Serap Yörübulut

Serap Yörübulut- Department of Statistics, Faculty of Engineering and Natural Sciences, Kırıkkale University, Kirikkale, Türkiye

Introduction: Agricultural production in Türkiye is increasingly exposed to risks stemming from climate change, environmental degradation, and economic volatility. Effective insurance mechanisms are crucial for building resilience in this sector.

Methods: This study analyzes agricultural insurance demand in Türkiye from 2006 to 2023 using Partial Least Squares Structural Equation Modeling (PLS-SEM). Three latent constructs are examined: Agricultural Economy (agricultural GDP, agricultural area, insured area), Insurance Economy (government subsidized premium, total premiums, insured values), and Ecological-Meteorological Risks (Load Capacity Factor and meteorological disasters count).

Results: The agricultural economy is identified as the strongest predictor of insurance demand, followed by the insurance economy and ecological-meteorological risks. The inclusion of Load Capacity Factor introduces a novel ecological dimension, revealing that insurance demand increases as ecological thresholds are approached.

Discussion: The study proposes that structural modeling outputs can be utilized in designing index-based insurance premiums. It recommends policy interventions such as ecological risk zoning, vulnerability-based premium subsidies, and adaptive insurance schemes. Integrating ecological indicators into insurance modeling offers a future-oriented approach to sustainable agricultural risk management.

1 Introduction

The agricultural sector is widely recognized as one of the most vulnerable components of economic systems due to its direct dependence on climatic and environmental conditions. This vulnerability has been exacerbated by the growing frequency and intensity of extreme weather events and ecological degradation associated with climate change (IPCC, 2021). Events such as droughts, hailstorms, frosts, floods, and windstorms not only disrupt agricultural production but also pose significant threats to the income stability of farmers (Hazell, 2001). Consequently, agricultural producers face multifaceted risks stemming from both yield and revenue losses.

In this context, agricultural insurance emerges as a crucial financial instrument that enhances farmers’ resilience and supports agricultural sustainability (Mahul and Stutley, 2010). However, in many countries including Türkiye, the demand for agricultural insurance remains below expectations, limiting both the financial sustainability and inclusiveness of such systems. In countries located in the Mediterranean basin, such as Türkiye, which are particularly vulnerable to climate-related risks, meteorological disasters have increased by more than 40% over the past 2 decades (Türkeş et al., 2020). This upward trend has heightened uncertainty in the agricultural sector and underscored the need for robust, insurance-based risk management mechanisms.

For instance, the hail disaster that occurred in Antalya in 2021 resulted in economic losses exceeding 150 million USD and led to a 65% surge in local insurance policy applications (TARSİM, 2023). This case demonstrates that insurance demand is sensitive to disaster occurrences; however, the overall level of insurance penetration remains insufficient. As of 2023, agricultural insurance penetration in Türkiye stands at approximately 42%, significantly below the 70%–90% levels observed in developed countries (OECD, 2023). This disparity is not solely attributed to economic capacity but also to factors such as environmental awareness, policy incentives, and systemic sustainability indicators.

While the existing literature has primarily focused on the economic determinants of agricultural insurance demand such as farmers’ income levels, premium rates, government subsidies, and financial literacy (Coble and Knight, 2002; Glauber, 2013) recent research increasingly acknowledges the role of environmental and climatic factors. Empirical evidence from Türkiye indicates that the rising frequency of natural disasters significantly influences insurance uptake (Hayran, 2023).

However, despite the growing recognition of climate and environmental risks, most existing studies fail to integrate comprehensive sustainability indicators into insurance demand modeling. Research tends to rely on individual weather events or general climate indices, without capturing the systemic ecological pressures such as the overuse of natural resources or biocapacity imbalance that may drive long-term risk behavior (Galli et al., 2014). This gap limits the ability of traditional models to reflect the broader environmental dynamics influencing insurance decisions.

Beyond economic and climatic variables, the demand for agricultural insurance is also shaped by indicators of environmental sustainability. Metrics such as the ecological footprint, biocapacity, and the LCF offer valuable insights into a country’s natural resource usage and its ecological balance. These indicators reflect the interaction between human activity and the environment, thereby enabling a more comprehensive understanding of environmental risks and their implications for insurance systems (Galli et al., 2014). Notably, LCF has gained attention in recent literature as a novel and robust indicator for assessing the environmental dimension of sustainability and its potential links to insurance dynamics.

To date, the existing literature has not explicitly integrated the LCF within a structural framework aimed at analyzing agricultural insurance demand, particularly in the context of emerging economies. This omission is significant, as LCF quantitatively reflects the extent to which ecological consumption exceeds biocapacity, thereby serving as a salient indicator of environmental pressure and heightened risk perception among agricultural stakeholders (Borucke et al., 2013). By incorporating LCF into the analytical model, the present study addresses a notable gap in the literature, providing a comprehensive and nuanced understanding of insurance demand dynamics under conditions of ecological stress and sustainability constraints.

Many previous studies have relied on micro-level datasets or adopted a narrow focus on specific economic or meteorological variables. Yet, agricultural insurance demand is a multidimensional and dynamic phenomenon that intersects with economic, environmental, and institutional domains. Therefore, it is essential to analyze the complex interplay between these factors using integrated and structural modeling approaches.

In addition to these interdisciplinary perspectives, actuarial modeling plays a pivotal role in transforming complex ecological and economic relationships into applicable insurance pricing mechanisms. Traditional premium-setting practices often rely on backward-looking models that focus on historical losses (Mayers and Smith, 1990; Powers and Shubik, 2006). However, in the context of climate volatility, there is a growing consensus that forward-looking actuarial approaches those that incorporate environmental indicators and latent constructs are essential for sustainable insurance design. By utilizing latent scores derived from structural modeling, insurers can generate composite risk indices that feed directly into index-based or dynamic premium rate structures, enhancing both the responsiveness and fairness of insurance systems.

Despite the availability of powerful structural methods such as PLS-SEM, very few studies in agricultural economics have leveraged this technique to model latent relationships in insurance behavior. This underutilization presents a methodological gap that limits the explanatory power and predictive accuracy of many empirical models (Hair et al., 2021; Sarstedt et al., 2016).

This study aims to analyze the determinants of agricultural insurance demand in Türkiye by examining the interrelationships between economic, environmental, and meteorological factors through the application of the PLS-SEM technique. Utilizing annual data spanning the period 2006–2023, we construct a conceptual model involving three latent variables: Agricultural Economy, Insurance Economy and Ecological and Meteorological Risks.

The present study contributes to the literature in three significant ways. First, it introduces environmental sustainability indicators particularly the LCF into the analysis of agricultural insurance demand for the first time in the Turkish context. This integration enables a more comprehensive modeling of climate-related risks that extend beyond short-term weather shocks and into systemic ecological conditions. Second, by employing PLS-SEM, it captures complex and nonlinear relationships beyond the scope of traditional regression models. The model also accounts for potential collinearity and measurement error, offering a more robust estimation of latent constructs and their predictive relevance (Henseler et al., 2015). Third, the findings are interpreted with a focus on policy implications for Türkiye, offering actionable insights for developing climate-resilient agricultural policies.

In this regard, the study seeks to provide both theoretical and practical contributions. It underscores the necessity of integrating environmental sustainability into insurance system design and offers a conceptual framework for understanding the role of insurance in building climate resilience in agriculture.

