Jing Zhang

Jing Zhang- School of Economics and Management, Ningde Normal University, Ningde, Fujian, China

Introduction: China achieved significant economic growth in the past two decades, and the sustained economic growth also brings negative implications for the environment. The Chinese government has introduced various fiscal reforms to mitigate the negative implication of the environment in the economy. Modernization of China's governance system and improvement of social development were the main goals of the 14th Five-Year Plan.

Methods: Literature combing method and Chart analysis method.

Result: Artificial intelligence promotes the efficiency of bonded governance environment and boosts national management modernization.

Discussion: This paper suggests that the artificial intelligence construction of the environmental protection tax system improves tax collection and management, tax payment service, and tax management. In addition, the government should adopt other strategies to promote a clean environment, such as tax exemption for green and cleaner production. Easy loans should be provided to the exports, especially those contributing to clean energy production.

1 Introduction

The fourth Plenary Session of the 19th CPC Central Committee emphasized on modernizing China’s governance system, and social development and tax reforms were the main goals of the 14th Five-year Plan. Implementing a modern governance system ensures tax reforms that could increase government revenue and mitigate the burden on people. Economic development increases the income of the people, helps achieve economic goals, and brings environmental challenges such as environmental pollution and environmental degradation (Ullah et al., 2022; Zeeshan et al., 2022). The Chinese government implemented various reforms to achieve sustainable environmental goals, such as pollution tax and green energy production (Wingender, 2018; Tan et al., 2022). In order to improve eco-environmental governance and accelerate the process of modernizing national governance, Big Data and information technology are integral parts of the national governance system. China introduced an environmental protection tax system in 2018 for ecological protection and environmental pollution control. Improvements and developments based on artificial intelligence can help modernize ecological environment governance by making it an influential policy tool (Faúndez-Ugalde et al., 2020). China began to investigate and implement tax information as early as the 1980s. After 30 years, the information system represented by the “Golden Tax Project” has progressed to its fourth phase (Xing and Whalley, 2014). The goal of the fourth phase of the Golden Tax Project is to promote the modernization of tax administration-based intelligent taxation. The environmental protection tax can rely on the experience and conditions of the development of the existing “Golden Tax Project,” which significantly improves the information and intelligence of tax categories and solves the problem of difficult measurement and monitoring of pollutant emissions. Therefore, this paper aims to illustrate the application of artificial intelligence in the environmental protection tax system.

Description of the research process: From the perspective of artificial intelligence optimization tax system construction, this paper discusses how to improve the environmental protection tax with the help of artificial intelligence technology. First of all, the paper analyzes the specific changes in pollutant discharge fee after it was changed into environmental protection tax, and the main research results after the current fee was changed into tax to provide a theoretical basis for sorting out the shortcomings of environmental protection tax. Second, the shortcomings of the environmental protection tax are analyzed from the perspective of tax principle, tax neutrality, tax substantive law, and tax procedural law. Then, based on the analysis of the existing problems of the environmental protection tax, the construction and improvement path of the environmental protection tax is discussed from the perspective of artificial intelligence. Finally, we focus on the future challenges of environmental protection tax.

This paper contributes to the literature in the following aspects: First, the paper summarizes and evaluates the changes and research emphases after the change in environmental “fee to tax.” As an important environmental regulation measure, environmental protection tax is an important tool to improve the ability of ecological environmental protection and governance. The study of its change and development is of great significance to the study of environmental protection tax reform and the improvement of the tax system. Second, the research perspectives of the environmental protection tax from the perspective of taxation principle should be expanded. Environmental protection tax comes from the reform of “fees” and has many characteristics of fees, so the purpose of environmental protection tax is significantly different from that of other taxes. The improvement and development of environmental protection tax and other taxes have a great difference, and from the perspective of taxation principle analysis, it can theoretically promote the construction of the environmental protection tax. Third, from the perspective of artificial intelligence to explore the environmental protection tax improvement path. The development of artificial intelligence technologies such as Big Data, Internet, blockchain, and cloud computing can solve the difficulties in environmental protection tax accounting, measurement, detection, and monitoring; make up for the deficiencies of existing measurement technologies and methods; provide quality of tax data; and improve the efficiency and effect of tax collection and management.

2 Review of literature

2.1 Specific changes of environmental “Fee to Tax”

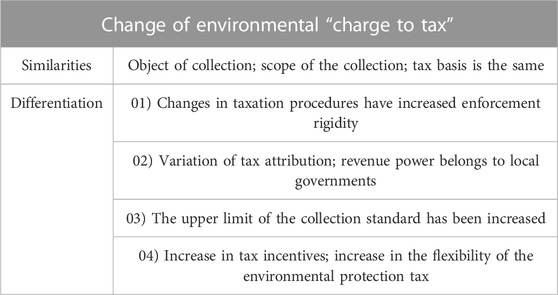

The current environmental protection tax is based on the reform of pollutant discharge fees, and it is basically the same in terms of the objects to be collected, the scope to be collected, and the basis for calculating taxes (fees). In order to not increase the tax burden of enterprises and smoothly promote the reform of fees and taxes, local governments basically adopt the principle of “Tax Burden Translation” to design tax rates (Lianchao et al., 2021). Therefore, there is no substantial difference between the current environmental protection tax and “Sewage Charge.” The main reasons for the change are endogenous law enforcement, low charging standards, and insufficient incentive effect on enterprises (Guo Junjie et al., 2019). It is anticipated that the system of the Environmental Protection Tax Law can be constructed and gradually improved through legislation to achieve the purpose of emission reduction and pollution control and improvement of ecological environment quality.

2.1.1 The main changes after the change of environmental charges are reflected in the following aspects

The first one is to increase the rigidity of law enforcement (Table 1). The collection procedure has been changed from “Environmental Protection Billing and Enterprise Payment” to “Tax Collection and Management, Enterprise Declaration, Environmental Protection Monitoring, Information Sharing, and Collaborative Governance.” The form of the collection was changed from “Fee” to “Tax,” which strengthened the enforcement of the environmental protection tax and confirmed its legal status. Tax collection and management, environmental monitoring, multi-department participation, law enforcement, and supervision occurred at the same time. It reduces the degree of local government intervention in tax collection, reduces the possibility of enterprise rent-seeking, reduces the risk of lax law enforcement, and can show the incentive of the environmental protection tax on enterprise economic behavior (Table 1).

TABLE 1. Changes before and after the introduction of environmental tax.

