Alexandra Sadler1*

Alexandra Sadler1* Yandrapu Bharath2

Yandrapu Bharath2 Jacqueline Tereza da Silva1

Jacqueline Tereza da Silva1 Daniel Carneiro de Abreu3

Daniel Carneiro de Abreu3 Emily Shankar1

Emily Shankar1 Karolyne Vieira Bassetto3

Karolyne Vieira Bassetto3 Lindsay Jaacks1

Lindsay Jaacks1- 1Division of Global Agriculture and Food Systems, Royal (Dick) School of Veterinary Studies, University of Edinburgh, Edinburgh, United Kingdom

- 2Centre for Health Analytics Research and Trends, Ashoka University, National Capital Region, Sonipat, India

- 3AgriSciences, Universidade Federal de Mato Grosso (UFMT), Sinop, Brazil

Background: Demand for organic foods remains low, despite the potential of organic products to contribute to sustainable food systems. Food purchasing decisions are influenced by the food environment, yet no study has systematically evaluated food environment dimensions for organic products.

Methods: We developed an organic food environment assessment tool that evaluates the availability, price, vendor and marketing characteristics of organic foods in urban food environments. We implemented the tool in nine cities across Brazil, India, and the United Kingdom for 14 sentinel products.

Results: We found that only 37% of 808 surveyed vendors sold an organic option. Organic rice was 1.8–2.5 times the price of non-organic rice. Only 8% of organic products used a price promotion, while 62% displayed a certification label. In India, health benefits were the predominant marketing message (59% of organic foods); in the UK, it was environmental benefits (50%).

Conclusion: Our findings indicate a need for a more evidence-based strategy in marketing organic foods and beverages to consumers. There is a need for further research and implementation of market-side initiatives to boost demand for organic foods and beverages in order to encourage a shift towards more sustainable food systems.

1 Introduction

Producing food for humanity comes with a significant environmental cost (Halpern et al., 2022). Half of ice-free land is used for growing crops and livestock pastures (Ellis et al., 2010), and 64% of that land has pesticide residues that exceed no-effect concentrations (Tang et al., 2021). Fertiliser and manure runoff have resulted in increased nutrient loads in marine and freshwater systems, leading to harmful algal blooms, dead zones and fish kills (Lee et al., 2016). A shift to more sustainable food production is urgently needed (FAO, IFAD, IFAD, UNICEF, WFP, and WHO, 2021; HLPE, 2019; Wezel et al., 2020; Willett et al., 2019).

Organic farming, which aims to produce agricultural commodities without the use of synthetic chemicals, is one such approach. Organic production is growing rapidly, yet still makes up just 2% of agricultural land globally (Willer et al., 2025). Likewise, the market for organic products is growing, rising to EUR 136 billion in 2023, but remains a small segment of the total food and beverage market (Willer et al., 2025, p. 20). Denmark, which has the highest organic share globally, is only at 12% (Willer et al., 2025, p. 285). Moreover, there is a global mismatch between where organic production occurs and where organic products are consumed: while 88% of organic producers are based in Asia, Africa and Latin America, 90% of organic food is consumed in North America and Europe (Willer et al., 2025).

There are a variety of factors influencing consumer demand for organic foods and beverages globally, which can be conceptualised within a food environment framework. Turner et al. (2018, p. 95) define the food environment as “the interface that mediates people’s food acquisition and consumption within the wider food system.” It encompasses both an ‘external domain’ comprised of exogenous dimensions (food availability, prices, vendor and product characteristics, and marketing and regulation) and a ‘personal domain’, which includes dimensions that vary at the individual level (food accessibility, affordability, convenience, and desirability) (Turner et al., 2018, 2020). Complex interactions between the personal and external domains shape consumers’ choices with regard to food and beverage acquisition and consumption, including organic foods and beverages. Existing research on consumer demand for organic foods and beverages has shown that while some consumers are motivated to buy organic products because of their perceived desirability (especially as a healthier and more sustainable product), many consumers are deterred by their perceived lower affordability and availability (Katt and Meixner, 2020; Kushwah et al., 2019; Massey et al., 2018; Wier et al., 2008). However, there has been limited research that actually quantifies the availability and price of organic foods and beverages in the food environment, with most existing studies concentrated in high-income countries (HICs) (Duvall et al., 2010; Garcia et al., 2020; Grilo et al., 2022; Lucan et al., 2015; Lupolt et al., 2019). Moreover, there is limited research on the marketing characteristics of organic foods and beverages (Sadler et al., 2024b) and no previous studies have comprehensively documented all dimensions of the external domain of the food environment for organic foods and beverages or compared across different scales and contexts.

This study therefore aimed to evaluate the external domain of the food environment for organic foods and beverages in urban areas. Following Turner et al.’s (2018) framework for conducting food environment research in LMICs, we chose a combined geospatial and market-based approach to documenting the external food environment by developing a market basket survey tool tailored to organic foods and beverages. We implemented the survey tool at the vendor-level across one high-income, middle-income, and lower-income neighbourhood across three cities per country in Brazil, India, and the UK. We captured Turner et al. (2018) four dimensions of external food environments: vendor properties, availability, prices, and marketing and regulation. For the marketing component, we classified marketing characteristics according to McCarthy’s ‘four P’ conceptual framework: product, price, place, and promotion (McCarthy, 1975). We identified ‘organic vendors’ as those selling at least one organic product from our list of 14 sentinel products.

Although we use the term organic throughout this paper for simplicity, we used a broad and inclusive definition of what constitutes organic in our survey. The use of the term organic in the marketing of foods and beverages is legally regulated in some contexts, including in Brazil, India, and the UK. In countries such as India and Brazil, obtaining the requisite certification to market products as officially organic can be prohibitively expensive and time-consuming, resulting in informal sales directly between producer and consumer or in the use of alternative terminologies, such as ‘natural’ in the Indian context (Candiotto, 2018; Khurana and Kumar, 2020; Meemken, 2020). As such, we included all products advertised using the terms ‘organic’, ‘natural’, ‘chemical-free’, ‘pesticide-free’, ‘bioproduct’, ‘bio’, ‘eco’, and ‘GMO-free’, while also capturing the presence or absence of certification labels for each product. Henceforth, we will use the term organic without quotation marks when it refers to the umbrella term, which includes these other terminologies, and ‘organic’ in quotation marks when referring to products specifically labelled with the term ‘organic’.

2 Materials and methods

This is an observational study of the availability, prices, and marketing characteristics of organic foods and beverages in urban food environments. The study was reviewed by the Human Ethical Review Committee at the University of Edinburgh and determined not to require ethical approval as it did not involve the collection of data from human subjects.

2.1 Study setting

This study was conducted in three cities per country in Brazil, India, and the UK. These countries were selected to represent a diverse set of regions and income levels, while also including both countries that predominantly produce or export organic foods and beverages (Brazil, India) and those that predominantly consume or import organic products (UK) (Willer et al., 2025). In each country, we selected a large, medium, and small city to ensure we captured a variety of contexts and sizes. The following nine cities were selected: Rio de Janeiro (Brazil), São Paulo (Brazil), Sinop (Brazil), Hyderabad (India), Latur (India), Visakhapatnam (India), Birmingham (UK), Edinburgh (UK), and London (UK). The selection of cities was designed to match these criteria of small, medium, and large cities within the constraints of personnel and financial resources. In each city, we selected a higher-, middle-, and lower-income neighbourhood to account for variation in socio-economic status. Neighbourhood selection was determined using relevant local datasets and was triangulated by validating the selection with local experts, such as university and non-profit workers and other local residents (Birmingham City Council, 2019; City of Edinburgh Council, 2022; MHCLG, 2019; Prefeitura da Cidade do Rio de Janeiro, 2018; Rede Nossa São Paulo, 2022). Where local datasets were not available at the requisite level of granularity, we relied on local expertise, corroborated by two or more sources.

2.2 Sampling

2.2.1 Neighbourhood selection

In each neighbourhood, we selected a circular sampling area with a 0.5 km radius, centred on the midpoint of the neighbourhood. While existing food environment surveys often use a 1 km radius per city (Chaudhry et al., 2021; Kirk et al., 2019), we adopted a stratified spatial sampling approach by selecting three smaller radius circles located in a higher-, middle-, and lower-income neighbourhood. This enabled us to capture socioeconomic variability within a city, while maintaining sufficient spatial coverage for analysis, in line with recommendations from the United Nations’ Food and Agriculture Organisation that socioeconomic status is an important factor for food environment assessments (FAO, GAIN, WOF, 2022). Within each circle, we systematically documented all vendors that met our inclusion criteria by walking along every street within the sampling area. Depending on the vendor type, we either entered the vendor site (for example, supermarkets) or surveyed from the exterior (for example, mobile vendors or open-front counter-service retail outlets) to collect data on the products sold by the vendor (FAO, GAIN, WOF, 2022).

2.2.2 Vendor selection

All vendors selling any of the 14 selected sentinel products (see section 2.2.3) for home consumption were surveyed within each circle, including both formal and informal vendors, in line with recommendations for conducting food environment analyses in LMICs (Ahmed et al., 2021). Vendors that sold food primarily for consumption in-store (e.g., restaurants) were excluded. Vendors that sold prepared foods and products for home consumption (e.g., cafes that also sold packaged coffee) were included and only the goods for home consumption were captured in the survey. We included both formal and informal vendors of all sizes, from large supermarket chains to small stationary local vendors and mobile vendors. In the case of marketplaces where multiple vendors were selling foods and beverages, we surveyed each vendor and classified them as mobile vendors. If vendors were closed or refused to allow data collection to proceed, we recorded this response (this variable was added after Edinburgh and Visakhapatnam data were collected). Out of the 533 vendors for which this variable was collected (excluding Edinburgh and Visakhapatnam), only 6 (1%) were closed and 5 (0.9%) refused to allow data collection to proceed (Supplementary Table S1).

2.2.3 Product selection

Fourteen sentinel products were selected for data collection, including bananas, chickpeas, coffee, (wheat) flour, fruit juice, green leafy vegetables, lentils, mangos, milk, millets, nuts, rice, tea, and tomatoes. These products were selected to represent different nutritionally-important product categories (fresh produce, whole grains, dairy, protein sources) (Willett et al., 2019) and different crop types (commercial, export-oriented crops such as coffee and tea, as well as more locally distributed crops such as fruits and vegetables), while remaining culturally relevant (for example, plant-based protein sources are more culturally relevant in India than animal-based protein). The specific fruits and vegetables were selected based on existing global food environment assessments (Chaudhry et al., 2021; Kirk et al., 2019), consumer preference surveys in each of the included countries (APEDA, 2024; Machado et al., 2018; YouGov, 2025a, 2025b), and in consultation with experts in each country to identify commonly available, high-volume products across different categories.1 Millets were included because of their association with organic farming and sustainable food systems, particularly in India, despite being a less common food item in Brazil and the UK (Erler et al., 2022; Raina et al., 2022).

