Sebastian Malte Carlsson1*

Sebastian Malte Carlsson1* Erik Hunter1

Erik Hunter1 Edona Arnesen1

Edona Arnesen1 Anne Odile Peschel2

Anne Odile Peschel2 Lennart Stein3,4

Lennart Stein3,4 Benjamin Oebel3

Benjamin Oebel3 Tobias Gaugler3Mark de Jong5

Tobias Gaugler3Mark de Jong5 John Thøgersen2

John Thøgersen2- 1Department of People and Society, Swedish University of Agricultural Sciences (SLU), Alnarp, Sweden

- 2MAPP Centre, Department of Management, Aarhus University, Aarhus, Denmark

- 3Faculty of Business Administration, Nuremberg Institute of Technology, Nuremberg, Germany

- 4Chair of Sustainability and Applied Geographie, University of Greifswald, Greifswald, Germany

- 5Southern Agriculture and Horticulture Organization (ZLTO), ‘s-Hertogenbosch, Netherlands

The global food system generates considerable negative externalities like greenhouse gas emissions, soil degradation, biodiversity loss, and labor inequities. Scholars advocate for internalizing these costs through True Cost Accounting (TCA), which reveals food’s True Price (TP) by reflecting the costs of externalities. Communicating TP to consumers via a True Price Label (TPL) has been proposed, however extant research lacks stakeholders’ insights into TPLs which are necessary for refining TCA methodology. This study explores the attitudes of nine value chain stakeholders across the EU toward supporting, adopting, and (possibly) improving True Price labeling in their organizations. Thematic analysis was used to identify stakeholder skepticism about TP calculations and price impacts as well as pragmatic solutions to mitigate externalities. Overall, the study reveals stakeholder support for TP as a policy instrument, however, more collaboration is needed between researchers and stakeholders when refining TCA methodology and TPL.

1 Introduction

The yearly costs of negative externalities from food systems have been estimated to be about 12 trillion US-dollars (FAO, 2023). These are spread over a wide range of areas in the environmental, social, and economic spheres, with examples like climate change, soil depletion, eutrophication of water sources, ecotoxicity, noise, smell, discrimination, inhumane working conditions, zoonoses, antimicrobial resistance, and unfair wealth distribution (FAO, 2023; Garnett, 2013; Hendriks et al., 2023). Transformational change needs to happen throughout the systems and at all nodes, from primary production, processing and handling to distribution and consumption. This is the focus of True Cost Accounting (TCA) (FAO, 2023; Gemmill-Herren et al., 2021; von Braun and Hendriks, 2023).

Generally, TCA is a method that assesses value chains –such as food systems– through Life Cycle Assessment (LCA), employing either product-specific or supply chain level data. By (a) quantifying and (b) monetizing externalities, such as environmental impacts, − typically absent from market prices – TCA makes them transparent (De Adelhart Toorop et al., 2023). At product level, as in this study, the damage cost approach is typically applied, assigning external costs based on the harm caused (Michalke et al., 2022). The abatement cost approach estimates prevention costs and is more commonly used at the policy level (Huang et al., 2016). TCA can serve as both an informational and decision-support tool across multiple levels: for consumers (e.g., via sustainability labeling), for supply chain actors (e.g., to target mitigation efforts and support sustainability reporting), and for policymakers [e.g., to inform fiscal measures like VAT reforms (Oebel et al., 2024) or targeted subsidies (Michalke et al., 2022)].

Mitigating negative externalities within food systems requires stakeholder awareness and positive attitudes toward sustainability actions such as internalization measures, as it will demand considerable efforts, costs and systems change. It is thus important for proponents of TCA to understand current stakeholder awareness and attitudes toward negative externality mitigation. This is a prerequisite for leveraging supportive attitudes and targeting negative attitudes with the most fitting and efficient instruments for transition, be it through policy or private business efforts. A recent suggestion for communicating true costs to end consumers in retail is adopting a comprehensive sustainability label, a True Price Label (TPL) for food (von Braun and Hendriks, 2023).

Environmental sustainability labeling has been shown to increase willingness to pay (WTP), primarily for organic labels (Bastounis et al., 2021; Shaikh et al., 2024), contingent on familiarity with the label (Sigurdsson et al., 2022). A decreasing marginal efficacy of multiple sustainability labels (such as having organic and Fairtrade labels on the same package) is well-documented (Thøgersen et al., forthcoming). However, little research has been conducted on offering a comprehensive label combining multiple sustainability aspects (Torma and Thøgersen, 2021).

Communicating information to consumers through food labeling can be complicated. Miscommunicating sustainability values confuses consumers, increasing their suspicion of greenwashing (Braga Junior et al., 2019). And the complexity of TP calculations arguably makes them susceptible to misinterpretation.

Since TP is based on the holistic framework of TCA, which considers both positive and negative externalities, a TPL could potentially encapsulate multiple sustainability dimensions, including environmental, social, and health. This could theoretically eliminate the risk of inter-label confusion for consumers, like a type of meta-labeling (Torma and Thøgersen, 2021). However, it also risks alienating consumers who are strongly concerned about a specific externality, such as animal welfare, but are generally skeptical about externalities or do not value the broader range of externality information.

Previous research on and attempts to implement TPL has mostly focused on end consumers. For example, TPL was trialed in Germany at PENNY retail stores (FAO, 2024; Semken et al., n.d.; Stein et al., 2024) and Albert Heijn in the Netherlands (True Price, 2023). To date, research on both cases has focused on consumer responses to labeling, where Michalke et al. (2022) found that the majority of customers viewed the TPL campaign positively. Most customers (94.5%) were willing to pay the true price for apples (500 g; 0.09€ TP markup), while only 33.7% were willing to pay an additional true price markup of 4.83€ for 500 g minced meat. Actual behavioral change was limited in these cases. Expert interviews conducted as part of the study viewed TPL as a useful tool for increasing awareness, but mentioned the need for systemic integration, institutional backing, and long-term consumer education to create impact.

An online experiment conducted by Taufik et al. (2023) revealed that consumer trust and purchase intention for TP increase significantly when products are perceived to offer social status and “green” value. In addition, based on two empirical studies, Wilken et al. (2024, p. 589) remarked that effective TP communication requires that “the hidden costs for the sustainable products must be lower than those for the conventional alternatives.” Moreover, based on the evaluation of a nationwide TP campaign in Germany, where costumers had to pay the TP of campaign products at checkout, Stein et al. (2024) found that 50.8% of participants noticed the TPL and 60.5% stated they would reduce their consumption of animal products when TP were implemented.

More research on attitudes toward TPL in retail is needed to help clarify potential demand and what adjustments are needed to effectively communicate TP in ways that encourage sustainable food consumption (Brumm and Fukushi, 2023; Fanzo et al., 2021; Oliver et al., 2018). Also, to promote systemic implementation and adoption of TPL, a broader range of stakeholders’ perspectives than hitherto needs to be considered, especially since TCA is a method that disrupts market practices along the whole value chain, across the food system.

The present study addresses this gap in the literature while responding to calls from, e.g., Baker et al. (2020) and De Adelhart Toorop et al. (2021) to focus more on under-researched stakeholders and their attitudes toward TPL when communicating negative externalities to end consumers and promoting sustainable consumption.

More specifically, the purpose of this study is to explore the attitudes of value chain stakeholders toward supporting, adopting, and possibly improving True Price Labeling in their organizations. In addition, we explore factors that value chain stakeholder organizations consider in the context of supporting, adopting, or suggesting improvements for TPL, including adoption barriers and normative beliefs about stakeholders they must answer to.

2 Methods

This study used in-depth “expert” (stakeholder) interviews to gather insights about food value chain stakeholders’ perceptions of “true costs,” “True Price,” and True Price Labeling. Interviews were transcribed and analyzed using thematic analysis, which was chosen for its flexibility and ability to uncover rich, detailed insights from qualitative data (Braun and Clarke, 2006).

Thematic analysis is well suited to exploring stakeholders’ nuanced perspectives on complex issues, such as calculating negative externalities and sustainability communication, allowing an in-depth exploration of the participants’ perspectives on negative externalities, TPL, and related topics. It is a commonly used method for qualitative analysis, including for the analysis of stakeholders’ perceptions (e.g., Mahadeva et al., 2024; Maity et al., 2024; Megyesi et al., 2024). Thematic analysis allows for an exploratory, inductive approach, free from pre-existing theoretical frameworks, which aligns with the overall design and execution of this study.

