Yanzhen Li

Yanzhen Li Huixia Liu

Huixia Liu Zixun Guo1

Zixun Guo1- 1School of Economics and Management, Northwest University, Xi’an, Shaanxi, China

- 2School of Accounting and Finance, Xi’an Eurasia University, Xi’an, Shaanxi, China

Introduction: Banking liberalisation helps introduce international capital and environmental, social and governance (ESG) concepts and practices. Clarifying how this institutional policy promotes corporate ESG performance is crucial to sustainable development in emerging economies.

Methods: Based on the exogenous policy shock of China’s removal of foreign ownership restrictions in the banking sector, the impact of banking liberalisation on corporate ESG performance is empirically tested using a generalised difference-in-differences (DID) model.

Results: The findings reveal that corporate ESG performance significantly improved after foreign ownership restrictions were removed in the banking sector. This conclusion holds after endogeneity and robustness tests. Mechanism analysis indicates that banking liberalisation enhances corporate ESG performance by improving ESG information disclosure, alleviating financing constraints, and curbing managerial myopia. Heterogeneity analysis shows that this effect is particularly pronounced in heavily polluting industries and firms with high loan dependency. Further analysis demonstrates that public environmental concerns positively moderate the benefits of liberalisation. The ESG-enhancing effect of liberalisation is stronger when firms face greater environmental scrutiny. The ESG improvement resulting from banking sector liberalisation exhibits regional spillover effects, with neighbouring firms simultaneously improving their ESG performance.

Conclusion: This study enriches research on the micro-level effects of financial liberalisation and provides important policy implications for emerging economies seeking to enhance corporate ESG performance.

1 Introduction

Climate change is a severe threat to humanity, requiring accelerated low-carbon transition and sustainable development. As engines of global economic growth and primary sources of carbon emissions, emerging market economies are pivotal in this transition (Onifade and Alola, 2022). Enterprises comprise the core of economic activity, and their environmental, social, and governance (ESG) performance determines an economy’s resource efficiency and pollution-control levels. Thus, corporate ESG performance is critical in low-carbon transitions (Eccles et al., 2014). However, corporate ESG practices, including environmental technology upgrades and employee welfare improvements, often involve high costs, long investment cycles, and significant uncertainty (Edmans, 2011; Lins et al., 2017). Efficient financial support provides a crucial guarantee companies will implement ESG principles (Schiederig et al., 2012). Therefore, financial system reform to diversify funding sources for corporate ESG practices is a core challenge for promoting sustainable development in emerging market economies.

Several emerging market economies have promoted financial liberalisation to attract international capital, drive financial system reforms, and enhance overall efficiency (Gourinchas and Jeanne, 2006; Kose et al., 2009). However, can financial liberalisation, particularly banking liberalisation as the cornerstone of some emerging economies’ financial systems, promote corporate ESG performance? If so, through what mechanisms? China, the world’s largest emerging economy, operates a banking-dominated financial system. Removing foreign ownership limits in banking in 2018 is among China’s most substantive recent financial liberalisation measures. This policy is relatively exogenous to individual corporate decisions, providing a quasi-natural experiment to identify banking liberalisation’s causal effects on corporate ESG practices. Consequently, examining how China’s banking liberalisation affects corporate ESG performance offers insights into how financial openness advances sustainable development in emerging markets.

Theoretically, banking liberalisation may improve corporate ESG performance. First, banking sector deregulation supplements domestic credit supply, alleviating corporate financing constraints (Hombert and Matray, 2017; Sheng and Wang, 2021). This influences corporate ESG practices and other behavioural decisions. Second, most of the international capital brought about by banking sector liberalisation comes from developed countries such as Europe and the United States, which have a better understanding and implementation of ESG investment concepts than emerging market countries (Gao et al., 2021) and more strongly prefer firms with high ESG performance (Wang et al., 2023; Yin et al., 2023; Wu and Liu, 2024). According to catering theory, firms will actively improve their ESG performance in order to attract investment from international investors. Third, banking liberalisation introduces foreign ESG expertise and management practices into domestic credit markets, prompting banks to incorporate ESG factors into credit business decision-making and management, thus encouraging borrowing companies to improve ESG performance such as by setting loan covenants (Galletta et al., 2022; Zhu and Wei, 2023). However, significant corporate ESG costs may divert limited corporate resources. In addition, in the current sluggish economic environment, companies may focus on short-term financial performance and allocate fewer resources to ESG activities, potentially weakening the ESG improvement effects of liberalisation. Thus, whether banking liberalisation ultimately improves corporate ESG performance requires rigorous examination.

Extant banking liberalisation research primarily comprises three strands. One strand focuses on the financial system and finds that it enhances bank competition (Lai et al., 2016) and improves operational efficiency by improving technology, management capabilities (Laeven et al., 2015; Ghosh, 2016), However, liberalisation increases banking crisis risk, with such crises most likely once liberalisation reaches a moderate level (Angkinand et al., 2010). Another strand focuses on the positive effects of banking sector liberalisation on macroeconomic outcomes such as resource allocation efficiency (Li and Zhang, 2021), real-economy employment (Zeng and Wei, 2024). A third strand adopts a micro-level perspective, demonstrating that banking sector openness alleviates financing constraints (Clarke et al., 2006; Giannetti and Ongena, 2012), improves corporate credit access (Gormley, 2010; Lin, 2011), innovation level (Zhu et al., 2020), and performance (Jin et al., 2022). Nevertheless, research on how banking sector liberalisation affects non-financial firm performance, particularly ESG performance, remains scarce. Research on the factors influencing corporate ESG performance has primarily explored institutional factors, such as government environmental regulations (Arminen et al., 2018), religion (Qoyum et al., 2022), market pressures such as investor attention (Khan et al., 2016; Dyck et al., 2010), and corporate characteristics such as CEO attributes (Huang et al., 2023), size (Drempetic et al., 2020), and governance (Mallin et al., 2013). However, although corporate ESG performance is closely tied to overall economic sustainability, how major national-level institutional reforms (e.g., financial openness) affect it has received little attention.

Some studies have begun focusing on how financial liberalisation affects corporate ESG performance. Research indicates that stock market opening and the inclusion of A-shares in the MSCI (Morgan Stanley Capital International Index) Emerging Markets Index improve corporate ESG performance (Yang et al., 2022; Wang et al., 2023; Yin et al., 2023; Song et al., 2024). However, these studies have almost exclusively focused on the effects of capital market opening. In emerging economies such as China, where the banking system dominates, the banking sector is the core financial resource allocation channel and banking liberalisation represents a more fundamental and far-reaching form of financial opening. Therefore, its opening effects exhibit greater systemic impact, exerting a broader and deeper influence on corporate performance. Unlike the opening of capital markets, which primarily influences corporate ESG performance through shareholder, the primary actors in the opening of the banking sector are banks, which serve as core creditors to corporations. This difference in the primary actors results in the opening of the banking sector having a more direct, powerful, and sustained impact on corporate ESG performance. First, by incorporating ESG factors into credit business decision-making and management, banks can impose stricter loan conditions or even refuse loans to companies with poor ESG performance. This financing constraint has an immediate and powerful effect on companies. Second, compared to investors in capital markets, banks can more directly, continuously, and effectively monitor corporate ESG practices and urge improvements through detailed due diligence and post-loan management processes (Houston and Shan, 2022). Unfortunately, despite the significant theoretical importance of banking sector liberalisation, its channels of influence differ fundamentally from those of capital market liberalisation, few studies have examined whether and how banking sector liberalisation promotes improvements in corporate ESG performance. This study addresses this gap by utilising China’s 2018 removal of foreign ownership limits in banking as a quasi-natural experiment to examine how this specific form of financial opening affects corporate ESG performance, providing rigorous causal evidence of how banking liberalisation affects ESG performance in emerging markets.

This study makes several contributions to the literature. First, it expands the research perspective on financial liberalisation’s effects on corporate ESG performance from the capital market to bank sector liberalisation. Utilising the exogenous policy shock of China’s banking sector lifting restrictions on foreign ownership, this study reveals the impact and mechanism of banking liberalisation, a form of financial liberalisation with a broader scope and deeper influence on enterprises, on corporate ESG performance in a banking-dominated economy. This enriches the research on the micro effects of banking liberalisation and provides a new perspective on the antecedents of corporate ESG practices.

Second, this study identifies and empirically tests three channels through which banking liberalisation improves corporate ESG performance: improving ESG disclosure, alleviating financing constraints, and curbing managerial myopia. This mechanism analysis opens the “black box” of how banking liberalisation influences sustainable corporate behaviour, providing a solid micro-foundation for understanding how banking sector liberalisation drives corporate ESG practices. Simultaneously, it offers a new theoretical perspective and empirical evidence for emerging markets seeking to leverage financial liberalisation policies and promote green and low-carbon economic transformations.

Third, this study examines enterprise motivations to improve ESG performance from the market forces perspective while considering institutional factors such as social environmental protection awareness (informal supervision). An analytical framework is established for the dual market and institutional drivers of banking sector liberalisation promoting corporate ESG performance. The findings provide an important supplement to the literature on how financial openness empowers corporate ESG improvements and contribute to a deeper understanding of the motivations and behaviours of emerging market firms engaged in ESG activities.

This paper is organised as follows. Section 2 presents the institutional background and hypotheses based on relevant literature. Section 3 introduces the data sample, empirical model, and variables. Section 4 reports the empirical results and robustness tests. Section 5 examines potential influencing mechanisms and heterogeneity. Section 6 provides further analysis, including moderating effect analysis and spillover effect analysis. Section 7 presents the study’s conclusions, implications and discussion of limitations.

2 Institutional background, theoretical analysis, and research hypotheses

2.1 Institutional background

Banking liberalisation is pivotal for financial market liberalisation, which is progressive relaxation of regulatory constraints on foreign capital participation in institutional market entry and operational scope expansion in a nation’s banking sector. China’s banking sector liberalisation evolved through distinct phases. First, 1979 to 2000 were the early years characterised by cautious exploration. China’s banking openness policies remained prudent. Foreign-funded banks faced stringent market entry restrictions, with their business scope primarily limited to foreign exchange operations. As China’s reform and opening-up deepened, gradual policy adjustments drove a progressive increase in foreign bank branches. However, the overall sector remained in a phase of limited openness, characterised by controlled institutional access and operational constraints.

