Lucie Kvasničková Stanislavská1

Lucie Kvasničková Stanislavská1 Ladislav Pilař1*

Ladislav Pilař1* Martin Fridrich2

Martin Fridrich2 Roman Kvasnička3

Roman Kvasnička3 Lucie Pilařová1Bilal Afsar4Matthew Gorton5

Lucie Pilařová1Bilal Afsar4Matthew Gorton5- 1Department of Management, Faculty of Economics and Management, Czech University of Life Sciences in Prague, Prague, Czechia

- 2Department of Informatics, Faculty of Business and Management, Brno University of Technology, Brno, Czechia

- 3Department of Systems Engineering, Faculty of Economics and Management, Czech University of Life Sciences in Prague, Prague, Czechia

- 4Department of Management Sciences, Hazara University, Mansehra, Pakistan

- 5Newcastle University Business School, Newcastle University, Newcastle Upon Tyne, United Kingdom

Achieving sustainability is a major challenge faced by many societies. The increasing moral consciousness of stakeholders has put pressure on companies, forcing these companies to include long-term policies that reflect the regionally specific needs of stakeholders. Using a structural topic model, this study identified differences between developing and developed countries with respect to sustainability disclosures. Data were obtained from 2100 sustainability reports published in the United Nations Global Compact database for the year 2020. In global terms, these sustainability reports addressed three main topics: 1) human rights, 2) diversity, equity, and inclusion, and 3) sustainable production. Moreover, the sustainability reports from developing and developed countries incorporated different communication strategies. Based on the prevalence (rate of occurrence) of content, sustainability reports from developed countries predominantly communicated issues related to “sustainable production” and “supply chain emissions”, whereas sustainability reports from developing countries more frequently communicated issues related to “education” and “human rights".

1 Introduction

Achieving sustainable production and consumption are among the biggest challenges of the 21st century (Karagiannis et al., 2022). An organisation’s ability to create long-term sustainable value is influenced by the management of relations with critical stakeholders (Ramadhini et al., 2020). The high level of stakeholder interest in social and environmental issues (Helmig et al., 2016; Latip et al., 2022) is one of the driving factors for development of corporate social responsibility (CSR) programs (Ying et al., 2021). CSR refers to a company’s voluntary actions to integrate sustainability as part of its business strategy (Osagie et al., 2016). To maintain competitiveness, companies must therefore not only operate according to a sustainable business model (Schaltegger et al., 2016) but also inform their stakeholders about this model (Stutz et al., 2022). Reports on sustainability reports have therefore become frequent in corporate reporting, as performance in the area of social responsibility is a key factor in determining the value of a company and its intangible assets (Patara and Dhalla, 2022).

According to KPMG (KPMG, 2020), approximately 80% of the top 100 companies by revenue in 52 countries and jurisdictions, called N100 companies, now publish sustainability reports. This represents a 68% increase compared with 1993, when KPMG started collecting data on sustainability reports. Sustainability reports, also called corporate responsibility reports (de Klerk and de Villiers, 2012), are important documents through which companies indicate their commitment to seriously consider issues of social and environmental responsibility (Fisher et al., 2019). Sustainability reporting positively affects consumers’ knowledge, trust, and perception of a company’s reputation (Hasseldine et al., 2005; Widiarto Sutantoputra, 2009; Antonia García-Benau et al., 2013; Kim, 2019), a company’s financial performance (Margolis et al., 2009; Angelia and Suryaningsih, 2015; Azzam et al., 2020; Ting, 2021), organisational appeal for potential employees (Kim and Park, 2011; Lis, 2012; Joo et al., 2016; Tkalac Verčič and Sinčić Ćorić, 2018), and a company’s market value (Berthelot et al., 2012; Plumlee et al., 2015), as well as reducing a company’s equity (Dhaliwal et al., 2011). These effects involved the three basic pillars of sustainability, economic, social and environmental activity (Księżak and Fischbach, 2018), which are implemented according to regional context (Bezzola et al., 2022).

This positive effect of sustainability reporting has resulted in an exponential increase in the number of sustainability reports worldwide, thus providing the opportunity to examine global CSR trends and to identify social and environmental problems targeted by CSR in a given locality (Randles, 2013) through regional segmentation. Previous studies focused on analysis of reports at the national level (Amin et al., 2021; Garanina and Aray, 2021; Ting, 2021), or compared selected regions of the world (Goloshchapova et al., 2019; Mućko, 2021; Saeed and Zamir, 2021). Moreover, the dimensions covered in these sustainability reports, and variations in these reports across different countries, remain unclear. This study addressed the identified gaps in previous research and attempted to answer the following questions: What are the main topics that appear in sustainability reports at the global level? Are there any differences in sustainability reporting between developing and developed countries? Do the reports cover all key dimensions of sustainability (i.e., economic, environmental, and social dimensions)? Do companies reflect the sustainable development goals (SDGs) in their sustainability reports?

Based on these research questions, this study aims to identify differences in sustainability reporting between developed and developing countries through a new research approach based on structural topic modelling.

2 Corporate sustainability and corporate social responsibility

Corporate sustainability is an approach in which companies not only set economic goals but also set social and environmental goals, specifically those related to sustainable development, and create value for stakeholders (Massa et al., 2015) without compromising the demands of future generations (Carroll et al., 2017). This concept has been defined as a combination of the creation of long-term economic prosperity (economic domain), an enterprise’s contribution to social governance in society (social domain), and the ecological integrity of the enterprise and its efforts to reduce the size of its ecological footprint (environmental domain) (Miska et al., 2018). By contrast, corporate sustainability has also been defined as a company’s activities that proactively seek to contribute to the balance of sustainability, including economic, environmental, and social dimensions, a concept called the first balance (Lozano et al., 2016). This concept also includes a temporal dimension or an intergenerational perspective, which dynamically interacts with the afore-mentioned dimensions concerning the future, addressing the corporate system and its stakeholders. Although the concept of corporate sustainability has global significance and covers developing and developed economies and all sectors (Pazienza et al., 2022), the main problem with corporate sustainability is the lack of a general definition (Swarnapali, 2017).

The pillars of sustainability (social, economic, and environmental) (Purvis et al., 2019), also called the triple bottom line (Elkington, 1998), have been incorporated explicitly into the formulation of SDGs (UN – United Nations, 2012). Corporate sustainability may be implemented through the concept of CSR, as previously reported (Topal et al., 2009; Garay and Font, 2012; Kang et al., 2015; Elmualim, 2017; Belas et al., 2021; Sánchez-Teba et al., 2021). Moreover, CSR is regarded as nothing more than a transitional phase in achieving sustainability (Montiel and Delgado-Ceballos, 2014), further indicating that CSR is related to the pillars of sustainability.

2.1 Sustainability reporting

Companies can disclose their sustainable activities in many ways. Sustainability reports are an important part of a company’s communication strategy and, to a certain extent, still serve as a marketing tool for the company (Bartikowski and Berens, 2021; Ngai and Singh, 2021). Sustainability reports provide information about the economic, social, and environmental impacts of a business over a certain period of time (Wolniak and Hąbek, 2016). Information is provided not only for the company, but also to influence the decision-making process of stakeholders (Moravcikova et al., 2015). For example, investors use a firm’s social disclosure in making investment decisions (Lock and Seele, 2016; Verbeeten et al., 2016). Annual reports have emerged as the most frequently utilized communication channel for companies to report on their sustainability activities when such communication models first became mainstream (Ramdhony et al., 2010). These reports can facilitate adoption of a systematic approach to the management of socially responsible activities, identify future risks and opportunities, and thus help boost a company’s competitiveness and its potential to continue its socially responsible activities (Moravcikova et al., 2015). Annual sustainability reports are utilized more frequently by larger multinational corporations to ensure that they connect with a wider range of stakeholders, whereas small- and medium-sized organisations may forgo this practice in favour of more direct communications with their stakeholders, who are more likely to be based locally (Wensen et al., 2011). Different terms have been used to describe published documents reporting sustainability activities, including CSR reports, sustainability reports, and non-financial reports (Mućko, 2021). In this study, these documents will be called sustainability reports.

Although the publication of sustainability reports is largely regarded as voluntary, regulations that make publication mandatory for some companies are already in place (Mućko, 2021). For example, companies listed on the Chinese Shenzhen Stock Exchange, Shanghai Stock Exchange (Yu and Zheng, 2020), and London Stock Exchange (Hamed et al., 2022) are obliged to report their CSR activities. Moreover, the European Directive 2014/95/EU requires certain large undertakings and groups to publish non-financial reports (Dumitru et al., 2017).

One current drawback to sustainability reports is that those that are not regulated by standards or external guidelines may become nothing more than marketing tools (Tschopp, 2005; Jahdi and Acikdilli, 2009). There is therefore a growing pressure for corporate sustainability reports to be evaluated externally, thereby increasing the credibility of the published information (Perego and Kolk, 2012; Michelon et al., 2015). Independent auditors are becoming increasingly important, and focus on the development of recognized sustainability reporting guidelines (Berthelot et al., 2012) such as the Global Reporting Initiative 2013, the UN Global Compact, the World Business Council for Sustainable Development, and the initiative launched by the International Organisation for Standardisation, has increased considerably. Verification of sustainability reports by independent organisations increases both the credibility and quality of these reports (Pflugrath et al., 2011; Hąbek, 2017).