2.2.4 Data collection

Data collection focused on direct observation of publicly available information in order to emulate the consumer experience of the food environment, therefore little human interaction was required. In contexts where small and informal vendors were more prevalent – particularly in India and Brazil – interaction with the store employees or mobile vendors was required in some instances to ask for details such as price, organic status and store open and closing times. However, no personal data were collected about the employees. Where human interaction was required, it was conducted in the native language of the vendor employee. Data collectors carried a letter explaining in the local language the details of the study to show to vendors if they had any questions about the study. Data collectors were trained on the survey protocol (Sadler et al., 2024a) and inclusion and exclusion criteria by the principal investigator (AS) prior to data collection. Data was collected between June 2022 and March 2024.

2.3 Survey tool

The survey tool was developed by the authors (AS, LJ, BY) in consultation with existing literature on food environment survey tools (Ahmed et al., 2021; FAO, GAIN, WOF, 2022). Existing survey tools capture the availability and price of specified foods and beverages (Chaudhry et al., 2021; Kirk et al., 2019), including organic products (Duvall et al., 2010; Lucan et al., 2015; Lupolt et al., 2019; Morland and Filomena, 2007). However, there are few survey tools that capture marketing characteristics, with Chaudhry et al. (2021) recording the presence of promotional materials and Lupolt et al. (2019) capturing details on organic certifications and keywords. We found no existing tools that systematically captured information on availability, prices, and comprehensive marketing characteristics (including marketing themes, terminology, product positioning, price promotions, branding and certification status), particularly for organic products.

The survey tool used in this study takes a market basket survey approach to capture data on: vendor characteristics, availability of 14 sentinel products, price of one sentinel product (rice), and marketing characteristics of organic products. We included both the term ‘organic’ as well as products with terms similar to organic, including ‘natural’, ‘chemical-free’, ‘pesticide-free’, ‘bioproduct’, ‘bio’, ‘eco’, and ‘GMO-free’. We captured various factors related to the ‘four Ps’ of marketing: product, price, place and promotion (McCarthy, 1975). For product-related marketing characteristics, we recorded the terminologies and certification logos used on the packaging. Capturing the certification logos enables the quantification of the availability of both certified and uncertified products, which is particularly important in contexts where certification schemes can be prohibitively expensive and time-consuming for some farmers (González and Nigh, 2005; Home et al., 2017; Nelson et al., 2010; Sacchi, 2015). The presence of certification logos on the packaging also acted as a physical indicator of regulatory interventions. For price, we captured the presence of price promotions. Place-based metrics included product positioning within the store and on the shelf. For promotions, we captured which brands were prominent, the marketing themes used on packaging, and the presence of promotional materials.

We collected the price of organic and non-organic rice in the local currency applicable to the context. We limited the price data collection to only one sentinel product, as it was the most sensitive data to collect and would have substantially increased the survey length and burden for data collectors and vendors, particularly in contexts with more informal vendors, where vendors had to be asked for price information in the absence of price labels. We selected rice because it is a global staple grain that is frequently consumed around the world (including in the selected countries) across different income groups, making it important for global food security and highly relevant for comparison within and between countries (Muthayya et al., 2014). Cereals (including rice) are one of the highest volume organic foods produced in Asia and Latin America and imported to Europe (CRISIL and APEDA, 2024; Willer et al., 2025) and previous studies have shown that some consumers are willing to pay a premium price for organic rice, including in LMICs (Grimm et al., 2023; My et al., 2018), making it a relevant product to gather organic and conventional price data on for our study. For comparability to other published market basket surveys (Chaudhry et al., 2021; Kirk et al., 2019; Lucan et al., 2015; Lupolt et al., 2019), which often publish in US dollars (USD), we converted all three currencies to USD in addition to presenting the local currencies.2 We used the World Bank’s Global Economic Monitor dataset, which converts Local Currency Units (LCU) to USD at the average monthly rate (World Bank, 2021).

Details of the variables that were measured in the survey and generated through our analysis are included in the codebook and analysis plan attached to our survey protocol (Sadler et al., 2024a). The survey was initially deployed in Qualtrics and later RedCAP. The detailed survey tool is included in our OSF pre-registration (Sadler et al., 2024a).

2.4 Statistical analysis

We employed a combination of descriptive and inferential statistics to conduct our analysis. We did not adjust for multiple comparisons because this was a first-of-its-kind study, and we were therefore more concerned about missing potentially important findings requiring further research (type II errors) than false positives (type I errors) (Rothman, 1990). All analyses, including our hypotheses, were pre-registered in our study protocol (Sadler et al., 2024a).3

To test variation in availability, we used descriptive statistics to calculate the absolute and relative frequency of vendors with at least one organic sentinel product available, as well as the median and interquartile range of organic sentinel products sold per vendor. We used a two-tailed Fisher’s Exact test to determine whether the variation in organic availability (as a binary variable per vendor) between neighbourhoods in the same city, between cities in the same country, and between countries was statistically significant. We used a two-tailed Kruskall-Wallis test to determine whether the variation in organic availability (as a count of organic sentinel products available per vendor) between neighbourhoods in the same city, between cities in the same country, and between countries was statistically significant.

To test variation in prices, we used descriptive statistics to calculate the median price and interquartile range of organic versus non-organic rice overall and at the country and city level. We used a one-tailed Mann–Whitney test (or Wilcoxon rank-sum test) to determine whether the price per kilogram of organic rice is significantly higher than the price of non-organic rice overall (between countries) and at the country level (between cities within a given country). For rice sold at the same vendor location, we used a one-tailed Wilcoxon Signed Rank test to evaluate the significance of the price difference for organic versus conventional rice. Our hypothesis was that the price of organic rice would be significantly higher than non-organic rice, in line with existing literature (Grimm et al., 2023; My et al., 2018), so we chose to use a one-tailed test for the statistical tests related to organic rice.

For marketing characteristics, we did not conduct hypothesis-driven statistical tests. We used descriptive statistics to summarise: the frequency of terminologies and themes associated with marketing organic sentinel products; the top brands and certifications associated with these products; the proportion of organic sentinel products with certification; the frequency and characteristics of promotional materials used for marketing organic sentinel products; the placement of organic sentinel products; and the frequency of the use of discounts to market organic sentinel products.

3 Results

In this section, we present the results of our comparative food environment survey according to the factors identified in Turner et al.’s (2018) framework for evaluating the external domain of the food environment: vendor properties (3.1), availability (3.2), prices (3.3), and marketing, regulation, and product characteristics (3.4). Vendor properties.

3.1 Vendor properties

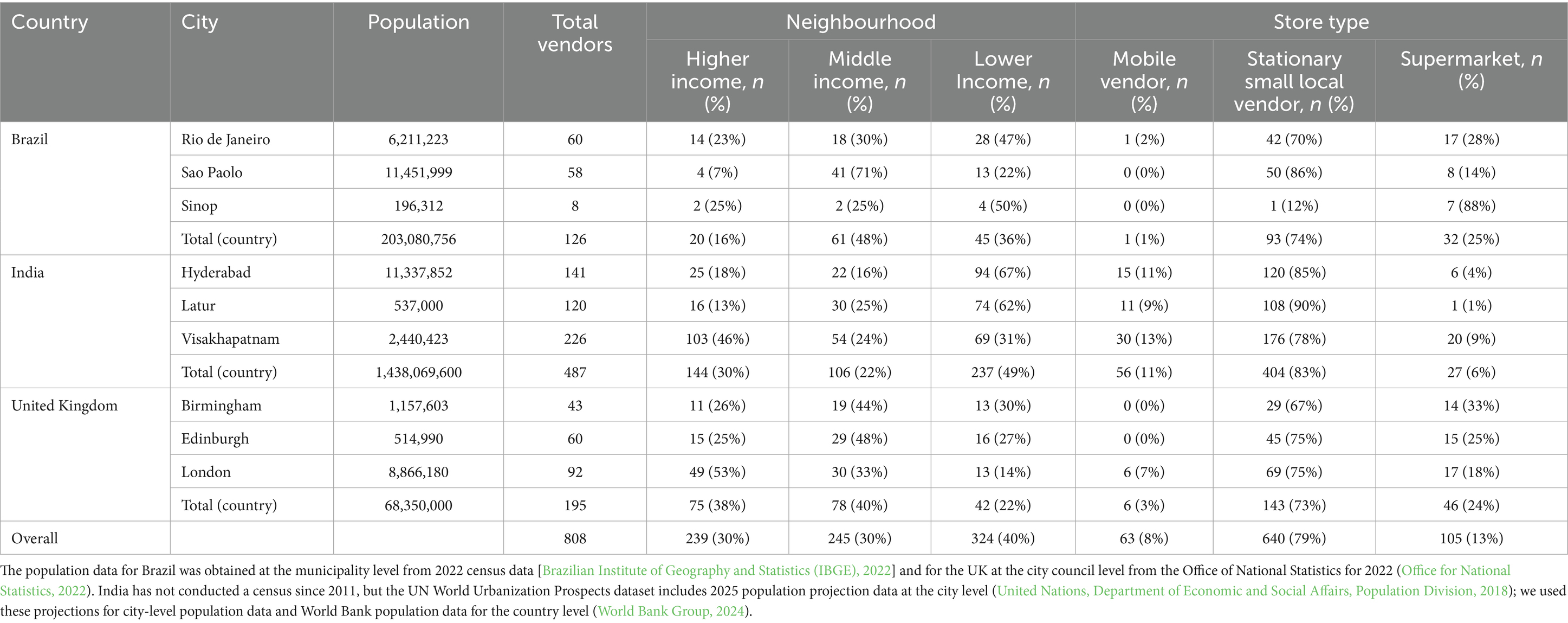

808 vendors were surveyed across Brazil (n = 126), India (n = 487), and the UK (n = 195) (Table 1). India had the highest number of vendors per neighbourhood across each city and income-level, with lower-income neighbourhoods having a particularly high concentration. Stationary small local vendors were the most common vendor type across all three countries (Brazil, 74%; India, 83%; UK, 73%). Organic and non-organic vendors had a similar proportion of days open per week (96 and 94% of vendors open 6–7 days, respectively) and were of a similar size (median of one cashier for both; range of 1–30 and 1–11, respectively) (Supplementary Table S2).

Table 1. City population and number of vendors surveyed per city by neighbourhood and store type.

