Jiahui Xia

Jiahui Xia Zhanchi Wu1*

Zhanchi Wu1*- 1Department of Management, Jinan University, Guangzhou, China

- 2ZRP Printing Group Co.,Ltd, Zhongshan, China

Digital technologies offer opportunities and challenges for corporate environmental management (CEM). In this paper, we provide an overview of the literature on the relationship between digital transformation (DT) and CEM using a systematic review approach in the Antecedents, Decisions, and Outcomes (ADO) format. We review 181 papers published in almost 30 years from 1997 to 2022 and identify studies and areas where DT has impacted on CEM. We find that the literature examining the DT-CEM relationship has surged since 2019 and is concentrated in areas such as green sustainable science technology and environmental sciences. Further, we analyze the economic consequences of DT, the drivers of CEM, and the mechanisms of DT on CEM. Based on the literature analysis, we find that there is still a large gap in the literature studying the mediators and moderators of the DT-CEM relationship. Further, we find that firms with DT have better responsiveness and improved CEM by using digital resources to accurately capture the demands of different stakeholders on the environment. Finally, we provide a research framework and possible research directions, and propose corresponding management insights and policy recommendations.

1 Introduction

With sustainability in the spotlight, corporate environmental management (CEM) is receiving increasing attention from companies and markets (Kearins et al., 2010). At the same time, digital technology changes are deeply penetrating into various industries. In the process of digital transformation (DT), digital technologies are the core elements of DT, such as big data, Internet of Things, artificial intelligence (AI), blockchain and cloud computing. The traditional manufacturing industry not only faces new challenges brought by uncertainty in the digital economy, but also ushers in new opportunities for development. Scholars have found that digital technologies such as AI transforms modern society and contributes to the achievement of the Sustainable Development Goals (SDGs) (Alonso et al., 2021). Thus, DT offers new opportunities and approaches for CEM.

Although studies have explored the relationship between DT and corporate environmental behavior, they have focused on corporate social responsibility (CSR) and environmental, social, and governance (ESG) (e.g., Alkaraan et al., 2022; Costa et al., 2022). For example, Verk et al. (2021) reviewed the CSR communication literature and point out that there is an additional cross-fertilisation process with digital communication. However, their research is limited to the field of communication and lacks exploration of corporate production operations. Moreover, Castro et al. (2021) and Isensee et al. (2020) provided a review of the relationship between sustainability and digitalization, but sustainability differs from CEM and their review is theoretically insufficient.

Notably, it is unclear which aspects of DT affects firms and whether these effects act on their environmental behavior. Most of the existing literature studies discuss DT based on a resource-based view (RBV) and explore corporate environmental behavior based on stakeholder theory (e.g., Betts et al., 2015; Fenech et al., 2019), but studies that directly explore the DT-CEM relationship and the theory behind it remains scarce. Therefore, in order for filling the research gap in the DT-CEM relationship, we attempted to elucidate the mechanisms of their roles using a systematic literature review and to explore the role of DT on CEM through the following three research questions.

RQ1. what are the economic consequences of DT?

RQ2. what are the drivers of CEM?

RQ3. why and how does DT affect CEM?We follow on Paul and Benito (2018) and adopt the Antecedents, Decisions, and Outcomes (ADO) systematic review analysis framework. The ADO framework systematically and comprehensively analyzes the drivers, effects, and related decisions of the research subject, possesses the breadth and depth of literature analysis, and is a widely accepted literature review method by scholars across subject areas (Dabić et al., 2020). We have deformed the ADO method in order to study more effectively the three questions studied in this paper.We select literature from Web of Science (SCIE and SSCI) by searching keywords, and snowball and filter the literature to finally obtain 181 papers. Through the analysis of the literature, we fully explore three research questions and uncover the mechanisms of DT on CEM, as well as provide the gap of the literature and possible future research directions.Specifically, we find that the existing literature fails to comprehensively understand the impact of DT on firms, the drivers of CEM, and the mechanisms by which DT acts on CEM. In addition, we find that there is still a significant gap in the literature examining the mediating and moderating variables in the relationship between DT and CEM. Furthermore, we find that DT firms have better responsiveness and improved CEM by using digital resources to accurately capture the environmental requirements of different stakeholders.Our literature review has the following three main research contributions. First, we review the DT-CEM relationship and further deepen our understanding of the DT-CEM relationship by exploring the economic consequences of DT and the drivers of CEM. The literature is still lacking in terms of clarifying the relationship between DT and CEM. Therefore, comprehensive and systematic research exploring the relationship is urgently needed to identify research gaps as well as to develop an agenda for the future.Second, we develop a model of the DT-CEM relationship that will help future research explore the mediators and moderators of DT-CEM. This is important because DT brings new growth opportunities for companies and CEM is a critical corporate governance matter, so it is urgent to clarify how companies can effectively use digital technologies to enhance the effectiveness of CEM. According to our model, future research can grasp more clearly the research direction of DT-CEM relationship, which greatly improves the research efficiency.Third, we have innovated a systematic literature review methodology for ADO to inform future qualitative and quantitative research. While the traditional ADO framework is more suitable for studying a single object and has certain limitations, our adapted ADO framework is more applicable to exploring multiple study object relationships.The rest of this paper is organized as follows. Section 2 states the theoretical backgrounds of DT and CEM. Section 3 is the literature identification strategy. Section 4 is the content analysis of the literature. Section 5 is the conclusions and discussions.

2 Theoretical backgrounds

2.1 Digital transformation

In line with existing research, we define digital transformation (DT) as a process in which companies use the changes and opportunities brought by digital technologies to accelerate the transformation of their production processes, business activities, and production technologies (Demirkan et al., 2016). DT brings changes to a firm’s business model, which in turn changes the product or organizational structure (Hess et al., 2016). Digital technologies inspire firms to find new strategies for DT by disrupting the value creation paths they already have in place (Vial, 2019). Verhoef et al. (2021) classify DT into three phases: digitization, digitalization, and DT. In the DT stage, firms use digital technologies to accurately grasp customer needs, create value, and realize their business model choices for the firm (Iansiti and Lakhani, 2014; Pagani and Pardo, 2017).

Digital capabilities are seen as the key to gaining new competitive advantages through DT for traditional manufacturing enterprises, as well as the main source of gaining sustained competitiveness (Annarelli et al., 2021). Thus, digital capabilities are the foundation for firms to improve customer experience, transform operational processes, and reorganize business models to effectively drive DT (Westerman et al., 2012). Annarelli et al. (2021) defined digital capabilities as organizational competencies that enable firms to extensively combine digital assets and business resources, leverage digital networks, innovate products, services, and processes to facilitate organizational learning and value creation, and gain sustained competitive advantage through management innovation. The dynamic capabilities that result from an enterprise building, optimizing, expanding, or aligning existing resources help to efficiently process information and facilitate DT (Rialti et al., 2019; Warner and Wäger, 2019).

2.2 Corporate environmental management

The definition of corporate environmental management (CEM) has been in a state of continuous development. Klassen and McLaughlin (1996) defined CEM as the effort to minimize the negative environmental impacts of a company’s products throughout its life cycle. Today, CEM has been given a new dimension with the goal of carbon neutrality and carbon peaking, and carbon footprinting is gradually being taken into account in CEM (Lee and Cheong, 2011; Beier et al., 2022).

However, scholars have found that firms did not support CEM from the start (Munasinghe, 1999). Early on, some managers believed that CEM required additional corporate costs and reduced corporate profits. However, Klassen and McLaughlin (1996), who examined the impact of CEM on stock market performance, found that strong CEM can effectively improve future corporate financial performance. The reason for this is that different approaches to CEM produce different CEM costs and economic performance outcomes, so the quality of CEM is assessed depending on what the firm wants to achieve in terms of market share, profitability, and social benefits (Schaltegger and Synnestvedt, 2002). Later, Kearins et al. (2010) found that entrepreneurs actively create a relationship between business and nature and feel sorry for the natural environment because the business is dominated by economic rationality. In recent years, CEM and financial performance have gradually become effectively integrated. Latan et al. (2018) studied the impact of environmental management accounting on corporate environmental performance and found that internal environmental strategies and executive attitudes as well as external environmental uncertainty of the firm have a significant positive impact on corporate environmental accounting and in turn improves corporate environmental performance.

3 Identification strategy

3.1 Antecedents, decisions and outcomes

To make our review more scientific and rational, we use the Antecedents, Decisions and Outcomes (ADO) framework of systematic literature review. The ADO framework was proposed by Paul and Benito (2018), which helps us identify the highest level of clarity and coverage of the literature (i.e., breadth and depth) and can systematically capture the development of the literature related to the subject of study.

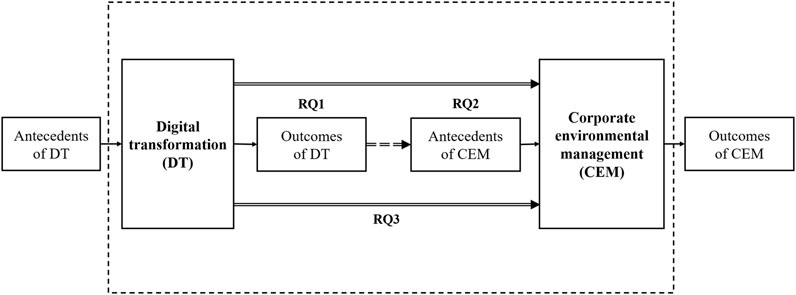

Using the ADO framework, we can identify the antecedents, decisions, and outcomes of DT and CEM. The core question of our literature review is how DT (X) affects CEM (Y). Since the ADO framework is suitable for reviewing literature on a single research subject, we innovatively propose a modified version of the ADO framework.

