indicate that hydrogen and its derivatives, such as ammonia and synthetic hydrocarbons, are likely to play an important role in future energy systems and economies. Global plans indicate that import-export energy markets will likely continue to be part of future energy systems, but there has been limited literature on the specific evolution of international energy trade with regards to magnitudes, potential energy carriers, and influence of social and economic factors. Here we review and discuss various aspects of hydrogen’s potential for becoming a globally tradeable energy commodity in the context of the Frontiers in Energy Research Topic: “Export and import of electrolytic hydrogen using renewable energy and subsequent synthetic fuels between regions–assessment of technology routes, potentials, and strategies”. Technical challenges are likely to impact that hydrogen potential including the form of energy being transported, primary energy and raw material availability and costs, hydrogen generation, derivative synthesis, and transport infrastructure. Timing of infrastructure development is a key consideration due to the potential economic impacts of unusable infrastructure if export, import, and transport capabilities become available at different times. Additionally, we identify and review social and market considerations including hydrogen certification, water availability and use, ecologic considerations, social acceptance, other human factors, investment risk, and market development. Based on those considerations, we propose factors that would benefit nations and investors to consider as they contemplate investments in hydrogen systems and set the stage for further research contributions to this Frontiers in Energy Research Topic.

1 Introduction and background on hydrogen technologies

Many nations around the world have objectives to limit carbon dioxide (CO2) emissions in the electricity, transport, and industrial sectors by 2050. Outlooks within the scientific literature and the energy policies of many countries anticipate that electrolytic hydrogen (H2) produced with renewable energy (RE) and its derivatives such as ammonia and synthetic hydrocarbons are likely to play a relevant role in future energy systems and economies (Pathak et al., 2023). Colloquially, this hydrogen produced using renewable electrolysis is commonly referred to as “green hydrogen”, hydrogen produced from fossil fuels with carbon capture and sequestration (CCS) is commonly referred to as “blue hydrogen”, and hydrogen produced from fossil fuels without CCS is commonly referred to as “gray hydrogen”.

Key considerations include how and at what costs the demand for electricity or thermal energy from RE, hydrogen, and its synthetic downstream products (synthetic fuels or raw materials) can be met. Given that electricity from RE comprises approximately 50% of the overall production costs of electrolytic hydrogen (Badgett et al., 2022), the availability of low-cost RE is a key factor. Low-cost RE resources often have limited availability in major industrialized nations, especially in Europe, Japan, and Korea, however, they are available elsewhere, such as in Australia, Brazil, China, Chile, the United States, the Middle East, North and South Africa, and parts of Northern Europe (European Commission, 2025; The Ministerial Council on Renewable Energy, Hydrogen and Related Issues, 2023; Federal Ministry for Economic Affairs and Climate Action, 2024; International Energy Agency, 2019). Yet, there are major uncertainties around how different demand and generation options can be realized in temporal and spatial synchronization, as quickly and resource-efficiently as possible, and under stable economic conditions. New trade relations through the export and import of different RE sources can play an important role. Initially, they can supplement today’s energy trade with the potential to replace it in the future. This trade is likely to be important both for achieving emission reduction targets in highly industrialized and densely populated countries and for helping to minimize the costs of meeting global energy demand. Yet, it is unclear what decision makers in importing or exporting countries should consider when identifying potential energy trade relations.

This paper provides an overview of the relevant aspects, requirements, and the current state of research for international hydrogen and synfuel trade. It shows the range of topics that require in-depth analysis and for which the collection of articles in “Export and import of electrolytic hydrogen using renewable energies and subsequent synthetic fuels between regions–assessment of technology routes, potentials and strategies” is seeking contributions.

2 Results

Section 2.1 provides an overview of factors impacting the energy trade: domestic resources, transport options, and global opportunities. This overview is followed by a summary of the current status of the relevant technologies and the opportunities for further research in Section 2.2, with a discussion of derivative product synthesis processes in Section 2.3, and a discussion of the timing challenges in Section 2.4. Section 2.5 contains other non-technical considerations because more extensive conditions for the origin of hydrogen are now being discussed than only the use of RE.

2.1 Factors impacting energy trade

Global energy markets are complex and interdependent, making them subject to impacts from a multitude of factors, ranging from technology advances to geopolitical shifts. The specific fuel carriers and technical options that are used today to transport and store energy are likely to change (Van de Graaf et al., 2020). This section provides an overview and discussion of the current global energy trade and qualitatively compares this business-as-usual system to potential hydrogen systems and energy trade. It outlines key elements for consideration in the near term and future, which are discussed in further detail in the following sections.

2.1.1 Domestic resources

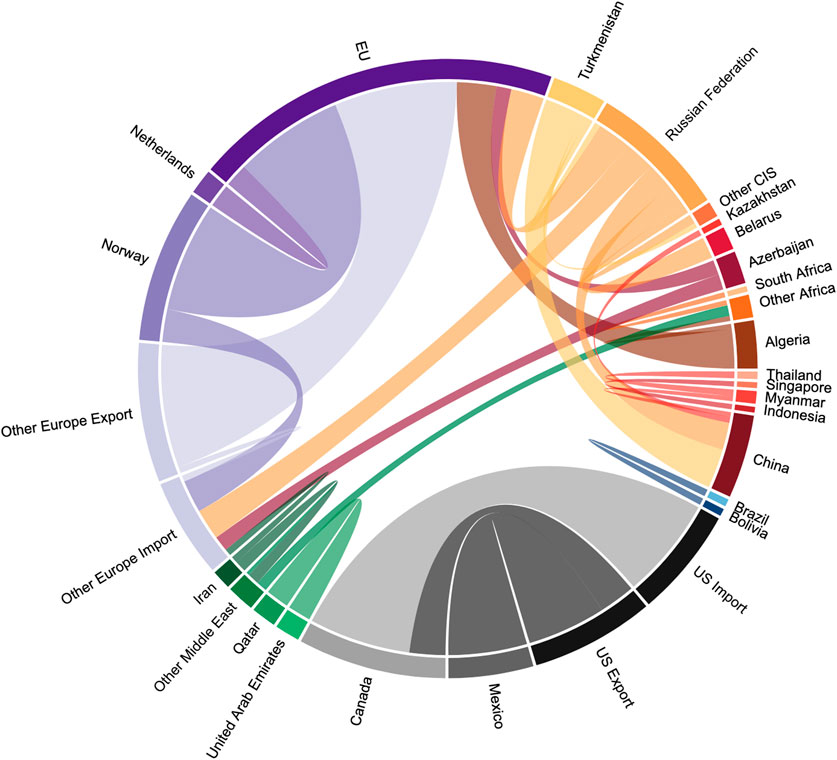

Domestic energy resource availability is one of the primary drivers of how energy is traded today. Countries that are rich with energy resources extract and secure these resources for domestic use and potentially export them to those that have less domestic supply. The export of energy products from countries with domestic production typically represents a significant industry for those that export; while importing and exporting countries both require investment in infrastructure to store, refine, and load the energy product. Figure 1 illustrates such exchanges with the example of natural gas (gaseous form). As shown, most trade between nations is constrained geographically by the availability of pipelines for moving the gas, illustrating the influence of infrastructure on how energy carriers are imported and exported.

Figure 1. Illustration of the current status of the global trade of piped natural gas (gaseous form) as an energy resource in 2023 (Source: Illustration by authors based on data from (Energy Institute, 2024) Energy Institute, 2024. Countries exporting/importing less than 2.5 billion cubic meters (bcm) were excluded for clarity). Chords are colored to correspond with the exporting entity. For example, black chords correspond to exports of liquefied natural gas (LNG) from the U.S. to various importing countries.

