Mayamiko Nathaniel Kakwera

Mayamiko Nathaniel Kakwera Daimon Kambewa2

Daimon Kambewa2 Ruth Haug

Ruth Haug- 1Department of International Environment and Development Studies, Faculty of Landscape and Society, Norwegian University of Life Sciences, Ås, Norway

- 2Extension Department, Lilongwe University of Agriculture and Natural Resources, Lilongwe, Malawi

We assess how Malawian smallholder farmers engage with legume markets in Dowa district and how these markets function to either support or hinder equitable livelihoods. The analysis is based on mixed methods, including surveying households that grow and sell soybeans, groundnuts, and common beans, farmer focus group discussions, in-depth interviews with traders and processors, and key informant interviews with market facilitatory actors. Our theoretical framework draws from food systems, equity, and farmer typology. We found that most farmers in Dowa rarely sell their legumes in the markets they perceive as lucrative namely, to large-scale traders and processors, as these markets require substantial volumes per sale and are often located far from the farms. The state-run Agricultural Development Market Corporation turned out to be ineffective. Yet, it remains the farmers’ preferred market option due to its history of adhering to floor prices and using accurate scales. Village and mobile traders are the main commodity off-takers, despite farmers reporting that they buy below the set floor prices and use inaccurate scales. In turn, the village and mobile traders face challenges in dealing with smallholder farmers, such as commodity adulteration, sparsely located farmers, and the distances travelled to gather significant volumes of commodity. Large-scale traders and processors provide village and mobile traders with the most viable offloading options. Village, district, and large-scale traders all reported declining market opportunities driven by unfavourable trade policies, which are seen to be lobbied by powerful actors in the legume supply chains; ultimately this affects how traders interact with farmers. Many smallholder farmers in the “dropping out” and “hanging in” categories are indebted and engage in advance crop sale debts, which seems to contribute towards inequity rather than equity. Despite the prevalence of market policies to protect smallholder farmers from exploitation, implementation is challenging, thus rendering market control on paper and market liberalisation in practice.

1 Introduction

In 2021, the United Nations organised a Food System Summit (UNFSS-2021) focusing on various action tracks with titles such as nourish all people (action track 1) and advance equitable livelihoods, decent work, and empowered communities (action track 4) (UNFSS, 2021). Countries were encouraged to develop country pathways to be monitored for progress every second year in UNFSS+2 + 2 events (UNFSS, 2023, 2025). The Malawian Government developed a country pathway, and for action track 4 on equitable livelihoods, systemic market failure was selected as one of three priority areas (GoM, 2021b). Following the development of the Malawian country pathway and the priority given to addressing systemic market failure, this study aims to assess how smallholder farmers, in Malawi engage with legume markets and how these markets operate to advance equitable livelihoods.

Sustainable food systems are central to achieving food and income security. However, persistent challenges undermine this potential and intensify existing inequalities, particularly among vulnerable smallholders (HLPE, 2023; CFS, 2024). Malawi’s, agri-food system is based primarily on smallholder farmers (World Bank, 2024), and has relatively high-income inequality across the food system showing a Gini coefficient of 0.45. (Matchaya and Guthiga, 2023). Malawi’s poverty rate, remained unchanged between 2010 and 2019, at 50.7 percent, with a rural poverty rate of 57 percent (Caruso et al., 2022). Smallholders in Malawi are subjected to markets that are characterised by urban-biased price controls, high transaction costs, and vulnerability to competing price effects of food aid and imports, thus exacerbating their inequitable livelihoods situations (Ochieng et al., 2020; Baulch et al., 2024). Market processes in the country thrive on informality, thus exposing smallholders to market exploitation and the subsequent capture of strategic agriproduce value chains by cartels of politicians, technocrats, and traders, both local and foreign (Chinsinga and Matita, 2021; Campenhout and Nabwire, 2022; Chitete et al., 2024; World Bank, 2024). The productivity of both farmers and small-scale traders is constrained by poor infrastructure, limited access to innovations and financing mechanisms, a lack of appropriate skilled labour and poor contract enforcement (Khonje et al., 2022; Ambler et al., 2023).

Several policies and interventions have been developed and rolled out in Malawi to address agricultural market failures, yet these attempts have achieved conflicting outcomes (Chitete et al., 2024). The interventions include setting trade standards, announcing price control measures such as export bans and floor and ceiling prices, strengthening farmer organisations, and promoting direct involvement of the state in agricultural markets through state agencies (GoM, 2016, 2021b, 2024; Banik and Chasukwa, 2019; Chinsinga et al., 2021; Chimombo et al., 2022). Structured agriproduce markets in the form of commodity exchange and warehouse receipt systems, contract farming and marketing, and collective marketing arrangements, have also been pursued (Smith, 2013; Baulch et al., 2018; Gomez and Vossenberg, 2018; Tuni et al., 2022). However, Malawi’s weak agricultural policy implementation capacity affects efforts to redress agriproduce market failures (Gomez and Vossenberg, 2018; Haug et al., 2021b; Tuni et al., 2022). For instance, price regulation enforcement is low due to budget constraints and inadequate institutional setup (Baulch and Ochieng, 2020; Duchoslav et al., 2022).

Banik and Chasukwa (2019) posit that the fragmented organisation of government ministries and departments working in the food, nutrition, and agricultural sectors in Malawi hinders the effective operationalisation of policies intended to guide these sectors. This fragmentation results in split budgets, leading to budgetary constraints, infighting, and institutional egos (Chinsinga and Cabral, 2010; Banik and Chasukwa, 2019). Other scholars emphasise the need for strong and committed leadership to ensure effective coordination and implementation of Malawi’s agri-food systems policies, especially in light of the fragmented organisational challenges facing the sector (Banik and Chasukwa, 2019). Other solutions to market failures are included in the UNFSS21 national pathway (GoM, 2021b). These suggested solutions are not new; they have existed for some time and are now part of Malawi’s national strategies for transforming its food systems (GoM, 2016) by advancing equitable livelihoods (GoM, 2021b).

In this article, we focus on legume markets to understand how they operate to advance equitable livelihoods (or not). Given their market potential, soybeans, common beans, and groundnuts were selected as the legumes of interest in this study. With low barriers to entry and increasing demand from rural and urban markets, these legumes could lead to better market opportunities amid existing supply deficits (Muoni et al., 2019; Snapp et al., 2019; Vanlauwe et al., 2019; Chinsinga and Matita, 2021).

We address the following three research questions.

a. What are the market options for different categories of legume farmers in Dowa district, Malawi and what factors determine their market option(s)?

b. How do different actors, such as smallholder farmers, small-and large scale-traders, perceive that they benefit or lose-out under the various legume marketing options?

c. To what degree and how do legume markets advance equitable livelihoods of smallholders as prioritised by the Government of Malawi in the country pathway of the UNFSS21?

We draw on food systems and equitable livelihoods theory (Huang et al., 2022; HLPE, 2023; CFS, 2024; FAO et al., 2023) and the farmer typology “dropping out” “hanging-in” and “stepping-up” adapted from Dorward et al. (2009) and Leach et al. (2020). Our main findings are that most smallholder legume farmers in Dowa do not perceive that they benefit from the market option(s) they choose and secondly, many smallholder farmers in the “dropping-out” and “hanging-in” categories are indebted due to engaging in advance crop sale, which contributes towards inequity.

2 Theorising inequitable livelihoods and farmer typology in food systems and markets

Although the concept of food system was introduced long before the United Nations Food System Summit in 2021 (UNFSS-2021), it has gained traction thereafter. FAO et al. (2021, p. 190) define food systems as follows:

Food systems encompass the entire range of actors, and their interlinked value-adding activities involved in the production, aggregation, processing, distribution, consumption, and disposal of food products. They comprise all food products that originate from crops and livestock production, forestry, fisheries, and aquaculture, as well as the broader economic, societal, and natural environments in which these diverse production systems are embedded.

Food systems embody inequalities underpinned by inequities at every component of the supply chain, observed in. These inequalities may be observed for instance, in the influence of policy and technology development in relations between actors across the supply chain, as well as return on investments (Cabral and Devereux, 2022a; HLPE, 2023; Sumberg and Thuijsman, 2024). Imbalances in power relations between diverse actors at different operational scales within food systems are presented as the underlying factors of the inequities (Leach et al., 2020; Clapp, 2021, 2023; HLPE, 2023; Sumberg and Thuijsman, 2024).

In terms of food systems, HLPE (2023, p. 8) define inequalities and inequities, respectively, as:

Inequalities are the observed differences in Food Security and Nutrition outcomes or related food systems factors (such as access to food production resources), between individuals and groups (when disaggregated by social, economic and geographical position).

Inequities are the avoidable reasons why uneven distribution exists and why disadvantages accrue systematically, based on asymmetries in social position, discrimination and power.

The concepts of inequality and inequity have attracted increased attention in research and development work that focus on food systems and food security (FAO et al., 2023). For example, the Committee on World Food Security has negotiated Policy Recommendations on reducing Inequalities in Food Security and Nutrition (CFS, 2024). A concept that binds both inequalities and inequities in food systems is equitable livelihoods, which gained emphasis following its inclusion in the UNFSS-2021.

Huang et al. (2022, p. 394) define inequitable livelihoods as:

… those with inequitable access to productive natural resources, technology and innovation, infrastructure, economic opportunities, education and public goods, financial services, healthy food, social protection and other livelihood opportunities for all people along with food systems especially smallholders, wage earners, women, youth, elderly, disabled, minority and Indigenous people also referred to as people in vulnerability.

We lean on this definition that outlines three key aspects of equitable livelihoods: access to resources, access to opportunities, and focusing on the needs of vulnerable populations.