Second, the upper limit of the collection standard has been increased. The upper and lower limits of environmental protection tax collection standards have been set, and the upper limit has been increased. The specific standards for collecting the environmental protection tax by regions are set by local governments and submitted to the National People’s Congress for approval and filing. Statistics show that 42 percent of the 31 provinces where the environmental protection tax has been implemented have raised the tax collection standard (Li Yue, 2021). In the Beijing–Tianjin–Hebei region, Jiangsu, and Shanghai and Henan provinces, the tax rate is five to 10 times higher than the minimum rate (TIAN Cui-Xiang,et al., 2021). It reflects the standard of adjusting measures to local conditions, gives room for tax collection adjustment, and gives full consideration to the level of regional ecological and economic development, while increasing the intensity of collection and incentive.

Third, the environmental protection tax has increased the number of tax exemptions and exemptions and preferential tax policies. The motto that says “one size fits all” should be avoided, the environmental protection tax should be made more specific to enterprises, and more incentive should be provided. As stipulated in the Environmental Protection Tax Law, if the concentration of taxable pollutants or water pollutants discharged by taxpayers is less than 30% of the national and local pollutant discharge standards, the environmental protection tax shall be reduced by 75%; and if the concentration is less than 50%, then the environmental protection tax shall be reduced by 50% to encourage enterprises to lower their pollutant discharge standards.

2.2 Literature review of environmental effects after tariff change

2.2.1 Domestic scholars focused on the following aspects after the introduction of environmental protection tax

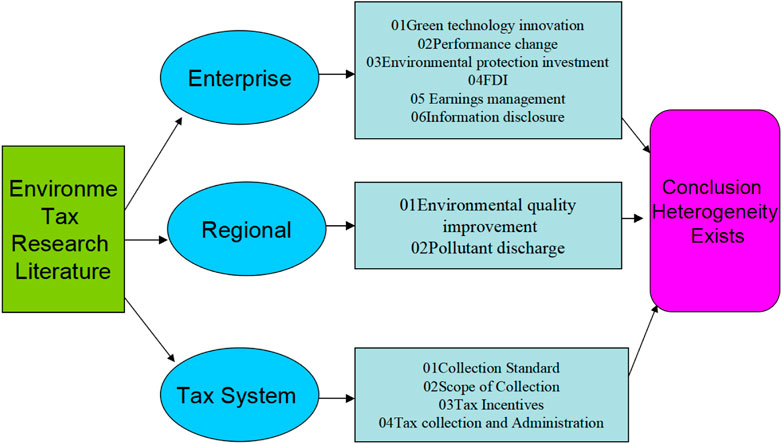

One example is the impact of environmental protection tax on enterprises (as Figure 1). First, the impact of environmental protection tax reform on enterprise environmental technology or green technology innovation: scholars took A-share listed companies in Shanghai and Shenzhen stock markets, A-share industrial listed companies in Shanghai and Shenzhen stock markets, enterprises in specific regions (such as the Yangtze River Delta, the Yangtze River Economic Belt, and the Beijing–Tianjin–Hebei region), clean production enterprises, and non-clean production enterprises as samples to analyze the impact of environmental protection tax reform on technological innovation. The basic conclusion is that the environmental protection tax reform has a positive incentive effect on green technology, which can promote the green transformation of heavily polluting enterprises and the production transformation of non-clean production enterprises, and the green innovation effect of large enterprises is significantly better than that of small and medium-sized enterprises. Second, the impact of environmental protection tax reform on enterprise performance capacity: the research on analyzing the effect of enterprise performance is mainly performed to compare the changes in enterprise performance before and after the implementation of the environmental tax, such as LONG Feng et al. (2021) and Xiao-Guang Liu et al. (2021). They concluded that there are differences: the former think green taxes on business performance are influenced by the institutional environment, favorable in the institutional environment in the eastern area, and green taxes have an inhibitory effect on corporate performance in the short term or think that green taxes impact on corporate performance, affected by technological innovation. In addition, technological innovation has a mediating effect, and environmental tax has little fluctuation on enterprise performance in the short term. Third, the impact of environmental protection tax reform on enterprises’ investment in environmental protection: Tian Lihui et al. (2022) believed that the environmental tax reform effectively improves the environmental protection investment of heavily polluting enterprises. The preventive environmental protection investment is more effective than the political environmental protection investment. The promotion effect of environmental protection investment of non-state-owned enterprises and small-scale enterprises is more significant. Niu Xiaoye et al. (2021) believed that the collection standard and enforcement intensity of the environmental protection tax affect enterprises’ environmental protection investment. Other scholars analyzed the impact of environmental protection tax reform on enterprises’ FDI, earning management and information disclosure (Figure 1).

FIGURE 1. Literature analysis of research results of environmental protection tax.

The second is the impact of the environmental protection tax on regional environmental protection and pollution control. In this part of the research, most scholars take provinces or economic zones as the main samples, select some taxable pollutant data, empirically analyze the data of several years before and after the introduction of the environmental protection tax, and test and analyze the effect of the environmental protection tax on emission reduction and pollution control. Xue Gang et al. (2020) selected the emissions of air pollutants and water pollutants to analyze the effect of environmental tax. They concluded that China’s environmental tax and pollutant emissions show an “inverted U” model, and the current tax collection standards find it difficult to achieve the goals of emission reduction and pollution control. Zhu Xinling et al. (2020) made an empirical analysis of environmental tax data in the Yangtze River Economic Belt considering tax effectiveness and tax timeliness and suggested that environmental tax had a positive promoting effect on regional economic development, which could reduce resource consumption and pollutant emissions, but its influence had a time lag. Lu Hongyou et al. (2019) used quasi-environmental tax data to study the double dividend of environmental tax in prefect-level cities. They believed that the collection of sulfur dioxide had an emission reduction effect on their pollution. According to the literature review, there are relatively few analyses on the effects of environmental protection tax reform on regional emission reduction and pollution control, which will be one of the focuses of future environmental tax reform research.

Third, the improvement and promotion of environmental protection tax revenue elements: the environmental protection tax is shifted from the sewage charge, which has deficiencies in many aspects. The concern of tax authorities and researchers is to improve the environmental protection tax system and enhance its collection effect. At present, most scholars believe that the current environmental protection tax has some problems, such as too low collection standards, too narrow a scope of taxation, and inappropriate tax preferential and reduction policies. The Research Group of “New- Era Public Finance and Tax Policy Reform Promoting Green Development” (2020) considers that volatile organic compounds and solid waste disposal should be included in the scope of collection. Xue Gang et al. (2020) believed that carbon dioxide, persistent organic matter, and household waste treatment should be included in the scope of collection. Huwei et al. (2020) showed that the adjustment of the environmental protection tax levy standard has a positive significance on enterprises’ green technology innovation engine oil and has a more prominent effect on high-pollution industries and cities with strong policy implementation. The Research Group of “New- Era Public Finance and Tax Policy Reform Promoting Green Development” (2020) suggested that the identification of tax preference and tax deduction should be set differently according to the local reality.