2.1.2 Transport options

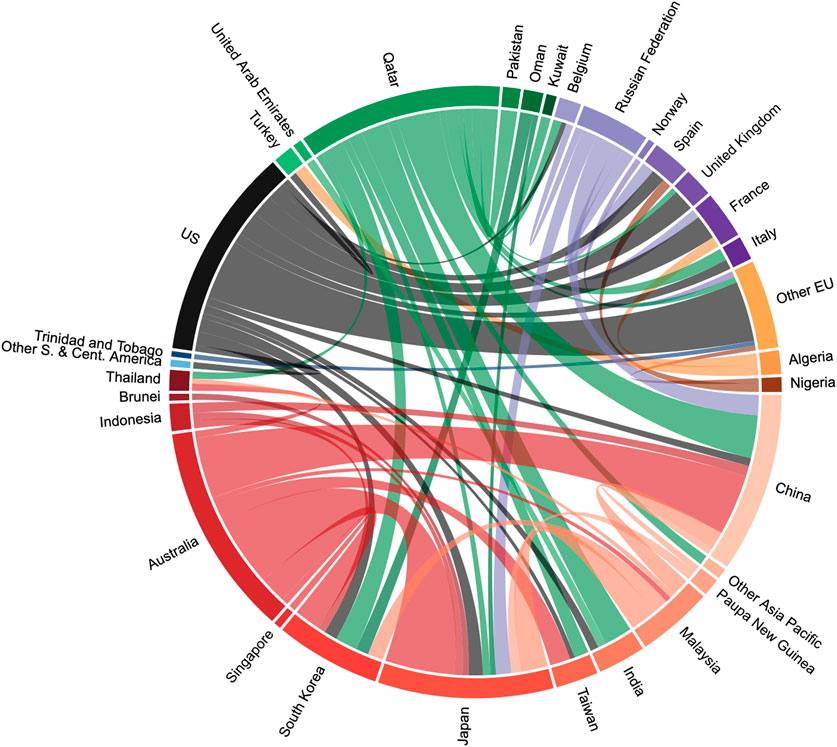

Nations move energy utilizing multiple types of energy carriers, including natural gas shown in Figures 1, 2. Natural gas, coal, and various crude oil-based products account for the bulk of the imported and exported energy products today with liquefied natural gas (LNG) nearly reaching 50B ft3/day of trade in 2023 (Energy Institute, 2024; U.S. Energy Information Administration (EIA), 2024). How energy is transported depends on the distance between the importer the exporter, the associated geography (i.e., land versus water), and the type of energy commodity being moved. The cost-optimal technology for transporting energy is highly situational, geographic, and varies with scale (DeSantis et al., 2021). Countries’ efforts to realize energy imports and exports over time have resulted in trillions of dollars invested in infrastructure to support these needs. Infrastructure deployments are not stagnant; they actively change based on emerging energy products and global market trends.

Figure 2. Illustration of the current status of the global trade of LNG as an energy resource in 2023 (Source: Illustration by authors based on data from (Energy Institute, 2024) Energy Institute, 2024. Countries importing/exporting less than 2.5 billion cubic meters (bcm) were excluded for clarity). Chords are colored to correspond with the exporting entity. For example, black chords correspond to exports of LNG from the U.S. to various importing countries.

The advent of horizontal drilling and hydraulic fracturing and the resulting shale gas boom in the United States in the early 2000s (U.S. Energy Information Administration (EIA), 2023) is an example of how drastically resource availability and cost can influence energy trade. The large increase in domestic natural gas production enabled by hydraulic fracturing and horizontal drilling technologies led the United States to become a net exporter, both north and south via pipelines and more broadly via LNG terminals at ports (Feijoo et al., 2018). This increase in supply impacts global energy prices, resilience both domestically and internationally, and growth in gross domestic product related to energy production, but there is also potentially a higher carbon footprint for LNG than for other fossil fuels such as coal due to energy use for liquefaction and transportation and methane leakage rates (Howarth, 1934; Gordon et al., 2023) as well as increasing environmental pollution and impacts on human health (Morett et al., 2024). Figure 2 illustrates the movement of LNG between major importers and exporters. Contrasted with Figure 1, which shows intracontinental trade largely via pipeline, Figure 2 demonstrates how the use of alternative energy (i.e., non-gaseous natural gas) carriers can influence energy trade flows through resource availability and other technical factors.

U.S. Energy Information Administration (EIA), (2024) For solid energy sources such as biomass and coal, transportation via shipping routes and rail are generally the most energy-efficient and play the largest roles for economic and geographic reasons, though trucks are also used for short distances. The situation is similar for liquid energy sources, such as crude oil and oil products, with pipelines as another possible transport route; however, maritime oil trade plays the largest role, accounting for more than 75% of the global supply (U.S. Energy Information Administration (EIA), 2024). Due to the lower volumetric energy density of gaseous products—in particular, natural gas—transportation in specially developed high-pressure pipelines (up to 200 bar) within a land mass and transportation in special ships for import and export across the ocean in the form of LNG play the biggest roles. According to (International Gas Union, 2024), the share of LNG transportation has continuously increased in recent years, and it has achieved a share of more than 50% of the global net exports of natural gas since 2022. In addition to existing gas distribution networks, rail and road transport are also used for further distribution to consumers.

2.1.3 Global trade opportunities

Quantifying the impact of energy systems on global energy trade, energy security, resilience, and the gross domestic product of each country is an exciting area of research in scenario-based analyses of possible developments. The optimal mix of technologies used to move energy is linked to many research questions, and many technologies are still under development, with the costs of production and delivery significantly varying from one carrier to another (Genge et al., 2023). The potential impact of research and development on global energy trade applies across the production, transportation, storage, and utilization stages of the life cycle.

In some prospective global energy systems analyses, renewable energy is projected to be the predominant primary energy source in the future and electricity infrastructure expansion is a high priority (IEA, 2024; Gielen et al., 2019; Teske et al., 2021). Accordingly, there is established literature on the long-distance transportation of electricity between countries and regions of the world (Trieb et al., 2012; Cooper and Sovacool, 2013). The trade in bioenergy across national borders is also described in the literature (Kaditi, 2009; Daioglou et al., 2020), but even if there is great potential for expansion, there are obstacles, mainly due to the limited energy density of biogenic raw materials, the possible environmental and social effects, and the fundamental limitations of sustainably produced biomass. In renewable energy scenarios, hydrogen and the synthetic fuels based on it could represent significant chemical energy sources, particularly in hard-to-abate emissions sectors. The dynamics of supply and demand developments, the speed of the expansion of new infrastructure along the value chains, regulatory frameworks, and geopolitical aspects will affect the development of these new regional and global markets. Several relevant considerations are described in the following sections.

2.2 Technical considerations for hydrogen energy trade

2.2.1 Hydrogen-based fuel production technologies

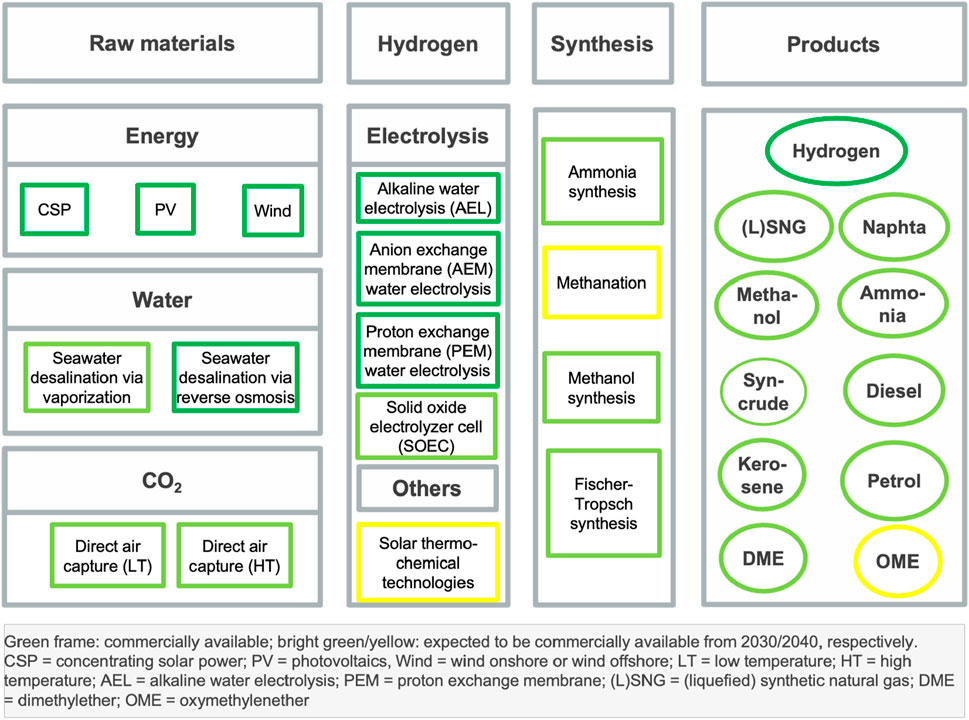

Several very different technologies can be used to produce hydrogen and its derivatives. The farther along the value chain toward the derivatives, the lower the technology readiness level (TRL) level, the greater the need for research, and the later the time of commercial availability (Figure 3). The combination of the technologies, accounting for dependencies and interactions, enables the investigation of possible layouts and operating modes of the systems in individual production routes and results in the efficiencies and costs of the value chains.

Figure 3. The main renewable energy-based technology groups in the hydrogen and hydrogen derivatives process chain and their (expected) times of commercial availability (Source: Illustration by authors based on data from (Viebahn et al., 2022)).

2.2.2 Primary energy and raw material resources

2.2.2.1 Renewable energies

A significant expansion of renewable electricity and heat generation is the basis for the development of large-scale renewable hydrogen production and trading. Common RE—such as solar photovoltaics (PV), wind energy, and concentrating solar power (CSP)—are commercially available and installed at a large scale globally. A recent review from Angliviel de La Beaumelle et al. (2023) reported that the global technical potential of (utility-scale) PV, CSP, onshore wind, and offshore wind is greater than 100 PWh/year of electricity each. Each technology alone would be able to cover the projected global electricity demand of 43.7–62.2 PWh in 2050.

