Yuzhong Zhou

Yuzhong Zhou Liming Wang2

Liming Wang2- 1School of Business Administration, Zhejiang Gongshang University, Hangzhou, Zhejiang, China

- 2School of Economics, Shandong University of Technology, Zibo, Shandong, China

- 3School of Economics, Shanghai University, Shanghai, China

- 4Business School of Yunnan University of Finance and Economics, Kunming, Yunnan, China

- 5School of Computer Science, Huanggang Normal University, Huanggang, Hubei, China

The start-up period is the most difficult period for enterprises to survive and innovate. How will government subsidies affect the innovation efficiency of enterprises in the start-up period? And, is there any heterogeneity? The academic research is still relatively preliminary and controversial. This study adopts the cash flow method to screen a sample of start-ups from Chinese GEM, STAR Market and SME board-listed companies from 2010 to 2020 for empirical research. The study found that financial subsidies can generally promote the innovation efficiency of start-ups, but there is also significant heterogeneity by industry, region and whether the subsidies are sustainable. Financial subsidies generally have a signaling effect that facilitates startups to attract external capital, and this effect is most significant in the industrial sector. Overall, fiscal decentralization negatively regulates the effect of subsidies on the innovation efficiency of start-ups, especially in the public utilities and industrial sectors. The government subsidies are relatively insignificant to improve the innovation efficiency of start-up enterprises in non-first-tier cities, especially in small and medium-sized cities, and the multiplier effect is relatively small. The effect of non-sustainable subsidies is not significant because they cannot produce a long-term mechanism and thus are difficult to influence future expectations and decisions. The subsidy effect is not significant in other industries outside the industrial sector, and the lower the level of industry competition, the weaker the signaling effect of enterprise credit, the less conducive to its access to external innovation resources to enhance innovation efficiency through the signaling effect of government subsidies. Moreover, financial decentralization does not improve the innovation efficiency of government subsidies as expected, but weakens the innovation efficiency of fiscal subsidies for start-up enterprises in general. The study proposed that the government (especially the small and medium-sized city government) should optimize the business environment and financial capital allocation, change the supervision and management mechanism, improve the efficiency of capital utilization and reduce the crowding out effect. The government’s subsidy policy should be further standardized and refined.

1 Introduction

Enterprises are the main body of scientific and technological innovation activities, and their innovation is characterized by long-term and high-risk, which requires continuous capital investment. As the basis for improving the innovation ability of enterprises, R&D investment is an essential means for enterprises to obtain competitive advantages. Small and medium-sized science and technology start-up enterprises are important supports for China’s economic resilience and the backbone of industrial transformation and upgrading. However, financing difficulties are still an important problem plaguing their innovation and upgrading, especially for start-up enterprises, and capital has become the key problem in their development (Wang and Yang, 2022). Neoclassical economics believes that R&D activities have strong positive externalities, so governments worldwide tend to strengthen the positive external effects by encouraging enterprises to innovate independently through economic policies such as financial subsidies. For a long time, the Chinese government has continuously increased its support for enterprises science and technology innovation, and a set of policy support systems, including government R&D subsidies and tax incentives, have been established from the central level to the local government level (Chen and Tian, 2020). Taking listed companies as an example, the total government subsidies reached 40.035 billion yuan in 2010, and the enterprises receiving subsidies accounted for 89% of the listed companies. By 2020, subsidies will rise to 211.6 billion-yuan, accounting for 98.45% of the listed companies. Whether the huge financial subsidies positively impact enterprise innovation, what is the effect and how to increase effectiveness? There is still a controversy in the academic community.

Based on the enterprise life cycle perspective, scholars have conducted studies on different aspects of the impact of fiscal subsidies on enterprise innovation and obtained different conclusions. Howell (2017) empirically studied the subsidy policies of the US government for start-up and growing enterprises and confirmed that such subsidies effectively stimulated the innovation activities of relevant enterprises Howell (2017) and Hou and Song, (2019) used the panel data of Chinese listed high-tech enterprises to study the impact of financial incentives on enterprise innovation and found that fiscal incentives in different life cycles of firms maintained a positive incentive effect, in which the fiscal subsidy effect showed an overall upward trend with the change of enterprise life cycle (Hou and Song, 2019). Duan and Yang, 2020) have taken private technology-based enterprises listed on China’s small and medium-sized boards as research samples and found that government subsidies had a significant incentive effect on the innovation intensity of private technology-based enterprises in the growth and mature periods, but had no significant impact on the innovation intensity of private technology-based enterprises in the start-up and recession periods (Duan and Yang, 2020). Chen and Tian (2020) conducted an empirical study with Chinese GEM-listed companies. They showed that government R&D subsidies have a significant promoting effect on the innovation efficiency of enterprises in the growth and mature periods, a weaker promoting effect on enterprises in the start-up periods, and a significant inhibiting effect on the innovation efficiency of enterprises in the recession (Chen and Tian, 2020). Yu and Wang (2022) took China’s A-share listed companies as samples. They found that financial subsidies have a significant incentive effect on the innovation of enterprises in the growing period but have no significant positive impact on the innovation of enterprises in the mature and declining periods (Yu and Wang, 2022). In summary, it can be seen that for different research samples and subjects, the effect of fiscal subsidies on innovation in different life cycle stages of firms does not yield universal results.