The growing number of published sustainability reports is also attracting attention from academia. These reports have been used in several studies evaluating the attitude of companies concerning sustainability disclosures (Mućko, 2021), the effects of CSR performance on external CSR assurance (Karaman et al., 2021), the motivation of companies to publish sustainability reports (Deegan, 2002), and the method by which state ownership, as well as host market location, influences the nature and content of sustainability reporting in Russia (Aray et al., 2021) and China (Marquis and Qian, 2014).

Inasmuch as the concept of sustainability reports was developed in Western countries (Idemudia, 2011), it is unsurprising that most of these reports are published in developed economies (Matten and Moon, 2008; Ali et al., 2017). Nevertheless, the number of sustainability reports published in developing economies has increased in recent years (Khan, 2010). Similar findings were observed in a KPMG survey of Sustainability Reporting (KPMG, 2020), which showed that the reporting of N100 companies worldwide rose by 5%–80% between 2017 and 2020. Although there have been above-average increases in certain developing countries, such as Kazakhstan (34%), Ecuador (31%), and Peru (15%), other developing economies are already among leaders in sustainability reporting, including Mexico (100%), India (98%), and Malaysia (93%).

Most enterprises in developing countries have already recognized the importance of CSR as a factor in their long-term success (Siwar and Harizan, 2009), although there are major differences in the determinants of sustainability disclosure between developed and developing countries. For example, public pressure to publish sustainability activities is lower for companies in developing than in developed countries (Ali et al., 2017). The main factor determining the publication of sustainability reports in developing countries tends to be stakeholders, such as international buyers, foreign investors, the international media, and international regulatory authorities (e.g., the World Bank).

2.2 Regional differences in sustainability reporting between developed and developing countries

Studies of differences in sustainability reporting between developing and developed countries show regional differences in the content, type, and extent of reporting (Dawkins and Ngunjiri, 2008; Vilar and Simão, 2015; Ali et al., 2017; Bhatia and Makkar, 2019; Sharma, 2019). Evaluation of content shows that reports from developing countries mainly address social performance, employees, and consumers, whereas reports from developed countries mainly address environmental performance (Bashtovaya, 2014). The main topic of sustainability reports in developed countries is management and reduction of environmental pollution, with these reports also emphasizing the support of groups within society (Sharma, 2019). By contrast, reports from developing countries mainly address investments in programs that positively affect living standards, such as investing in education or providing food and water. For example, CSR programs in developing countries focus on social areas through philanthropy, whereas programs in developed countries prioritize environmental issues (Khojastehpour and Jamali, 2021). Sustainability reports from developing countries place little emphasis on the area of human resources, such as equal opportunities for employees or the welfare of employees, whereas reports from developed countries did not prioritize community issues, such as donations/charities and community awareness programs (Bhatia and Makkar, 2019). Companies in both developed and developing countries assigned the highest importance to reporting on Customers and Products, such as product innovations or responsible marketing and communication. These findings indicate that sustainability reporting by companies is directed more at customers than at employees, as customers are regarded as the more important interest group.

Subsequent studies focused on the causes of differences in sustainability reporting by companies in developed and developing countries. Institutional factors (Welford, 2005; Bashtovaya, 2014), as well as political and economic conditions (Welford, 2005) have been reported responsible for these differences. Companies in developing countries, adapt to government programs and try to use sustainability activities to solve local social and economic issues (Sharma, 2019). Companies in developing countries may try to use their CSR programs to eliminate institutional gaps caused by corrupt governments or governments with insufficient resources (Visser, 2009). By contrast, companies operating in developed countries do not deal with issues such as lack of basic healthcare and education, regarding provision of these services to be the responsibility of their governments, thereby enabling them to invest in other areas as part of their CSR programs (Bhatia and Makkar, 2019).

Taken together, these findings indicate that sustainability policies in individual regions of the world reflect issues in these regions. Thus, analyses of sustainability reports would enable deeper insight into regional problems. None of the above-mentioned studies provides a comprehensive view of global sustainability reporting, as they only address selected parts of the world or compare selected countries. Although these studies showed differences in sustainability reporting in the analysed countries, they did not present a holistic view of the differences in sustainability reporting in developing and developed countries (Ali et al., 2017). Taken together, these findings highlight the need for comprehensive analyses of the contents of sustainability reports.

3 Materials and methods

This study used a computer-assisted strategy based on topic models and traditional qualitative reviews to analyse a large number of sustainability reports and contextualize possible findings. Although previous studies utilized a similar approach, those studies partially assumed identical topic distributions across external covariates (Goloshchapova et al., 2019; Zhou, 2021). To overcome this limitation, the present study used an STM (Roberts et al., 2016), which enabled incorporation of document metadata into the modelling process and further assessment of the relationships through simulations (Egami et al., 2018).

3.1 Structural topic model

An STM is classified as a non-linear generative probability model, a type of model that relies on an anticipated problem structure (document-topic, topic-word distributions) and calibration of its parameters with actual observations (texts) using iterative methods. In addition, an STM enables incorporation of external metadata. Inner workings can be described to a high level using plate notation. The model consists of three conceptual elements: (1) a document-topic component, (2) a topic-word component, and (3) a core language model that removes both sources of variation to produce actual topic-word assignments (Roberts et al., 2016).

The first component, the document-topic distribution, follows a log-normal probability distribution with the product of document covariates and outlining the expected value and the variation. The second component, the topic-word distribution, follows an exponential probability distribution based on the observed vocabulary and content covariates. Consequently, topic-word Dirichlet probability distributions using the respective components were reconciled using a non-conjugated variational expectation-maximization algorithm. Further details and technical implementation have been described (Roberts et al., 2016).

3.2 Topic quality

The FREX metric assesses topic quality with regard to exclusivity and word frequency. It is essential to offset these two outlooks because recurring terms are not usually exclusive to a specific topic and specific terms are not usually informative (Airoldi and Bischof, 2012), followed by moderation of both aspects with a weighted harmonic mean. For words and topics, the metric was defined as:

where w indicates weight,

Semantic coherence is influenced by the concept of pointwise mutual information and assumes that highly probable terms based on incoherent latent factors should co-occur within the exact text. Moreover, this metric approximates human judgment regarding topic quality (Mimno et al., 2011). Based on the words f_i and f_j, the metric for the set of the M most likely words in topic k can be expressed as:

where

3.3 Methodology and implementation

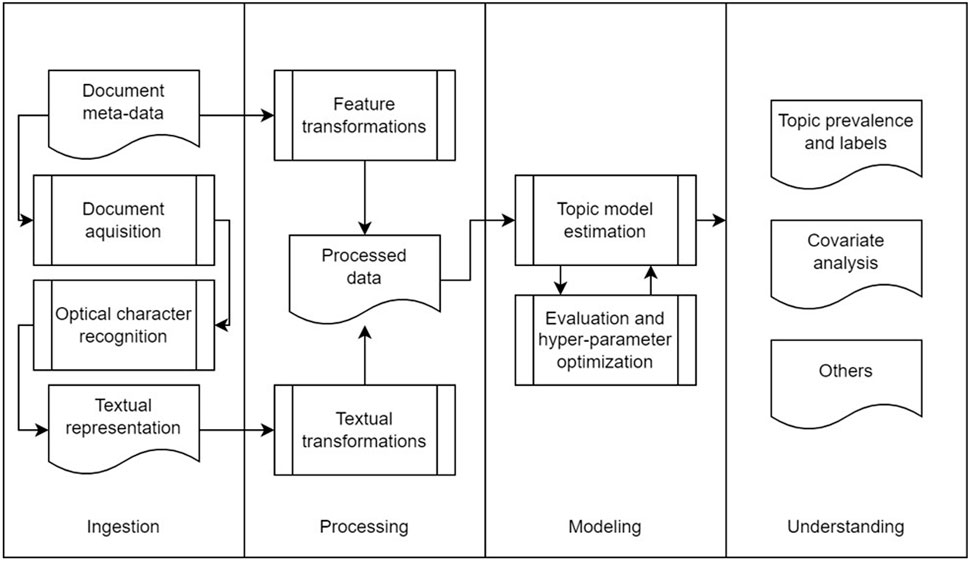

Topic modelling is an iterative process that consists of ingestion, processing, modelling, and understanding. The relationships between these steps are depicted in Figure 1. The solution is based on a systematic approach (Roberts et al., 2019), with essential modifications involving syntactical decomposition and model selection.

FIGURE 1. Building blocks of the iterative natural language processing pipeline. The crucial conceptual steps included Ingestion, Processing, Modelling, and Understanding.