2.1 Data collection

Semi-structured interviews (Adeoye-Olatunde and Olenik, 2021) were conducted face-to-face or via online video calls in the participants’ preferred language. Each interview lasted 60–90 min, was recorded with consent, and subsequently transcribed. When necessary, transcripts were translated into English. Identifying information was removed to ensure confidentiality.

An interview protocol (Supplementary Appendix 1) was used to provide a framework for exploring attitudes toward TCA and TPLs and ensure that all participants had a baseline understanding of the key concepts studied (e.g., externalities, TCA, TPL). This was important since not all participants had experience with TCA or TPL. To facilitate this, participants, for example, read a detailed explanation of TCA and how externalities were conceptualized under this framework and follow up questions determined whether participants had a firm grasp of the concepts. Also, participants were shown pictures of actual TPLs that were pilot tested by retailers in Europe as a basis for discussion.

After confirming their understanding of key concepts, participants answered questions about any actions they or their organization had taken to internalize externalities, communicate externalities, and attitudes toward supporting, adopting, and/or improving a potential TP label.

2.2 Sampling and data material

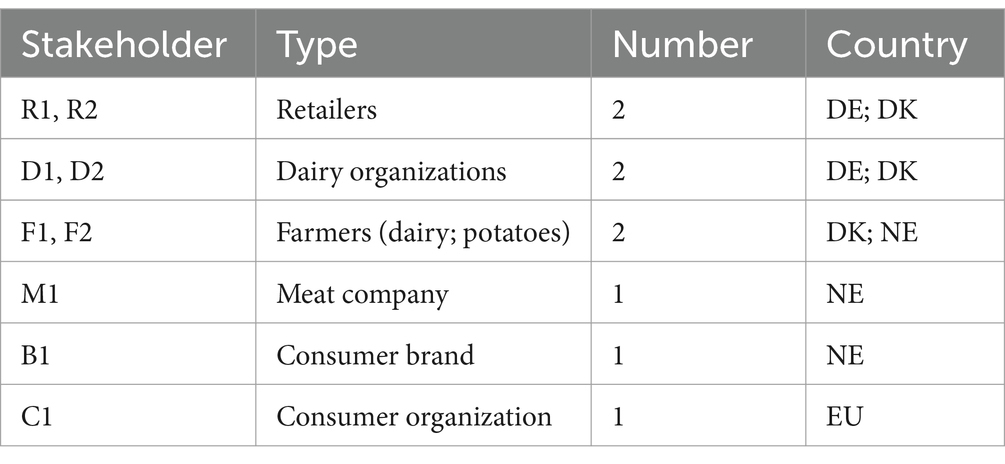

Nine semi-structured interviews were conducted with stakeholders across the European food value chain, which were selected using a purposive convenience sampling approach, drawing from the international research team’s professional networks and informant suggestions (snowballing). The goal was to include at least one informed representative from each major value chain segment—namely, production, processing, retail, and consumption—and, where possible, to engage individuals or organizations actively working with true pricing, true cost accounting, or the calculation of externalities. This was not feasible for all stakeholder categories, particularly in the Danish context. In such cases, we targeted individuals likely to be familiar with or interested in true pricing as a concept, or based on their sustainability focus and organizational mandate.

The final sample included two national retailers (see Table 1 for a summary of reference codes used to identify each participant). One (R1), based in Germany, had previously piloted pricing mechanisms aligned with the principles of true pricing, but not implemented them at scale. While this retailer’s engagement was among the more advanced in the sample, they (and others) are referred to in generalized terms to preserve anonymity. The second retailer representative (R2) represented the sustainability department of a major retail chain in Denmark. While not directly involved in true pricing, this stakeholder was engaged in broader sustainability initiatives and actively involved in discussions around labeling.

Table 1. Informants classified by stakeholder type and country.

Also two dairy organizations participated in the study. One (D1) was a German dairy cooperative involved in sustainable farming practices, though not directly applying true cost accounting methods. The second (D2) was a Danish dairy industry representative with a specialization in nutrition and public health communication, who also participates in various European-level dairy policy initiatives but not currently with true pricing.

The sample also included two farmers. The first (F1), a Danish dairy farmer, was engaged in general sustainability practices. The second (F2), a Dutch potato grower, was directly involved in true pricing initiatives. This grower participates in expert groups working on monetizing externalities and has experience implementing true pricing labels on fresh products.

In addition, the sample included a Dutch meat company (M1). While not formally applying true pricing labels, the company actively explores related concepts such as value chain transparency and true cost internalization through nature-inclusive farming, regional sourcing, and sustainability-driven procurement models. Its operational principles closely align with the goals of true pricing.

Also a Dutch consumer brand (B1) was represented in the sample. This company runs a participatory pricing model in which consumers influence product characteristics such as origin, cultivation method, and sustainability level through online surveys. Although not explicitly labeled as a true pricing initiative, the company’s approach overlaps conceptually with true cost communication and consumer-driven pricing strategies.

Finally, a representative from a European-level consumer organization (C1) was interviewed. While not currently focused on true pricing, this stakeholder represents consumer interests in the broader context of food labeling, transparency, and sustainability. Their input offered insight into how consumers might respond to true pricing labels and how such initiatives might align with EU-level policy goals.

2.3 Units of analysis

In thematic analysis, the unit of analysis is defined by the scope of the research questions and the content being examined (Braun and Clarke, 2006). For this study, the units were specified as, first, analyzed units, i.e., the complete dataset of interviews, comprising all transcripts as the primary source material for thematic analysis. Second, context units, the individual interview transcripts, ensure that the meaning of individual statements was interpreted in the broader context of the participant’s narrative. Third, registration units, which are meaningful segments of text (e.g., phrases or sentences) relevant to the study’s themes, such as statements about externalities or labeling practices.

2.4 Data analysis

First, interview transcripts were read multiple times to ensure a thorough understanding of the content and context. Following this, data segments relevant to the research questions were systematically coded. Coding was conducted inductively, allowing themes to emerge organically rather than imposed a priori. Subsequently, codes were grouped and categorized based on patterns observed across the dataset. After refining the sub-themes, eleven sub-themes remained. The sub-themes were grouped into potential main themes based on similarities. And coding was reevaluated throughout the process to ensure its fit across the whole material, following an approach where “coding continues to be developed and defined throughout the entire analysis” (Braun and Clarke, 2006, p. 87).

The identified themes were recurring ideas or issues that captured significant aspects of the data concerning the research questions. After identifying the initial themes, the transcripts were read through again and themes refined to ensure coherence within them and clear distinctions between them. This iterative process involved checking their validity against the dataset and collapsing or dividing them as needed.

Two main themes were identified, the first incorporating four sub-themes and the second the remaining seven. Each theme was defined clearly, capturing its essence and relevance to the research questions. Finally, a detailed theme analysis was conducted, linking findings to the research questions and integrating illustrative data extracts to support interpretations.

As discussed by Braun and Clarke (2006), identifying themes and sub-themes is a reiterative process. In the present study, themes and sub-themes were revised back and forth. Hence, the structure of the coding procedure was not as linear as it may seem from the above or from the write-up of the analysis.

2.5 Reliability and validation

The coding framework was reviewed iteratively to enhance reliability, and a second researcher double coded a subset of the data. Discrepancies in coding were resolved through discussion to ensure consistency. This mirrors the recommendations provided for a rigorous analysis by Braun and Clarke (2006, Table 2, p. 96): “5, Themes have been checked against each other and back to the original data. 6, Themes are internally coherent, consistent, and distinctive.” The final themes were validated by comparing the study’s findings with feedback gathered during a stakeholder workshop. While the workshop material was not systematically analyzed for this article, it provided a valuable reference point for interpreting the results.

Table 2. Sub-theme categorization.

2.6 Ethical considerations

Participants provided informed consent, and interviews were conducted in compliance with ethical guidelines for qualitative research. Data was anonymized during transcription to ensure confidentiality. Additionally, participants could withdraw their data at any stage of the study.