3.2 Availability

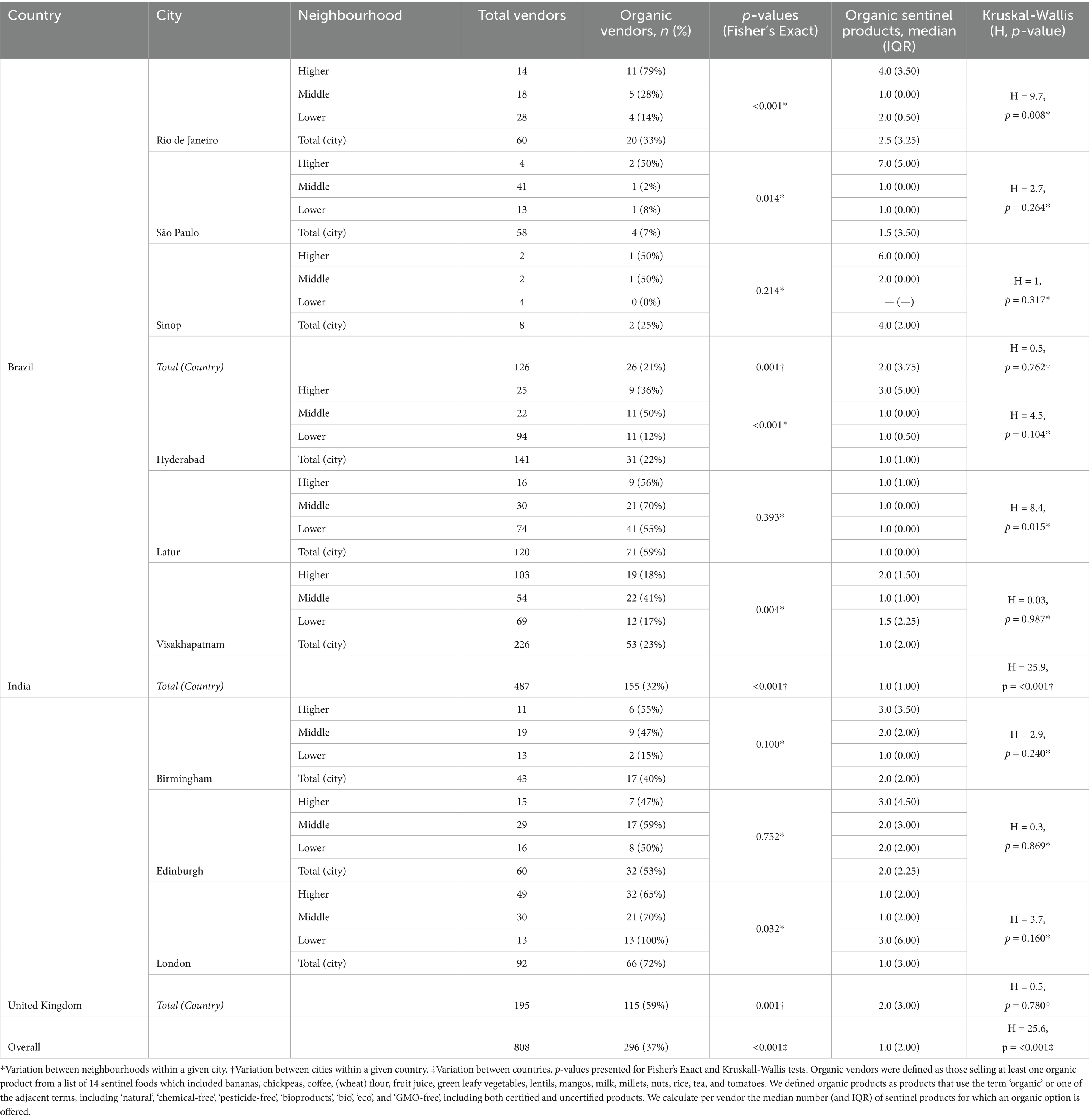

The UK had significantly (H = 25.6, p < 0.001) greater availability of organic products (59% of vendors sold at least one organic sentinel product4) than India (32%) and Brazil (21%) (Table 2). When beverages were excluded, these proportions dropped, with only 30% of vendors selling at least one organic sentinel food in the UK and 15% of vendors in India and Brazil (Supplementary Information, Supplementary Table S3). Generally, in Brazil and India, the smaller cities had greater availability of organic products whereas in the UK, the largest city had greater availability (Table 2).

Table 2. Count and proportion of vendors with at least one organic sentinel product and median (interquartile range - IQR) number of organic sentinel products per vendor by country, city, and neighbourhood.

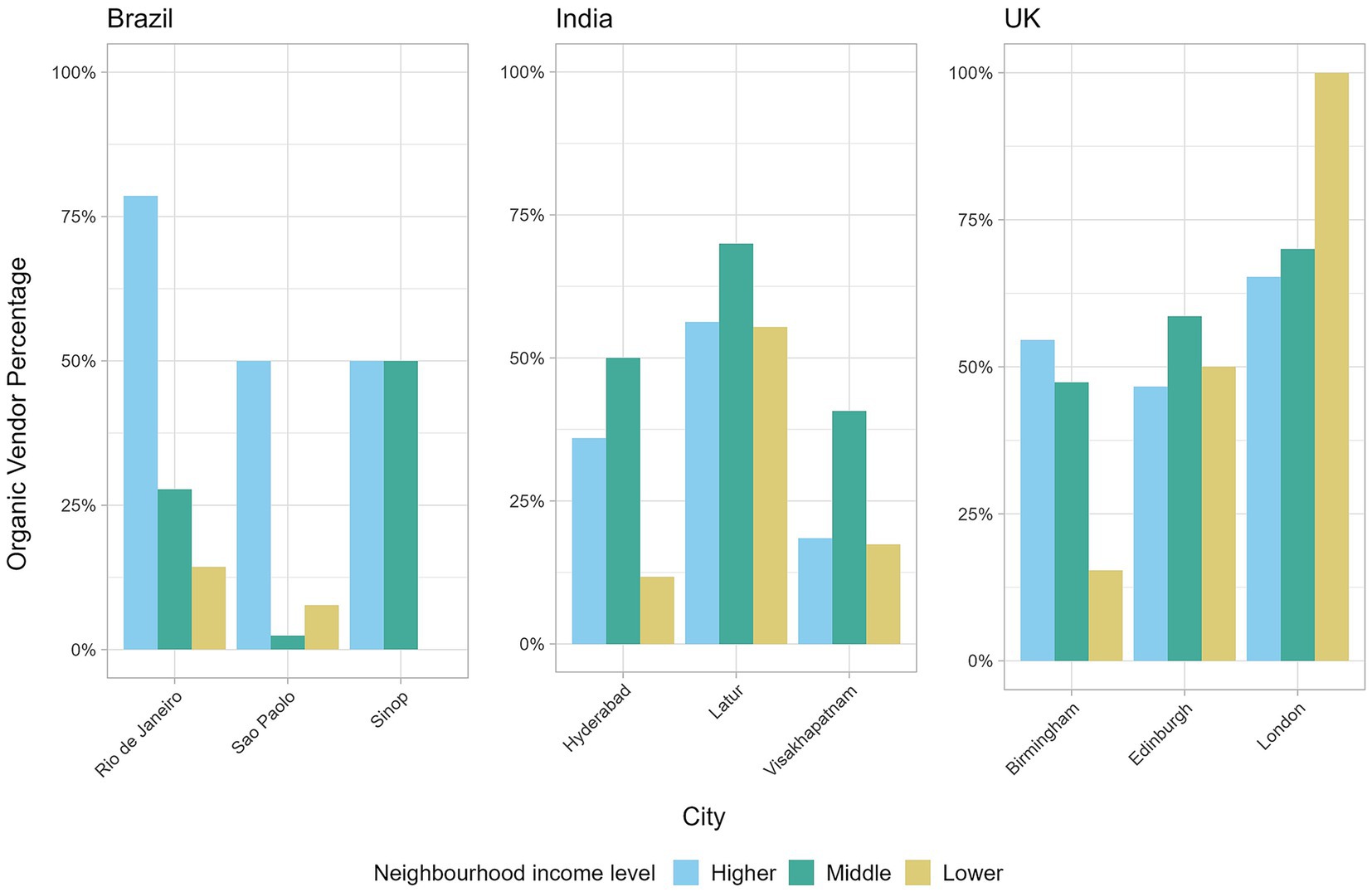

The association between neighbourhood income level and availability of organic vendors (i.e., proportion of vendors who sold at least one organic option) was not consistent across cities (Table 2; Figure <bold>1</bold> ). The higher-income neighbourhoods had the greatest availability of organic vendors in Rio de Janeiro and São Paulo, the middle-income neighbourhoods had the greatest availability in Hyderabad and Visakhapatnam, and the lower-income neighbourhood had the greatest availability in London. Amongst organic vendors, vendors in higher-income neighbourhoods tended to have a higher median number of organic sentinel products than organic vendors in lower-income neighbourhoods, although this trend was not consistent across all cities (Table 2).

Figure 1. Proportion of organic vendors out of total vendors by neighbourhood (lower-, middle-, and higher-income), disaggregated by country and city (n = 808 total vendors). Organic vendors were defined as those selling at least one organic product from a list of 14 sentinel foods which included bananas, chickpeas, coffee (wheat) flour, fruit juice, green leafy vegetables, lentils, mangos, milk, millets, nuts, rice, tea, and tomatoes. We defined organic products as products that use the term ‘organic’ or one of the adjacent terms, including ‘natural’, ‘chemical-free’, ‘pesticide-free’, ‘bioproducts’, ‘bio’, ‘eco’, and ‘GMO-free’, including both certified and uncertified products.

Amongst organic vendors, the median (IQR) number of organic products sold was only 1 (2) out of the 14 sentinel products surveyed (Table 2). Brazil and the UK sold significantly (p < 0.001) more organic sentinel products than India, with a median (IQR) of 2 (3.75), 2 (3), and 1 (1), respectively (Table 2). About half (47%) of organic vendors sold multiple options for at least one organic product. Vendors in Brazil and the UK were significantly more likely to sell multiple options for at least one organic product than those in India: 85, 69, and 25%, respectively (Supplementary Information, Supplementary Table S4). In the UK, tea (58%) and milk (43%) were the most widely available organic sentinel products and mangoes (3%) the least available (Supplementary Table S5). In Brazil, green leafy vegetables (21%) and tomatoes (20%) were the most widely available and milk (1%) the least available. In India, flour (27%) and milk (26%) were the most widely available and coffee (2%) the least available.