3.3.1 Ingestion

The study sample consisted of 2100 sustainability reports, known as Communications on Progress (COPs), downloaded from the United Nations Global Impact database. In these reports, business participants inform company stakeholders about progress made during a given year in implementing the Global Compact principles in each of the four issue areas: human rights, labour, environment, and anti-corruption. Each COP had to contain three elements: 1) a statement by the chief executive expressing continued support for the Global Compact; 2) a description of practical actions taken by the company; and 3) a measurement of outcomes. The overall format of a COP is flexible, can be prepared in any language, and should be fully integrated into the company’s non-financial reports, e.g., a sustainability report (UN-United Nations, 2012). All English-language reports published in 2020 were included in the sample. Moreover, all documents were in portable document format (pdf), allowing extraction of textual information using the Tesseract open-source OCR tool (OCR, 2021).

3.4 Processing

In the second stage, both structured and unstructured input data were organized using two processing branches. The first branch retained the required metadata, i.e., type economy type. Countries with advanced economies were considered developed countries, whereas countries with emerging economies and emerging markets were considered developing countries, as determined by the International Monetary Fund (e.g., Wieser and Silfvenius, 2000; Nielsen, 2013; Ylyash, et al., 2021). These classifications were based on three criteria: per capita income, export diversification, and degree of integration into the global financial system.

The second branch dealt with unstructured textual data. First, all characters were converted to lower-case, special characters were removed, and multiple spaces were collapsed. Second, only unique texts longer than 1000 characters written in English were retained. Finally, a vectorized spaCy language model (Honnibal, et al., 2019) was used for parsing, lemmatization, tokenization, and part-of-speech tagging. Thus, original documents could be reconstructed with the relevant lemmas using preselected part-of-speech tags and frequency thresholds. This approach avoided the time-consuming process of manual stop-word selection and improved the computational time of downstream models; however, it may also adversely impact performance.

3.4.1 Modelling

The building blocks were subsequently assembled on the preprocessed texts and covariates used in the previous processing stage. This allowed the relationship between topical prevalence and external covariates to be determined and resolved the parameter estimation options. Finally, viable models were preselected for further interpretation by a human reader.

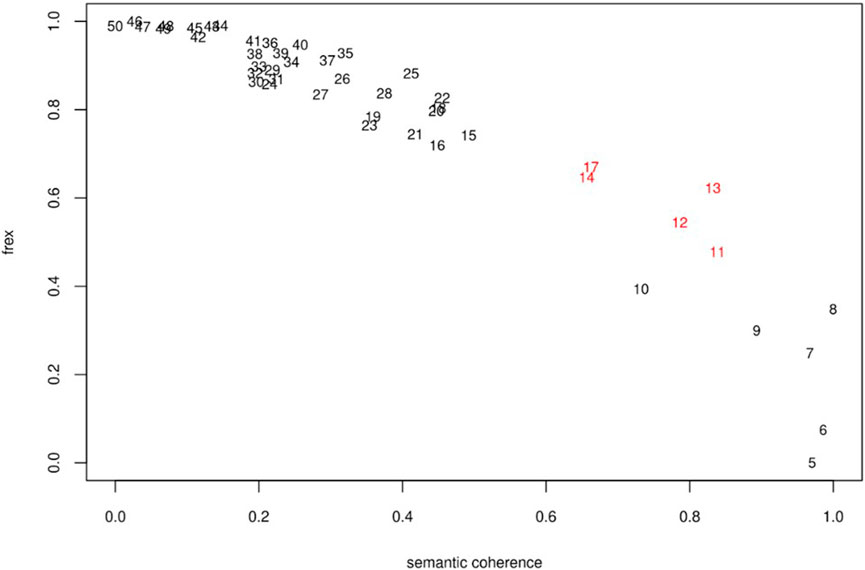

First, the topical prevalence was hypothesized to depend linearly on the one-hot encoded type of economy. The internal parameters of the topic model were initialized using the spectral method and further refined using an additional 750 expectation-maximization iterations. A grid search was performed over a range of 5–50 topics, and the model was evaluated using the average FREX and average semantic coherence. Optimization was approached as a no-preference multi-objective problem with a utopian solution. Non-dominated observations closest to the ideal state were set as candidates. The resulting subset consisted of five models covering 11–17 underlying topics. Figure 2 shows the model selection procedure, with dimensions scaled for comparability and candidate models in red.

FIGURE 2. Model quality trade-off between FREX and Semantic coherence concerning the feasible number of topics. The models on the non-dominated decision boundary and closest to the utopia point are depicted in red.

3.4.2 Understanding

A previously described approach (Roberts et al., 2019) was utilized to aid in interpretation of the imprinted model. However, the procedure was streamlined to (1) identify documents and tokens connected to particular topics, add labels, and estimate prevalence, and (2) describe associations between the latent factors and covariates. Representative tokens for each topic were obtained using the conditional probability of occurrence or FREX. Similarly, documents with a high prevalence of underlying factors were investigated. Consequently, the topic labels were suggested and discussed, and the overall topic prevalence was estimated. The expected difference between the classes of interest was computed using a simulation with global uncertainty (e.g., Roberts et al., 2019). The candidate set was explored and evaluated using the outlined strategy. This resulted in selection of an STM consisting of 11 latent factors, with an average semantic coherence of −7.89 and an average FREX of 9.05.

4 Results

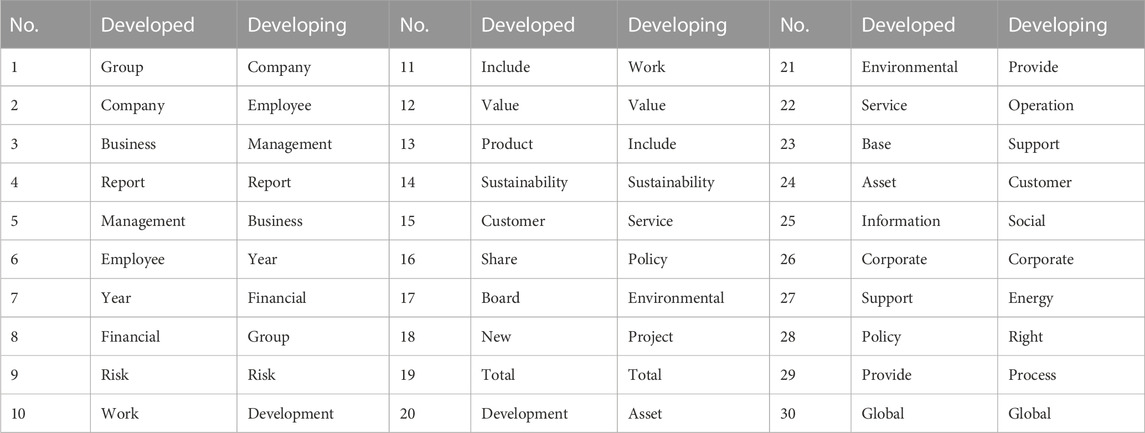

Frequency analysis of the 30 most used individual words (Table 1) revealed no important differences between developed and developing countries. The five most frequent words published in sustainability report in both developed and developing countries were “group”, “company”, “business”, “report”, and “management”. The word “employee” was in second place in developing countries, and in sixth place in developed countries. By contrast, the word “group” was in first place in developed countries and in eighth place in developing countries.

TABLE 1. The 30 most frequently used individual words in sustainability reports from developed and developing countries.

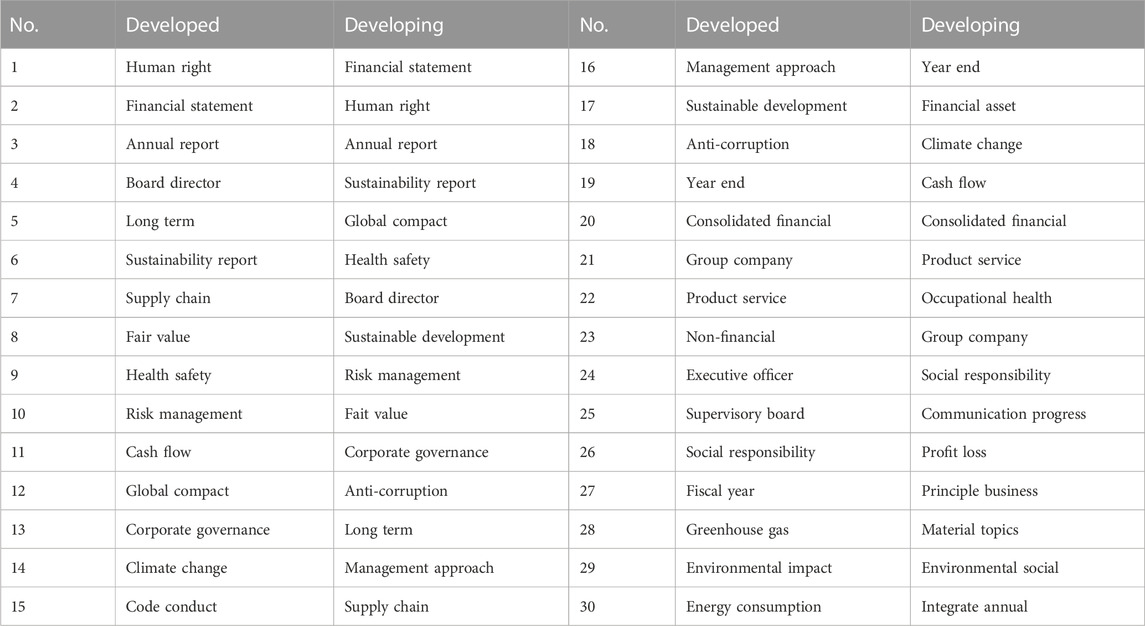

Frequency analysis of the 30 most used two-word connection or bigrams (Table 2), showed that the most significant representation of bigrams was also from the economic area of sustainability. The most frequent bigrams in reports from developed countries included “financial statement” (second place), “annual report” (third place), “board director” (fourth place), and “cash flow” (eleventh place), whereas the most frequent bigrams in reports from developing countries included “financial statement” (first place), “annual report” (third place), “board director” (seventh place), “cash flow” (nineteenth place), and others. In the social area, the most frequent bigrams in reports from developed countries included “human rights” (first place) and “health safety” (ninth place), whereas the most frequent bigrams in reports from developing countries included “human rights” (second place) and “health safety” (sixth place). In the environmental area, “climate change” appeared in third place in reports from developed and eighteenth place in reports from developing countries. Interestingly, the bigrams “greenhouse gas” (twenty-eighth place), “environmental impact” (twenty-ninth place), and “energy consumption” (thirtieth place) appeared in reports from developed but were not among the top 30 bigrams in developing countries. This finding indicates that developed countries place greater emphasis on topics associated with the environment.

