Katherine Snyder1*

Katherine Snyder1* Pauline Muindi2

Pauline Muindi2 Colleta Khaemba2Pieter Rutsaert2Judy Mutegi2Francis Omondi2Jason Donovan3

Colleta Khaemba2Pieter Rutsaert2Judy Mutegi2Francis Omondi2Jason Donovan3- 1Independent Consultant, Tucson, AZ, United States

- 2The International Maize and Wheat Improvement Center (CIMMYT), Nairobi, Kenya

- 3International Center for Research and Development, Guanajuato, Mexico

The conflict between Russia and Ukraine, and the associated disruptions in global wheat supply has resulted in concern for food security throughout sub-Saharan Africa. In Kenya, which depends heavily on wheat imports to meet demand, this concern has intensified calls for self-sufficiency in wheat production. Wheat shortages have led to price hikes that hit all consumers but the urban poor in particular. To decrease reliance on imports, for both food security and for nutrition, Kenya has implemented policy measures to spur increased wheat production. This paper explores the context for increasing wheat production in Kenya to respond to increasing demand, and for addressing the needs of the stakeholders in the sector. Findings suggest that wheat self-sufficiency is unlikely to be achieved soon. Major public and private investments would be required to build the infrastructure, systems, and institutions required to support smallholders to expand and intensify their production. Millers have relied on cheap wheat imports for decades and show limited signs of willingness to support backward linkages with farmers. Critical public infrastructure (e.g., wheat seed systems, extension systems) is ill-equipped to support the growth of the wheat sector. Researchers and policy makers would better serve the interests of smallholder wheat growers by identifying feasible objectives for sustainable and equitable industry growth. We conclude with recommendations for targeted investment and interventions.

1 Introduction: demand and production of wheat in sub-Saharan Africa

The ongoing effects of the Russia-Ukraine war on cereal production and trade has received considerable attention and concern for global food security and particularly for food and nutrition in the Global South. As Erenstein et al. (2022) note, wheat plays an important role in global food/nutrition security, “supplying a fifth of global food calories and protein” (p. 48). In addition, wheat production takes up a significant part of land globally; “By 2018, wheat was cultivated on an estimated 217 million (M) ha of land… making it the most widely grown crop in the world” (p. 48). Of global land production, approximately “29% of the global wheat area is in low and lower-middle income countries (L/LM-ICs), contributing some 25% to the global wheat production” (ibid: 50). Within these low and lower middle-income regions, millions of farmers are engaged in wheat production, sales and consumption. For the period of 2016–2018, global wheat production averaged 750 million tons with Asia (China and India), Europe (Russia, Ukraine and France), and North America as the largest producers. After rice, wheat is the second most consumed cereal globally. In Asia and Africa, consumption exceeds production and these two regions rely heavily on wheat importation to meet demand (Grote et al., 2021, p. 2).

In sub-Saharan Africa, particularly in urban areas, wheat consumption, spurred in part by inexpensive imported wheat, has grown considerably. Bread, pasta and other wheat products are convenient and quick sources of food compared to maize or rice (Morris and Byerlee, 1993; Kennedy and Reardon, 1994; Boughton and Reardon, 1997; Noort et al., 2022; Minot et al., 2015). As Mason et al. (2015) observe, for women who work outside the home and in urban settings, wheat products (such as bread and pasta) can reduce the time they need to spend on cooking and food preparation.

In the early 1990s, Morris and Byerlee (1993, p. 737) noted that “Over the past 3 decades, dietary patterns in sub-Saharan Africa have undergone dramatic changes. Perhaps the single most remarkable development has been the rapid growth in wheat consumption.” The upward trend in wheat consumption across much of the region has continued since then. Wheat products are now thoroughly embedded in diets in African countries. The rising cost of the Ugandan “rolex” snack (rolled chapati stuffed with eggs) due to the Russia/Ukraine war caught the attention of the New York Times in February 28, 2023. Packaged bread, chapati and pasta have become a regular feature of urban diets in particular. Wheat consumption continues to grow and Mason et al. (2015) report that the gap between maize, the dominant staple in sub-Saharan Africa, and wheat consumption is shrinking (p. 582). Demand in sub-Saharan Africa has largely been met with the importation of inexpensive wheat.

Given the demand, and the uncertainties around disruptions in supply chains due to climate events and global conflicts, there has been increased interest in improving wheat production on the African continent to better meet demand and decrease reliance on imports (Gumisiriza et al., 1994; Dorward et al., 2004; Baudron et al., 2019; Anteneh and Asrat, 2020). In neighboring Ethiopia, there has been considerable attention to how to increase wheat production for smallholder farmers through improved access to improved seed varieties, and market and policy interventions (Biggeri et al., 2018; Demeke and Di Marcantonio, 2019; Gabre-Madhin, 2001; Gebreselassie et al., 2017; Minot et al., 2015; Shiferaw et al., 2011; Spielman et al., 2010). Silva et al. point out that “Africa spends 85 billion USD annually on food imports, of which 15% are for wheat imports alone” (p. 1). They argue that decreasing reliance on imports is essential for food and national security and lay out a series of recommendations for a “pathway to wheat self-sufficiency.”

While there may be scope for increasing wheat production in Ethiopia, this paper focuses on the plausibility of wheat self-sufficiency in Kenya. The results from Kenya may be more broadly applicable across the continent other than Ethiopia. Our research asks what is inhibiting an increase in production of what in Kenya. To answer this question, we explore the challenges, opportunities and constraints in the wheat sector which have relevance to the crop sector more broadly. Rather than focusing on the potential for technical interventions such as improved seed or agronomic practices, we adopt a systems lens and place wheat value chain stakeholder perspectives through qualitative research at the center of our analysis. Orr et al. (2018, p. 15) argue that components of these systems, such as “policy, institutional and market trends, culture and local circumstances could shape the possible outcomes of interventions to strengthen specific value chains.” We adopt this systems approach to explore in depth the myriad factors that contribute to, but also constrain, wheat production in Kenya. Understanding these perspectives is essential for designing policy and other interventions but also for assessing the role that wheat has in rural economies. Others have also argued for this broader approach which goes beyond a focus on farmers to include such stakeholders as “extension agents, agricultural exporters and processors” to gain a fuller picture of how the agricultural system functions and where the challenges are within it (Snapp et al., 2003, p. 349). Indeed, in a study of wheat in Nigeria in the 1980s, Andrae and Beckman (1985) showed how pivotal millers were to both wheat production and consumption.

2 The wheat sector in Kenya

Countries in the northern, eastern and southern regions of Africa possess the agroclimatic conditions to produce spring wheat, and wheat production has featured (with varied levels of enthusiasm) as part of their agricultural development discussions and strategies. In Kenya, wheat is grown primarily in highland areas (1,500 meters and above) and medium and large-scale farmers produce roughly 80 percent of Kenya’s wheat. While wheat cultivation has expanded since independence, the area farmed has stayed fairly constant for over the last decade at 120,000 ha in total (FAO, 2015, p. 3). Wheat was first produced in the highlands during the colonial era. As Makanda and Oehmke (1993) note, wheat was central to colonial agriculture and export trade FAO (2015, p. 3). Lord Delamere was instrumental in promoting wheat and planted 1,200 acres of it in 1906. After this, European settlers expanded wheat production on land alienated from Africans. Delamere hired the first wheat breeder in Kenya and established a research station in Njoro. The government took over wheat breeding research in 1911 (Makanda and Oehmke, 1993, p. 4). A focus of wheat research and breeding, from the colonial era onwards, has been on addressing rust varieties which continue to plague wheat production globally. Interestingly, Makanda and Oehmke state that “Kenya was a net exporter of wheat throughout the late 1960’s and early 1970’s. By the end of the 1970’s, Kenya was importing wheat to meet domestic demand” (Makanda and Oehmke, 1993, p. 1). They also observe that “wheat is still one of the seven crops that the government considers as central to achieving the development goals established for agriculture” (Makanda and Oehmke, 1993, p. 2).