Based on the enterprise life cycle theory, this study elects the start-up enterprises listed on GEM, STAR Market, and SME board as the research objects and purposefully studies the heterogeneous characteristics of financial subsidies on start-up enterprises and their effects on innovation efficiency in different regions, industries, and whether they are continuous or not, which is important for the structural optimization of government financial subsidies. As the existing relevant studies are mainly carried out for A-share listed companies, there are fewer comprehensive studies on SME Board, STAR Market and GEM listed companies, and the findings of the studies only for the situation of A-share listed companies may not be directly applicable due to their special characteristics. Therefore, it is necessary to study the impact and heterogeneity of financial subsidies on the innovation efficiency of start-up companies listed on the SME Board, STAR Market and GEM.

2 Theoretical analysis and research assumptions

2.1 Financial subsidies and innovation efficiency of start-up enterprises

The improvement of the innovation ability and efficiency of enterprises in the start-up period is of great significance to the high-quality development of enterprises in the future (Liu and Wu, 2021), especially for small and medium-sized scientific and technological enterprises. As start-ups are committed to transforming laboratory technology into applied results, they have problems of high risk, long profitability cycle and information asymmetry, and face the real dilemma of difficult and expensive financing, so they usually need more preferential government policies and financial support in the early stage of life cycle, among which financial subsidies are an important choice for governments at all levels due to their flexibility and targeting. However, there are two different theoretical perspectives on the impact of financial subsidies on the innovation efficiency of start-up firms.

The first view is that financial subsidies cannot substantially impact the improvement of innovation efficiency of start-up enterprises. Because of the low product awareness and market credibility, as well as the lack of R&D experience and weak technological innovation system, startups have significant business risks, and R&D innovation is a long-term process, so in the startup period, the funds received by firms will be more inclined to sustain their survival and other project expenditures. In addition, some scholars pointed out that the government’s improvement of innovation performance of small and medium-sized enterprises may come from indirect influence, and a direct relationship with enterprises may not be the optimal way (Huang, et al., 2016). Xie (2010) also argues that there is no correlation between the “business-government” collaborative innovation network and the innovation performance of small and medium-sized enterprises, which cannot directly affect enterprise innovation (Xie, 2010). Therefore, the financial subsidies in this period may not significantly promote enterprises’ innovation efficiency.

The second view is that financial subsidies significantly impact the innovation efficiency of start-up enterprises.

Both the resource dependence theory and the signaling theory argue that financial subsidies alleviate firms’ resource constraints of enterprises through direct financial support and indirect signaling. At the same time, the financial subsidy is more like a booster that increases the firms’ risk acceptance and affordability, thus managing their innovation. Although startups are short of funds, they have the advantage of a strong innovation spirit and innovative vitality, are more sensitive to the market and are easy to win with innovation. Therefore, the infusion of financial resources can become their innovation support, generating help in funding, management, and strategy, thus promoting the improvement of the innovation level. (Liu and Wu, 2021) study on the innovation efficiency of Chinese entrepreneurial enterprises during the start-up period also showed that the government should provide more preferential policies for startups and develop personalized policies for different industries to promote the innovation efficiency of startups (Liu and Wu 2021). Therefore, financial subsidies can promote the innovation efficiency of startups. Based on the above analysis, the following two opposing hypotheses are proposed.

H1: Financial subsidies can significantly improve the innovation efficiency of start-up enterprises;

H2: Financial subsidies cannot significantly improve the innovation efficiency of start-up enterprises;

2.2 Heterogeneous impact of financial subsidies on innovation efficiency of start-up enterprises

Cities are naturally heterogeneous, and the impact of financial subsidies on the innovation of enterprises at the start-up stage in different cities is bound to differ. In general, large cities such as first-tier cities have higher levels of economic development, better financial systems, and complete hardware and software facilities such as talents to support enterprise innovation. They tend to rely on science and technology for development. Under this environment, the government’s financial subsidies can effectively reduce the financing constraints of start-up enterprises, provide more funds for enterprise innovation, and more easily release the multiplier effect of fiscal policy, thus promoting the innovation efficiency of enterprises.

For small and medium-sized cities, the external economic environment faced by small and medium-sized scientific and technological enterprises has yet to be improved, and the “signal effect” released by financial subsidies is not apparent. Therefore, enterprises will be more cautious about carrying out such high-investment, high-risk, and slow-reward activities during the start-up period, so small and medium-sized scientific and technological enterprises located in small and medium-sized cities may not respond positively to the government’s fiscal policy (Li and Shi, 2021). Based on this, hypothesis 3 is proposed in this study.