TABLE 2. The 30 most frequently used two-word connections (bigrams) in sustainability reports from developed and developing countries.

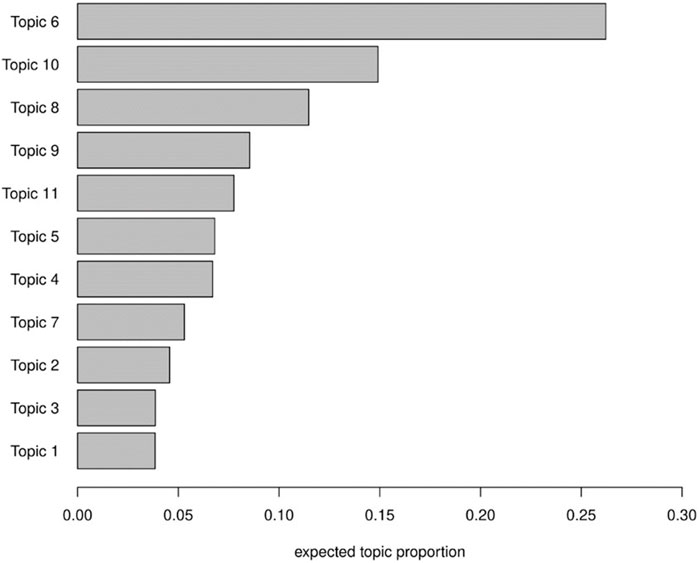

An STM was used to extract 11 topics, with Figure 3 showing their expected topic proportions.

FIGURE 3. Proportion of topics (x-axis) estimated by the final STM model, with topics sorted from the most to the least prevalent.

This study identified five main topics based on their expected proportion in sustainability reports: Human Rights; Diversity, Equity, and Inclusion (DEI); Sustainable Production; Education; and Global Reporting Initiative (GRI). The dominant topic from a global perspective was Human Rights. Table 3 shows the most frequent words within individual topics according to FREX and Prob. Conditional probability showed that the topic Human Rights included terms such as “employee”, “principle”, and “policy”; whereas FREX showed that the topic Human Right included terms such as “labour”, “discrimination”, “respect”, “communication”, and “staff”. The second most frequent topic was DEI, which included words such as “people”, “help”, “team”, and “community” as determined by Prob and terms such as “team”, “partnership”, “inclusion”, “leadership”, and “network” as determined by FREX. The third most frequent topic was Sustainable Production, which included words such as “sustainability”, “material”, “supplier”, “food”, and “waste” according to Prob and terms such as “food”, “production”, “plastic”, “forest”, “produce”, and “wood” according to FREX. The next most frequent topic was Education, which included words such as “employee”, “management”, and “training” according to Prob and terms such as “school”, “education”, “prevention”, and “child” according to FREX. Of the five topics, the least frequent was GRI, which included aspects relating to sustainability reporting initiative.

TABLE 3. Topic labels and defining tokens.

An extrapolation of individual topics revealed that the most frequently mentioned topics in sustainability reports were Human Rights and DEI. These issues are related (Lin et al., 2018; Hamed et al., 2022); for example, their joint application can have a positive impact on a company’s image (Bear et al., 2010) and can increase CSR performance (Harjoto et al., 2015). Topics associated with Sustainable Production were the third most prevalent.

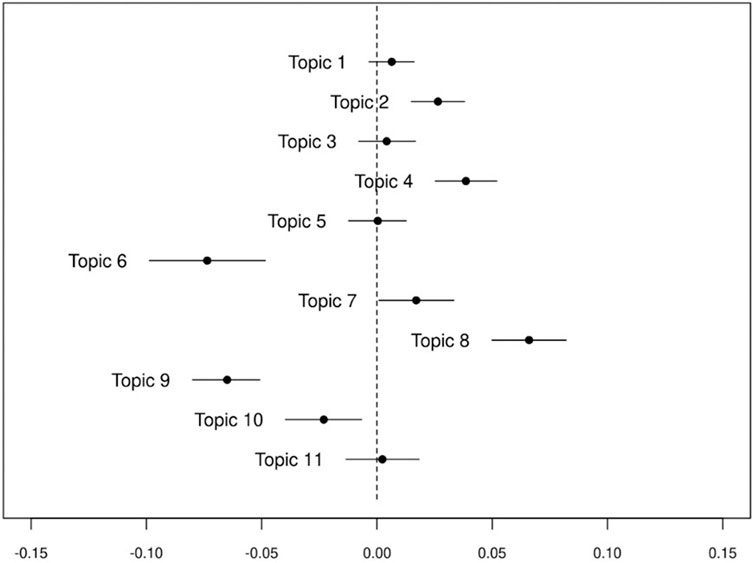

Figure 4 outlines differences in topic prevalence between developed and developing countries, including their respective 95% confidence intervals, with the dashed line representing no difference. The right side of the plot shows topics with a higher prevalence within developed countries, whereas the left side shows topics more frequent within developing countries. Sustainable Production, Supply Chain Emissions, and Value Management were more closely associated with sustainability reports from developed economies; whereas Human Rights, Education, and Diversity, Equity, and Inclusion initiatives were more prevalent within sustainability reports from developing economies. The prevalence of the remaining factors showed little (Financial Statements) to no (Corporate Governance, Risk Management, Energy Management) differences between developed and developing economies.

FIGURE 4. Estimated differences in topic prevalence as a function of the type of economy. A positive difference (x-axis) indicated higher prevalence in developed states, whereas a negative difference indicated higher prevalence in developing countries.

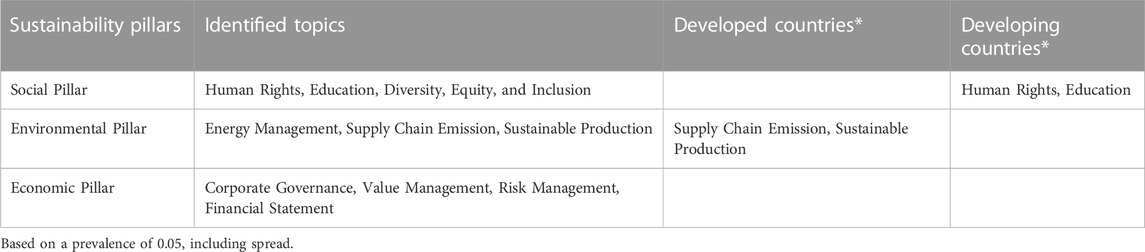

Table 4 shows the distribution of identified topics according to the individual dimensions of sustainability (social, environmental, and economic). Thematically, the economic dimension was the most frequently covered, but these were the four proportionally smallest identified topics. By contrast, the social dimension was proportionally the largest content in sustainability reports, with the topics Human Rights and DEI being the largest identified.

TABLE 4. Identified topics in relation to sustainability pillars.

Based on a prevalence of 0.05, including spread.

5 Discussion

5.1 Global view

The present results reveal that topics relating to human rights are highly prevalent worldwide in sustainability reports, thereby confirming the significant links between human rights and the CSR concept (Ramasastry, 2015; Wheeler, 2015; Obara and Peattie, 2018; Grosser and Tyler, 2021). Together with the finding that the second most prevalent topic was DEI, these results show that companies are responding to the challenge of the United Nations Sustainable Development Goals (United Nations, 2015) and are implementing diversity and inclusion rules in practice.

DEI has been closely linked to “human rights”, the importance of which was underlined by a 2013 initiative by governing bodies that called for the establishment of a World Health Organisation (WHO) initiative dealing with “Gender, Equity and Human Rights” (Magar et al., 2019). This initiative was designed to mainstream gender, equity, and human rights criteria across all organisational levels within a 5-year period. Gender, equity, and human rights were integrated to expose and analyse determinants lacking on barrier assessments, using the results of this analysis to reduce inequities and monitor progress through continual reporting. The aim of this scheme was to identify the causes of inequality and poor health and to identify solutions to these problems (Nidumolu et al., 2015).