Second, 2001 to 2007 saw accelerated liberalisation after China’s World Trade Organization (WTO) accession. China joined the WTO in 2001, catalysing substantial banking sector reforms. Complying with WTO commitments, the government progressively eliminated geographic restrictions and operational constraints on foreign banks’ RMB-denominated business activities. This deregulatory shift precipitated a surge in foreign banking, with 312 operational entities by 2006. Foreign-funded banks’ total assets demonstrated sustained growth, peaking at 2.06% of China’s banking sector assets in 2007, marking the zenith of foreign participation under WTO’s transitional framework.

Third, 2008 to 2017 was characterised by post-crisis prudential contraction. The 2008 global financial crisis severely affected developed economies’ financial sectors. In response, the Basel Committee introduced the Basel III Capital Accord in 2010, imposing more stringent capital adequacy, leverage ratios, and liquidity requirements for international banks. In 2013, China’s economy entered a new standard structural adjustment, facilitating a downward trend. Increased risks in the financial sector (e.g., breakage of the capital chain of private financing) led China to implement macroprudential regulation with a penetrative supervision framework in 2015. Under these factors’ combined effects, the pace of the opening up of China’s banking sector slowed. Foreign banks were either unable or unmotivated to continue their expansion, and some closed and downsized their branches in China with a declining trend in market share.

Fourth, from 2018 to the Present has been the “high-standard opening up in the high-quality development era.” Since 2018, China’s banking sector liberalisation has been on the fast track. Several policies encourage foreign institutional investment in China’s banking industry. Key measures include removing foreign ownership limits for commercial banks and financial asset management companies, coupled with expanded business scope authorisation. In August 2018, the China Banking and Insurance Regulatory Commission issued the Decision on the Repeal and Amendment of Certain Regulations, repealing restrictive clauses on foreign ownership ratios from the original Administrative Measures for the Investment and Equity Participation of Foreign Financial Institutions in Chinese Financial Institutions. This explicitly abolished restrictions limiting a single foreign investor’s shareholding in Chinese commercial banks to 20% and the aggregate foreign ownership ratio to 25%.

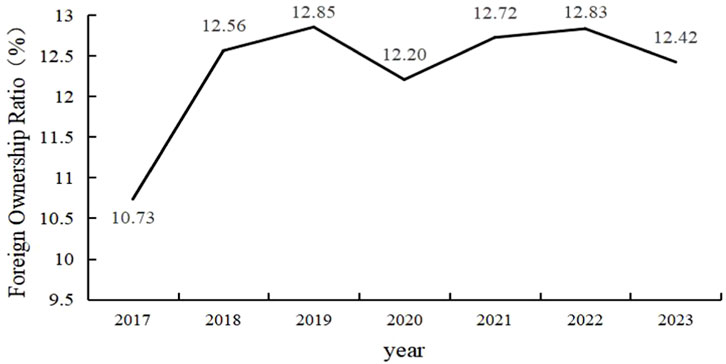

Further liberalisation of China’s banking sector, epitomised by removing foreign ownership restrictions, has attracted substantial inflows of high-calibre foreign banking capital, infusing domestic financial markets with ample liquidity. Furthermore, it helped introduce advanced managerial expertise and innovative financial products. This not only enhanced financial market vitality and optimised resource allocation but also built a solid financial foundation for fostering innovation-driven development and industrial upgrading and transformation across various sectors of the real economy. Unlike previous opening-up practices, removing foreign ownership restrictions was a landmark event in the banking sector’s liberalisation (Jin et al., 2022; Zeng and Wei, 2024). This reform includes deepened institutional innovations implemented during the high-quality development phase, specifically under the framework of pre-establishment national treatment and a negative list management model. The removal of foreign ownership restrictions has had a profound impact on China’s domestic banks. Taking city commercial banks with relatively low valuations and strong growth potential as an example, their foreign ownership ratios have increased significantly, rising from 10.73% in 2017 to 12.42% in 2023. The foreign ownership ratios of the Bank of Ningbo, Bank of Zhengzhou, Bank of Qingdao, Bank of Xiamen, and Bank of Chengdu exceeded 20% (Figure 1).1 The number of foreign banking institutions and their asset proportions demonstrate dual growth. As of September 2023, 202 banking institutions from 52 countries and regions have established operations in China, with total foreign bank assets reaching 3.79 trillion yuan, representing a 0.07 percentage point increase in the banking sector’s asset share compared to 2018 levels. Foreign institutions are increasingly leveraging their competitive advantages in cross-border finance, wealth management, and derivatives trading. In 2023, the financial derivatives business scale of foreign banks was 19.2 trillion yuan, capturing 19% of commercial banks’ market share in this sector. Current research on the economic effects of banking sector openness in the new era remains relatively underdeveloped, lacking substantive discussion of micro-level corporate sustainability. Leveraging the exogenous shock of China’s removal of foreign ownership restrictions in banking as a quasi-natural experiment, this study explores whether financial liberalisation improves corporate ESG performance and its potential to drive green economic transition and sustainable development.

Figure 1. Changes in Foreign Ownership Ratios of City Commercial Banks, 2017–2023. Data Source: City commercial banks’ annual reports.

2.2 Theoretical analysis and research hypotheses

2.2.1 Banking liberalisation and corporate ESG performance

As a cornerstone of the financial system, the further opening of China’s banking sector by removing foreign ownership restrictions has introduced international capital with ESG preferences. Foreign capital exhibits stronger ESG inclinations than domestic investment for two reasons. First, foreign capital primarily originate from developed economies with a longer history and greater prevalence of ESG practices such as in Europe and the United States. Due to the inertia of adhering to their home countries’ ESG investment social norms and external pressure from investors for responsible investment, they tend to prefer companies with good ESG performance (Yang et al., 2022; Wang et al., 2023; Yin et al., 2023; Wu and Liu, 2024). Second, foreign institutions with longer investment horizons tend to prioritise ESG screening to mitigate tail risks, such as environmental litigation (Barber et al., 2021). Along with cross-border capital flow, responsible banking and experience in ESG strategic planning and practices have been introduced into the domestic banking sector. Foreign investors can send directors or executives to encourage banks to incorporate ESG objectives into their business operations and scientifically plan and practice ESG strategies. Additionally, along with the increased proportion of foreign ownership, foreign investors have more incentives to provide banks with advanced technology and management experience (including ESG information screening and management), optimise their governance as strategic investors (Liu and Nie, 2016), and implement responsible banking concepts and ESG preferences in banks’ strategic planning and business decision-making through the board of directors’ seats and voting rights. Foreign shareholders, as large external shareholders, can check insiders and reduce agency costs through board seats and voting rights (Shleifer and Vishny, 1997).

The profound impact of further banking sector liberalisation on the banking sector encourages enterprises to practice sustainable development and improve the ESG performance through lending and borrowing relationships from the supply and demand sides of funds in both directions. From the supply-side perspective, introducing responsible banking philosophies and practical ESG expertise through opening-up drives the banking sector to establish credit decision-making and management systems incorporating ESG factors, exerting external governance pressure on borrowing enterprises (Hasan et al., 2017; Dai et al., 2021). First, foreign shareholders’responsible banking philosophies and practical ESG expertise prompt banks to integrate ESG factors into loan decision-making considerations, restructuring credit evaluation frameworks. Second, banks will place greater emphasis on corporate ESG risks throughout the credit process to mitigate potential credit risks (Zhu and Wei, 2023). Environmental incidents, such as pollution accidents, may incur substantial environmental remediation costs or administrative penalties, undermining borrowers’ business revenue (Sun and Liu, 2021). Concurrently, internal governance deficiencies may trigger financial fraud or managerial corruption, eroding debt repayment capacity. Social controversies, including labour disputes and food safety incidents, risk diminishing consumer brand trust and amplifying operational uncertainties (Deng and Long, 2017), jeopardising timely loan repayments. Finally, grounded in the Principles for Responsible Banking, providing sustained capital commitment to enterprises with superior ESG performance constitutes a strategic imperative for the banking sector to align with the global sustainability transition, cultivate positive social legitimacy, and implement reputational stewardship (Zhu and Wei, 2023). Such enterprises typically demonstrate enhanced operational resilience and innovation capacity, serving as conduits for stable yield streams and anchors for portfolio robustness.

From the demand-side perspective, foreign capital introduced through banking sector openness demonstrates stronger preferences for enterprises with superior ESG performance (Chen and Jia, 2025). Driven by financing accessibility and comparative advantages, enterprises will improve their ESG performance to secure bank credit support. First, motivated by the desire to align with international capital preferences, companies will proactively enhance their ESG performance to increase the likelihood of accessing credit resources (Hoepner et al., 2018; Hu et al., 2023). Second, according to signalling theory, ESG practices can convey the positive information of enterprises regarding environmental risk management, social reputation maintenance, and governance effectiveness to banks and other stakeholders. As banks incorporate ESG factors into their credit decisions, enterprises’ improved ESG performance can alleviate information asymmetry through the signalling mechanism, creating a comparative advantage in financing, and obtaining credit support at lower costs, higher credit limits, or longer terms. Thus, the following is proposed:

Hypothesis 1. Banking liberalisation improves corporate ESG performance.

2.2.2 Banking liberalisation, ESG information disclosure, and corporate ESG performance

With relaxed foreign ownership restrictions, ESG-preferring international capital inflows into domestic credit markets compel banks to prioritise potential borrowers’ ESG evaluations, increasing firms’ initiative and motivation to disclose ESG information. First, motivated by the need to cater to banks’ preferences for superior ESG performers, enterprises will enhance their willingness to disclose ESG information. Second, compared with investors, creditors have stronger information advantages and more stringent auditing capabilities (Sun et al., 2023), Rather than having negative information about environmental responsibilities and other aspects collected by creditors, decision-makers tend to take the initiative to disclose the implementation of their ESG concepts. Third, as legally binding instruments delineating rights and obligations, responsible banking institutions use loan contract stipulations to mandate ESG disclosure. Underpinned by sustainability-oriented policy frameworks, such as the Green Finance Guidelines (which explicitly require banks to incorporate ESG risk-reporting requirements in loan agreements for clients and projects involving material ESG risks), enterprises are increasingly compelled to enhance ESG disclosure in response to intensified creditor scrutiny. Moreover, enterprises’ complete ESG information disclosure is not only conducive to banks and other stakeholders monitoring enterprises’ ESG practices but also helps signal active social responsibility (Fang and Hu, 2023), enhancing enterprises’ reputations. Firms will proactively assume social responsibility and improve their ESG performance to cope with external monitoring pressures or maintain their reputations. Thus, the following is proposed:

Hypothesis 2. Banking liberalisation improves corporate ESG performance by increasing ESG information disclosure.