Wheat in Kenya is produced entirely as a cash crop and it is the second most important cereal crop in the country “from a food security viewpoint both in terms of quantity and calories consumed” (Monroy et al., 2013, p. 5). The Russia-Ukraine war has dramatically affected the imports the country relies upon to meet demand. The resulting shortages of imported wheat, together with the significant increase in importation costs, led the Kenyan government to ban wheat imports in October 2023 to encourage domestic production by easing competition with cheaply produced imports. Mwangi et al. (2021) reported that Kenya produces, on average, 300,000 metric tons of wheat annually on roughly 140,000 hectares (p. 1–2). It imports about six times what it produces (ibid: 2). Approximately 31% of imported wheat to Kenya comes from Russia, followed by 29% from Argentina.1 Wheat production in Kenya has been largely stagnant over the past two decades, the reasons for which will be explored in the sections to follow. Briefly however, climate change, low global wheat prices, land fragmentation, insecure leasing arrangements, lack of access to improved varieties and cost of production are the main factors contributing to low production (Figure 1).

Figure 1. Wheat supplies in Kenya 2017–2021. Source: Kenya National Bureau of Statistics-KNBS 2022.

There has been very little socio-economic research on wheat in Kenya that assesses the differences in incentives, capacities and circumstances of smallholder, middle-sized farmers, and large commercial farmers. In addition, there has been little inclusion of the perspectives of traders, agrodealers, millers and service providers in the wheat sector. Recently, Mwangi et al. (2021) carried out a study on smallholder wheat in NW Kenya which contributed to understanding constraints faced by farmers. The discussions on the inefficiencies of wheat production in Kenya, especially for smaller-scale production, however, date back at least 20 years. Previous research highlighted wheat production inefficiencies stemming from low yields combined with high costs for inputs (e.g., improved seed, fertilizer) and services (e.g., machinery, transport) (Longmire and Lugogo, 1989; Gitau et al., 2011). No study has been carried out on a country-wide scale or examined all the actors engaged in the wheat sector. In addition, some of the wider impacts of wheat production on the local economy have not been explored. In our results below, a more complete picture of both the constraints and opportunities in wheat emerge as well as an analysis of the overall contribution of wheat, and its byproducts, to the Kenyan economy and rural livelihoods.

Finally, it is also important to situate wheat within the wider political economy of agriculture and food in Africa, as broader interests affect production and investment. As Mason et al. (2015) point out, while demand for wheat increases, it is the interests of millers, bakers and middle to high-income urban consumers that influence national policies more than small-scale farmers or poor urban consumers (Mason et al., 2015). In their analysis of the political economy of wheat in Africa, Byerlee and Morris (1988) suggest that urbanization, increased income, national economic policies, and food aid all aligned to promote greater wheat consumption. They argue that a variety of national pre-structural adjustment policies (exchange rates, consumer subsidies) made wheat products both available and affordable compared to many domestic grain staples. In addition, they contend that different private sector actors also bias policy interventions toward wheat consumption and imports.

These interest groups include middle-income urban consumers (who often can influence food policy decisions), the wheat-processing sector (which exercises considerable market power in protecting its vested interests), and exporting interests in developed countries, such as grain exporters or milling and shipping industries (which frequently have strong commercial linkages with processors in importing countries). In addition, interest groups in exporting countries also succeed in distorting the policies of these countries toward wheat exports to the developing world. To a large extent, all of these interest groups reinforce each other in promoting wheat consumption (1987, p. 369).

These forces continue to influence policy around wheat production and importation today across the continent. So, while demand has risen significantly, production has not. This paper exposes some of the reasons for this gap.

3 Methodology

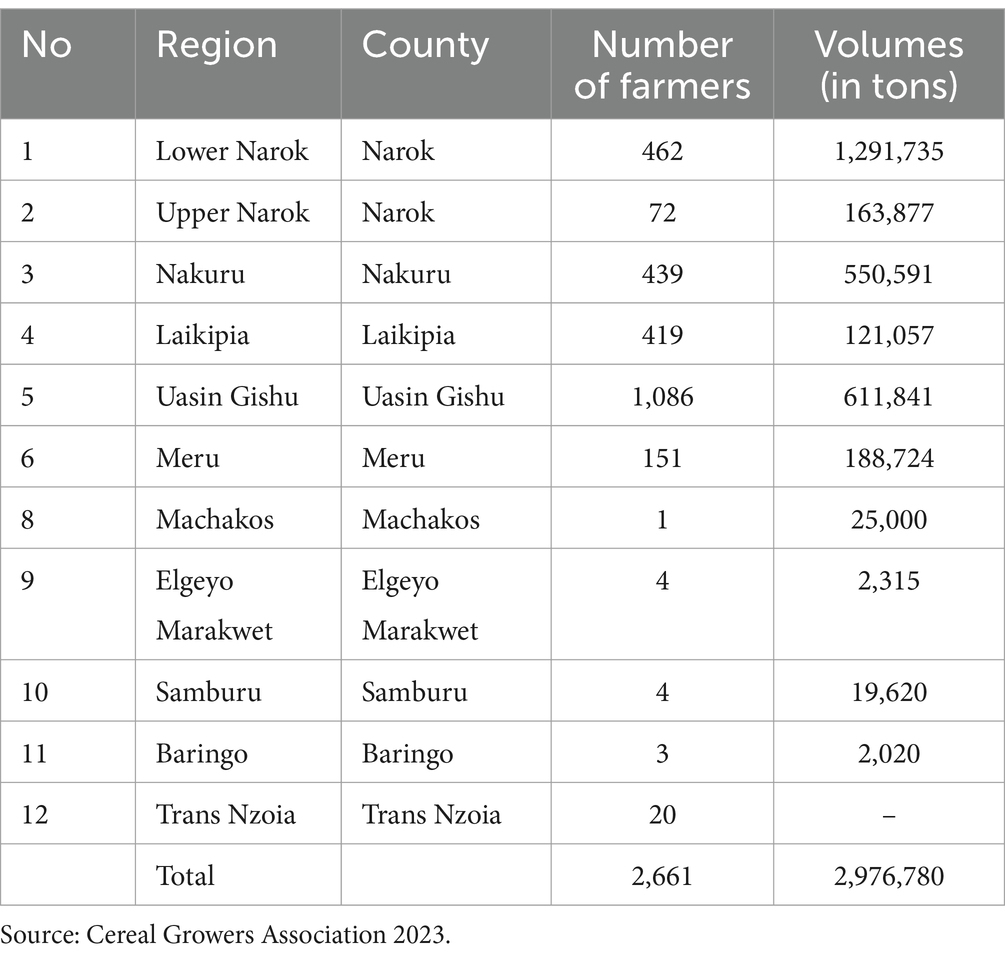

This research employed qualitative methods and reviewed relevant policy and trade documents concerning wheat. We focused the research on the major wheat producing counties in Kenya: Narok, Nakuru, Uasin Gishu, Meru and Samburu. We chose these counties based on their production volumes, but also their potential for wheat expansion (Samburu). We carried out key informant interviews with smallholder farmers, medium and large-scale farmers, landowners, traders, agrodealers, private service providers, millers and government officials. We also interviewed seed companies and researchers in the Kenya Agriculture and Livestock Research Organization (KALRO). We conducted focus groups in each county, except Samburu where there were not enough farmers available. In total, we carried out 15 focus groups: 5 with women and 10 with men, carried out separately. The lower number of FGDs for women reflects the fact that there are far fewer women wheat farmers, and also that their overall workloads make it hard for them to take the time for focus groups. The FGDs were primarily with smallholder farmers, though medium-scale farmers were included in Narok, Uasin Gishu and Nakuru. The number of participants in the focus groups ranged from 6 to 12 and most of the smallholder farmers cultivated 15 acres or less. In the six counties, we conducted 74 interviews, 13 with women and the remainder with men. The farmers selected came from a list of 2,661 farmers that the Cereal Growers Association provided us (see Table 1 below). While not all wheat farmers are members of CGA, the majority mostly likely are. Working in partnership with the CGA was the most efficient way to find farmers with experience in wheat farming as these data are not collected at the County level.