DEI is a complex topic that involves factors such as age, race, ethnicity, cultural background, gender, sexual orientation, and religion. Society is now actively trying to reduce these inequalities by exerting pressure through various initiatives, such as the well-known #MeToo, #BlackLivesMatter, and #StopAAPIHate campaigns. These initiatives have encouraged individual companies to develop programs to reduce these inequities (Byerley, 2018; Prothero and Tadajewski, 2021). Indeed, one study shows that a single claim of sexual harassment could have a marked adverse impact on a company’s reputation (Does et al., 2018). Therefore, companies now strive to adopt a proactive approach by implementing anti-harassment policies and introducing mandatory training to prevent sexual harassment and the subsequent public outcry. Because investors are cautious regarding this issue, anti-sexual harassment policies are becoming a crucial criterion in investment-related decision-making. Thus, sustainability reports may play a key role in developing corporate culture, and demonstrate companies’ proactive strategies (Does et al., 2018).

Similar situations have been observed regarding race, ethnicity, age, and religion, whereby companies produce sustainability reports to prevent inappropriate behaviours, as well as to communicate their commitment to society (Schulz, 2017). Moreover, diversity with respect to age, professional tenure, and expertise can benefit company performance by, for example, enhancing innovation and worker productivity (Arioglu, 2021; Mothe and Nguyen-Thi, 2021). However, diversity in the workplace can also result in problems with communication, cooperation, and cohesion among employees, having a negative impact on the performance of the company (Kunze et al., 2011; Arioglu, 2021; Talavera et al., 2021). Efforts to enhance diversity should therefore be thought out correctly, and not just implemented.

Another important topic across regions was Sustainable Production. Sustainable production and consumption have received considerable attention in recent decades (Karagiannis et al., 2022) and have become standard elements in the agendas of policymakers and institutions, as well as being included in company strategies (Pilař et al., 2019).

5.2 Regional view

Analysis of regionally segmented topics showed that words associated with sustainable production and the environment were more prevalent in developed than in developing countries. Similar results were observed in a study examining the differences between developed and developing countries regarding perception of CSR on social media (Kvasničková Stanislavská et al., 2020). Large corporations in developed countries have long been pressured by their stakeholders to adopt a more sustainable approach (Hassini et al., 2012), with the results of the present study confirming that environmental issues are currently the main priority in Western countries (Kvasničková Stanislavská et al., 2020), with many initiatives in these countries, such as the 2030 Agenda, Rio+20, and the European Green Deal, focusing on this area. In developing countries, however, keeping product prices low is the main priority of stakeholders, and there is less demand for an environmental approach (Sardana et al., 2020). Companies in developing countries are concerned that increased sustainable production will actually have an adverse impact on competitiveness and profitability, as sustainability requires deployment of additional resources (Nidumoluet al., 2015). However, conditions regarding solid waste production (Das et al., 2019) and inadequate sustainable supply chain management (Ali and Kaur, 2021) have become alarming in many developing countries, suggesting that future sustainability reports will place greater emphasis on sustainable production.

The present study also found that the topic of education was more prevalent in sustainability reports from developing countries than from developed countries, in agreement with previous findings (Chapple and Moon, 2005; Makka and Nieuwenhuizen, 2018; Massoud et al., 2019). The developing world is facing problems that, to a large extent, could be resolved by improving education (Kvasničková Stanislavská et al., 2020), making it logical for companies in developing countries to devote special attention to education in their CSR programs.

These results identified several significant regional differences. Based on the definition of CSR as painting a picture of regional problems (Randles, 2013), the present study identified human rights and education as major issues in developing countries, as well as representing opportunities for socially responsible companies in these countries. By contrast, sustainable production and supply chain emissions were found to be major challenges for companies in developed countries.

5.3 The theoretical and practical implications

The many theoretical contributions of this study can be used by academics, company managers, and policymakers. First, to the best of our knowledge, there are no holistic views of sustainability reporting described to date. Although studies have identified several factors relevant to sustainability reporting (e.g., Bashtovaya, 2014; Bhatia and Makkar, 2019), the present study is the first (to the best of our knowledge) to analyse factors in detail. Second, a thorough comparison of sustainability reporting in developing and developed countries would add to the current body of knowledge. Third, the present study provided a methodological contribution by introducing an automated machine learning approach to analyse the contents of sustainability reports. Previous studies analysed the contents of these reports using the manual coding techniques commonly used in mainstream sustainability disclosure/communication research.

The results of the present study also have several key practical implications. These findings can be viewed from two perspectives. The first is a reflection of the regional issues dealt with by individual companies, with the activities addressing these issues included in sustainability reports. This perspective made possible the identification of Supply Chain Emission and Sustainable Production as key areas for developed countries and the identification of Human Rights and Education as key areas for developing countries. These findings may be important for policymakers, allowing them to prepare early for future challenges faced by their regions. The second perspective is the shift of individual areas from developing to developed countries. Improvements in lifestyle may result in the increased predominance in developing countries of factors encountered in developed countries. Business managers in developing countries should also consider that, although challenges vary among these countries, sustainability reports from developing countries should include factors such as sustainable production and supply chain emissions. Companies’ sustainability reports should include not only regional but also global aspects of sustainability, thereby communicating more effectively about their sustainability perspectives.

6 Future studies and limitations

The findings of this study reveal several opportunities for future studies. For example, follow-up studies can focus on individual industrial segments, determining whether there are any differences between individual areas of an economy, such as differences between services and industry. These studies can include comparisons between companies in the service and manufacturing sectors and/or a comparison between companies within the same sector.

Because DEI was the second most frequent topic in sustainability reports, further research should examine the qualitative aspects of DEI by focusing on the representation and strategies of individual areas of DEI in sustainability reports. These results should also be compared among individual countries and regions.

The present study had several limitations. First, it only included data from 2020. Thus, it did not evaluate changes in individual topics over time. Second, it used the World Bank classification of regional economies, which might not fully reflect differences between developing and developed countries.

7 Conclusion

Corporate sustainability is of global interest, but the challenges faced by individual companies differ by country and region. By analysing the contents of sustainability reports, the present study determined the method by which companies communicate sustainability. A structural modelling method was used to examine the content of sustainability reports from two basic perspectives—a global perspective and a regional perspective, according to the economic status of a country (i.e., developed or developing).

From a methodological point of view, this study represents a new approach to the analysis of sustainability reporting and contributes to the literature in several ways. First, this study provides a comprehensive view and new findings and insights into sustainability report publishing worldwide. To the best of our knowledge, this study is the first to examine sustainability reporting activities to such an extent, including all countries in the world that disclose sustainability reports through the United Nations Global Compact. Second, in examining sustainable activities included in sustainability reports, the study used an automated machine-learning approach rather than the manual coding technique commonly used in mainstream sustainability disclosure/communication research. Third, the study expands the literature by identifying differences in reporting of sustainable activities between developed and developing countries. Because CSR programs can be regarded as pictures of regional problems, identifying the main topics in these CSR programs can reveal the main problems within monitored regions.

Data availability statement

The raw data supporting the conclusion of this article will be made available by the authors, without undue reservation.

Author contributions

LK initiated the study and co-wrote the manuscript; LaP assessed the feasibility of the research and co-wrote the manuscript; MF processed the data and created a structural model; RK assessed the systematic quality and adequacy of the methodology; LuP co-wrote the manuscript: BA and MG revised the manuscript. All authors made a substantial contribution to the article and approved the final submitted version.

Funding

This study was supported by the Internal Grant Agency (IGA) of FEM CULS in Prague, registration 2022B0009—Application of artificial intelligence to regional segmentation using Big Data.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Airoldi, E. M., and Bischof, J. M. (2012). A Poisson convolution model for characterizing topical content with word frequency and exclusivity. available at: http://arxiv.org/abs/1206.4631 (Accessed Jun 18, 2012).