The costs of RE have historically seen reductions, making it difficult to present current figures. For example, the Intergovernmental Panel on Climate Change reported the realized levelized cost of electricity per kWh from 3.8 US-ct2020 for solar PV, from 15 US-ct2020 for CSP, from 7.3 US-ct2020 for offshore wind, and a range from 3.4 to 7.6 US-ct2020 for onshore wind in 2020 (Pathak et al., 2023). These figures are confirmed by the results of the renewable energies’ potential analysis in the MENA-Fuels project (Viebahn et al., 2022), in which the most favorable technical levelized cost of energy (LCOE) per kWh of a country across all countries worldwide ranges from EUR-ct 1.8 to 4.1 (US-ct2020 1.7–3.8) for solar PV, EUR-ct 8.7 to 16.2 for CSP (US-ct2020 8.1–15.1), EUR-ct 3.2 to 14.5 for offshore wind (US-ct2020 2.9–13.5), and EUR-ct 1.7 to 8.4 for onshore wind (US-ct2020 1.6–7.8).

However, in estimating the realistic global market potential, it is essential to account for social, political, and environmental constraints alongside technical and economic considerations (see Section 2.4). While cross-country cost estimates and broad evaluations of resource availability offer valuable initial insights, they do not necessarily translate into bankable projects or tangible market potential. Such projections often mask significant uncertainties, including variability in cost assumptions, the performance and scalability of electrolyzer technologies, and the reliability of long-term policy and regulatory frameworks. These constraints are typically defined at the national or regional level, reflecting context-specific conditions that can substantially influence project feasibility. This underscores the considerable uncertainty and complexity inherent in translating theoretical potentials into forecasts of global trade flows, highlighting the need for more nuanced, context-sensitive analyses. A robust understanding of global trade dynamics requires the integration of these multifaceted uncertainties into both modeling frameworks and policy evaluations. Further needs for research are identified as general technological improvements and further cost reductions; the large-scale integration of renewable resources and their associated requirements, such as long-distance transmission, the scarcity of critical materials, the need for both flexible generation and storage, market design, incentives and supporting regulations, and social awareness and acceptance; and the impacts of changing weather patterns on RE resources, their resilience, and their sustainable design (Angliviel De La Beaumelle et al., 2023; Ang et al., 2022; Osman et al., 2023; Russo et al., 2022).

2.2.2.2 Seawater desalination

Seawater desalination is the process of turning seawater into fresh potable water or high-purity water for industrial purposes. Presently, common desalination technologies are reverse osmosis (RO), multistage flash desalination (MSF), and multi-effect desalination (MED), accounting for 68.7%, 17.6%, and 6.9% of installed capacity, respectively (Curto et al., 2021). RO uses mechanical work to create a pressure difference to drive seawater through a semipermeable membrane that allows only freshwater to pass through. MSF and MED are thermal technologies that both boil the saline water to separate it into water vapor and brine (Curto et al., 2021).

These common technologies can be classified as TRL 9; they are commercially available and installed worldwide. The challenges involved in linking RO to RE are assessed as lower; the pilot and demonstration phases still need to be completed for the delivery of regenerative low-pressure steam for the vaporization process. MSF and MED are predominantly (if not exclusively) coupled to fossil fuel-based power plants (Ettouney et al., 2009).

Interest in the use of solar energy for thermal desalination processes has increased in recent years. Several concepts have been proposed and investigated (Ghaffour et al., 2015). Despite extensive efforts to develop new materials and configurations for solar thermal desalination technologies, there are gaps in the knowledge on how these innovations can contribute to the overall improvement of the performance and economic feasibility of (fully) renewable desalination plants (Wang et al., 2019). Research and development in this technology area (see (Wang et al., 2019; Jones et al., 2019; Ullah and Rasul, 2019)) suggest that the first medium-sized solar thermal desalination concepts can be used in commercial operation within the next 5–10 years, while small-sized concepts already achieved a TRL of 8.

In addition to the challenges associated with the use of RE, further challenges are the general water requirement for electrolysis, the associated energy costs, and the resulting brine (see Sections 2.5.2 and 2.5.3).

2.2.2.3 Carbon capture

To produce carbon-based derivatives such as fuels and chemicals, the carbon might come from biomass, from chemical recycling of fossil-based plastics, be captured from fossil industries, or be extracted from the air. Since this work focuses on RE resources, biomass or direct air capture (DAC) would be the options of choice. Because biomass is not sufficiently available in many regions and can be expensive to transport (U.S. Department of Energy, 2024b), only DAC is considered here. DAC technologies are currently not ready for the market at a large scale and could therefore prove to be a bottleneck for the production of derivatives. Although numerous companies and startups are working on DAC on the laboratory and pilot scales and are researching various new DAC approaches, so far, the technology has only been successfully implemented in a few plants worldwide and reached a TRL of 6 (Intern ational Energy Agency, 2022; Ozkan et al., 2022). The most advanced technologies can be divided into two approaches: a “low-temperature” adsorption process and a “high-temperature” absorption process (Ozkan et al., 2022).

The adsorption process requires a heat level of approximately 100 °C and is based on a design that enables small-scale container-based solutions. Adsorption and desorption take place cyclically in a state of a vacuum in the same chamber that exposes the technical components to strong fluctuations in temperature, pressure, and humidity. There are currently 17 adsorption plants in operation (Intern ational Energy Agency, 2022), and some of them can produce water as a byproduct. The absorption process runs at a heat level of 900 °C. The separation of absorption and desorption enables continuous operation at ambient pressure, less stress on the components due to temperature and pressure fluctuations, and better protection of the system components. In contrast to the low-temperature approach, this process requires water. Because both large plant components, such as calciners and steam quenchers, and high temperatures are required, significantly larger units are needed than for the adsorption process. The only pilot plant currently operating uses natural gas with a downstream carbon capture and storage process to generate the required high temperature (Keith et al., 2018).

Ozkan et al. (2022) identified the contactor, the sorbent, and the regeneration of the solvent as key research fields for improving performance and cost. Young et al. (2023) assume that the costs of both high-temperature and low-temperature DAC could reach USD 100 to 600 per ton of CO2 by 2050 in the best-case scenario; however, their analysis shows that this is only likely to be the case with a massive rollout, which is why market and incentive programs are relevant to quickly reduce costs in addition to supporting technical improvements. This also aligns with Hanna et al. (2021), who state that the growth rate of the DAC industry is the most critical parameter and that rapid learning through economies of scale and volume would be particularly important to reduce costs.

2.2.3 Hydrogen production technologies

2.2.3.1 Water electrolysis

Water electrolysis is a key technology for production of hydrogen by splitting water using electricity. There are four main types of water electrolysis: alkaline water electrolysis (AEL) with a TRL of 9; anion exchange membrane (AEM) water electrolysis (TRL 6); proton exchange membrane (PEM) water electrolysis (TRL 9); and solid oxide electrolyzer cells (SOEC), also called high-temperature electrolysis (HTE) with a TRL of 7–8 (Sebbahi et al., 2024).

In AEL, the electrolyte is usually potassium hydroxide solution, and hydroxide ions (OH-) move through a diaphragm from the cathode to the anode. The operating temperature range is 40 °C–90 °C, and the typical current density is 0.2–0.6 A/cm2. This is an established technology that has been used at the industrial scale for around 100 years (Roeb et al., 2020). Although AEL is a well-established technology, it is still mainly used where electricity is available at a low cost or where relatively small quantities of high-purity hydrogen are required. Only approximately 5% of the hydrogen consumed annually is produced by AEL (Adolf et al., 2017). When coupled with fluctuating power sources, alkaline electrolysis has some disadvantages. In partial load operation, the achievable gas purity decreases, and degradation problems occur. In addition, alkaline electrolysis requires a relatively long cold start time, approximately 50 min (Smolinka, 2021). Research into better electrode materials that are cost-effective and stable over the long term in intermittent operation is further needed. Even this established technology has potential for optimization: An efficiency of around 70%–80% is expected (IEA, 2019).

AEM water electrolysis is similar to AEL water electrolysis, but the traditional diaphragms are substituted with an AEM (Miller et al., 2020). The benefit of AEM water electrolysis is the use of cost-effective transition metal catalysts instead of noble metal catalysts, as in PEM.

The functional principle of PEM water electrolysis is based on the proton-conducting polymer membrane. Protons are transported through the membrane from the anode to the cathode, where they combine to form hydrogen molecules. The operating temperature can be up to 100 °C, and typical current densities of 1.0–2.5 A/cm2 are higher than with AEL (Dikschas and Smolinka, 2019). PEM electrolyzer technologies have been commercially available at the industrial scale for several years. Due to the less complex peripherals, PEM electrolysis can operate dynamically and might be more suitable for coupling with fluctuating power sources than AEL. A cold start takes only approximately 15 min (Smolinka, 2021). Other advantages are the dynamic behavior and product gas purity in partial load operation; however, the need for the corrosion-resistant rare-metal iridium, which is required for the anode side electrode increases costs (Alex et al., 2024). Research for new electrode materials that are cheaper than iridium (Roeb et al., 2020) and development of systems and components that minimize costs and degradation while maximizing performance is an active area of research (Badgett, 2021).