2.2.3 Banking liberalisation, financing constraints, and corporate ESG performance

The severe financing constraints faced by enterprises significantly hinder improvements in their ESG performance. Alleviating financing constraints can provide the necessary financial support to enhance ESG performance. On one hand, increasing the liberalisation of the banking sector can attract more foreign investment, thereby increasing the total supply of credit and further enhancing enterprises’ access to credit resources, thereby alleviating financing constraints (Wang, 2019). On the other hand, foreign banks have distinct advantages in business operations and risk management. As the number of foreign banks entering the market increases, they can play a ‘catalyst effect,’ thereby incentivising local banks to improve operational efficiency and provide high-quality financial services to enterprises, thereby alleviating financing constraints. With adequate credit funding support, enterprises will increase their investment in environmental protection facilities, develop energy-saving and emission-reduction technologies, and optimise production processes to minimise energy intensity (Chen and Chen, 2018). At the same time, enterprises will establish competitive compensation packages, optimise working conditions, and provide professional development pathways for employees (Liu et al., 2024) while actively engaging in community development initiatives and philanthropic engagements. Furthermore, the participation of international investors will incentivise enterprises to improve their internal governance mechanisms (Xiao and Lin, 2024), thereby enhancing their ESG performance. Thus, the following is proposed:

Hypothesis 3. Banking liberalisation improves ESG performance by alleviating financing constraints.

2.2.4 Banking liberalisation, managerial myopia, and corporate ESG performance

Enterprises must not only pay certain economic costs to implement ESG practices but may also face challenges in producing short-term results. Under short-term performance pressure and performance-based assessment incentive mechanisms, management is not sufficiently motivated to integrate ESG concepts into operations and management decisions, exhibiting a certain degree of myopia (Wang, 2023). The liberalisation of the banking sector has allowed more foreign capital to enter the Chinese market, which has optimised bank governance and encouraged banks to focus on long-term benefits (Hasan and Xie, 2013). The advanced risk management experience brought by foreign banks also helps enhance the risk management awareness and capabilities of domestic banks (Havrylchyk et al., 2009), and prompting the banking sector to choose loan recipients prudently. Enterprises with good governance and sound management decision-making are more likely to obtain financial support, which incentivises them to continuously optimise their governance mechanisms and improve their governance levels (Ashbaugh-Skaife et al., 2006). As advanced management concepts and technologies are introduced, through cooperation with banks, enterprises can draw on the risk management experience and internal governance mechanisms foreign investors introduce, better monitor managerial decision-making behaviour, and curb managerial myopia that pursues short-term performance to the detriment of long-term development. Thus, the following is proposed:

Hypothesis 4. Banking liberalisation improves ESG performance by curbing managerial myopia.

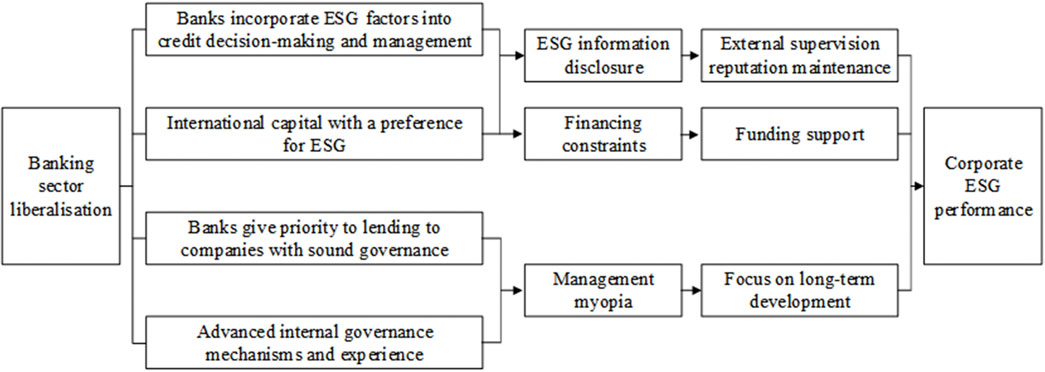

Figure 2 summarises the logical framework of the above transmission mechanisms. The empirical section below will test the validity of these three mechanisms separately.

Figure 2. The mechanism through which banking sector liberalisation affects corporate ESG performance.

3 Research design

3.1 Sample selection and data source

This study uses data from Chinese A-share listed companies from 2012 to 2023. Corporate ESG performance is measured using environmental protection, social responsibility, and corporate governance scores from the Huazheng ESG Index sourced from the Wind Financial Terminal. Other firm-level data are from the CSMAR Database.

Based on raw data collection, the following treatments are performed: (1) excluding listed companies in ST, ST*, and financial industries, (2) excluding samples with missing observations for key variables, (3) excluding samples with obvious data bias such as debt ratios less than zero or greater than 1, and (4) winsorizing the continuous variables at the 1st and 99th percentiles to control for the possible effects of extreme values. Ultimately, 23,938 firm-year observations are obtained.

3.2 Model construction and variable definitions

This study uses a difference-in-differences (DID) approach to examine whether and how banking sector liberalisation, proxied by removing foreign ownership restrictions, improves corporate ESG practices. The 2018 removal of foreign ownership restrictions in the banking industry was a national-level policy to promote liberalisation. Its formulation, deliberations, and implementation processes were macro-level in nature, independent of individual corporate characteristics and ESG performance. Micro-level enterprises were unable to influence the formulation and implementation of the policy through their own actions, ensuring the exogenous nature of the policy impact. However, restrictions on foreign ownership in China’s banks were liberalised nationwide in 2018. Therefore, firm-level standard experimental and control groups are unavailable for constructing standard DID models. The liberalisation of the banking sector represents a significant adjustment at the macro-institutional level, with its core effects being the introduction of international capital and the enhancement of credit allocation efficiency, thereby ultimately influencing corporate behaviour by alleviating regional financial repression. In cities with higher levels of financial repression, the capital supplementation effect and credit allocation efficiency effect of banking sector liberalisation are more pronounced, exerting a greater influence on corporate ESG practices; conversely, in cities with lower levels of financial repression, the marginal impact of the policy is smaller. Therefore, the degree of financial repression largely reflects the differentiated impact of banking sector liberalisation on different cities, ultimately influencing corporate behaviour through its impact on urban financial development. This provides a theoretical foundation for the design of intensity variables in a generalised DID framework. Based on this, this study uses pre-policy urban financial repression levels as intensity variables. Following Bai et al.’s (2018) modelling framework, a generalised DID model is constructed to explore the impact of banking liberalisation on corporate ESG performance as follows:

where i denotes sample individuals, t denotes years, and j denotes cities. The dependent variable reflects a company’s ESG performance. Existing literature primarily uses third-party rating data to measure corporate ESG performance. Current mainstream ESG rating indices include international indices such as MSCI, Dow Jones, Thomson Reuters, FTSE (Financial Times Stock Exchange), and Bloomberg ESG index, as well as domestic indices such as the Huazheng ESG Index, Shangdao Ronglv, Hexun ESG, CSI(China Securities Index) ESG Index, and Wind ESG. Due to significant differences in external environments such as policies, markets, and societies across countries, foreign ESG indices are not entirely applicable to Chinese companies. Considering that the Huazheng ESG Index is constructed based on the core principles of foreign mainstream ESG indices, combined with the information disclosure situation and characteristics of Chinese companies, covering all A-share listed companies and widely recognised and applied in the academic community (Xie and Lv, 2022; Fang and Hu, 2023), this paper uses the Huazheng ESG score as a proxy variable for corporate ESG performance in the baseline regression. Higher values indicate better ESG performance. Considering that systematic differences may exist in the ESG performance of firms in different industries, referring to Zhu and Wei (2023), the industry median is adjusted for ESG scores. However, relying on third-party ESG ratings to measure corporate ESG performance carries certain risks of measurement error. These risks primarily manifest in rating discrepancies caused by methodological differences in rating systems, scales, and data sources; challenges in quantifying and validating qualitative ESG data; and unavoidable subjective interference from rating agencies. Therefore, it is necessary to select different rating indices for cross-validation. In the Chinese context, due to the incomplete ESG disclosure system and rating framework during the sample period, the rating market is in a relatively early stage with insufficient standardisation, making the measurement error challenges faced by domestic ESG rating indices even more severe. Therefore, this paper selects the internationally recognised Bloomberg ESG Index as an alternative variable for robustness testing in the subsequent analysis.

The core independent variable is the interaction term between the time dummy (equal to 1 for 2018 and subsequent years and 0 otherwise) and city-level pre-deregulation financial repression intensity. In the banking sector, financial repression primarily manifests as high market concentration, insufficient competition, and low efficiency in the allocation of credit resources. Therefore, the level of banking competition effectively reflects the intensity of financial repression in a banking-dominated economy. Following the approach of Wu and Feng (2022) this paper uses the level of banking sector competition as a proxy variable for the degree of financial repression in cities. Specifically, following the method of Jiang et al. (2019), we utilise financial licence information on financial institutions from the National Financial Regulatory Bureau to calculate the number of branches of each bank (Considering that the credit decisions of policy banks, rural cooperative banks and credit unions are constrained by government policies or service targets, and are therefore less market-oriented, these three types of banks have been excluded, leaving only commercial banks to more fully reflect the market structure characteristics of the banking industry.). The number of branches in each city is then used to construct the Herfindahl-Hirschman Index (HHI) for the banking sector in each city to measure the level of banking competition. The index ranges from 0 to 10,000 and is a negative indicator, with higher values indicating lower banking competition and higher financial repression. Additionally, to futher ensure the exogeneity and ex ante nature of the intensity variables and to smooth out potential short-term fluctuations to some extent, this paper references Zhang et al. (2023), the average of the competition intensity of banks in each city in 2016 and 2017 (the 2 years prior to the relaxation of foreign equity ownership restrictions) is used as a proxy variable for financial repression intensity, which is then log-transformed. The coefficient of primary interest is β1.