Fourth, environmental protection tax collection and administration: pollutant discharge fees are mainly collected and used by environmental departments. The environmental protection department is responsible for the substantive identification of the nature and quantity of pollutants, and its work efficiency is directly related to the amount of the environmental protection tax collected by the tax department. At present, most scholars believe that the factors affecting the efficiency of environmental protection tax collection are lack of synergy between the environmental protection department and the tax department, lack of cooperation mechanism, and insufficient tax collection and management. In order to ensure coordination and efficiency of collection and management cooperation, the problems such as unclear cooperation orientation, unreasonable allocation of responsibilities, and unknown incentive measures should be solved in cross-department cooperation (LIN Wei, 2021). Due to the limitations of technology, capacity, and equipment, tax authorities are unable to substantially review the data provided by environmental protection departments, which is inconsistent with the original intention of setting tax authorities as the main and environmental protection departments as the auxiliary in environmental tax legislation. If environmental protection departments do not cooperate or taxpayers seek rent, the efficiency of collection and management will be affected.

From the literature review, the main methods used by scholars to study the environmental protection tax are the dual difference and triple difference formula. Xue Gang et al. (2020), Zhu Xinling et al. (2020), and Lu Hongyou et al. (2019) investigated the environmental tax on air pollution. However, tax efficiency and mechanism of the environmental tax implementation are not discovered in the previous literature. Therefore, this study uses artificial intelligence in the environmental protection tax system. Furthermore, it provides more robust estimations and policy recommendations such as efficiency of taxation, especially from the perspective of taxation principle. The application of artificial intelligence provides robust results and policy implications. Improvements in the quality of tax data, as well as in the efficiency and effectiveness of tax collection and management, are all partly attributable to implement the artificial intelligence technologies like Big Data, the Internet, blockchain, and cloud computing, which have been developed to address problems with environmental protection tax accounting, measurement, detection, and monitoring by adjusting for the shortfalls of existing measurement technologies and methods.

3 Environmental protection tax and the angle of taxation principle

3.1 Quantitative interest taxation principle

Western tax theory believes that taxpayers benefit from public services at different levels of welfare, the level of tax payment should match their benefit level, and the benefit should be the basis to judge the fairness of tax payment Verboon et al. (2009 and Edmund (1986). The quantitative interest taxation principle and quantitative energy taxation principle are the secondary principles of the principle of tax fairness (SU Ri-sha,2020). The quantifiable taxation principle focuses on whether the tax paid by taxpayers can meet the financial needs, while the quantifiable taxation principle focuses on the extent to which taxpayers benefit and pays the state fees or consideration. The main purpose of the environmental protection tax is environmental protection, supplemented by increasing fiscal revenue. From this point of view, the environmental protection tax is more suitable for the quantitative interest taxation principle. Ye Jinyu (2019) analyzed the significance of the existence of Environmental Protection Tax Law from the perspective of the imputation mechanism and accrual mechanism to make up for the absence of tort law and environmental law. The imputation mechanism determines the tax object and tax subject of the environmental protection tax, and the accrual mechanism determines the measurement performance of the environmental protection tax. Due to the particularity of the environmental protection tax, the traditional tax basis based on accounting standards cannot effectively measure pollution emissions. The professionalism and complexity of the measurement based on the amount of emissions or decibels increases, and the measurement of the benefit degree of environmental protection tax is subject to advanced technology and a perfect system.

3.2 Neutral taxation principle

Tax neutrality is the basis for determining tax efficiency. Western taxation defines tax neutrality as taxation that should not affect the original resource allocation of the private sector. As tax is a means of government intervention in the economy, tax neutrality has become an ideal theory. In reality, tax neutrality is emphasized to reduce the interference degree of tax on the economy as much as possible and reduce the excess burden of tax payment on the subject of negative tax. From the perspective of sewage discharge fee, it belongs to the category of “usage fee,” that is, the public authority collects fees from beneficiaries of public facilities according to law, which has the characteristics of special funds and special use, which is opposite to those of the principle of tax neutrality. The nature of the environmental protection tax has not changed significantly after the “fee to tax.” It can also be said that the idea of special funds for the environmental protection tax is not in line with the principle of tax neutrality, which will affect the efficiency of environmental protection tax collection. In addition, the environmental protection tax is regressive, that is, the taxpayer’s environmental protection tax burden has a diminishing marginal propensity to consume. The low-income group bears more tax burden due to the elasticity of commodity demand than the high-income group, and the poor group bears environmental protection tax burden due to the income difference than the rich group (LIN Xingyang, 2021). The regressive character of the environmental protection tax directly leads to the loss of tax fairness, which seriously deviates from tax neutrality principle.

3.3 Substantive tax law

The tax entity factors will affect the scope, object, burden transfer, destination, and efficiency of the environmental protection tax and then affect the accumulation of human capital and economic growth. As the current environmental protection tax is a shift from the sewage charge tax, its tax scope and tax standard have not changed much. Taking the Taxation Standard as an example, the environmental protection tax rate should not be too low, which cannot give full play to the efficiency of the environmental protection tax and deviates from the purpose of environmental protection tax. However, if the environmental protection tax rate is too high, it will reduce the enthusiasm of enterprises to participate in economic activities and inhibit economic growth. Wei Sichao et al. (2020) proposed that the rate of the environmental protection tax should achieve the goal of maximizing social welfare, to promote the transformation from the maximization of economic output to the maximization of social welfare (the specific formula is designed as follows, 5–7). B represents the level of production technology; K represents physical capital; L represents labor, capital, and labor elasticity coefficient related to total output; R represents the interest rate; and W represents wages. Then, we consider the maximization of steady-state social welfare to take the derivative, while proving that the goal of economic maximization is not equal to the goal of social welfare maximization, and deduce the optimal tax rate formula. However, there is no uniform standard for tax rates, Wang Youxing et al. (2016), and the design formula is as follows (8). The denominator is pollution equivalent, and the numerator represents the cost of environmental governance. The author believes that the upper and lower limits of the tax rate can be designed, and the upper limit takes tax burden, economy, and employment factors into account. The lower limit considers the direct cost and opportunity cost (formula 9). However, in general, the reasonable environmental tax rate is helpful to promote the coordinated governance of pollution reduction and carbon reduction.