First, we explore the economic outcomes of DT (X) adoption by companies and categorize and analyze them to observe the relevant literature trends. In other words, in this stage, we take DT as the object of study, which has its own antecedents and outcomes. The consequences of DT appear later in the third step as antecedents that affect the CEM. Second, we analyze the antecedents of CEM (Y) and classify them according to the subject. Third, we analyze the impact and mechanism of DT and its economic outcomes (X) on CEM and its antecedents (Y). That is to say, the result of the first step is used as the antecedents, and the result of the second step is used as the outcomes, and the mechanism of the antecedents to the outcomes is studied.

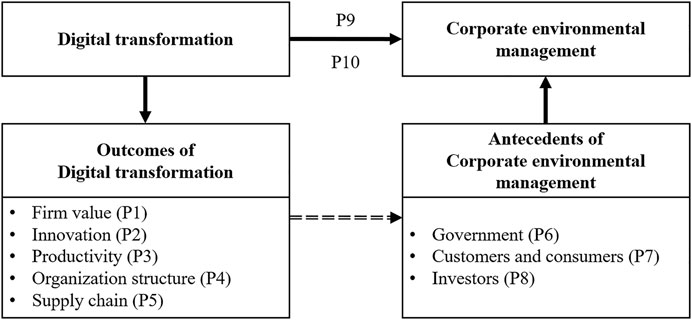

Our variant ADO framework not only satisfies the research method of systematic literature review, but also comprehensively and systematically analyzes two research subjects. At the same time, we dig out the possible connection between the two research subjects, and explore the mechanism and impact between the two as comprehensively as possible. Therefore, it is reasonable for us to innovatively use the deformed version of ADO to analyze DT and CEM. Figure 1 shows the analytical framework of the research questions.

FIGURE 1. Analysis framework of research questions.

3.2 Literature search strategy

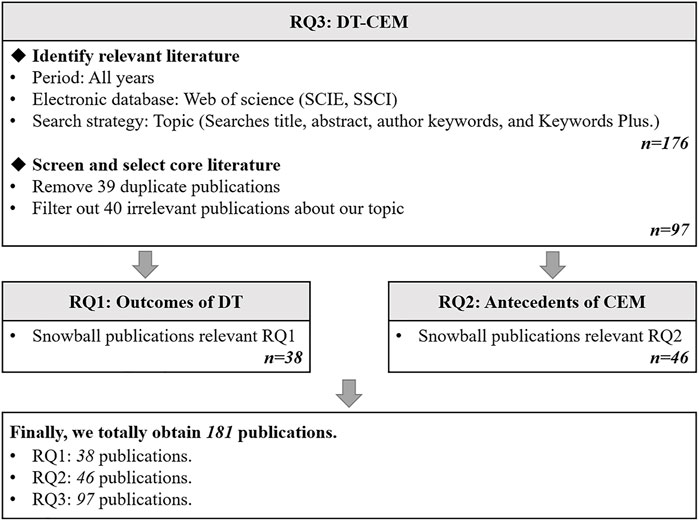

Since we are divided into three research questions to explore the mechanisms of DT on CEM, involving multiple subject knowledge and with CEM as the main key theme, we follow Ameer and Khan (2022) and use a keyword combination approach to collect relevant literature. In addition, to fit the research idea, we take the literature related to RQ3, i.e., DT-CEM, as the base literature and use a snowball to collect its references as well as the literature related to RQ1 and RQ2 in the cited literature.

First, to ensure the quality of the paper, we search the Web of Science (SCIE and SSCI) for relevant literature by keywords. Based on the preliminary literature review, we combined the keywords of DT with the keywords of CEM using Boolean connectives (e.g., “OR” and “AND”). The keywords include but are not limited to “digital”, “digit*”, “artificial intelligence”, “information and communications technology”, “big data”, “cloud computing”, “Internet of Things”, “blockchain” and “corporate environmental management”. In this phase, we obtain 176 papers.

Next, we stepwise screen the obtained documents. First, we remove 39 duplicate documents (n = 137). Second, we read the full text of the papers and filter out 40 articles that are not relevant to our research question (n = 97). So far, we have obtained 97 articles about RQ3. Third, we snowball articles that fit the research topic to collect their references as well as those in the cited literature related to the research question, expanding the literature by 84 articles (n = 181).

Finally, we obtain 181 publications on DT and CEM in different fields, with RQ1 involving 38 publications, RQ2 involving 46 publications, and RQ3 involving 97 publications. Our literature review process is shown in Figure 2.

FIGURE 2. Systematic review process.

4 Results

4.1 Descriptive analysis

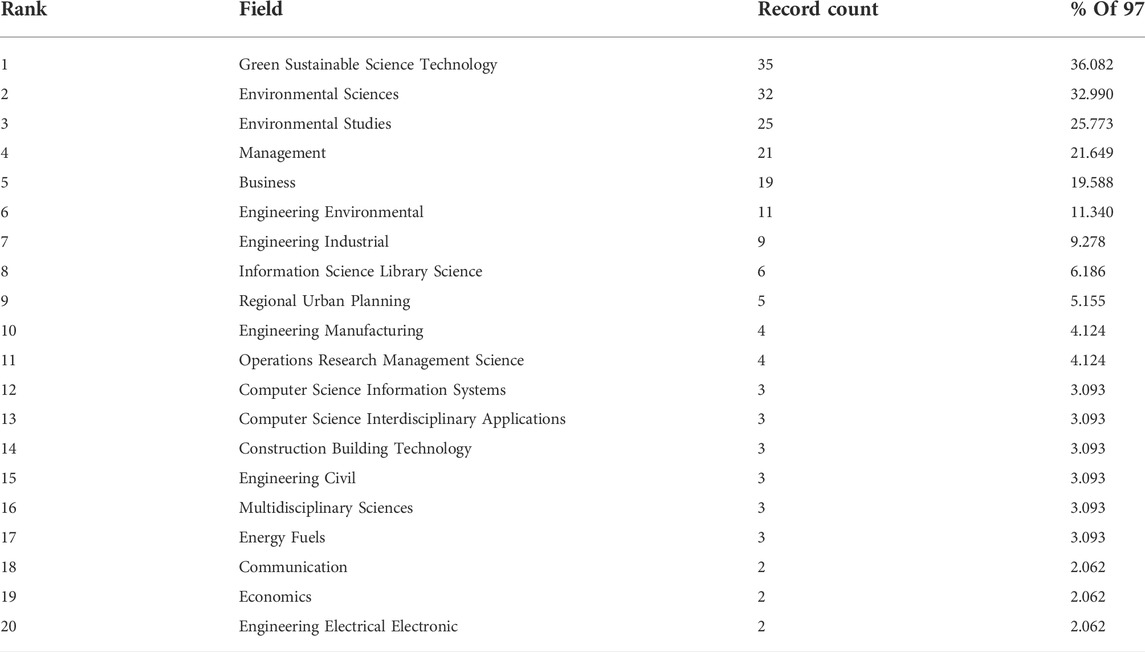

We categorize and list the Web of Science Categories covered by the 97 publications in RQ3 in Table 1. From Table 1, we can see that the most relevant field of DT-CEM related literature is Green Sustainable Science Technology, with 35 publications involved, accounting for 36.082%. Secondly, DT-CEM involves more fields in Environmental Sciences. There are 32 publications, accounting for 32.990%. The third-ranked field is Environmental Studies. After that, Management and Business follow, covering 21 and 19 publications, respectively. Due to the characteristics of DT, the literature of DT-CEM also involves fields such as Computer Science Information Systems and Engineering Electrical Electronic. From this, it can be seen that DT-CEM is an interdisciplinary topic. The researchers explored the DT-CEM relationship in the context of corporate governance, combining knowledge from multiple domains of technology, environment, and management.

TABLE 1. Top20 research fields of DT-CEM.

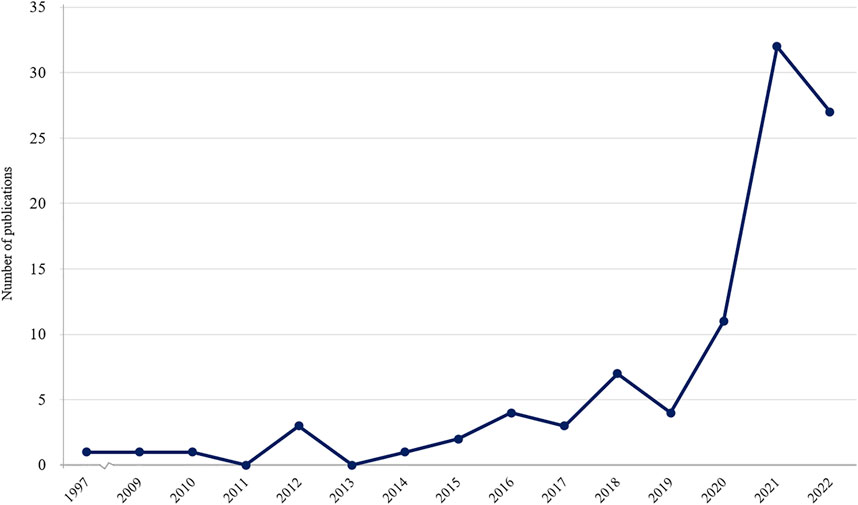

Next, we count the years of DT-CEM publications. Figure 3 shows that the first articles examining the DT-CEM relationship appeared in 1997. However, the literature was sparse for nearly a decade after that. DT-CEM-related publications continued to appear until after 2009. Notably, the publications on DT-CEM increased rapidly from 2016 onwards, especially from 2019 onwards with a sudden rise. Thus, DT-CEM literature has largely evolved with the changes in digital technologies, which have brought new opportunities and challenges not only to companies but also to researchers.