To mitigate potential omitted variable bias, the empirical specification incorporates a comprehensive set of firm-level control variables following the approach of Wang et al. (2023) and Zhu and Wei (2023): (1) firm size (size), the natural logarithm of total assets; (2) financial leverage (lev), total liabilities/total assets; (3) liquidity ratio (liq), current assets divided by current liabilities; (4) cash flow level (cashflow), net operating cash flow divided by total assets; (5) profitability (ROA), ratio of net profit to total assets; (6) growth (growth), growth rate of operating revenue; (7) book-to-market ratio (MB), ratio of shareholders’ equity to market value, (8) firm age (age), current year minus the year the company was established, (9) board independence (indratio), ratio of independent directors to total board members, (10) equity concentration (Top10), shareholding ratio of the top ten shareholders, and (11) dual role (dual): whether the chairperson is also the general manager. Among these, the first eight variables primarily reflect basic information about the company, such as its age and size, as well as its financial characteristics. These variables not only influence a company’s ability to obtain and allocate resources, thereby affecting its ESG investments, but are also susceptible to the impact of banking sector liberalisation policies (e.g., financial leverage, liquidity ratio) or may have differentiated effects on the microeconomic impacts of liberalisation policies (e.g., firm size, firm age). The last three variables reflect a company’s governance structure, which is a key driver of its implementation of ESG principles and may also be influenced by banking sector liberalisation policies. This study controls for firm and year fixed effects, where εi,t are residual terms.

In addition to the exogeneity of the policy and the validity of the intensity variables analysed earlier, the causal identification in this paper also relies on the parallel trend assumption, which states that prior to the implementation of the policy (2018), there were no systematic differences in the trends of ESG changes among enterprises in cities with different levels of financial repression. The parallel trend test in the subsequent section will verify whether this assumption holds. If the coefficients of the core variables are not significant prior to the policy implementation, this supports the parallel trend assumption. When the above identification assumptions hold, the coefficient β1 of the core variables in the model can be interpreted as the causal promotional effect of banking sector liberalisation on corporate ESG performance. Based on the theoretical analysis in the preceding section, this paper expects the regression coefficient β1 to be significantly positive, indicating that banking sector liberalisation has a significant promotional effect on corporate ESG performance.

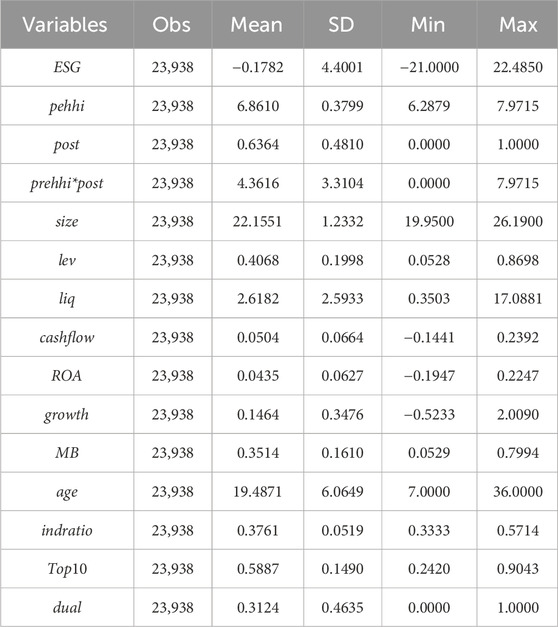

Table 1 presents the descriptive statistics for key variables. The listed firms exhibit substantial variation in ESG performance, evidenced by a mean ESG score of −0.1782 (standard deviation = 4.4001). The financial repression measure (prehhi), calculated as the HHI of city-level banking sector concentration, has a mean of 6.8610 (SD = 0.3799). This indicates the high intensity and significant cross-city dispersion of financial repression, with the standard deviation exceeding 5% of the mean. The core explanatory variable prehhi*post has a mean of 4.3616 and standard deviation of 3.3104, indicating a significant difference in the impact of banking sector liberalisation across firms before and after policy implementation. For sample firms, on average, return on assets (ROA) is 0.0435, growth rate of operating income (growth) is 0.1464, and age is 19.4871. Table 1 shows descriptive statistics for the other control variables, in which the distributions of firm size (size) and liquidity ratio (liq) are more discrete.

Table 1. Descriptive statistics of the main variables.

4 Effects of banking liberalisation on corporate ESG performance

4.1 Baseline regression analysis

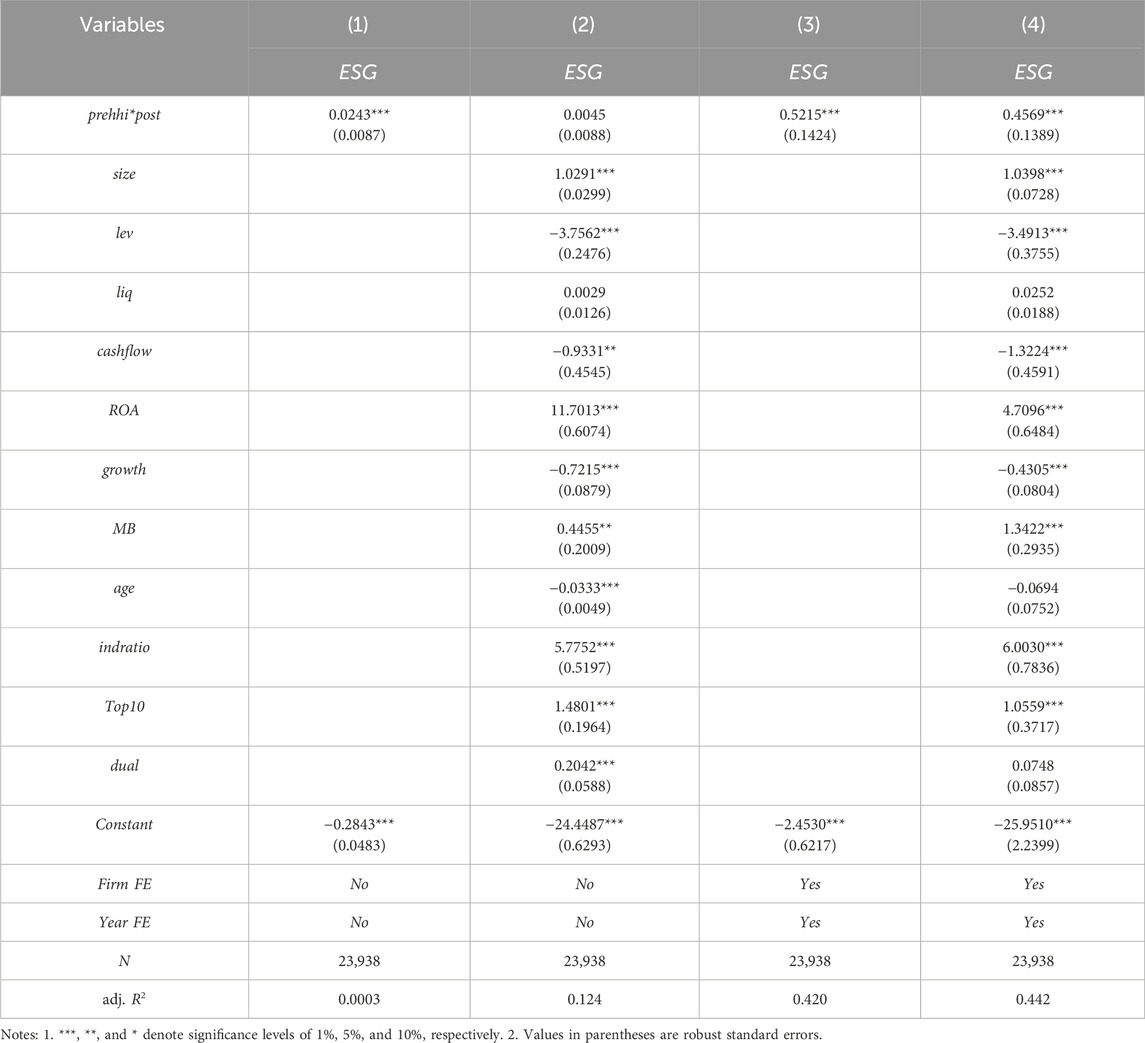

Table 2 presents the regression results of banking sector liberalisation on corporate ESG scores. Columns (1) and (3) report the estimates for the core explanatory variable prehhi*post. Column (3) augments column (1) by incorporating time and firm fixed effects. Columns (2) and (4) introduce control variables into the specifications in columns (1) and (3). The results demonstrate that the coefficient of prehhi*post, the interaction term that captures banking liberalisation, is statistically significant at the 1% level and positive across all specifications, regardless of whether control variables are included. Thus, removing foreign ownership restrictions in the banking sector significantly enhances corporate ESG performance. In economic terms, the coefficient of prehhi*post in column (4) indicates that after further liberalisation of the banking sector, the ESG score of enterprises increased by 0.4569 points. This increase is approximately one-tenth of the Huazheng ESG rating scale (under Huazheng’s rating rules, except for scores below 60, which are the lowest grade C, and scores above 95, which are the highest grade AAA, all other grades are divided into intervals of 5 points),equivalent to 0.6% of its mean value (73.4537), which is significantly higher than the annual average growth rate of 0.05% during the sample period. This coefficient also indicates that a 1% increase in the standard deviation of banking sector liberalisation leads to a 0.3437 standard deviation increase in corporate ESG performance. Inshort, after banking sector liberalisation, companies actively improved their environmental, social and governance practices, which significantly improved their ESG performance. The above results support Hypothesis 1.

Table 2. Banking liberalisation and corporate ESG performance.