We recognise smallholders as being vulnerable populations, as suggested by Huang et al. (2022), and adapt the definition put by CFS, p. (2024, p. 3), which defines smallholders as:

… small-scale producers and processors, pastoralists, artisans, fishers, communities closely dependent on forests, Indigenous Peoples and agricultural workers for the food system.

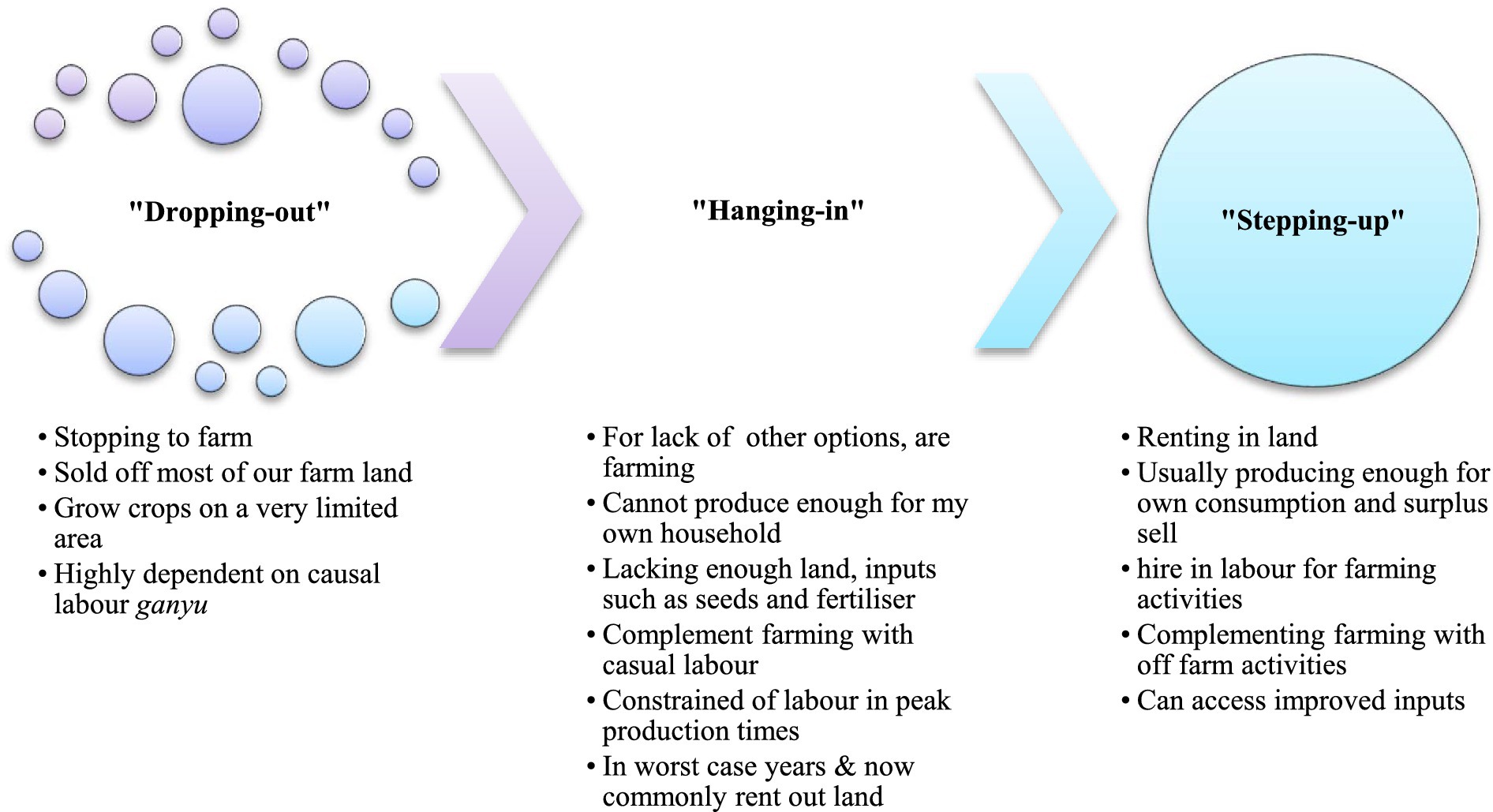

We limit the term smallholder to smallholder farmers. We treat smallholder farmers as a heterogeneous group drawing on the categories of “dropping-out,” “hanging-in,” and “stepping-up” adapting the work of Dorward et al. (2009) and Leach et al. (2020). Our category of “dropping-out” farmers is what Leach et al. (2020) call “moving-out,” referring to poor people transitioning from their current livelihood activities to pursue alternative opportunities, such as non-agricultural activities or migration. On the other hand, “hanging-in” farmers maintain their livelihood activities in challenging circumstances to sustain their well-being (Dorward et al., 2009). The “stepping-up” farmers focus on investing in assets and expanding their activities to increase production and income, thus aiming to improve their livelihoods (Dorward et al., 2009).

We operationalise inequitable livelihoods by analysing smallholders’ access to legume markets in Dowa, Malawi, in the light of the fairness of market transactions, which have described as ‘economic opportunities’ (Huang et al., 2022). Smallholders are often marginalised, and their inequitable livelihoods are aggravated by high enterprise entry costs, stringent price regulatory standards, lack of access to market information and growing market concentration in agri-produce markets (Huang et al., 2022; HLPE, 2023; CFS, 2024). In addition, commodity price volatility is another market failure, leading to income instability and vulnerability as smallholder farmers who often lack the means to hedge the price fluctuations (Chirwa et al., 2005; Campenhout and Nabwire, 2022). Some challenges fall into the category of economic and political drivers of food systems, which often preclude the smallholders from attaining equitable livelihoods by limiting their participation in beneficial agricultural trade activities (Huang et al., 2022; Neufeld et al., 2023; CFS, 2024).

To address the three research questions formulated in the introduction and based on the abovementioned theories, we examine economic and political drivers in the study context, such as agricultural commodity floor prices, regulated weighing scales, trader registration, market concentration, and enforcement mechanisms. We underline the fact that these elements have long been part of Malawi’s policy framework and, since 2021, have been re-emphasised in the UNFSS-2021 country pathway in the light of the government’s commitment to transforming food systems in order to promote equitable livelihoods (Government of Malawi, 1963; GoM, 2021b).

3 Methods

3.1 Study area

The capital city of Malawi, Lilongwe and Dowa districts were selected for conducting the fieldwork. Lilongwe was selected because it hosts large-scale traders, processors, and stakeholders who are central to legume policy-making processes, whom we identified as relevant key informants. Dowa is located north and northeast of Lilongwe, has favourable conditions for growing groundnuts, soybeans, and common beans, and is close to markets (GoM, 2017). The district is reasonably close to Lilongwe City, the hosts of most big traders and processors of the three legumes which are also the apex markets (Lifeyo, 2017; Chinsinga and Matita, 2021).