3 Results

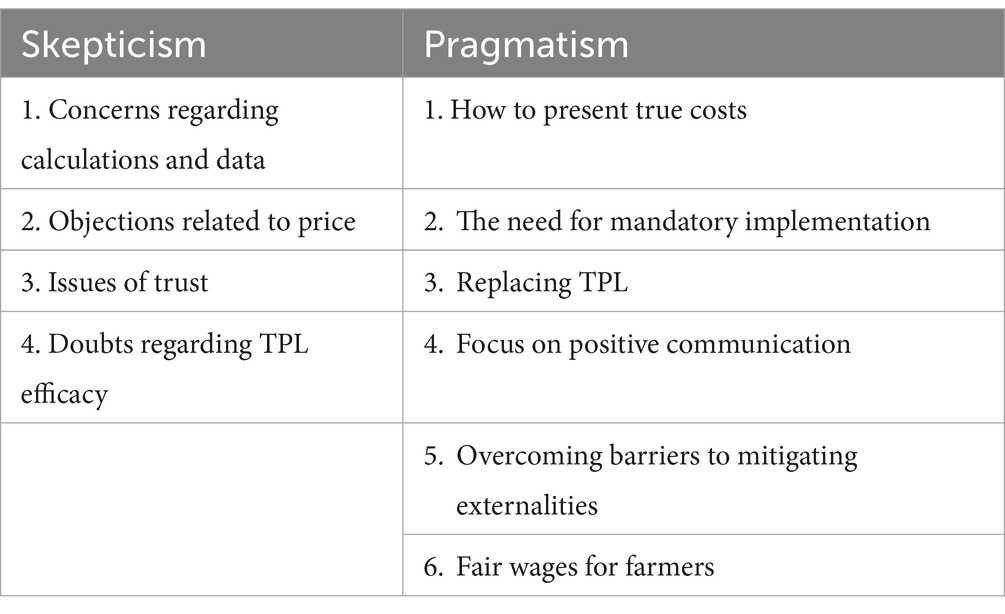

The thematic analysis (Braun and Clarke, 2006) identified two main themes, “Skepticism” and “Pragmatism.” The first main theme consists of four and the second of seven sub-themes (see Table 2).

3.1 Skepticism

Overall, the stakeholder representatives expressed a positive view of TCA’s aspirations and generally supported intentions to mitigate negative externalities within the food value chain. However, they also expressed skepticism regarding TCA that needs to be addressed if various stakeholders are to support it wholesale. This reflects the general recognition of sustainability issues within the food system as well as the need to consolidate all perspectives of, at times, conflicting opinions regarding how these issues may best be solved.

3.1.1 Concerns regarding calculations and data

Most participants expressed concerns about estimating negative externalities and emphasized the need to reach a consensus on the criteria behind the estimations. Several stakeholders also expressed uncertainty about how the estimations would be performed and how fair they would be in practice. For example, a dairy sector representative expressed worry about what they believed to be unfair comparability for concentrated versus diluted products from the same source.

We discussed this a lot regarding climate labeling: when you have a concentrated product and a diluted one, it can appear that the diluted one has a better climate impact. So, there’s some kind of imbalance when you look at it this way, and it worries me. (D1).

The point is that if a product has a negative environmental impact, it is problematic if its score can be improved simply by diluting it. This would effectively offer a loophole and reduce the incentive to improve production methods.

A representative for a Dutch consumer brand that has previously incorporated true costs into its product line mentioned the complexities involved in calculating positive health benefits, which may impact the overall balance between negative and positive externalities. They elaborated that while negative externalities are more straightforward to quantify than positive ones, producers are currently not incentivized to adopt practices that increase positive health externalities.

Retailer representatives raised the issue of mixed-ingredient products, such as frozen pizzas, where, for example, the tomato paste in a product can come from Italy or China interchangeably. This complicates calculations, and a decision has to be made on whether the monetization factor should be made up of an average of the two sources or if they should be updated according to which ingredient matches the product at a specific point in time within the production line. The German retailer representative explained the complications:

It will be challenging to arrive at a score that does not have to consist of around 5,000 individual categories. So, if you now say topics from A to Z, you have 26 categories at your disposal, and weighting will undoubtedly play a significant role. Above all, it must be transparent because your customers will have an individual weighting […] The big challenge will undoubtedly be to get a fair weighting. To say where I place the priority. (R1).

In the participant’s understanding of TCA, the “weighing of externalities” entails prioritizing different externalities where TP may include some and exclude others.

By highlighting end-consumers’ individual preferences and personal concerns, this retailer representative implies that people may care more about some externalities (e.g., water) than others (e.g., biodiversity loss). They further suggest that this necessitates full disclosure of which externalities are involved in the calculation and how their impacts on relevant dimensions of sustainability were accounted for. Only then can consumers who care especially about a specific externality, say soil health, prioritize that externality across products.

The German retailer representative argued that an exhaustive database is required to achieve the level of transparency necessary to accommodate individual weighing of externalities by stakeholders and end consumers alike. The Danish retailer representative also cautioned that the data management aspect of such products poses unrealistic expectations. The German retailer representative added that the available data would likely limit these calculations to retailer-branded articles, as they have limited access to all other articles.

These examples illustrate stakeholders’ skepticism regarding TCA’s current ability to balance negative and positive externalities and provide a just and holistic calculation of true costs.

3.1.2 Objections related to price

Another issue for data management, calculations of externalities, and the implications of internalizing true costs is the effect on the final price. The issue of price is adjacent to the above-mentioned concerns regarding calculations. However, the skepticism expressed by stakeholders here concerns the ability of TP to represent less quantifiable values fairly, rather than the method underlying the calculation of TP.

A representative of a Danish dairy association explained their reservations to TCA calculations of externalities like this:

We are disappointed that we only have to focus on the negative side here, as it may lead to more expensive products due to additional costs. But you also get something valuable in return. It’s not just an expense. (D2).

This echoes the previously mentioned concern of balancing positive and negative externalities. Stakeholders who are expected to adopt new practices conducive to mitigating, for example, climate change and public health decline, are worried that the TCA framework glosses over less tangible, yet positive externalities produced by their products.

A representative from a Dutch meat company exemplified positive externalities that can add value to a product in ways that are hard to monetize, referring to the commonly held image of the Dutch rural landscape as one filled with grazing ruminants:

Well, we believe that the rural country has to be occupied by cattle, by beef, because that’s part of Holland and if you do not have them anymore, then all rural areas are so changed it is not Holland anymore. (M1).

The stakeholder portrays this national image as enforcing positive values and social cohesion within the country. Needless to say, the preservation of such national imagery is in the interest of the meat company since its business model depends on cattle demands.

The same meat company representative also mentioned the lack of a standard definition of “nature.” They argued that the nature concept holds very different intrinsic value for a Londoner than for a rural Dutch person, which could affect whether and how maintaining grazing cows in the countryside is a positive externality.

There is some confusion regarding the intended outcome of true cost calculations, as evidenced by the European consumer organization representative:

Sometimes, I get confused between True Cost Accounting and true pricing because if the goal is to raise the price to the true price, there could be some backlash. (C1).

They argue that it would be paramount to share the true costs evenly along the food value chain, as prices would otherwise surpass what most consumers could afford.

The issue of TP’s effect on the final price and what intangible values may be lost in its implementation creates skepticism among some stakeholders regarding TCA’s alignment with their values. The uncertainty about who will pay the additional costs inferred by the true cost calculations further suggests worry about TP’s impact. This uncertainty could also be an issue of trust. Still, throughout the interview, the consumer organization representative expressed overall support for TCA and believed price is an effective lever for driving sustainable consumption. However, as a consumer organization, their focus is on consumer risks.

3.1.3 Issues of trust

Distrust in the TCA approach to mitigating externalities is another example of the skepticism hindering the internalization of negative externalities. Various expressions of mistrust surfaced from stakeholders. The most antagonistic expression to the widespread implementation of TCA came from a Danish farmer:

Well, I personally do not trust such scales because one would have to delve into what underlies the costs and how they are assigned. As a consumer, I would not trust that they are accurate, and I would not trust them myself. (F1).

This general distrust in calculating all externalities fairly may be due to a lack of insight into TCA methodologies. For example, a Dutch meat producer raised the question whether the salary to the farmer in a TCA calculation of true costs was financially sustainable.

3.1.4 Doubts regarding TPL effectiveness

TPL’s effectiveness for changing consumer choices toward more sustainable food in the supermarket was questioned by several stakeholder representatives. A representative from a Danish retailer said:

Something entirely different is needed if you want this to impact the end consumer’s choice of products, and that’s ultimately what we want. I think that requires different means than labeling. (R2).

This assessment refers to a voluntary TPL that is applied as information only without changing the product’s price. The retailer representative expressed that such information would not be effective at nudging consumers toward products with fewer externalities and would only make them feel guilty.

Despite labels generally being considered practical tools for communicating specific values, participants did not have much faith in true costs and/or True Price being communicated successfully through labeling. Some participants say the underlying framework is too complex for the average consumer. A Dutch meat company representative had the following critique of sustainability labels in general:

I do not know if [consumers] really want communication, but they are getting forced to read information. As a result, we are making the customers quite lazy […] There’s a certain label on it [then it] should be okay […] If there’s a label, everyone can say, “We are doing a good job because we are buying and selling certified products.” (M1).