Table 1. Wheat production in Kenya in all counties.

As a qualitative study of the wheat sector, this study aims to capture the perspectives, opinions and behavior of the relevant actors. It does not focus on gathering quantitative data for statistical analysis or on agronomic data, or specific details on yields, costs, and income except in broad terms that focus on how and why actors engage in the wheat sector. Through thematic content analysis, we assessed data produced from focus groups and key informant interviews across a wide selection of actors and geographical locations.

3.1 Farmer interviews and focus groups

In total, combining focus groups or interviews, we spoke with 143 small-scale, 15 medium-scale and 25 large-scale farmers. The farm size classification for wheat is unique to that crop. Small-scale farmers are defined as those with farm sizes <100 acres. However, the majority of the farmers we spoke with and who defined themselves as small-scale wheat farmers, cultivated around 15 acres or less. Women, due to constraints explored below, usually cultivated 6 acres or less. The farm size classification for wheat farming is specific only to wheat. While small-scale farmers are defined as having <100 acres, most of the farmers we interviewed did not come even remotely close to that number. Rather, they had between 2 and 6 acres. Medium-scale have farms between 100 and 500 acres and large-scale have over 500 acres.

The semi-structured questionnaires covered a several topics, from land size and tenure, reasons for and benefits of farming wheat, yields of wheat, costs of production, use and access to inputs (seed, fertilizer, herbicides, fungicides, machinery, etc.), post-harvest storage and income from sales. We explored the major constraints in wheat production and sales as well as the perceived benefits and opportunities.

All focus groups and interviews were carried out primarily in Kiswahili, with English used with a few stakeholders and took from 1 to 2 h each. Interviews and FGDs were all recorded using digital voice recorders and downloaded into secure folders. Each interview and focus group had at least two note-takers documenting the discussions and notes were compiled and organized by county. We analyzed the data in these documents to expose recurring themes and issues raised around participation in the wheat sector.

3.2 Key informant interviews

In addition to engaging with farmers of all scales, we carried out 31 interviews in total with men and women agrodealers, aggregators, storage facility managers, extension officers, county government officials, traders, landholders (who lease out their land to wheat farmers) and millers. At the national level, we interviewed staff at CGA and in the Ministry of Agriculture. These interviews aimed to gain a deeper understanding of the wider agrarian economy around wheat in Kenya and how wheat contributes to different actors’ livelihoods, as well as the challenges in producing, selling or processing wheat. This broad lens on wheat in Kenya revealed both the challenges but also the myriad ways in which wheat contributes to rural livelihoods and the national economy.

4 Results and discussion

Our discussion focuses first on wheat production and the variation in context according to different types of wheat farmers, differentiated by scale and by gender. We then turn to an analysis of post-production factors that affect the benefits farmers obtain from wheat commercialization, as well as the factors that shape other actors’ decisions, such as traders and millers. The open-ended questions and our analysis reflect respondents’ experiences, opinions and perceptions and are not meant to capture precise quantitative data. We combined content, narrative and thematic analysis of the recorded and transcribed transcripts of all interviews and focus groups to arrive at our results and conclusions.

4.1 Wheat production: “we have no voice, we have no help, we just survive”

4.1.1 Access to land

In Kenya, the competition for land is considerable and, with population growth, land fragmentation (where multiple inheritors over generations receive increasingly smaller plots) poses numerous challenges, to all agricultural production. For wheat production in particular, access to land is a major constraint that farmers address primarily through leasing land. Indeed, most wheat farmers, independent of their production scale, lease at least part of the land used for the crop’s cultivation. For small-scale farmers, this may mean leasing plots at different locations, which in itself poses challenges. Many small and medium-scale farmers we interviewed leased more than one parcel to make it more profitable if climate, pest, disease and low prices at harvest did not get in the way.

Leasing is an opportunity, for both landholder and leasee, but also creates uncertainty. Rarely do landholders agree to lease their land for longer than a year’s time. Lease agreements vary by county. All those who leased land remarked upon the tenuousness of leasing. When leasing more than one parcel, the parcels might be quite distant from one another, making various steps in the production and harvesting process more challenging, as one woman farmer in Laikipia explained: “Land leasing agreements are short term and mostly the lands are not centralized; they are in far different places.” Leasing for 1 year does not guarantee future leases: “Accessing land can be a challenge because you lease land for 1 year and the following year the owner of the land may decide not to lease it to you.”2 Indeed, throughout the counties covered in our sample, the uncertainty around leasing was a constant concern. One woman’s account was not an uncommon one:

If you are to lease land, you need to lease it early because there is great demand for farmland. We have had disputes before with land leasing because the landowner had leased it to more than 3 people. Because of that, I want to use the written land lease agreement; which will have signature of the two parties entering the agreement and a witness….last year, I had a problem in acquiring land. I first got 7 acres, then after a month I got 3 acres.3

In rangeland areas, such as Narok and Samburu, formerly occupied primarily by pastoralists (Maasai and Samburu), and operating under communal land tenure, group ranch titling has given way to individual land titling. The result of this process is highly varied, but in many instances the plot sizes allotted to individual land holders are not sufficient for livestock grazing. So, many Maasai and Samburu community members are now leasing their lands to investors who grow wheat and maize. Investors are increasingly flocking to Samburu country, which is a relatively new area for growing wheat, as the price of leasing is less than in other wheat growing areas like Nakuru or even Narok. For example, leasing land in Samburu runs about 3,000 Kshs per acre, whereas in Nakuru costs are closer to 11,500 Kshs and in Uasin Gishu run as high as 15,000 Kshs per acre. While individual titling, has made leasing land, by both internal and external investors easier, it also leads to the fragmentation that was cited as a problem throughout the counties of this study.

4.1.2 Knowledge and information

Access to information about improved seed varieties, agronomic practices for wheat, chemicals and post-harvest practices for wheat is scarce in Kenya, particularly for small-scale farmers, and for women in particular. Women are less mobile than men due to domestic responsibilities, so they rely on kin, neighbors and friends for information. Getting reliable information on wheat prices is also a major challenge for many small-scale farmers as brokers present them with numerous reasons for offering them the prices they do, such as miller preferences, bushel weight, transport costs, etc. Small-scale farmers have little bargaining power given their constraints so often take what price they are offered.

Due to structural adjustment policies in the late 80s and early 90s, extension services across the continent have declined. Kenya is no different. Overall, extension agents, when they are available, may handle as many as 1,000 farmers or more (Bonilla et al., 2024). A statement by one woman farmer in Laikipia county was reiterated by almost all the farmers we spoke with: “We have never seen extension agents around here so mostly we get information from fellow farmers.”4 At county offices, officials suggested it is difficult to replace agents when they retire, both due to lack of funding but also due to lack of interest by younger people in filling these roles.

Large-scale farmers and agribusinesses often provide services that would usually be supplied by government extension, such as advice on seed varieties, agronomic practices, post-harvest practices, etc. Many small-scale and medium-scale farmers stated that they have participated in several field days hosted by large-scale farmers who provide valuable information on traits (yield expectations, resistance to pests and diseases), seed rate and input requirements, and the importance of crop rotation and zero or minimal tillage.

4.1.3 Obtaining seed

For small and medium-scale farmers, access to quality seed and to the best varieties is a major challenge. For large-scale farmers, who have broader and often global networks, and access to more capital, acquiring the appropriate seeds is not as significant a challenge. Small-scale farmers in particular struggle to find and purchase certified seed. If it is available, they may not have the capital to buy it. In many instances, it is simply not available, and they rely on their own recycled seed, or seed from other farmers. Large-scale farms, such as Kisima Farm in Timau, historically sold untreated commercial grain to small and medium-scale farmers which those farmers used as seed. More recently, Agventure Ltd., which Kisima and other large farms are shareholders of, has been established as a Seed Company and now sells certified dressed seed to farmers. According to both small-scale and medium-scale farmers, large-scale farmers play a crucial role in providing a reliable and accessible source of wheat seed as they have resources (land, finances, and technical know-how) for seed production and storage.