FIGURE 3. DT-CEM publications per year.

4.2 Theory, methods and variables

4.2.1 Theory

Most of the existing literature analyzes DT based on RBV and dynamic capabilities perspective (e.g., Chen et al., 2016; Fenech et al., 2019; He et al., 2020). DT enhances a company’s dynamic capabilities and has an irreplaceable role in adapting to market uncertainty and customer demand for individualized products. From RBV, the strategic role of DT as a continuous fundamental organizational change (Hanelt et al., 2021) is to guide enterprises to add, remove and reconfigure their organizational resource base through the introduction and penetration of digital technologies, and to drive the overall coordination, optimization and implementation of DT in enterprises (Helfat et al., 2009; Matt et al., 2015).

From the perspective of analyzing the antecedents of CEM, most of the existing literature is based on stakeholder theory (e.g., Betts et al., 2015), RBV (e.g., Aragón-Correa and Sharma, 2003), reputation theory (e.g., Martín-de Castro et al., 2020) to conduct research. The RBV was earlier incorporated into the analytical framework of CEM. Verbeke et al. (2006) argued that incorporating RBV into corporate environmental investments, rather than environmental strategies per se, has a significant impact on corporate performance. Later, Sarkis et al. (2010) constructed an analytical framework for CEM based on stakeholder theory and the dynamic capabilities perspective of the RBV. In analyzing the CEM of small and medium-sized enterprises (SMEs), some articles have found the dilemma of lack of resources for SMEs to actively choose CEM. However, Aragón-Correa et al. (2008) combined stakeholder theory and the RBV and found that SMEs attempted a range of environmental strategies from passive regulatory compliance to proactive pollution prevention. Among them, factors such as SMEs’ organizational vision and internal organizational structure are important influences in the implementation of proactive corporate environmental strategies and can lead to good financial performance. According to this logic, stakeholders are the key drivers that motivate CEM, and CEM can bring competitive resource advantages to companies.

4.2.2 Methods and variables

There are two main manifestations of DT in the literature that explores the relationship between DT and CEM. First, the literature explores the impact of DT on CEM behavior using a particular digital technology as an independent variable, such as blockchain (Saberi et al., 2019), AI (Cortès et al., 2000), cloud computing (Sun, 2013). Second, the literature uses digital technology as a moderating variable to explore the role that DT plays in the relationship between other factors and CEM (e.g., Khin and Ho, 2018).

In contrast, there are many metrics for CEM, which can be grouped into two main categories. First, whether the firm manages the environment in its production operations, e.g., controlling the release of pollutants (Kim et al., 2019) and reducing carbon emissions (Yao et al., 2019). Second, whether the firm discloses environmental information (e.g., Wang et al., 2021).

4.3 Content analysis

In this section, we group and analyze the selected literature according to the research questions. Referring to most of the literature, we explore the relationship between DT and CEM using stakeholder theory and RBV. The content analysis of the literature is divided into three parts. First, we analyze the existing literature on the economic consequences of DT based on RBV, and present possible research gaps and proposals. Next, we describe in detail the drivers of CEM based on stakeholder theory and pose possible research gaps and proposals. Finally, we describe the existing literature on the impact of DT on CEM and present the proposals with the RBV and stakeholder theory.

4.3.1 Economic outcomes of DT

RQ1 of this study is to determine the economic outcomes of DT on firms. Since the impact of DT on firms is multifaceted, we categorize and analyze the literature in a comprehensive manner. From RBV, companies undergo DT, which develops digital capabilities, improves their resource endowment, and enhances their competitiveness. In other words, DT triggers corporate change. Based on an initial classification of the literature, we analyze the impact of DT on enterprises in five dimensions: firm value, innovation, productivity, organizational structure, and supply chain.

4.3.1.1 Firm value

Why and how does DT affect enterprise value? The literature has found that firms implement DT that use new technologies to disrupt existing business models and change the way firms create value, thereby improving firm performance (Matt et al., 2015). Vial (2019) shared a similar view, arguing that digital technologies disrupt the previous state of the firm, triggering a strategic response as firms seek to change the path of value creation while dealing with these disruptions create structural changes and organizational barriers. The reason for this is that evolving digital technologies drive change in markets and industries, and business executives transform and innovate in response to the new landscape (Gurbaxani and Dunkle, 2019).

Based on RBV, digital dynamic capabilities become an inevitable choice for firms in the digital economy (Warner and Wäger, 2019). Mikalef and Pateli (2017) found that information technology-supported dynamic capabilities effectively contribute to the market capitalization and operational alignment agility of firms, helping them to develop a competitive advantage in an uncertain environment, thereby improving competitive performance. Subsequently, further research found that non-technology firms adopting digital technology had significantly higher market capitalization and asset turnover, but significantly lower profitability and sales growth (Chen and Srinivasan, 2019). From a dynamic capabilities perspective, Mikalef et al. (2020) analyzed the relationship between big data analytics capabilities and competitive performance and found that big data analytics capabilities are based on dynamic capabilities to have a positive effect on firms’ marketing and technology capabilities.

Considering firm value from a customer perspective, the literature has explored the impact of DT on firm value, finding that firms mastering digital technologies can transform production models, enable new business, and enhance customer experience and loyalty (Verhoef et al., 2021). Matarazzo et al. (2021) found that enterprise perception and learning capabilities are triggers for DT to stimulate enterprise value creation.

As a result, DT facilitates firms to increase resources and enhance capabilities, which in turn increases firm value. The propensity for resource-driven change often has a positive or even beneficial impact on performance (Kraatz and Zajac, 2001). From the above analysis, we can see that firms integrate existing resources and learn technologies through DT, which can prompt them to change their original models, develop dynamic capabilities, and enhance their learning capacity and competitiveness. Therefore, the accumulation of enterprise resources promotes the enhancement of enterprise value. Based on this, we propose the following proposal:

Proposal 1: Digital transformation is positively correlated with firm value.

4.3.1.2 Innovation

From the literature in the above section, we know that DT drives firms to change their production models and that firms thus innovate actively or passively. Some digital technologies can help firms to develop new technologies. For example, AI facilitates firms to develop new technologies and use big data effectively (Cockburn et al., 2019). In addition, AI affordances support digital innovation in firms (Trocin et al., 2021). Furthermore, a firm’s own digital orientation and capabilities have a significant positive impact on its digital innovation, and digital innovation positively moderates the impact of a firm’s digital capabilities on financial and non-financial performance (Khin and Ho, 2018). However, some scholars are skeptical. Usai et al. (2021) argued that a generalized consideration of digital technologies hinders the accurate assessment of innovation performance. Using R&D expenditure as a measure of innovation performance, they found that digital technologies have very little impact on firms’ innovation performance, and they argued that overuse of digital technologies is likely to deplete firms’ long-term innovation capacity.

Overall, although scholars disagree on the impact of DT on firms’ innovation performance, most of them believe that DT drives firms’ innovative behavior. Based on RBV, on the one hand, the leverage of digital resources activates the traditional resources of enterprises, expands the range of resources at their disposal, and realizes the effective combination of digital resources and traditional resources. On the other hand, the digital capabilities of enterprises strengthen the resilience of traditional resources, and when facing uncertainty, enterprises exert digital capabilities to realize the restructuring of traditional resources. Therefore, we propose the following proposal:

Proposal 2: Digital transformation is positively correlated with corporate innovation.

4.3.1.3 Productivity

DT has stimulated companies to innovate R&D and use new technologies, reshaping production models and significantly increasing productivity (Brynjolfsson and Saunders, 2009). Pilloni (2018) argued that data and information are crucial in the era of Industry 4.0, and that crowd-sensing and crowdsourcing that come as a result of data and information will bring new advantages and challenges. In response, scholars have found that companies investing in employees learning digital technologies significantly increase productivity (Tambe, 2014). In fact, from RBV, digital technologies can identify, analyze, and reorganize existing resources and knowledge to solve new problems and achieve accelerated innovation, and the analytical capabilities of non-inventor employees in firms are key players in helping firms create new knowledge in decentralized structures (Wu et al., 2019). In addition, digital technologies may pose new challenges for firms influenced by their resource endowments. For example, Babina et al. (2020) found that firms that invest in AI have higher valuations due to the role of AI in promoting product innovation in firms’ trademarks, patents, and portfolios, which is concentrated on the head firms in the industry, creating a winner-take-all situation. Firms develop their resource base to transform their competitiveness (Uhlenbruck et al., 2003). Therefore, DT drives companies and employees to improve their learning capabilities, increase their resources and improve the efficiency of their use of resources. Based on this, we propose the following proposal:

Proposal 3: Digital transformation is positively correlated with productivity.