This illustrates skepticism regarding customers’ ability to absorb complex information in a supermarket context. Calling consumers “lazy” implies that their consumption decisions are understood more as habits than as ideologically motivated. Also, labels are not believed to evoke personal reflections by the consumer. Once inside the supermarket, nothing other than price steers their purchase choice, and labels are taken at face value without further investigation or reflection.

3.1.5 Skepticism wrap up

Overall, stakeholder skepticism expressed in these interviews centers around concerns about TCA’s ability to be holistic and represent all externalities. Additionally, these stakeholders are not convinced that TP will do justice to less tangible or non-quantifiable values that are important to the general public. Concerns about potential price increases and mistrust in TP calculations regarding transparency for consumers and farmers also emerged. Finally, some express skepticism about TPL’s capability to shift consumption from products with high to those with low externalities. These views were expressed on the backcloth of a general recognition of sustainability issues within the food system. They also provide insight into the, at times, conflicting opinions that need consolidation if a holistic solution is to be achieved.

3.2 Pragmatism

In this section, stakeholder perceptions of negative externalities and TPL’s potential as a tool for communicating true costs are presented from the angle of pragmatism. Pragmatism is here used as a contrast to skepticism, not as a linguistic opposite but as a different approach. The participants expressed varying beliefs about whether a TPL could help the internalization of negative externalities in a retail context. When they expressed perspectives categorized as examples of pragmatism, it conveyed a sense of opportunity and potential for TCA to positively impact sustainable development while also indicating viable remedies to flaws inherent to TPL.

3.2.1 How to present true costs

Many participants suggested consumers are already fatigued by information outside and inside the supermarket. Therefore, the only way to convey information effectively is through simple communication. Many were positively inclined toward labels that incorporate the ideas behind the Eco-Score label (Supplementary Appendix 2). Some proposed a condensed version of Eco-Score, Nutri-Score (a label designed similarly to Eco-Score with categories ranging from A to E based on nutritional values), and a True Price Label (TPL) that aggregates values from all three into one single score while realizing that such a label requires transparency, trust, and data availability.

A Danish retailer representative believed that the methods underlying TCA are too complicated for consumers to understand and consider when choosing between products. “We can barely handle percentage calculations or adding or subtracting sales tax as ordinary customers” (R2). Instead, they suggested focusing on a product’s general impact rather than calculating precise costs.

A Danish dairy association representative had this experience to add:

In the context of climate labeling, we have invested significant effort into understanding what information consumers can comprehend and retain. We want to avoid making it so complicated that people abandon it and revert to their usual choices. If that occurs, then we have failed in our communication. (D2).

Together, these two statements caution the need for care when designing and implementing TPL. If the label is too dense or complex to understand, consumer behavior may be unaffected.

Multiple stakeholder representatives championed the idea of making the TCA methodology and all the relevant measurements and data points included to arrive at the score on the label transparent to everyone by making it available online. For example, calculations and explanations that are too complex for the actual label could be easily accessible via a QR code. A German retailer representative explains the appeal of such a solution:

Experience also shows that customers are no longer willing to deal with this. The packaging is often too small unless I use mini fonts, such as 3 or 6 points. This information can be easily displayed online through a barcode or a link. Otherwise, the customer is not interested in that. (R1).

This solves the issues of overcomplication and full disclosure. It also reduces the need for consumers to familiarize themselves with new concepts and ideas while shopping for groceries.

3.2.2 The need for mandatory implementation

An aspect of TPL of great concern for the participants was the degree to which it offers fair comparability between products. It is not entirely clear if an aggregated TPL score would enhance comparability. The European consumer organization representative described their concern surrounding a condensed version of a nutritional and environmental score:

[One business] will score well on a certain dimension but poorly on another. But if everything is averaged and aggregated, at the end of the day […] we could find eggs on the markets regardless of the production method, free range, barn, etc. They will all have the same score, so it does not provide any information to consumers at the end of the day. (C1).

The primary benefit of an aggregated label is its visual appeal and the easily digestible information provided by an average score. However, in some product segments, an average score can create a dilemma as it may obscure the varying weights of externalities perceived by different constituents.

The German retailer representative argued that a voluntary TPL could offer consumers transparency in production. Still, it risks effectively discriminating against the labeled products, as the non-labeled products are likely to be worse. Therefore, they would prefer mandatory labeling.

The Danish retailer representative added weight to this argument by stating that if labels are voluntary, brands with the lowest ranking refrain from adopting them. This leads to the perceived lowest rank available being the second lowest or higher, potentially decreasing preference for those brands compared to the non-labeled.

I cannot imagine introducing this as a voluntary label solely for our own brand products, as that would stigmatize our items, leading consumers to opt for unlabeled products to avoid the guilt associated with the labeling. For this to be effective, it needs to be mandatory for all products, period! Otherwise, we would have no interest in implementing it. (R2).

This statement poignantly illustrates a prevalent view among the participating stakeholders: mandating TPL is required to make it fair and comparable. According to them, TPL must be mandatory for production methods to change and for consumers to shift toward food products with fewer negative externalities.

Information campaigns to raise general awareness of the TP issue are considered a promising approach. The consumer organization representative supported TPL because they supported the idea that market prices should be TP. Still, they were not convinced that TPL would be the best way to achieve this:

I think it could be interesting from an awareness perspective. Perhaps we aren’t ready to shift from one product to another, but if it is accompanied by a large information campaign to raise consumer awareness that the price in the supermarket does not reflect the true value costs. (C1).

The representative of the Danish dairy association expressed concern about being associated with greenwashing, stating that the unclear regulations surrounding sustainability communication cause businesses to avoid taking an official stance on these issues.

Discussing sustainability is a challenging area […] No one wants to take risks with their communication, given the unclear regulations and rules. (D2).

If consumers prefer clear and positive communication from producers about the food they buy, the complex nature of negative externalities in food production makes it challenging to meet these preferences. Additionally, businesses may feel discouraged from sharing the environmental benefits of their products because they risk being accused of greenwashing.

A representative from a Dutch consumer brand suggested this as another reason for making TPL mandatory. It could help protect against accusations of greenwashing. If it were widely enforced, all parties would be required to adopt TPL, pre-empting any accusation of greenwashing marketing tactics.

The representative of the German dairy association also emphasized the benefits of universally mandating TPL. They called for trade agreements to limit the ability of countries with lax regulations to compete with European brands that follow stricter standards. “It’s simply not feasible for Brazil to clear forests, produce beef and soy, and then [export] it to Europe without consequences” (D1).

The desired scope of such a mandate varied between stakeholders. The most extreme view was that it should be cross-sectorial (e.g., TP for air travel should be implemented simultaneously with TP for food products). A more lenient view advocated a mandate across all food products in retail.

3.2.3 Replacing TPL

The Dutch meat company’s skepticism toward TPL extended to food labels in general. Their alternative solution to ensure a product’s commitment to mitigating negative externalities was a stronger attachment to brands and brand accountability. They argued that if brands were held to a higher standard of accountability, people could pick and choose more easily in supermarkets without needing as much or as advanced an understanding of calculations or even externalities per se. Hence, labels would be superfluous if brands were truly responsible for their practices, according to this view.

3.2.4 Focus on positive communication

Some stakeholders objected to the focus on negative externalities in true cost or TP communication because they were ignorant of less tangible, positive externalities. Others argued for a focus on positive externalities for pragmatic reasons.

Some believed that consumers are willing to pay a higher price when positive impacts from production are communicated, compared to competitor products that do not. For example, a Danish retailer representative mentioned that they only state that their products have the “strictest pesticide requirements in the market,” because going into detail about how many requirements exist on other products would deter consumers. The Danish dairy farmer representative further expressed a desire for positive communication:

From my experience and understanding, I believe customers prefer concrete examples. For instance, mentioning that we have phased out soy communicates our commitment better than simply stating we have become greener […] Similarly, highlighting that our cows are on pasture […] or that we dedicate a portion of our land to nature instead of just agricultural production resonates more with them. These specific actions are what I believe connect with customers. (F1).

The farmer representative further suggested providing imagery that consumers can more easily relate to and understand on a fundamental level. By promoting a tangible result like “cows out on pasture,” the consumer might not receive a receipt detailing the measurable benefits his or her purchase contributes to the environment. Still, through their consumption, they actively partake in actions that evoke emotional connections to the product and the means of production. If this truly “resonates with the customers,” they may be more successfully nudged toward choosing this product over others.