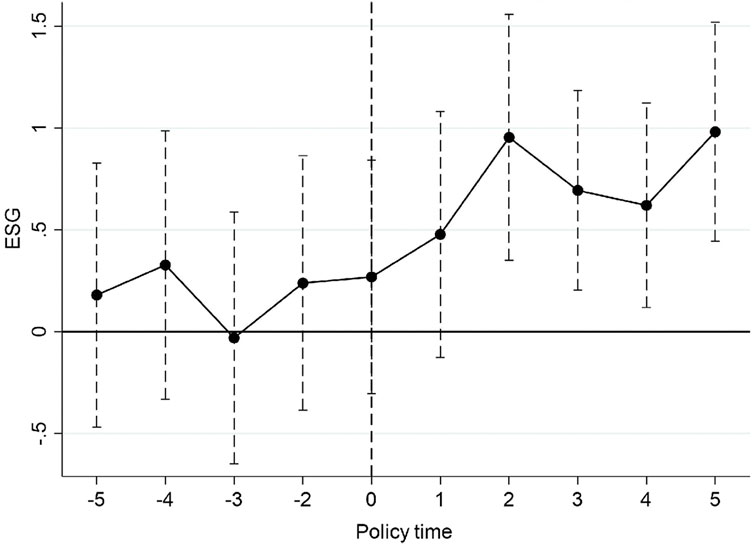

4.2 Parallel trend test

The validity of the generalised DID model relies on parallel trend testing. Drawing on Beck et al. (2010) and Bian et al. (2019), year dummy variables are constructed for the fifth, fourth, third, second, and first years preceding the deregulation of foreign ownership limits in the banking sector, the implementation year itself, and the first, second, third, fourth, and fifth years following deregulation. These dummies then interact with regional financial repression intensity (prehhi) to test the parallel trend assumption. Using the interaction term from the year immediately preceding the deregulation of foreign ownership limits in banking as the baseline category, these constructed variables are incorporated into the baseline regression specification. Econometric estimation is performed by visually inspecting parallel trends through dynamic treatment effect plotting. The estimation results demonstrate that before foreign ownership limits deregulation in banking, the interaction terms between policy shock dummies and regional financial repression intensity (prehhi) show statistically insignificant coefficients (p > 0.10), satisfying the parallel trends assumption. Furthermore, the analysis reveals dynamic treatment effects, in which the ESG-enhancing impact of banking sector liberalisation emerges gradually, with statistically significant coefficients at the 5% level materialising 2 years post-deregulation and persisting throughout the five-year observation window (Figure 3).

Figure 3. Parallel trend in banking sector liberalisation to corporate ESG performance.

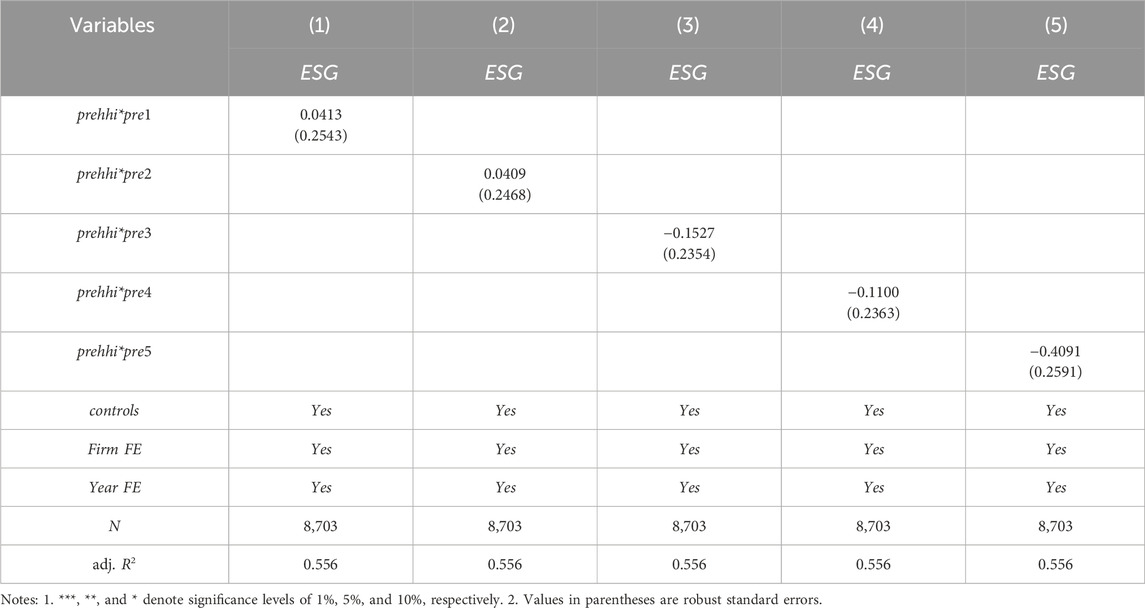

4.3 Placebo test

Placebo tests are implemented by artificially reassigning the policy enactment year to mitigate concerns regarding unobserved confounders. Specifically, the pre-treatment sample (2012–2017) is retained, and the hypothetical policy shock year sequentially shifted from 2013 to 2017. For each counterfactual scenario, the key explanatory variable is reconstructed as the interaction term between urban financial repression indices and pseudo-treatment dummies. Equation 1 is then re-estimated. None of the estimated coefficients of the interaction terms are significant at the 10% level, implying that banking sector liberalisation did not improve firms’ ESG performance before the liberalisation of foreign ownership restrictions in the banking sector. Thus, the baseline regression results are unlikely to be affected by unobservable factors (Table 3).

Table 3. Placebo test.

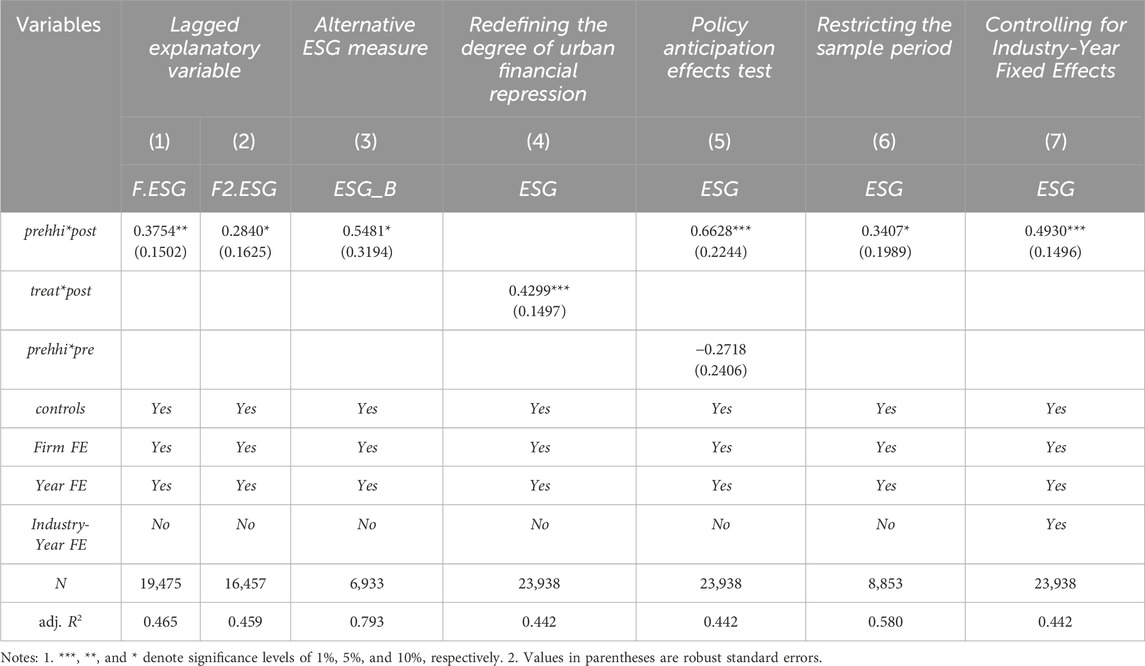

4.4 Robustness tests

4.4.1 Lagged explanatory variable

Considering a potential lag in the effect of banking sector liberalisation on corporate ESG performance, the explanatory variables in the benchmark regression are lagged by one and two periods, respectively, and re-analysed. Columns (1) and (2) of Table 4 present the results. After considering the lagged effect, banking sector liberalisation continues to significantly promote corporate ESG practices.

Table 4. Robustness tests.

4.4.2 Alternative ESG measure

As mentioned earlier, relying on third-party ratings to measure a company’s ESG performance inherently carries a certain risk of measurement error, and this issue is even more severe in China’s ESG rating market. First, the regulations and mandatory systems for ESG information disclosure during the sample period are still incomplete, leading to significant differences in the level of disclosure and information quality among companies. Strong ESG performance helps enterprises establish a responsible social image (Fang and Hu, 2023), thereby earning public trust and aggregating production and operational resources. Consequently, firms may have incentives to exaggerate their green practices in ESG reports, potentially skewing assessment agencies’ ratings. Second, China’s ESG rating industry is in its infancy and characterised by underdeveloped evaluation frameworks. Certain agencies provide rating and consulting services simultaneously, inherently creating conflicts of interest and undermining the impartiality of ratings. To mitigate the potential impact of ESG rating measurement errors (especially those of domestic Chinese rating indices) on benchmark results, Bloomberg ESG score (ESG_B, a widely used global ESG index with relatively transparent methodology and international comparability) is adopted as an alternative measure for corporate ESG performance to re-estimate model (1), finding that the baseline conclusion holds.

4.4.3 Redefining the degree of urban financial repression

Median-split analysis is performed to mitigate measurement errors in the financial repression index (prehhi). Cities scoring above or equal to the median value are classified as the high-repression group (treat = 1), with the others constituting the low-repression group (treat = 0). The coefficients yielded by the dummy variable specification are consistent in sign and significance with the baseline results.

4.4.4 Policy anticipation effects test

Although the open policy cancelling restrictions on foreign shareholding in the banking sector was officially announced in 2018, the report The Second Half of China’s Financial liberalisation, released by the China Financial Forty Forum in 2017, had already recommended cancelling restrictions on foreign shareholding proportions in the banking sector. Zhu Guangyao, the Vice Minister of Finance, also explicitly indicated that these restrictions would be cancelled at the China–US premier’s meeting. The echo of industry voices and official statements may have driven positive market expectations of the opening-up policy, thus generating a certain anticipatory effect. To exclude this potential impact on the estimation results, the interaction term between the dummy variable of 1 year before the liberalisation of foreign ownership (pre) and the degree of financial inhibition (prehhi) is added to the baseline regression for validation. Consequently, the conclusions remain unchanged.

4.4.5 Restricting the sample period

The sample period is restricted to 2012–2019 and 2023 to account for the extraordinary disruptions caused by the COVID-19 pandemic. Excluding firm-year observations in 2020–2022 yields coefficient estimates quantitatively aligned with the baseline results, passing the 10% significance threshold.