In SOEC, the water vapor is supplied to the cathode and is split into hydrogen and oxygen ions by the applied voltage. The operating range is 700 °C–1000 °C, and the typical current density is 1.0 A/cm2 (Dikschas and Smolinka, 2019). The major advantage of SOEC is the lower electricity requirement for water splitting compared to low-temperature electrolysis, where water vapor is electrochemically split instead of using liquid water. The fact that no heat of vaporization is required reduces the necessary cell voltage. As the temperature rises, a greater proportion of the energy required for water splitting can also be introduced as thermal energy, while the power requirement and therefore the required cell voltage fall. There is still a great development potential, and efficiencies up to 90% can be achieved at high operating temperatures (Roeb et al., 2020). In addition to the high electrical efficiency, other advantages are the possibility of fuel cell operation in reverse mode and of co-electrolysis to produce synthesis gas for green fuel generation directly from water vapor and CO2. This technology is still in development, and so far, it has been used in pilot plants.

Between the different types of water electrolysis, low-temperature electrolysis has an advantage in the short term. For this reason, current and planned larger projects for producing green hydrogen are likely to be based primarily on AEL, as this technology is well advanced, and PEM electrolysis which is well suited to coupling with RE sources. HTE still needs sharp cost decreases to see a rapid technology ramp-up, but from a long-term perspective, it has long-term commercial potential due to its high efficiency and the low need for critical raw materials.

2.2.3.2 Solar thermochemical processes

Solar thermochemical pathways that use high-temperature heat provided by concentrating solar thermal energy are very promising processes to produce hydrogen, synthesis gas, and so-called “solar fuels.’ They show high efficiencies and low production costs by water splitting, as they mostly need thermal energy, which is readily available in the form of concentrated sunlight (Pregger et al., 2009). The TRL for solar thermochemical technologies is 3–7, depending on the technology. The pathways comprise solar thermochemical cycles, solar reforming, and solar gasification. Two routes to water splitting by thermochemical cycles have been identified to be very promising in terms of efficiency: The first is metal oxide redox, and the other is sulfur cycle processes. In the first, a metal oxide is heated to a high temperature (1,400 °C–1,500 °C) by solar high-temperature heat. At this temperature level, the metal oxide is reduced and releases oxygen. The reduced metal oxide is then able to split water or CO2 molecules at a lower temperature level (around 900 °C) by absorbing their oxygen atoms. This means that the process can be used to produce not only hydrogen but also synthesis gas directly (Agrafiotis et al., 2021).

Cerium oxide is currently regarded as the most promising metal oxide for technical realization. The first thermochemical cycle pilot facilities are in operation, and concepts for scaling the technology up are now being researched. Accordingly, in the Plataforma Solar de Almeria (Spain), a thermochemical receiver reactor for water splitting with a thermal output of 750 kW was successfully tested (Säck et al., 2016). Moreover, as part of the Sun-to-Liquid European project, a 50-kW test reactor was also successfully tested and run in Spain to convert CO2 and water into solar synthesis gas, which was then used in a Fischer-Tropsch reactor to create synthetic paraffin.

The sulfur cycle processes also represent a promising way of economically producing hydrogen on a large scale. The large-scale implementation of these processes requires further research efforts. Of central importance is the development of efficient and durable reactors for sulfuric acid splitting with concentrating solar thermal energy.

Regarding the core components required for the solarization of such thermochemical processes, adjustments are still necessary to achieve further increases in efficiency. The wide range of possible redox materials and process concepts suggest that further increases in efficiency and an associated reduction in costs are also possible in the future (Roeb et al., 2020). Research is also being carried out on concepts for heat recovery, which plays an important role in the overall process efficiency, and in the continuous operation on new redox materials.

Although there are still some research needs depending on the processes, some technologies to produce solar fuels are already available for large scaling, as demonstrated by the new DAWN plant from Synhelion in Jülich, Germany, which plans to produce several thousand liters of solar fuel per year (Synhelion, 2024). Once thermochemical cycles reach market maturity, these technologies could also reduce future demand for multistage processes to produce synthesis gas via reverse water gas shift, which, at present, is also still far from reaching market maturity.

2.3 Derivative product synthesis processes

Large-scale reactors are generally used for conventional syntheses, with capacities usually ranging from 3,000 to 10,000 tons of product per day (1,095–3,650 kt per year) (Niklaß, 2016), and they often have lifetimes exceeding 50 years and therefore entail correspondingly strong lock-in effects (Zelt et al., 2020). Hydrogen-based syntheses are, at least so far, only available in much smaller units (Zelt et al., 2020). “There is a need for research—regardless of the renewable synthesis gas origin—with regard to validation in an industrial environment (e.g., in terms of performance levels, service life, operational flexibility)” (Niklaß, 2016). Further, in many cases, the challenge is integrating the overall process on the basis of RE (Zelt et al., 2020).

2.3.1 Ammonia synthesis

In discussions on the design of energy systems entirely based on RE sources, ammonia is considered to have relevant potential, both as a fuel in the maritime sector and as a chemical storage for hydrogen, particularly for long-range transport (Zelt et al., 2020). Today, ammonia is produced almost exclusively in large-scale plants (up to 3,300 tons per day) using the Haber-Bosch process and natural gas as feedstock. Ammonia synthesis based on renewable electricity would mean that both the hydrogen (via electrolysis) and the nitrogen (via air separation) are produced separately. Additional energy is required to bring the mixture to the pressure (150–350 bar) and temperature conditions (350 °C–550 °C) required for synthesis. The individual technologies that can be used in such a process are available in principle, but the integration of the overall process has not yet reached the commercial stage (Bazzanella and Ausfelder, 2017). Zelt et al. (2020) assume that the large-scale commercial application of ammonia synthesis plants based entirely on renewable energies will be possible from 2030 onward.

The International Renewable Energy Agency (IRENA) and the ammonia Energy Association (AEA) (IRENA, 2022) estimate that the annual production capacity for green ammonia could reach 566 million tons by 2050. The 71 million tons of projects announced so far therefore correspond to slightly more than 10% of the production capacity required in the long term; however, only a few of them are under construction. According to IRENA and AEA (IRENA, 2022), production costs can be reduced by lowering the hydrogen cost, upscaling to the gigawatt size, creating high demand for electrolyzers, and generally promoting technical innovations that integrate mature technologies into new applications. If additional market incentives were created, such as contracts for difference (CFD), the production of green ammonia could be largely competitive from 2030 onward.

2.3.2 Methanation

Methanation refers to the conversion of hydrogen and carbon oxides into (synthetic) methane. Fossil-based methanation plants using the fixed-bed reactor concept are already being used commercially and on a large scale (Ding et al., 2013; Wang, 2017). Concepts for methane synthesis based purely on RE are still under development, only individual concepts already achieve a TRL of 8 (Zelt et al., 2020). Most concepts are based on the use of catalysts (Sabatier process), and they can be divided into three categories: fixed-bed, fluidized-bed, and three-phase reactors. A second, smaller group refers to biocatalytic processes, carried out by microorganisms.

Bailera et al. (2017) show that only a few fixed-bed reactor projects are almost ready for the market or are in demonstration. During a meta-analysis, Barbaresi et al. (2022) found 87 research projects, most of which are based on an electrolysis capacity of less than 1 MW. According to them, plant design, carbon capture and use, and heat management are at the forefront of research activities, followed by energy systems integration, material research, technical and economic feasibility, and the optimization of the operating condition. In view of the low capacities and the usual duration for the upscaling of plants, large-scale implementation is only assumed from 2040 onward.

2.3.3 Methanol synthesis

Large-scale methanol plants with an annual production capacity greater than 1,000 kt are operated worldwide based on the fossil fuel technologies coal-to-liquid (mainly in China) or gas-to-liquid (mainly in the Middle East) (Zelt et al., 2020). The most important chemical derivatives of methanol include formaldehyde, olefins, methylamines, and methyl acrylate. The use of CO2 as a feedstock represents the main innovation compared to the classic fossil fuel-based process (Álvarez et al., 2017). To obtain conventional CO/H2 synthesis gas, CO2 must first be reduced to CO by hydrogen in a reverse water gas shift reactor; however, a direct methanol synthesis pathway from CO2 is also being developed (Bazzanella and Ausfelder, 2017). Under suitable reaction conditions, the mixture of H2 and CO can be fed into the reactor at temperatures ranging from 300 °C to 400 °C.