Access to high quality seed is critical for meeting production goals. As an agricultural crop officer in Meru County stated, “most farmers source seed from Agventure because they trust the seed produced.”5 But, for many farmers that we interviewed, the remarks of one woman in a focus group in Meru hold true for other counties: “We are unable to access certified seeds hence we use the already recycled seeds mostly with low yields…. We do not have access to certified seeds…you just plant what you can access.”6 Often, farmers are unsure of the varieties they are planting. One farmer in a focus group in Uasin Gishu explained the potential drawback of obtaining seeds from other farmers: “We sometimes buy wheat seeds from farmers in other places without the knowledge that the varieties in those areas will not perform well in our ecological zone.”7

If farmers do have the capital for purchasing seeds, there may be significant delays in accessing those seeds due to lack of supply. We interviewed medium-scale farmers who had put down cash for seeds but were waiting for months to actually get them. These delays pose critical challenges to production and eventual profits.

The main supplier for wheat seeds is Kenya Seed Company (KSC), followed by KALRO. KSC is unable to meet demand, in part because they cannot find enough outgrowers to produce seed for them. KALRO, who also produce seeds for the market, also noted this impediment. Lack of adequate land to bulk seed, due to fragmentation and also to population growth and expansion of urban areas, is a serious constraint on seed production. At the Cereal Growers Association (CGA), they also underscored that producing and obtaining access to new seed varieties is a major bottleneck in wheat production. Wheat seed is mostly produced in Nakuru and the cost to transport it to other parts of the country raises the overall price of the seed.

For small-scale farmers, the cost of seed is a major concern. Raising enough cash to purchase seed, then the high cost of transportation can be very difficult. Farmers may rely on brokers to access seeds. As a participant in a female focus group discussion explained, “There are men who buy seeds in bulk and come to sell to us. We buy these seeds because it is expensive to buy certified seeds from Nakuru town and transport seed to Elementaita. These brokers sell us the wheat seed in kilos (150 Kshs per kilo – USD $1.08) and most of the time we do not know the varieties they sell to us” (Female FGD in Elementaita, Nakuru County). While 150 Kshs may not seem to be that much, 50kgs are needed for one acre. When buying from brokers, just as with buying from their fellow farmers, farmers may not know the variety of seed they are obtaining.

4.1.4 Inputs and machinery

Achieving higher levels of wheat productivity requires other inputs such as fertilizer, insecticides, herbicides and fungicides. The costs of these inputs is high for small-scale farmers. Most small-scale farmers rely on hiring the equipment necessary for plowing, planting and harvesting wheat from small enterprises or from medium-scale farmers who lease out their equipment. Medium-scale and large-scale farmers own their equipment. A variety of small-scale enterprises have sprung up to provide mechanization services to small-scale farmers. The demand for these services is high and can be difficult to provide if farms are spread out over a wide geographical area and all the farmers need services at the same time. Fuel prices continue to rise so it is costly to travel long distances to service non-contiguous plots across the landscape. While these are challenges, all farmers pointed to mechanization as a major advantage in wheat farming, particularly if compared to maize. As one woman farmer underscored, “you just plant it, apply chemicals and go. You do not have to visit the farm constantly like you do with maize and other crops.”8

Finally, small-scale farmers also noted that the quality of the chemicals they purchase is often poor. This issue affects farming more broadly, not only wheat. Either the product has been tampered with or is cheaper because of poor quality. Quality products are essential for good harvests. Medium-scale and large-scale farmers have access to, and can afford, better, more reliable products.

4.2 Post-harvest challenges

4.2.1 Drying, storing and transporting harvest

How well the grain has been dried after harvesting greatly influences the price that farmers get. Most small-scale farmers do not have access to commercial driers, nor can they afford to purchase them, so they rely on sun-drying their wheat. Because drying wheat is so critical, small-scale farmers are pushed to sell to brokers quickly at the farm gate and may not be getting the best price. Furthermore, they do not have access to storage where they could hold on to their harvest until the prices go up. Medium-scale farmers also sometimes rely on sun-drying but usually can access driers that they either own or pay to use. Large-scale farmers generally own driers.

Storage facilities are largely absent from most wheat producing areas or are seen to be too expensive to use for small-scale farmers. Medium-scale and large-scale farmers generally have arrangements directly with millers to sell their harvest or transport their crop to aggregators which buy it and sells on to millers.

Finally, for small-scale farmers, hiring transport to bring purchased seed to their farms or to take their harvest to better markets is outside of their ability.

4.3 Wheat sales

Until the recent decline in wheat importation, wheat prices paid to farmers have been low. The high cost of production, combined with low market prices, has driven many small-scale farmers out of the market. However, many of these farmers have stuck with wheat because it provides cash income in a short time period. In October 2023, the Kenyan government temporarily suspended the importation of wheat, ostensibly to protect wheat farmers from depressed prices from cheap imports.

The Cereal Millers Association, the Cereal Growers’ Association (CGA), millers’ and farmers’ representatives together with the government Agriculture and Food Authority discuss, negotiate, and determine the price of wheat which is usually calculated by assessing the cost of production incurred by farmers. However, small-scale farmers may not be aware of these prices or may not be able to bargain successfully with brokers to get them. Millers have considerable influence over the price of wheat nationally and regionally (according to where the miller is located).

4.4 Brokers/traders

Farmers complain about poor prices and unfair practices of brokers/traders, but they rely upon them greatly for selling and transport. Traders will buy unclean wheat from farmers, and clean and store it at their stores which saves farmers’ labor and time waiting for their cash. Aggregators usually have equipment to measure moisture content and can assess and grade grain. They also often provide facilities to dry farmers’ grain and then sell the grain on to millers. Traders claim that ultimately, the price for grain is determined by millers “as a trader, you first get the prices the millers are buying at, which depends on the market. If the price is good, you offer good prices to the farmers. If not, then you offer low prices” (trader, Meru town).9

Traders bear high costs for transportation and the risks on the market as well as stiff competition from other traders. They also often face delayed payments from millers. Many traders have also taken up producing animal feeds so they can buy sub-standard wheat and turn it into livestock feed.

4.5 Millers

There are a variety of companies at different scales and locations involved in milling wheat. According to data from the World Food Program, The Cereal Millers Association (CMA), which has around 35 milling companies, accounts for 40% of millers in Kenya. Small and medium-scale millers are mostly registered under the Grain Mill Owners Association (GMOA). CMA accounts for over 80% of wheat milling capacity.10 Given the demand for wheat-based foods in Kenya, milling wheat promises significant returns. One respondent began as a trader and then moved into milling, starting his own company. He moved into milling maize and wheat from selling cereals and now mills both flour and animal feeds.

Yet, milling wheat has its own challenges. A miller in Meru explained that he had moved out of wheat due to logistical challenges of getting the wheat from Narok county. Also, he explained that “most of the wheat produced in Kenya is soft wheat and it was difficult to get hard wheat which is sought after for milling. We therefore had to change from wheat milling to milling maize.” In addition, the competition among millers is high and traders may sell their wheat to more than one miller, which decreases the amount received by any one miller. Traders may also mix wheat of different quality and moisture content, adding to millers’ challenges. Inadequate supply of wheat and fluctuating prices have a bigger impact on small-scale millers. To mill flour and make a profit, large quantities of wheat are needed. Furthermore, some varieties have higher prices than others. For example, one miller noted, “the Asian market wants white and clean wheat like Duma and Korongo. The price difference between white and brown wheat is around 100–300 Kshs ($0.72–$2.17).” Many millers will blend local wheat with imported wheat to meet their production goals and the criteria required by the government that local wheat is purchased before imported.