3.2 Sampling and data collection

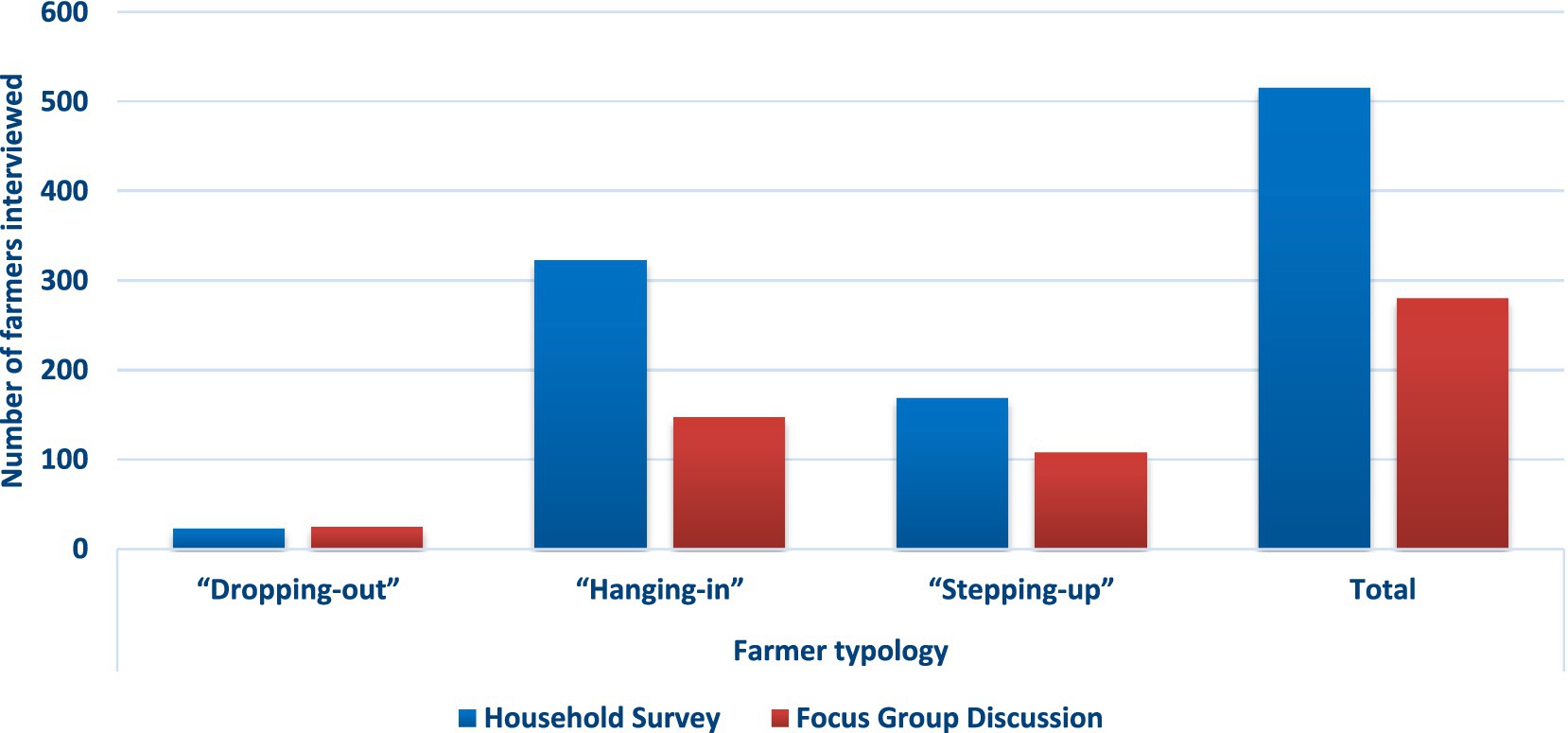

This study used mixed-methods research design. Qualitative data was collected through focus group discussions (FGDs), key informant interviews, in-depth interviews, direct observations and document reviews. Forty-eight FGDs were conducted in eight villages in Dowa district, with each village hosting six FGDs, thus three FGDs for men and women, respectively. Each FGD consisted of a minimum of four and a maximum of 16 participants. In anticipation of possible absences, 18 participants were selected from each village’s database provided by the Extension Planning Area (EPA). This resulted in 280 participants in the FGDs, including 162 women, as shown in Figure 1. The FGDs were scheduled to coincide with the legumes’ production and marketing season. The farmers interviewed through the FGD came from eight villages of Chibvala Extension Planning Area (EPA). Two villages were randomly selected from the four purposively selected sections of EPA. Chibvala EPA has 11 sections (GoM, 2017). The choice of the EPA and sections was based on reported ecological suitability for growing soybean, groundnut, and common bean (GoM, 2017).

Figure 1. Tally of farmers surveyed and interviewed in focus group discussions (Source: Farmer household survey and focus group discussions).

The study also collected data from 26 commodity traders and processors. These traders and processors highlighted marketing opportunities for farmers and other traders involved in the production and sale of soybeans, groundnuts, and common beans. Interviews were conducted with traders and processors based in Chibvala EPA, as well as those operating in nearby markets and in Lilongwe. In addition, quantitative data were collected through a survey including 515 households, as indicated in Figure 1, drawn from 44 randomly selected villages within four Chibvala EPA sections in Dowa district (the choice of EPA and sections is as earlier explained). This survey was conducted during the peak agricultural produce marketing season, from May to July 2023. Villages and households were randomly selected from a population frame specific to each section and village, following a sample size proportionate to their population. Figure 1 shows how the household survey and the focus group participants are distributed in the typologies of “dropping-out,” “hanging-in,” and “stepping-up.”

After the researchers described the options, the farmers classified themselves into one of the three typologies “dropping-out,” “hanging-in,” and “stepping-up,” and indicated the reasons that made them identify with the respective farmer typologies (see Figure 2).

Figure 2. Farmer typology in practice (Source: Authors own drawing based on results from farmer focus group discussions).

Key informants for the study were selected using purposive sampling methods, primarily through snowball techniques. Based on prior literature review, we identified key informants in Dowa and Lilongwe whose work in civil society organisations and the public and private sectors focused on agricultural commodity marketing, particularly legumes. During our engagement with these pre-identified informants, we obtained recommendations for additional informants whose expertise was relevant to the issues we explored. We ended up with 15 key informants.

Multi-stage sampling was employed to select 26 traders and processors for the study. Among them, five were large-scale traders, three were processors, eight were village traders, seven were mobile traders, and three were district traders, where five were large scale traders, three were processors, eight were village traders, seven were mobile traders and three were district traders. Village and mobile traders were chosen based on their availability in the sampled farmer villages at the time of the research. Of the 38 village traders identified during the scoping exercise, we selected 11; however, three dropped out after the first interview, so only eight participated in the study. Additionally, we randomly interviewed seven mobile traders we encountered while trading in the villages and three district traders, from nine who were found to be trading with the village and mobile traders in our study area. Furthermore, we interacted with three processors during the fieldwork and five large-scale traders, of which two were based in Dowa and three operated in Lilongwe.

Our direct observations of legume marketing actors in Dowa and Lilongwe provided detailed insights into market options, pricing, trading practices, adherence to legume trade policies, and issues regarding enforcement. We also used document reviews on policies, laws and strategies regarding Malawi’s commodity markets and agri-food system transformation. The documents reviewed were sourced from key government ministries and Bunda college library.

3.3 Data analysis

The qualitative data from the focus group discussions, key informants, and traders’ qualitative data were subjected to deductive analysis to align it with the study’s research questions and theoretical framework following Fife and Gossner (2024), and Gilgun (2015). This alignment involved the reading through the transcribed data set and in vivo coding. The qualitative data was analysed using QDA Miner Lite’s free software version. Using content analysis, the data was interpreted from the viewpoints of various legume agri-food system actors regarding how several macro-decisions are made in legume marketing, who is involved (or excluded), and who wins (or loses) regarding market options and processes for legumes. Descriptive statistics were applied to quantitative data on farmers’ agri-produce markets and prices they obtain from selling in such markets, in order to generate frequencies, means, modes and analysis of variance (ANOVA). We used Statistical Package for the Social Sciences version 22 to analyse quantitative data.

3.4 Ethical clearance

We obtained ethical clearance for the study from the Norwegian Center for Research Data (NSD) upon submission and vetting of the data management plan. Before commencing the fieldwork, permission to operate in the EPA, sections and villages was obtained from the relevant administrative officers and chiefs at the district and village levels. The study participants were briefed on the study objective, and consent was requested before commencing the interview. The data has been suitably anonymised.

4 Results

We have structured the results in three subsections based on the research questions and theory of equitable livelihoods and smallholder typology, as presented in sections 1 and 2. First is a subsection on findings of market options for legume farmers and traders, followed by results on perceptions of market processes in the different market options. The third subsection has findings on the degree to which legume markets advance equitable livelihoods of smallholders, as reflected in Action Track 4 of UNFSS21.

4.1 Smallholders’ legume marketing options

Findings on market options and smallholders’ rationale for using respective options are the core of this subsection. Most smallholder farmers in Dowa have multiple market options for selling their legumes. However, they are trading in a few market options due to limitations. We also present emergent rent-seeking behaviour and market concentration among the powerful actors at the vertical apex of the legume markets.

Nearly all farmers sell their legumes in the ‘nearby’ markets, as tracked by distances. However, such nearby markets were not the most preferred by the farmers, as indicated in Table 1. Whereby soybean farmers in the “dropping-out” category were the farthest from the market (they reported substantial distances), while “hanging-in” and “stepping-up” farmers also show high variability in distances, indicating mixed proximity. Market proximity is reportedly good for “hanging-in” and “stepping-up” groundnut farmers. Women in one of our FGDs reported that:

“Similar to men, we sell most of our legumes to door-to-door traders due to convenience, yet traders offer low prices and use larger, exploitative measuring units. Government markets1 are not timely, forcing sales to traders.” [FGD with women]