By responding directly to the shortcomings of prior research both in terms of variables used and methods applied this paper aims to advance the scholarly understanding of agricultural risk management and deliver meaningful value to policymakers, insurers, and researchers alike.

2 Literature review

The agricultural sector is inherently sensitive to adverse climate impacts due to its strong dependency on natural conditions. Increasing temperature fluctuations, sudden droughts, floods, hailstorms, and windstorms have amplified uncertainties in agricultural production. Consequently, agricultural insurance has become a strategic risk management tool for both producers and policymakers. As highlighted by Mahul and Stutley (2010), agricultural insurance helps ensure the sustainability of farming activities by protecting producers’ incomes against climate-induced yield losses. However, the effectiveness of insurance systems depends not only on their technical design but also on economic and environmental factors influencing demand. Recent studies, such as Hu et al. (2024), challenge the assumption that higher premium subsidies universally enhance welfare, demonstrating that excessive subsidies may distort risk perceptions and reduce long-term resilience a critical consideration for Türkiye’s TARSİM system, where subsidies exceed 50% of premiums.

Moreover, agricultural insurance participation is not only a financial decision but also reflects how farmers perceive and react to environmental uncertainties. This highlights the need to explore the behavioral, cognitive, and psychological factors that shape farmers’ willingness to adopt insurance, including their prior exposure to climate events, risk tolerance, and trust in the insurance system.

Most existing studies on insurance demand emphasize socio-economic characteristics of farmers, income levels, farm size, and government support mechanisms. For instance, Coble and Knight (2002) demonstrated that producer income levels and public subsidies play a decisive role in insurance participation. Similar results have been observed in studies focusing on Turkey, where factors such as agricultural GDP, crop-based subsidies, and damage compensation have shown statistically significant relationships with farmers’ insurance preferences (Özgür, 2019). However, the majority of these studies tend to focus on economic variables, with limited attention to environmental and ecological dimensions. This gap is partially addressed by Chai and Zhang (2024), whose work in Inner Mongolia reveals that insurance adoption significantly alters planting structures toward higher-risk crops, suggesting that environmental risk internalization occurs even without explicit ecological indicators in insurance models.

However, these studies often overlook the multifaceted impact of ecological degradation and meteorological instability on crop patterns and farming livelihoods. Thus, incorporating region-specific climate scenarios and landscape vulnerability assessments can enrich insurance demand modeling by aligning it with the lived realities of farmers under environmental stress.

In recent years, a growing body of research has emphasized that the demand for agricultural insurance is shaped not only by economic indicators but also by perceived climate risk, environmental sustainability, and ecological stress factors. For example, Boháčiková et al. (2017) argued that uncertainty caused by climate change increases farmers’ perception of risk, thereby enhancing interest in insurance systems. Similarly, Jin et al. (2016) found a significant positive relationship between the frequency of meteorological disasters and insurance uptake, suggesting that environmental stress drives farmers toward insurance. These findings are reinforced by Manescu et al. (2025), who quantify how extreme weather events across Europe systematically increase insurance demand while simultaneously straining insurer solvency a dual dynamic directly relevant to Türkiye’s diverse agroclimatic context.

Building on these insights, it becomes increasingly important to contextualize insurance demand within the broader framework of climate resilience and adaptive capacity. In particular, understanding how insurance can act as both a reactive and proactive tool in farmers’ long-term adaptation strategies is crucial, especially in regions facing chronic environmental vulnerability.

Despite this emerging evidence, the integration of measurable environmental sustainability indicators into insurance models remains limited. In this context, ecological indicators such as the LCF offer a valuable methodological innovation. LCF measures the ratio between a country’s biocapacity and its ecological footprint, thereby indicating the sustainability level of pressure placed on nature (Galli et al., 2014). Such indicators are increasingly featured in environment-economy-oriented academic literature and contribute to the development of sustainability-based insurance analyses. The predictive potential of ecological metrics is further validated by Seamon et al. (2023), who demonstrate that climatic damage causation patterns (e.g., drought vs hail) require distinct insurance modeling approaches—a nuance absent in traditional economic-centric studies.

Integrating these ecological metrics, such as LCF, provides a way to capture the latent environmental stressors that may not be immediately observable but have profound effects on long-term farming viability and insurance viability. It also offers a path toward the design of index-based insurance products tailored to ecosystem-specific vulnerabilities.

The literature also shows that the performance of agricultural insurance systems is generally assessed using traditional statistical techniques such as regression and correlation. However, in recent years, PLS-SEM has emerged as a powerful tool for analyzing complex, multidimensional structures. As detailed by Hair et al. (2021), PLS-SEM is capable of modeling relationships between unobserved (latent) variables and generating robust results even with small sample sizes. The limited use of this technique in agricultural insurance studies presents a theoretical and methodological research gap that this study aims to address. Recent applications of PLS-SEM in insurance contexts, such as Falsafian et al. (2024)’s welfare analysis of area-yield insurance, underscore its suitability for capturing latent behavioral and environmental drivers—a key advantage leveraged in our study.

Additionally, PLS-SEM allows for simultaneous modeling of economic, ecological, and psychological constructs, which enhances the explanatory power of structural models in complex systems like agricultural insurance. This methodological strength supports a more integrated and realistic understanding of insurance demand in environmentally stressed regions.

In light of these advancements, our study positions itself at the intersection of SEM methodology and actuarial modeling. Although this paper does not perform direct premium estimation, it provides a structural basis by generating composite indices through SEM, which could be operationalized in index-based premium formulations in future research. In doing so, we align with recent actuarial literature that advocates for hybrid risk modeling combining data-driven latent indicators with traditional pricing formulas (Zhang, 2024; Zeng et al., 2025).

In conclusion, while the economic dimensions of insurance demand have been extensively analyzed in the literature, the number of structural models that holistically evaluate environmental and climatic factors remains very limited. This study’s originality lies in its integration of the LCF a globally recognized ecological sustainability metric into a PLS-SEM framework alongside traditional economic variables, a approach not yet explored in the agriculture insurance literature. By doing so, the research not only provides insights into the future of agricultural insurance in developing countries but also offers policy recommendations to support climate change adaptation strategies. The work of Kurdyś-Kujawska et al. (2021) on insurance-environment-productivity triads provides a conceptual foundation for our model, while Rusteika and Skinulienė (2023)’s findings on participant expectations inform our policy proposals for enhancing TARSİM’s transparency and accessibility.

Ultimately, this study aims to contribute to a more inclusive and sustainability-driven insurance discourse by advancing a comprehensive analytical framework that bridges economic reasoning with ecological accountability in the context of agricultural risk. This also opens the door for a new generation of actuarial models informed by latent environmental and economic variables, moving agricultural insurance toward a more adaptive, predictive, and data-integrated future.

3 The structure and practices of agricultural insurance in Türkiye: current situation and trend analysis (2006–2023)

Agriculture is one of the most risk-prone economic sectors, especially vulnerable to natural disasters, climate variability, market fluctuations, and various biotic/abiotic stresses. Agricultural insurance, therefore, stands out as a crucial risk management tool for protecting farmers against such uncertainties. In Türkiye, the institutional foundation of agricultural insurance was established with the enactment of Law No. 5363 in 2005. Subsequently, in 2006, the TARSİM was launched as a public-private partnership model, marking the beginning of a state-subsidized insurance system.