Ali, S. S., and Kaur, R. (2021). Effectiveness of corporate social responsibility (CSR) in implementation of social sustainability in warehousing of developing countries: A hybrid approach. J. Clean. Prod. 324, 129154. doi:10.1016/j.jclepro.2021.129154

Ali, W., Frynas, J. G., and Mahmood, Z. (2017). Determinants of corporate social responsibility (CSR) disclosure in developed and developing countries: A literature review. Corp. Soc. Responsib. Environ. Manag. 24 (4), 273–294. doi:10.1002/csr.1410

Amin, M. H., Mohamed, E. K. A., and Elragal, A. (2021). CSR disclosure on twitter: Evidence from the UK. Int. J. Account. Inf. Syst. 40, 100500. doi:10.1016/j.accinf.2021.100500

Angelia, D., and Suryaningsih, R. (2015). The effect of environmental performance and corporate social responsibility disclosure towards financial performance (case study to manufacture, infrastructure, and service companies that listed at Indonesia Stock Exchange). Procedia - Soc. Behav. Sci. 211, 348–355. doi:10.1016/j.sbspro.2015.11.045

Antonia García-Benau, M., Sierra-Garcia, L., and Zorio, A. (2013). Financial crisis impact on sustainability reporting. Manag. Decis. 51 (7), 1528–1542. doi:10.1108/MD-03-2013-0102

Aray, Y., Dikova, D., Garanina, T., and Veselova, A. (2021). The hunt for international legitimacy: Examining the relationship between internationalization, state ownership, location and CSR reporting of Russian firms. Int. Bus. Rev. 30 (5), 101858. doi:10.1016/j.ibusrev.2021.101858

Arioglu, E. (2021). Board age and value diversity: Evidence from a collectivistic and paternalistic culture. Borsa Istanb. Rev. 21 (3), 209–226. doi:10.1016/j.bir.2020.10.004

Azzam, M., AlQudah, A., Abu Haija, A., and Shakhatreh, M. (2020). The association between sustainability disclosures and the financial performance of Jordanian firms. Bus. Manag. 7 (1), 1859437. doi:10.1080/23311975.2020.1859437

Bartikowski, B., and Berens, G. (2021). Attribute framing in CSR communication: Doing good and spreading the word – but how? J. Bus. Res. 131, 700–708. doi:10.1016/j.jbusres.2020.12.059

Bashtovaya, V. (2014). CSR reporting in the United States and Russia. Soc. Responsib. J. 10 (1), 68–84. doi:10.1108/SRJ-11-2012-0150

Bear, S., Rahman, N., and Post, C. (2010). Corporate social responsibility and sustainability issues of small and medium-sized enterprises. J. Bus. Ethics 97 (2), 207–221. doi:10.1002/csr.2083

Belas, J., Çera, G., Dvorský, J., and Čepel, M. (2021). Corporate social responsibility and sustainability issues of small- and medium-sized enterprises. Corp. Soc. Responsib. Environ. Manag. 28 (2), 721–730.

Berthelot, S., Coulmont, M., and Serret, V. (2012). Do investors value sustainability reports? A Canadian study. Corp. Soc. Responsib. Environ. Manag. 19 (6), 355–363. doi:10.1002/csr.285

Bezzola, S., Günther, I., Brugger, F., and Lefoll, E. (2022). CSR and local conflicts in African mining communities. World Dev. 158, 105968. doi:10.1016/j.worlddev.2022.105968

Bhatia, A., and Makkar, B. (2019). CSR disclosure in developing and developed countries: A comparative study. J. Glob. Responsib. 11 (1), 1–26. doi:10.1108/JGR-04-2019-0043

Byerley, J. S. (2018). Mentoring in the era of #MeToo. JAMA 319 (12), 1199. doi:10.1001/jama.2018.2128

Carroll, A. B., Brown, J., and Buchholtz, A. K. (2017). Business and society: Ethics, sustainability and stakeholder management. 10th edition. Massachusetts, United States: Cengage Learning. 978-1305959828.

Chapple, W., and Moon, J. (2005). Corporate social responsibility (CSR) in asia. Bus. Soc. 44 (4), 415–441. doi:10.1177/0007650305281658

Das, S., Lee, S.-H., Kumar, P., Kim, K.-H., Lee, S. S., and Bhattacharya, S. S. (2019). Solid waste management: Scope and the challenge of sustainability. J. Clean. Prod. 228, 658–678. doi:10.1016/j.jclepro.2019.04.323

Dawkins, C., and Ngunjiri, F. W. (2008). Corporate social responsibility reporting in south Africa: A descriptive and comparative analysis. J. Bus. Commun. 45 (3), 286–307. doi:10.1177/0021943608317111

de Klerk, M., and de Villiers, C. (2012). The value relevance of corporate responsibility reporting: South African evidence. Meditari Account. Res. 20 (1), 21–38. doi:10.1108/10222521211234200

Deegan, C. (2002). Introduction. Account. Auditing Account. J. 15 (3), 282–311. doi:10.1108/09513570210435852

Dhaliwal, D. S., Li, O. Z., Tsang, A., and Yang, Y. G. (2011). Voluntary nonfinancial disclosure and the cost of equity capital: The initiation of corporate social responsibility reporting. Account. Rev. 86 (1), 59–100. doi:10.2308/accr.00000005

Does, S., Gundemil, S., and Shih, M. (2018). Research: How sexual harassment affects a company’s public image. available at: https://hbr.org/2018/06/research-how-sexual-harassment-affects-a-companys-public-image (Accessed June 11, 2018).

Dumitru, M., Dyduch, J., Gușe, R.-G., and Krasodomska, J. (2017). Corporate reporting practices in Poland and Romania – an ex-ante study to the new non-financial reporting European directive. Account. Eur. 14 (3), 279–304. doi:10.1080/17449480.2017.1378427

Egami, N., Fong, C. J., Grimmer, J., Roberts, M. E., and Stewart, B. M. (2018). How to make causal inferences using texts. available at: http://arxiv.org/abs/1802.02163 (Accessed Oct 19, 2022).

Elkington, J. (1998). Cannibals with forks – triple bottom line of 21st century business. Gabriola Island: New Society Publishers.

Elmualim, A. (2017). CSR and sustainability in FM: Evolving practices and an integrated index. Procedia Eng. 180, 1577–1584. doi:10.1016/j.proeng.2017.04.320

Fisher, R., van Staden, C. J., and Richards, G. (2019). Watch that tone. Account. Auditing Account. J. 33 (1), 77–105. doi:10.1108/AAAJ-10-2016-2745

Garanina, T., and Aray, Y. (2021). Enhancing CSR disclosure through foreign ownership, foreign board members, and cross-listing: Does it work in Russian context? Emerg. Mark. Rev. 46, 100754. doi:10.1016/j.ememar.2020.100754

Garay, L., and Font, X. (2012). Doing good to do well? Corporate social responsibility reasons, practices and impacts in small and medium accommodation enterprises. Int. J. Hosp. Manag. 31 (2), 329–337. doi:10.1016/j.ijhm.2011.04.013

Global Reporting Initiative (2013). G4 sustainability reporting guidelines. Amsterdam: Global Reporting Initiative.

Goloshchapova, I., Poon, S.-H., Pritchard, M., and Reed, P. (2019). Corporate social responsibility reports: Topic analysis and big data approach. Eur. J. Finance 25 (17), 1637–1654. doi:10.1080/1351847X.2019.1572637

Grosser, K., and Tyler, M. (2021). Sexual harassment, sexual violence and CSR: Radical feminist theory and a human rights perspective. J. Bus. Ethics 177, 217–232. doi:10.1007/s10551-020-04724-w

Hąbek, P. (2017). CSR reporting practices in visegrad group countries and the quality of disclosure. Sustainability 9 (12), 2322. doi:10.3390/su9122322

Hamed, R. S., Al-Shattarat, B. K., Al-Shattarat, W. K., and Hussainey, K. (2022). The impact of introducing new regulations on the quality of CSR reporting: Evidence from the UK. J. Int. Account. Auditing Tax. 46, 100444. doi:10.1016/j.intaccaudtax.2021.100444

Harjoto, M., Laksmana, I., and Lee, R. (2015). Board diversity and corporate social responsibility. J. Bus. Ethics 132 (4), 641–660. doi:10.1007/s10551-014-2343-0

Hasseldine, J., Salama, A. I., and Toms, J. S. (2005). Quantity versus quality: The impact of environmental disclosures on the reputations of UK plcs. Br. Account. Rev. 37 (2), 231–248. doi:10.1016/j.bar.2004.10.003

Hassini, E., Surti, C., and Searcy, C. (2012). A literature review and a case study of sustainable supply chains with a focus on metrics. Int. J. Prod. Econ. 140 (1), 69–82. doi:10.1016/j.ijpe.2012.01.042

Helmig, B., Spraul, K., and Ingenhoff, D. (2016). Under positive pressure. Bus. Soc. 55 (2), 151–187. doi:10.1177/0007650313477841

Honnibal, M., Montani, I., Honnibal, M., Peters, H., Landeghem, S., Samsonov, M., et al. (2019). explosion/spaCy: v2.1.7: Improved evaluation, better language factories and bug fixes. available at: https://zenodo.org/record/3358113/export/csl#.ZBkqzHZBx8M.