In 2019, China’s environmental protection tax accounted for .14% of the total tax revenue. The average proportion of the environmental protection tax in European and American countries was more than 2% of the total tax revenue. The empirical data show that there is still room for increasing the current environmental tax rate in China. The establishment of tax rate should be combined with regional environmental carrying capacity, ecological pollution and treatment, economic and social development level, etc., to establish the corresponding tax rate for different industries and achieve sustainable development of the regional ecological economy. In addition, due to the complexity of taxable items, the environmental protection tax has higher professional requirements on the identification of tax objects, detection of taxable pollutants, and calculation of tax burden. Artificial intelligence is needed to improve the accuracy of identification, detection, and calculation to improve the effect of environmental protection tax collection.

3.4 Tax procedure law

Tax legislation not only needs to consider its ability to increase fiscal revenue and its impact on economic activities but also needs to pay attention to the tax costs generated in the process of tax collection. The government's ideal tax design should be to obtain sufficient revenue with a small tax cost, that is, to achieve the efficiency of the tax system. Western taxation includes administrative cost, compliance cost, and political cost in tax expenses. The purpose of tax collection and administration is to realize the efficiency of tax collection at a lower cost. As a new tax, the environmental protection tax has no practical experience in tax collection. There are differences between environmental protection and tax departments in terms of work content, working methods, and professional background and the inconsistency of rights and obligations in the current environmental protection tax collection process. It results in serious information asymmetry of environmental protection tax collection, ultimately resulting in the omission, under-collection, and wrong collection of the environmental protection tax. The environmental protection tax has a strong professional accounting of taxable pollutants. Tax collection and management informatization can improve the standardization of data processing, solve the professional requirements of tax-related indicators and calculation methods, improve the professional judgment ability of tax-related information of tax departments, and enhance the strength and effectiveness of tax collection and management. At present, the basic level of tax collection, management, and payment services is not high. Tax authorities can build an information sharing platform with the help of artificial intelligence to increase environmental protection tax collection and payment services and monitor public opinion on environmental protection tax.

4 Improve the design of environmental protection tax from the perspective of artificial intelligence

4.1 Artificial intelligence and tax modernization

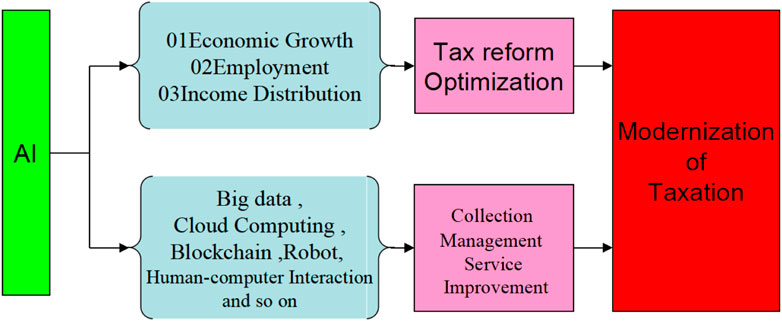

Artificial intelligence in economic growth (Kromann et al., 2011; D Autor et al., 2018), labor force employment (Sarah Bankins1CA1,2021; Amisha Bhargava et al., 2021), and income distribution, Ullah et al. (2020) (T Gries et al., 2020; A Goyal et al., 2020) has a direct effect on social economy. Driven by artificial intelligence, tax modernization has entered a stage of rapid development. In 2021, China launched the fourth phase of the Golden Tax Project. The logical relationship of artificial intelligence to tax modernization is shown in Figure 2. The specialization and complexity of environmental protection tax put forward new requirements for artificial intelligence. The collection, identification, sorting, and analysis of tax-related data can standardize the workflow of tax personnel with the help of machine learning, pattern recognition, and human–computer interaction technologies and significantly improve their efficiency.

FIGURE 2. Effects of artificial intelligence on tax modernization.

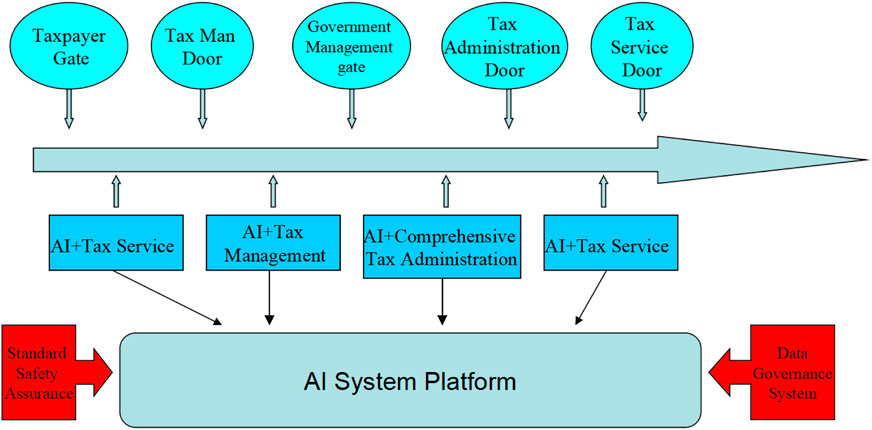

Based on the aforementioned analysis, this paper attempts to form the perspective of artificial intelligence, improve the environmental protection tax design and environmental protection tax information construction goals in the safety standard system and data management system, and implement environment tax efficiency between stakeholders, tax services, tax administration, and intelligent tax management, as shown in Figure 3.

FIGURE 3. Environmental protection tax information construction objectives.

4.2 Artificial intelligence and environmental protection tax system improved

First of all, the problems reflected by the principle of volume benefit taxation and the principle of tax neutrality of environmental protection tax must be solved. We can draw lessons from the advanced experience of foreign countries and adopt the way of coordinated taxation with other taxes. From the perspective of the development of the environmental protection tax system in developed countries, in the beginning, most countries only levied taxes on certain specific pollutants. With economic development and social demand, many countries began to impose taxes on two or more types of pollutants. For example, the Eco-tax in the United States covers taxes related to individual consumption, such as automobile fuel charges and corporate resource extraction taxes. These taxes are reflected in China’s consumption tax and resource tax. Therefore, in order to reduce double taxation, environmental protection tax can be levied in coordination with other related taxes.

Second, for tax object recognition: using Big Data, accurate recognition of artificial intelligence in government, business, services, and other taxable objects, based on dynamic input information through various channels, such as centralized data processing, the identification is taxable natural area distribution of the pollutants, taxable enterprise mode of production, taxable personal way of life, etc, we extract the main cause set of taxable pollutant discharge. Data processing of these external information and internal tax information can increase the recognition of taxpayers. On this basis, we established environmental protection tax files and card data for enterprises and gradually built the environmental protection tax information resource database.