The TRLs of conventional methanol syntheses are 7–9 (Niklaß, 2016; Bazzanella and Ausfelder, 2017; Álvarez et al., 2017) and plants are commercially available in various sizes. The need for further development includes efficiency increases, electrification to achieve greenhouse gas (GHG) neutrality, the capture of exhaust gases, and flexibilization (Niklaß, 2016). The CO2-based methanol route using low-temperature electrolysis is currently technologically advanced in terms of component development; however, work still needs to be done on the closed implementation of the entire route from renewable electricity generation to the further processing of methanol, for example, into kerosene or dimethyl ether. Further development of the routes using high-temperature or co-electrolysis appear promising in terms of overall energy efficiency, but they are still at an early stage (Niklaß, 2016). It is expected that large-scale commercial availability will be achieved by 2030 (Zelt et al., 2020).

2.3.4 Fischer-Tropsch synthesis

Fischer-Tropsch (FT) synthesis is a process for CO polymerization and hydrogenation, i.e., long-chain hydrocarbons are produced from a synthesis gas (carbon monoxide and hydrogen). The broad spectrum of oxygen-containing compounds includes alcohols and aliphatic hydrocarbons with carbon numbers from C1–C3 (gases) to C35+ (solid waxes). For synthetic fuels, the desired products are olefinic hydrocarbons in the C5–C10 range. As FT synthesis takes place at temperatures between 200 °C and 340 °C, the waste heat can be used for other processes relevant to the overall pathway, such as for high-temperature electrolysis to provide hydrogen and, in the case of heat flows at lower temperatures, for process steps in CO2 separation (low-temperature DAC). This heat can also be used for the further processing steps of the synthesis products, such as distillation to obtain kerosene from the FT synthesis product (Niklaß, 2016).

In contrast to methanol or ethanol, which are blended with petrol or can be used 100% after engine conversion, the FT fuels are drop-in fuels, which have almost the same chemical composition as fossil fuels and could completely replace them without engine conversion; however, there is still a need for the development of FT technology because there are still no fully developed catalysts for CO2-based synthesis. In addition, the coprocessing of kerosene and the logistics of decentralized production are seen as further challenges that still need to be solved (Zelt et al., 2020).

Fossil-fueled FT reactors have been in use since the 1950s (particularly in China and South Africa for the production of coal-based fuels), and various reactor designs exist. Bazzanella and Ausfelder (Bazzanella and Ausfelder, 2017) (2017) report TRLs of 5–7 for an integrated FT synthesis plant including electrolyzers. Some components have already been developed to a very large extent, but there is still no commercial plant of industrial size; however, various demonstration projects are underway, so it seems plausible that commercial plants of industrial size could be available by 2030 if intensive development work is carried out (Zelt et al., 2020).

2.3.5 Transport infrastructures

Hydrogen can be transported in liquid, gaseous, or in derivative form via pipelines, rail and road tankers, or ships. The development of suitable port infrastructure is crucial for long-range transportation via ships. According to the literature review of Chen et al. (2023), the technological requirements for large-scale hydrogen transportation via ports are mostly neglected in the current literature on hydrogen supply chains. Their analysis focuses on the readiness of ports for possible international hydrogen trade and identifies 20 potentially promising ports for the ramp-up of hydrogen exports and imports. Important aspects are infrastructure, risk management, public acceptance, regulations and standards, as well as education and training. According to their findings, liquid hydrogen (LH2), ammonia, methanol, and liquid organic hydrogen carriers are suitable forms for international hydrogen trade. Compressed gaseous hydrogen was not considered due to its low transport efficiency and the lack of technological maturity of the ship concepts developed to date. Depending on the supply route, compression and liquefaction plants, gas ammonia, methanol and LH2 tanks, hydrogenation and dehydrogenation facilities, berths, regasification units, and pipelines and truck loading skids should be considered as infrastructure components. The identified research gaps include key technologies for the development of large-scale port LH2 facilities, port risk management, information and knowledge-sharing to promote public acceptance, education and training, as well as harmonized international regulations and standards for port hydrogen handling. The type of carrier used will impact the number of ports available to export to or import from. Countries would benefit by considering the availability of not only hydrogen but also the ability to process the hydrogen carrier.

Wei et al. (2023) recently provided a review of material compatibility, storage, and bunkering technology for maritime shipping to explore the major changes that are required for ports and long-distance large cargo ships to store, feed, and use alternative fuels. They point to several challenges, such as the lower energy density of fuels; a possible need for liquefaction and/or pressurization to reduce storage requirements and facilitate the loading of fuels; and the need for different materials, such as stainless and mild steel and double-walled techniques for storage and loading. In addition, increased safety precautions might be required if the fuels are highly toxic and to prevent water contamination, particularly in the case of biofuels, ammonia, and methanol. The latter two fuels require additional ventilation equipment inside the vessels.

As an example of a much more in-depth analysis of infrastructure needs in ports, Kim et al. (2024) presented a design for a large-scale transportable liquid hydrogen export terminal and investigated its technical feasibility. The terminal should have a daily capacity of 120 tons, a storage capacity of 75,000 m3, and include on-site hydrogen production based on RE sources; thus, the terminal consists of the components of hydrogen production, liquefaction, storage, handling, and transfer. The study deals with the technical feasibility of the individual systems and describes the technical challenges and possible solutions based on the current state of the art. It also outlines the need for further development, such as scaling up single-stack electrolysis systems, liquefaction processes, and LH2 storage systems with vacuum insulation.

2.4 Production, use, and infrastructure timing

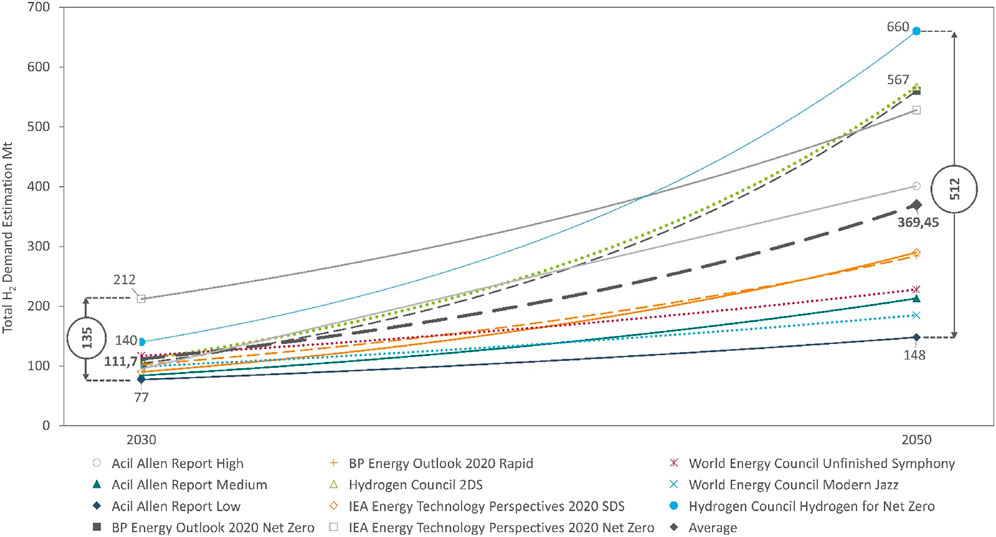

Global hydrogen demand growth projections range from 6% to more than 10% annually to meet projected 2050 demands of 150–700 Mt (Megatonnes) per year (Wappler et al., 2022), as shown in Figure 4. The primary causes of the differences between the scenarios are assumptions regarding the development of end-use applications with the conversion of current hydrogen applications (e.g., refining, ammonia production) potentially occurring sooner and new applications (vehicle fuel, synfuels, energy storage) driving later growth. In addition, it is possible that the current production technologies used to meet 100-Mt per-year current demand will diversify; thus, both market and technological evolution are likely to impact international trade, especially when and how it develops.

Figure 4. Comparison of global hydrogen demand evolution across multiple studies showing growth rates of 6%–10% annually. Note that some studies rely on net-zero constraints which drive increased hydrogen usage. Figure source: Wappler et al. (2022). Y-axis units are expressed in megatonnes, (million metric tonnes) of hydrogen demand.

If rapid growth in hydrogen production and resulting implications for import and export markets materialize, international energy trade in 2050 is likely to be different from both today’s trade (as discussed in Section 2.1) and from intermediate years. The Hydrogen Council published estimates of expected major hydrogen flows in 2030 and 2050 (Figure 5). They estimate that early trade routes are likely to be established by 2030 and will increase to more than 40 different routes by 2050. They foresee the use of proximate hydrogen supplies (e.g., Norway-Europe) and direct routes (e.g., United States-South Korea and Australia-Japan) being developed in the earlier time frame with a preference for end products (ammonia and methanol). They expect the initial shipping routes to grow following 2030 and the development of additional hydrogen production in the Middle East and northern Africa (MENA) to supply additional Asian markets, ultimately resulting in “significant [market] liquidity” (Hydrogen Council and McKinsey & Company, 2024).

Figure 5. Global hydrogen trade flow scenario for 2050, showing import and export flows, net importers and exporters, and possible transportation infrastructure. Implementation of policy and investment in infrastructure are likely to impact import and export of hydrogen between countries. (figure reproduced with permission from source: Hydrogen Council) see Hydrogen Council and McKinsey and Company, 2024. (Hydrogen Council and McKinsey& Company, 2024).