The Danish retailer representative further emphasized their stance against “negative labeling” by stating that if the TPLs were not expressed in positive terms, they would not be adopted in their supermarkets. These examples illustrate the widely held opinion among the participants that communicating positive outcomes of TPL is necessary for its acceptance on the market.

3.2.5 Overcoming barriers to mitigating externalities

The Dutch meat company representative considered the dominance of supermarkets, which exert disproportionate control over the value chain, a fundamental obstacle to widespread change in today’s food system. They claimed that, at the end of the day, retailers decide on the price, which sets the course for the rest of the chain. If retailers do not take responsibility and action, nothing will change meaningfully, so pressure should be put on them.

The retailer representatives admitted that implementing TCA on a voluntary, full-scale basis would be practically insurmountable. According to the German representative, “leaving aside the legal framework, … the costs would be immense because we have a huge number of articles” (R1).

From the retailers’ perspective, consumers are unwilling or unable to pay the extra cost of mitigating negative externalities. They also rebut the claim that action should start with them by stating that they have little to no access to data upstream by any other means than through auditing their suppliers, which is not deemed ideal. The primary levers were instead identified as price and packaging, which are concurrently being explored.

According to the German retailer representative, a pragmatic problem is that food accounts for such a small proportion of the disposable income of most European households. They believe that food has become so cheap because consumers value low prices above all other criteria:

Actually, food needs to become significantly more expensive […] the amount spent on food is notoriously low in Germany […] A change is needed at the end of the day. (R1).

From this perspective, consumers must adjust their spending on other goods, such as entertainment, leisure, and transport, to make up for the price increase necessary to adjust all levers along the food value chain contributing to the negative externalities. Hence, they imply that the costs of externalities will increase the consumer’s price.

The Dutch meat company representative explicitly stated that the food sector should be linked to other sectors, demanding trans-sectorial comparability in externality calculations:

It’s always the beef that’s under attack by the NGOs […], but OK, we also have the airports, the planes, etc. […] What will we do about those? Maybe they are not as polluting as our farmer […], but still, he needs to pay a bit. But when we have an equal costing method […] I will agree on that. (M1).

In this quote, the Dutch meat company representative expressed a sense of injustice in the pressure to mitigate negative externalities. An injustice that could be alleviated if all sectors were held to the same expectations and methods of calculating their true costs.

3.2.6 Target audience

A final example of stakeholder pragmatism is their advocating fair pricing for farmers. According to the Dutch consumer brand representative, this is the most promising lever for mitigating negative externalities. They proposed a knock-on effect relating to two issues: involving citizens in information about food production (including transparency regarding negative externalities in their production) and then charging prices that ensure financial sustainability for their farmers. The underlying rationale is that informed consumers who pay fair prices will create incentives and opportunities for farmers to modify their production methods toward alternative approaches that produce fewer negative externalities.

The Dutch meat company representative concurred but added nuances by suggesting that there might be a way for farmers to benefit directly, and preferably financially, from choosing, for example, extensive over intensive cattle farming. In their experience, farmers are left with rising costs and diminishing returns when choosing sustainability within their production, and the only real profit is made by the retailers and the landowners renting out land for grazing. They suggest that farmers should be rewarded for choosing sustainable practices rather than being expected to do so, regardless of the impact it has on their income.

The Danish retailer representative attacked the issue from the opposite side by emphasizing the misplaced focus on consumers:

I think it’s the wrong target audience. It’s not the consumer who needs to know this. The policymakers can change it for us or work with us, right? […] What I’m saying is that as a customer, why should I be burdened with something that I cannot change anyway, and why should it create guilt in the buying situation? We have no interest in burdening our customers with that. (R2).

This highlights the participating stakeholders’ fundamental objections to TPL as a tool for mitigating negative externalities by communicating true costs to end consumers. If presented to consumers in a supermarket context, aiming to change their purchase patterns, TPL is not believed to impact the internalization of externalities positively. According to the Danish retailer representative, it would only create an unwarranted sense of guilt for the customer.

The interviewed stakeholders generally believed that the only way TPL could effectively increase the internalization of negative externalities was through governments enforcing it. If TPL were voluntary in supermarkets, it would be limited to raising awareness. The Dutch meat company representative assumed a lack of knowledge by the general consumer:

We have to tell the people what happens and what they must do to get a proper piece of meat on the table. I think politics will play a major role in this, and I think communication must change. (F1).

In other words, governments need to change the narrative around food. Otherwise, business as usual will prevail. The German retailer representative concurred:

It must be solved at the EU level (…). We do not have much time left, which would require that a completely different domestic policy prevails in the EU. (R1).

The same retailer representative also suggested that new policies attempting to advance a food system transformation agenda must implement a sufficient transition period for businesses to adjust.

3.2.7 Pragmatism wrap up

These examples illustrate stakeholders’ advocacy for using TCA primarily to influence governments, rather than consumers, including securing fair pricing for farmers and changing the narrative around food by raising awareness of food system externalities.

4 Discussion

The stakeholder skepticism uncovered in this study reveals an apparent gap in the communication between TCA experts and food value chain stakeholders. First, the expressed doubts about TCA’s ability to capture externalities holistically and thereby fairly represent less tangible positive externalities, suggest a need for clearer communication of calculation criteria and more transparency about the underlying evaluations of externalities. Attempts to address positive externalities are not unique to TCA, and it remains to be seen if nascent approaches, e.g., Sustainable Performance Accounting (Walkiewicz et al., 2021), will be effective at internalizing positive externalities.

The stakeholder representatives interviewed for this study appear generally underinformed about the details of the TCA methodology, which is probably one of the reasons why they are skeptical about the proclaimed holistic nature of the externality calculations. This observation supports calls for harmonization of TCA methodologies (De Adelhart Toorop et al., 2021, p. 661) and the need for exhaustive externality inventories (Bandel et al., 2020).

It has been argued that a single framework methodology for TCA is impossible due to the complex nature of the agri-food sector (Notarnicola et al., 2015). In this perspective, stakeholder skepticism is understandable. It helps that research into possible ways to bridge readily quantifiable externalities with less tangible ones is emerging (e.g., Brumm and Fukushi, 2023) and consensus is being sought on functional units for TCA assessments (e.g., Bandel et al., 2020).

Another reason to critically evaluate TCA communication strategies is the risk that TP would be unaffordable to consumers. This risk contradicts some of the basic principles of TCA, namely that “the enforcement of rights and regulations should also be part of true pricing to ensure that affordable and healthy food is accessible to all.” (Hendriks et al., 2021, p. 3, emphasis added).

That equity plays a pivotal role in securing positive outcomes from TCA for all stakeholders (end consumers included) has been disseminated poorly to the participants of this study. Hence, TCA experts and advocates need to engage more closely with the food value chain to ensure that this underlying value of TCA is clearly understood by the public (e.g., Stein et al., 2024). In addition, more focus on developing promotional material to increase the “green value” attached to TP has also been suggested (Taufik et al., 2023).

Examples of supplementary policy interventions to counter that TP would make food unaffordable include a VAT reform making organic produce cheaper than conventional (Oebel et al., 2024; Springmann et al., 2025). TP rests on the assumption that shifting prices based on externalities, making products with high externalities more expensive and those with low externalities cheaper, will incentivize consumers to choose products with fewer negative externalities (Azarkamand et al., 2024; Pieper et al., 2020; Weishaupt et al., 2020). Recent studies show positive consumer attitudes toward such consumption changes (Michalke et al., 2022; Seubelt et al., 2022; Stein et al., 2024), with reservations if TP has a measurable negative effect on their spending abilities (Stein et al., 2024).

Data availability is important to TCA calculations, and stakeholders and researchers face issues with data transparency (Notarnicola et al., 2015). As extant databases are nowhere near the standard advocated by the TCA framework (Bandel et al., 2020; Brumm and Fukushi, 2023, p. 25930; Springmann, 2024), it is no surprise that stakeholders remain skeptical regarding the efficacy of TP or a TPL based on that foundation.

Perceived consumer information fatigue is another reason for some stakeholders to be skeptical about TPL. Some believe that consumers may be as effectively nudged by more general communication of a product’s “green” aspects as by labels certifying its environmental sustainability (Sigurdsson et al., 2022), inviting a discussion of viable alternatives.

Neither interviewed stakeholders nor the reviewed research currently identifies which node(s) along the food value chain is (are) most suitable for initiating externality internalization efforts. The argument that farmers need more compensation when they choose sustainable production methods may be self-serving. The same is the case for the expressed view among farmers that such choices have greater positive outcomes for the public than for the farmers themselves (Small and Maseyk, 2022).