3.3 Price

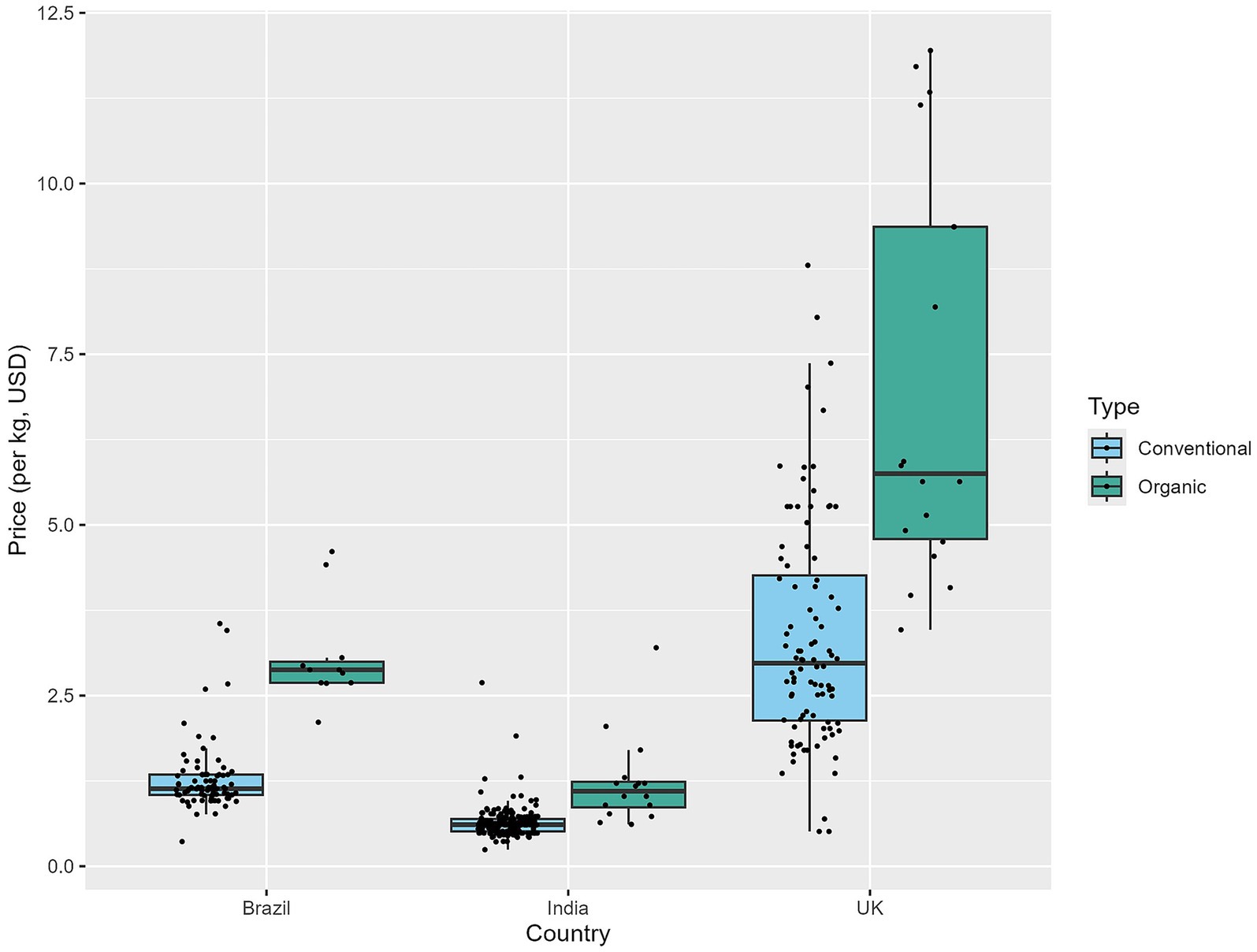

The price of organic rice was significantly higher than the price of non-organic rice overall (W = 13,910, p < 0.001), in each country (Figure 2 and Supplementary Table S6), and within a given vendor selling both organic and non-organic rice (Supplementary Table S7). The price of organic rice was approximately double the price of non-organic rice, with a ratio of 2.5:1 in Brazil, 1.8:1 in India, and 1.9:1 in the UK. Median organic prices were higher than conventional prices even in lower-income neighbourhoods (Supplementary Table S8).

Figure 2. Boxplot of organic and non-organic rice prices (USD/kg) by country (n = 51 for organic rice vendors and n = 378 for conventional rice vendors). We defined organic rice as products that use the term ‘organic’ or one of the adjacent terms, including ‘natural’, ‘chemical-free’, ‘pesticide-free’, ‘bioproducts’, ‘bio’, ‘eco’, and ‘GMO-free’, including both certified and uncertified products. Vendors included those who sold only organic rice, only conventional rice, or both organic and conventional rice. Rice prices were converted from local currencies to USD using the World Bank’s Global Economic Monitor dataset (World Bank, 2021).

3.4 Marketing, regulation, and product characteristics

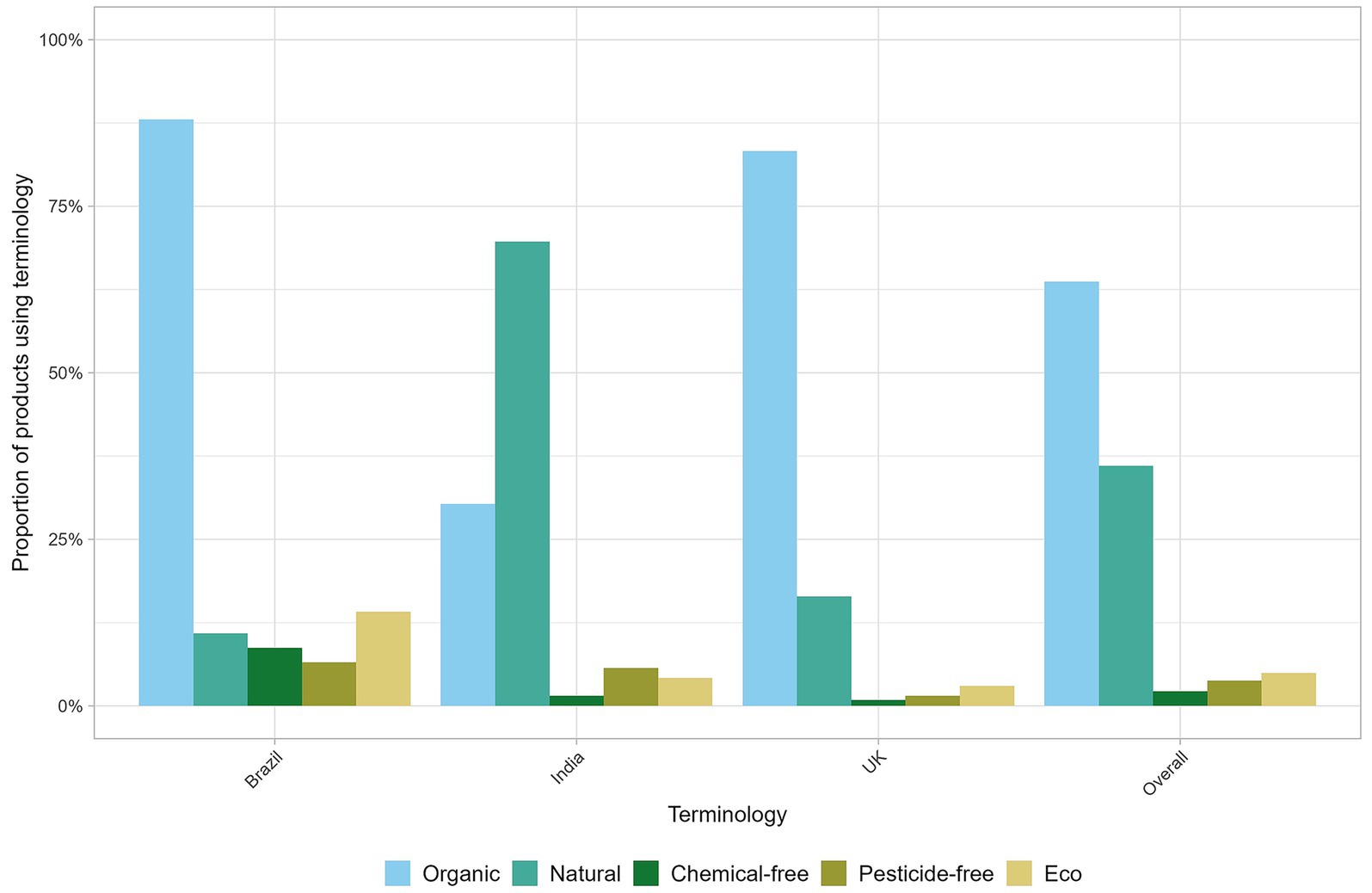

3.4.1 Product: terminologies and certification

‘Organic’ was the most frequently used term in both Brazil (88% of sustainable products used the term ‘organic’) and the UK (83%), however, in India, ‘natural’ was the most-used term (70% of sustainable products versus 30% using ‘organic’) (Figure 3; Supplementary Table S9). Beverages had a more even split between the terms ‘organic’ (54%) and ‘natural’ (47%) – with this trend dominated in particular by beverages in India (90% of sustainable beverages used the term ‘natural’ compared to 12% for ‘organic’) – while fresh produce was more frequently associated with the term ‘organic’ (79%) (Supplementary Table S9).

Figure 3. Proportion of organic products using each terminology overall and by country (n = 691 organic products). We defined organic products as products that use the term ‘organic’ or one of the adjacent terms, including ‘natural’, ‘chemical-free’, ‘pesticide-free’, ‘bioproducts’, ‘bio’, ‘eco’, and ‘GMO-free’, including both certified and uncertified products. We calculated the proportion of products using a specific term – for example, ‘natural’ – out of the total number of organic products. We presented the proportions only for terms that were used by >10% products overall or in any country (‘bioproducts’, ‘bio’, and ‘GMO-free’ terms were thus excluded). Proportions and counts of all terms are presented by country and product category in Supplementary Table S9.

A majority of organic products were certified in Brazil (89%) and the UK (78%) whereas only one-third were certified in India (Supplementary Table S10). Certification was higher in supermarkets (84% of all organic products), relative to stationary small local vendors (39%) and mobile vendors (44%). Chickpeas (86%), bananas (82%), and lentils (79%) had the highest proportion certified organic of the 14 sentinel products. All products labelled as ‘bio’, ‘bioproducts’, or ‘chemical-free’ were certified.

The most common types of certification were ‘organic’ standards (Supplementary Table S11), including IBD Brasil and Produto Organico in Brazil, India Organic, USDA Organic and Jaivik Bharat in India, and the Soil Association and EU Green Leaf in the UK.

3.4.2 Price: discounts

Only 8% of organic products were sold with a discount or price promotion (Supplementary Table S12). The proportion of organic products sold with a price promotion was higher in the UK and Brazil (9%) than in India (5%).

3.4.3 Place: product positioning

The most common approach to displaying organic products was a dispersed arrangement (68%), whereby organic products are displayed next to their non-organic counterparts (Supplementary Table S13). Only 14% of organic products were displayed in a cluster alongside other organic products, while 18% were sold in mostly organic stores. Dispersed arrangements were common in India (66%) and the UK (77%), while Brazil had a more even split of dispersed (46%) and clustered (42%) arrangements. Disaggregated by product type, most products were displayed in a dispersed arrangement, except for lentils and tomatoes, which were split between clustered and dispersed, and mangos, which were mainly clustered. Millets had the highest proportion sold in mostly organic stores (44%), with most sales occurring in India.

Organic products were predominantly positioned in the middle of the store (52% of all organic products), with only a small proportion (17%) in a position of prominence at the front; this trend was replicated across each country (Supplementary Table S14). Overall and across countries, organic products were predominantly positioned on the middle third of the shelf display (60%).