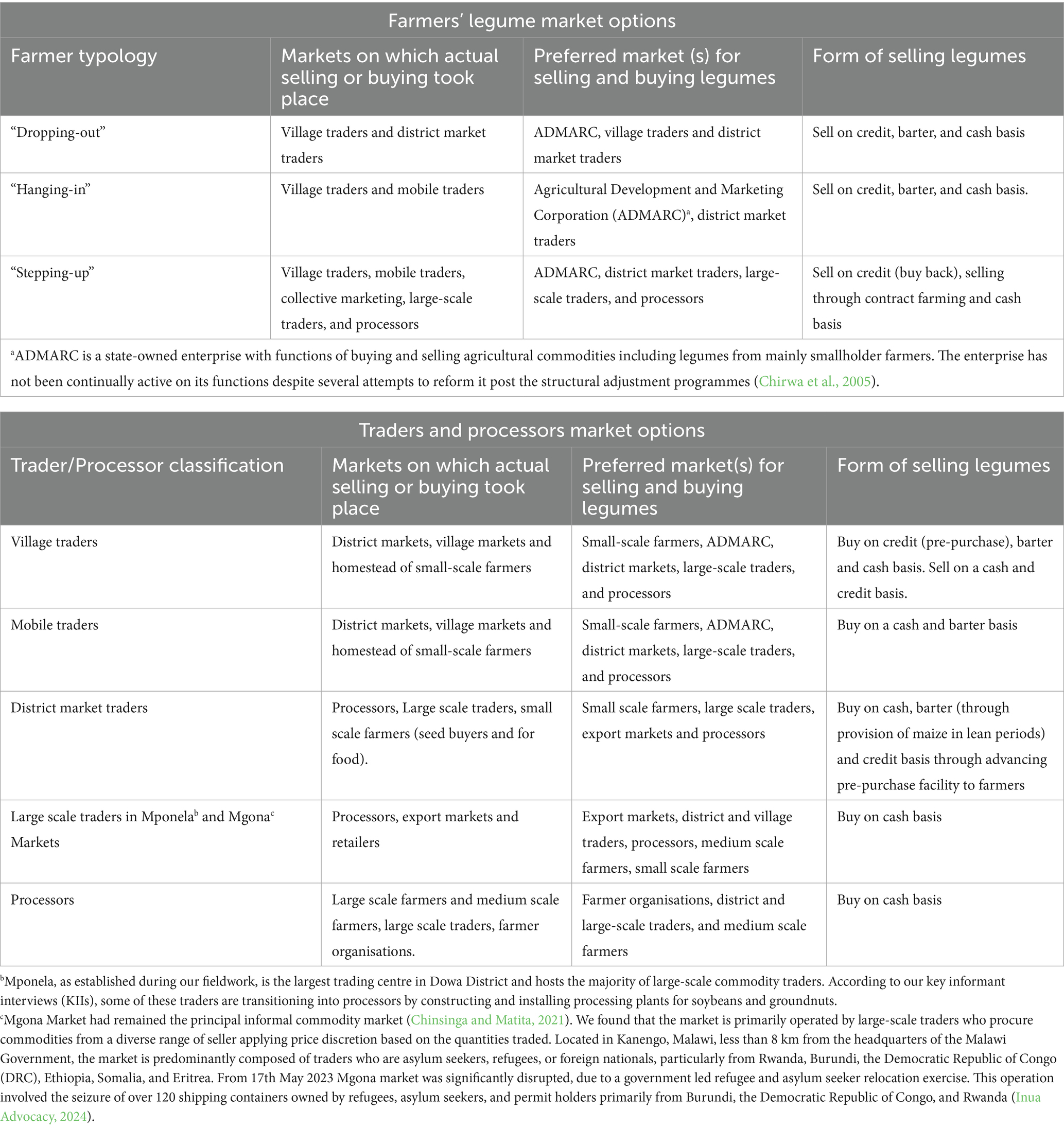

Table 1. Smallholders, traders and processors legume market options (Source: Farmer focus group discussions and In-depth interviews with traders and processors).

Nevertheless, we learned that the farmers continued to trade with village and mobile traders partly due to their limited produce volume, which deters them from investing in market search. The ‘village’ and ‘mobile traders’ operating in such convenient markets use their capital to venture into such a business and resell the aggregated commodity to large-scale traders or are outsourced by large-scale traders to buy the commodity on their behalf. Most ‘mobile’ and ‘large-scale’ traders attested to the flexibility of commodity price negotiation when approached by farmers, which is subject to significant volumes, usually if it is more than 5 tonnes and depending on the time in the market season plus the commodity flow in that market year.

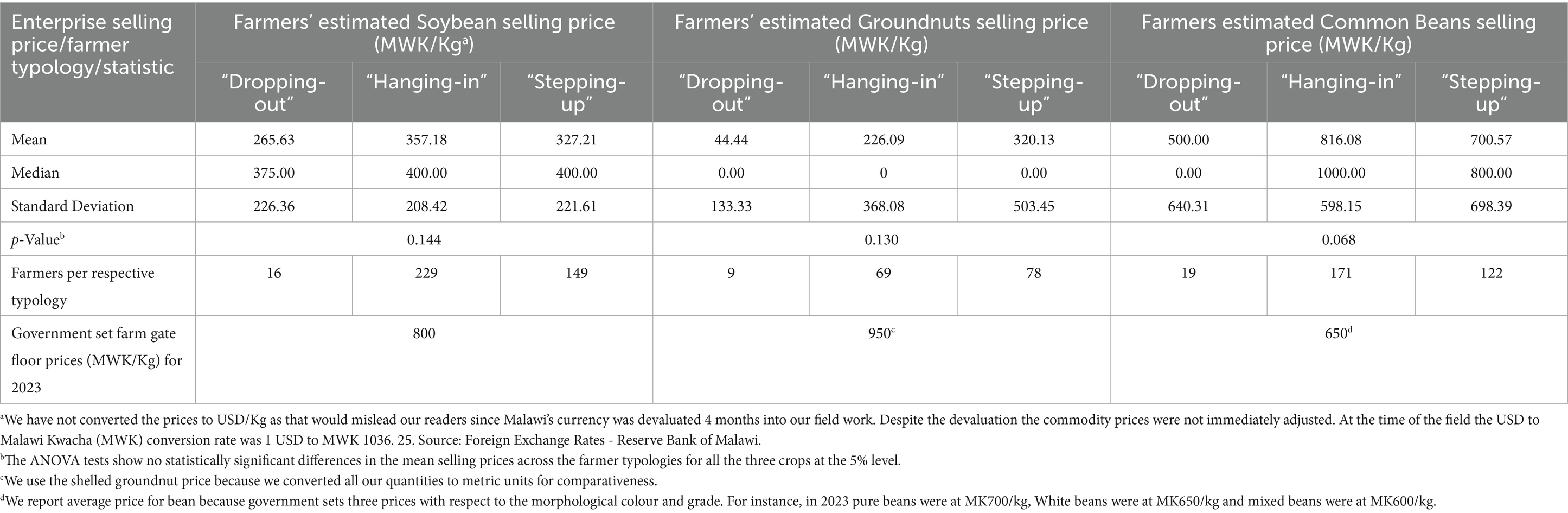

About 74 percent of the 515 surveyed farmers sold one of the three legumes, with soybeans having the most farmers (394). Besides the convenience of shorter distances, farmers who had sold their legumes reported that ‘village’ and ‘mobile traders’ usually buy their commodity at below farm gate floor prices set by the government, as shown in Table 2. Farmers unveiled that ‘mobile traders’ buy commodity using ‘unorthodox weights and measures,’ such as buckets or cups, to determine the weight or volume of the produce. The cups and buckets such traders use are at their discretion, and farmers reported having reservations about their true weight or volume calibration. Using the unstandardised measures proved challenging, as “hanging-in” soybeans and common beans reported to suspect they get lower selling prices. Farmers were also sceptical of scales used by ‘mobile’ and ‘village traders’ in that they failed to reflect the accurate measure.

“These mobile traders are using fake scales, and sometimes you wonder why they can pay relatively higher prices than those close to the district or major trading centres. I suspect they know that they will make up on the price by the much volume undermeasured by their scales.” [KII government officer 4]

Table 2. Farmer reported legume selling price [in Malawi Kwacha (MWK), where 1 United States Dollar (USD) = MWK 1036.25 at the time of the study)] for 2023 (Source: Farmer Household Survey).

Farmers expressed reservations with the re-emergence of barter trade despite their growing use, usually when dealing with mobile traders. Farmers said mobile traders exchanged cooking salt, sugar, plastic containers, cups, and cloth wrappers (also called printed cotton fabric or locally known as Chitenje) for legumes. The reservations stemmed from the lack of clear equivalent monetary value attached to such items and the men’s perceptions that it tends to lure women into trading the crops to address immediate household food and clothing needs. Beyond barter trade, it was also reported that village traders usually engage in advance sell and buy transactions, which we will return to later in this chapter when we present results on equitable livelihoods. The indicated preferred markets earned their status due to what farmers reported as better buying prices in the case of the district market traders and the assumption that floor prices and use of good weighing scales would be adhered to if Agricultural Development and Marketing Corporation (ADMARC) was to buy. As we learnt from the KIIs and FGDs ADMARC as had not operated as an off-taker market in Dowa for several years.

Selling through farmer cooperative and collective marketing arrangements buy-back schemes and forward contracts with loans was less common, as deduced from survey results. Only two groundnuts surveyed farmers had traded their crop in some collective market arrangement in the 2022/23 market season; 13 of the survey farmers had traded soybeans2 in such an arrangement. None traded their common beans in a collective market arrangement.

Farmers reported promising experiences with direct sales to agro-processors. For instance, in one group, it was revealed that upon learning about a soybean market option at a nearby large-scale agro-processor, the farmers organised themselves in one of the villages where we conducted FGDs. On inquiring with the processor and obtaining details about their bulk buying arrangements, the farmers, particularly those with more than 150 kg of soybean, pooled their produce, totalling 3.5 tonnes. They hired a vehicle to transport the produce to the processor. The farmers reported that this arrangement worked well, allowing them to achieve better returns. Unfortunately, they could not replicate this success in the 2023/24 season due to low production caused by soybean rust. The local chiefs played a leading role in this initiative.

Legume seed buy-back schemes have contributed to the rise of collective marketing arrangements. Farmers obtained seeds, particularly for soybeans and groundnuts, and reimbursed them with grain. However, farmers had reservations about the repayment conditions, as indicated in the following excerpt.

“We got seed from a farmer organisation on loan. The arrangement was to form a farmer’s club and register members of not more than twenty per club. Each member could benefit from up to 5 Kgs of seed and was required to pay back 15Kgs of grain at the end of the production season. While this arrangement availed seed to us, we had some challenges due to the amount we were supposed to pay back, which we thought was high. In some instances, farmers reported problems with germination rates of the planted seed.” [FGD with men]

In addition to paying back the seed, the companies in such arrangements also buy the farmer’s produce. While this arrangement works, the farmers reported having had challenges with it in that the companies are quick to come and collect the loan repayment but slow to buy off the commodity of the farmers, which stretches their waiting muscle. In some places, it was reported that even if companies come to buy commodities late, their prices are lower than prevailing market prices offered by traders.

“Cooperatives and contract farming have had mixed impacts. For instance, in 2018, there was an agreement with a processor to sell farmer’s soybeans at a predetermined price, but the purchase price was lower than initially agreed, leading to farmer dissatisfaction. Despite this, cooperatives can provide a sense of security and bulk selling benefit”. [KII government officer 3]

Farmers lacked operational cooperatives in their communities, as they indicated. This was reported to constrain their ability to market their produce effectively. Extension workers collaborated with farmers to highlight the lack of cooperation in the area as per our KIIs. Key informants collaborated with farmers on the fact that the main reason for established cooperatives’ limited success and subsequent collapse was inadequate pre-financing. This pre-financing would have enabled the cooperatives to buy the legumes from their members. At the same time, they (cooperatives) were taken up with searching for profitable markets, in attempting to relieve the members of financial distress; this would also maximise later profits from more lucrative markets. The established cooperatives struggled to aggregate commodities from farmers and find successful markets without the provision of pre-financing.