Some participants singled out the supermarkets as the stronghold of the status quo of the modern food system, a view which is also expressed in the food system literature (e.g., Popkin and Kenan, 2016; Reardon et al., 2003, 2012). Others suggest that the livestock sector holds significant political influence related to the ability to transform the global agri-food system (Springmann, 2024). Transport and packaging are the two main levers available for retailers to influence and are still important issues to tackle, even if they are considered small impacts in TCA assessments, compared to fertilizer or land use, for example. Still, prioritization requires an assessment of the full picture, and what is being consumed matters more than where it comes from. Why consumption occurs (i.e., consumer motives) also matters for understanding food choices and how to transform the food system (Fernqvist et al., 2024).

Regardless of who is to blame or who is expected to act, governments play a vital role in eliminating or reducing negative externalities (Buckley and Liesch, 2023). This aligns with the views of interviewed stakeholders, who generally saw policy and regulation as two fundamental tools for achieving meaningful change in the food system.

In general, the interviewed stakeholders’ suggestions for paradigmatic changes to EU agricultural and trading regulations align with scholarly observations (i.e., Springmann et al., 2018; Weishaupt et al., 2020). This underlines the importance of inviting stakeholders to contribute to policy development (cf. Stein et al., 2024).

Stakeholders along the food value chain possess unique, often region-specific insights into global food systems, including barriers to sustainable development, and their insights should not be ignored. This includes first-hand insight into the dilemma of increasing demand for sustainability on EU production while allowing imports with lower sustainability standards. However, “import bans may not be justifiable under world trade law” (Weishaupt et al., 2020, p. 13), and international courts may not necessarily support regulations that ban unsustainable production methods. However, food value chain stakeholders can address externalities in ways national governments cannot (Buckley and Liesch, 2023). Policy and regulations should, therefore, incentivize stakeholder engagement in mitigating negative externalities, preferably based on an open discussion between policymakers and food value chain stakeholders.

The stakeholders interviewed have good reason to claim that price is the number one factor when choosing food products. Opting for the cheapest price often means ignoring health and environmental sustainability aspects (Seubelt et al., 2022). The environmental and health externalities are largely attributed to the increased production and consumption of processed foods (Popkin and Kenan, 2016; Springmann, 2024). The pragmatic solution suggested by both stakeholders and experts is to change the narrative around food. Public policies should incentivize consumers and producers toward healthier and environmentally sustainable food choices, steering them away from unhealthy and unsustainable processed food (Seubelt et al., 2022; Springmann, 2024).

The idea that TCA can inform politicians and policymakers and aid the transition to sustainable development is not new; it is at the core of the TCA framework (Baker et al., 2020). However, when stakeholders argue that TP and TPL can only work if mandated politically, they discard the potential of TPL to effectively signal and incentivize sustainable choices (Manta et al., 2022; Taufik et al., 2023). Obviously, to realize this potential, TP and TPL must be dissociated from suspicions of greenwashing.

TCA is constantly developing and is arguably still in its nascent phase. A relevant step might be for users to perform their own TCA analysis (De Adelhart Toorop et al., 2021), which invites participatory and influential mediation on behalf of stakeholders. Buckley and Liesch (2023) posited that stakeholders’ agency is a crucial component of their ability to mitigate externalities. They propose a joint effort of business strategies and legislative action, encouraging openness and transparency along the whole value chain.

Despite the skepticism, the present material does not indicate that key stakeholders distance themselves from TCA as a concept per se. However, they expressed significant objections toward TPL, recommending alterations and minimum requirements for a TPL to be considered for implementation. Most of these were specific and clear (e.g., designing the label with simplicity in mind while providing explanations of calculations and externalities online, accessible via QR codes), but a couple deserve further discussion.

First, there were mixed opinions on whether a TPL should use an aggregated score averaging multiple types of externalities into one or if it should be a unified meta-label displaying, but integrating several scores (e.g., environmental, social, and nutritional). Shaikh et al. (2024) provide evidence against the all-encompassing option, finding that customers still respond more positively to an organic label than to a broader eco-label that also includes organic. This might partly be due to any new sustainability label lacking consumers familiarity with the label (Sigurdsson et al. 2022). Thus, more research is needed to settle whether a TPL should preferably be a single score or multiple. In both cases, the public dissemination of the label (for example, the logo, color scheme, and general visual appearance) may be more important than the complex calculations underlying the actual score on the label.

Second, the stakeholders interviewed argued that mandating TPL is the only way to secure fair comparability and safeguards against accusations of greenwashing. Labels can be used for greenwashing (Manta et al., 2022) and since research has shown that even non-certified sustainability tags can have a positive impact on WTP (Sigurdsson et al., 2022), these are reasonable concerns. It seems plausible that mandatory TPL could reduce confusion and offer fairer comparability than the current plethora of labels on the market and, in this way, facilitate the necessary transformations of the food system. Notwithstanding these concerns, the proposal regarding the Green Claims Directive (European Commission, 2023) has been drafted specifically to deal with the issue of greenwashing.

However, objections to mandating TPL across the food value chain remain. Notably, the two retail representatives interviewed had diverging views on the matter. The German retailer representative deemed it impossible to implement TPL across their 5,000-plus inventory, while the Danish believed it possible with the help of external databases and government assistance. Still, in light of stakeholder objections identified in this study and elsewhere, especially the barriers to policy influencing food production outside of the EU (Weishaupt et al., 2020), a mandate on TPL for all products on the market seems unrealistic. Taxing certain inputs could arguably circumvent this issue, leading to associated costs being internalized. Unsustainable products would become more expensive, and consumer preferences would hypothetically shift. A corollary is that TCA becomes effectively mandatory while TPL adoption remains voluntary. A question remains: What unintended consequences may follow such a top-down approach to internalizing negative externalities?

4.1 Limitations

The study’s reliance on a small sample size limits the generalizability of the findings. Additionally, theoretical sampling may have introduced selection bias, as participants were chosen for their expertise, potentially excluding alternative perspectives.

The data collection also had its issues. Although the interviewees were introduced to TCA as a holistic method for monetizing negative and positive externalities, the interview guide explicitly focused on identifying and discussing negative externalities. Regardless of the good reasons for this, it constitutes a missed opportunity to understand participants’ preconceptions of possible positive externalities.

It is also worth mentioning that more time could have been spent going over the individual participants’ interpretation of TCA and their personal affiliation with the framework. As the interview guide was designed, the TCA framework was discussed in a matter offering a baseline understanding for the research team as to what degree the interviewee was familiar with the concept, rather than their personal affiliation and philosophical understanding of the TCA approach to mitigating negative externalities within the food value chain. A deeper understanding of these more philosophical underpinnings might have afforded the study a more distinct explanation of why skepticism was so prevalent.

5 Conclusion

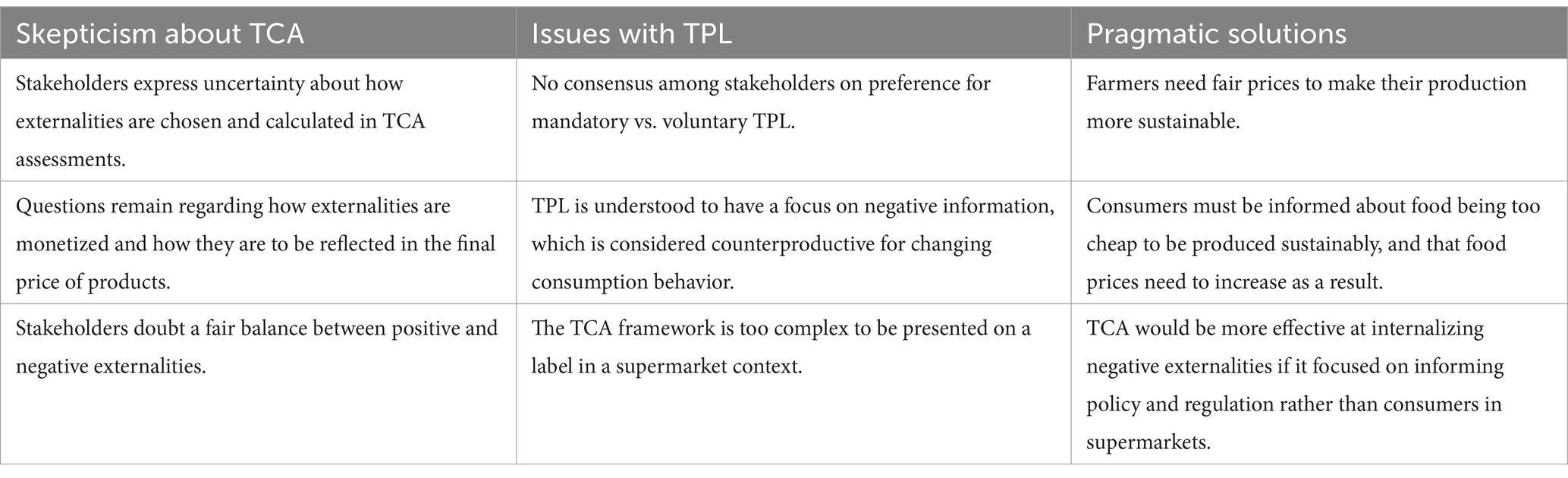

Stakeholders express skepticism regarding True Cost Accounting’s (TCA) ability to represent all externalities holistically. Similarly, they are concerned that less tangible values of importance to the general public are not given the appropriate weight in True Price (TP) calculations, about potential price increases, and about insufficient transparency for consumers and farmers regarding TP calculations. Finally, some voiced skepticism regarding True Price Labeling’s (TPL) potential to impact consumption toward less externality-laden products. For an overview of the key takeaways, see Table 3.