4.6 The wider context: broader impacts and motivations for farming wheat

Even with the myriad challenges described above, most farmers express continued interest in producing wheat. In part, this is due to recent prices being high because imports have dropped due to the Russia-Ukraine war. While farmers may keep some wheat for their own consumption, wheat is mainly grown as a cash crop. For smallholders, it is attractive for a number of reasons. First, it is a shorter duration crop than maize, the other main cereal in Kenya. And, importantly, it does not require the labor that maize does. So, while the investment in hiring machinery and purchasing chemicals is substantial, there is little need to hire labor. Casual farm labor (kibarua) is both costly, often hard to find and hard to adequately supervise. Small-scale farmers stated repeatedly that shorter duration and low labor requirements were the two main reasons to grow wheat. One farmer explained the benefits of wheat: “Wheat is early maturing than maize. So, we can harvest and sell wheat to facilitate us to farm maize”.11 A woman participant in a focus group in Uasin Gishu further elaborated: “you can easily rotate with maize to ensure full land utilization.”12

While wheat is attractive for many farmers, some also indicated that if another crop came along that was well adapted to their local conditions and had some of the factors that make wheat attractive, they would consider switching. A woman’s focus group in Laikipia spelled out these reasons:

Production of wheat is very low. You use a lot of money for example in preparing land, application of fertilizers and chemicals etc. and get very little from it. The profits are very minimal, and some make losses. Some of us have made small profits in farming wheat, whereas others have never made any profits from wheat farming. We are not able to diversify because the weather in Oljororok is harsh, such that maize and beans would not do well. We can plant peas and groundnuts, however getting labor during harvesting time is a challenge. The advantage of wheat is that it takes a shorter time, and it is a bit tolerant to harsh weather compared to other crops. But if another crop can do better in such kind of weather, we would gladly adopt it.13

What is clear from examining the perspectives of farmers from across such a wide diversity of wheat growing areas is that multiple factors shape both the costs and the benefits obtained from wheat. In particular, proximity to markets, road networks, environmental conditions, availability of land and access to services all affect the profits that farmers earn and the decisions they make on how to farm wheat.

4.7 Women and the wheat sector

Throughout this study, we endeavored to capture the perspectives of women farmers, traders, and small enterprise owners. While there are far fewer women farming wheat, particularly in the medium and large-scale farmer category, there is considerable and growing interest from women small-scale farmers. The constraints they face are similar to men – cost of leasing, costs and availability of seeds and inputs, and low prices offered by brokers. However, these constraints are magnified by the perception that women should work through men, or that they are easy to take advantage of. As one medium-scale woman farmer explained, “all the agreements we do with my husband.”14 It is hard for women to get their husbands to give them the capital to start wheat farming and female-headed households experience even greater challenges to access cash. They rely on borrowing from friends and neighbors, from women’s groups or from selling maize and chickens and using the proceeds to invest in wheat farming. In Laikipia County, one woman explained “the men have the money and sometimes it is hard to obtain money from them, so we borrow from our neighbors.”15 One woman summarized: “The biggest challenge facing women is that we do not have many sources of income, compared to men. We rely on farming as the only source of income.”16

The experiences of women were highly varied. In some, such as in Meru County, women reported that they work and make decisions together with their husbands and they do not perceive gender as a severely constraining factor. In Laikipia County however, women stated “when it comes to farm operations, we help our husbands on their lands, but they do not help us on our lands.”17 And, “wheat is a crop that we grow secretly without our husbands’ knowledge…leased land is not my husband’s and he will not know how much I harvested.”18

Access to and use of inputs such as chemicals can also be a challenge for women. They are often advised, for health reasons, to avoid spraying chemicals so they must hire labor instead. It is also harder for women to access information and knowledge of different wheat varieties and agronomic practices as their networks are more local and their movement away from home more limited. Most women turn to fellow farmers for advice. A young woman farmer and agrodealer in Laikipia is making some extra income on providing advice to others. She explained “I have been able to influence other women to join wheat farming. They contracted me to help with the farming. I charge them 1,500 Kshs (USD $11) for a farm visit, depending on the farm location.”19

Even with all the constraints, there are many women actively engaged in wheat farming and starting small businesses to serve the interests of farmers by supplying inputs, and the machinery to cultivate and harvest wheat. Various opportunities exist for both men and women to engage in enterprises that support farming, and wheat in particular due to mechanization. Leasing out the machinery for wheat cultivation is a growing business and we spoke to a number of women who were engaged in it. One woman interviewed in Narok started off as a wheat farmer and currently cultivates 20 acres. The capital she gets from wheat farming served as her “source capital for my aggregation business.”20 Taking on roles usually dominated by men can be challenging for women as one-woman agrodealer in Nyahururu explained: “There are very many challenges of being a young lady in business. And many people do not believe you can do the farming; they will always ask where my husband is.21

4.8 Wider economic benefits

Land leases as income: leasing out land can be an important income generating activity, particularly for those landholders who have land they struggle to farm productively. In pastoralist areas such as Narok and Samburu, where many landholders do not have experience in farming, leasing out land provides valuable cash and also access to crop residues for their livestock. Even medium-scale farmers will lease out land given the demand in any given year. For example, one medium-scale farmer in Narok may lease out 30% of his land depending on demand. What he charges varies by year, “in 2022, we charged 8,000 Kshs (USD $58) per acre and this year, 2023, will charge 10,000 Kshs (USD $72) per acre.”22

A woman landholder in Meru explained the benefits of leasing out her land:

I have 2 pieces of land which are in different places. I own 50 acres in Timau and 20 acres in Kiirua. I have leased out land for over 10 years and I lease it out because of the rain patterns we have experienced in this region. Land leasing is a good business, you make some money out of it. At the same time, the tenants are protecting your property.23

Wheat byproducts: the grain of wheat is not the only useful and economically important product in the wheat value chain. Wheat straw is an important commodity. In the rangelands, where pastoralists lease out their land, wheat farmers leave the straw for the landlords’ cattle. In other areas, farmers collect the straw, bale it and sell it. One farmer said that in a year when wheat prices were particularly low, he made more money from selling straw bales than wheat grain. When farmers own the land they farm for wheat, they may leave the wheat straw as crop residue on their fields to improve soil quality. In Nakuru, a small-scale woman farmer stated that “we leave the straw on the land and charge livestock owners 3,000 Ksh (USD $22) to use the straw for feed, and if they have a herd of cattle, it is 5,000 Kshs (USD $36) per acre. To livestock owners who prefer to buy straw, we charge 300ksh (USD $2) per bale.”24 The price range for straw varies greatly by location, from 90 Kshs per bale to 400 Kshs ($0.65 to $3). A large-scale farmer in Nakuru County reported that they bale and sell straw to farmers who then use it for mulching. Because they have storage capacity, they also store and sell straw when prices are higher: “Last year, straw was another cash crop. Last year was very dry, so wheat straw was marketable. I sold the wheat straw and the buyers baled themselves. I sold at 100 Kshs per bale. The money from selling straw last year enabled most farmers to have capital for farming wheat this year.”25

Wheat bran also has high value for producing animal feed. A miller explained that the profit margins in animal feed are higher than in producing flour. One miller noted that they mixed maize and wheat bran and “sell maize germ at 35 Kshs (USD $0.25) per kilo and 31 Kshs (USD $0.22) per kilo for wheat pollard.”26

4.9 Wheat’s relevance for broader rural development goals

Wheat farming has far-reaching impacts on the Kenyan economy and on individual and household livelihoods, from small-scale to large-scale farmers, to traders, to those actors who make an income from leasing land and machinery to millers. There are also many other stakeholders who rely on wheat for their livelihoods, from small-scale chapati and mandazi (donuts) makers to large-scale bread and bakery item producers and companies.