4.3.1.4 Organizational structure

The literature has identified a new situation for corporate organizations in the digital economy (Fitzgerald et al., 2014). Developments in information technology (IT) have profound implications for organizational design (Garicano, 2000). Digital technology, as a new resource endowment, disrupts the inherent organizational forms of business. In the study of the relationship between the diffusion of new technologies and corporate decentralization, Acemoglu et al. (2007) found that firms with more advanced technologies, firms in an environment of greater uncertainty, and younger firms were more likely to choose decentralization. IT can help managers plan production and increase their autonomy and span of control (Bloom et al., 2014). Further, Bonanomi et al. (2019) used network theory to explore the impact of digital technology on a firm’s organizational structure and found that people seeking advice and information about digital technology construct an informal social network that acts on the organization. In addition, Kretschmer and Khashabi (2020) found that digital technology affects different levels and dimensions of a firm’s product creation process, thus stimulating changes in operations and processes within the organization. Since the dynamic resources of the enterprise influence the establishment, development and maturity of organizational capabilities (Helfat and Peteraf, 2003), the changes in digital technology brought about by DT have triggered a series of changes in the enterprise organization. Based on the above analysis, we propose the following proposal:

Proposal 4: Digital transformation is positively correlated with organizational change.

4.3.1.5 Supply chain

Digital technologies have enabled disruptive changes in the supply chain (e.g., Koh et al., 2019; Jabbour et al., 2020; Lezoche et al., 2020). More prominently, blockchain technology brings new resource endowments to businesses. With the globalization of supply chains, it has become more difficult to manage and control supply chain operations, and blockchain technology has made this less of a problem. Saberi et al. (2019) found that blockchain with high transparency, traceability, and security combined with smart contracts can help companies remove possible barriers to sustainable supply chain development. Sheel and Nath (2019) surveyed 397 supply chain practitioners in India and found that blockchain technology can effectively improve consistency, agility, and adaptability in supply chain segments, achieving enhanced co-competitiveness of firms in the supply chain and increasing business performance. Moreover, the use of digital technologies by firms can facilitate collaborative supply chain optimization and identify and achieve lean production (Camuffo and Gerli, 2018). Furthermore, Ivanov et al. (2019) found that digital technologies can mitigate the risk of supply chain disruptions as well as enhance supply chain management for ripple effect control. It is thus clear that the dynamic capabilities empowered by digital technology offer new possibilities for the development of the supply chain. Therefore, we propose the following proposal:

Proposal 5: Digital transformation is positively correlated with supply chain transformation.

4.3.2 Drivers of CEM

From a basic review of the literature, we can see that the demands of corporate stakeholders on the corporate environment are the main pressure for CEM. Although there is also literature that discusses the drivers of CEM in terms of external and internal to the firm, or active or passive to the firm, stakeholders clearly understand the relevance of the firm to environmental quality and play a decisive role in CEM. Therefore, based on stakeholder theory, the section analyzes the relevant literature on the drivers of CEM from the perspective of three major corporate stakeholders: government, customers, and investors.

4.3.2.1 Government

Government is one of the important stakeholders of business stakeholders. The existing literature suggests that government regulation is the most important driver of CEM, being the initial source of pressure and persisting in its role (Andrews, 1998; Zhang et al., 2008). In some heavily polluting industries, government policies and regulations set increasingly stringent requirements for corporate performance patterns, prompting CEM (Sanchez, 1998). In addition, there is also literature that corroborates the role of government from the perspective of the lack of government regulation. Alemagi (2007) found that the oil industry caused serious pollution mainly due to inadequate regulations and lack of governmental role.

However, influenced by differences in economic development, it is necessary for the literature to consider institutional contexts when exploring the role of government. Valentine (2012) developed a CEM lifecycle and found that the Singapore government developed CEM support programs to meet the potential needs of firms in the first three stages of CEM. Rowe and Guthrie (2010) examined executives’ attitudes toward CEM and CEM’s reporting in Chinese firms and found that government regulation has the most influential and unpredictable role on CEM. In addition, Yee et al. (2013) compared the main arguments of ecological modernization theory based on the experience of developed countries with the environmental practices of Chinese firms through interviews with Chinese Hong Kong business executives. They found that the pattern of interaction between stakeholders and firms, such as the Chinese government, differs from the Western European experience, with the informal relationship between the Chinese government and firms characterized more prominently. By examining CEM in the Pearl River Delta region of China, Liu et al. (2018) argued that policy ambiguity is negatively associated with CEM, and that intensive inspections mitigate the negative association between the two.

In terms of regulatory approach, Raff and Earnhart (2018) found that government enforcement, such as federal inspections and monetary penalties, has a stronger effect on CEM. Rowe and Guthrie (2010) also found ‘coercive government institutional involvement’ to be a strong factor for CEM in their survey of Chinese firms. Ding and Shahzad (2022) found that environmental administrative penalties effectively supervise CEM, mediated by the fact that fines significantly reduce firms’ cash flows in the following year.

It can be seen that there is a consensus in the literature that government plays a non-negligible role in the CEM. Usually, companies must be consistent with their institutional environment in order to gain legitimacy and resources. Facing with governmental demands for corporate environmental responsibility, companies actively manage their environment to respond to governmental demands to avoid environmental penalties and maintain their corporate image. Therefore, we propose the following proposal.

Proposal 6: Government environmental regulation is positively related to corporate environmental management.

4.3.2.2 Customers

Corporate environmental responsibility is no longer only a moral constraint of the enterprise’s own economic behavior, but also a social responsibility to the whole value chain system. Customer is one of the important stakeholders of an enterprise, and customer relationship is a contractual relationship between an enterprise and its customers based on purchase and sale transactions, which has an important influence on the choice of business model of an enterprise. The role of customers in CEM has been well explored by scholars. Zhang et al. (2012) found that as consumers become more environmentally conscious, they encourage firms to pursue proactive CEM practices by purchasing environmentally friendly products. Moreover, high-income consumers are willing to pay a premium for environmentally friendly products (Arora and Gangopadhyay, 1995). Crucially, consumers’ perception of CSR somewhat triggers corporate managers to engage in CEM (Gonzalez-Rodriguez et al., 2015). At the same time, consumers who are aware of a company’s fulfillment of social responsibility are more likely to purchase that company’s products because of its implementation of social responsibility (Boccia and Sarnacchiaro, 2018).

In addition, customer demands for environmental protection are to some extent the driving factor for the very popular “green” supply chain management (Hoejmose et al., 2012). In the study of firms in transition economies, Earnhart et al. (2014) and Earnhart (2017) found that foreign ownership and foreign customers put environmental pressure on firms to manage their environment. Earlier, Christmann and Taylor (2001), in their study of Chinese firms, found that foreign-owned customers exert environmental self-regulatory pressure on firms through the supply chain, prompting Chinese suppliers to adopt the ISO 14001 environmental system standard.

It is noteworthy that the maintenance of customer loyalty is one of the motives of CEM. Moreover, CSR has an important impact on building corporate and product image and influencing customer satisfaction and loyalty (Choi and La, 2013; Martínez and Rodríguez del Bosque, 2013; Latif et al., 2020; Liu et al., 2020). In addition, the fulfillment of environmental responsibility by companies positively affects the identification of customers with the company, the emotions evoked by the company and satisfaction, the identification also affects the emotions generated by service performance, and customer satisfaction determines loyalty behavior (Pérez and Rodríguez del Bosque, 2015). Hence, CEM and the establishment of a socially responsible image are highly attractive to customers and help form customer stickiness, remedy corporate failure services and consolidate customer loyalty. Further, companies actively or passively engage in CEM and develop appropriate environmental management strategies in order to meet customers’ needs for corporate environmental responsibility. Therefore, we propose the following proposal:

Proposal 7: Customers’ environmental protection requirements are positively correlated with corporate environmental management.

4.3.2.3 Investors

Investors value CEM, mainly because it is an important indication of the level of corporate governance (Wahba, 2008). Much of the literature finds that institutional ownership is one of the ways in which investors exert pressure on firms. Kim et al. (2019) found that institutional ownership is significantly negatively associated with corporate toxic emissions and significantly positively associated with the likelihood of corporate environmental, social, and governance proposals. In addition, environmental information quality disclosure is an important measure of CEM. Wang et al. (2021) found that institutional investors significantly positively moderate the effect of air pollution on corporate environmental information disclosure by studying China’s New Environmental Protection Law, which plays a monitoring role. There are exceptions, however. For example, Mura et al. (2019) found that most Italian organizations, except those with environmental and social certification, rarely disclose their environmental information and CEM to stakeholders.

Institutional investors increasingly prefer socially responsible companies (Dyck et al., 2019; Chen et al., 2020). On the one hand, influenced by their own moral ethics, investors want their investments to contribute to the achievement of social goals and are willing to assign their own values to them (Lewis and Mackenzie, 2000). On the other hand, because companies that implement sustainable development and social responsibility are able to deal with social and environmental issues properly, which in turn improves their reputation and increases their competitive advantage, making investors gain more wealth (Petersen and Vredenburg, 2009). In contrast, the exposure of environmental issues may damage the value of investors (Chan and Welford, 2005). In addition, some researchers have pointed out that institutional investors can improve corporate social performance (Cox et al., 2004). This is mainly due to the fact that institutional investors with higher shareholdings promote CSR by influencing board social responsibility issues (Pucheta-Martínez and Chiva-Ortells, 2018), which not only increases corporate involvement in social responsibility, but also improves CSR performance.