Considering only the ammonia demand caused by its potential use in global shipping, Verschuur et al. (2024) used a spatial modeling framework to quantify the cost-optimal fuel supply for shipping in 2050 using green ammonia. According to their results, only a few large supply clusters might serve regional demand centers, based on several production sites located in the sunbelt, i.e., sites within 40 latitudes north and south; however, this, in turn, means that these countries would account for a large proportion of the required infrastructure, including many low- and middle-income countries, such as Morocco and Mauritania.

Balancing the ultimate hydrogen production locations, application locations, and the necessary transport infrastructure and markets is not the only challenge that needs to be addressed. Mismatched development of production, applications, and international transport would be far from optimal and could lead to market failures that could slow the development of a hydrogen economy. Unbalanced hydrogen supply and demands could lead to market inefficiencies that would negatively impact the financial position of hydrogen producers and/or applications. Demand applications that cannot access expected hydrogen supplies have higher costs to obtain access to alternative supplies; use suppliers that are missing the desired reductions in carbon intensity; and/or not produce their products, thus leaving capital unused. Hydrogen producers who build assuming they will have customers will also have unused capital assets if those customers do not materialize as expected. Thus, it is likely to be challenging for markets to balance the uncertainty of performance of new hydrogen applications and the certainty of hydrogen production.

Likewise, hydrogen has multiple forms in which it can be transported (gaseous, liquid, ammonia, methanol, and in other carriers) (Hossain Bhuiyan and Siddique, 2025). Both export and import ports are likely to limit the forms of hydrogen that they can manage to control investments in capital that are likely to have limited use. As a result, hydrogen might not be as fungible as expected because each import port is likely to have a limited number of sources that they can import hydrogen from. That additional constraint has the potential to limit when and where both hydrogen producers and applications are built. For example, many nations are likely to have the desire to import ammonia for use as a fertilizer in the near term; however, they will likely need additional infrastructure and different suppliers if and when they desire to import hydrogen for iron reduction, as fuel for maritime transport, or for other applications because there might be more economic options than cracking ammonia and purifying the resulting hydrogen.

An additional constraint is the time necessary to build and start up new infrastructure. Large capital projects such as ports tend to have delays. As a result, matching the timing of hydrogen production, the export ports, the import ports, and hydrogen demand is likely to be challenging. Finally, ecologic and community considerations are likely to evolve, resulting in incongruities between demands and supplies that can meet those requirements. Considering temporal changes in those requirements would benefit both the hydrogen users and the suppliers.

One option for managing those challenges is offtake agreements where the producers, shipping companies, and applications agree to common expectations with financial penalties for not meeting them.

2.5 Other considerations

2.5.1 Environmental certification

The certification of imported renewable hydrogen and its derivatives plays a role in potential import export agreements (IRENA and RMI, 2023). In two delegated acts of the European revised Renewable Energy Directive (RED II) (European Union, 2023), criteria were specifically defined for the renewable share of the electricity used (at least 90% for grid supply), the GHG reduction through e-fuels (70% compared to the replaced fossil fuels), and the origin of carbon for synthetic hydrocarbons (e.g., no emissions from fossil fuel power generation after 2035). These requirements also apply to imports and can be met by means of certification from an EU-recognized certification body. In the United States, the 45V hydrogen production tax credit creates an incentive for clean hydrogen up to $3/kg H2. 45V provides a tiered incentive amount depending on the carbon intensity of hydrogen up to the point of production and depending on whether the project meets “prevailing wage and apprenticeship requirements” (U.S. Department of Energy, 2025).

Renewable energy-based hydrogen and its derivatives are the basis for roadmaps focusing on net-zero economies by 2045/2050 (The Ministerial Council on Renewable Energy, Hydrogen and Related Issues, 2023; Federal Ministry for Economic Affairs and Climate Action, 2024; International Energy Agency, 2019; DCCEEW, 2024; Fuel Cells and Hydrogen 2 Joint Undertaking, 2016; Sakib et al., 2024). This requires standardization of the determination and reporting of the carbon footprint; however, the establishment of a global certification system will not be easy to implement. IRENA has conducted a review of global certification systems and the regulation of trade in hydrogen and its derivatives and identified gaps that hinder the development of cross-border certification (IRENA and RMI, 2023; IRENA, 2024). The authors point out important policy tasks, in particular the harmonization of standards and evaluation criteria, the development of transparent and cost-effective systems for tracking certificates, and the initiation of appropriate diplomacy on hydrogen trade rules and public-private dialogues between stakeholders in import and export regions. The experience of European certification could also represent a starting point. So far, the certification criteria only relate to the reduction in carbon emissions associated with green hydrogen production. If hydrogen is to be not only green but also sustainable in a holistic sense, other resource, economic, social, and societal dimensions should also be considered. In a meta-analysis, Krieger et al. (2024) mapped hydrogen certification dimensions that were found in 19 publications on hydrogen production, in particular referring to the Global South. They grouped them into environmental impact, broader socioeconomic impact, responsible project development, governance at the system and country level, and human rights. Although water availability and its ecologic impacts (Sections 2.5.2 and 2.5.3) are to be regarded as core aspects of hydrogen production, further aspects, described next (Sections 2.5.4-2.5.7), might also need to be considered.

2.5.2 Water availability and consumption

A growing dialogue about water security is developing in parallel to deploying hydrogen technologies. Different hydrogen production technologies consume and withdraw different amounts of water per kilogram of hydrogen generated; the consumption is the total amount of water converted to H2+1/2O2, and the withdrawal is the total amount of water taken from the reservoir to operate the plant, for instance, for cooling. Water that is not consumed after being withdrawn can be put back into the environment, provided it is free from pollutants. Water electrolysis technologies are produced via renewable electrons that consume/withdraw, for example, 17.5/25.7 L/kg and 22.3/32.2 L/kg for PEM and liquid alkaline water electrolysis technologies, respectively, compared to blue hydrogen (natural gas + steam methane reforming + carbon capture and storage) at 25/33 L/kg or (coal + gasification + carbon capture, utilization, and storage) at 50/80 L/kg, grey hydrogen (natural gas + steam methane reforming) at 17.5/20 L/kg, and black hydrogen (coal + gasification) at 31/49.8 L/kg (IRENA and Bluerisk, 2023).

With many countries developing hydrogen roadmaps, examining the amount of water required for the estimated hydrogen production is too broad of an approach to understand water stress. When discussing water concerns for the production of hydrogen, it is important to consider the local impacts of a proposed plant because water scarcity is local (Kummu et al., 2016). Depending on the location of the project, the water stress and scarcity impacts substantially change, and there might be a larger concern about any additional withdraws from a body of water. It is not sufficient to say that countries have no water scarcity concerns if the total water consumption of the proposed hydrogen economy is not a significant portion of the total water availability. Local water and environmental concerns should be considered for hydrogen to be successful in the public view as well as the sustainable one. If projects do not consider these impacts, significant local pushback could delay or halt them.

Another factor that might exacerbate water stress for a country is limiting the locations where a facility can be constructed (Tonelli et al., 2023). This could cause multiple/larger plants to be constructed, which could induce a higher amount of water stress, or it could cause facilities to be localized on the same river system. Additionally, many analyses regarding water scarcity include obtaining the water from desalination plants. This might not significantly increase the overall cost or reduce the efficiency of the hydrogen production, but what to do with the generated brine discharge is under discussion (Tonelli et al., 2023).

2.5.3 Ecologic considerations

Broadly speaking, the ecologic considerations stemming from hydrogen mirror those of other industries. When producing hydrogen, the ecologic impact is entirely dependent on the type of production technology, the source of the water and energy used, and the disposal of waste from producing hydrogen. As discussed in the previous section, if it is sourced properly, the water supply is not of major concern; however, if hydrogen is produced in a water-stressed environment, or from desalination, there are ecologic, environmental, and social concerns.

The GHG emissions associated with desalination (Section 2.2.2.2) are generally attributed to the source of the energy used for the plant (Shokri and Sanavi Fard, 2023), so, if the electricity has a low carbon intensity, such as wind or solar RE, desalination does not have a major GHG impact. A large concern with using desalination for the water source for hydrogen production is the brine waste streams byproduct. Also, these brine waste streams commonly contain various solvents and chemicals used in the pretreatment process to reduce the corrosion effects of seawater. The most common way to dispose of the reject stream has been to discharge it back into the ocean. The exact effects of this tend to be specific to the exact mode of dispersion technique used; however, it is generally accepted that dumping large concentrations of hot, high-salinity brine can have severe consequences on marine life and ecosystems (Shokri and Sanavi Fard, 2023). Water desalination brine disposal methods should be included in clean hydrogen certifications to ensure the entire operational process minimizes ecologic impacts.