Table 3. Summary of key results.

Stakeholders also suggested pragmatic solutions for a future TPL to be adopted. Most importantly, there seems to be wide consensus among interviewed stakeholders that TPL must be mandatory for it to fulfill the intended goals and be widely applied. The design of the label and the information on it must be simple and easy to grasp., and calculations of true costs must be transparent and enable a fair comparison between products. Exhaustive information and details regarding externalities and monetization criteria could be online and accessible via, e.g., QR codes. Regarding the design of a TPL, most stakeholder representatives were drawn to the graded traffic-light colors model, which also has the strongest scholarly support (cf. Thøgersen et al., 2024).

This study highlights the complexity of addressing externalities within the food system through TCA, TP, and TPL. While the interviewed stakeholders share a commitment to sustainability, their perspectives on the role and feasibility of TPL vary widely. Their main objections concerned TP’s effect on affordability and the validity of its underlying calculations of true costs. The findings underscore the need for collaborative efforts to refine TCA methodologies and explore alternative versions of a potential TPL.

Despite the objections by participating stakeholders, there are strong arguments backing TP and a TPL (von Braun and Hendriks, 2023). However, the voiced objections demonstrate that the calculation and communication of true costs need to be qualified considerably before TP and TPL can be implemented.

The views expressed by the participants in this study should neither be seen as evidence of a potential acceptance of TP and TPL nor as completely rejecting the idea. Rather, the study evidences a gap in communication between stakeholders and TCA proponents, insufficient transparency of the underlying calculations of true costs, and a general skepticism regarding the usefulness of TP and a TPL in mitigating negative externalities. It also highlights ways of mitigating stakeholder skepticism by spreading knowledge of the TCA methodologies.

5.1 Future research

The present study invites further research on the implications of TCA and TP in practice, including research engaging key stakeholders. The limited scope of this study calls for further research to corroborate the evidence of widespread skepticism of TP and TPL among stakeholders, not least regarding their suspicions regarding the underlying calculations of true costs.

Reading this paper as a case-study of stakeholder skepticism toward TP and TPL may be fruitful. The sample represents groups that hold key roles in potentially adopting such a label and some of them have experience with similar projects. The empirical evidence suggests that it is prudent to expect skepticism in other contexts, and among other stakeholders. Therefore, it would be interesting to see more in-depth case-studies on stakeholders in other contexts. In addition, quantitative studies on larger samples would also enrich the nascent field of TPL, by providing statistical generalizability of attitudes toward TPL, which this study cannot.

Future research should also more systematically investigate the pros, cons, and feasibility of the mandatory versus voluntary implementation of TP and TPL. Since stakeholders favor mandatory TPL, possible unintended consequences of making it mandatory should be investigated.

Given stakeholders’ doubts about TP’s affordability for end consumers, it would be advisable to do research in real-life settings and from a cross-cultural perspective to better assess this position (Fernqvist et al., 2024). Considering the issue of power imbalances along the food value chain (Popkin and Kenan, 2016; Reardon et al., 2003, 2012), it would be interesting to investigate how such power imbalances influence stakeholders’ ability to shift production methods toward alternatives promoting social, health, and environmental sustainability.

Finally, more research is needed on why and when consumers associate TPL with greenwashing and what steps could be taken against such accusations. A recent systematic literature review reported a lack of empirical studies of greenwashing (Bernini et al., 2024), and the present study further suggests a need to understand better what drives the perception of greenwashing (see also Stein et al., forthcoming). It also remains to be seen to what degree the Green Claims Directive (European Commission, 2023) may or may not help mitigate the greenwashing issue.

Data availability statement

The datasets presented in this article are not readily available because the information in the datasets cannot be made 100% anonymous and contains personal data. Consequently, GDPR protects the privacy of the participants and restricts the author(s) from sharing the interview transcripts. Requests to access the datasets should be directed to c2ViYXN0aWFuLmNhcmxzc29uQHNsdS5zZQ==.

Author contributions

SC: Writing – original draft, Conceptualization, Writing – review & editing, Visualization, Formal analysis. EH: Project administration, Validation, Methodology, Supervision, Conceptualization, Writing – review & editing. EA: Writing – review & editing, Conceptualization. AP: Writing – review & editing, Investigation. LS: Investigation, Writing – review & editing. BO: Writing – review & editing, Investigation. TG: Writing – review & editing. MJ: Investigation, Writing – review & editing. JT: Writing – review & editing, Conceptualization, Methodology.

Funding

The author(s) declare that financial support was received for the research and/or publication of this article. This research was carried out as part of the FOODCoST project, funded by Horizon Europe (grant number: 101060481).

Acknowledgments

The authors would like to acknowledge the time and insights provided to us by the participants of this study.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Generative AI statement

The authors declare that no Gen AI was used in the creation of this manuscript.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Supplementary material

The Supplementary material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fsufs.2025.1599970/full#supplementary-material

Abbreviations

TCA, True Cost Accounting; TP, True Price; TPL, True Price Label.

References

Adeoye-Olatunde, O. A., and Olenik, N. L. (2021). Research and scholarly methods: semi-structured interviews. JACCP 4, 1358–1367. doi: 10.1002/jac5.1441

Azarkamand, S., Fernández Ríos, A., Batlle-Bayer, L., Bala, A., Sazdovski, I., Roca, M., et al. (2024). Calculating the true costs of protein sources by integrating environmental costs and market prices. Sustainable Production Consumption 49, 28–41. doi: 10.1016/j.spc.2024.06.006

Baker, L., Castilleja, G., De Groot Ruiz, A., and Jones, A. (2020). Prospects for the true cost accounting of food systems. Nature Food 1, 765–767. doi: 10.1038/s43016-020-00193-6

Bandel, T., Sotomayor, M. C., Kayatz, B., Müller, A., Riemer, O., and Wollesen, G. (2020). True cost accounting inventory report [research report]. Global Alliance for the Future of Food. Available online at: https://www.natureandmore.com/files/documenten/tca-inventory-report.pdf

Bastounis, A., Buckell, J., Hartmann-Boyce, J., Cook, B., King, S., Potter, C., et al. (2021). The impact of environmental sustainability labels on willingness-to-pay for foods: a systematic review and Meta-analysis of discrete choice experiments. Nutrients 13:2677. doi: 10.3390/nu13082677

Bernini, F., Giuliani, M., and La Rosa, F. (2024). Measuring greenwashing: a systematic methodological literature review. Business Ethics Environ. Responsibility 33, 649–667. doi: 10.1111/beer.12631

Braga Junior, S., Martínez, M. P., Correa, C. M., Moura-Leite, R. C., and Da Silva, D. (2019). Greenwashing effect, attitudes, and beliefs in green consumption. RAUSP Management J. 54, 226–241. doi: 10.1108/RAUSP-08-2018-0070

Braun, V., and Clarke, V. (2006). Using thematic analysis in psychology. Qual. Res. Psychol. 3, 77–101. doi: 10.1191/1478088706qp063oa

Brumm, A., and Fukushi, K. (2023). Introducing the food value framework (FVF) to empower transdisciplinary research and unite stakeholders in their efforts of building a sustainable global food system. Environ. Dev. Sustain. 26, 25921–25943. doi: 10.1007/s10668-023-03713-z

Buckley, P. J., and Liesch, P. W. (2023). Externalities in global value chains: firm solutions for regulation challenges. Glob. Strateg. J. 13, 420–439. doi: 10.1002/gsj.1471