H3: The impacts of financial subsidies on the innovation efficiency of start-up enterprises will show certain urban heterogeneity due to the different cities to which the enterprises belong.

Financial subsidies play an important role in alleviating the risks and unknowns of enterprise R&D as well as reducing financing constraints and compensating for market failures. Aschhoff (2009) pointed out that if the sustainability of government funding for R&D projects is stronger, the stronger the government funding is, the enterprises will be willing to increase their R&D investment and thus improve their innovation capacity (Aschhoff, 2009). However, the government’s financial subsidies are not completely inclusive policies. Only enterprises with good development prospects and certain competitiveness can obtain them, and they must go through the procedures such as enterprise application and government assessment. If enterprises can continuously receive government subsidies, innovation-conscious enterprises will also take the initiative to increase their R&D investment, improve their innovation capacity and efficiency, and increase the possibility of receiving financial subsidies again. For the government to reduce the cost of errors, compared with the first application for financial subsidies and other enterprises that have successfully applied for subsidies many times, the government is more inclined to choose the former, which is easy to form a vicious circle and Matthew effect. Therefore, when the subsidy policy lacks continuity, especially for small and medium-sized science and technology innovation enterprises, they still reduce their innovation activities to avoid risks. Based on the above analysis, hypothesis 4 is proposed in this study.

H4: The continuity of financial subsidies positively impacts the innovation efficiency of startups. Continuous financial subsidies will significantly impact expectations more than one-off subsidies to guide investment decisions and form a long-term impact mechanism, which can strengthen the effect of R&D subsidies, alleviate the financing pressure of startups, and improve innovation efficiency.

3 Study design

3.1 Data source and description

This study selects listed enterprises listed on China GEM, STAR Market, and SME Board from 2010 to 2020, and excludes ST, *ST category, financial companies and companies with missing severe key data as the research objects, and excludes st, St, financial companies, and enterprises with a severe lack of key data, and all data are subject to a 2.5% upper and lower tailing process. The fiscal decentralization data used in this paper is from the China Statistical Yearbook (2011–2021), and all other data are from Wind and CSMAR databases. The data samples are unbalanced panel data due to the discontinuity of fiscal subsidies received by enterprises and the partial absence of other data.

3.2 Definitions of variables and measurements

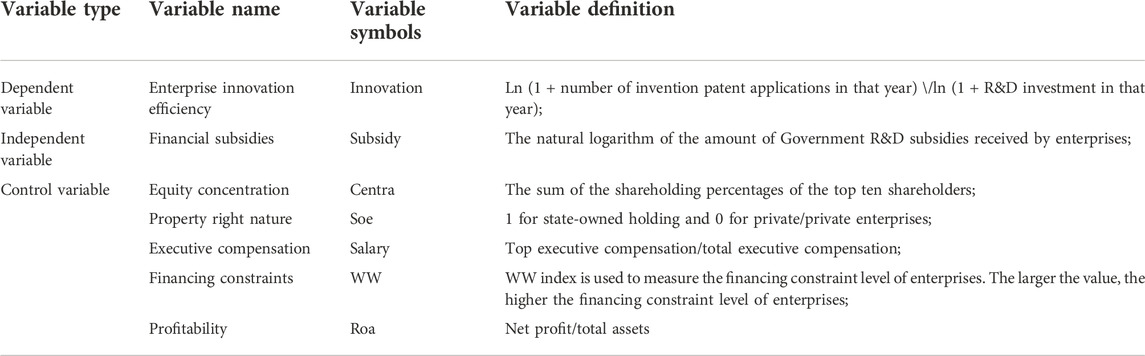

3.2.1 Explained variable

Enterprise innovation efficiency. Most of the existing literature measures the innovation efficiency of enterprises from the perspective of the patent application and R&D investment. Still, this measurement standard cannot accurately analyze the innovation capability of enterprises, and the data of the DEA model based on data envelopment analysis from the perspective of input and output to measure the efficiency of decision-making units is difficult to obtain. Therefore, this paper uses the practice of Shi and Li, (2021) to measure enterprises’ innovation efficiency by the ratio of the number of patent applications and the R&D capital investment.

3.2.2 Explanatory variable

Financial subsidy. This study takes reference from the practices of Yang et al. (2015), Zheng et al. (2019), and Yu and Wang (2022), Howell (2017), and takes the logarithm of the raw subsidy value.

3.2.3 Control variables

Referring to the existing studies of Wang and Yang (2022), Lin et al. (2015), Tong and Wei (2016), and Shi and Xie (2015), this study selects equity concentration, property right nature, executive compensation, financing constraint index and profitability as control variables.