Institutional investors are key stakeholders in corporate finance, and the capital market’s “voting with their feet” approach to decision-making directly or indirectly affects corporate governance (Kejing, 2018). Institutional investors are financially strong and have a greater influence on corporate finance. Moreover, there is a herding effect among investors, with other investors following institutional investors in their decisions (Scharfstein and Stein, 1990; Xiaqing et al., 2019). It is noteworthy that institutional investors tend to select firms with a better level of corporate governance as well as threaten to sell firms with poor corporate governance to promote corporate governance (Aggarwal et al., 2011). In response, the active implementation of CEM and CSR by firms can reflect the current status of their production operations and financial performance. For example, Dhar et al. (2022) found that the implementation of green accounting in heavily polluting firms in Bangladesh significantly improved the level of corporate sustainability. Therefore, management takes the initiative in CEM and discloses CSR information in order to cater to the preferences of institutional investors and to reduce information asymmetry in order to meet corporate financing needs (Brammer et al., 2012). Based on the above analysis, we propose the following proposal:

Proposal 8: Investors’ environmental preferences are positively related to corporate environmental management.

4.3.3 DT and CEM

The literature directly examining the impact of DT on CEM is still relatively scarce and mostly discussed in terms of its impact on CSR and sustainability. For example, Seele (2017) discussed the potential of transferring big data algorithms for “predictive” purposes to the field of corporate sustainability. The changes brought about by the DT of companies correspond to the information efficiency required for CSR (Zyglidopoulos et al., 2012). At the theoretical level, the rapid development of digital technology has increased the resource endowment of companies, which in turn has changed the way companies communicate with their stakeholders. Troise and Camilleri (2021) explored the use of digital communication channels by companies and found that companies use social media for product marketing and promotion, CSR practices, and stakeholder interaction with financial stakeholders. In the digital age, barriers to business-society communication are greatly reduced, so businesses can quickly and accurately capture consumers’ demands for corporate environmental responsibility (Kıymalıoğlu, 2022), while DT drives the ability of companies to fulfil their environmental responsibility (Orbik and Zozuľaková, 2019). Verina and Titko (2019) proposed that companies undergo “organizational change” and “cultural transformation” and find “ways to move towards customer centricity” in the context of DT. Moreover, DT is a strong partial mediator between CSR attributes and CSR authenticity (Liu and Jung, 2021). In addition, Camodeca and Almici (2021) found that digital technologies significantly improve ESG and help companies to achieve Sustainability Development Goals. In terms of supply chain, the use of big data analytics by firms can positively moderate the relationship between sustainable supply chain management and organizational performance (Zhu et al., 2022).

Based on the above literature, we can see that DT improves the responsiveness of a firm’s resource endowment to stakeholder requirements. Therefore, combining the RBV and stakeholder theory, we propose the following proposal:

Proposal 9: Digital transformation is positively associated with the implementation of CEM.

In some industries, the use of digital technology can effectively capture the environmental impact of a company’s production. For example, in the construction sector, the use of digital technology can accurately predict the carbon emissions of commercial buildings in China (Xiang et al., 2022a; Xiang et al., 2022b), providing valuable business insights (Chen et al., 2022; Li et al., 2022), and drive companies to achieve their carbon peak and carbon neutrality targets (Sun et al., 2022). In the energy industry, the digital economy has been effective in mitigating the impact of a coal-based energy mix on carbon emissions (Li et al., 2021). At the same time, however, a few studies have found that the digital economy has a negative impact on carbon emissions. For example, Ma et al. (2022) found that the digital economy and exports have a negative impact on consumption-based carbon emissions using provincial panel data for China.

In addition, on CEM disclosure, Cerchiaro et al. (2021) found that Distributed Ledger Technologies can simplify the processing and packaging of ESG reports by creating agile, transparent, and automated data collection processes. In further, Hughes et al. (2021) found that technological innovations in ESG ratings based on data scraping and AI are increasingly influential, as evidenced by digital technology-based ESG ratings with higher levels of standardization, more transparent rating perspectives, more democratic aggregation processes, and more rigorous real-time analysis. Moreover, the information transparency brought by blockchain technology largely contributes to corporate sustainability (Ronaghi and Mosakhani, 2022).

It follows that the use of digital technologies by companies can advance the capture of results and more accurate ratings of CEM. In turn, stakeholders can have a more accurate and direct understanding of the effectiveness of CEM. Based on this, we propose the following proposal:

Proposal 10: Digital transformation is positively correlated with capturing the results of corporate environmental management.

5 Conclusions and discussions

5.1 Conclusions

As DT and CEM research continues to evolve, we review the literature on DT-CEM. We adopt a systematic review approach using the Antecedents, Decisions and Outcomes (ADO) format and adapt the ADO framework to our research questions. Specifically, we explore the economic consequences of DT, the drivers of CEM, and the relationship between DT and CEM. A review of the literature leads us to the following four main conclusions.

First, the existing literature fails to comprehensively understand the impact of DT on firms. Through reviewing the literature, we find that most of the existing studies are based on the RBV and dynamic capability perspective to explore the impact of DT on enterprise resources and capability enhancement, and the focus of the research object is still concentrated on the micro level. In particular, through the content analysis of the literature, we conclude that the economic consequences of DT can be divided into five main areas: firm value, innovation, productivity, organizational structure, and supply chain. In addition, we find that DT drives corporate change, and most of the existing studies focus on the impact of DT on the micro level of enterprises. However, there is still a lack of research exploring the impact of DT bringing about macroeconomic changes on firms.

Second, the existing literature fails to consider the drivers of CEM in a comprehensive and direct manner. Through a review of the literature, we find that the existing literature examining the drivers of CEM is limited to the requirements of corporate responses to stakeholders and lacks a framework for a systematic and comprehensive understanding of the drivers of CEM. Further, the existing literature still pays less attention to the micro-level aspects of CEM. Therefore, we can conclude that studying CEM drivers requires exploring the impact of drivers and the relationship between factors on CEM through multiple research designs.

Third, there is a serious lack of research in the existing literature to understand the mechanisms of the role of DT on CEM. Through a review of the literature, we find that the existing literature mostly refers to environmental factors in the context of the impact of DT on CSR, while studies that directly explore the DT-CEM relationship are still insufficient. In particular, in the study with DT and CEM as the main subjects, most of the literature is limited to exploring the direct DT-CEM relationship, and there is a lack of research on the mechanisms of the mediating and moderating roles from within and outside the firm. In addition, it is essential to explore the quantitative analysis of the relationship.

Fourth, based on the resource-based change perspective and stakeholder theory, we can find that DT helps companies accumulate resources and improve their learning ability and technology. More importantly, enterprises integrate and reconfigure traditional resources through DT to mitigate the disadvantageous situation brought by resource proprietary. Further, in facing multiple stakeholders, DT companies are able to accurately capture the requirements of different stakeholders and have better responsiveness. As a conclusion, we find that DT effectively improves the CEM level.

Based on the above analysis, we propose a conceptual framework of the DT-CEM relationship, which is shown in Figure 4.

FIGURE 4. Mechanisms of digital transformation for corporate environmental management.

5.2 Future research directions and limitations

By reviewing the DT-CEM-related literature, we propose the following three possible future research directions. First, future research still needs to further explore the mechanisms by which DT affects CEM. For example, how companies capture as well as respond to stakeholder demands for CEM through digital technologies? What are the gaps in the capabilities of CEM before and after DT and why? Whether DT has stimulated corporate environmental disclosure and why?

Second, future research can continue to explore the impact of DT on firms at the macro, meso, and micro levels. Future research still needs to further explore the definition of DT and how to measure the process and effects of DT in enterprises. In addition, future research could add quantitative analysis of the economic consequences of DT.

Finally, future research could further explore the evaluation of the effects of CEM, using a combination of qualitative and quantitative analysis. In addition, future research could expand the theoretical and empirical studies of the factors that drive proactive CEM. It should be reminded that while focusing on foreign customers valuing CEM, the literature focusing on domestic customers is still relatively small. In particular, whether CEM is heterogeneous for some companies that have both foreign and domestic customers’ needs to be further explored.

Our study also suffers from the following shortcomings. Our literature has explored DT on CEM as the research topic. However, the literature on the impact of DT on CSR may involve a small number of discussions of corporate environmental behavior. In these discussions, the existence of factors other than environmental responsibility in CSR that act together with DT on CEM remains worthy of continued exploration and may be one of the directions for future research.

5.3 Managerial implications and policy recommendations

The implications of this study are to provide a feasible path for companies and managers to deal with the relationship between DT and CEM. In the era of digital economy, companies are facing more severe challenges. The diversification of stakeholder needs and the explosive growth of big data have substantially increased environmental uncertainty, and companies must enhance their ability to cope with uncertainty and react quickly to develop core competitive advantages. DT reshapes corporate strategy, organizational structure, production processes and internal culture to enhance enterprise value, innovation capabilities, productivity, organizational change and supply chain to adapt to the ever-changing digital environment. By implementing DT, managers can further analyze the environment in which the enterprise operates, accurately adjust corporate strategic decisions, and respond to the demands of all parties for sustainable business development. In addition, companies can proactively cultivate digital capabilities to capture potential opportunities in the market.