TARSİM covers a wide range of insurance products, including crop insurance, livestock insurance, greenhouse insurance, aquaculture insurance, and beekeeping insurance. Particularly, crop insurance provides coverage against meteorological events such as frost, hail, storm, flood, and drought. Despite this wide scope, insurance penetration in Turkish agriculture remains relatively low compared to developed countries. This limited coverage is largely due to factors such as low financial literacy, insufficient risk awareness, inadequate record-keeping of agricultural activities in some regions, and limited perception of insurance as a preventive tool (Burhan, 2023; Zhichkin et al., 2023).

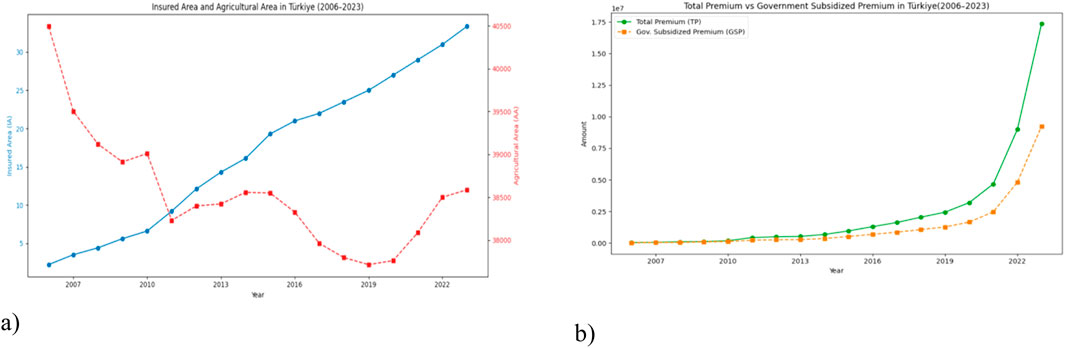

State support plays a key role in the expansion and sustainability of Türkiye’s agricultural insurance system. Between 50% and 67% of premium costs are subsidized by the government. As shown in Figure 1b, this support has led to a noticeable increase in premium volumes between 2012 and 2016. However, the 2018 economic downturn significantly impacted the trend, although partial recovery was observed post-2020. Notably, government subsidies continued to maintain a stabilizing influence during this period.

Figure 1. (a,b) Changes in Agricultural and Insured Land and Premium Levels Over Time.

The effectiveness and uptake of the agricultural insurance system are strongly tied to government interventions. As shown in Figure 1a, although the total agricultural area in Türkiye has remained relatively stable between 2006 and 2023, the insured area has remained significantly low. This suggests that large portions of agricultural production are not adequately protected against environmental and climatic risks.

Correspondingly, Figure 1b illustrates the temporal evolution of premium volumes. While total and state-supported premium values increased sharply between 2012 and 2016 due to active subsidy policies, a decline occurred during the 2018 financial crisis. Nevertheless, a partial recovery followed after 2020, indicating the stabilizing role of government support.

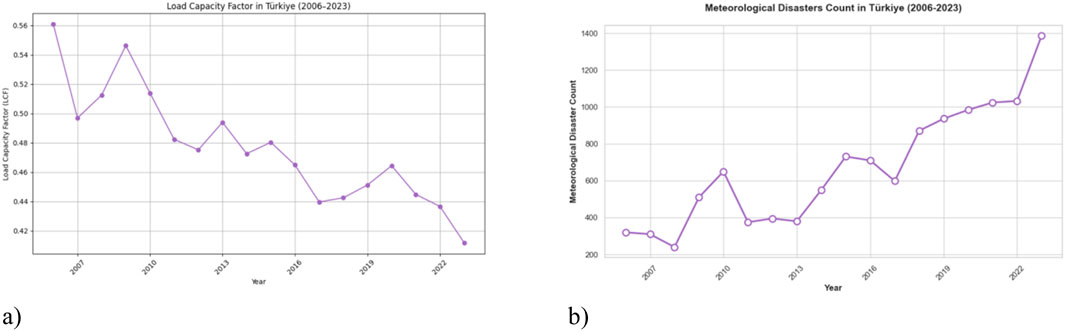

Figures 2a highlights long-term changes in the LCF a proxy for ecological sustainability. LCF declined steadily from 0.36 in 2006 to 0.30 in 2014, spiked to 0.48 in 2016, and then gradually decreased to 0.40 by 2022. Despite temporary improvements, the overall decreasing trend signals weaknesses in environmental sustainability and the need for integrating ecological indicators into risk modeling for agriculture.

Figure 2. (a,b) LCF and Meteorological Disaster Trends.

Moreover, Figures 2b presents the annual number of meteorological disasters in Türkiye, showing a marked increase since 2012, with record highs observed between 2016 and 2020. This rise underscores the intensifying impacts of climate change and the increasing urgency for adaptive insurance models.

When compared to global practices, Türkiye’s agricultural insurance model shows both strengths and areas for development. Countries like the United States and Spain have long-established systems where coverage rates exceed 70% of arable land and include advanced risk modeling approaches that integrate satellite data, climate scenarios, and yield indices (Mahul and Stutley, 2010). Türkiye’s system, while institutionalized, has yet to fully integrate such predictive environmental variables and faces persistent challenges in expanding coverage to smallholder farmers.

Moreover, the increasing frequency and severity of climate-related events call for a paradigm shift in Türkiye’s insurance modeling. The inclusion of environmental variables such as temperature anomalies, precipitation variability, and LCF into actuarial models and insurance pricing strategies is imperative. Recent studies emphasize that climate-adaptive insurance policies, particularly index-based products, can significantly improve resilience in rural economies (Hazell et al., 2017; Carter et al., 2017).

Türkiye’s agricultural insurance system has made significant progress over the past 2 decades, driven largely by institutional reforms and public subsidies. However, the system still faces structural limitations in terms of coverage rates, regional disparities, and the integration of environmental risks into pricing and design mechanisms. In particular, the increasing frequency and severity of meteorological events call for a paradigm shift in risk assessment and insurance planning.

In light of global climate change and Türkiye’s specific environmental vulnerabilities, enhancing insurance penetration, targeting smallholder farmers, and embedding climate-adaptive mechanisms in TARSİM policies are crucial for achieving long-term agricultural sustainability.

4 Methodology

Structural Equation Modeling (SEM) is a widely used multivariate statistical approach that enables the simultaneous estimation of both measurement models, which link latent constructs to their observable indicators, and structural models, which define relationships among latent constructs (Hair et al., 2019).

There are two primary SEM approaches: covariance-based SEM (CB-SEM) and variance-based SEM, commonly referred to as PLS-SEM. This study adopts PLS-SEM due to several advantages: it does not require multivariate normality assumptions, it handles complex models with a limited sample size, and it emphasizes prediction and theory development rather than confirmation. Moreover, PLS-SEM accommodates both reflective and formative measurement models and performs well even when the theoretical foundation is not yet fully established (Hair et al., 2011; Henseler et al., 2015).

Mathematically, in reflective measurement models, each observed indicator is modeled as:

where

where

Here,

Before proceeding with the estimation of the structural model, diagnostic tests for multicollinearity were conducted using the Variance Inflation Factor (VIF). VIF values exceeding 10 are generally indicative of problematic multicollinearity, which may inflate standard errors and bias parameter estimates (Hair et al., 2019; O'Brien, 2007). The presence of high collinearity among predictors serves as an important justification for the application of PLS-SEM, which is recognized for its robustness under such conditions (Ringle et al., 2015; Hair et al., 2021).