Then, there is the problem of low levy standards. Because the current environmental protection tax collection standard is shifted to the sewage charge, the time span of the establishment of the sewage charge standard is too long, and the guiding significance for the current social and economic development is insufficient. Local governments can use Big Data analysis of artificial intelligence, cloud computing, and blockchain to obtain data related to the tax area, for example, natural resource endowment, ecological environment quality, economic and social development level, taxable enterprises, and taxable pollutants. To realize the differentiation of environmental tax rate standards, we gradually increased the lower limit of environmental tax rate and set multiple targeted preferential tax rates to increase the tax incentive effect.

Finally, we considered the tax burden transfer, destination, efficiency, and other issues. We can learn from foreign environmental tax collection methods to optimize. For example, the United States follows emission trading, supplemented by environmental taxes; Russia uses the form of ecological fund to collect pollutant tax; Germany has a relatively perfect eco-tax system; and British tax department and environmental protection department division of labor and cooperation.

4.3 Artificial intelligence and tax collection and administration of environmental protection tax

This study suggests artificial intelligence (IA) for the analysis, the IA is a significant tool that evaluates the complex problem and provide optimal solution. Following are the main reasons for using IA essential for this study; first, artificial intelligence will refine environmental tax data. Information is the starting point of tax source management. Artificial intelligence can help tax collection departments collect, screen, analyze, and transfer data related to taxable pollutants from massive tax-related information. The “Golden Tax Phase iii” intelligent information system project has replaced experiential management decision by Big Data analysis decision. On this basis, the environmental protection tax can promote the tax department and the environmental department to integrate the information resources and technological advantages of the province and build the exchange and sharing system of pollutant discharge and treatment data. The basic contents of the system shall include the data index specification, data exchange system, and data sharing system for the discharge of taxable pollutants and environmental treatment. Part of the index specification is mainly compiled in accordance with the work requirements of environmental quality of the national ecological environment force and the work management requirements of environmental protection tax collection by the State Administration of Taxation. The content should cover the specific accounting indicators and monitoring methods of taxable pollutants and provide reference value as data samples. The data exchange system is mainly used to realize data sharing, especially the particularity of environmental protection tax requires environmental departments and tax departments to cooperate in collecting, to ensure the accuracy and timeliness of data.

The data sharing system can improve the efficiency of environmental protection tax collection.

Second, artificial intelligence reduces the asymmetry of tax-related information. The environmental protection tax involves complex tax objects and requires strong professional requirements for the detection, measurement, and accounting of taxable pollutants, which requires the cooperation of ecological environment authorities. The cooperation efficiency of departments is affected by the allocation of rights and responsibilities and information communication. The data exchange and sharing system of pollutant discharge and treatment can realize timely communication of data flow among departments. Specifically, cloud video and voice can be used to accurately deploy taxable pollutant discharge and treatment work, and artificial intelligence can be used in the form of application software. In addition, it is necessary to clarify the rights and obligations of tax authorities and ecological and environmental authorities. Environmental monitoring, data collection, data review, and other work also need a lot of resource consumption. The corresponding tax can be allocated based on the role and effect of the ecological environment department in the tax collection process.

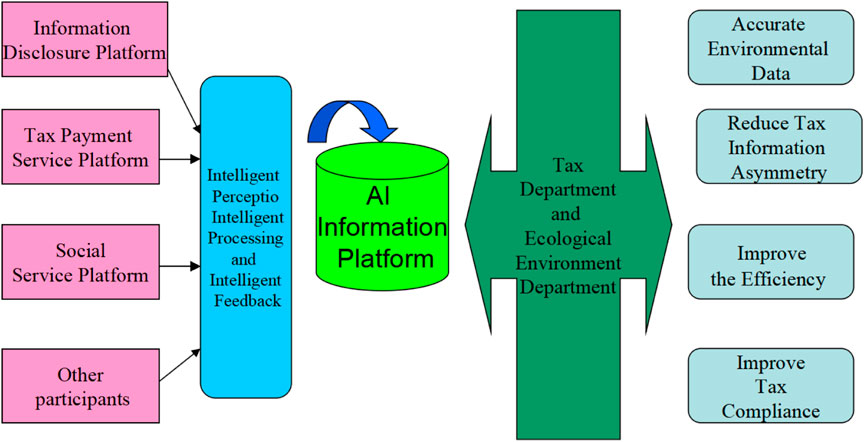

Third, artificial intelligence can improve the efficiency of environmental protection tax collection and management. At present, tax administration adopts the online and offline mode mixed management, but in practice, the efficiency of tax collection and management is low due to the impact of tax collection cost and tax efficiency of tax authorities. In particular, due to the limitation of various factors, the accuracy of detection and calculation of taxable pollutant data of environmental protection tax is low, and the efficiency of tax collection and management is not ideal. The artificial intelligence information platform by using intelligent perception, intelligent processing, and intelligent feedback based on three key links integrates and feedbacks fragmented tax-related information to improve the accuracy of taxable pollutant data monitoring. Using the database of multiple data types, we identified the false information of taxable objects, obtained the new trends of the discharge and treatment of taxable pollutants in a timely manner, and comprehensively supervised the collection efficiency and tax effect of the environmental protection tax. Also, artificial intelligence could improve tax compliance. The construction of the tax-related information sharing platform of the environmental protection tax can accurately manage the risk of tax-related behaviors and reduce tax evasion and tax avoidance behaviors of taxpayers when the risk cost of tax evasion increases. Artificial intelligence simplifies the tax declaration process of environmental protection tax, reduces the cost of tax declaration, and enhances the willingness of taxpayers to pay. Artificial intelligence can actively publicize and popularize the knowledge of taxation and ecological environment, improve citizens’ awareness of taxation and environmental protection, and improve their willingness to comply with tax payment. In addition, various forms of the government transfer payment can be adopted. For example, the tax rebate and other special expenses will be used to encourage taxable enterprises to install automatic online monitoring equipment to provide accurate environmental protection tax data.

The concrete framework structure is shown in Figure 4.

FIGURE 4. AI and environmental protection tax governance.

4.4 Artificial intelligence and tax payment service of environmental protection tax

Tax payment services should be designed according to the characteristics of the environmental protection tax. Figure 5 shows the design process.

FIGURE 5. AI and environmental protection tax payment services.