3.4.4 Promotion: brands, themes, and promotional materials

Brand prominence varied by country and product type, with strong representation of store own-brands, large international and national brands (Unilever, Coca-Cola, Amazon, Tata Consumer Products, ITC Limited), independent organic brands, and conventional brands offering organic options (Supplementary Table S15).

The most common themes used in marketing organic products were health benefits (43% of organic products), followed by environmental benefits (33%), quality (30%), taste (26%), and social justice (26%) (Figure 4; Supplementary Table S16). In Brazil, there was a lower presence of marketing themes on organic products and a more equitable spread of topics. In India, health was a predominant focus of organic marketing (59% of all organic products), while in the UK, environmental benefits were the most frequent theme (50%).

Figure 4. Proportion of organic products displaying each theme overall and by country (n = 691 organic products). We defined organic products as products that use the term ‘organic’ or one of the adjacent terms, including ‘natural’, ‘chemical-free’, ‘pesticide-free’, ‘bioproducts’, ‘bio’, ‘eco’, and ‘GMO-free’, including both certified and uncertified products. We calculated the proportion of these organic products that employ different marketing themes, including promoting the health benefits, environmental benefits, quality, taste, social justice characteristics, tradition or cultural characteristics, or lifestyle associated with the product. Proportions and counts of all themes are presented by country in Supplementary Table S16.

Only 6% of organic products featured promotional materials overall, with low rates (<10%) across all countries (Supplementary Table S17). Amongst products featuring promotional materials, 61% featured shelf signage, 34% were large promotional displays, 7% involved signage external to the store, and 2% involved an in-store product representative. The themes featured on these promotional materials ranged from advertising the quality of the products (50%), to emphasising their health (36%) or environmental benefits (34%), taste (23%), social justice impacts (11%), and their links to tradition or culture (7%).

4 Discussion

We found that only 37% of the 808 retailers surveyed across Brazil, India and the UK sold at least one of 14 commonly consumed sentinel organic foods or beverages, suggesting limited availability of organic foods and beverages. Moreover, organic rice was significantly more expensive than conventional rice, posing a barrier to consumers. There were notable regional differences in the way organic foods and beverages were marketed to consumers, with variation in both theme and terminology, suggesting that the drivers of consumer demand for these products may differ around the world, necessitating context-specific marketing strategies. The large variety of terms, themes and certification standards used to promote organic foods and beverages may also be contributing to consumer confusion regarding the benefits and authenticity of organic products. As this is the first systematic evaluation of food environment domains for organic products, more work is needed to inform interventions to promote consumer demand for organic foods and beverages.

Consistent with previous research showing organic consumption is concentrated in higher-income countries (Willer et al., 2025), we found greater availability of organic products in the UK (59%) than in India (32%) and Brazil (21%). India had a substantially higher number of organic vendors (155 versus 26 in Brazil), which may reflect general differences in the retail food environment, with India having high volumes of daily mobile vendors of fresh fruits and vegetables, while in Brazil, recurrent pop-up markets (known as Feira Livres) popular amongst organic consumers are available only on set days (Organis, 2023; Zinkhan et al., 1999). Our finding that only 7% of vendors in São Paulo sold an organic option was comparable with a prior study of Campinas in Brazil, which found that 6% of commercial food establishments were organic pop-up markets, although the study excluded organic options available at other vendor types, such as supermarkets (Grilo et al., 2022). To our knowledge, no previous studies have evaluated organic food availability in the UK or India. Contrary to our expectations that larger cities would have higher organic availability (Curl et al., 2013), we found no clear trend in availability by city size.

At the neighbourhood level, we expected greater organic availability in higher-income areas. While organic vendors in higher-income areas tended to offer a higher median number of organic sentinel products than organic vendors in lower-income neighbourhoods, the actual proportion of vendors offering at least one organic option was not higher in higher-income neighbourhoods in India and the UK, contrary to expectations. This may be due to the limitation of surveying only one neighbourhood per income level, which could mask intra-city variation. Additionally, we did not capture data on the volume of organic products sold per vendor, so it is possible that higher-income neighbourhoods have a higher absolute volume of organic products, even if they do not have a higher proportional availability of organic vendors. Future research could replicate the study in several neighbourhoods per income-level and repeat it at multiple points in time to capture variation in neighbourhood availability and the presence of pop-up markets, as well as confirming the generalisability of our findings. Increasing the availability of granular demographic data – including, for example, median household income level – at the neighbourhood level within cities would greatly enhance the ability of future research to examine the association between organic food availability and income-level within and between cities.

Variety is an important dimension of availability in the food environment (Bodor et al., 2008; Duran et al., 2016; Turner et al., 2018). Amongst the population of vendors that sold at least one organic product, we found that the median number of organic sentinel products sold was one (out of a possible 14 products), suggesting that the variety of organic options available to consumers in retail food environments is low. Only 47% of organic vendors surveyed globally stocked more than one organic option for at least one product type, implying that consumers’ choices regarding brands and price points remain limited. The low variety of organic products could be partly due to the methodological limitation of selecting only 14 sentinel products, though we tried to reduce this bias by selecting a diversity of product categories and staples such as flour, rice and milk. Additionally, the survey was conducted in different months per city, which may have affected the comparability of the absolute frequency of organic fresh produce in different cities and countries, particularly in LMIC food environments where there is higher seasonal variability, especially amongst informal vendors (Turner et al., 2018) and in rural households (Kapoor et al., 2024). However, given the rising dominance of supermarkets in LMICs (Reardon et al., 2012; Reardon et al., 2003; Turner et al., 2018), this seasonality of diets is decreasing, especially in urban areas (Kapoor et al., 2024). Regardless, this limitation is mitigated by presenting both the absolute and relative frequency of organic options for each product; as such, even if a specific product had lower overall availability in a given month of data collection, the proportion of this volume that was organic should remain relatively unchanged.

There is debate as to whether organic products behave as normal goods – whereby lower prices stimulate demand, while higher prices disincentivise purchase – or as luxury goods, for which higher prices signal superior quality and discounts act as a deterrent (Aschemann-Witzel and Zielke, 2017; Bastounis et al., 2021; Rodiger and Hamm, 2015; Yiridoe et al., 2005). Studies suggest that most organic consumers are responsive to price promotions, while a subset of consumers treat organics as a luxury good, although existing evidence is sparse (Sadler et al., 2024b). We found that only 8% of organic products were sold with a discount, suggesting that this is not a common marketing strategy used by retailers. Our findings corroborate existing evidence that organic foods and beverages are typically more expensive than their conventional counterparts (Aschemann-Witzel and Zielke, 2017; Lupolt et al., 2019; Marian et al., 2014; Rodiger and Hamm, 2015). We found that the median price of organic rice was substantially higher than conventional rice, raising concerns about the affordability of organic products.

In recent years, there has been a proliferation of terminologies used in reference to sustainable agriculture, including terms such as ‘organic’, ‘natural’, ‘chemical-free’, and ‘pesticide-free’ (Abrams et al., 2010; Kuchler et al., 2020; Nitzko, 2024). Preliminary research into consumer perceptions has shown that consumers often conflate the terms ‘organic’, ‘natural’, and ‘pesticide-free’, presuming that they refer to similar practices or product characteristics (Abrams et al., 2010; Kuchler et al., 2020; Nitzko, 2024). However, products advertised with these terms may differ substantially in practice, with the term ‘natural’, for example, sometimes referring to the absence of additives or used as a marketing technique to evoke sentiments of products being closer to nature, without any specific regulations on the production side restricting the use of synthetic chemical pesticides or fertilisers (Aarset et al., 2004; Abrams et al., 2010). There is therefore some concern that the term ‘natural’ could be used to mislead customers to purchase products that require less regulation (Abrams et al., 2010; Kuchler et al., 2020). More generally, there is some concern that the proliferation of alternative terminologies to ‘organic’ could contribute to consumer confusion and thus erode their trust in certified ‘organic’ products (Abrams et al., 2010; Gullo, 2016; Henryks and Pearson, 2010; Kuchler et al., 2020).

We found that ‘organic’ was the most frequently used terminology globally, as well as in the UK and Brazil. ‘Natural’ was the next most frequent term, driven primarily by its prominence in India, where it was the most common term, likely due to the current political salience of natural farming (Bhattacharya, 2017; Fitzpatrick et al., 2022; Münster, 2018; PM India, 2024; Veluguri et al., 2021). The related terms ‘chemical-free’ and ‘pesticide-free’ were common in Brazil and India, but not in the UK, perhaps due to its more stringent labelling requirements. While the variety of terminologies may indeed be contributing to consumer confusion and thus act as a barrier to demand, they also offer a potential opportunity for differentiated marketing. For example, in India, the growing segment of ‘pesticide-free’ products are positioning themselves as a more affordable alternative to certified ‘organic’ products, as they restrict the use of synthetic pesticides but not fertilisers, thus offering a lower price point to consumers and a more palatable option to farmers worried about profitability losses from potential yield dips with organic production (Khandelwal et al., 2022). In LMIC contexts, alternatives to certified ‘organic’ products may offer a more affordable way for consumers to access safer and more sustainable products and could be integrated as part of future policy approaches to increasing sustainable consumption.

Many consumers report a lack of trust in the authenticity of organic products, particularly in the context of higher prices for organic food items (Basha and Lal, 2019; Tandon et al., 2020). Certification programs, such as organic standards and quality assurance programs, have been implemented in many countries as a means of verifying that products are authentically organic (Bastounis et al., 2021; Potter et al., 2021). We found that only 62% of all products (Brazil: 89%; India: 34%; UK: 78%) were certified. This suggests that the availability of certified organic foods is even lower than what we have reported above, particularly in India. The relatively low presence of certification in India may be due to the higher presence of ‘natural’ foods, for which certification schemes are not yet in force. It may also be due to the higher presence of mobile vendors, for which certification rates were low (44%). The dominant forms of certification present on the packaging were third-party audit systems, such as USDA, India Organic, Soil Association, and IBD Brasil. Participatory guarantee system (PGS) logos did not appear in our dataset, despite the growing prevalence of these peer-based certification schemes in countries like Brazil and India, suggesting that this has not yet proliferated as a common consumer-facing option in the urban retail food environment. This raises some concerns, as PGS certification is intended to provide a more affordable and feasible certification option for small and marginal farmers, for whom third-party certification can be prohibitively expensive (González and Nigh, 2005; Home et al., 2017; Nelson et al., 2010; Sacchi, 2015). A government report on the organic sector in India indicated that PGS certified products are not yet favoured by branded distributors and thus are typically sold informally (CRISIL and APEDA, 2024). The absence of PGS-certified products even amongst less formal vendors in our sample thus highlights a need for future policy interventions to enhance the marketability of these products, in order to ensure profitability of PGS-certified farmers. In India, no fruits and vegetables were certified, unlike in Brazil and the UK. This may be due to the comparatively lower volumes of certified organic fruits and vegetables in India relative to packaged goods (CRISIL and APEDA, 2024) or could indicate challenges at the vendor end in communicating the certification status for predominantly unpackaged goods.