Idemudia, U. (2011). Corporate social responsibility and developing countries: Moving the critical CSR research agenda in Africa forward. Prog. Dev. Stud. 11 (1), 1–18. doi:10.1177/146499341001100101

Jahdi, K. S., and Acikdilli, G. (2009). Marketing communications and corporate social responsibility (CSR): Marriage of convenience or shotgun wedding? J. Bus. Ethics 88 (1), 103–113. doi:10.1007/s10551-009-0113-1

Joo, Y. R., Moon, H. K., and Choi, B. K. (2016). A moderated mediation model of CSR and organizational attractiveness among job applicants. Manag. Decis. 54 (6), 1269–1293. doi:10.1108/MD-10-2015-0475

Kang, J.-S., Chiang, C.-F., Huangthanapan, K., and Downing, S. (2015). Corporate social responsibility and sustainability balanced scorecard: The case study of family-owned hotels. Int. J. Hosp. Manag. 48, 124–134. doi:10.1016/j.ijhm.2015.05.001

Karagiannis, I., Vouros, P., Sioutas, N., and Evangelinos, K. (2022). Mapping the maritime CSR agenda: A cross-sectoral materiality analysis of sustainability reporting. J. Clean. Prod. 338, 130139. doi:10.1016/j.jclepro.2021.130139

Karaman, A. S., Orazalin, N., Uyar, A., and Shahbaz, M. (2021). CSR achievement, reporting, and assurance in the energy sector: Does economic development matter? Energy Policy 149, 112007. doi:10.1016/j.enpol.2020.112007

Khan, H. (2010). The effect of corporate governance elements on corporate social responsibility (CSR) reporting. Int. J. Law Manag. 52 (2), 82–109. doi:10.1108/17542431011029406

Khojastehpour, M., and Jamali, D. (2021). Institutional complexity of host country and corporate social responsibility: Developing vs developed countries. Soc. Responsib. J. 17 (5), 593–612. doi:10.1108/SRJ-04-2019-0138

Kim, S.-Y., and Park, H. (2011). Corporate social responsibility as an organizational attractiveness for prospective public relations practitioners. J. Bus. Ethics 103 (4), 639–653. doi:10.1007/s10551-011-0886-x

Kim, S. (2019). The process model of corporate social responsibility (CSR) communication: CSR communication and its relationship with consumers’ CSR knowledge, trust, and corporate reputation perception. J. Bus. Ethics 154 (4), 1143–1159. doi:10.1007/s10551-017-3433-6

Kpmg, I. M. P. A. C. T. (2020). The time has come the KPMG survey of sustainability reporting 2020. available at: https://assets.kpmg/content/dam/kpmg/uk/pdf/2020/12/the-time-has-come-kpmg-survey-of-sustainability-reporting-2020.pdf.

Księżak, , and Fischbach, B. (2018), “Triple bottom line: The pillars of CSR”, J. Corp. Responsib. Leadersh., 4 3, 95, doi:10.12775/jcrl.2017.018

Kunze, F., Boehm, S. A., and Bruch, H. (2011). Age diversity, age discrimination climate and performance consequences-a cross organizational study. J. Organ. Behav. 32 (2), 264–290. doi:10.1002/job.698

Kvasničková Stanislavská, L., Pilař, L., Margarisová, K., and Kvasnička, R. (2020). Corporate social responsibility and social media: Comparison between developing and developed countries. Sustainability 12 (13), 5255. doi:10.3390/su12135255

Latip, M., Sharkawi, I., Mohamed, Z., and Kasron, N. (2022). The impact of external stakeholders’ pressures on the intention to adopt environmental management practices and the moderating effects of firm size. J. Small Bus. Strategy 32, 3. doi:10.53703/001c.35342

Lin, W.-J., Chen, S.-H., Hsu, Y.-H., and Yang, C.-C. (2018). A review of human rights protection in Taiwan’s health and welfare policies based on International Covenants. J. Formos. Med. Assoc. 117 (5), 356–357. doi:10.1016/j.jfma.2018.02.011

Lis, B. (2012). The relevance of corporate social responsibility for a sustainable human resource management: An analysis of organizational attractiveness as a determinant in employees’ selection of a (potential) employer. Manag. Rev. Socio-Economic Stud. 23 (3), 279–295. doi:10.5771/0935-9915-2012-3-279

Lock, I., and Seele, P. (2016). The credibility of CSR (corporate social responsibility) reports in Europe. Evidence from a quantitative content analysis in 11 countries. J. Clean. Prod. 122, 186–200. doi:10.1016/j.jclepro.2016.02.060

Lozano, R., Nummert, B., and Ceulemans, K. (2016). Elucidating the relationship between sustainability reporting and organisational change management for sustainability. J. Clean. Prod. 125, 168–188. doi:10.1016/j.jclepro.2016.03.021

Magar, V., Heidari, S., Zamora, G., Coates, A., Simelela, P. N., and Swaminathan, S. (2019). Gender mainstreaming within WHO: Not without equity and human rights. Lancet 393, 1678–1679. doi:10.1016/S0140-6736(19)30763-9

Makka, A., and Nieuwenhuizen, C. (2018). Multinational enterprises perceptions of the national corporate social responsibility priority issues in South Africa. Soc. Responsib. J. 14 (4), 828–842. doi:10.1108/SRJ-10-2017-0194

Margolis, J. D., Elfenbein, H. A., and Walsh, J. (2009). Does it pay to Be Good.And does it matter? A meta-analysis of the relationship between corporate social and financial performance. Available at https://ssrn.com/abstract=1866371 March 1, 2009).

Marquis, C., and Qian, C. (2014). Corporate social responsibility reporting in China: Symbol or substance? Organ. Sci. 25 (1), 127–148. doi:10.1287/orsc.2013.0837

Massa, L., Farneti, F., and Scappini, B. (2015). Developing a sustainability report in a small to medium enterprise: Process and consequences. Meditari Account. Res. 23 (1), 62–91. doi:10.1108/MEDAR-02-2014-0030

Massoud, J. A., Daily, B. F., and Willi, A. (2019). How do Argentine SMEs define CSR? Cases in educational social development. World J. Entrepreneursh. Manag. Sustain. Dev. 15 (2), 139–148. doi:10.1108/WJEMSD-10-2018-0090

Matten, D., and Moon, J. (2008). Implicit’ and ‘explicit’ CSR: A conceptual framework for a comparative understanding of corporate social responsibility. Acad. Manag. Rev. 33 (2), 404–424. doi:10.5465/amr.2008.31193458

Michelon, G., Pilonato, S., and Ricceri, F. (2015). CSR reporting practices and the quality of disclosure: An empirical analysis. Crit. Perspect. Account. 33, 59–78. doi:10.1016/j.cpa.2014.10.003

Mimno, D., Wallach, H. W., Edmund, T., Leenders, M., and McCallum, A. (2011). Optimizing semantic coherence in topic models. EMNLP 11, 262–272. doi:10.5555/2145432.2145462

Miska, C., Szőcs, I., and Schiffinger, M. (2018). Culture’s effects on corporate sustainability practices: A multi-domain and multi-level view. J. World Bus. 53 (2), 263–279. doi:10.1016/j.jwb.2017.12.001,

Montiel, I., and Delgado-Ceballos, J. (2014). Defining and measuring corporate sustainability. Organ. Environ. 27 (2), 113–139. doi:10.1177/1086026614526413

Moravcikova, K., Stefanikova, Ľ., and Rypakova, M. (2015). CSR reporting as an important tool of CSR communication. Procedia Econ. Finance 26 (15), 332–338. doi:10.1016/S2212-5671(15)00861-8

Mothe, C., and Nguyen-Thi, T. U. (2021). Does age diversity boost technological innovation? Exploring the moderating role of HR practices. Eur. Manag. J. 39 (6), 829–843. doi:10.1016/j.emj.2021.01.013

Mućko, P. (2021). Sentiment analysis of CSR disclosures in annual reports of EU companies. Procedia Comput. Sci. 192, 3351–3359. doi:10.1016/j.procs.2021.09.108

Ngai, C. S. B., and Singh, R. G. (2021). Operationalizing genuineness in CSR communication for public engagement on social media. Public Relat. Rev. 47 (5), 102122. doi:10.1016/j.pubrev.2021.102122

Nidumolu, R., Prahalad, C. K., and Rangaswami, M. R. (2015). Why sustainability is now the key driver of innovation. IEEE Eng. Manag. Rev. 43 (2), 85–91. doi:10.1109/EMR.2015.7123233

Nielsen, L. (2013). How to classify countries based on their level of development. Indic. Res. 114, 1087–1107. doi:10.1007/s11205-012-0191-9

Obara, L. J., and Peattie, K. (2018). Bridging the great divide? Making sense of the human rights-CSR relationship in UK multinational companies. J. World Bus. 53 (6), 781–793. doi:10.1016/j.jwb.2017.10.002

Ocr, T. (2021). Tesseract open source OCR engine. available at: https://github.com/tesseract-ocr/tesseract (Accessed March 30, 2021).