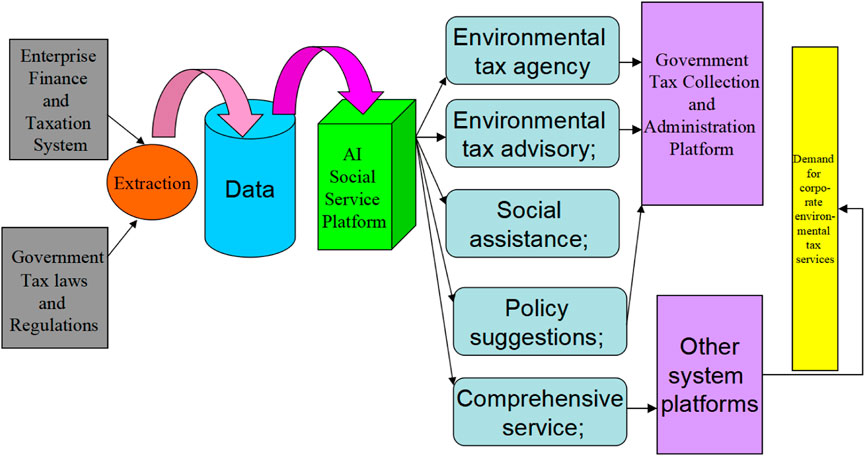

First, artificial intelligence can improve the efficiency of tax services. In the tax payment service, some cadres could not meet the demand of tax payment due to lack of patience and objective data integration ability. Blockchain technology can connect the collection platform of the Department of Affairs with the financial management platform of taxpayers and the service platform of social service organizations into a comprehensive service platform integrating information collection, analysis, feedback, and decision-making. Taxpayers can access round-the-clock all-inclusive environmental protection tax services powered by artificial intelligence technology. It can not only avoid the emotional tax service providers but also obtain reliable information services, reduce the difficulty of tax declaration, and improve the efficiency of tax management.

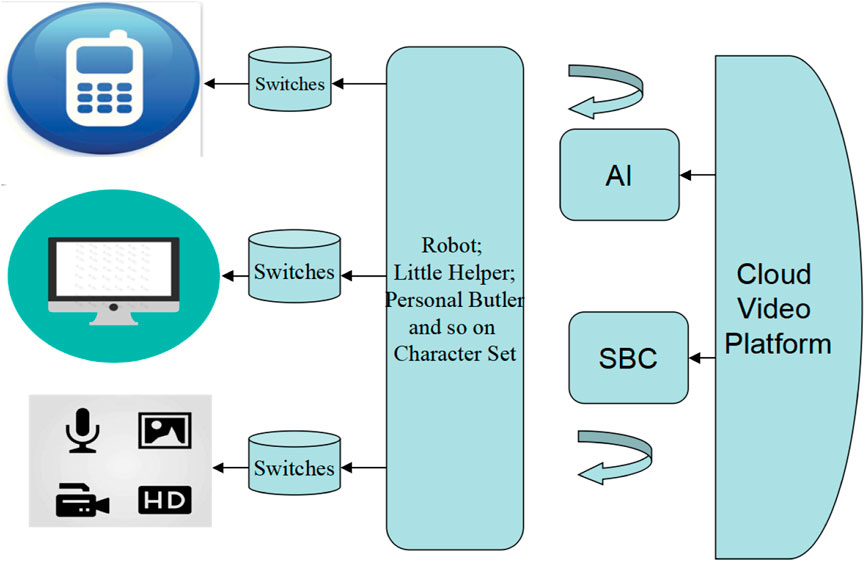

Second, artificial intelligence can reduce the negative impact of asymmetric tax information. The speed of data flow is critical in the information age. The cloud video platform can be built with the help of artificial intelligence technology to realize the link between government agencies at all levels in the province and combine pollutant discharge and ecological governance system with the video system. It can connect with the national ecological and environmental departments upward and can connect with the provincial municipal, county, and township ecological and environmental management departments or institutions downward to realize the visual communication of ecological and environmental governance instructions and tax policy information, as shown in Figure 6. Users of environmental protection tax information can use mobile phone clients, PC clients, and multimedia terminals to connect to the cloud video platform to achieve smooth information communication. In addition, the robot, small assistant, personal butler, and other roles are set to help users answer questions, understand customer information needs, early warning of tax risks, and grasp the real-time dynamic information of environmental protection tax. It can not only meet the tax payment needs of users but also improve the government’s supervision of users and ultimately reduce the information asymmetry between taxpayers and tax authorities.

FIGURE 6. Cloud video platform.

Finally, artificial intelligence can improve the accuracy of tax services. The powerful information processing capacity and machine algorithm analysis of artificial intelligence can quickly analyze and integrate massive tax-related information, match the requirements of tax-related information users more accurately, and provide intelligent tax consultation and tax-related services. Users can obtain information by means of multiple terminals, realize information service acquisition anytime and anywhere by means of a portable mobile service platform, and track the whole process of service process, which can improve service efficiency and supervision efficiency. Blockchain technology can help solve the problem of the invisibility and uncertainty of environmental tax data. The various service ends connected by the Internet provide various communication channels for pollutant discharge and environmental governance information, which not only improves tax payment services but also better publicizes and popularizes tax information, contributing to the improvement of tax awareness of the whole people.

5 Artificial intelligence and tax governance of environmental protection tax

First, artificial intelligence can improve the level of tax governance. Information is the basis of the tax administration process, and the application logic of information determines the efficiency of tax administration. The application of artificial intelligence technology in tax collection and management is an inevitable requirement to improve the level of tax administration. The purpose of environmental protection tax is to reduce the discharge of taxable pollutants and improve the ability of ecological environmental governance. The main reasons why the current environmental protection tax has no obvious effect on environmental governance are unreasonable collection standards, narrow collection scope, and ineffective tax collection and management. According to the aforementioned analysis, artificial intelligence can solve these problems. In addition, artificial intelligence uses computer processing technology to evaluate and monitor the efficiency of regional environmental protection taxes and the progress of the treatment of taxable pollutants.