Model evaluation in PLS-SEM is conducted in two primary stages: the assessment of the measurement model and the assessment of the structural model. In the measurement model, internal consistency reliability is assessed through Composite Reliability (CR), with acceptable values typically above 0.70. Convergent validity is evaluated via the Average Variance Extracted (AVE), which should exceed the 0.50 threshold to indicate that a construct explains more than half of the variance in its indicators (Fornell and Larcker, 1981). Discriminant validity is established using the Fornell–Larcker criterion and the Heterotrait-Monotrait ratio (HTMT), with HTMT values below 0.85 suggesting sufficient distinction between constructs (Henseler et al., 2015).

For the structural model, the significance of path coefficients is examined through non-parametric bootstrapping procedures, typically employing 5,000 resamples. The model’s explanatory power is evaluated using R2 values, where higher values indicate stronger predictive accuracy. Effect size (f2) is also computed to assess the relative impact of each exogenous construct. Additionally, predictive relevance (Q2) is calculated using the blindfolding technique, and out-of-sample predictive performance can be validated through the PLS Predict procedure (Shmueli et al., 2019). Collinearity among constructs in the inner model is re-checked via inner VIF values, ensuring they remain within acceptable limits (typically <5) to preserve the interpretability of the structural paths (Hair et al., 2019).

This methodological approach ensures a rigorous assessment of both measurement quality and theoretical relationships, while simultaneously addressing key statistical concerns such as multicollinearity and measurement validity. By leveraging the strengths of PLS-SEM, this study provides a robust framework for examining complex structural relationships within the proposed conceptual model.

5 Data and finding

This study examines the determinants of agricultural insurance demand in Turkey using an annual national-level dataset for the period 2006–2023. By combining economic, insurance, and climatic indicators, the dataset aims to analyze agricultural insurance dynamics at the macro level. The study is not spatially subdivided but is conducted solely across Turkey. This approach allows for assessments at the national policy level and aligns with the study’s objectives.

The variables used in the study are defined in Table 1. The dependent variable is the number of agricultural insurance policies issued annually. Independent variables are represented by indicators such as government-supported premium production, insurance amount, agricultural GDP, agricultural area, insured area, total premium production, number of meteorological disasters, and load capacity factor (LCF). Data for the variables were obtained from institutional and reliable sources such as the Turkish Statistical Institute (TÜİK), the Agricultural Insurance Pool (TARSİM), the General Directorate of Meteorology, and the Global Footprint Network.

Table 1. Description of variables and data sources.

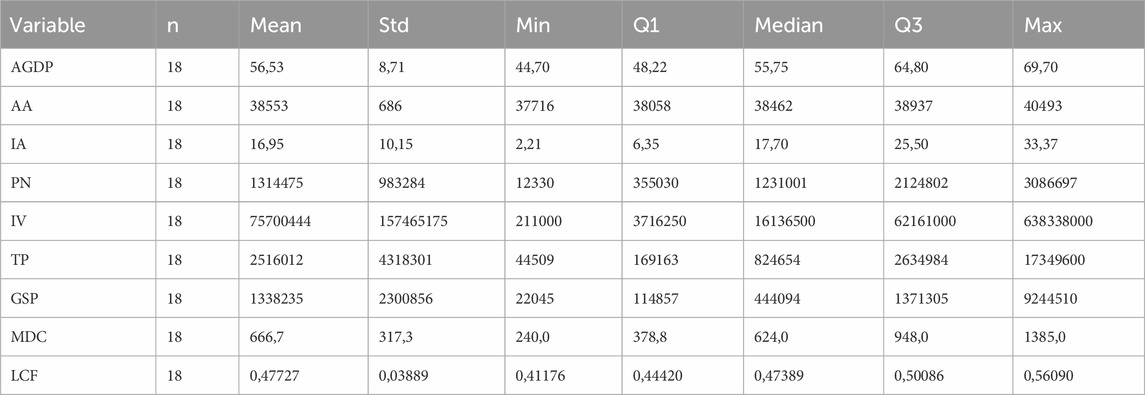

The inclusion of LCF and MDC reflects a broader effort to embed environmental performance and climate extremes into the modeling of economic behavior. In this context, agriculture is not merely treated as an economic activity, but also as a system highly sensitive to ecological limits and meteorological volatility. By examining the interlinkages between these domains, the analysis aims to offer insights that are both policy-relevant and theoretically grounded. A descriptive summary of the dataset is provided in Table 2.

Table 2. Descriptive statistics.

Descriptive statistics presented in the Table 2 provide an overview of the central tendency and dispersion characteristics of the key variables used in the study. The results indicate considerable variation across all variables, suggesting heterogeneity in agricultural economic indicators, insurance dynamics, and ecological conditions over the observed period. Such diversity highlights the importance of capturing both economic and environmental dimensions when analyzing the determinants of agricultural insurance demand.

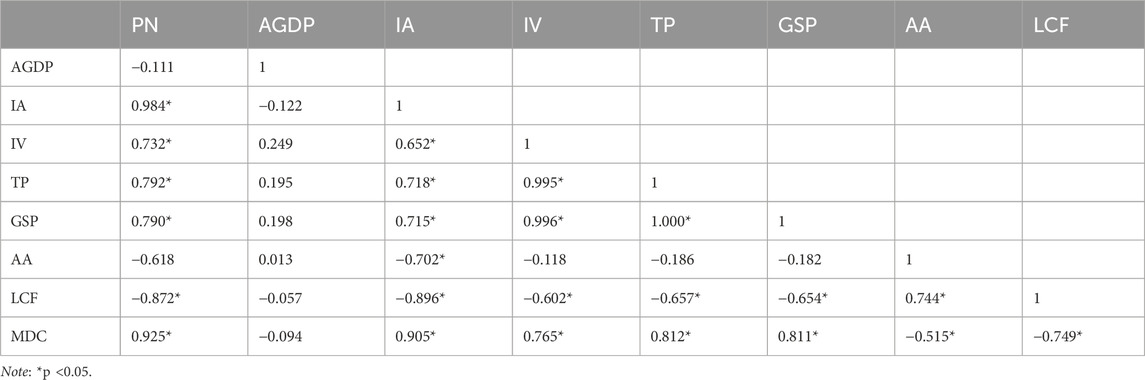

Correlation analysis, presented in Table 3, reveals strong and statistically significant relationships between the number of issued policies and several independent variables. For instance, insured area (r = 0.984), total premium income (r = 0.792), and the number of meteorological disasters (r = 0.925) exhibit strong positive correlations with policy numbers. Conversely, the LCF shows a strong negative association (r = −0.872), suggesting that ecological degradation is associated with increased insurance uptake. This supports the theoretical expectation that heightened environmental stress leads to greater risk awareness and thus higher insurance demand.

Table 3. Pearson correlation matrix showing the relationships among all observed variables.

Methodologically, the study employs both Multiple Regression Analysis and PLS-SEM. While regression analysis enables the identification of statistically significant direct relationships, PLS-SEM is used to explore latent constructs and multidimensional pathways influencing insurance demand. This dual approach enhances the explanatory depth of the study and aligns with the interdisciplinary ethos of sustainability research.