During the focus group discussions, farmers shared their experiences with cooperatives, including their benefits and challenges:

“Some farmers have sold through cooperatives but faced disagreements on prices. The advantage is the ability to sell larger quantities safely.” [FGD with men]

Most farmers’ experiences with cooperatives have been mixed, with benefits including bulk selling, access to quality seed, unfulfilled price promises, and lower-than-agreed prices as presented in the three excerpts from the FGDs.

“We have limited experience with cooperatives, which influences our crop choice based on the cooperative’s offerings” [FGD with women]

“In other instances, cooperatives have helped farmers by providing seeds and buying produce directly, which eliminates transportation costs and can offer better prices compared to individual sales.” [FGD with women]

“Our experiences with cooperatives have been mixed. The prices promised were not met, leading to dissatisfaction. Benefits include easier bargaining for better prices and access to certified seeds”. [FGD with men]

Regardless of not using the cooperatives, the farmers were aware that working in such arrangements could address some of their concerns about commodity prices. In one FGD, it was alluded that:

“We (Farmers) cannot negotiate with traders, who often dictate prices. Some cooperative arrangements allow for better price negotiation due to bulk selling and collective bargaining.” [FGD with men]

Traders operate at various scales with differing market options, as described in Table 1. The data shows that although all categories of traders buy from smallholder farmers, village and mobile traders interact with them the most. The distance to markets limited most smallholder farmers from trading with districts and large-scale traders operating within Dowa. For processors, indicated buying from farmers who can pool a minimum of 3.5 metric tonnes per sale. Often, only farmers organised in farmer groups were the most successful at tapping off this opportunity. While regularly buying at floor prices and above, processors are located further away from the smallholder farmers, which introduces the element of transportation and handling costs if the small-scale farmers are to sell to these processors.

Discussing with the representatives from these processors revealed that large-scale traders and district and village traders usually sell produce to them and are offered farm gate floor prices or above. The selling prices at the processors are negotiable depending on the commodity volume and scarcity, as was indicated by large-scale, district, and village traders. The village, district and large scale traders, highlighted that the price negotiations and selling commodities to processors is not all rosy. As sell negotiations sometimes involve under-the-table dealings where intermediaries (commonly called Andangwira or Mwini mgodi) hold contracts with the processors and yet without produce. Such intermediaries tend to float the contracts to large-scale district and village traders on an agreement that a percentage of the selling price will be paid to them.

The mobile and village traders also lamented the growing practice of intermediaries distorting the marketing processes in the produce business. It is based on the practices of Andangwira that the low-end trader would have preferred if ADMARC were in operation and they sold there. Asked why and how ADMARC would be their preferred market option, they hinted that perhaps the Andangwira syndrome would not prevail since ADMARC bought from across the market when it could, opening the market to many willing sellers. They also highlighted that most small-scale farmers they service in their markets may not be able to sell to ADMARC, given that when it was in operation, it could open markets later in the marketing season. By then, the farmers sold off most of their produce to these traders through advanced debt or early sales, given their limited income opportunities, which limited them to holding the produce.

We observed, and traders reported that the central large-scale soybean and groundnut market had just been affected by government enforcement of a policy that relocated refugees and asylum seekers from cities and towns of Malawi to a designated refugee camp in Dowa district.3 The enforcement coincided with the peak of the legume marketing season, where ordinarily the market season runs from March 2023. The refugees and asylum seekers ran this central agri-produce market in Lilongwe City, operated as district market traders across Malawi, and were off-takers for small-scale traders such as village and mobile traders. Interviews with these refugees and asylum seeker traders revealed that they had markets for commodities in eastern African countries and South Africa. In their absence, village traders mainly sell the aggregated commodities to the processors. In very few cases, the refugees and asylum seekers were reported and observed in front of their Malawian counterparts to operate the large-scale aggregation. However, trust issues regarding the money the refugees would advance to the Malawian counterpart limited the traded volumes.

4.2 Benefits and losing-out in the markets

This subsection addresses the second research question on perceptions of who benefits and who loses out on the various legume marketing options. We present findings on marketing practices, compliance with floor prices, and insights from farmers, traders, processors, and government officials. The results indicate weak enforcement of floor prices, trading standards, and weights used by traders in village markets. Additionally, determining floor prices is contentious, affecting various stakeholders in the legume markets.

The lack of adherence to floor prices prevails despite the prevalence of legislation empowering the Minister and Ministry of Agriculture to determine and enforce floor prices, albeit such legislation is old and not aligned with the dispersion of a liberalised market. The Ministry of Agriculture (MoA) applies the Agriculture (General Purposes) Act of 1987 (hereinafter referred to as Agriculture Act) to declare minimum (floor) buying prices for crops, including the three legumes (GoM, 1987). Through our KIs at the MoA and Civil Society Organisation (CSOs) leaders, we found that the Agriculture Act determines the establishment of minimum prices and ensures accurate weights and measures are used to safeguard farmers from being exploited through unfair prices and use of inappropriate weights, which all affect the returns and income they earn from marketing their crops. However, findings from the farmers show that, despite existing legislation, they remain exploited because the legislation is not being enforced.

A common finding across the FGDs (irrespective of participants’ gender), was that traders operating in their common markets hardly buy their produce at set floor prices (or above). Farmers also reported that some traders use inaccurate scales to weigh produce, all of which were reported to disadvantage the farmers. On enquiring as to why the farmers cannot act by refraining from selling their produce to such traders, it was said that they (the farmers) are aware that if they do not sell their commodities to the traders, they will not get any other market opportunities, and then their subsistence needs would remain pressing.

“These traders remain the only available market options in our vicinity. We cannot sell the produce elsewhere as such options don’t come easily. We have heard about better markets in Lilongwe and Lumbadzi through radio programs. However, our produce volumes are too small to benefit from such markets if we include transport costs.” [FGD with women]

The KIIs and FGDs widely acknowledged that enforcing legislation such as farm gate prices remains problematic. First, the state does not provide alternative marketing options for the farmers, so they are at the mercy of the traders and their terms of trade. The second aspect is that the state lacks a comprehensive agricultural marketing strategy that would protect farmers from exploitation, foster working relationships among agriproduce actors, and ensure compliance with the sector’s agreements, legislation, and bylaws. Our further analysis of government, development partners, and civil society funding to the agricultural sector reveals that programmes on agricultural marketing account for 3 per cent of the overall budgets (Ministry of Agriculture, 2024, p. 14).

The floor price had other issues apart from lack of enforcement. To start with, our KII from the government district office noted that the prices are usually announced late relative to when commodity trade starts. “It is now common for farmgate prices to come out when farmers have already started selling their produce,” narrated our KII. The informant also observed that, although the process requires them to calculate the gross margin annually using data from the farmers, this exercise is rarely done due to limited resources for such work at the district level.

“Minimum prices (floor prices) are set with the farmers in mind. We do this by estimating the cost of production, mainly using gross margins. The committee that sits to consolidate, consider and suggest to the Minister of Agriculture the floor farmgate price usually does that with the reflection of the farmer’s cost of production.” [KII government officer 1]

“The floor prices are supposed to inform the farmers when planning their next season’s production activities. It is insufficient for farmers to know the price they will sell their produce for that season, yet they have already produced it. These prices should help them plan. Our agribusiness section is weak to conveying out such messages to farmers. I would have loved to see farmers minimising the cost of production based on the estimated gross margins.” [KII government officer 2]

The traders’ and processors’ reservations on floor farmgate prices affect their profits and business, as the price determination process is often not aligned with regional commodity prices. They complained that this puts them off the competitive market grid in the region.

“The process (of determining floor prices) is somehow problematic because it is inward looking. We are rarely willing to discuss the estimated prices in the context of the regional and global supply of commodities, particularly when regional and global prospects indicate that prices are decreasing. We often shoot ourselves in the foot in situations where farmgate prices are set too high (for instance, soybean prices in 2023/24 production and marketing season were 200 to 250 USD higher per tonne in Malawi than in Zambia). Our farmers are left with a wrong image that they are exploited.” [KII from the Traders Association]

Large-scale traders and processors also pointed out that the floor prices the government determines overlook the realities of poor-quality crop presentation, as most farmers on the market typically present. Many large-scale traders and processors the study interfaced with have to re-dry, sort and grade the commodity before exporting or processing. This exercise was reported to cost more for the traders and processors, and they often pass the cost indirectly to small-scale traders and farmers through a lower floor price.

“We are only concerned with the quality of the produce we buy, trade and process. Look at that heap of soil we got from the produce that the small-scale traders presented. Through winnowing, we removed all that soil and other non-related materials. Yet, that was after we had paid the small-scale traders their dues in full as we buy on an as-is-basis. However, this has meant taking up transactional costs and losing time, but we have limited choices. What farmers produce is what we trade. Most of the produce we get must be rehandled to meet the quality of our markets, which is an extra cost.” [KII with trader 09]

The processors also noted that higher farmgate prices often result from inefficient farm production, which has implications for their business in the short term and the farmer’s livelihoods in the medium term, as they all need each other.

“We are asked to buy expensive products because the gross margins mask the production inefficiencies associated with our farmers. The yields in Malawi are so low that farmers would want to make up for their costs by selling expensive rather than producing more per unit area to cover their costs, making our finished product expensive if we buy raw materials at the set floor prices.” [KII with processor 01]

The civil society’s perspective on the floor farm gate price was that the determination process is often contested, prolonged and can quickly become political charged. They reported that there had been instances where prices of certain agricultural commodities were adjusted upwards and downwards after the committee’s opinion but before being officially announced, to the committee’s dismay. Additionally, CSO informants noted a discrepancy between the actual prices of common beans, which consistently remained higher than the set floor prices. They also pointed out that among the three legumes observed, soybean prices have generally been the subject of contention between processors and traders on one side and farmers and the government on the other.