3.2.4 Enterprise life cycle

This paper uses the classification and combination of cash flow to find enterprises in the start-up period. The cash flow composition method was first proposed by Dickinson (2011). The enterprise development is divided by observing the enterprise’s operating cash flow, investment cash flow, and financing cash flow.

The whole financial information set of the enterprise is reflected by the cash flow agency model, which can fully reflect the enterprise’s profitability, resource allocation ability, and cash status, avoiding the determination of the enterprise’s life cycle by a single metric. The specific division of the enterprise’s life cycle is shown in Table 1.

TABLE 1. Division method of enterprise life cycle.

According to the above conditions, the start-up enterprises were divided, and a total of 1763 valid data of Listed Companies in the start-up period. The data are mainly from Wind and CSMAR databases, with some missing data supplemented accordingly through the annual reports of some enterprises. Table 2 shows the definition and measurement summary of main variables. Table 2 shows the definition and measurement summary of main variables.

TABLE 2. Summary of definitions and measures of main variables.

3.3 Model setting

To test the impact of financial subsidies on the innovation efficiency of start-up enterprises, this paper constructs a panel fixed effect model for regression analysis Eq. 1.

where i represents the enterprise, t represents the year, λt represents the individual fixed effect at the enterprise level, and vt represents the time fixed effect at the year level. µ is error term, assumed to be normally distributed at zero mean value (Razzaq et al., 2019; Razzaq et al., 2021; Zhang et al., 2022) and constant variance (Elahi et al., 2021a; Elahi et al., 2022b; Elahi and Khalid, 2022).

4 Results

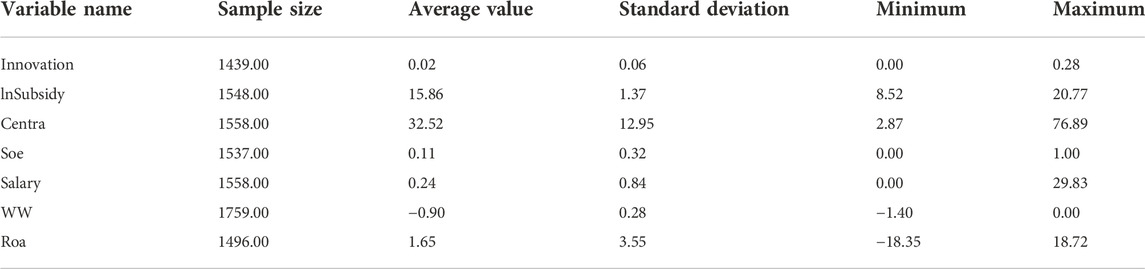

4.1 Descriptive statistics

To understand the numerical characteristics of specific variables, this study conducts a descriptive statistical analysis of the samples, as shown in Table 3. In this paper, the variables are also tested for multicollinearity, with a mean of 1.05 and a maximum of 1.15 (consistent with a mean of less than five and a maximum of less than 10), excluding interference from multicollinearity.

TABLE 3. Descriptive statistics of variables.

4.2 Benchmark regression results

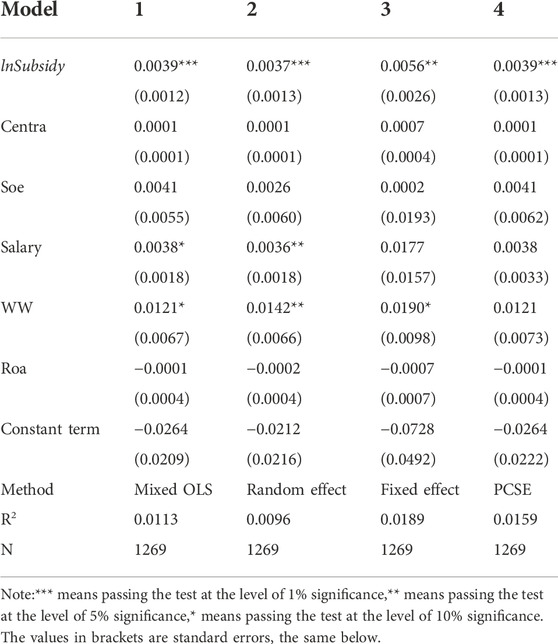

To test the hypothetical relationship between financial subsidies and innovation efficiency of start-up enterprises in the theoretical analysis, the paper first selects four estimation methods, namely mixed OLS, fixed effect model, random effect model, and PCSE model, to estimate all enterprise samples. Among them, the PCSE model is the estimation method of Panel Corrected Standard Errors (PCSE) proposed by Beck and Katz (1995), which can effectively deal with complex panel error structures, such as synchronous heteroscedasticity and sequence correlation. It is especially effective when the sample size is not large enough, allowing heteroscedasticity in different sections and weighting by cross-section weights. The benchmark regression results are shown in Table 4, which shows that the direction and significance level of the regression coefficients for each variable does not change substantially when different estimation methods are applied. The BP and Hausman test results revealed that the fixed effect model is the optimal choice. Therefore, the benchmark regression result analysis here is mainly based on the regression result of the fixed effect model.