Kenyan farmers are responsive to markets and when wheat prices rise, many move quickly to enter into or expand their wheat cultivation. There is never a fear that there will be no market for wheat, even if prices rise and fall, as the demand for wheat flour and products continues to rise for urban consumers in particular (Mason et al., 2015). As wheat products are modern convenience foods, they have benefits for working urban women (who do most of the cooking) and their families. While these products may offer limited nutritional benefits in terms of micronutrients, they can offer an important source of fiber and calories.

While successful wheat farming requires capital for seeds, inputs, land leasing and machinery hire, it is also still perceived to be an “easy” crop compared to maize. Not having to hire and supervise labor is seen as a huge benefit. For women, who are more constrained for time due to domestic labor responsibilities, saving time and not having to manage labor are particularly critical (Alkire et al., 2013; Addison and Schnurr, 2016). Also, wheat is seen to be a short duration crop so farmers are able to recoup their costs (if market prices are good) and gain income in a short amount of time compared to maize. While there are undoubtedly many years where small-scale farmers barely cover the costs of production, they are still drawn to the crop as they perceive the risk to be worth it, given the potential benefits of income and the low maintenance quality of cultivation.

As wheat byproducts are important for farmers, breeding efforts should take these factors into consideration. Farmers may use crop residues to improve the organic matter of their soils, or they may or they may sell wheat straw if grain prices are low in the market, providing additional income. Both small and medium scale farmers derive extra income from straw that is sold for livestock feed, or sometimes for crop residues to apply to soils. Thus, when assessing how wheat contributes to rural livelihoods, the byproducts of the crop need also to be considered.

While smallholders contribute only a small part of overall wheat production for Kenya, engaging in wheat cultivation is clearly important for their livelihoods. It supports the growth of small businesses aimed at providing mechanization services to these farmers. So, the ripple effects on local rural economies are important. Women take a keen interest in wheat cultivation for its promise of income. Due to gender norms around land tenure, it is not easy to use their household’s land for their independent wheat cultivation. However, if they can find the capital to lease land, wheat offers them a unique opportunity due to its shorter duration and not having to hire labor. A few women we interviewed attested that cultivating wheat has allowed them to move into other enterprises such as trading and providing services to farmers.

Leasing land for wheat provides increased opportunity, and income for landholders. It also is a constraint due to the annual uncertainty about availability and cost. Improvement on leasing contracts could provide better benefits for both landholders and leasees. Improved contracts might also lead to increased numbers of farmers willing to serve as outgrowers. Improved access to seed is clearly a major hurdle to increasing production for small and medium scale farmers. Without addressing this obstacle, production is unlikely to increase.

Access to information, whether on improved seed varieties, agronomic practices or markets is almost entirely dependent on social networks. Small-scale farmers rely on each other and on large-scale farmers for access to knowledge. There is no formal mechanism for knowledge transmission, so access is more ad hoc. The lack of extension services and government support for farmers in general is felt keenly by all farmers but is most detrimental for small-scale farmers.

5 Conclusion and policy implications

5.1 Directions for policy

The challenges facing wheat production in Kenya are well known. Stem rust in Kenya has been an ongoing challenge for wheat production since the early 1900s. Mutants of the virus that causes stem rust are common in Kenya as large pathogen populations survive on wheat crops planted throughout the year, with virulence to effective major genes developing shortly after release of resistant cultivars (Fetch et al., 2021). Others have highlighted the high costs of production due to taxes, transport and lack of and cost of inputs. Access to quality seed and difficulties for small-scale farmers to access machinery are also significant challenges (Nyoro et al., 2001; Gitau et al., 2011). In their assessment of the potential for local production to substitute imported wheat, Gitau et al. (2011) noted “Inefficiencies encountered by transporters include high maintenance costs, high fuel prices, poor infrastructure (especially feeder roads connecting production areas and the markets) and roadblocks” (2019: iv). Makanda Oehmke argued that “in the absence of increasing subsidies, wheat self-sufficiency in the next 10 years is not a realistic goal for Kenya. … A realistic goal may be a four-percent annual growth rate for wheat yields, accomplished by increases in the use of non-land inputs, management skills and technical progress” (1993, p. 22).

Numerous countries across Africa have the agroclimatic conditions to produce wheat but share challenges like those in Kenya to advance production and productivity goals. In recognition of these challenges, researchers have consistently advocated for public investments to achieve wheat self-sufficiency. In response to the Russia-Ukraine war and its threat to food security across Africa, various authors argued that African countries need to expand their domestic wheat production (Mottaleb et al., 2022; Mottaleb and Govindan, 2023; Silva et al., 2023; Balma et al., 2024). Prior to the war, researchers had been calling for African countries to invest more to address low wheat productivity in the face of rising domestic demand via crop breeding and management practices (Macharia and Ngina, 2017; Tadesse et al., 2019; Zegeye et al., 2020; Shikur, 2022). Various countries (e.g., Egypt, Ethiopia, Afghanistan) have declared wheat self-sufficiency as a strategic agricultural development priority, with major investments proposed in irrigation and price supports (Abdalla et al., 2022; Senbeta and Worku, 2023; Najmuddin et al., 2021).

The calls for wheat self-sufficiently, however, ignore the complexity of wheat value chains in many African countries. Andrae and Beckman (1985, p. 145) study of wheat in Nigeria decades ago illustrates these complexities well. They describe how a variety of interests, from local millers, to importers, to the exporters of wheat from the USA have aligned to make bread the most affordable and widely available staple food in the country. While there have been efforts to increase domestic production, agroclimatic (soils, climate, water availability, etc.) and social challenges (local farmer preferences for guinea corn which is less risky) have limited expansion of wheat production. In sum,

Imported wheat cannot be substituted on any significant scale by wheat grown in Nigeria. Domestic wheat faces major natural and social constraints which reinforce each other. For wheat to grow well over wide areas, a number of technical and social preconditions must be met. The problems of establishing and maintaining these are staggering and so are the financial and social costs involved (Andrae and Beckman, 1985, p. 156).

5.2 Is self-sufficiency realistic?

Is self-sufficiency in wheat possible for Kenya? Expansion of wheat production in Kenya is certainly possible, however it will be limited by available land due to fragmentation and suitability. Given the huge and increasing demand for the crop, self-sufficiency is unlikely. Public investments in smallholder wheat production however can increase their production, and hence farmer incomes as well, if the challenges they describe can be addressed. Challenges that should and can be tackled include: addressing the lack of extension services, improving access to capital, increasing access to quality seed and inputs; building and improving storage facilities for crops. Researchers have been describing these challenges for decades (c.f. Jayne et al., 2010 for sub-Saharan Africa as a whole).

In the Government of Kenya’s new “manifesto,” termed the “Bottom Up Transformation Agenda,”27 agricultural transformation and inclusive growth are at the top of the agenda. The manifesto makes a budget pledge of Ksh.250 billion to be distributed between 2023 and 2027 towars the sector. Budgetary pledges have been made before, such as the countries who signed up to the CAADP Comprehensive African Agricultural Development Programme (CAADP) in which 10 percent of national budgets are to be designated for agriculture. Few countries have fully instituted these commitments. Ultimately, while policies to address the constraints in the wheat sector are important, they need to be implemented to be effective in improving production and the livelihoods of all actors in the wheat value chain.

It is a hopeful sign that agricultural development has such a strong focus in the government’s manifesto and budget plan. As so many countries recognize that agriculture is the “backbone” of their economies, this investment is essential. The government has focused on wheat in its Agricultural and Food Authority’s Wheat Purchase Programme that requires millers to purchase locally produced wheat before considering imports, and it has imposed a 10% duty on all imported wheat to encourage local wheat production.28 These are important measures, but they will not entirely address the constraints detailed by stakeholders in the wheat sector. The manifesto’s goals of raising productivity, improving finance, increasing extension services and decreasing reliance on imports are all essential but they will require the political will to ensure that this investment in agriculture comes to fruition.