Additional ecologic considerations associated with green hydrogen production stem from the electricity generation source of that hydrogen. Compared to fossil fuel electricity generation plants, RE takes up more land, which increases competition with food security and biodiversity (Tran et al., 2022). Note that the land use for renewable technologies drastically varies from one location to another due to significant changes in production potentials, and as such, there are ranges of accepted values for land-use requirements for these technologies (Tran et al., 2022). Global averages for wind and solar produce approximately 9,000 GJ/ha/year and 4,500 GJ/ha/year, respectively, whereas gas produces 180,000 GJ/ha/year (Tran et al., 2022). However, compared to other bioenergy technologies, solar is significantly more efficient from a land use perspective (Tran et al., 2022; van de Ven et al., 2021). The land-use implications of solar depend on the total estimated penetration level of solar in the electricity grid mix (van de Ven et al., 2021). This is because new solar installations will likely first take over low-production farmland, which would improve the productivity of the land, but as more solar production is deployed, there would be increased competition for useful land or forested land, except if the solar installation takes place on non-useful land, e.g., on roofs or carports or is combined with agriculture to have dual-use of land and solar energy (agrivoltaics). This changes not only the land use but also the total life cycle emissions of the solar plant (van de Ven et al., 2021).

For a typical wind plant footprint, roughly 96%–99% of the land does not contain permanent physical infrastructure, allowing for multiple types of land use between the wind turbines (Harrison-Atlas et al., 2022). In the United States, the bulk of the installed wind plants come from either farmland or rangeland, accounting for 48.4% and 45% of installed wind plants in 2022, respectively (Harrison-Atlas et al., 2022). This allows for multiple land uses and lessens the land-use impacts from wind plants. Also, wind turbines strike birds and bats in flight during operation, which can stress the population (Choi et al., 2020), although bird deaths from wind turbine collisions are orders of magnitude smaller than those from cat predation and collisions with buildings and vehicles (Loss et al., 2015). Most bird populations are not significantly impacted by wind turbines, but raptors are generally of more concern due to their low numbers and low reproductivity rates (Choi et al., 2020). Stressors on keystone species, such as raptors, can cause long-lasting and unforeseen ecologic damage (National Geographic Society, 2009; Fan et al., 2023) and secondary effects on other species.

Another environmental impact of hydrogen concerns its possible atmospheric effects. Hydrogen can be released into the atmosphere throughout its entire production and use chain, for example, through leaks, which can impact the climate through various chemical processes. For example, the maximum water input of a large-scale global hydrogen market in the stratosphere was estimated by Vogel et al. (2011), Vogel et al. (2012). Atmospheric hydrogen can change concentrations of methane, ozone, and water vapor through various reaction mechanisms (Vogel et al., 2011; Sand et al., 2023). To be able to reliably quantify and evaluate this impact, possible sources along the production and use chain should be identified, the emissions should be determined, and the climate-impacting processes should be investigated in detail. Progress and investments in hydrogen detection and mitigation technologies are occurring across technologies, with supporting work focused on evaluation of representing hydrogen in global climate modeling efforts (U.S. Department of Energy, 2024a).

2.5.4 Social acceptance

The social acceptance of a new technology depends on the level of knowledge, public perception, and personal concern. In this respect, hydrogen is not different from other energy sources. For hydrogen development, social acceptance plays a key role on the front end in the development of infrastructure, including RE plants for the provision of electricity, and with the end user. It can either support the uptake of innovation or present challenges to project implementation. Research on the social acceptability of hydrogen can draw on the extensive literature on the social acceptability of energy technologies; however, in practice, social acceptance remains a major challenge for the energy transition. As Gordon et al. (2024) emphasized, the dynamics of the social acceptance of hydrogen have not yet been extensively researched.

To date, only a few authors have studied the social acceptability of hydrogen. Early work focused on the mobility sector, such as Yetano Roche et al. (2010), who analyzed public attitudes toward new transport technologies. Subsequently, the focus of the discussion shifted to the use of hydrogen in the energy sector. Here, Emodi et al. (2021) found low awareness of hydrogen technologies in the studies they reviewed, which were dominated by western European studies, similar to general energy research. This focus seems to prevail in more recent publications, such as Häußermann et al. (2023) and Schönauer and Glanz (2022), Schönauer and Glanz (2021), which assessed the social acceptance of green hydrogen in Germany. Or Jikiun et al. (2023), who analyzed opposition to onshore wind power in Norway and concluded that using wind energy to produce zero-emission hydrogen and then selling it locally (instead of exporting it) increases public acceptance. Sala et al. (2025), who focused on Spain, found that local acceptance was slightly lower than general acceptance, highlighting the need for more localized, context-specific research that can capture place-based variations in public attitudes toward hydrogen infrastructure. Research on other regions includes a publication from Lozano et al. (2022), who investigated the social acceptance of hydrogen for domestic and export use in Australia and found that knowledge of and familiarity with hydrogen and its associated opportunities was low. Also focusing on Australia, the results of Beasy et al. (2023) reveal a misalignment between industry stakeholders’ assumptions and community concerns regarding hydrogen infrastructure. While industry perspectives often prioritize technical aspects, community responses are often shaped by normative considerations. For Japan Yap and McLellan (2024) found that public perception of hydrogen is generally neutral to positive; however, their study also reveals a significant gap between public understanding and the realities of hydrogen production. Akhtar et al. (2023) did not focus directly on social acceptability, but they conducted a social life cycle assessment in seven countries, including non-Western ones, showing that social risks related to child labor, fair pay, unemployment, associational rights and collective bargaining, and gender pay gaps could be drastically reduced when key equipment is produced domestically rather than imported from other countries. Cumulatively, the existing body of literature remains predominantly focused on Western and industrialized contexts, resulting in a notable geographic imbalance in current research. This concentration limits the generalizability of findings and constrains a comprehensive understanding of how hydrogen technologies are perceived and accepted in diverse sociocultural, political, and economic settings.

Not only is the current literature geographically narrow, but the overall understanding of social acceptance remains limited for hydrogen and related infrastructure such as RE, desalination plants, and transport infrastructures, especially for different geographic locations and at different scales. According to Vallejos-Romero et al. (2022), to date, the social dimension is often not included in assessments. Studies assessing the social and environmental impacts of hydrogen on local communities and indigenous groups are lacking. This also applies, for example, to the MENA region, a potential energy and hydrogen production region (Terrapon-Pfaff and Ersoy, 2022). Examining social acceptance in potential export countries is likely to be beneficial and increase the probability of establishing an international hydrogen value chain. To address these gaps, more localized, context-specific research is needed to account for the influence of geographic and cultural factors in shaping public acceptance and community responses.

2.5.5 Human factors

Literature suggests that a hydrogen economy could be a pillar of energy systems and consequently impacts to communities and developmental trajectories are being discussed within the context of hydrogen development, but the number of publications is still limited. Against this backdrop, Scott and Powells (2020) called for a new social science research agenda for the transition to a hydrogen economy that should include a focus on these aspects, among others. Within this context, (Dillman and Heinonen (2022) conducted a normative assessment along the hydrogen value chain to highlight potential barriers and community impacts. Meanwhile, Fladvad (2023) focused on the sovereignty of Indigenous communities and argued that green hydrogen could reinforce neocolonial ties between the Global North and Global South. Similarly, Lindner (2022) pointed to several shortcomings of Global North-Global South green hydrogen partnerships, such as missing sociopolitical considerations and the fact that donors’ economic priorities tend to eclipse sustainable development in partner countries. Kalt et al. (2023) discussed these factors in light of South Africa’s hydrogen transition and noted the prevalent risks of extractivism and neocolonialism.

According to Müller et al. (2022), community opposition and impacts related to hydrogen can occur in connection with access to energy in countries with high energy poverty, access to water in arid regions, forced displacement, interference with the livelihoods of Indigenous peoples, and the strengthening of authoritarian rule.

Overall, this relatively small number of publications should be the starting point for more systematic empirical research on community impacts from the global development of green hydrogen. As Scott and Powell. (2020) emphasized, further research is needed to understand and interpret the social and economic changes associated with the development of the hydrogen economy. There is likely a benefit to assessing and sharing the burdens and benefits between potential exporting and importing countries and local aspects related to infrastructure development, access to and the availability of RE and water, and other key inputs for green hydrogen production. In addition, it would also be beneficial to link local impacts, as a dimension of sustainability, to other aspects of sustainability in relation to the environment and socioeconomic realities, as outlined by Müller et al. (2022).

2.5.6 Investment risk

The profitability and success of investments in RE generally depend on various financial risks and factors (Egli et al., 2025; Terrapon-Pfaff et al., 2024) that also largely apply to the development of production routes for synthetic fuels. Market conditions can lead to fluctuating energy prices and correspondingly uncertain revenues, which can be responded to with long-term contracts and hedging strategies. Political and regulatory requirements can change and affect operations and profitability. There are also technological risks of breakdowns and efficiency losses as well as operational risks due to disruptions, high maintenance costs, and a shortage of skilled workers. Financing and credit conditions are also very relevant, which can vary greatly depending on country-specific risk assessments; see Terrapon-Pfaff et al. (2025), in which country-specific risks for the production costs of hydrogen and synthetic fuels are included in the form of varying the weighted average cost of capital. Other risks mentioned in the literature can arise from disruptive environmental events, acceptance problems, and cybersecurity risks.