TABLE 4. Benchmark regression results.

Models 1–4 in Table 4 show the detailed results of the four estimation methods. It can be found that no matter which estimation method is used, financial subsidies significantly positively impact the innovation efficiency of start-up enterprises. According to model 3, each unit increase in financial subsidies is associated with 0.0056 units increase in the innovation efficiency of enterprises in the start-up period, thus, hypothesis 1 is verified.

4.3 Test of robustness

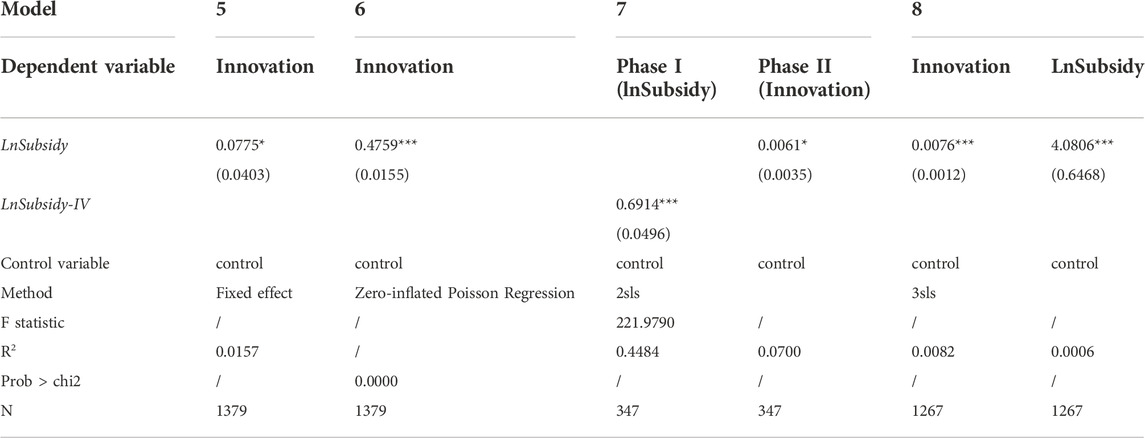

To test the robustness of the above results, this study focuses on the robustness test in the following ways, and all results are shown in Table 5, Model 5–Model 8.

TABLE 5. Robustness test and treatment of reverse causality.

4.3.1 Replace the core variable

The innovation efficiency of enterprises is measured by the proportion of the number of patent applications and the R&D capital investment. In this part, the natural logarithm of the number of invention patents is used as the replacement variable, and the fixed effect model is used for estimation. The empirical results are shown in Model 5, and the test results are generally consistent with this paper’s conclusions, regardless of the measurement method used.

4.3.2 Transform estimation method

When the number of invention patent applications measures the innovation efficiency of enterprises, it is a count variable. To prevent errors caused by the selection of measurement models, this section uses the zero-inflated Poisson count model for re-examination. The test results are shown in Model 6, which has not changed substantially.

4.3.3 Instrumental variable method

In terms of the selection of instrumental variables, this study refers to the methods commonly used in academia, uses the independent variable lagged by one period as the instrumental variable, and uses the two-stage least square method to estimate. The results are shown in Model 7. The two-stage regression results are consistent with the estimation results of the benchmark model. Financial subsidies significantly affect the innovation efficiency of startups, which further confirms the robustness of the benchmark regression results of this study.

4.4 Treatment of reverse causality

In theory, the improvement of innovation efficiency of enterprises at the start-up stage helps enterprises to obtain financial subsidies. It is difficult to describe the relationship between financial subsidies and the innovation efficiency of start-up enterprises through a single equation, which does not capture the interaction between various variables, and endogeneity is challenging to overcome. For this reason, this study uses the simultaneous equations model to explain the interaction between the two by combining another group of variables jointly determined by one group of variables to be measured to characterize the interaction (Pei, 2018). The specific model is as follows:

where all definitions in Eqs 2 and 3 are consistent with Eq. 1; Zit represents the control variables in Eq 2, which are also consistent with the control variables in Eq. 1; Eit represents the control variables of Eq 3, including local economic development degree (GDP), local government fiscal revenue (fisc), etc., The natural logarithm of GDP measures the degree of local economic development at the provincial level; Local government fiscal revenue is the natural logarithm of fiscal revenue at the provincial level.