“We note that farmgate prices of common beans, which equally suffer from low yields, are not contested. Yet when it comes to the marketing season, the actual prices are usually higher than the set farmgate prices. We also are aware that groundnuts are not as heavily contested as beans. Both beans and groundnuts (until 2022, when Pyxus Agriculture Limited commissioned its plant) have not been of excellent trade interest to the corporate players except in a few instances of packed beans sold by NASFAM.” [KII from civil society]

A related finding regarding soybean, a crop with corporate interest, was on lobbying for and executing export bans. Informants from civil society and traders’ representatives were worried that the Ministry of Trade often enforces export trade bans on soybeans. Such export bans are pursued at times when the prices of soybeans are higher outside Malawi. This denies the Malawian farmers an opportunity to earn a better income. The justification has usually been that this is done to protect the local livestock and cooking oil industries, as soybeans are a critical ingredient and raw material for processing feed and cooking oil. Our KIIs questioned the lobbying strategies employed by the feed and cooking oil processors as they harm the majority and benefit a few.

Government policy-makers express unwavering support for the established floor prices, which are reportedly adhered to when large-scale traders and processors buy from other traders and farmers supplying substantial quantities, but not when they buy from small-scale smallholder farmers. Their rationale, as conveyed through key informant interviews, stems from their recognition that the cost of production for these commodities is increasing. In their view, traders and processors retain more profits.

4.3 Legume markets and smallholder equitable livelihoods

In this subsection, we are presenting findings on how legume markets advance equitable livelihoods (or not), as outlined in Action Track 4 of the UN Food Systems Summit (UNFSS21). Our findings show a growing tendency of advanced debt being incurred by smallholder farmers, especially those categorised as “hanging-in.” Additionally, this section builds upon earlier presented issues of traders’ use of adulterated scales and weights in the context of equitable livelihoods for farmers.

The advanced loans discussed in our focus group sessions involve mobile and village traders providing farmers with cash and food when they are in urgent need. The farmers agree to repay these loans by pre-selling their field crops, showing the lender the crop field, providing an estimated quantity of produce, and agreeing on the repayment amount. Local chiefs and the farmers’ relatives serve as witnesses to this agreement. Based on this trust and understanding, the traders await the farmers’ delivery of the agreed-upon crop volume upon harvest. The selling farm gate price used in the agreement is typically based on the prevailing market price at the beginning of the previous marketing season. We observed that most lenders were either residents of the communities where farmers operated or had proxies in these communities to ensure that farmers did not sell their produce before repaying the loan. When it is time for harvest, lenders from outside the village come to collect their dues, often camping in the area and relying on their proxies and local leadership for support during the collection process.

These sales arrangements are reportedly typical for groundnuts and soybeans. The advance sale arrangement was reported as quite familiar among the “hanging-in” farmers. They indicated that this arrangement is used to meet their pressing needs, such as food or money for medical care or school fees during lean periods when they hardly have produced to sell or opportunities for causal labour (ganyu). Yet, in some instances, we interacted with farmers who took the advance debt in the form of pork or beef distributed in the village during the Christmas and New Year seasons.

“On Christmas Day in 2022, I borrowed 5 kilograms of pork from a village vendor, planning to repay with one twenty-litre pail of soybeans. Due to a soybean crop failure, I had to repay with maize instead, using two pails. I got the pork so my kids could have a better Christmas.” [Farmer in male FGD]

Farmers and traders faced significant challenges in the 2022/23 and 2023/24 seasons due to failed soybean production, forcing many to change their trade agreements and pay with maize instead. Some farmers even hid from mobile traders seeking repayments. Focus group discussions indicated that many households lost years of accumulated assets, with bicycles being the most seized items. In response, village chiefs intervened, postponing loan collections to the next season, acknowledging that repayment failures were due to natural disasters rather than farmers’ choices.

We observed that the advanced debt arrangement functioned without farmers considering floor prices and issues related to weights and standards. Our follow-up discussions with key informants, specifically local extension workers, revealed that they know this practice. However, they have not reflected on how the issues of floor prices, standards, and weights are being overlooked or circumvented in this context.

Some traders initially hesitated to engage with us, fearing that we were undercover police officers seeking to confiscate their unassessed and unregistered scales. When they felt more comfortable, they raised the issue that some farmers tend to soak their groundnuts, because then they weigh more. However, the practice is being curbed by the growing demand and trade for unshelled groundnuts. The prevalence of unassessed scales continues, in spite of the fact that the Government of Malawi mandates annual registration for traders involved in crop marketing – the 2022/2023 reassessment required payment of MK50,000 [$48.25]. The Malawi Bureau of Standards periodically monitors traders to ensure that they use certified scales for agricultural transactions.

Our findings reveal that in many village markets, traders purchase commodities without the requisite registration certificates and reassessed, certified scales. Nearly half of the mobile and village traders in Dowa procured produce without certified scales or trader registration, attributing their non-compliance to limited resources and time constraints associated with processing and certifying scales in Lilongwe. Beyond encountering unregistered traders and uncertified scales, we frequently observed traders purchasing soybeans and groundnuts below the stipulated floor prices. This disparity was most pronounced at the beginning of the marketing season. While price adjustments occurred as the season progressed, they were not consistently enforced.

Officials from the Ministry of Agriculture, the Ministry of Trade and Industries, and the Malawi Police Services are supposed to conduct market visits to enforce adherence to floor prices, scrutinise scale certification, and verify trader registration, in order to protect farmers from exploitation. However, on only two instances throughout our fieldwork did we observe the district officials conducting such joint operations, and word that they were coming had already spread in the marketplace before their arrival. Notably, these operations occurred at the Chimwanza and Dzaleka markets, which are not situated in deep rural areas where most small-scale farmers sell their produce. In deep rural areas, the Ministry of Agriculture employs frontline extension workers who can perform monitoring exercises. However, they are not very engaged in ensuring that the market processes are not exploitative to either farmers or traders, such as when farmers soak the groundnuts. Our inquiries with these extension workers regarding their non-enforcement of market regulations on scale and trader registration yielded the responses below.

“As a frontline extension worker, my superiors do not tell me who is and who is not a registered trader. We only hear about such and have had their scale confiscated or arrested once our superiors come for monitoring visits. I cannot recall when we got briefed on how to monitor the markets and market regulation adherence by our superiors”. [KII government officer 6].

“I would detest to work on the market issues to deal with monitoring the traders. This a business for [anthu akulu akulu] our bosses, be it in the line of duty or those that are connected to the powerful people. You can easily burn your fingers if you work against the establishments. Those that get punished are small fish.” [KII government officer 4].

As reported in-depth interviews with small-scale traders’ their livelihoods were also reported are negatively affected by terms of trade, which big players are continuously offering, and policy changes that the government is pushing, such as export bans and export mandates. According to the export mandates, the government requires all exporters of agricultural commodities to use designated warehouses if they do not have their own (GoM, 2021a). They must also declare the commodity’s destination, market, and value (GoM, 2021a). During a briefing workshop organised by the Reserve Bank of Malawi, the Ministry of Trade, and the Ministry of Agriculture in June 2023, traders expressed concerns about the execution of export mandates. They raised issues regarding conflicts of interest, particularly concerning the pre-assigned warehouses, most of which were owned by large-scale traders and processors of the commodities.

Additionally, traders were worried about the confidentiality of the market information they shared with the authorities, as some indicated that this information often ends up being shared with other traders connected to the authorities. This practice disadvantages those who invest in facilitatory market activities such as, market intelligence. As indicated in subsection 4.1 traders worried that such policies would limit their search for better prices, increase business costs, and set the bar too high to participate in the market. They indicated that this is slowly pushing-out the commodity trading business to be less lucrative for traders with low-capital.

5 Discussion

In this section, in line with the study research questions we discuss the legume market options for smallholder farmers in Dowa district, the perceived benefits and lose-outs in the legume markets, and the degree to which the legume markets enhance or equitable livelihoods (or not), as outlined in the UNFSS-2021 Action Track 4.

Legume market options for smallholder in Dowa district: Despite smallholder farmers considering several market options, in effect, nearby small-scale mobile and village traders are their primary buyers of soybeans, groundnuts, and common beans. However, these market options offer lower farmgate prices than the set floor price. Notably, farmers in the “hanging-in” and “dropping-out” categories trade in such market options. Issues of market information asymmetry and the low volumes traded by all three categories of smallholder farmers are core aspects that limit their actual market options (Kakwera et al., forthcoming; Ochieng et al., 2020). The low volumes stem from smallholders’ limited access to land for productive agriculture (Ragasa and Comstock, 2019; Giller et al., 2021), productivity-enhancing inputs and extension services (Matita et al., 2022; Benson and De Weerdt, 2023). In practice, the limited market options in practice, which reduce opportunities for better prices, exacerbate the smallholders’ poverty status (Baulch and Ochieng, 2020), and the potential of using legumes for inclusive growth (Hazell et al., 2010; Chinsinga et al., 2022).

Our findings show that legume markets are paying less than the farmers’ expectations. Manda et al. (2021) attribute the low returns to smallholder farmers’ limited use of several market options, as well as the inability to store their produce, which could ideally improve the produce price (Campenhout and Nabwire, 2022; De Weerdt et al., 2024). Increasingly, farmers are failing to sell their produce at prices that adequately cover production costs, thus exacerbating their vulnerability and limiting the role of agriculture in breaking poverty cycle (Chinsinga and Chasukwa, 2018; Benson and De Weerdt, 2023). This is also the result of the ‘selling low and buying high’ phenomenon among legume farmers (Burke et al., 2019; De Weerdt et al., 2024). The ‘selling low and buying high’ findings align with the general trend of plummeting agricultural commodity prices, when the cost of production is on the rise, thus marginalising smallholder farmers even further (Poulton et al., 2010; Giller et al., 2021).