In further, based on our findings, we recommend that governments formulate policies to bring about better sustainable development outcomes. First, we suggest that regulators recommend an effective CEM evaluation framework that includes corporate response to corporate environmental responsibility requirements of various stakeholders. Second, we suggest that the government should enact appropriate laws and regulations to promote the development of digital technology and the fulfillment of corporate environmental responsibility. From our results, we can find that the corporate environment is largely influenced by laws and regulations. In addition, digital technology is becoming more and more innovative, and laws and regulations can effectively prevent the abuse of digital technology and promote the benign development of digital technology. Finally, we suggest a platform for real-time communication between government, business and market, and a platform that accurately captures government and market requirements for corporate environmental responsibility based on digital technology.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Author contributions

JX: Conceptualization, Data curation, Formal analysis, Investigation, Software, Writing—original draft. ZW: Conceptualization, Funding acquisition, Investigation, Supervision, Writing—review and editing. BC: Investigation, Writing—review and editing, Validation.

Funding

This study is financially supported by the National Natural Science Foundation of China (Grant numbers: 72173057, 7211101263 and 71672077), Natural Science Foundation of Guangdong Province, China (2021A1515011536), and Fundamental Research Funds for the Central Universities (19JNKY08).

Conflict of Interest

Author BC was employed by ZRP Printing Group Co., Ltd.

The remaining authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Acemoglu, D., Aghion, P., Lelarge, C., Van Reenen, J., and Zilibotti, F. (2007). Technology, information, and the decentralization of the firm. Q. J. Econ. 122 (4), 1759–1799. doi:10.1162/qjec.2007.122.4.1759

Aggarwal, R., Erel, I., Ferreira, M., and Matos, P. (2011). Does governance travel around the world? Evidence from institutional investors. J. Financial Econ. 100 (1), 154–181. doi:10.1016/j.jfineco.2010.10.018

Alemagi, D. (2007). The oil industry along the Atlantic coast of Cameroon: Assessing impacts and possible solutions. Resour. Policy 32 (3), 135–145. doi:10.1016/j.resourpol.2007.08.007

Alkaraan, F., Albitar, K., Hussainey, K., and Venkatesh, V. G. (2022). Corporate transformation toward Industry 4.0 and financial performance: The influence of environmental, social, and governance (ESG). Technol. Forecast. Soc. Change 175, 121423. doi:10.1016/j.techfore.2021.121423

Alonso, S., Montes, R., Molina, D., Palomares, I., Martinez-Camara, E., Chiachio, M., et al. (2021). Ordering artificial intelligence based recommendations to tackle the SDGs with a decision-making model based on surveys. Sustainability 13 (11), 6038. doi:10.3390/su13116038

Ameer, F., and Khan, N. R. (2022). Green entrepreneurial orientation and corporate environmental performance: A systematic literature review. Eur. Manag. J.. doi:10.1016/j.emj.2022.04.003

Andrews, C. J. (1998). Environmental business strategy: Corporate leaders’ perceptions. Soc. Nat. Resour. 11 (5), 531–540. doi:10.1080/08941929809381099

Annarelli, A., Battistella, C., Nonino, F., Parida, V., and Pessot, E. (2021). Literature review on digitalization capabilities: Co-Citation analysis of antecedents, conceptualization and consequences. Technol. Forecast. Soc. Change 166, 120635. doi:10.1016/j.techfore.2021.120635

Aragón-Correa, J. A., Hurtado-Torres, N., Sharma, S., and García-Morales, V. J. (2008). Environmental strategy and performance in small firms: A resource-based perspective. J. Environ. Manag. 86 (1), 88–103. doi:10.1016/j.jenvman.2006.11.022

Aragón-Correa, J. A., and Sharma, S. (2003). A contingent resource-based view of proactive corporate environmental strategy. Acad. Manage. Rev. 28 (1), 71–88. doi:10.5465/amr.2003.8925233

Arora, S., and Gangopadhyay, S. (1995). Toward a theoretical model of voluntary overcompliance. J. Econ. Behav. Organ. 28 (3), 289–309. doi:10.1016/0167-2681(95)00037-2

Babina, T., Fedyk, A., He, A. X., and Hodson, J. (2020). Artificial intelligence, firm growth, and industry concentration. Firm Growth, Industry Concentration. (November 22, 2020).

Beier, G., Kiefer, J., and Knopf, J. (2022). Potentials of big data for corporate environmental management: A case study from the German automotive industry. J. Ind. Ecol. 26 (1), 336–349. doi:10.1111/jiec.13062

Betts, T. K., Wiengarten, F., and Tadisina, S. K. (2015). Exploring the impact of stakeholder pressure on environmental management strategies at the plant level: What does industry have to do with it? J. Clean. Prod. 92, 282–294. doi:10.1016/j.jclepro.2015.01.002

Bloom, N., Garicano, L., Sadun, R., and Van Reenen, J. (2014). The distinct effects of information technology and communication technology on firm organization. Manag. Sci. 60 (12), 2859–2885. doi:10.1287/mnsc.2014.2013

Boccia, F., and Sarnacchiaro, P. (2018). The impact of corporate social responsibility on consumer preference: A structural equation analysis. Corp. Soc. Responsib. Environ. Manag. 25 (2), 151–163. doi:10.1002/csr.1446

Bonanomi, M. M., Hall, D. M., Staub-French, S., Tucker, A., and Talamo, C. M. L. (2019). The impact of digital transformation on formal and informal organizational structures of large architecture and engineering firms. Eng. Constr. Archit. Manag. 27 (4), 872–892. doi:10.1108/ECAM-03-2019-0119

Brammer, S., Hoejmose, S., and Marchant, K. (2012). Environmental management in SME s in the UK: Practices, pressures and perceived benefits. Bus. Strategy Environ. 21 (7), 423–434. doi:10.1002/bse.717

Brynjolfsson, E., and Saunders, A. (2009). Wired for innovation: How information technology is reshaping the economy. Cambridge, MA: Mit Press.

Camodeca, R., and Almici, A. (2021). Digital transformation and convergence toward the 2030 agenda's sustainability development goals: Evidence from Italian listed firms. Sustainability 13 (21), 11831. doi:10.3390/su132111831

Camuffo, A., and Gerli, F. (2018). Modeling management behaviors in lean production environments. Int. J. Operations Prod. Manag. 38 (2), 403–423. doi:10.1108/IJOPM-12-2015-0760

Castro, G. D. R., Fernandez, M. C. G., and Colsa, Á. U. (2021). Unleashing the convergence amid digitalization and sustainability towards pursuing the sustainable development goals (SDGs): A holistic review. J. Clean. Prod. 280, 122204. doi:10.1016/j.jclepro.2020.122204

Cerchiaro, D., Leo, S., Landriault, E., and De Vega, P. (2021). DLT to boost efficiency for financial intermediaries. An application in ESG reporting activities. Technol. Analysis Strategic Manag., 1–14. doi:10.1080/09537325.2021.1999921

Chan, J. C. h., and Welford, R. (2005). Assessing corporate environmental risk in China: An evaluation of reporting activities of Hong Kong listed enterprises. Corp. Soc. Responsib. Environ. Manag. 12 (2), 88–104. doi:10.1002/csr.88

Chen, M., Ma, M., Lin, Y., Ma, Z., and Li, K. (2022). Carbon Kuznets curve in China’s building operations: Retrospective and prospective trajectories. Sci. Total Environ. 803, 150104. doi:10.1016/j.scitotenv.2021.150104

Chen, T., Dong, H., and Lin, C. (2020). Institutional shareholders and corporate social responsibility. J. Financial Econ. 135 (2), 483–504. doi:10.1016/j.jfineco.2019.06.007

Chen, W., and Srinivasan, S. (2019). Going digital: Implications for firm value and performance. Boston: Harvard Business School.

Chen, Y.-Y. K., Jaw, Y.-L., and Wu, B.-L. (2016). Effect of digital transformation on organisational performance of SMEs: Evidence from the Taiwanese textile industry’s web portal. Internet Res. 26 (1), 186–212. doi:10.1108/IntR-12-2013-0265

Choi, B., and La, S. (2013). The impact of corporate social responsibility (CSR) and customer trust on the restoration of loyalty after service failure and recovery. J. Serv. Mark. 27 (3), 223–233. doi:10.1108/08876041311330717

Christmann, P., and Taylor, G. (2001). Globalization and the environment: Determinants of firm self-regulation in China. J. Int. Bus. Stud. 32 (3), 439–458. doi:10.1057/palgrave.jibs.8490976

Cockburn, I. M., Henderson, R., and Stern, S. (2019). “4. The impact of artificial intelligence on innovation: An exploratory analysis,” in The Economics of Artificial Intelligence (Chicago: University of Chicago Press), 115–148. doi:10.7208/9780226613475-006

Cortès, U., Sànchez-Marrè, M., Ceccaroni, L., and Poch, M. (2000). Artificial intelligence and environmental decision support systems. Appl. Intell. (Dordr). 13 (1), 77–91. doi:10.1023/A:1008331413864

Costa, I., Riccotta, R., Montini, P., Stefani, E., de Souza Goes, R., Gaspar, M. A., et al. (2022). The degree of contribution of digital transformation technology on company sustainability areas. Sustainability 14 (1), 462. doi:10.3390/su14010462

Cox, P., Brammer, S., and Millington, A. (2004). An empirical examination of institutional investor preferences for corporate social performance. J. Bus. Ethics 52 (1), 27–43. doi:10.1023/B:BUSI.0000033105.77051.9d