De Adelhart Toorop, R., van Veen, B., Verdonk, L., and Schmiedler, B. (2023). True cost accounting applications for agrifood systems policymakers—background paper for the state of food and agriculture 2023. FAO Agricultural Development Economics Working Paper, No. 23-11. Rome. doi: 10.4060/cc8341en

De Adelhart Toorop, R., Yates, J., Watkins, M., Bernard, J., and De Groot Ruiz, A. (2021). Methodologies for true cost accounting in the food sector. Nature Food 2, 655–663. doi: 10.1038/s43016-021-00364-z

European Commission. (2023), Directive of the European Parliament and of the council on substantiation and communication of explicit environmental claims (green claims directive), COM(2023) 166 final. Brussels: European Commission. Available online at: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52023PC0166

Fanzo, J., Haddad, L., Schneider, K. R., Béné, C., Covic, N. M., Guarin, A., et al. (2021). Viewpoint: rigorous monitoring is necessary to guide food system transformation in the countdown to the 2030 global goals. Food Policy 104:102163. doi: 10.1016/j.foodpol.2021.102163

FAO (2023). The state of food and agriculture 2023. FAO. Revealing the true cost of food to transform agrifood systems. Rome. doi: 10.4060/cc7724en

FAO (2024). The state of food and agriculture 2024 – value-driven transformation of agrifood systems. FAO. doi: 10.4060/cd2616en

Fernqvist, F., Spendrup, S., and Tellström, R. (2024). Understanding food choice: a systematic review of reviews. Heliyon 10:e32492. doi: 10.1016/j.heliyon.2024.e32492

Garnett, T. (2013). Food sustainability: problems, perspectives and solutions. Proc. Nutr. Soc. 72, 29–39. doi: 10.1017/S0029665112002947

Gemmill-Herren, B., Baker, L. E., and Daniels, P. A. (2021). True cost accounting for food: Balancing the scale : Routledge.

Hendriks, S., De Groot Ruiz, A., Acosta, M. H., Baumers, H., Galgani, P., Mason-D’Croz, D., et al. (2023). The true cost of food: a preliminary assessment. In J. BraunVon, K. Afsana, L. O. Fresco, and M. H. A. Hassan (Eds.), Science and innovations for food systems transformation (pp. 581–601). Springer International Publishing.

Hendriks, S., Ruiz, A., Herrero, M., Baumers, H., Galgani, P., Mason-D’Croz, D., et al. (2021). The true cost and true price of food. A paper from the scientific group of the U.N. Food systems summit. [Technical Report]. United Nations Food Systems Summit 2021.

Huang, S. K., Kuo, L., and Chou, K.-L. (2016). The applicability of marginal abatement cost approach: A comprehensive review. J. Clean. Prod. 127, 59–71. doi: 10.1016/j.jclepro.2016.04.013

Mahadeva, E., Ganji, E. N., and Shah, S. (2024). Sustainable consumer behaviours through comparisons of developed and developing nations. Int. J. Environ. Eng. Dev. 2, 106–125. doi: 10.37394/232033.2024.2.10

Maity, K., Gandhi, S., Thirthalli, J., and Sinha, P. (2024). Stakeholders’ perspectives on adverse effects of ECT: A qualitative thematic analysis. Indian J Psychiatry. 66, 553–565. doi: 10.4103/indianjpsychiatry.indianjpsychiatry_614_23

Manta, F., Campobasso, F., Tarulli, A., and Morrone, D. (2022). Showcasing green: how culture influences sustainable behavior in food eco-labeling. Br. Food J. 124, 3582–3594. doi: 10.1108/BFJ-05-2021-0478

Megyesi, B., Gholipour, A., Cuomo, F., Canga, E., Tsatsou, A., Zihlmann, V., et al. (2024). Perceptions of stakeholders on nature-based solutions in urban planning: a thematic analysis in six European cities. Urban For. Urban Green. 96:128344. doi: 10.1016/j.ufug.2024.128344

Michalke, A., Stein, L., Fichtner, R., Gaugler, T., and Stoll-Kleemann, S. (2022). True cost accounting in Agri-food networks: a German case study on informational campaigning and responsible implementation. Sustain. Sci. 17, 2269–2285. doi: 10.1007/s11625-022-01105-2

Notarnicola, B., Salomone, R., Petti, L., Renzulli, P. A., Roma, R., and Cerutti, A. K. (2015). Life cycle assessment in the Agri-food sector: Case studies, methodological issues and best practices : Springer International Publishing.

Oebel, B., Stein, L., Michalke, A., Stoll-Kleemann, S., and Gaugler, T. (2024). Towards true prices in food retailing: the value added tax as an instrument transforming Agri-food systems. Sustain. Sci. doi: 10.1007/s11625-024-01477-7

Oliver, T. H., Boyd, E., Balcombe, K., Benton, T. G., Bullock, J. M., Donovan, D., et al. (2018). Overcoming undesirable resilience in the global food system. Global Sustainability 1:e9. doi: 10.1017/sus.2018.9

Pieper, M., Michalke, A., and Gaugler, T. (2020). Calculation of external climate costs for food highlights inadequate pricing of animal products. Nat. Commun. 11:6117. doi: 10.1038/s41467-020-19474-6

Popkin, B. M., and Kenan, W. R. (2016). Preventing type 2 diabetes: changing the food industry. Best Pract. Res. Clin. Endocrinol. Metab. 30, 373–383. doi: 10.1016/j.beem.2016.05.001

Reardon, T., Timmer, C. P., Barrett, C. B., and Berdegué, J. (2003). The rise of supermarkets in Africa, Asia, and Latin America. Am. J. Agric. Econ. 85, 1140–1146. doi: 10.1111/j.0092-5853.2003.00520.x

Reardon, T., Timmer, C. P., and Minten, B. (2012). Supermarket revolution in Asia and emerging development strategies to include small farmers. Proc. Natl. Acad. Sci. 109, 12332–12337. doi: 10.1073/pnas.1003160108

Semken, C., Michalke, A., Stein, L., Gaugler, T., and Allcott, H. (n.d.). Optimal green retailing: Theory and evidence : National Bureau of Economic Research.

Seubelt, N., Michalke, A., and Gaugler, T. (2022). Influencing factors for sustainable dietary transformation—a case study of German food consumption. Food Secur. 11:227. doi: 10.3390/foods11020227

Shaikh, S., Yamim, A. P., and Werle, C. O. C. (2024). Are all-encompassing better than one-trait sustainable labels? The influence of eco-score and organic labels on food perception and willingness to pay. Appetite 203:107670. doi: 10.1016/j.appet.2024.107670

Sigurdsson, V., Larsen, N. M., Pálsdóttir, R. G., Folwarczny, M., Menon, R. G. V., and Fagerstrøm, A. (2022). Increasing the effectiveness of ecological food signaling: comparing sustainability tags with eco-labels. J. Bus. Res. 139, 1099–1110. doi: 10.1016/j.jbusres.2021.10.052

Small, B., and Maseyk, F. (2022). Understanding farmer behaviour: a psychological approach to encouraging pro-biodiversity actions on-farm. N. Z. J. Ecol. doi: 10.20417/nzjecol.46.20

Springmann, M. (2024). A multicriteria analysis of meat and milk alternatives from nutritional, health, environmental, and cost perspectives. Proc. Natl. Acad. Sci. 121:e2319010121. doi: 10.1073/pnas.2319010121

Springmann, M., Clark, M., Mason-D’Croz, D., Wiebe, K., Bodirsky, B. L., Lassaletta, L., et al. (2018). Options for keeping the food system within environmental limits. Nature 562, 519–525. doi: 10.1038/s41586-018-0594-0

Springmann, M., Dinivitzer, E., Freund, F., Jensen, J. D., and Bouyssou, C. G. (2025). A reform of value-added taxes on foods can have health, environmental and economic benefits in Europe. Nature Food 6, 161–169. doi: 10.1038/s43016-024-01097-5

Stein, L., Michalke, A., Gaugler, T., and Stoll-Kleemann, S. (2024). Sustainability science communication: case study of a true cost campaign in Germany. Sustain. For. 16:3842. doi: 10.3390/su16093842

Taufik, D., Van Haaster-de Winter, M. A., and Reinders, M. J. (2023). Creating trust and consumer value for true price food products. J. Clean. Prod. 390:136145. doi: 10.1016/j.jclepro.2023.136145

Thøgersen, J., Dessart, F. J., Marandola, G., and Hille, S. L. (2024). Positive, negative or graded sustainability labelling? Which is most effective at promoting a shift towards more sustainable product choices? Bus. Strateg. Environ. 33, 6795–6813. doi: 10.1002/bse.3838