Most “hanging-in” and “stepping-up” smallholder farmers in our study would prefer to sell to large-scale traders and processors as they offered better prices and trusted scales; however, they tend to be inaccessible. Smallholder farmers in these two categories are too vulnerable to wait for such markets to open up in the season, or to aggregate to meet volume requirements. Individually they produced volumes that are too low compared to the minimum tonnage required by such off-takers. Ochieng et al. (2020) note that in their study, only 1% of smallholder farmers and traders in Malawi whom they surveyed had access to structured and better market options. Aside from smallholder farmers’ vulnerability, Baulch et al. (2018) underlines the challenge that using structured market options and their proxies is constrained by limited storage infrastructure, and a lack of strong farmer organisations. While Chinsinga and Matita (2021) found that “stepping-up” farmers can more easily commercialise their operations, in this study we notice that this is untapped potential as shown by the use of few market options due to the limited market surplus the “stepping-up” farmers register on their farms.

Markets for soybeans and groundnuts have recently picked up following their export potential and growing commercialisation for animal feed and cooking oil (Tinsley, 2009; Khojely et al., 2018; Baulch and Jolex, 2021). The emerging market potential for legumes is not without gender disparities. We found that the feminisation of agriculture in legume supply chains remains an issue (Haug et al., 2021a), despite men taking up the decisions about which legumes to grow and the best potential markets those legumes. Despite the observed dynamics in decisions about selling legumes, women remain the primary providers of labour in legume fields (Kakwera et al., forthcoming; Tinsley, 2009; Khojely et al., 2018; Baulch and Jolex, 2021). Women farmers trade most with mobile and village traders due to the convenience of these markets. These findings relate to the structural dynamics in gender studies (Quisumbing et al., 2023), where the vicinity to markets tends to attract women, who are expected not to travel too far from their homes (Mgalamadzi et al., 2024). On the other hand, the shifts in intrahousehold dynamics regarding who makes decisions about which crops to sell highlight the fact that gender roles are not fixed and tend to change with the profitability of various the enterprises undertaken (Mgalamadzi et al., 2021; Matita et al., 2022).

Benefits and lose-outs in legume markets: Village and mobile traders and, in some cases, large-scale traders are concerned about their increasing marginalisation. Small-scale and large-scale traders, who are the immediate market options for “hanging-in” and “dropping-out” farmers, perceive that unfavourable trade policies, such as export bans and mandates (which are understood to be lobbied by powerful actors), negatively affect domestic prices. Chinsinga and Matita (2021), studying the groundnut value chain, describe this situation as the prevalence of cartels of politicians, technocrats, and traders, which limit beneficial opportunities for smallholder farmers and small-scale traders. The cartels are influential in lobbying for policies such as export bans and export mandates that limit market opportunities and prevent farmers from securing better prices, thus creating constraints throughout the supply chain (Chinsinga and Matita, 2021; Clapp, 2021, 2023).

Despite Malawi’s controlled agri-produce market regulatory framework, (which predates the 1960s), such as floor price and use of appropriate weights and standards, actual operations on the domestic scene are largely liberal in terms of floor prices, standards and weights (Government of Malawi, 1963; Duchoslav et al., 2022). Determination of farm gate floor price and adherence to it is a thorny issue among several actors, including small-scale traders, since it renders the markets open to discretionary state interventions (Goletti and Babu, 1994; Banik and Chasukwa, 2019; Duchoslav et al., 2022; Chitete et al., 2024). Traders, exporters and processors argue that farm gate floor prices usually hinder export activities and product pricing relative to products produced from neighbouring countries, as the set farm gate floor prices are higher than those in regional markets (Aragie et al., 2018). Discretionary policy interventions in agricultural markets are recorded by the World Bank (2024) as restraining their functionalism for better welfare and trade effects.

In this study, a lack of coordination was observed among key state agencies namely, the Ministry of Agriculture, the Malawi Bureau of Standards, the Malawi Police Service, and the Ministry of Trade, in enforcing farm gate floor prices, the use of certified scales, and trader registration. This issue was further compounded by organisational politics, reflected in hierarchical power dynamics between field staff and those at district and headquarters levels. Field staff often operated in fear of reprisal when apprehending traders acting against regulations and the law, particularly when they suspected those traders had connections with, or were acting on behalf of, their senior officers. Banik and Chasukwa (2019) expound on Malawi’s institutional and political deficiencies in coordinating agricultural policy matters, such as minimum farm gate prices, by highlighting that not only are the legal instruments weak, but there is also a lack of personnel to ensure enforcement. Farmers are left to bargain with traders, which often puts them at a disadvantage, given their immediate cash need (Banik and Chasukwa, 2019).

Chirwa and Chinsinga (2012) and Chinsinga et al. (2021) argue that Malawi’s agricultural policy is predominantly biased against smallholder farmers as policy tools like export bans and export mandates could be considered as mechanisms that subsidise agro-processors. On the other hand, export bans are often used to keep domestic food prices low, which, in the short run, might benefit smallholder farmers who are often net consumers (Haug and Hella, 2013; Diao et al., 2023). It is critical to consider the reported mistrust between farmers and small-scale and district traders regarding issues related to commodity trading quality, quantity, and weight is critical in addressing systematic market failures, in order to promote better welfare outcomes (Minten et al., 2017).

Degree to which the markets advance equitable food systems in practice (or not): The Malawian Government has selected systemic market failure as one of three priority areas in UNFSS-2021 Action Track 4 on enhancing equitable livelihoods (GoM, 2021b). Our finding that some smallholders are hit harder than others by market failure supports the government’s priority to address marketing in order to enhance equity. The advanced debt incurred by some farmers limits their ability to achieve equitable livelihoods, as they become indebted and often unable to escape the destructive debt spiral. With such debts owed to the better-off farmers and traders, there is a risk that failing markets, apart from driving smallholder farmers destitute, increase the concentration of power among those who are better-off, thereby exacerbating existing inequalities (Swinnen et al., 2021; Cabral and Devereux, 2022a; HLPE, 2023). The indebtedness of smallholder farmers’ needs to be reflected in the transformation of food systems, to prevent such transformation from failing them (Davis et al., 2022). This proposition aligns with Cabral and Devereux (2022b), and Huang et al. (2022) who advance calls for food system transformation with emphasis on enhancing smallholder farmers’ agency in order to deliver equitable access to markets and livelihoods. HLPE (2023) and CFS (2024) call out social inequities in the markets, observed as exploitation of vulnerable smallholder farmers (and recently small-scale traders), should be core focus of attention in delivering equitable livelihoods in food systems.

While Malawi’s Food System Summit country pathway prioritises resolving market failures to promote equitable livelihoods (GoM, 2021b), our findings from Dowa district underscore the omission of key factors for resolving the identified problems inclusively. Efforts to addressing market failure in relation to equitable livelihoods, must pay attention to the nature and structure of smallholder farmers’ indebtedness, market actor power concentration (Fanzo et al., 2024), and the accumulation of wealth through dispossession in agricultural commodity and factor markets (Anseeuw et al., 2016). Achieving equitable livelihoods is about access to resources and opportunities and focusing on the needs of vulnerable populations along food supply chains in food systems (Huang et al., 2022). Accordingly, if resolving market failures is to contribute towards equitable livelihoods for smallholder farmers and small-scale traders, the direction of market change will be critical in achieving such results.

6 Conclusion

In this article, we have assessed how smallholder farmers in Dowa engage with legume markets and how these markets operate to advance equitable livelihoods (or not). Most smallholder farmers of legumes, particularly those in the “dropping-out” and “hanging-in” categories, use mobile and village traders as their markets, due to proximity, limited volumes of produce, and the ability to enter the market relatively early in the season. These farmers tend not to sell their produce in their so-called ‘preferred’ markets, namely the state-run Agricultural Development and Marketing Corporation (ADMARC), large-scale traders, and processors. Although ADMARC has been inoperative for several years, farmers stated that ADMARC had been their desired market, since it could pay farm gate floor prices and used accurate scales, in contrast to local traders who do not necessarily align with the set floor prices, nor use the correct scales. Large-scale traders and processors, who do buy commodities at farm gate floor prices, are located far from farmers and require considerable minimum commodity volumes per transaction, all of which work to the disadvantage of most smallholder farmers who participated in this study. The low market surplus of smallholder farmers is due primarily to limited production capacity, climatic shocks, lack of functional farmers’ organisations, and pressing livelihood needs, all of which affect farmers across the three typology categories.

Traders across their respective categories perceive that their market options are limited due to unfavourable policies such as export bans and mandates. The legume marketing policy is regulated on paper but liberalised in practice, to the disadvantages of smallholder farmers. The regulatory framework governing legume marketing and markets is ineffective, marginalising, and restricting smallholders’ ability to achieve equitable livelihoods. Despite promoting legumes in Malawi’s policies to promote equitable living standards, the situation in Dowa shows that achieving the desired results is unlikely, since structural, social, and income inequalities, particularly among smallholders, limit production capacity and increase debt, especially where off-farm income options are scarce. In transforming the Malawian food system to advance equitable livelihoods, the Government of Malawi needs to move from addressing systemic market failure in policy documents to initiating action that makes a real difference in practice for smallholder farmers. That said, our conclusions are based on findings specific to the Dowa Chibvala Extension Planning Area. Due to the design of our study, the findings and conclusions are not intended to be generalised beyond this specific context.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors without undue reservation.