5.3 Recommendations for improving wheat production

In short, productivity can be improved and thus farmers and all who are engaged in the wheat sector can benefit and Kenya can decrease its importation bill. A multi-pronged approach to wheat production is needed. First, wheat breeding, to produce new varieties that improve resistance to disease and pests as well as being adapted to changing climate conditions remains essential and requires investment. Next, access to quality seeds is a major bottleneck that must be addressed with urgency. Extension and finance are already in the plans, but it should be carefully targeted to where there is the greatest need. Irrigation may also provide opportunities for increased production. Another priority must be storage which is an enormous challenge for small-scale and many medium-scale farmers and significantly affects the prices they get for their grain.

While all small-scale farmers experience the same constraints, they are magnified for women whose networks and opportunities are more limited. Women farmers are clearly very interested in and benefitting from wheat production, though they face greater constraints on their time and in raising capital. These women farmers need targeted support, starting with better access to information about wheat farming, access to seeds, prices on the market, agronomic practices and of course, finance. Women farmer groups have addressed some of the constraints around access to knowledge and to inputs and capital. However, these groups are very few and increasing and/or strengthening these groups could have important benefits that extend well beyond just wheat production.

This research has demonstrated the importance of applying a broader lens to understanding the wheat sector in Kenya. It details from production to sales and milling the myriad constraints of stakeholders but also the interest and opportunities that exist. It shows the interconnectedness of all actors and how challenges for each group can affect the other. It illustrates the impacts not only on farmer incomes, but on the stakeholders that provide services and supporting enterprises for wheat farmers. It also demonstrates that wheat is not solely about the grain, but also the byproducts produced that can contribute to incomes, but also to the soils on which farmers depend. It is essential to understand these wider impacts to get the full picture of the potential of agriculture to contribute to livelihoods and reduce poverty, as well as to understand the potential for wheat in Kenya. This knowledge is central to designing policies that address specific constraints and opportunities.

Wheat is an important livelihood strategy for many farmers in Kenya, and thus an important crop for Kenya. While urban consumers may drive much food policy, it is the farmers who produce this food who need support. It is impressive what farmers in Kenya already accomplish with so little assistance. It is interesting to think about what successes they could have if they actually received targeted support in their farming.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Author contributions

KS: Conceptualization, Formal analysis, Methodology, Writing – original draft, Writing – review & editing. PM: Data curation, Formal analysis, Investigation, Writing – review & editing, Project administration. CK: Data curation, Investigation, Writing – review & editing, Formal analysis. PR: Conceptualization, Funding acquisition, Project administration, Writing – original draft, Writing – review & editing. JM: Writing – review & editing, Data curation, Investigation. FO: Data curation, Investigation, Writing – review & editing. JD: Writing – review & editing, Conceptualization, Formal analysis, Funding acquisition, Project administration, Writing – original draft.

Funding

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article. This work was funded by the Bill & Melinda Gates Foundation, Foundation for Food and Agriculture Research (FFAR), and USAID through the Accelerating Genetic Gains in Maize and Wheat (AGG) project (INV-003439) as well as the One-CGIAR initiative Seed Equal.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Generative AI statement

The author(s) declare that no Generative AI was used in the creation of this manuscript.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Author disclaimer

The views expressed here are those of the authors and do not necessarily reflect the views of the funders or associated institutions.

Footnotes

1. ^https://kippra.or.ke/russia-ukraine-conflict-and-wheat-supply-in-kenya/

2. ^15/06/2023.

3. ^15/06/2023.

4. ^16/06/2023.

5. ^19/06/2023.

6. ^20/06/2023.

7. ^07/07/2023.

8. ^15/06/2023.

9. ^20/06/2023.

10. ^https://dlca.logcluster.org/kenya-27-milling-assessment#:~:text=Kenya%20has%20about%2020%20%E2%80%93%2025,%E2809320150%20Mt%20per%20day

11. ^03/07/2023

12. ^07/07/2023

13. ^15/06/2023

14. ^16/06/2023.

15. ^15/06/2023.

16. ^15/06/2023.

17. ^16/06/2023.

18. ^16/06/2023.

19. ^15/06/2023.

20. ^10/07/2023.

21. ^15/06/2023.

22. ^16/06/2023.

23. ^21/06/2023.

24. ^21/07/2023.

25. ^16/06/2023.

26. ^21/06/2023.

27. ^http://www.parliament.go.ke/sites/default/files/2023-09/Budget%20Watch%202023_0.pdf

28. ^https://kippra.or.ke/russia-ukraine-conflict-and-wheat-supply-in-kenya/#:~:text=The%20key%20policy%20interventions%20that,the%20same%20at%20discounted%20tariffs%2C

References

Abdalla, A., Stellmacher, T., and Becker, M. (2022). Trends and prospects of change in wheat self-sufficiency in Egypt. Agriculture 13:7. doi: 10.3390/agriculture13010007

Addison, L., and Schnurr, M. (2016). Introduction to symposium on labor, gender and new sources of agrarian change. Agric. Hum. Values 33, 961–965. doi: 10.1007/s10460-015-9656-1

Alkire, S., Meinzen-Dick, R., Peterman, A., Quisumbing, A., Seymour, G., and Vaz, A. (2013). The women’s empowerment in agriculture index. World Dev. 52, 71–91. doi: 10.1016/j.worlddev.2013.06.007

Andrae, G., and Beckman, B. (1985). The wheat trap. Bread and underdevelopment in Nigeria : Cabi Digital Library.

Anteneh, A., and Asrat, D. (2020). Wheat production and marketing in Ethiopia: review study. Cogent Food Agric. 6:1778893. doi: 10.1080/23311932.2020.1778893

Balma, L., Heidland, T., Jävervall, S., Mahlkow, H., Mukasa, A. N., and Woldemichael, A. (2024). Long-run impacts of the conflict in Ukraine on grain imports and prices in Africa. Afr. Dev. Rev. 36:12745. doi: 10.1111/1467-8268.12745

Baudron, F., Ndoli, A., Habarurema, I., and Vasco Silva, J. (2019). How to increase the productivity and profitability of smallholder rainfed wheat in the eastern African highlights? Northern Rwanda as a case study. Field Crop Res. 236, 121–131. doi: 10.1016/j.fcr.2019.03.023

Biggeri, M., Burchi, F., Ciani, F., and Herrmann, R. (2018). Linking small-scale farmers to the durum wheat value chain in Ethiopia: assessing the effects on production and wellbeing. Food Policy 79, 77–91. doi: 10.1016/j.foodpol.2018.06.001

Bonilla, J. D., Coombes, A., Romney, D., and Winters, P. C. (2024). Changing the logic in agricultural extension: evidence from a demand-driven extension programme in Kenya. J. Dev. Eff. 16, 118–141. doi: 10.1080/19439342.2023.2181848

Boughton, D., and Reardon, T. (1997). Will promotion of coarse grain processing turn the tide for traditional cereals in the Sahel? Recent empirical evidence from Mali. Food Policy 22, 307–316. doi: 10.1016/S0306-9192(97)00021-3

Byerlee, D., and Morris, M. L. (1988). The political economy of wheat consumption and production with special reference to sub-Saharan Africa. Harare: Department of Agricultural Economics and Extension UZ/MSU Food Security Research in Southern Africa Project.

Demeke, M., and Di Marcantonio, F. (2019). Analysis of incentives and disincentives for wheat in Ethiopia. Gates Open Res. 3:419. doi: 10.21955/gatesopenres.1115517.1

Dorward, A., Kydd, J., Morrison, J., and Urey, I. (2004). A policy agenda for pro-poor agricultural growth. World Dev. 32, 73–89. doi: 10.1016/j.worlddev.2003.06.012

Erenstein, O., Jaleta, M., Mottaleb, K. A., Sonder, K., Donovan, J., and Braun, H. J. (2022). “Global trends in wheat production, consumption and trade” in Wheat improvement: Food security in a changing climate. eds. M. P. Reynolds and H. J. Braun (Cham: Springer International Publishing), 47–66.