The positioning of foods and beverages within a retail store has an important impact on consumer purchases (Hollands et al., 2019; Shaw et al., 2020). Studies of the positioning of organic products within a store found that arranging organic products in a cluster, rather than alongside non-organic counterparts, positively impacted consumer demand (Groeppel-Klein and Kamm, 2014; Sadler et al., 2024b; van Herpen et al., 2012). Interestingly, we found that most organic products were displayed alongside their conventional counterparts in a dispersed (68%) rather than cluster-based (14%) arrangement. Previous studies of organic product arrangement did not disaggregate by product type; however, their inclusion of similar products to our survey (tea, milk, rice, and coffee, alongside additional products) suggests that their findings that cluster-based arrangements were more effective apply to these product types, whereas our results indicate that tea, milk, rice, and coffee were all more frequently displayed in dispersed rather than clustered arrangements (Supplementary Table S13). This indicates that implementation of organic product positioning diverges in practice from research recommendations. However, the current dispersed approach to product arrangement aligns with research on plant-based meat replacement products, wherein dispersed arrangements have been shown to be more effective at increasing purchases of meat replacements (Piernas et al., 2021; Plant Based Food Association, 2020; Vandenbroele et al., 2021). Future research evaluating the relative effectiveness of dispersed versus clustered arrangements for organic products is needed.

Research suggests consumers’ intention to purchase organic and other sustainable products is driven by a variety of factors, including their perceived healthiness, benefits to the environment and animal welfare, as well as product-related attributes such as taste and quality (Hansmann et al., 2020; Katt and Meixner, 2020; Kushwah et al., 2019; Massey et al., 2018; Schleenbecker and Hamm, 2013). Some studies have suggested that organic marketing is more effective when abstract themes (such as environmental health) are used, as opposed to concrete, detailed or personal themes (such as human health), due to the perceived abstract nature of the concept of organic (Jäger and Weber, 2020; Loebnitz et al., 2022). While our study is unable to test the effectiveness of organic marketing on consumer purchases, we found a higher presence collectively of concrete, personal themes (such as human health and product quality and taste), although abstract themes such as environmental impacts and social justice were also present.

The use of promotional materials in retail food environments has been shown to increase demand for organic products amongst some subsets of consumers and for certain product types (Sadler et al., 2024b). Shelf signage has shown mixed effectiveness in previous studies (Sadler et al., 2024b), yet it was the most common form of promotional material across all countries included in our study. This may be due to its ease of implementation, while large displays and exterior signage require higher investment and likely would be linked to brand-specific advertisement. The most common themes on these promotional materials were environmental and health benefits, consistent with the thematic focuses on packaging above.

As previously mentioned, consumer demand for organic foods and beverages is influenced by the food environment, including both the personal domain (accessibility, affordability, desirability, and convenience) and external domain (availability, prices, vendor and product characteristics, and marketing and regulation) (Turner et al., 2018). This study focused on documenting the external domain of the food environment for organic foods and beverages through a vendor-oriented market basket survey tool. Therefore, while we were able to capture external factors such as the prices and availability of organic foods and beverages in the food environment, we were not able to measure the corresponding personal dimensions of affordability and accessibility of these products, which vary at the individual consumer level (Turner et al., 2018). As such, while the results of our study can inform efforts to boost availability, reduce price premiums, and enhance marketing characteristics of organic products in order to increase consumer demand, personal factors also mediate consumers’ purchasing decisions. Existing research has explored some personal factors, such as organic product desirability, through consumer surveys and interviews (Katt and Meixner, 2020; Kushwah et al., 2019; Massey et al., 2018; Wier et al., 2008). However, future research that links external factors such as organic vendor availability with consumer-level data – such as the relative location of the home, consumer purchasing power, and perceived desirability of organic products – would help to further illuminate the complex interactions between the personal and external domains in influencing consumer demand for organic foods and beverages.

Collectively, our findings indicate a need for a more evidence-based strategy in marketing organic foods and beverages to consumers. This will require multi-stakeholder efforts including public-private partnerships to build consumer confidence in, and awareness of, certification logos and the key benefits associated with organics. Denmark has historically provided a strong example of collaborative organic interventions through their ‘organic action plans,’ which have taken a demand-side approach that couples government procurement and state-led certification with a common messaging campaign about the benefits of organics (Daugbjerg, 2023; Sørensen et al., 2016). Another example of public-private coordination in organic marketing is L’Agence Bio’s (The Organic Agency in France)5 annual organic campaign, ‘Le Printemps Bio’ (The Organic Spring), which aims to bring public awareness to the organic sector and has shown documented success at increasing sales of private label organic milk brands, although further evidence is required (Bougherara et al., 2022). Public information campaigns to increase awareness of, and trust in, participatory forms of organic certification – which aim to enhance the inclusion and profitability of small and marginal farmers in accessing organic markets – could be especially useful, given the absence of PGS-certified products in our surveyed vendor sites. There is a particular need for well-designed evaluations of organic marketing interventions, which incorporate control groups and a pre-post design, especially in LMICs where there is a dearth of evidence on the effectiveness of marketing interventions at increasing consumer demand for organic products (Sadler et al., 2024b). Studies that aim to test the effectiveness of public informational and other promotional campaigns, product placement interventions (clustering versus dispersed arrangements), and product labelling interventions (such as different certification logos) in LMIC contexts would be particularly valuable (Sadler et al., 2024b).

Beyond marketing interventions, there is a clear need for broader structural change to support greater availability and affordability of organic foods and beverages in Brazil, India, and the UK, which we expect will be relevant in other HIC and LMIC contexts, as well. The price differential between organic and conventional products is not only a result of marketing interventions that aim to advertise the ‘premium’ nature of the products. Rather, organic products are often more expensive than their conventional counterparts because of the relatively higher costs of organic production and distribution, particularly given the smaller volumes of organic products (Michalke et al., 2023), as well as the subsidisation of chemical-based inputs in contexts such as India (Tandon and Aggarwal, 2021), and the failure to incorporate the environmental externalities of chemical-based production into conventional food prices (Michalke et al., 2023). Efforts to incorporate ‘true cost accounting’ or other transparent pricing methods (Michalke et al., 2023) and to restructure subsidies to support organic production and distribution infrastructure could help to balance out the price differential. Additionally, efforts to increase access to certified organic products with shorter supply chains (such as farmers’ markets), or to provide marketing opportunities for alternative sustainable products (such as uncertified organic or ‘natural’ or ‘pesticide-free’ products) could offer a more affordable alternative pathway, particularly for lower-income consumers or in economies such as India and Brazil where there is a larger informal sector (Cáceres, 2005; Khandelwal et al., 2022). The growth of e-commerce may also present an opportunity to increase the availability and affordability of organic foods and beverages. India, for example, is already leveraging their large informal sector to provide immediate, small-volume delivery of sustainable and healthy products directly to consumers’ homes (Laxmikanth, 2024; Nautiyal and Lal, 2025) and also launched a partnership in 2025 between the Ministry of Cooperation, a large milk cooperative (Amul), and a home delivery e-commerce platform, offering a promising pathway towards increasing organic food availability (Ministry of Cooperation, 2025). Overall, there is a clear need for further research and implementation of market-side initiatives to boost demand for organic foods and beverages in order to encourage a shift towards more sustainable food systems.

Data availability statement

The datasets presented in this study can be found in online repositories. The names of the repository/repositories and accession numbefs) can be found in the article/Supplementary material.

Author contributions

AS: Conceptualization, Data curation, Formal analysis, Investigation, Methodology, Project administration, Writing – original draft, Writing – review & editing. YB: Conceptualization, Data curation, Investigation, Methodology, Writing – review & editing. JT: Data curation, Formal analysis, Investigation, Methodology, Writing – review & editing. DA: Writing – review & editing. ES: Data curation, Formal analysis, Investigation, Methodology, Writing – review & editing. KB: Data curation, Methodology, Writing – review & editing. LJ: Conceptualization, Data curation, Investigation, Methodology, Supervision, Writing – review & editing.

Funding

The author(s) declare that financial support was received for the research and/or publication of this article. AS was supported by a studentship from the Natural Environment Research Council and LJ was supported by a Future Leaders Fellowship from UKRI (Grant Ref: MR/T044527/1).

Acknowledgments

We thank the following data collectors for their work in surveying vendors across Brazil, India and the UK: A. M. Bertolini, A. Bellows, A. de Oliveira, A. Singh, A. Sooraj, A. Thawre, D. de Sousa Roger, D. Mujmule, D. Veluguri, D. Wayal, Daas, E. M. F. Pereira, G. Lovakumar, G. Rigote, Gangarao, H. N. G. Pinheiro, I. de Oliveira Parente Martins, I. Wiputra, J. Souza Borges, L. Ahirrao, M. E. M. da Silva, M. H. Amaral, M. M. S. Mesquita, Pratiksha, R. Naik, R. Varma, Ravi, S. Kumar, S. Ramesh, Sallaama, Tirupathi.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Generative AI statement

The authors declare that no Gen AI was used in the creation of this manuscript.

Any alternative text (alt text) provided alongside figures in this article has been generated by Frontiers with the support of artificial intelligence and reasonable efforts have been made to ensure accuracy, including review by the authors wherever possible. If you identify any issues, please contact us.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Supplementary material

The Supplementary material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fsufs.2025.1670638/full#supplementary-material

Footnotes

1. ^For the Brazil cities and for London, the relevant city data collection coordinators additionally collected data on apples, potatoes, eggs, and chicken, as they were deemed to be commonly available products and the coordinators were interested in locally-specific analysis of these additional products. However, these products were not included in the results presented in this global paper as they were not collected for all cities and countries.

2. ^In our detailed protocol, we stated that we would convert the Indian and Brazilian currencies to British pounds; however, for comparability to other published market basket surveys (Chaudhry et al., 2021; Kirk et al., 2019; Lucan et al., 2015; Lupolt et al., 2019), which often publish in US dollars (USD), we decided to convert all three currencies to USD.

3. ^The protocol originally stated that we would use the Mann–Whitney test for organic availability; however, this test is appropriate for samples with only two comparison groups. We compared three countries, three cities per country, and three neighbourhoods per city. We therefore chose to use the Kruskall-Wallis test, which expands the Mann–Whitney test to comparison groups higher than two.

4. ^In this paper, the use of the term organic without quotation marks is an umbrella term that includes both products labelled specifically with the term ‘organic’, as well as the broader range of terms similar to organic, including ‘natural’, ‘chemical-free’, ‘pesticide-free’, ‘bioproduct’, ‘bio’, ‘eco’, and ‘GMO-free’. The use of the term ‘organic’ in quotation marks refers to products labelled specifically with the term ‘organic’. Unless explicitly specified, results relating to organic products include both certified and uncertified products.