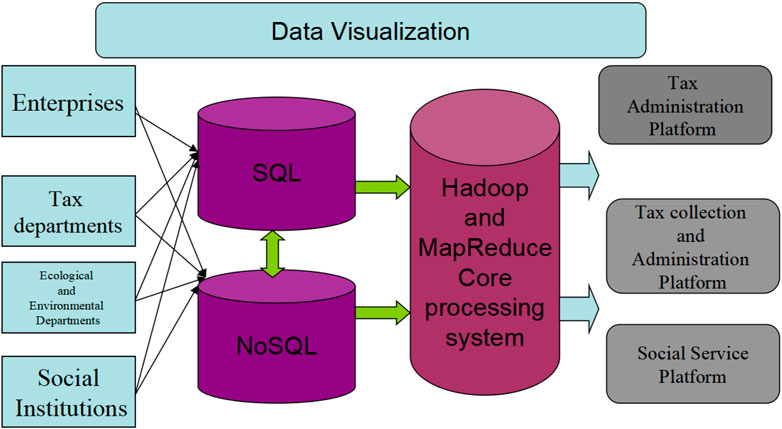

Second, artificial intelligence can strengthen tax risk control. Artificial intelligence can use Hadoop and MapReduce to construct a computing and processing ecosystem for Big Data ecological pollution control. With HDFS and Hbase as the data core systems, artificial intelligence uses SQL and NoSQL to store data, meeting the requirements for structured data processing and processing diversified data formats such as files, images, and logs (as shown in Figure 7). Information security has become a problem that artificial intelligence must pay attention. Tax departments can develop a special information security management platform and risk management platform by relying on their own technical forces. The former monitors and prevents security threats brought by AI applications, while the latter tracks hotspots and trends in the field of tax risks in time. They can perceive significant risks in tax risk management and implement tax risk response. Third, artificial intelligence can improve the supervision efficiency of environmental protection tax. We used Big Data information technology, GIS technology, and new media information technology for construction of the tax-related information dynamic tracking system. The accuracy of taxable pollutant data monitoring should be improved by screening massive amounts of taxable pollutant information, environmental governance information, and tax-related information of industries and enterprises. At the same time, dynamic monitoring of tax-related activities, tax-related activities, tax-related industries, and enterprises will be implemented. Multi-directional and multi-level monitoring can identify the new trends in the discharge and treatment of taxable pollutants and comprehensively improve the efficiency and treatment effect of environmental protection tax.

FIGURE 7. Environmental protection tax governance data system.

Considering the professional requirements of environmental protection tax testing, measurement, accounting, and monitoring and the level of economic and social development, we can vigorously promote the neutral testing business of third-party professional institutions. It can not only reduce the cost of small- and medium-sized enterprises to purchase testing equipment but also guarantee the fairness, justice, and openness of tax information with the independence of the third party and improve the quality and efficiency of tax collection and administration. Tax authorities may strengthen supervision over third-party testing institutions in terms of technical guidance, qualification assessment, archives management, and industry self-discipline. Third-party professional monitoring organizations can use artificial intelligence to realize policy guidance, information exchange, dynamic monitoring, etc., to ensure the authenticity and reliability of tax-related information.

6 Conclusion and prospects

This paper analyzes the application of artificial intelligence in environmental protection tax from four perspectives: tax system improvement, tax collection and management, tax payment service, and tax administration. The conclusion is that artificial intelligence can improve the improvement and construction of the environmental protection tax system, improve the efficiency and effect of environmental bonded tax collection, and promote the realization of the fundamental purpose of environmental protection tax. It can promote the realization of the fundamental purpose of the environmental protection tax, which is an important component of the construction of the environmental protection tax and the construction of the future tax system. The application of artificial intelligence technology in environmental protection tax collection, service, and governance needs to pay attention to its challenge to the current tax system. First, artificial intelligence has higher requirements for the intelligent tax system, including information architecture design, information management, hardware and software resource allocation, and professional and technical personnel. Second, relevant tax legal system norms have not been established, so relevant applicable norms should be added to the Tax Collection and Administration Law. Third, the tax authorities should strengthen the cooperation with tax-related service organizations, construct the information sharing center of the tax industry, and better realize the service and collection of the environmental protection tax. Fourth, to promote a green environment, government should also give corporate tax reductions to those industries which adopt renewable energy in the production process. Fifth, the government may provide easy access to the credit to the firms who have good tax record, which motivates the producers to participate in the tax collection activity. Sixth, from the tax revenue, the government may compensate those industries which are affected from the environmental degradation, such as agriculture and fisheries. In addition, government should raise the public’s awareness of environmental protection, actively promote policy publicity through Internet platforms, set up special lines for environmental tax business, and answer questions related to the environmental tax in a timely manner. This paper has some limitations; first, this study covers only environmental tax using artificial intelligence, which can be further expanded by adding other methods. Second, this paper is only related to one country, which can be applied to many countries’ cases. Third, the study did not add the institutional aspects to the tax system; and institutional aspects can be added in future research in the tax system Deborah Knirsch (2007), Liu and Shao, 2021, Zijie, 2020.

Data availability statement

The datasets presented in this study can be found in online repositories. The names of the repository/repositories and accession number(s) can be found in the article/Supplementary Material.

Author contributions

The author confirms being the sole contributor of this work and has approved it for publication.

Funding

This work was supported by Collaborative Innovation Center and Innovation Team of Ningde Normal University (Project No.2022T12), and Ningde Normal College university-level special Research Projects under the Funding Scheme (Project No. 2022ZX313).

Conflict of interest

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors, and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Autor, D., and Salomons, A. (2018). Is automation labor-displacing? Productivity growth, employment, and the labor share[J]. Brookings Pap. Econ. Activity 2018 (7), 1–87. doi:10.1353/eca.2018.0000

Bankins1Ca1, S (2021). The ethical use of artificial intelligence in human resource management: A decision-making framework. Ethics Inf. Technol. 23 (4), 841–854. doi:10.1007/s10676-021-09619-6

Bhargava, A, Bester, M, and Bolton, L (2021). Employees’ perceptions of the implementation of robotics, artificial intelligence, and automation (RAIA) on job satisfaction, job security, and employability. J. Technol. Behav. Sci. 6 (6), 106–113. doi:10.1007/s41347-020-00153-8

Deborah, K. (2007). Measuring tax distortions with neutrality-based effective tax rates. Rev. Manag. Sci. 1 (2), 151–165. doi:10.1007/s11846-007-0012-8

Edmund, S. P. (1986). Profits Theory and Profits Taxation (Theorie des benefices et imposition des benefices) (Teoria y tributacion de las utilidades). IMF Staff Pap. 33 (4), 674–696. doi:10.2307/3867213

Faúndez-Ugalde, Antonio, Rafael, Mellado-Silva, and Aldunate-Lizana, Eduardo (2020). Use of artificial intelligence by tax administrations: An analysis regarding taxpayers’ rights in Latin American countries. Comput. Law Secur. Rev. 38, 105441. doi:10.1016/j.clsr.2020.105441

Goyal, A., and Aneja, R. (2020). Artificial intelligence and income inequality: Do technological changes and worker's position matter?[J]. J. Public Aff. (9), 1–10.