Dabić, M., Vlačić, B., Paul, J., Dana, L.-P., Sahasranamam, S., and Glinka, B. (2020). Immigrant entrepreneurship: A review and research agenda. J. Bus. Res. 113, 25–38. doi:10.1016/j.jbusres.2020.03.013

Demirkan, H., Spohrer, J. C., and Welser, J. J. (2016). Digital innovation and strategic transformation. IT Prof. 18 (6), 14–18. doi:10.1109/MITP.2016.115

Dhar, B. K., Sarkar, S. M., and Ayittey, F. K. (2022). Impact of social responsibility disclosure between implementation of green accounting and sustainable development: A study on heavily polluting companies in Bangladesh. Corp. Soc. Responsib. Environ. Manag. 29 (1), 71–78. doi:10.1002/csr.2174

Ding, X. A., and Shahzad, M. (2022). Environmental administrative penalty, environmental disclosures, and the firm’s cash flow: Evidence from manufacturing firms in China. Environ. Sci. Pollut. Res. 29 (24), 36674–36683. doi:10.1007/s11356-021-18145-3

Dyck, A., Lins, K. V., Roth, L., and Wagner, H. F. (2019). Do institutional investors drive corporate social responsibility? International evidence. J. Financial Econ. 131 (3), 693–714. doi:10.1016/j.jfineco.2018.08.013

Earnhart, D. (2017). Corporate environmental strategies in transition economies: Survey of the literature. East. Eur. Econ. 55 (2), 111–145. doi:10.1080/00128775.2016.1271279

Earnhart, D. H., Khanna, M., and Lyon, T. P. (2014). Corporate environmental strategies in emerging economies. Rev. Environ. Econ. Policy 8 (2), 164–185. doi:10.1093/reep/reu001

Fenech, R., Baguant, P., and Ivanov, D. (2019). The changing role of human resource management in an era of digital transformation. J. Manag. Inf. Decis. Sci. 22 (2), 166–175.

Fitzgerald, M., Kruschwitz, N., Bonnet, D., and Welch, M. (2014). Embracing digital technology: A new strategic imperative. MIT Sloan Manag. Rev. 55 (2), 1–14.

Garicano, L. (2000). Hierarchies and the organization of knowledge in production. J. Polit. Econ. 108, 874–904. doi:10.1086/317671

Gonzalez-Rodriguez, M. R., Diaz-Fernandez, M. C., and Simonetti, B. (2015). The social, economic and environmental dimensions of corporate social responsibility: The role played by consumers and potential entrepreneurs. Int. Bus. Rev. 24 (5), 836–848. doi:10.1016/j.ibusrev.2015.03.002

Gurbaxani, V., and Dunkle, D. (2019). Gearing up for successful digital transformation. MIS Q. Exec. 18 (3), 209–220. doi:10.17705/2msqe.00017

Hanelt, A., Bohnsack, R., Marz, D., and Antunes Marante, C. (2021). A systematic review of the literature on digital transformation: Insights and implications for strategy and organizational change. J. Manag. Stud. 58 (5), 1159–1197. doi:10.1111/joms.12639

He, Q., Meadows, M., Angwin, D., Gomes, E., and Child, J. (2020). Strategic alliance research in the era of digital transformation: Perspectives on future research. Brit. J. Manage. 31 (3), 589–617. doi:10.1111/1467-8551.12406

Helfat, C. E., Finkelstein, S., Mitchell, W., Peteraf, M., Singh, H., Teece, D., et al. (2009). Dynamic capabilities: Understanding strategic change in organizations. New York: John Wiley & Sons.

Helfat, C. E., and Peteraf, M. A. (2003). The dynamic resource-based view: Capability lifecycles. Strateg. Manag. J. 24 (10), 997–1010. doi:10.1002/smj.332

Hess, T., Matt, C., Benlian, A., and Wiesböck, F. (2016). Options for formulating a digital transformation strategy. MIS Q. Exec. 15 (2), 123–139.

Hoejmose, S., Brammer, S., and Millington, A. (2012). Green” supply chain management: The role of trust and top management in B2B and B2C markets. Ind. Mark. Manag. 41 (4), 609–620. doi:10.1016/j.indmarman.2012.04.008

Hughes, A., Urban, M. A., and Wójcik, D. (2021). Alternative ESG ratings: How technological innovation is reshaping sustainable investment. Sustainability 13 (6), 3551. doi:10.3390/su13063551

Iansiti, M., and Lakhani, K. R. (2014). Digital ubiquity: How connections, sensors, and data are revolutionizing business. Harv. Bus. Rev. 92 (11), 19.

Isensee, C., Teuteberg, F., Griese, K.-M., and Topi, C. (2020). The relationship between organizational culture, sustainability, and digitalization in SMEs: A systematic review. J. Clean. Prod. 275, 122944. doi:10.1016/j.jclepro.2020.122944

Ivanov, D., Dolgui, A., and Sokolov, B. (2019). The impact of digital technology and Industry 4.0 on the ripple effect and supply chain risk analytics. Int. J. Prod. Res. 57, 829–846. doi:10.1080/00207543.2018.1488086

Jabbour, C. J. C., Fiorini, P. D. C., Ndubisi, N. O., Queiroz, M. M., and Piato, É. L. (2020). Digitally-enabled sustainable supply chains in the 21st century: A review and a research agenda. Sci. Total Environ. 725, 138177. doi:10.1016/j.scitotenv.2020.138177

Kearins, K., Collins, E., and Tregidga, H. (2010). Beyond corporate environmental management to a consideration of nature in visionary small enterprise. Bus. Soc. 49 (3), 512–547. doi:10.1177/0007650310368988

Kejing, C. (2018). The exit threat and corporate governance: From the perspective of earnings management. J. Finance Econ. 44 (11), 18–32. doi:10.16538/j.cnki.jfe.2018.11.002

Khin, S., and Ho, T. C. (2018). Digital technology, digital capability and organizational performance: A mediating role of digital innovation. Int. J. Innovation Sci. 11, 177–195. doi:10.1108/IJIS-08-2018-0083

Kim, I., Wan, H., Wang, B., and Yang, T. (2019). Institutional investors and corporate environmental, social, and governance policies: Evidence from toxics release data. Manag. Sci. 65 (10), 4901–4926. doi:10.1287/mnsc.2018.3055

Kıymalıoğlu, A. (2022). “Impact of digital transformations on corporate social responsibility (CSR) practices in Turkey: A study of the current environment,” in Research anthology on developing socially responsible businesses (Hershey: IGI Global), 1688–1704.

Klassen, R. D., and McLaughlin, C. P. (1996). The impact of environmental management on firm performance. Manag. Sci. 42 (8), 1199–1214. doi:10.1287/mnsc.42.8.1199

Koh, L., Orzes, G., and Jia, F. J. (2019). The fourth industrial revolution (industry 4.0): Technologies disruption on operations and supply chain management. Int. J. Operations Prod. Manag. 39 (6/7/8), 817–828. doi:10.1108/IJOPM-08-2019-788

Kraatz, M. S., and Zajac, E. J. (2001). How organizational resources affect strategic change and performance in turbulent environments: Theory and evidence. Organ. Sci. 12 (5), 632–657. doi:10.1287/orsc.12.5.632.10088

Kretschmer, T., and Khashabi, P. (2020). Digital transformation and organization design: An integrated approach. Calif. Manag. Rev. 62 (4), 86–104. doi:10.1177/0008125620940296

Latan, H., Jabbour, C. J. C., de Sousa Jabbour, A. B. L., Wamba, S. F., and Shahbaz, M. (2018). Effects of environmental strategy, environmental uncertainty and top management’s commitment on corporate environmental performance: The role of environmental management accounting. J. Clean. Prod. 180, 297–306. doi:10.1016/j.jclepro.2018.01.106

Latif, K. F., Pérez, A., and Sahibzada, U. F. (2020). Corporate social responsibility (CSR) and customer loyalty in the hotel industry: A cross-country study. Int. J. Hosp. Manag. 89, 102565. doi:10.1016/j.ijhm.2020.102565

Lee, K. H., and Cheong, I. M. (2011). Measuring a carbon footprint and environmental practice: The case of hyundai motors Co.(HMC). Industrial Manag. Data Syst. 111 (6), 961–978. doi:10.1108/02635571111144991

Lewis, A., and Mackenzie, C. (2000). Support for investor activism among UK ethical investors. J. Bus. Ethics 24 (3), 215–222. doi:10.1023/A:1006082125886

Lezoche, M., Hernandez, J. E., Díaz, M. d. M. E. A., Panetto, H., and Kacprzyk, J. (2020). Agri-food 4.0: A survey of the supply chains and technologies for the future agriculture. Comput. Industry 117, 103187. doi:10.1016/j.compind.2020.103187

Li, K., Ma, M., Xiang, X., Feng, W., Ma, Z., Cai, W., et al. (2022). Carbon reduction in commercial building operations: A provincial retrospection in China. Appl. Energy 306, 118098. doi:10.1016/j.apenergy.2021.118098

Li, Y., Yang, X., Ran, Q., Wu, H., Irfan, M., and Ahmad, M. (2021). Energy structure, digital economy, and carbon emissions: Evidence from China. Environ. Sci. Pollut. Res. 28 (45), 64606–64629. doi:10.1007/s11356-021-15304-4

Liu, H., and Jung, J.-S. (2021). The effect of CSR attributes on CSR authenticity: Focusing on mediating effects of digital transformation. Sustainability 13 (13), 7206. doi:10.3390/su13137206