Osagie, E. R., Wesselink, R., Blok, V., Lans, T., and Mulder, M. (2016). Individual competencies for corporate social responsibility: A literature and practice perspective. J. Bus. Ethics 135 (2), 233–252. doi:10.1007/s10551-014-2469-0

Patara, S., and Dhalla, R. (2022). Sustainability reporting tools: Examining the merits of sustainability rankings. J. Clean. Prod. 366, 132960. doi:10.1016/j.jclepro.2022.132960

Pazienza, M., de Jong, M., and Schoenmaker, D. (2022). Clarifying the concept of corporate sustainability and providing convergence for its definition. Sustainability 17, 7838. doi:10.3390/su14137838

Perego, , and Kolk, A. (2012), “Multinationals’ accountability on sustainability: The evolution of third-party assurance of sustainability reports”, J. Bus. Ethics, 110 2, 173–190. doi:10.1007/s10551-012-1420-5

Pflugrath, G., Roebuck, , and Simnett, R. (2011), “Impact of assurance and assurer’s professional affiliation on financial analysts’ assessment of credibility of corporate social responsibility information”, AUDITING A J. Pract. Theory, 30 3, 239–254. doi:10.2308/ajpt-10047

Pilař, L., Kvasničková Stanislavská, L., Pitrová, J., Krejčí, I., Tichá, I., and Chalupová, M. (2019). Twitter analysis of global communication in the field of sustainability. Sustainability 11 (24), 6958. doi:10.3390/su11246958

Plumlee, M., Brown, D., Hayes, R. M., and Marshall, R. S. (2015). Voluntary environmental disclosure quality and firm value: Further evidence. J. Account. Public Policy 34 (4), 336–361. doi:10.1016/j.jaccpubpol.2015.04.004

Prothero, A., and Tadajewski, M. (2021). ##MeToo and beyond: Inequality and injustice in marketing practice and academia. J. Mark. Manag. 37 (1–2), 1–20. doi:10.1080/0267257X.2021.1889140

Purvis, B., Mao, Y., and Robinson, D. (2019). Three pillars of sustainability: In search of conceptual origins. Sustain. Sci. 14 (3), 681–695. doi:10.1007/s11625-018-0627-5

Ramadhini, A., Adhariani, D., and Djakman, C. D. (2020). The effects of external stakeholder pressure on CSR disclosure: Evidence from Indonesia. Djakman 29 (2), 29–39.

Ramasastry, A. (2015). Corporate social responsibility versus business and human rights: Bridging the gap between responsibility and accountability. J. Hum. Rights 14 (2), 237–259. doi:10.1080/14754835.2015.1037953

Ramdhony, D., Padachi, K., and Giroffle, L. (2010). Environmental reporting in Mauritian listed companies. South Korea: International Research Symposium in Service Management, 24–27.

Randles, G. (2013). Do CSR reports really tell us anything about businesses’ social impact? available at: https://www.theguardian.com/voluntary-sector-network/2013/oct/04/corporate-social-responsibility-reports-impact (Accessed Oct 04, 2013).

Roberts, M. E., Stewart, B. M., and Airoldi, E. M. (2016). A model of text for experimentation in the social Sciences. J. Am. Stat. Assoc. 111 (515), 988–1003. doi:10.1080/01621459.2016.1141684

Roberts, M. E., Stewart, B. M., and Tingley, D. (2019). Stm: An R package for structural topic models. J. Stat. Softw. 91 (2). doi:10.18637/jss.v091.i02

Saeed, A., and Zamir, F. (2021). How does CSR disclosure affect dividend payments in emerging markets? Emerg. Mark. Rev. 46, 100747. doi:10.1016/j.ememar.2020.100747

Sánchez-Teba, E. M., Benítez-Márquez, M. D., Bermúdez-González, G., Luna-Pereira, M., and del, M. (2021). Mapping the knowledge of CSR and sustainability. Sustainability 13 (18), 10106. doi:10.3390/su131810106

Sardana, D., Gupta, N., Kumar, V., and Terziovski, M. (2020). CSR ‘sustainability’ practices and firm performance in an emerging economy. J. Clean. Prod. 258, 120766. doi:10.1016/j.jclepro.2020.120766

Schaltegger, S., Hansen, E. G., and Lüdeke-Freund, F. (2016). Business models for sustainability. Organ. Environ. 29 (1), 3–10. doi:10.1177/1086026615599806

Schulz, M. (2017). An analysis of corporate responses to the black lives matter movement. Elon J. Undergrad. Res. Commun. 8 (1), 55–65.

Sharma, E. (2019). A review of corporate social responsibility in developed and developing nations. Bangkok: Corporate Social Responsibility and Environmental Management, 1739. csr. doi:10.1002/csr.1739

Siwar, C., and Harizan, S. H. M. (2009). A study on corporate social responsibility practices amongst business organisations in Malaysia”. Universiti Kebangsaan Malaysia: Institute for Environment and Development.

Stutz, A., Schell, S., and Hack, A. (2022). In family firms we trust – experimental evidence on the credibility of sustainability reporting: A replication study with extension. J. Fam. Bus. Strategy 13, 100498. doi:10.1016/j.jfbs.2022.100498

Swarnapali, R. M. N. C. (2017). Corporate sustainability: A literature review. J. Account. Res. Educ. (JARE) 1 (1), 1–17.

Talavera, O., Yin, S., and Zhang, M. (2021). Tournament incentives, age diversity and firm performance. J. Empir. Finance 61, 139–162. doi:10.1016/j.jempfin.2021.01.003

Ting, P.-H. (2021). Do large firms just talk corporate social responsibility? - the evidence from CSR report disclosure. Finance Res. Lett. 38, 101476. doi:10.1016/j.frl.2020.101476

Tkalac Verčič, A., and Sinčić Ćorić, D. (2018). The relationship between reputation, employer branding and corporate social responsibility. Public Relat. Rev. 44 (4), 444–452. doi:10.1016/j.pubrev.2018.06.005

Topal, R. S., Ongen, A., and Filho, W. L. (2009). An analysis of corporate social responsibility and its usefulness in catalysing ecosystem sustainability. Int. J. Environ. Sustain. Dev. 8 (2), 173. doi:10.1504/IJESD.2009.023993

Tschopp, D. J. (2005). Corporate social responsibility: A comparison between the United States and the European union. Corp. Soc. Responsib. Environ. Manag. 12 (1), 55–59. doi:10.1002/csr.69

UN – United Nation (2012). United Nations conference on sustainable development, Rio+20. available at: https://sustainabledevelopment.un.org/rio20.

United Nation (2015). Transforming our world: The 2030 agenda for sustainable development. available at: https://sdgs.un.org/2030agenda.

Verbeeten, F. H. M., Gamerschlag, R., and Möller, K. (2016). Are CSR disclosures relevant for investors? Empirical evidence from Germany. Manag. Decis. 54 (6), 1359–1382. doi:10.1108/MD-08-2015-0345

Vilar, V. H., and Simão, J. (2015). CSR disclosure on the web: Major themes in the banking sector. Int. J. Soc. Econ. 42 (3), 296–318. doi:10.1108/IJSE-10-2013-0240

Visser, W. (2009). Corporate social responsibility in developing countries. Oxford, United Kingdom: Oxford University Press.

Welford, R. (2005). Corporate social responsibility in europe, north America and asia. J. Corp. Citizsh. 17, 33–52. doi:10.9774/gleaf.4700.2005.sp.00007

Wensen, K. v., Broer, W., Klein, J., and Knopf, J. (2011). The state of play in sustainability reporting in the EU. available at: https://www.somo.nl/wp-content/uploads/2011/04/The-State-of-Play-in-Sustainability-Reporting-in-the-European-Union.pdf.

Wheeler, S. (2015). Global production, CSR and human rights: The courts of public opinion and the social licence to operate. Int. J. Hum. Rights 19 (6), 757–778. doi:10.1080/13642987.2015.1016712

Widiarto Sutantoputra, A. (2009). Social disclosure rating system for assessing firms’ CSR reports. Corp. Commun. Int. J. 14 (1), 34–48.

Wieser, H. G., and Silfvenius, H. (2000), “Overview: Epilepsy surgery in developing countries”, Epilepsia, 41, S3–S9. doi:10.1111/j.1528-1157.2000.tb01538.x

Wolniak, R., and Hąbek, O. (2016). Quality assessment of CSR reports – factor analysis. Procedia - Soc. Behav. Sci. 220, 541–547. doi:10.1108/13563280910931063

Ying, M., Shan, H., and Tikuye, G. A. (2021). How do stakeholder pressures affect corporate social responsibility adoption? Evidence from Chinese manufacturing enterprises in Ethiopia. Sustainability 14 (1), 443. doi:10.3390/su14010443

Ylyash, O., Trofymenko, O., Dzhadan, I., and Tsarova, T. (2021). Ecological and economic effects of industrial and technological development. IOP Conf. Ser. Earth Environ. Sci. 915, 012004. doi:10.1088/1755-1315/915/1/012004

Yu, W., and Zheng, Y. (2020). Does CSR reporting matter to foreign institutional investors in China? J. Int. Account. Auditing Tax. 40, 100322. doi:10.1016/j.intaccaudtax.2020.100322

Keywords: developed countries, structural topic modeling, sustainability report, developing counties, human rights, sustainable production

Citation: Kvasničková Stanislavská L, Pilař L, Fridrich M, Kvasnička R, Pilařová L, Afsar B and Gorton M (2023) Sustainability reports: Differences between developing and developed countries. Front. Environ. Sci. 11:1085936. doi: 10.3389/fenvs.2023.1085936

Received: 31 October 2022; Accepted: 20 March 2023;

Published: 29 March 2023.

Edited by:

Wu Yufeng, Beijing University of Technology, ChinaReviewed by:

Augustine Ovie Edegbene, Federal University of Health Sciences Otukpo, NigeriaAyodeji Emmanuel Oke, Federal University of Technology, Nigeria

Copyright © 2023 Kvasničková Stanislavská, Pilař, Fridrich, Kvasnička, Pilařová, Afsar and Gorton. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Ladislav Pilař, cGlsYXJsQHBlZi5jenUuY3o=