In the simultaneous equation model of financial subsidies and innovation efficiency of start-up enterprises, since financial subsidies and innovation efficiency of enterprises are endogenous variables, the perturbation terms of the two equations are likely to be correlated theoretically (Chen, 2014). Therefore, this study adopts the three-stage least squares (3SLS) in system estimation to estimate the parameters in the simultaneous equation. It incorporates all available information into its estimation value to obtain a better asymptotically valid estimator. For a multi-equation system where the equations contain endogenous explanatory variables, 2SLS estimation for each equation is consistent but not the most efficient because a single equation ignores the possible correlation between the perturbation terms of differential equations. At this time, it is efficient to use SUR (Seemly Unrelated Regression Estimation) to estimate the entire equation system simultaneously. For this reason, SUR estimation is carried out in this study, and the regression results are shown in Table 6.

TABLE 6. Heterogeneity test results.

The results of model 8 show a significant interaction between financial subsidies and innovation efficiency of start-up enterprises, with a significance level of 1%. All other things being equal, for every unit increase in financial subsidies, the innovation efficiency of start-up enterprises increases by 0.0076 units. In contrast, financial subsidies increase by 4.0806 units for every unit of innovation efficiency of start-up enterprises. It shows that there is indeed a reverse causal relationship between the two, and it also suggests that hypothesis 1 of this paper is still valid even after considering the reverse contribution of start-up enterprises’ innovation efficiency to financial subsidies.

5 Heterogeneity analysis

5.1 Heterogeneity test at the city level

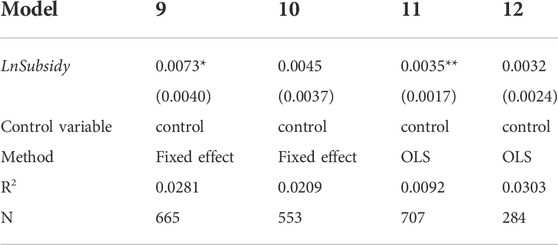

This study discusses the impact of financial subsidies of different levels of cities on the innovation efficiency of start-up enterprises by samples. The first-tier cities include Beijing, Shanghai, Guangzhou, and Shenzhen. Shanghai’s First Business Weekly selects the new first-tier cities. As there are floating changes in the annual evaluation, the new first-tier cities are identified based on the floating changes. If an enterprise is registered in a first-tier city or a new first-tier City, it is classified as a first-tier city group. At the same time, an enterprise registered in other cities is classified as a non-first-tier city group. The regression results are shown in Table 6, Models 9–10. Model 9 shows the regression results of the first-tier (including the new first-tier) city group, with a significantly positive coefficient. In contrast, Model 10 shows the regression results of the non-new first-tier city group with a positive but insignificant coefficient. This result shows that financial subsidies have a prominent role in promoting the innovation efficiency of start-up enterprises in large cities and also shows that the multiplier effect of financial funds can be better released in large cities.

5.2 Continuity and non-continuity test of subsidies

Firstly, this study deals with the original sample for the persistence of financial subsidies. The sample interval is 2010-2020. If an enterprise has received financial subsidies for 2 years or more in the sample interval, it is classified as the continuous group; if it has received financial subsidies in a particular year in the sample interval, it is classified as the non-sustainable group. Then, a grouping test is carried out. Since the discontinuous group’s data is cross-sectional, OLS regression is adopted. To maintain the consistency of the measurement methods of the two groups, the OLS estimation method is also adopted for the continuous group. The regression results are shown in Table 6, Model 11–Model 2. Model 11 shows the regression results for the persistent group, and the coefficient is significantly positive. In contrast, Model 12 shows the regression results for the non-persistent group and the coefficient is positive but not significant. This indicates that persistent financial subsidies are more conducive to improving the innovation efficiency of start-up enterprises, thus verifying Hypothesis 4 of this paper.

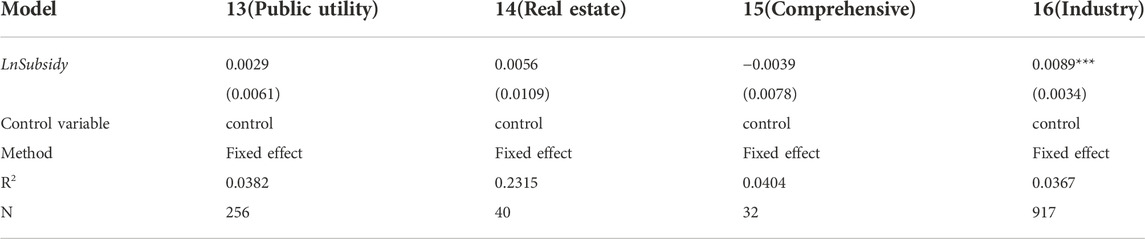

5.3 Industry heterogeneity test

Firstly, enterprises are divided into different industries according to the classification standard of CSMAR database. At the same time, considering the sample size of this study and excluding the data from financial enterprises, the sample is finally divided into the public utility industry, the real estate industry, the comprehensive industry, and the industrial industry. Then, the sample is regressed, and the results are shown in Table 7. Financial subsidies have a significant positive impact on the innovation efficiency of start-up enterprises, while all other industries fail the significance test.