Liu, M. T., Liu, Y., Mo, Z., Zhao, Z., and Zhu, Z. (2020). How CSR influences customer behavioural loyalty in the Chinese hotel industry. Asia Pac. J. Mark. Logist. 32 (1), 1–22. doi:10.1108/APJML-04-2018-0160

Liu, N., Tang, S. Y., Zhan, X. Y., and Lo, C. W. H. (2018). Political commitment, policy ambiguity, and corporate environmental practices. Policy Stud. J. 46 (1), 190–214. doi:10.1111/psj.12130

Ma, Q., Khan, Z., Tariq, M., IŞik, H., and Rjoub, H. (2022). Sustainable digital economy and trade adjusted carbon emissions: Evidence from China’s provincial data. Economic Research-Ekonomska Istrazivanja. 35, 1–17. doi:10.1080/1331677X.2022.2028179

Martín-de Castro, G., Amores-Salvadó, J., Navas-López, J. E., and Balarezo-Núñez, R. M. (2020). Corporate environmental reputation: Exploring its definitional landscape. Bus. Ethics A Eur. Rev. 29 (1), 130–142. doi:10.1111/beer.12250

Martínez, P., and Rodríguez del Bosque, I. (2013). CSR and customer loyalty: The roles of trust, customer identification with the company and satisfaction. Int. J. Hosp. Manag. 35, 89–99. doi:10.1016/j.ijhm.2013.05.009

Matarazzo, M., Penco, L., Profumo, G., and Quaglia, R. (2021). Digital transformation and customer value creation in made in Italy SMEs: A dynamic capabilities perspective. J. Bus. Res. 123, 642–656. doi:10.1016/j.jbusres.2020.10.033

Matt, C., Hess, T., and Benlian, A. (2015). Digital transformation strategies. Bus. Inf. Syst. Eng. 57 (5), 339–343. doi:10.1007/s12599-015-0401-5

Mikalef, P., Krogstie, J., Pappas, I. O., and Pavlou, P. (2020). Exploring the relationship between big data analytics capability and competitive performance: The mediating roles of dynamic and operational capabilities. Inf. Manag. 57 (2), 103169. doi:10.1016/j.im.2019.05.004

Mikalef, P., and Pateli, A. (2017). Information technology-enabled dynamic capabilities and their indirect effect on competitive performance: Findings from PLS-SEM and fsQCA. J. Bus. Res. 70, 1–16. doi:10.1016/j.jbusres.2016.09.004

Munasinghe, M. (1999). Is environmental degradation an inevitable consequence of economic growth: Tunneling through the environmental kuznets curve. Ecol. Econ. 29 (1), 89–109. doi:10.1016/S0921-8009(98)00062-7

Mura, M., Longo, M., Domingues, A. R., and Zanni, S. (2019). An exploration of content and drivers of online sustainability disclosure: A study of Italian organisations. Sustainability 11 (12), 3422. doi:10.3390/su11123422

Orbik, Z., and Zozuľaková, V. (2019). Corporate social and digital responsibility. Manag. Syst. Prod. Eng. 2 (27), 79–83. doi:10.1515/mspe-2019-0013

Pagani, M., and Pardo, C. (2017). The impact of digital technology on relationships in a business network. Ind. Mark. Manag. 67, 185–192. doi:10.1016/j.indmarman.2017.08.009

Paul, J., and Benito, G. R. (2018). A review of research on outward foreign direct investment from emerging countries, including China: What do we know, how do we know and where should we be heading? Asia Pac. Bus. Rev. 24 (1), 90–115. doi:10.1080/13602381.2017.1357316

Pérez, A., and Rodríguez del Bosque, I. (2015). An integrative framework to understand how CSR affects customer loyalty through identification, emotions and satisfaction. J. Bus. Ethics 129 (3), 571–584. doi:10.1007/s10551-014-2177-9

Petersen, H. L., and Vredenburg, H. (2009). Morals or economics? Institutional investor preferences for corporate social responsibility. J. Bus. Ethics 90 (1), 1–14. doi:10.1007/s10551-009-0030-3

Pilloni, V. (2018). How data will transform industrial processes: Crowdsensing, crowdsourcing and big data as pillars of industry 4.0. Future Internet 10 (3), 24. doi:10.3390/fi10030024

Pucheta-Martínez, M. C., and Chiva-Ortells, C. (2018). The role of directors representing institutional ownership in sustainable development through corporate social responsibility reporting. Sustain. Dev. 26 (6), 835–846. doi:10.1002/sd.1853

Raff, Z., and Earnhart, D. (2018). Effect of cooperative enforcement strategies on wastewater management. Econ. Inq. 56 (2), 1357–1379. doi:10.1111/ecin.12549

Rialti, R., Marzi, G., Ciappei, C., and Busso, D. (2019). Big data and dynamic capabilities: A bibliometric analysis and systematic literature review. Manag. Decis. 57 (8), 2052–2068. doi:10.1108/MD-07-2018-0821

Ronaghi, M. H., and Mosakhani, M. (2022). The effects of blockchain technology adoption on business ethics and social sustainability: Evidence from the Middle East. Environ. Dev. Sustain. 24 (5), 6834–6859. doi:10.1007/s10668-021-01729-x

Rowe, A. L., and Guthrie, J. (2010). The Chinese government’s formal institutional influence on corporate environmental management. Public Manag. Rev. 12 (4), 511–529. doi:10.1080/14719037.2010.496265

Saberi, S., Kouhizadeh, M., Sarkis, J., and Shen, L. (2019). Blockchain technology and its relationships to sustainable supply chain management. Int. J. Prod. Res. 57 (7), 2117–2135. doi:10.1080/00207543.2018.1533261

Sanchez, L. E. (1998). Industry response to the challenge of sustainability: The case of the Canadian nonferrous mining sector. Environ. Manag. 22 (4), 521–531. doi:10.1007/s002679900125

Sarkis, J., Gonzalez-Torre, P., and Adenso-Diaz, B. (2010). Stakeholder pressure and the adoption of environmental practices: The mediating effect of training. J. Operations Manag. 28 (2), 163–176. doi:10.1016/j.jom.2009.10.001

Schaltegger, S., and Synnestvedt, T. (2002). The link between ‘green’ and economic success: Environmental management as the crucial trigger between environmental and economic performance. J. Environ. Manag. 65 (4), 339–346. doi:10.1006/jema.2002.0555

Scharfstein, D. S., and Stein, J. C. (1990). Herd behavior and investment. Am. Econ. Rev. 80 (3), 465–479.

Seele, P. (2017). Predictive sustainability control: A review assessing the potential to transfer big data driven ‘predictive policing’ to corporate sustainability management. J. Clean. Prod. 153, 673–686. doi:10.1016/j.jclepro.2016.10.175

Sheel, A., and Nath, V. (2019). Effect of blockchain technology adoption on supply chain adaptability, agility, alignment and performance. Manag. Res. Rev. 42 (12), 1353–1374. doi:10.1108/MRR-12-2018-0490

Sun, A. (2013). Enabling collaborative decision-making in watershed management using cloud-computing services. Environ. Model. Softw. 41, 93–97. doi:10.1016/j.envsoft.2012.11.008

Sun, Z., Ma, Z., Ma, M., Cai, W., Xiang, X., Zhang, S., et al. (2022). Carbon peak and carbon neutrality in the building sector: A bibliometric review. Buildings 12 (2), 128. doi:10.3390/buildings12020128

Tambe, P. (2014). Big data investment, skills, and firm value. Manag. Sci. 60 (6), 1452–1469. doi:10.1287/mnsc.2014.1899

Trocin, C., Hovland, I. V., Mikalef, P., and Dremel, C. (2021). How artificial intelligence affords digital innovation: A cross-case analysis of scandinavian companies. Technol. Forecast. Soc. Change 173, 121081. doi:10.1016/j.techfore.2021.121081

Troise, C., and Camilleri, M. A. (2021). “The use of digital media for marketing, CSR communication and stakeholder engagement,” in Strategic corporate communication in the digital age (Bingley: Emerald Publishing Limited).

Uhlenbruck, K., Meyer, K. E., and Hitt, M. A. (2003). Organizational transformation in transition economies: Resource-based and organizational learning perspectives. J. Manag. Stud. 40 (2), 257–282. doi:10.1111/1467-6486.00340

Usai, A., Fiano, F., Petruzzelli, A. M., Paoloni, P., Briamonte, M. F., and Orlando, B. (2021). Unveiling the impact of the adoption of digital technologies on firms’ innovation performance. J. Bus. Res. 133, 327–336. doi:10.1016/j.jbusres.2021.04.035

Valentine, S. V. (2012). Policies for enhancing corporate environmental management: A framework and an applied example. Bus. Strategy Environ. 21 (5), 338–350. doi:10.1002/bse.745

Verbeke, A., Bowen, F., and Sellers, M. (2006). “Corporate environmental strategy: Extending the natural resource-based view of the firm,” in Academy of MANAgement proceedings (New York: Academy of Management), 2006, A1–A6. doi:10.5465/ambpp.2006.27176644

Verhoef, P. C., Broekhuizen, T., Bart, Y., Bhattacharya, A., Dong, J. Q., Fabian, N., et al. (2021). Digital transformation: A multidisciplinary reflection and research agenda. J. Bus. Res. 122, 889–901. doi:10.1016/j.jbusres.2019.09.022