5. ^‘L’Agence Bio’ (The Organic Agency) is a French public interest group that brings together public and private sector representatives to coordinate the development and promotion of French organic production and consumption (L’Agence Bio, 2025).

References

Aarset, B., Beckmann, S., Bigne, E., Beveridge, M., Bjorndal, T., Bunting, J., et al. (2004). The European consumers’ understanding and perceptions of the “organic” food regime. Br. Food J. 106, 93–105. doi: 10.1108/00070700410516784

Abrams, K. M., Meyers, C. A., and Irani, T. A. (2010). Naturally confused: consumers’ perceptions of all-natural and organic pork products. Agric. Hum. Values 27, 365–374. doi: 10.1007/s104609-9234-5

Ahmed, S., Kennedy, G., Crum, J., Vogliano, C., McClung, S., and Anderson, C. (2021). Suitability of data-collection methods, tools, and metrics for evaluating market food environments in low- and middle-income countries. Foods 10:d. doi: 10.3390/foods10112728

APEDA. (2024). Fresh fruits & vegetables [WWW document]. Available online at: https://apeda.gov.in/FreshFruitsAndVegetables (accessed January 9, 2025).

Aschemann-Witzel, J., and Zielke, S. (2017). Can’t buy me green? A review of consumer perceptions of and behavior toward the price of organic food. J. Consum. Aff. 51, 211–251. doi: 10.1111/joca.12092

Basha, M. B., and Lal, D. (2019). Indian consumers’ attitudes towards purchasing organically produced foods: an empirical study. J. Clean. Prod. 215, 99–111. doi: 10.1016/J.JCLEPRO.2018.12.098

Bastounis, A., Buckell, J., Hartmann-Boyce, J., Cook, B., King, S., Potter, C., et al. (2021). The impact of environmental sustainability labels on willingness-to-pay for foods: a systematic review and Meta-analysis of discrete choice experiments. Nutrients 13:2677. doi: 10.3390/nu13082677

Bhattacharya, N. (2017). Food sovereignty and agro-ecology in Karnataka: interplay of discourses, identities, and practices. Dev. Pract. 27, 544–554. doi: 10.1080/09614524.2017.1305328

Birmingham City Council (2019). Deprivation in Birmingham: Analysis of the 2019 indices of deprivation. Birmingham, UK:

Bodor, J. N., Rose, D., Farley, T. A., Swalm, C., and Scott, S. K. (2008). Neighbourhood fruit and vegetable availability and consumption: the role of small food stores in an urban environment. Public Health Nutr. 11, 413–420. doi: 10.1017/S1368980007000493

Bougherara, D., Ropars-Collet, C., and Saint-Gilles, J. (2022). Impact of private labels and information campaigns on organic and fair trade food demand. J. Agric. Food Ind. Org. 20, 39–59. doi: 10.1515/jafio-2019-0018

Brazilian Institute of Geography and Statistics (IBGE) (2022). Censo Demográfico 2022. Rio de Janeiro: IBGE.

Cáceres, D. (2005). Non-certified organic agriculture: an opportunity for resource-poor farmers? Outlook Agric. 34, 135–140. doi: 10.5367/000000005774378775

Candiotto, L. Z. P. (2018). Organic products policy in Brazil. Land Use Policy 71, 422–430. doi: 10.1016/j.landusepol.2017.12.014

Chaudhry, M., Jaacks, L. M., Bansal, M., Mahajan, P., Singh, A., and Khandelwal, S. (2021). A direct assessment of the external domain of food environments in the National Capital Region of India. Front. Sustain. Food Syst. 5:726819. doi: 10.3389/fsufs.2021.726819

City of Edinburgh Council (2022). Edinburgh locality and Ward profiles. Edinburgh: City of Edinburgh Council.

CRISIL and APEDA (2024). Study of Indian organic market and export promotion strategy. CRISIL Limited & APEDA.

Curl, C. L., Beresford, S. A. A., Hajat, A., Kaufman, J. D., Moore, K., Nettleton, J. A., et al. (2013). Associations of organic produce consumption with socioeconomic status and the local food environment: multi-ethnic study of atherosclerosis (MESA). PLoS One 8:e69778. doi: 10.1371/journal.pone.0069778

Daugbjerg, C. (2023). Using public procurement of organic food to promote pesticide-free farming: a comparison of governance modes in Denmark and Sweden. Environ. Sci. Pol. 140, 271–278. doi: 10.1016/j.envsci.2022.12.012

Duran, A. C., Almeida, S. L., Latorre, M. d. R. D., and Jaime, P. C. (2016). The role of the local retail food environment in fruit, vegetable and sugar-sweetened beverage consumption in Brazil. Public Health Nutr. 19, 1093–1102. doi: 10.1017/S1368980015001524

Duvall, C. S., Howard, P. H., and Goldsberry, K. (2010). Apples and oranges? Classifying food retailers in a Midwestern US city based on the availability of fresh produce. J. Hunger Environ. Nutr. 5, 526–541. doi: 10.1080/19320248.2010.527281

Ellis, E. C., Klein Goldewijk, K., Siebert, S., Lightman, D., and Ramankutty, N. (2010). Anthropogenic transformation of the biomes, 1700 to 2000. Glob. Ecol. Biogeogr. 19, 589–606. doi: 10.1111/j.1466-8238.2010.00540.x

Erler, M., Keck, M., and Dittrich, C. (2022). The changing meaning of millets: organic shops and distinctive consumption practices in Bengaluru, India. J. Consum. Cult. 22, 124–142. doi: 10.1177/1469540520902508

FAO, GAIN, WOF (2022). Assessment of retail food environments and green spaces for healthy cities: Methodological guidance based on the experiences in Dar Es Salaam, Lima, Tunis. Rome: FAO.

FAO, IFAD, IFAD, UNICEF, WFP, and WHO (2021). The state of food security and nutrition in the world 2021. Transforming food systems for food security, improved nutrition and affordable healthy diets for all FAO. Rome: FAO.

Fitzpatrick, I. C., Millner, N., and Ginn, F. (2022). Governing the soil: natural farming and bionationalism in India. Agric. Hum. Values 39, 1391–1406. doi: 10.1007/s10460-022-10327-0

Garcia, X., Garcia-Sierra, M., and Domene, E. (2020). Spatial inequality and its relationship with local food environments: the case of Barcelona. Appl. Geogr. 115:102140. doi: 10.1016/j.apgeog.2019.102140

González, A. A., and Nigh, R. (2005). Smallholder participation and certification of organic farm products in Mexico. J. Rural. Stud. 21, 449–460. doi: 10.1016/j.jrurstud.2005.08.004

Grilo, M., de Menezes, C., and Duran, A. (2022). Food swamps in Campinas, Brazil. Ciênc. Saúde Coletiva 27, 2717–2728. doi: 10.1590/1413-81232022277.17772021EN

Grimm, M., Luck, N., and Steinhübel, F. (2023). Consumers’ willingness to pay for organic rice: insights from a non-hypothetical experiment in Indonesia. Aust. J. Agric. Resour. Econ. 67, 83–103. doi: 10.1111/1467-8489.12501

Groeppel-Klein, A., and Kamm, F. (2014). Space utilisation and retail store image: how the arrangement of organic foods impacts on the overall image of retail stores. Marketing ZFP 36, 69–81. doi: 10.15358/0344-1369_2014_2_69

Gullo, E. (2016). The European Union solution: fighting the American epidemic of consumer confusion in the organic food industry. J. Int. Bus. Law. 16, 119–138. Available at: https://scholarlycommons.law.hofstra.edu/jibl/vol16/iss1/11

Halpern, B. S., Frazier, M., Verstaen, J., Rayner, P.-E., Clawson, G., Blanchard, J. L., et al. (2022). The environmental footprint of global food production. Nat. Sustain. 5, 1027–1039. doi: 10.1038/s41893-022-00965-x

Hansmann, R., Baur, I., and Binder, C. R. (2020). Increasing organic food consumption: an integrating model of drivers and barriers. J. Clean. Prod. 275:123058. doi: 10.1016/j.jclepro.2020.123058

Henryks, J., and Pearson, D. (2010). Misreading between the lines: consumer confusion over organic food labelling. Aust. J. Commun. 37, 73–86.

HLPE (2019). Agroecological and other innovative approaches for sustainable agriculture and food systems that enhance food security and nutrition. Rome: High Level Panel of Experts on Food Security and Nutrition of the Committee on World Food Security, Rome.

Hollands, G. J., Carter, P., Anwer, S., King, S. E., Jebb, S. A., Ogilvie, D., et al. (2019). Altering the availability or proximity of food, alcohol, and tobacco products to change their selection and consumption. Cochrane Database Syst. Rev. 9:2573. doi: 10.1002/14651858.CD012573.pub3

Home, R., Bouagnimbeck, H., Ugas, R., Arbenz, M., and Stolze, M. (2017). Participatory guarantee systems: organic certification to empower farmers and strengthen communities. Agroecol. Sustain. Food Syst. 41, 526–545. doi: 10.1080/21683565.2017.1279702

Jäger, A.-K., and Weber, A. (2020). Increasing sustainable consumption: message framing and in-store technology. Int. J. Retail Distrib. Manage. 48, 803–824. doi: 10.1108/IJRDM-02-2019-0044

Kapoor, M., Ravi, S., Rajan, S., Dhamija, G., and Sareen, N. (2024). Changes in India’s food consumption and policy implications: A comprehensive analysis of household consumption expenditure survey 2022–23 and 2011–12 (no. EAC-PM/WP/30/2024), EAC-PM working paper series. New Delhi: Economic Advisory Council to the Prime Minister (EAC-PM), Government of India.

Katt, F., and Meixner, O. (2020). A systematic review of drivers influencing consumer willingness to pay for organic food. Trends Food Sci. Technol. 100, 374–388. doi: 10.1016/j.tifs.2020.04.029

Khandelwal, A., Agarwal, N., Jain, B., Gupta, D., John, A. T., and Cox, P. F. (2022). Scaling up sustainability through new product categories and certification: two cases from India. Front. Sustain. Food Syst. 6:1014691. doi: 10.3389/fsufs.2022.1014691

Khurana, A., and Kumar, V. (2020). State of organic and natural farming: Challenges and possibilities. New Delhi, India: Centre for Science and Environment.

Kirk, B., Melloy, B., Iyer, V., and Jaacks, L. M. (2019). Variety, Price, and consumer desirability of fresh fruits and vegetables in 7 cities around the world. Curr. Dev. Nutr. 3:nzz085. doi: 10.1093/cdn/nzz085

Kuchler, F., Bowman, M., Sweitzer, M., and Greene, C. (2020). Evidence from retail food markets that consumers are confused by natural and organic food labels. J. Consum. Policy 43, 379–395. doi: 10.1007/s10603-018-9396-x

Kushwah, S., Dhir, A., Sagar, M., and Gupta, B. (2019). Determinants of organic food consumption. A systematic literature review on motives and barriers. Appetite 143:104402. doi: 10.1016/j.appet.2019.104402

L’Agence Bio. (2025). Qui sommes nous? L’Agence Bio. L’Agence Bio. Available online at: https://www.agencebio.org/qui-sommes-nous/ (accessed February 9, 2025).