4.4.6 Controlling for industry-year fixed effects

In order to eliminate the interference of time-varying industry factors, this paper further controls for industry-year fixed effects on the basis of the benchmark regression. This method can absorb industry-level confounding factors that evolve over time, thereby reducing bias in the conclusions. The results show that the coefficients of the core explanatory variables remain significantly positive, consistent with the baseline regression.

5 Mediation and heterogeneity analyses

5.1 Mediation analysis

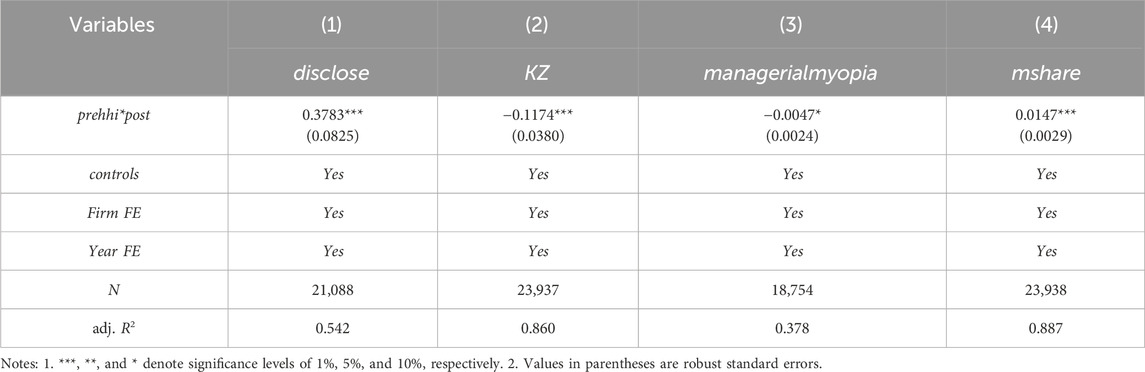

5.1.1 Enhancing ESG information disclosure

Following the liberalisation of foreign ownership restrictions in the banking sector, financial institutions will more intensely scrutinise corporate ESG practices, prompting enterprises to enhance their ESG information disclosures, improving their ESG performance. To validate this transmission mechanism, this study draws on the methodology of Han and Li (2021) and employs the disclosure status of stakeholder-related social responsibility fulfilment as a proxy metric for ESG information disclosure in listed companies. An ESG disclosure index is constructed based on 12 disclosure dimensions extracted from the CSMAR Database’s Corporate Social Responsibility Report Information Sheet. A binary indicator (1 = disclosed, 0 = non-disclosed) is assigned for each dimension, and the composite index derived through summation. This approach yields an ordinal metric, in which higher values correspond to more comprehensive disclosure. Raw scores are further adjusted by subtracting their respective industry medians, resulting in an industry-median-adjusted disclosure measure (disclose) accounting for cross-industry heterogeneity in disclosure baselines. The results are shown in Column (1) of Table 5. It can be seen that the coefficient of the core explanatory variable is significantly positive at the 1% level, indicating that after further liberalisation of the banking sector, enterprises will improve their ESG disclosure levels. From an economic perspective, the regression coefficient of 0.3783 means that after further liberalisation of the banking sector, companies increased their ESG information disclosure by an average of 0.3783 dimension (equivalent to 6.51% of the average number of disclosure dimensions of the sample companies). It also shows that for every 1% increase in the standard deviation of banking sector liberalisation, the level of ESG disclosure by companies increases by 0.4248 standard deviations. The above results support Hypothesis 2, which states that after the banking sector expands its liberalisation, companies will enhance their ESG disclosure levels to align with foreign investors’ preference for companies with good ESG performance and maintain their credit relationships with banks, thereby improving their ESG performance.

Table 5. Mediation analysis.

5.1.2 Alleviating financing constraints

Banking sector liberalisation expands corporate ESG initiatives’ capital access, mitigating the effects of financing constraints on ESG implementation. Following Xu et al. (2024), the Kaplan-Zingales (KZ) index is used to measure listed firms’ financing constraints to examine this mechanism. Higher index values correspond to more severe financing constraints. As shown in Column (2) of Table 5, the coefficient of the core explanatory variable is significantly negative, indicating that the relaxation of foreign ownership restrictions in the banking sector has effectively alleviated the financing constraints of the sample firms. The regression coefficient shows that after the expansion of banking sector liberalisation, the financing constraint index decreased by 0.1174, equivalent to 10.84% of the sample firms’ mean value. The coefficient of 0.1174 also indicates that for every 1% increase in the standard deviation of banking sector liberalisation, the ESG financing constraints of enterprises will decrease by 0.1576 standard deviations. Inaddition, after the expansion of banking sector liberalisation, the financing constraints of the sample enterprises were effectively alleviated, and enterprises may have more sufficient funds to improve production processes, engage in green technological innovation, enhance employee welfare, maintain good cooperative relationships with suppliers, and other activities to improve their ESG performance. Thus, Hypothesis 3 is supported.

5.1.3 Mitigating managerial myopia

Influx of foreign capital enhances banks’ governance quality and risk management awareness, prompting prudent borrower selection. This compels enterprises to improve corporate governance. Concurrently, foreign capital introduces advanced internal governance mechanisms. The dual effects mitigate managerial myopia, incentivising executives to prioritise long-term corporate development and adopt ESG principles. Building on this framework, this study investigates whether banking sector liberalisation enhances corporate ESG performance by curbing managerial myopia. This mechanism is operationalised by first employing textual analysis following Hu et al. (2021) to quantify managerial short-termism. The ratio of short-term horizon lexicon frequency to total word count in the Management Discussion and Analysis (MD&A) sections of annual reports is calculated and multiplied by 100. This metric, constructed using Word2Vec semantic expansion and lexicon-based approaches, captures managerial myopia through MD&A disclosures (managerialmyopia). Higher values indicate more severe managerial myopia, with textual data sourced from the WinGO Financial Text Analytics Platform. Following Zhong et al. (2017) and Wang (2023), the management shareholding ratio (mshare) is used as a proxy for managerial myopia. This captures the degree of interest alignment between management and shareholders. Higher mshare values indicate stronger convergence in principal–agent incentives, motivating executives to prioritise long-term value creation over short-termism. Columns (3) and (4) of Table 5 present the results. The coefficients of core explanatory variable are significant, regardless of the measure used. Thus, opening up the banking sector further suppresses managerial myopia to a certain extent. The regression coefficient of −0.0047 in column (3) indicates that a 1% increase in the standard deviation of banking sector liberalisation reduces the frequency of management myopia by 0.2386 standard deviations. The coefficient of 0.0147 in column (4) means that after banking sector liberalisation, the average shareholding ratio of corporate management increased by 0.0147% (equivalent to 0.26% of the sample mean). These results jointly indicate that further expansion of banking sector liberalisation effectively suppresses managerial myopia, enabling management to adopt a long-term perspective, actively engage in ESG practices, and thereby improve ESG performance. Thus, Hypothesis 4 is supported.

5.2 Heterogeneity analysis

5.2.1 Heterogeneity analysis based on property rights

Enterprises’ ownership structure may influence the ESG improvement effects of banking liberalisation. State-owned enterprises (SOEs) often face more significant political mandates than private enterprises. Amid the prevailing sustainable development trend, SOEs have increasingly been regarded as strategic instruments for governmental agencies to promote high-quality economic growth through critical functions of exemplary leadership and policy transmission (Fang and Hu, 2023). Under the effects of ESG concepts introduced through foreign equity participation and multidimensional regulatory and market supervision pressures, SOEs demonstrate a decisive institutional impetus for engaging in ESG practices. Soft budget constraints and implicit government guarantees enable easier access to access credit resources for SOEs. This enhanced financial capacity empowers SOEs to systematically translate banks’ ESG governance recommendations into institutionalised practices, facilitating proactive green innovation initiative engagement, employee compensation enhancement, and sustainability-oriented activities.

Comparatively, privately owned enterprises face intensified market competition constraints. Deregulation of foreign ownership limits and banks’ incorporation of ESG metrics into credit assessments jointly amplify privately owned enterprises’ incentives to alleviate financing constraints by enhancing ESG performance. However, constrained by inferior resource orchestration capacity, privately owned enterprises’ ESG improvements tend to cluster in governance dimensions (G-Score) with manageable compliance costs while underinvesting in capital-intensive environmental (E-Score) and social (S-Score) dimensions.