TABLE 7. Industry heterogeneity test.

6 Discussion

The above empirical analysis results support the research hypothesis proposed in this paper, but some constraints have also been identified. Subsequently, the reasons for their formation are further explored based on the problems and constraints identified by the empirical study.

6.1 Constraints of an imperfect market system in small and medium-sized cities

Financial subsidies do not significantly improve the innovation efficiency of enterprises in small and medium-sized cities (non-first-tier cities) during the start-up period. Kang, (2018) believed that in regions with a low level of intellectual property protection, the role of financial subsidies in promoting enterprise innovation was not prominent enough (Kang, 2018). Small and medium-sized cities are not usually political, economic, and cultural centers of the region, and the construction of the market system environment lags behind, so the role of government subsidies in improving the innovation efficiency of start-up enterprises is not significant enough; in many small and medium-sized cities in China, because the level of intellectual property protection, business environment, and other institutional environments are not perfect and the degree of marketization is not high. It is difficult for enterprises’ innovation achievements to be protected by law, thus weakening the impact of financial subsidies on enterprises’ innovation efficiency.

6.2 Unsustainable subsidies are difficult to affect enterprise innovation decisions

Unsustainable financial subsidies cannot significantly affect the innovation efficiency of start-up enterprises, similar to Wen (2017) and Shi and Wang (2022). Unsustainable financial subsidies cannot significantly improve the innovation efficiency of start-ups because the innovation activities of start-ups face high adjustment costs, and intermittent and fluctuating subsidies cause a shortage of enterprise funds and thus affect the development of enterprise innovation activities. In addition, the government’s discontinuous subsidy also shows the “distrust” of enterprises. This “distrust” will have a chain reaction to enterprise financing, which will also reduce the R&D confidence of enterprises in the start-up period.

6.3 Industry characteristics limit the incentive effect of financial subsidies

It is difficult for financial subsidies to significantly improve the innovation efficiency in the public utilities, real estate industries and comprehensive industries because these industries have more obvious natural monopoly characteristics. It is difficult for industries with significant investment scales and a long period of scale change to achieve short-term results and return to scale to reduce costs. In addition, innovation efficiency is the integration of innovation capability and resource allocation effect. Enterprises in the public utilities, real estate, and comprehensive industries usually have low pure technical efficiency, leading to low innovation efficiency. In other words, since the sample enterprises in this study are small and medium-sized science and technology innovation enterprises in the start-up stage, there are generally problems such as low management level, low technology level, and poor resource allocation, which reduces the overall innovation efficiency of the enterprise.

6.4 The degree of competition in the industry affects the signal strength of subsidies

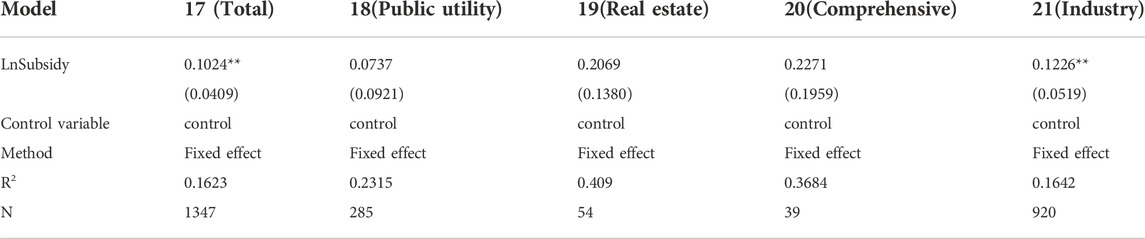

Signal theory points out that the magnitude of signal action depends on the degree of information asymmetry between both parties, signal quality, and other factors, and the content of signal transmission includes quality signal and intention signal, with a quality signal indicating the capacity characteristics within the organization that are not easy to observe and intention signal indicating organizational behavior or behavior intention (Stiglitz, 2000). The behavioral theories have also been applied in many studies (Elahi et al., 2021b; Elahi et al., 2022a). Based on the signal theory, the government’s financial subsidies can transmit positive signals about the actual quality of enterprises to the outside world, reduce the information asymmetry of external institutional investors, and have important significance in alleviating financing constraints, obtaining external innovation resources, and improving innovation efficiency (Xia and He, 2020).

The main sources of external financing of enterprises include cash received from absorbing equity investment, cash received from issuing bonds, and cash received from obtaining loans (Huang et al., 2016). This study uses the practices of Yu and Wang, (2022) for reference. It uses the natural logarithm of the annual net amount of the three to measure the scale of external financing of enterprises (lnout ). The signal transmission mechanism is constructed for testing by industry, and the results are shown in Table 8, which is consistent with the results in Table 7 in significance. Model 17 is the total sample estimation result, and Model 18–Model 21 is the sub-sample estimation result. The results show that financial subsidies can help start-ups expand the scale of external financing, but this effect is more significant for industrial enterprises.