Investment risks could also be minimized on the demand side; a robust and sustainable supply of green hydrogen is essential for new steelworks based on direct reduced iron technology, for example. There are risks of stranded investments along the entire supply chain in the medium to long term; for example, strong trade market developments can lead to low costs and high price pressure for domestic producers in importing countries, or rising hydrogen prices can drive up the operating costs of hydrogen technologies and make their use unprofitable. Measures to ensure investment security are also valuable in order to avoid lock-ins in technology expansion, which could mean that GHG reduction potentials cannot be realized in the long term or can only at significantly higher costs.

2.5.7 Market development

The conditions for the development of a green hydrogen market vary greatly from one country to another, depending on the possible future demand as an integral part of energy development strategies and depending on the potential and know-how for production. Economic policy motives and objectives can also play a role, for example, if high-value creation potential is seen on the technology and infrastructure sides. On one hand, the development of value chains for the export and import of hydrogen is likely to follow the basic market and trade theories. On the other hand, the specific complexities of building a hydrogen economy require the national and international synchronization of developments on the demand, storage, transport and distribution infrastructure as well as the supply side. This requires enormous investments along the entire value chain in addition to close international cooperation in the development of new, stable trade relationships, such as through energy partnerships. In this context, there are high demands on political, regulatory, and administrative governance to enable parallel development of the different submarkets. And given the high production costs compared to fossil fuels, appropriate market incentives are being set in each case, for example, through the provision of targeted investment subsidies (Dong et al., 2022). Ikonnikova et al. (2022) used their hydrogen market model to emphasize the impact of carbon pricing in parallel with the consistent expansion of RE and the decreasing influence of the price of natural gas on market development when promoting a green hydrogen market. The respective national boundary conditions in the energy industry and foreign trade play a role on both the export and import sides, but local/regional conditions and players are also considerations in early market development (Ersoy et al., 2024). Strategic behavior and imperfect market conditions can lead to pricing that is significantly above techno-economic cost assumptions (Barner, 2024). This discrepancy arises because market inefficiencies—such as limited competition, information asymmetry, and bottlenecks in the supply chain—allow certain market participants to strategically influence prices. Strategies based on cost-based analyses of potential hydrogen trading can be thwarted by inflated market prices, and the expected market dynamics can be misjudged.

In the past, a lack of technological readiness and infrastructure were the main reasons for investment delays in the hydrogen economy (Bento, 2010). In the long term, newly developed individual value chains and an increasing number of actors could lead to a new market that establishes new hydrogen trade relationships between countries. Initially, regional markets are likely to emerge, and in the long run, global competition for hydrogen and fuels based on hydrogen is likely to play a defining role in price determination. Above all, we see open questions in the control and management of the complex interplay of sectoral demand developments and the development of generation, storage, transportation, and distribution infrastructures. The possible role of blue versus green hydrogen in early market development and in the long-term path to a purely green hydrogen supply has not yet been sufficiently described, nor have the associated risks of lock-in effects and stranded investments (Ueckerdt et al., 2024). The sensitivity, robustness, and feasibility of theoretical market modeling represent a broad field for relevant further investigations. Realizing the existing efficiency potential in all areas of the hydrogen economy as quickly as possible can help to significantly reduce the challenges in terms of resource and investment requirements and achieve a faster transition to green hydrogen. The rapid and consistent expansion of renewable power generation structures is the key prerequisite for this globally. From the stakeholders’ perspective, there are open questions within the context of national energy system strategies and market conditions that are closely linked to the dimensioning of production routes and entire national energy systems.

From the systems and macroeconomic perspectives, an important additional motivation for establishing international hydrogen trade was mentioned: increasing the security of supply through a diversity of importing countries. For example, system modeling by Fattahi et al. (2024) showed that Europeans’ motivation for trading hydrogen and ammonia could be primarily based on improving the diversity and security of the energy supply rather than the expectation of significant cost savings, whereas in the MENA region, the motivation for exports is likely to come from the potential for long-term economic benefits at the regional level. Nuñez-Jimenez et al. (2022) also showed that long-distance hydrogen imports can enhance EU energy security through supplier diversification.

3 Discussion

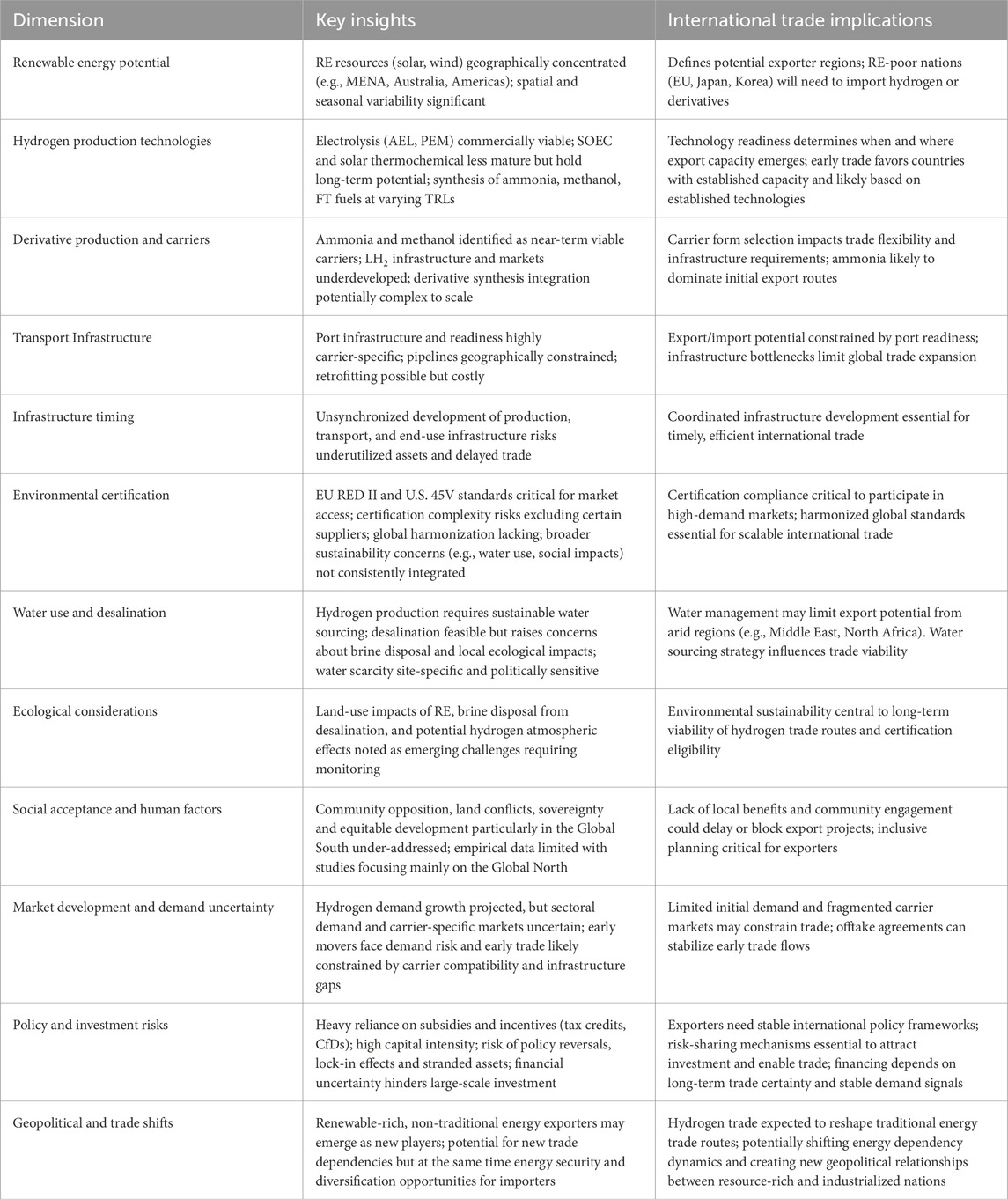

This study aims to provide a comprehensive summary of the current state of knowledge on the potential of international trade in hydrogen and its derivatives. The study is qualitative in nature and does not include quantitative modelling, spatial analysis or techno-economic simulation that would allow for a more accurate assessment of trade flows. Furthermore, while the study highlights important factors influencing hydrogen trade, such as cost variability, resource availability and social acceptability, the level of detail varies across these dimensions, reflecting the evolving research landscape. These methodological limitations are inherent to the review format and underscore the need for continued multidisciplinary research efforts that integrate empirical findings, model-based approaches and context-specific analyses. Within the scope of these methodological boundaries, several key factors emerge as particularly influential in shaping the future of international hydrogen trade, which are summarized in Table 1.

Table 1. Key insights and implications for international hydrogen trade development.