Fetch, T. G., Park, R. F., Pretorius, Z. A., and Depauw, R. M. (2021). Stem rust: its history in Kenya and research to combat a global wheat threat. Can. J. Plant Pathol. 43, S275–S297.

Gabre-Madhin, Z. E. (2001). Market institutions, transaction costs, and social Capital in the Ethiopian Grain Market. Washington, DC: IFPRI.

Gebreselassie, S., Haile, M. G., and Kalkuhl, M. (2017). The wheat sector in Ethiopia: Current status and key challenges for future value chain development (ZEF working paper series 160, Center for Development Research). Bonn: University of Bonn.

Gitau, R., Mburu, S., Mathenge, M. K., and Smale, M. (2011). Trade and agricultural competitiveness for growth, food security and poverty reduction: A case of wheat and rice production in Kenya (Information provided on Tegemeo Institute of Agricultural Policy and Development, working paper series no. 45).

Grote, U., Fasse, A., Nguyen, T. T., and Erenstein, O. (2021). Food security and the dynamics of wheat and maize value chains in Africa and Asia. Front. Sust. Food Syst. 4:617009. doi: 10.3389/fsufs.2020.617009

Gumisiriza, G., Wagoire, W., and Bungutsiki, B. (1994). “Wheat production and research in Uganda: constraints and sustainability” in Developing sustainable wheat production systems: The eighth regional wheat workshop for eastern, central, and southern Africa. ed. Tanner (Addis Ababa: CIMMYT).

Jayne, T. S., Mather, D., and Mghenyi, E. (2010). Principal challenges confronting smallholder agriculture in sub-Saharan Africa. World Dev. 38, 1384–1398. doi: 10.1016/j.worlddev.2010.06.002

Kennedy, E., and Reardon, T. (1994). Shift to non-traditional grains in the diets of east and West Africa: role of women's opportunity cost of time. Food Policy 19, 45–56. doi: 10.1016/0306-9192(94)90007-8

Longmire, J., and Lugogo, J. (1989). The economics of small-scale wheat production technologies for Kenya. El Batán: CIMMYT.

Macharia, G., and Ngina, B. (2017). Wheat in Kenya: past and twenty-first century breeding. Wheat Improvement Manage. Utilization 24, 3–15. doi: 10.5772/67271

Makanda, D. W., and Oehmke, J. (1993). Promise and problem in the development of Kenya's wheat agriculture. Washington, DC: USAID.

Mason, N. M., Jayne, T. S., and Shiferaw, B. (2015). Africa's rising demand for wheat: trends, drivers, and policy implications. Dev. Policy Review 33, 581–613. doi: 10.1111/dpr.12129

Minot, N., Warner, J., Lemma, S., Kasa, L., Gashaw, A., and Rashid, S. (2015). The wheat supply chain in Ethiopia: patterns, trends, and policy options. Washington, DC: International Food Policy Research Institute (IFPRI). doi: 10.21955/gatesopenres.1115226.1

Monroy, L., Mulinge, W., and Witwer, M. (2013). Analysis of incentives and disincentives for wheat in Kenya. Rome: MAFAP, FAO.

Morris, M. L., and Byerlee, D. (1993). Narrowing the wheat gap in sub-Saharan Africa: a review of consumption and production issues. Econ. Dev. Cult. Chang. 41, 737–761. doi: 10.1086/452046

Mottaleb, K. A., and Govindan, V. (2023). How the ongoing armed conflict between Russia and Ukraine can affect the global wheat food security? Front. Food Sci. Technol. 3:1072872. doi: 10.3389/frfst.2023.1072872

Mottaleb, K. A., Kruseman, G., and Snapp, S. (2022). Potential impacts of Ukraine-Russia armed conflict on global wheat food security: a quantitative exploration. Glob. Food Sec. 35:100659. doi: 10.1016/j.gfs.2022.100659

Mwangi, V., Owuor, S., Kiteme, B., and Giger, M. (2021). Assessing smallholder Farmer's participation in the wheat value chain in north-west Mt Kenya. Front. Sust. Food Syst. 5:657744. doi: 10.3389/fsufs.2021.657744

Najmuddin, O., Qamer, F. M., Gul, H., Zhuang, W., and Zhang, F. (2021). Cropland use preferences under land, water and labour constraints—implications for wheat self-sufficiency in the Kabul River basin, Afghanistan. Food Secur. 13, 955–979. doi: 10.1007/s12571-021-01147-x

Noort, M. W. J., Renzetti, S., Linderhof, V., du Rand, G. E., Marx-Pienaar, N. J. M. M., de Kock, H. L., et al. (2022). Towards sustainable shifts to healthy diets and food security in sub-Saharan Africa with climate-resilient crops in bread-type products: a food system analysis. Food Secur. 11:135. doi: 10.3390/foods11020135

Nyoro, J. K., Wanzala, M., and Awour, T. (2001). Increasing Kenya’s agricultural competitiveness: farm level issue. Tegemeo working paper no. 4. Njoro: Egerton University.

Orr, A., Donovan, J., and Stoian, D. (2018). Smallholder value chains as complex adaptive systems: a conceptual framework. J. Agribusiness Dev. Emerg. Econ. 8, 14–33. doi: 10.1108/JADEE-03-2017-0031

Senbeta, A. F., and Worku, W. (2023). Ethiopia’s wheat production pathways to self-sufficiency through land area expansion, irrigation advance, and yield gap closure. Heliyon. 9:e20720. doi: 10.1016/j.heliyon.2023.e20720

Shiferaw, B., Negassa, A., Koo, J., Wood, J., Sonder, K., Braun, J. A., et al. (2011). Future of wheat production in sub-Saharan Africa: Analyses of the expanding gap between supply and demand and economic profitability of domestic production. Turrialba, CR: SIDALC.

Shikur, Z. H. (2022). Wheat policy, wheat yield and production in Ethiopia. Cogent Econ. Financ. 10:2079586.

Silva, J. V., Jaleta, M., Tesfaye, K., Abeyo, B., Devkota, M., Frija, A., et al. (2023). Pathways to wheat self-sufficiency in Africa. Glob. Food Sec. 37:100684. doi: 10.1016/j.gfs.2023.100684

Snapp, S. S., Blackie, M. J., and Donovan, C. (2003). Realigning research and extension to focus on farmers’ constraints and opportunities. Food Policy 28, 349–363. doi: 10.1016/j.foodpol.2003.08.002

Spielman, D. J., Byerlee, D., Alemu, D., and Kelemework, D. (2010). Policies to promote cereal intensification in Ethiopia: the search for appropriate public and private roles. Food Policy 35, 185–194. doi: 10.1016/j.foodpol.2009.12.002

Tadesse, W., Sanchez-Garcia, M., Assefa, S. G., Amri, A., Bishaw, Z., Ogbonnaya, F. C., et al. (2019). Genetic gains in wheat breeding and its role in feeding the world. Crop Breeding Genet. Genom. 1, 1–28.

Keywords: agricultural development, wheat, Kenya, yield gap, value chains, system approach

Citation: Snyder K, Muindi P, Khaemba C, Rutsaert P, Mutegi J, Omondi F and Donovan J (2025) Wheat in Kenya: toward self-sufficiency or toward broader development goals. Front. Sustain. Food Syst. 9:1532337. doi: 10.3389/fsufs.2025.1532337

Edited by:

Wenjin Long, China Agricultural University, ChinaReviewed by:

Janpriy Sharma, University of Trento, ItalySiphe Zantsi, Agricultural Research Council of South Africa (ARC-SA), South Africa

Copyright © 2025 Snyder, Muindi, Khaemba, Rutsaert, Mutegi, Omondi and Donovan. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Katherine Snyder, c255ZGVyLmthdGhlcmluZUBnbWFpbC5jb20=