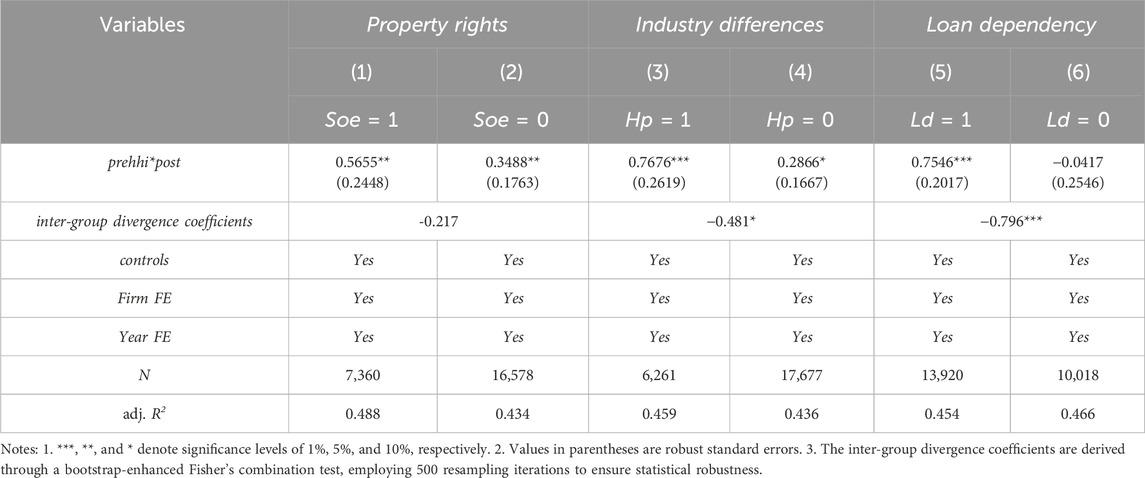

A subsample analysis is performed by partitioning the dataset into SOEs and non-SOEs to examine the heterogeneous effects of banking sector liberalisation on ESG enhancement according to property rights. Specifically, an SOE dummy variable (Soe) is constructed, equalling 1 if a firm is ultimately controlled by a state entity and 0 otherwise. Columns (1) and (2) of Table 6 present the re-estimated specification results. The improved ESG performance caused by banking sector liberalisation is significant in both SOEs and non-SOEs, and the interaction term coefficient is higher for SOEs than non-SOEs (0.5655 vs. 0.3488). In other words, in terms of the coefficient, banking sector liberalisation has a more pronounced promotion effect on SOEs’ ESG performance. However, the between-group coefficient difference test indicates no significant between-group differences. This phenomenon has possible five potential explanations. First, in the face of the removal of foreign ownership restrictions, banks have incorporated ESG factors into their credit decision-making and management processes. SOEs can quickly improve their ESG performance in the short term due to their resource advantages, but they lack the motivation for further improvement in the long term, resulting in weak sustainability of ESG performance improvements. In contrast, private enterprises, which face stronger financing constraints, improve their ESG performance at a slower pace but with greater sustainability. This may have weakened the differences in the ESG improvement effects of banking sector liberalisation between the two groups of enterprises. Second, the multi-layered principal–agent relationships inherent in SOEs’ governance structures attenuate the disciplinary effects of banking sector openness, partially counterbalancing their resource-driven advantages in ESG implementation. Simultaneously, private enterprises engage in strategic isomorphism by replicating SOEs’ ESG practices to meet banks’ financing requirements. As a result, the difference in the ESG improvement effect of banking sector liberalisation between the two types of enterprises has narrowed. Third, in 2015, the State Council of China issued the “Comments on the Development of a Mixed Ownership Economy in State-owned Enterprises,” which made specific arrangements for the principles, path and operational norms of mixed ownership reform. The implementation of the “mixed ownership reform” policy has gradually narrowed the gap between the two types of enterprises in terms of resource acquisition, thereby reducing the difference in the ESG effect of banking sector liberalisation. Fourth, the current domestic ESG evaluation system in China places greater emphasis on “social contributions” (such as employment and environmental protection and emissions reduction). SOEs place greater emphasis on these non-economic objectives, resulting in generally higher ESG scores compared to non-SOEs. This measurement error may lead to an overestimation of the coefficients for the state-owned enterprise group (Sun et al., 2024). Fifth, in the sample used in this paper, state-owned enterprises account for approximately 30.7%, far lower than non-state-owned enterprises (69.3%). The imbalance in the sample structure may result in insufficient statistical power for intergroup tests.

Table 6. Heterogeneity analysis.

5.2.2 Heterogeneity analysis based on industry differences

Specific environmental practices have substantial effects on sustainable enterprise development. The business activities of companies in heavily polluting industries have more substantial negative environmental externalities, and thus face stricter environmental regulatory pressure and continuous monitoring by multiple interests. To cater to foreign preferences for good ESG performance or adapt to banks’ prudent credit policies towards high-environmental-risk sectors because of cross-border capital flows, such companies are more likely to increase their investments in pollution prevention and social responsibility. Accordingly, banking sector openness is hypothesised to exert a more pronounced improvement effect on ESG performance among pollution-intensive enterprises. A dual classification framework integrating the 2010 Environmental Information Disclosure Guidelines for Listed Companies (Exposure Draft) issued by the former Ministry of Environmental Protection with the 2012 Industry Classification Guidance for Listed Companies revised by the China Securities Regulatory Commission is used to identify 19 industries subject to stringent environmental regulations.2 A dichotomous pollution-intensity variable (Hp) is constructed, equalling 1 for pollution-intensive firms and 0 otherwise. Heterogenous effects are tested using subsample regression analyses. Columns (3) and (4) of Table 6 show that banking liberalisation enhances ESG performance significantly more in pollution-intensive industries (coefficient: 0.7676) than in their non-polluting counterparts (0.2866). Rigorous bootstrap-based differential testing indicates this intergroup disparity is significant (p < 0.1).

5.2.3 Heterogeneity analysis based on loan dependency

A bank–firm lending relationship is a prerequisite for banking sector liberalisation to drive corporate adoption of sustainable development principles and ESG improvements. Consequently, the ESG-enhancing effects of removing foreign ownership restrictions may vary with firms’ loan dependency. Following He et al. (2024), loan dependency is measured as the ratio of bank loans to total assets to examine whether the ESG effects of banking liberalisation differ across firms with varying loan dependency levels. The sample is categorised by industry and year, median loan dependency is calculated for each group, and a loan dependency dummy variable (Ld) is constructed. Firms with loan dependency above the industry-year median are classified as high loan dependency (Ld = 1); others are designated as low loan dependency (Ld = 0). Subgroup analyses are performed. Columns (5) and (6) of Table 6 show that the banking liberalisation policy exerts a statistically significant positive effect on ESG performance for high-loan-dependency firms (coefficient = 0.7546, p < 0.01). The effect is insignificant for low-loan-dependency firms (coefficient = −0.0417, p > 0.10). A between-group coefficient difference test shows significantly different coefficients between groups. Banking sector liberalisation more significantly improves ESG performance for high-loan-dependency firms.

6 Further analysis

6.1 Moderating effect of public environmental concern

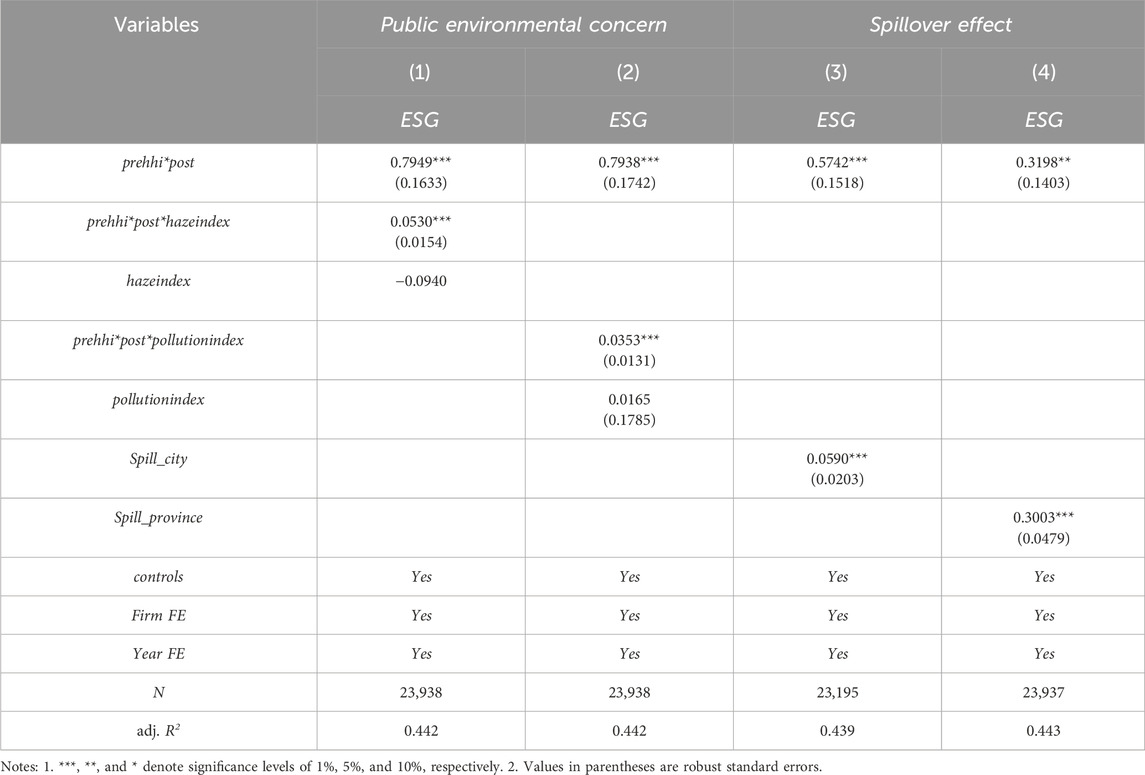

In China, implementing environmental policies entails a vertical game of strong central supervision–weak local implementation. Public environmental concern is an important informal institution and a powerful complementary social force created through new media and other forms of enterprise monitoring, including banks. This informal monitoring power may prompt banks to incorporate public pressure facing firms into environmental risk assessments underlying their credit decisions, amplifying the ESG improvement effect of banking sector openness. Thus, the moderating effect of social environmental concern is tested. Following Wu et al. (2022), the Baidu search haze (hazeindex) and environmental pollution (pollutionindex) indices in each province are used to proxy public environmental concerns. The cross-multiplier terms between them and banking liberalisation policy are incorporated into the regression model. Regardless of whether public environmental concern is measured by hazeindex or pollutionindex, public environmental concern positively moderates banking liberalisation’s ESG improvement effect. The greater the public environmental concern, the more significant banking liberalisation’s promotion effect on corporate ESG performance (Table 7, columns (1) and (2)).

Table 7. Further analysis.

6.2 Spillover effect

Corporate ESG performance involves peer pressure to some extent. Therefore, specific companies’ ESG practices may prompt other companies in the same region to adjust their production and operational decisions, improving their ESG performance. Referring to Song et al. (2024) and incorporating the average ESG scores of other companies in the same city (Spill_city) or province (Spill_province), a benchmark regression is performed to test for spillover effects. Columns (3) and (4) of Table 7 show that the coefficients of Spill_city and Spill_province are significantly positive at the 1% level; thus, the ESG improvement driven by banking sector liberalisation has certain spillover effects. Following banking sector liberalisation, companies improve their ESG practices, driving other companies in the same city or province to enhance their ESG performance.

7 Research conclusion and implications

Against the backdrop of accelerating global climate governance, whether banking liberalisation improves enterprises’ ESG performance is a key policy issue for emerging economies aiming for green transitions. This study utilises the exogenous event of China’s 2018 removal of foreign ownership restrictions in the banking sector to construct a generalised DID model, exploring whether and how banking sector liberalisation improves corporate ESG performance. Firms’ motivations for ESG performance improvement are examined from a market forces perspective, while the moderating effects of informal institutional factors (social environmental protection awareness) on liberalisation policy effectiveness are also considered.