The use of PLS-SEM is particularly valuable for integrating diverse variables ranging from financial incentives to ecological degradation into a coherent analytical framework. Moreover, PLS-SEM accommodates the relatively small sample size (annual data over 18 years) and is well-suited for theory-building in complex, multi-factor systems. This methodological strategy supports a more nuanced understanding of how environmental stressors and institutional mechanisms jointly affect risk perception and adaptive financial behavior in agriculture.

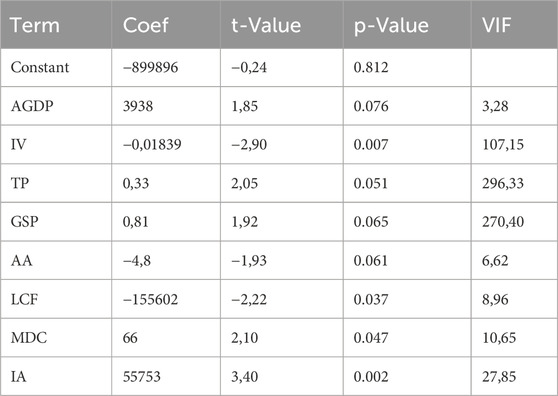

In the multiple regression model (Table 4), the overall model is statistically significant (F (8,9) = 185.60, p < 0.001), with a high explanatory power (R2 = 98.86%). Among the predictors, insured area (IA, β = 55.753, p = 0.002), insured value (IV, β = −0.018, p = 0.007), and meteorological disaster count (MDC, β = 66, p = 0.047) emerged as statistically significant. However, the model suffered from severe multicollinearity, with VIF values exceeding the commonly accepted threshold of 10 (Hair et al., 2019; O'Brien, 2007). Notably, VIF scores for total premium income (TP = 296.33), government subsidized premium (GSP = 270.40), and insured value (IV = 107.15) indicate a problematic degree of collinearity, which can distort coefficient estimates and reduce the reliability of inferential statistics.

Table 4. Regression coefficients.

Due to the presence of multicollinearity, the analysis proceeded with PLS-SEM, a variance-based SEM approach suitable for small to medium-sized datasets and highly collinear data (Hair et al., 2021; Ringle et al., 2015). In the structural model, variables were grouped into three latent constructs: Insurance Economy (IV, TP, GSP), Agricultural Economy (AGDP, AA, IA), and Ecological and Meteorological Risks (LCF, MDC). The PLS-SEM analysis was conducted using SmartPLS 4.0 software, allowing for robust estimations even under conditions of multicollinearity.

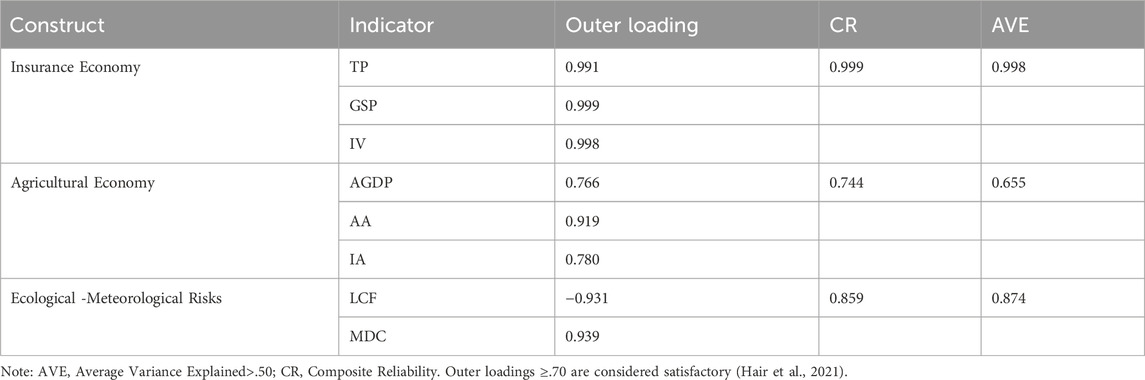

The measurement model demonstrates robust validity and reliability across all constructs. As presented in Table 5.

Table 5. Measurement model assessment.

All outer loadings exceed the 0.70 threshold (Hair et al., 2021), confirming that ≥49% of each indicator’s variance is explained by its latent construct. Notably, Insurance Economy indicators show near-perfect loadings (0.991–0.999), suggesting exceptional item representation.

CR values (0.744–0.999) surpass the 0.70 benchmark, indicating high construct reliability (Fornell and Larcker, 1981). The Insurance Economy construct achieves CR = 0.999, reflecting minimal measurement error.

All AVE values exceed 0.50 (range: 0.655–0.998), verifying that latent constructs explain >50% of their indicators’ variance. The Ecological-Meteorological Risks construct shows particularly strong convergent validity (AVE = 0.874).

These results satisfy all PLS-SEM criteria for measurement model adequacy, as per contemporary standards in agricultural economics research (Henseler et al., 2015; Sarstedt et al., 2016). The high AVE/CR values for Insurance Economy variables may reflect Turkey’s standardized premium calculation system, while slightly lower Agricultural Economy loadings (0.766–0.919) could indicate regional heterogeneity in reporting practices (TARSİM, 2025).

As presented in Table 6, the HTMT ratios demonstrate strong discriminant validity, with all values significantly below the 0.85 threshold (Insurance Economy-Agricultural Economy: 0.612; Insurance Economy-Ecological-Meteorological Risks: 0.558; Agricultural Economy-Ecological-Meteorological Risks: 0.631), satisfying Henseler et al.'s (2015) criterion.

Table 6. HTMT ratios between latent constructs indicating discriminant validity.

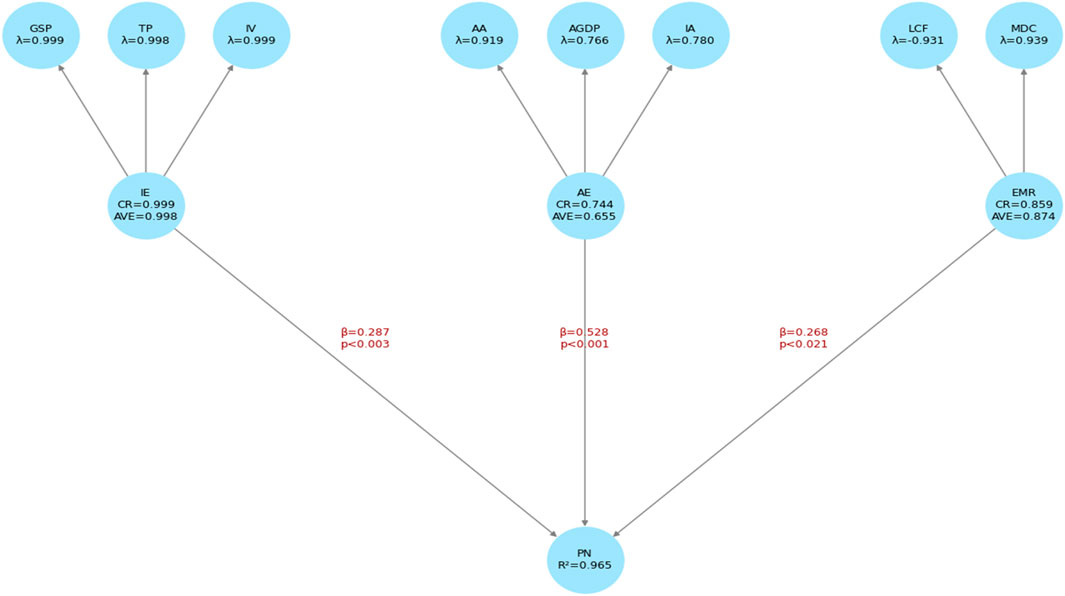

The results of the structural model evaluation, as summarized in Table 7 and visualized in Figure 3, indicate statistically significant relationships between all latent constructs and agricultural insurance policy numbers (PN). The Agricultural Economy construct demonstrated the strongest positive effect on PN (β = 0.528, t = 4.876, p = 0.001), highlighting the influence of sector-specific variables such as agricultural GDP, total cultivated area, and insured area. This finding is consistent with the view that insurance uptake is closely tied to the scale and productivity of agricultural activity (Hazell, 2001; Mahul and Stutley, 2010).