Gries, T., and Naude, W. Artificial intelligence, income distribution and economic growth[J]. VfS Annual Conference 2020 (Virtual Conference): Gender Economics. 2020(8), 1–72.

Guo, J, Fang, Y, and Yang, Y (2019). Does China's pollution levy standards reform promote emissions reduction?[J]. J. World Econ. 11 (12), 121–144. doi:10.3390/su11216186

Hu-wei, W, and Qi-ming, Z. Environmental protection taxes and green technology innovation of enterprises--- evidence from the adjustment of pollution charges standard in China[J]. J. Guizhou Univ. Finance Econ. 2020 (3), 91–100.

Kromann, L., Skaksen, J. R., and Srensen, A (2011). Automation, labor productivity and employment -a cross country comparison[J]. ResearchGate (6), 1–16.

Li, Yue (2021). Research on the effect of fiscal policy on environmental governance in China[D]. Liaoning University. doi:10.3389/fenvs.2022.1006272

Lian, C, Zhang, W, and Qian, B. I. (2021). Can the reform of environmental protection fee-to-tax promote the green transformation of high-pollutingenterprises?-evidence from quasi-natural experiments implementedin accordance with the Environmental Protection TaxLaw[J]. China Popul. Resour. Environ. 31 (5), 109–118. doi:10.1016/j.jclepro.2022.132287

Lin, W (2021). Cross-sector collaboration: The cooperation mechanisms of environmental protection TaxCollection and management[J]. J. south China normal Univ. ( Soc. Sci. Ed. (4), 152–164+208.

Lin, X (2021). Coordination path of the taxation neutral principle from the perspective of environmental tax[J]. J. Beijing Inst. Technol. Soc. Sci. Ed. (2), 131–140.

Liu, X, and Shao, R (2021). Environmental protection tax, technological innovation and corporate financial performance-A study based on the difference-in-differences method[J]. J. Industrial Technol. Econ. (9), 24–30.

Long, F, Ge, C. Z, Lin, F, Lian, C, Bi, F, and Hu, T (2021). Impact of environmental protection Taxon corporate performance based on tax rate increase[J]. Chin. J. Environ. Manag. (5), 127–134+60.

Lu, H, Liu, Q, Xu, X, et al. (2019). Can Environmental Protection Taxachieve‘reducing pollution’and‘economic growth’?[J]. China Popul. Resour. Environ. 29 (6), 130–137.

Research Group of (2020). ‘New- Era Public finance and tax policy reform promoting green Development’.An evaluation of environmental protection taxat two-YearAnniversary and improvement suggestions[J]. Fiscal Sci. (11), 31–44.

Ri-sha, S. U. (2020). The justification and application of the principleof taxation based on quantity and benefit in tax law[J]. Tax. Econ. (6), 73–79.

Tan, Z, Wu, Y, Gu, Y, Liu, T, Wang, W, and Liu, X (2022). An overview on implementation of environmental tax and related economic instruments in typical countries. J. Clean. Prod. 330, 129688. doi:10.1016/j.jclepro.2021.129688

Tian, C, and Sun, R(2021). Analysis of the policy effect of fee-to-tax reform on heavy pollution enterprises[J]. Account. Finance (1), 62–66+79.

Tian, L, Guan, X, Zheng, L, and Xin, L (2022). Reform of environmental protection fee-to-tax and enterprise environmental protection investment:A quasi-natural experiment based on the implementation ofthe environmental protection TaxLaw[J]. J. Finance Econ. M (4), 1–17.

Ullah, I, Alam, R, Svobodova, L, Akbar, A, Shah, M. H, Zeeshan, M, et al. (2022). Investigating relationships between tourism, economic growth, and CO2 emissions in Brazil: An application of the nonlinear ARDL approach. Front. Environ. Sci. 10, 52. doi:10.3389/fenvs.2022.843906

Ullah, I, Qian, X, Shah, M. H, Alam, R, Ali, S, and Ahmed, Z (2020). Forecasting wages inequality in response of trade openness in Pakistan: An artificial neural network approach. Singap. Econ. Rev., 1–16.

Verboon, P., and Heerlen, (2009). The role of fairness in tax compliance. Neth. J. Psychol. 4, 136–145. doi:10.1007/bf03080136

Wang, Y (2016). Study on the design of environmental protection tax rate and regional floating standard[J]. Contemp. Finance Econmics (11), 23–31.

Wei, Sichao, and Fan, Zijie (2020). Study on the optimal Environmental Protection Taxrate in the high-quality development stage in China[J]. China Popul. Resour. andenvironment 30 (1), 57–66.

Xiao-ye, N, Liu, H, and Zhi-wen, C. A. O. (2021). An empirical study on the impact of sewage charge tax change on enterprise environmental protection investment [J]. Friends Account. (12), 75–81.

Xing, W, and Whalley, J (2014). The Golden Tax Project, value-added tax statistics, and the analysis of internal trade in China. China Econ. Rev. 30, 448–458. doi:10.1016/j.chieco.2014.05.005

Xue, G, Ming, H, and Liu, Y (2020). The "inverted U" effect of environmental protection tax on emission reduction and pollution control: Based on the calculation of regional levy intensity [J]. Tax Econ. Res. (3), 25–34.

Ye, J (2019). Interpretation, enactment and operation of the principle of volume benefit taxation of environmental tax [J]. Law Sci. (3), 74–91.

Zeeshan, M, Han, J., Ullah, I., Afridi, F. E. A., and Fareed, Z. (2022). Comparative analysis of trade liberalization, CO2 emissions, energy consumption and economic growth in southeast asian and Latin American regions: A structural equation modeling approach. Front. Environ. Sci. 10, 79. doi:10.3389/fenvs.2022.854590

Zhu, X, Lan-jing, H. E., and Xiao-cao, L. I. U. (2020). Can environmental tax promote regional green development---empirical evidence from the Yangtze River Economic Belt. J]Journal statistics (6), 45–59.

Keywords: ecological, environmental protection tax, artificial intelligence, profit tax amount, tax administration

Citation: Zhang J (2023) Optimization of the environmental protection tax system design based on artificial intelligence. Front. Environ. Sci. 10:1076158. doi: 10.3389/fenvs.2022.1076158

Received: 21 October 2022; Accepted: 12 December 2022;

Published: 06 January 2023.

Edited by:

Zeeshan Fareed, Huzhou University, ChinaReviewed by:

Irfan Ullah, Nanjing University of Information Science and Technology, ChinaAbid Khan, Nanjing University of Information Science and Technology, China

Copyright © 2023 Zhang. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Jing Zhang, dDEyMTZAbmRudS5lZHUuY24=