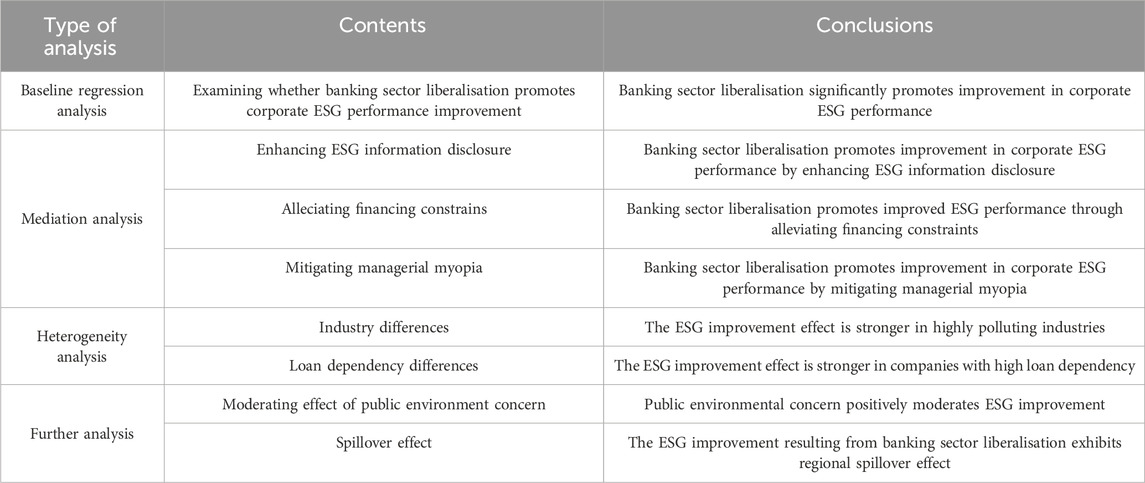

This study finds that corporate ESG performance improves significantly after removing foreign ownership restrictions in the banking sector. Mechanism tests reveal that banking sector liberalisation primarily promotes corporate ESG practices through three mechanisms: improving ESG disclosure, alleviating financing constraints, and curbing managerial myopia. Heterogeneity analysis shows that banking sector liberalisation has stronger ESG-enhancing effects in firms in heavily polluting industries or with high loan dependency. Further analysis indicates that public environmental concern positively moderates ESG improvement, The greater the public environmental concern, the more significant banking liberalisation’s promotion effect on corporate ESG performance. Additionally, the ESG improvement effect of banking sector liberalisation has a regional spillover effect, with companies improving their ESG performance promoting other companies in the same city or province to enhance ESG performance. Table 8 summarises the key conclusions of this paper. This study expands research on how financial liberalisation promotes corporate ESG performance and enriches findings on the motivations underlying corporate ESG practices. The conclusions provide important empirical evidence and policy implications for emerging economies such as China, particularly those with banking-dominated financial systems, for enhancing corporate ESG performance through financial institutional reforms, thereby driving green and low-carbon economic transformation.

Table 8. Reserch conclusions.

This study’s conclusions have important policy implications. First, promote greater openness and guide the banking industry to better serve the broader goal of sustainable development. Banking liberalisation is at the forefront of financial liberalisation. It not only brings international capital that favours ESG criteria but also introduces sustainable development concepts, encouraging enterprises to improve their ESG practices. The government should leverage the power of international capital to promote a higher level of opening-up and guide the banking sector to better facilitate sustainable development to promote sustainable economic development.

Second, accelerate ESG rating system standards refinement and promote ESG audit assurance service development. Prevalent rating divergences stemming from selective disclosure, greenwashing, inconsistent evaluation criteria, and quality variances in rating methodologies may distort banks’ assessments of corporate ESG performance, undermining the ESG improvement facilitated by banking sector openness. Therefore, regulatory authorities should prioritise the institutionalisation of a unified ESG rating framework through top-down policy design to standardise market practices. Concerted efforts are needed to cultivate an ESG audit assurance ecosystem by harnessing professional third-party verification capacities, thus substantially enhancing the reliability and comparability of corporate sustainability disclosures.

Third, strengthen the promotion of sustainable development concepts and guide attention towards environmental protection. This study indicates that banking sector liberalisation has more pronounced effects on ESG improvement in regions with greater public environmental protection awareness and in heavily polluting industries. Given the urgency of green and low-carbon transition, the government should promote green development concepts, provide public environmental protection education, and encourage enterprises, government agencies, and the public to form a consistent green development philosophy. This will further leverage banking sector liberalisation’s ESG improvement effects and promote sustainable economic development by establishing a sound institutional ecosystem.

This paper has the following limitations, which are worth further exploration in the future:

1. The paper measures corporate ESG performance using third-party ESG ratings. Although the measurement error risks inherent in ESG ratings and specific to China’s emerging markets were thoroughly discussed, and attempts were made to mitigate these risks through robustness tests, the issue was not fully resolved due to limitations imposed by the specific stage of development and data availability. Future research could explore the integration of more diverse ESG data sources or conduct more in-depth measurement and analysis once China’s ESG disclosure system and rating framework become more mature and robust.

2. When examining the role of corporate ESG disclosure, the study uses a counting metric based on the number of disclosure items related to stakeholders’ social responsibility fulfilment in corporate social responsibility reports to measure the level of corporate ESG disclosure. While this method is transparent, clear, and effective in distinguishing ESG performance metrics, it struggles to capture the depth and quality of disclosure. Future research could conduct in-depth analysis of corporate social responsibility reports to distinguish between the level of detail and clarity of ESG information disclosure, rather than simply whether disclosure occurs or not, thereby developing more specific ESG information disclosure measurement indicators.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Author contributions

YL: Writing – original draft, Software, Writing – review and editing, Formal Analysis, Conceptualization. HL: Methodology, Project administration, Writing – review and editing, Funding acquisition. ZiG: Software, Writing – review and editing. ZhG: Writing – review and editing, Investigation, Software.

Funding

The author(s) declare that financial support was received for the research and/or publication of this article. This research was funded by the Shaanxi Provincial Social Science Foundation Project (Grants No. 2023D034), and the National Social Science Fund Project (Western Region Project) (Grants No. 24XJY017).

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Generative AI statement

The author(s) declare that no Generative AI was used in the creation of this manuscript.

Any alternative text (alt text) provided alongside figures in this article has been generated by Frontiers with the support of artificial intelligence and reasonable efforts have been made to ensure accuracy, including review by the authors wherever possible. If you identify any issues, please contact us.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Footnotes

1Note: China’s commercial banks primarily fit into four categories: state-owned commercial, joint-equity commercial, city commercial, and rural commercial. State-owned and joint-equity commercial banks, characterised by more advanced operational philosophies and robust institutional frameworks, had initiated internationalisation earlier, achieving higher levels of internationalisation prior to the implementation of the policy. Rural commercial banks primarily serve local agricultural households and micro-enterprises, exhibiting structural disparities with listed enterprises (large and medium-sized enterprises) in financing needs and operational scales. City commercial banks, due to their lower valuations and better growth prospects, have been more significantly impacted by the policy change lifting restrictions on foreign ownership in the banking sector. Therefore, this section uses city commercial banks as an example to illustrate the impact of this policy on Chinese commercial banks. Among China’s 19 city commercial banks, Bank of Beijing and Bank of Guiyang were excluded because of severe data unavailability regarding foreign shareholders. Statistical analyses were conducted on the average foreign ownership ratios of the remaining 17 city commercial banks from 2017 to 2023.

2The selection basis and results of high-pollution industries in the analysis of industry heterogeneity are as follows:The Ministry of Environmental Protection’s 2010 Environmental Information Disclosure Guidelines for Listed Companies (Exposure Draft) classified 16 industries as heavily polluting sectors, including thermal power, steel, cement, electrolytic aluminum, coal, metallurgy, chemicals, petrochemicals, building materials, papermaking, brewing, pharmaceuticals, fermentation, textiles, tanning, and mining. Building upon this framework and incorporating the industry codes from the China Securities Regulatory Commission’s 2012 Industry Classification Guidance for Listed Companies, we have systematically screened and identified the following 19 heavily polluting industries: “Non-metallic Mineral Products Manufacturing,” “Non-metallic Mining and Dressing,” “Textile Industry,” “Alcohol, Beverages & Refined Tea Manufacturing,” “Electric Power, Thermal Production and Supply,” “Metal Products Manufacturing,” “Petroleum Processing, Coking & Nuclear Fuel Processing,” “Non-ferrous Metal Smelting & Rolling Processing,” “Chemical Raw Materials & Chemical Products Manufacturing,” “Rubber & Plastic Products Manufacturing,” “Chemical Fiber Manufacturing,” “Petroleum & Natural Gas Extraction,” “Ferrous Metal Mining & Dressing,” “Non-ferrous Metal Mining & Dressing,” “Paper & Paper Products Manufacturing,” “Coal Mining and Washing,” “Ferrous Metal Smelting & Rolling Processing,” “Textile & Apparel Manufacturing,” and “Leather, Fur, Feather & Related Products, and Footwear Manufacturing.”

References

Angkinand, A. P., Sawangngoenyuang, W., and Wihlborg, C. (2010). Financial liberalization and banking crises: a cross-country analysis. Int. Rev. Fin. 10, 263–292. doi:10.1111/j.1468-2443.2010.01114.x

Arminen, H., Puumalainen, K., Pätäri, S., and Fellnhofer, K. (2018). Corporate social performance: inter-industry and international differences. J. Clean. Prod. 177, 426–437. doi:10.1016/j.jclepro.2017.12.250

Ashbaugh-Skaife, H., Collins, D. W., and Lafond, R. (2006). The effects of corporate governance on firms’ credit ratings. J. Acc. Econ. 42, 203–243. doi:10.1016/j.jacceco.2006.02.003

Bai, J., Carvalho, D., and Phillips, G. M. (2018). The impact of bank credit on labor reallocation and aggregate industry productivity. J. Fin. 73, 2787–2836. doi:10.1111/jofi.12726

Barber, B. M., Morse, A., and Yasuda, A. (2021). Impact investing. J. Financ. Econ. 139, 162–185. doi:10.1016/j.jfineco.2020.07.008

Beck, T., Levine, R., and Levkov, A. (2010). Big bad banks? The winners and losers from bank deregulation in the United States. J. Fin. 65, 1637–1667. doi:10.1111/j.1540-6261.2010.01589.x

Bian, Y., Wu, L., and Bai, J. (2019). Does high-speed rail improve regional innovation in China? J. Financ. Res. 6, 132–149.