Table 7. PLS-SEM Structural Model Results: Path Coefficients, t-values, and Significance.

Figure 3. PLS-SEM structural model diagram.

Similarly, Insurance Economy comprising government-supported premium subsidies, insured values, and total premium income was positively associated with policy numbers (β = 0.287, t = 2.942, p = 0.003). This result supports previous findings that financial incentives and support mechanisms significantly influence farmers’ willingness to insure (Glauber, 2013; Goodwin and Smith, 2013).

In addition, Ecological and Meteorological Risks also had a statistically significant impact (β = 0.268, t = 2.315, p = 0.021), suggesting that both climatic stress (as measured by LCF) and disaster frequency increase risk perception, thus stimulating insurance participation (Jin et al., 2016; Surminski and Oramas-Dorta, 2014).

Overall, the model demonstrated excellent explanatory power with an R2 of 0.965, far exceeding the threshold of 0.10 recommended by Falk and Miller (1992), and confirming the model’s robustness. As illustrated in Figure 3, the final PLS-SEM model captures both the economic and environmental determinants of agricultural insurance uptake in an integrated framework.

6 Integration of SEM-Derived latent scores into actuarial index-based premium calculations

In this section, the integration of latent variable scores derived through PLS-SEM into actuarial computations is discussed. Particularly in the context of agricultural insurance, the assessment of risk and the determination of corresponding premium rates should not be constrained to deterministic methods based solely on historical loss data. Instead, there is a growing need for holistic, data-driven approaches that account for the complex interdependencies among environmental, economic, and climatic factors. Within this framework, latent variable scores extracted from the PLS-SEM model can be incorporated into traditional actuarial methods, allowing for the development of a more dynamic and predictive risk assessment structure.

The PLS-SEM approach reveals the underlying latent constructs by modeling the complex relationships among observed variables (Hair et al., 2019). In this study, latent structures are modeled around three thematic dimensions: climatic factors, economic indicators and ecological risk variables. The latent scores associated with each construct serve as quantitative proxies for the underlying determinants of insurance demand. These scores can be transformed into index values for each year and region, capturing localized risk levels and enabling more equitable and risk-sensitive premium calculations.

For example, let

where

Based on the calculated index, the actuarial premium rate can be defined dynamically using a parametric expression such as:

where

This methodological approach offers a significant innovation in the actuarial modeling of agricultural insurance, particularly as the impacts of climate change become increasingly pronounced. The integration of multidimensional structural models into insurance pricing has been widely advocated in recent literature as a necessary step toward building adaptive and resilient insurance systems (Zeng et al., 2025; Mahul and Stutley, 2010). This study, therefore, not only offers an empirical example of such integration but also demonstrates the direct applicability of SEM-based results in insurance mathematics and premium estimation.

In conclusion, the use of latent variable scores derived from PLS-SEM as indices in actuarial applications represents a valuable methodological advancement for both academic and professional contexts. This hybrid modeling approach may serve as a foundational step toward developing future-oriented premium systems that simultaneously consider climatic risk profiles and economic indicators in a unified framework.

7 Conclusion and policy implications

This study presents a comprehensive macro-level analysis of the determinants influencing agricultural insurance demand in Türkiye from 2006 to 2023. By integrating Multiple Regression Analysis and PLS-SEM, the research introduces a three-dimensional latent structure (Agricultural Economy, Insurance Economy and Ecological-Meteorological Risks) to explain the factors driving insurance policy uptake. This hybrid methodological approach not only enhances model robustness under multicollinearity but also offers valuable empirical insights for the design of sustainable insurance systems in the face of growing climate variability.

The most significant determinant identified was the Agricultural Economy construct (β = 0.528, p < 0.01), underscoring the central role of production dynamics in shaping insurance behavior. Specifically, the insured area exhibited the strongest correlation with the number of policies issued (r = 0.984, p < 0.05), reflecting the increased risk awareness and coverage needs of large-scale producers. This finding is consistent with previous literature, which highlights farm size and market integration as crucial predictors of insurance adoption (Hazell, 2001; Mahul and Stutley, 2010; Jin et al., 2016). Moreover, the positive interaction between insured areas and climatic uncertainty reaffirms the importance of scale in navigating ecological risk exposure (Azahra et al., 2024).

The second major construct, Insurance Economy, had a moderate but significant effect (β = 0.287, p = 0.003). Variables such as premium subsidies, total insured value, and policyholder contributions proved influential in incentivizing uptake. These results validate earlier studies that emphasize the catalytic role of financial incentives (Iturrioz, 2009; Glauber, 2013), especially in middle-income economies. However, the presence of diminishing marginal returns under increasing ecological stress conditions, as revealed in our model, signals the need for a more differentiated subsidy regime an argument echoed in recent critiques of flat-rate systems (Chen and Zhao, 2024; OECD, 2023).

Perhaps most critically, Ecological-Meteorological Risks were shown to exert a statistically significant influence (β = 0.268, p = 0.021) on insurance demand. The inclusion of the LCF and Meteorological Disaster Count as observable variables adds a crucial ecological dimension to our framework. The strong negative correlation between LCF and insurance demand (r = −0.872) suggests that as ecological resilience deteriorates, farmers increasingly seek financial instruments as buffers. This finding aligns with prior studies that highlight the behavioral impact of environmental volatility on insurance participation (Surminski and Oramas-Dorta, 2014; Hu et al., 2024). The result also supports arguments for embedding environmental stress indicators into actuarial models to better capture climate-induced risk salience.

Methodologically, the application of PLS-SEM enabled the consolidation of highly correlated variables into latent constructs, resulting in a model with high explanatory power (R2 = 0.965). This exceeds the explanatory benchmarks observed in comparable SEM applications (Hair et al., 2021; Sarstedt et al., 2016) and demonstrates the utility of integrating macroeconomic and ecological metrics within a unified insurance modeling framework. Compared to traditional regression models (e.g., Giné et al., 2008), our approach offers deeper insight into the interdependencies between environmental degradation, policy incentives, and behavioral responses.

Given the layered nature of the findings, several policy recommendations emerge. First, the current uniform subsidy structure should be replaced with tiered and geographically differentiated subsidy schemes that incorporate ecological vulnerability and farm scale. A “one-size-fits-all” subsidy design, while administratively convenient, risks inefficiency and maladaptation, particularly under heightened environmental stress (OECD, 2023).