Ethics statement

The studies involving humans were approved by Norwegian Center for Research Data (NSD). The studies were conducted in accordance with the local legislation and institutional requirements. The participants provided their written informed consent to participate in this study.

Author contributions

MK: Conceptualization, Data curation, Formal analysis, Investigation, Methodology, Software, Validation, Visualization, Writing – original draft, Writing – review & editing. DK: Conceptualization, Investigation, Supervision, Validation, Writing – review & editing. RH: Conceptualization, Data curation, Formal analysis, Investigation, Methodology, Resources, Supervision, Validation, Visualization, Writing – review & editing.

Funding

The author(s) declare that financial support was received for the research and/or publication of this article. The Norwegian Ministry of Foreign Affairs supported this study through the Malawi Sustainable Food Systems Programme FoodMa (Grant Number MWI-19/0018).

Acknowledgments

We appreciate the comments on the rough draft manuscript by Shai André Divon, Markus Schemmer, and Lars Kåre Grimsby.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Generative AI statement

The authors declare that no Gen AI was used in the creation of this manuscript.

Any alternative text (alt text) provided alongside figures in this article has been generated by Frontiers with the support of artificial intelligence and reasonable efforts have been made to ensure accuracy, including review by the authors wherever possible. If you identify any issues, please contact us.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Footnotes

1. ^Government markets (Msika wa Boma as it was commonly called by farmers) meant the markets operated by Agricultural Market Development Corporation (ADMARC).

2. ^The low numbers of farmers trading under such arrangement for soybean, the 2022/23 production season was heavily affected by soybean rust. This fungicide significantly affected farmers’ yields and disrupted traded volumes and arrangements.

3. ^See Inua Advocacy (2024) for an account on the commodity market disruptions following Malawi government directive to relocate refugees, asylum seekers and permit holders.

References

Ambler, K., de Brauw, A., Herskowitz, S., and Pulido, C. (2023). Viewpoint: finance needs of the agricultural midstream. Food Policy 121:102530. doi: 10.1016/J.FOODPOL.2023.102530

Anseeuw, W., Jayne, T., Kachule, R., and Kotsopoulos, J. (2016). The quiet rise of medium-scale farms in Malawi. Land (Basel) 5:19. doi: 10.3390/land5030019

Aragie, E., Pauw, K., and Pernechele, V. (2018). Achieving food security and industrial development in Malawi: are export restrictions the solution? World Dev. 108, 1–15. doi: 10.1016/J.WORLDDEV.2018.03.020

Banik, D., and Chasukwa, M. (2019). The politics of hunger in an SDG era: food policy in Malawi. Food Ethics 4, 189–206. doi: 10.1007/s41055-019-00055-3

Baulch, B., Gross, A., Nkhoma Chimgonda, J., and Mtemwa, C. (2018). Commodity exchanges and warehouse receipts in Malawi: current status and their Implications for the development of structured markets. Washington DC.

Baulch, B., and Jolex, A. (2021). Mixed fortunes prices paid to soybean farmers have improved in 2021…but not those to maize farmers. 1–5. Available online at: https://www.researchgate.net/publication/354328547 (Accessed June 22, 2022).

Baulch, B., Kok, S. K., and Jolex, A. (2024). A new approach to monitoring farmer prices: method and an application to Malawi. J. Dev. Stud. 60, 874–894. doi: 10.1080/00220388.2023.2291320

Baulch, B., and Ochieng, O. D. (2020). Most Malawian maize and soybean farmers sell below official minimum farmgate prices. Project Note. doi: 10.2499/p15738coll2.133911

Benson, T., and De Weerdt, J. (2023). Employment options and challenges for rural households in Malawi. Washington, D.C. Available online at: https://ebrary.ifpri.org/utils/getfile/collection/p15738coll2/id/136607/filename/136817.pdf (Accessed February 18, 2024).

Burke, M., Bergquist, L. F., and Miguel, E. (2019). Sell low and buy high: arbitrage and local price effects in Kenyan markets. Q. J. Econ. 134, 785–842. doi: 10.1093/qje/qjy034

Cabral, L., and Devereux, S. (2022). Food equity: a pluralistic framework. doi: 10.19088/IDS.2022.083

Campenhout, B. V., and Nabwire, L. (2022). Seasonality and smallholder market participation in Malawi: A baseline report. Available online at: https://ebrary.ifpri.org/utils/getfile/collection/p15738coll2/id/136366/filename/136574.pdf (Accessed September 30, 2022).

Caruso, G. D., Sosa, C., and Marcela, L. (2022). Malawi poverty assessment: Poverty persistence in Malawi-climate shocks, low agricultural productivity and slow structural transformation Malawi. Available online at: http://documents.worldbank.org/curated/en/09992000630221525 (Accessed July 17, 2025).

CFS (2024). 50 Years of CFS: Acting together for a world free from hunger and malnutrition-CFS policy recommendations on reducing inequalities for food security and nutrition. Rome. Available at: https://www.fao.org/fileadmin/templates/cfs/Docs2324/Inequalities/Designed_Version/2025_ReducingInequalities_EN.pdf

Chimombo, M., Matita, M., Mgalamadzi, L., Chinsinga, B., Chirwa, E. W., Kaiyatsa, S., et al. (2022). Interrogating the effectiveness of farmer producer organisations in enhancing smallholder commercialisation–frontline experiences from Central Malawi. doi: 10.19088/APRA.2022.004

Chinsinga, B., and Cabral, L. (2010). The limits of decentralised governance: the case of agriculture in Malawi. Policy Brief. Available online at: www.future-agricultures.org (Accessed March 7, 2025).

Chinsinga, B., and Chasukwa, M. (2018). Agricultural policy, employment opportunities and social mobility in rural Malawi. Agrarian South J. Polit. Econ. 7, 28–50. doi: 10.1177/2277976018758077

Chinsinga, B., and Matita, M. (2021). Political economy of groundnut value chain in Malawi: its re-emergence amidst policy chaos, strategic neglect and opportunism. Brighton. doi: 10.19088/APRA.2021.010

Chinsinga, B., Matita, M., Chimombo, M., Msofi, L., Kaiyatsa, S., and Mazalale, J. (2021). Agricultural commercialisation and rural livelihoods in Malawi: a historical and contemporary agrarian inquiry. Brighton. doi: 10.19088/APRA.2021.043

Chinsinga, B., Weldeghebrael, E. H., Kelsall, T., Schulz, N., and Williams, T. P. (2022). Using political settlements analysis to explain poverty trends in Ethiopia, Malawi, Rwanda and Tanzania. World Dev. 153:105827. doi: 10.1016/J.WORLDDEV.2022.105827

Chirwa, E. W., and Chinsinga, B. (2012). The political economy of food price policy in Malawi. doi: 10.1093/acprof:oso/9780198718574.003.0007

Chirwa, E. W., Mvula, P., and Kadzandira, J. (2005). Agricultural marketing liberalisation and the plight of the poor in Malawi. Zomba. Available online at: https://www.researchgate.net/publication/228538546 (Accessed May 17, 2019).

Chitete, M. M. N., Mgomezulu, W. R., Bwanaisa, M., Damazio, C., Kaunda, R. T., and Dzanja, J. (2024). A systematic review of the performance of agricultural marketing in Malawi. J. Asian Afr. Stud. 60, 2829–2846. doi: 10.1177/00219096231224679

Clapp, J. (2021). The problem with growing corporate concentration and power in the global food system. Nat. Food 2, 404–408. doi: 10.1038/s43016-021-00297-7

Clapp, J. (2023). Concentration and crises: exploring the deep roots of vulnerability in the global industrial food system. J. Peasant Stud. 50, 1–25. doi: 10.1080/03066150.2022.2129013

Davis, B., Lipper, L., and Winters, P. (2022). Do not transform food systems on the backs of the rural poor. Food Secur. 14, 729–740. doi: 10.1007/s12571-021-01214-3

De Weerdt, J., Dillon, B., Hami, E., Campenhout, B. V., and Nabwire, L. (2024). Expecting too much, foreseeing too little? Behavioral explanations for the sell low-buy high puzzle in smallholder market participation. Washington, DC. Available at: https://massp.ifpri.info/files/2024/07/Expecting-too-much-foreseeing-too-little-Behavioral-explanations-for-the-sell-low-buy-high-puzzle-in-smallholder-market-participation.pdf (Accessed August 15, 2024).

Diao, X., Reardon, T., Kennedy, A., DeFries, R. S., Koo, J., Minten, B., et al. (2023). “The future of small farms: innovations for inclusive transformation” in Science and innovations for food systems transformation (Cham: Springer International Publishing), 191–205.

Dorward, A., Anderson, S., Bernal, Y. N., Vera, E. S., Rushton, J., Pattison, J., et al. (2009). Hanging in, stepping up and stepping out: livelihood aspirations and strategies of the poor. Dev. Pract. 19, 240–247. doi: 10.1080/09614520802689535

Duchoslav, J., Nyondo, C., Comstock, A., and Benson, T. (2022). Regulation of agricultural markets in Malawi. Strategy Support Program Policy Note 45. Available online at: https://cgspace.cgiar.org/server/api/core/bitstreams/bea9fb2b-1a08-4518-8230-ab2d5ee53db4/content (Accessed July 17, 2025).

Fanzo, J., de Steenhuijsen Piters, B., Soto-Caro, A., Saint Ville, A., Mainuddin, M., and Battersby, J. (2024). Global and local perspectives on food security and food systems. Commun. Earth Environ. 5:227. doi: 10.1038/s43247-024-01398-4