Laxmikanth, P. (2024). The taste of homemade: trusting ‘healthy’ food on app-based delivery services in Hyderabad, India. J. Cult. Econ. 22, 1–18. doi: 10.1080/17530350.2024.2378473

Lee, R. Y., Seitzinger, S., and Mayorga, E. (2016). Land-based nutrient loading to LMEs: a global watershed perspective on magnitudes and sources. Environ. Dev. 17, 220–229. doi: 10.1016/j.envdev.2015.09.006

Loebnitz, N., Frank, P., and Otterbring, T. (2022). Stairway to organic heaven: the impact of social and temporal distance in print ads. J. Bus. Res. 139, 1044–1057. doi: 10.1016/j.jbusres.2021.10.020

Lucan, S. C., Maroko, A. R., Sanon, O., Frias, R., and Schechter, C. B. (2015). Urban farmers’ markets: accessibility, offerings, and produce variety, quality, and price compared to nearby stores. Appetite 90, 23–30. doi: 10.1016/j.appet.2015.02.034

Lupolt, S., Buczynski, A., Zota, A. R., and Robien, K. (2019). Development of a healthy and sustainable food availability inventory (HSFAI): an assessment of Washington, DC, grocery stores. J. Hunger Environ. Nutr. 14, 365–380. doi: 10.1080/19320248.2018.1434098

Machado, S. T., Mendes dos Reis, J. G., Maniçoba da Silva, A., Bueno, R. C., and Tanaka, W. Y. (2018). Brazilian consumers’ preference towards fruits: The drivers of Banana, Orange, lemon and apple supply chain. Presented at the International Conference on Information Systems. Lyon, France: Logistics and Supply Chain.

Marian, L., Chrysochou, P., Krystallis, A., and Thogersen, J. (2014). The role of price as a product attribute in the organic food context: an exploration based on actual purchase data. Food Qual. Prefer. 37, 52–60. doi: 10.1016/j.foodqual.2014.05.001

Massey, M., O’Cass, A., and Otahal, P. (2018). A meta-analytic study of the factors driving the purchase of organic food. Appetite 125, 418–427. doi: 10.1016/j.appet.2018.02.029

McCarthy, J. E. (1975). Basic marketing: A managerial approach. Homewood, Ill: Richard D. Irwin, Inc.

Meemken, E. M. (2020). Do smallholder farmers benefit from sustainability standards? A systematic review and meta-analysis. Glob. Food Sec. 26:100373. doi: 10.1016/j.gfs.2020.100373

Michalke, A., Köhler, S., Messmann, L., Thorenz, A., Tuma, A., and Gaugler, T. (2023). True cost accounting of organic and conventional food production. J. Clean. Prod. 408:137134. doi: 10.1016/j.jclepro.2023.137134

Ministry of Cooperation. (2025). Secretary, Ministry of Cooperation attends signing of MoU between Ministry of Cooperation and Swiggy Instamart for onboarding of the cooperative dairy and other products. Available online at: https://www.pib.gov.in/www.pib.gov.in/Pressreleaseshare.aspx?PRID=2124533 (accessed September 2, 2025).

Morland, K., and Filomena, S. (2007). Disparities in the availability of fruits and vegetables between racially segregated urban neighbourhoods. Public Health Nutr. 10, 1481–1489. doi: 10.1017/S1368980007000079

Münster, D. (2018). Performing alternative agriculture: critique and recuperation in zero budget natural farming, South India. J. Politic. Ecol. 25:22388. doi: 10.2458/v25i1.22388

Muthayya, S., Sugimoto, J. D., Montgomery, S., and Maberly, G. F. (2014). An overview of global rice production, supply, trade, and consumption. Ann. N. Y. Acad. Sci. 1324, 7–14. doi: 10.1111/nyas.12540

My, N. H. D., Demont, M., Van Loo, E. J., de Guia, A., Rutsaert, P., Tuan, T. H., et al. (2018). What is the value of sustainably-produced rice? Consumer evidence from experimental auctions in Vietnam. Food Policy 79, 283–296. doi: 10.1016/j.foodpol.2018.08.004

Nautiyal, S., and Lal, C. (2025). Navigating organic consumption in emerging markets: a comparative study of consumer preferences and market realities in India. Br. Food J. 127, 2065–2090. doi: 10.1108/BFJ-10-2024-1064

Nelson, E., Tovar, L. G., Rindermann, R. S., and Cruz, M. A. G. (2010). Participatory organic certification in Mexico: an alternative approach to maintaining the integrity of the organic label. Agric. Hum. Values 27, 227–237. doi: 10.1007/s10460-009-9205-x

Nitzko, S. (2024). Consumer evaluation of food from pesticide-free agriculture in relation to conventional and organic products. Farming System 2:100112. doi: 10.1016/j.farsys.2024.100112

Office for National Statistics (2022). Estimates of the population for the UK, England, Wales, Scotland, and Northern Ireland. Office for National Statistics.

Piernas, C., Cook, B., Stevens, R., Stewart, C., Hollowell, J., Scarborough, P., et al. (2021). Estimating the effect of moving meat-free products to the meat aisle on sales of meat and meat-free products: a non-randomised controlled intervention study in a large UK supermarket chain. PLoS Med. 18:e1003715. doi: 10.1371/journal.pmed.1003715

Plant Based Food Association. (2020). PBFA and Kroger plant-based meat study. Plant Based Foods Association. Available online at: https://www.plantbasedfoods.org/marketplace/pbfa-and-kroger-plant-based-meat-study/ (accessed September 26, 2022).

PM India. (2024). News updates: Launch of National Mission on natural farming. Available online at: https://www.pmindia.gov.in/en/news_updates/launch-of-national-mission-on-natural-farming/#:~:text=NMNF%20aims%20at%20promoting%20NF,dependency%20to%20externally%20purchased%20inputs (accessed January 23, 2025).

Potter, C., Bastounis, A., Hartmann-Boyce, J., Stewart, C., Frie, K., Tudor, K., et al. (2021). The effects of environmental sustainability labels on selection, purchase, and consumption of food and drink products: a systematic review. Environ. Behav. 53, 891–925. doi: 10.1177/0013916521995473

Prefeitura da Cidade do Rio de Janeiro (2018). Rendimento nominal familiar per capita, segundo Bairros ou grupos de Bairros, no Município do Rio de Janeiro em 2000/2010. Rio de Janeiro: Prefeitura da Cidade do Rio de Janeiro.

Raina, R., Mishra, S., Ravindra, A., Balam, D., and Gunturu, A. (2022). Reorienting India’s agricultural policy: millets and institutional change for sustainability. J. Ecol. Soc. 34, 1–15. doi: 10.54081/JES.028/01

Reardon, T., Timmer, P., Barrett, C., and Berdegué, J. (2003). The rise of supermarkets in Africa, Asia, and Latin America. Am. J. Agric. Econ. 85, 1140–1146. doi: 10.1111/j.0092-5853.2003.00520.x

Reardon, T., Timmer, C. P., and Minten, B. (2012). Supermarket revolution in Asia and emerging development strategies to include small farmers. Proc. Natl. Acad. Sci. 109, 12332–12337. doi: 10.1073/pnas.1003160108

Rede Nossa São Paulo. (2022). Mapa da Desigualdade. Rede Nossa São Paulo. São Paulo: Rede Nossa São Paulo.

Rodiger, M., and Hamm, U. (2015). How are organic food prices affecting consumer behaviour? A review. Food Qual. Prefer. 43, 10–20. doi: 10.1016/j.foodqual.2015.02.002

Rothman, K. J. (1990). No adjustments are needed for multiple comparisons. Epidemiology 1, 43–46. doi: 10.1097/00001648-199001000-00010

Sacchi, G. (2015). The development of participatory guarantee systems for organic agriculture: comparison of experiences worldwide. Econ. Agro-Aliment. 17, 77–92. doi: 10.3280/ECAG2015-002005

Sadler, A., Jaacks, L., Shankar, E., Yandrapu, B., Tereza da Silva, J., and Bassetto, K. (2024a). The availability, affordability, and marketing characteristics of organic food: A comparative food environment assessment. OSF Registries.

Sadler, A., Moran, D., and Jaacks, L. (2024b). Effectiveness of real-world marketing of organic foods and beverages: a systematic review of recent evidence. PLoS Sustain. Transform. 3:e0000123. doi: 10.1371/journal.pstr.0000123

Schleenbecker, R., and Hamm, U. (2013). Consumers’ perception of organic product characteristics. A review. Appetite 71, 420–429. doi: 10.1016/j.appet.2013.08.020

Shaw, S. C., Ntani, G., Baird, J., and Vogel, C. A. (2020). A systematic review of the influences of food store product placement on dietary-related outcomes. Nutr. Rev. 78, 1030–1045. doi: 10.1093/nutrit/nuaa024

Sørensen, N. N., Tetens, I., Løje, H., and Lassen, A. D. (2016). The effectiveness of the Danish organic action plan 2020 to increase the level of organic public procurement in Danish public kitchens. Public Health Nutr. 19, 3428–3435. doi: 10.1017/S1368980016001737

Tandon, A., and Aggarwal, R. (2021). “Evaluating the role of subsidies in sustainable agriculture: a case study of India” in Indian agriculture under the shadows of WTO and FTAs: Issues and concerns. eds. R. Sudesh Ratna, S. K. Sharma, R. Kumar, and A. Dobhal (Singapore: Springer), 161–176.

Tandon, A., Dhir, A., Kaur, P., Kushwah, S., and Salo, J. (2020). Why do people buy organic food? The moderating role of environmental concerns and trust. J. Retail. Consum. Serv. 57:102247. doi: 10.1016/j.jretconser.2020.102247

Tang, F. H. M., Lenzen, M., McBratney, A., and Maggi, F. (2021). Risk of pesticide pollution at the global scale. Nat. Geosci. 14, 206–210. doi: 10.1038/s41561-021-00712-5

Turner, C., Aggarwal, A., Walls, H., Herforth, A., Drewnowski, A., Coates, J., et al. (2018). Concepts and critical perspectives for food environment research: a global framework with implications for action in low- and middle-income countries. Glob. Food Secur. 18, 93–101. doi: 10.1016/j.gfs.2018.08.003

Turner, C., Kalamatianou, S., Drewnowski, A., Kulkarni, B., Kinra, S., and Kadiyala, S. (2020). Food environment research in low- and middle-income countries: a systematic scoping review. Adv. Nutr. 11, 387–397. doi: 10.1093/advances/nmz031

United Nations, Department of Economic and Social Affairs, Population Division (2018). World urbanization prospects. United Nations: The 2018 revision.