Second, real time ecological indicators such as LCF and MDC should be integrated into insurance product design and pricing models. The demonstrated impact of environmental factors on insurance behavior suggests that ecological stress must be treated not as an exogenous background variable but as a primary design input. As shown by Iwahashi et al. (2022), the use of remote sensing and UAV-based technologies can significantly improve the ecological responsiveness and actuarial soundness of insurance systems.

Third, behavioral interventions and financial literacy programs must complement financial mechanisms. As noted by Giné et al. (2008), structural barriers such as low risk awareness and mistrust in insurance systems persist, especially among smallholder farmers. Awareness campaigns, localized training programs, and digital access tools should be implemented to bridge this informational gap.

Fourth, technological innovation in index-based insurance offers a promising frontier. Our findings support the transition from static financial instruments to climate-responsive, technology-driven platforms. The incorporation of IoT sensors and blockchain for real-time data validation, as proposed by Makkithaya and VG (2024) and Dalhaus and Finger (2023), could foster transparency and adaptability in index insurance models especially in regions prone to rapidly evolving climate risks.

While this study delivers valuable insights at the national level, future research should explore spatial and household-level disaggregation to address heterogeneity in risk perception, adaptation capacity, and institutional trust. Combining the macro-latent structure identified here with micro-analytic frameworks such as the Insurance–Environment–Productivity model (Kurdyś-Kujawska et al., 2021) could yield more granular insights for targeting and evaluating insurance interventions.

By demonstrating the joint influence of economic structure, insurance systems and ecological stress on agricultural insurance demand, this study bridges critical gaps in the literature on climate resilience and risk finance. The integration of ecological metrics into structural equation modeling constitutes a novel contribution with practical implications for emerging economies navigating the dual pressures of agricultural transformation and climate disruption. In challenging the dominance of subsidy-centric paradigms, our findings advocate for a holistic, sustainability aligned insurance strategy one that is adaptable, ecologically informed, and behaviorally sensitive.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Author contributions

SY: Writing – original draft, Writing – review and editing.

Funding

The author(s) declare that no financial support was received for the research and/or publication of this article.

Conflict of interest

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Generative AI statement

The author(s) declare that Generative AI was used in the creation of this manuscript. During the preparation of this manuscript, the author used ChatGPT (OpenAI, version 4) solely for language editing and trial versions of Minitab and SmartPLS for data analysis; all outputs were manually verified and the author assumes full responsibility for the research.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Azahra, A. S., and Johansyah, M. D.Sukono (2024). Agricultural insurance premium determination model for risk mitigation based on rainfall index: systematic literature review. Risks 12 (12), 205. doi:10.3390/risks12120205

Boháčiková, A., Serenčéš, P., and Tóth, M. (2017). “Farmers' risk perception and risk management strategies in Slovak agriculture,” in Managerial trends in the development of enterprises in globalization era, 26.

Borucke, M., Moore, D., Cranston, G., Gracey, K., Iha, K., Larson, J., et al. (2013). Accounting for demand and supply of the biosphere's regenerative capacity: the national footprint accounts’ underlying methodology and framework. Ecol. Indic. 24 (*24*), 518–533. doi:10.1016/j.ecolind.2012.08.005

Burhan, H. A. (2023). Agricultural insurance and natural disasters: an assessment of the financial performance of the Turkish agricultural insurance pool (TARSIM) through selected criteria. Ardahan Üniversitesi İktisadi ve İdari Bilim. Fakültesi Derg. 5 (5*), 126–136. doi:10.58588/aru-jfeas.1393228

Carter, M., de Janvry, A., Sadoulet, E., and Sarris, A. (2017). Index insurance for developing country agriculture: a reassessment. Annu. Rev. Resour. Econ. 9 (9), 421–438. doi:10.1146/annurev-resource-100516-053352

Chai, Z., and Zhang, X. (2024). The impact of agricultural insurance on planting structure adjustment—an empirical study from Inner Mongolia autonomous region, China. Agriculture 14 (1), 41. doi:10.3390/agriculture14010041

Chen, X. L., and Zhao, Y. F. (2024). Study on the impact of climate risk on the agricultural insurance purchasing behavior of herding Households—An empirical analysis based on Inner Mongolia. Front. Sustain. Food Syst. 8, 1365536. doi:10.3389/fsufs.2024.1365536

Chin, W. W. (1998). “The partial least squares approach to structural equation modeling,” in Modern methods for business research. Editor G. A. Marcoulides (Mahwah, NJ, USA: Lawrence Erlbaum Associates), 295–336.

Coble, K. H., and Knight, T. O. (2002). “Crop insurance as a tool for price and yield risk management,” in A comprehensive assessment of the role of risk in U.S. agriculture. Editors R. E. Just,, and R. D. Pope (New York, NY, USA: Springer), 445–494.

Dalhaus, T., and Finger, R. (2023). Blockchain for agricultural insurance: evidence from smart contracts. Agric. Econ. (1), 1–15. doi:10.1111/agec.12772

Falk, R. F., and Miller, N. B. (1992). A primer for soft modeling. Akron, OH, USA: University of Akron Press.

Falsafian, A., Ghahremanzadeh, M., Aref Eshghi, T., Rasooli Sharabiani, V., Szymanek, M., and Dziwulska-Hunek, A. (2024). Producer welfare benefits of rating area yield crop insurance. Agriculture 14 (9), 1512. doi:10.3390/agriculture14091512

Fornell, C., and Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 18*, 39–50. doi:10.1177/002224378101800104

Galli, A., Wackernagel, M., Iha, K., and Lazarus, E. (2014). Ecological footprint: implications for biodiversity. Biol. Conserv. 173*, 121–132. doi:10.1016/j.biocon.2013.10.019

Giné, X., Townsend, R., and Vickery, J. (2008). Patterns of rainfall insurance participation in rural India. World Bank Econ. Rev. 22, 539–566. doi:10.1093/wber/lhn015

Glauber, J. W. (2013). The growth of the federal crop insurance program, 1990-2011. Am. J. Agric. Econ. 95 (95*), 482–488. doi:10.1093/ajae/aas091

Global Footprint Network (2025). National footprint accounts. Oakland, CA, USA: Ecological Footprint; Global Footprint Network. Available online at: https://data.footprintnetwork.org (Accessed on July 5, 2025).

Goodwin, B. K., and Smith, V. H. (2013). What harm is done by subsidizing crop insurance? Am. J. Agric. Econ. 95*, 489–497. doi:10.1093/ajae/aas092

Hair, J. F., Ringle, C. M., and Sarstedt, M. (2011). PLS-SEM: indeed a silver bullet. J. Mark. Theory Pract. 19 (*), 139–152. doi:10.2753/MTP1069-6679190202

Hair, J. F., Risher, J. J., Sarstedt, M., and Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. Eur. Bus. Rev. 31*, 2–24. doi:10.1108/EBR-11-2018-0203

Hair, J. F., Astrachan, C. B., Moisescu, O. I., Radomir, L., Sarstedt, M., Vaithilingam, S., et al. (2021). Executing and interpreting applications of PLS-SEM: updates for family business researchers. J. Fam. Bus. Strategy 12 (12*), 100392. doi:10.1016/j.jfbs.2020.100392

Hayran, S. (2023). Farmers' flood risk perception in Turkey: the case of Mersin province. Emir. J. Food Agric. (*35*), 481–487. doi:10.9755/ejfa.2023.v35.i5.3101

Hazell, P. (2001). Potential role for insurance in managing catastrophic risk in developing countries. Washington, DC, USA: International Food Policy Research Institute.

Hazell, P., Sberro-Kessler, R., and Varangis, P. (2017). When and how should agricultural insurance be subsidized? Issues and good practices. Washington, DC, USA: World Bank.

Henseler, J., Ringle, C. M., and Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 43, 115–135. doi:10.1007/s11747-014-0403-8

Hu, M., Yi, F., Zhou, H., and Yan, F. (2024). The more the better? Reconsidering the welfare effect of crop insurance premium subsidy. Agriculture 14 (11), 2050. doi:10.3390/agriculture14112050

IPCC (2021). Climate change 2021: the physical science basis. Cambridge, UK: Cambridge University Press. doi:10.1017/9781009157896

Iturrioz, R. (2009). Agricultural insurance: primer series on insurance, 12. Washington, DC, USA: World Bank.

Iwahashi, Y., Sigit, G., Utoyo, B., Lubis, I., Junaedi, A., Trisasongko, B. H., et al. (2022). Drought damage assessment for crop insurance based on vegetation index by unmanned aerial vehicle (UAV) multispectral images of paddy fields in Indonesia. Agriculture 13 (1), 113. doi:10.3390/agriculture13010113

Jin, J., Wang, W., and Wang, X. (2016). Farmers' risk preferences and agricultural weather index insurance uptake in rural China. Int. J. Disaster Risk Sci. 7*, 366–373. doi:10.1007/s13753-016-0108-3

Kurdyś-Kujawska, A., Sompolska-Rzechuła, A., Pawłowska-Tyszko, J., and Soliwoda, M. (2021). Crop insurance, land productivity and the environment: a way forward to a better understanding. Agriculture 11 (11), 1108. doi:10.3390/agriculture11111108

Mahul, O., and Stutley, C. J. (2010). Government support to agricultural insurance: challenges and options for developing countries. Washington, DC, USA: World Bank Publications.

Makkithaya, K., and Vg, N. (2024). Blockchain oracles for decentralized agricultural insurance using trusted IoT data. Front. Blockchain 7, 1481339. doi:10.3389/fbloc.2024.1481339

Manescu, A. C., Barna, F. M., Regep, H. D., Manescu, C. M., and Cerba, C. (2025). The impact of extreme weather events on agricultural insurance in Europe. Agriculture 15 (9), 995. doi:10.3390/agriculture15090995

Mayers, D., and Smith, C. W. (1990). On the corporate demand for insurance: evidence from the reinsurance market. J. Bus., 19–40. Avaialble online at: https://www.jstor.org/stable/2353235.

O'Brien, R. M. (2007). A caution regarding rules of thumb for variance inflation factors. Qual. and Quantity 41*, 673–690. doi:10.1007/s11135-006-9018-6

Özgür, R. Ö. (2019). Türkiye’de tarim sektörü sigorta sistemi: problemler ve çözüm önerileri. Muhasebe ve Finans. İncelemeleri Derg. 2 (2*), 104–117. doi:10.32951/mufider.594826

Powers, M. R., and Shubik, M. (2006). A “square-root rule” for reinsurance. Revista Contabilidade and Finanças 17*, 101–107. doi:10.1590/s1519-70772006000500008

Ringle, C. M., Wende, S., and Becker, J. M. (2015). SmartPLS 3. Boenningstedt, Germany: SmartPLS GmbH. Available online at: http://www.smartpls.com (Accessed on July 1, 2025).

Rusteika, M., and Skinulienė, L. (2023). Expectations of the participants of the crop insurance system and their implementation. Agriculture 13 (3), 649. doi:10.3390/agriculture13030649

Sarstedt, M., Hair, J. F., Ringle, C. M., Thiele, K. O., and Gudergan, S. P. (2016). Estimation issues with PLS and CBSEM: where the bias lies. J. Bus. Res. 69, 3998–4010. doi:10.1016/j.jbusres.2016.06.007

Seamon, E., Gessler, P. E., Abatzoglou, J. T., Mote, P. W., and Lee, S. S. (2023). Climatic damage cause variations of agricultural insurance loss for the Pacific northwest region of the United States. Agriculture 13 (12), 2214. doi:10.3390/agriculture13122214

Shmueli, G., Sarstedt, M., Hair, J. F., Cheah, J. H., Ting, H., Vaithilingam, S., et al. (2019). Predictive model assessment in PLS-SEM: guidelines for using PLSpredict. Eur. J. Mark. 53*, 2322–2347. doi:10.1108/EJM-02-2019-0189

Surminski, S., and Oramas-Dorta, D. (2014). Flood insurance schemes and climate adaptation in developing countries. Int. J. Disaster Risk Reduct. 7 (7*), 154–164. doi:10.1016/j.ijdrr.2013.10.005

TARSİM (2023). Agricultural insurance pool activity reports 2006-2022*; TARSİM: ankara, Turkey. Available online at: https://www.tarsim.gov.tr (Accessed on March 5, 2025).

TARSİM (2025). Agricultural insurance pool reports. TARSİM Ank. Turk. Available online at: https://www.tarsim.gov.tr (Accessed on March 5, 2025).

Türkeş, M., Turp, M. T., An, N., Ozturk, T., and Kurnaz, M. L. (2020). “Impacts of climate change on precipitation climatology and variability in Turkey,” in Water resources of Turkey (Cham, Switzerland: Springer), 467–491.

Turkish State Meteorological Service (2025). Climate data portal; MGM: ankara, Turkey. Available online at: https://www.mgm.gov.tr (Accessed on March 1, 2025).

Turkish Statistical Institute Database (2025). TUİK: ankara, Turkey. Available online at: https://www.tuik.gov.tr (Accessed on March 10, 2025).

Zeng, X., Lu, H., Qi, H., and Ji, L. (2025). Does extreme weather affect the resilience of agricultural economies? Analysis based on agricultural insurance. Front. Environ. Sci. 13, 1551030. doi:10.3389/fenvs.2025.1551030

Zhang, J. (2024). Assessing climate change impacts and associated risks: applications in finance and insurance. Uwaterloo. Ca. Available online at: https://hdl.handle.net/10012/21256.

Keywords: agricultural insurance, crop insurance demand, climate risk, PLS-SEM, ecological sustainability, load capacity factor, meteorological disasters, actuarial models

Citation: Yörübulut S (2025) Determinants of crop insurance demand in Türkiye: a PLS-SEM analysis integrating economic and ecological factors. Front. Environ. Sci. 13:1651603. doi: 10.3389/fenvs.2025.1651603

Received: 22 June 2025; Accepted: 30 July 2025;

Published: 15 August 2025.

Edited by:

Justice Gameli Djokoto, Dominion University College, GhanaReviewed by:

Wentai Bi, Bohai University, ChinaAnzhi Liu, Heilongjiang Bayi Agricultural University, China

Marcos Roberto Benso, University of São Paulo, Brazil

Copyright © 2025 Yörübulut. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Serap Yörübulut, c2l5YnVsdXRAZ21haWwuY29t

†ORCID: Serap Yörübulut, orcid.org/0000-0003-0781-4405