TABLE 8. Mechanism test.

The signal transmission mechanism of financial subsidies differs in different industries due to the obvious natural monopoly characteristics of public utilities, real estate and comprehensive industries compared with industrial industries, making it easy to obtain commercial financing by virtue of their own market position. Van Horen (2005) believed that investors were more willing to cooperate with enterprises that occupied a dominant market position because of their lower level of information asymmetry, which made it easier to achieve commercial financing. Yu (2017) pointed out that the industry competition level is one of the decisive factors affecting the signal effect’s strength. The lower the industry competition level, the weaker the signal effect of enterprise credit. Therefore, the signal effect of financial subsidies is more evident in the industrial sector (Yu, 2017).

6.5 Crowding-out effect of fiscal decentralization

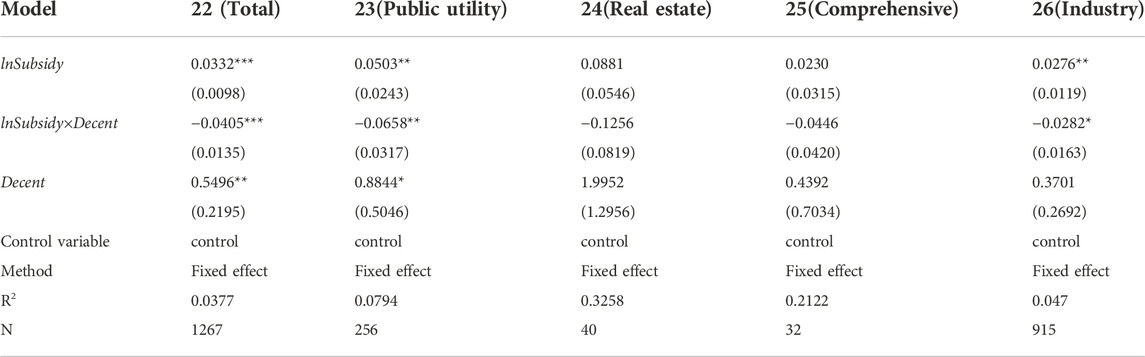

Based on the perspective of fiscal decentralization, this study examines the impact of fiscal freedom on fiscal subsidies and the innovation efficiency of start-up enterprises. The fiscal decentralization system endows local governments with the independent discretion of fiscal revenue and expenditure, enabling local governments to determine the expenditure intensity of fiscal subsidies independently, thus affecting enterprises’ innovation activities. According to finance and taxation theory, the greater the degree of fiscal decentralization, the stronger the financial strength of local governments and the greater the degree of fiscal freedom. On the one hand, the improvement of financial freedom can reduce costs through taxation to encourage enterprises to increase R&D investment. On the other hand, it can also support enterprise innovation activities through direct subsidies (Mao et al., 2022). However, some scholars pointed out that since it is difficult for enterprise innovation activities to promote GDP growth in a relatively short period greatly, if local governments are eager to pursue GDP, tax, and other performance growth, financial funds will be more inclined to other fields and financial science and technology subsidies will be reduced (Zou, 2018).

The measurement method of fiscal decentralization refers to the research of Chen and Gao, (2012), and Zhang et al. (2022). The ratio of provincial fiscal revenue to provincial fiscal expenditure is used to construct an indicator of fiscal autonomy to measure fiscal decentralization (Decent). The larger the value, the greater the fiscal revenue of local governments and the greater the fiscal freedom of local governments. At the same time, the cross-term of financial subsidies and fiscal decentralization (lnSubsidy×Decent) are added to the model and the results are shown in Table 9, Model 22, Model 26. It can be found that fiscal decentralization generally weakens the impact of fiscal subsidies on the innovation efficiency of start-up enterprises, and this effect is more significant in public utilities and industrial industries.

TABLE 9. Results of the regulation effect.

Fiscal decentralization weakens financial subsidies’ impact on startups’ innovation efficiency, and the impact is more pronounced in the public utilities and industrial sectors. One possible reason is that the public utilities and industrial industry usually need to invest a lot of funds in the start-up period, which are not fully utilized, resulting in the “crowding out effect” of innovation, thus increasing the burden on enterprises and reducing innovation efficiency. Another possible reason is that the R&D system of small and medium-sized enterprises in the start-up stage is usually not sound, especially the lack of scientific research personnel. Therefore, there are serious problems, such as unreasonable allocation structure of scientific research funds and scientific research personnel. The element input cannot achieve the optimal allocation. It cannot be effectively converted into achievements, which to some extent echoes the research conclusions of Liu and Wu (2021).

7 Conclusion and policy implications

Based on the listed start-ups on the GEM, STAR Market and the SME Board from 2010 to 2020 in China, this study empirically tested the impact of financial subsidies on the innovation efficiency of start-ups. It also examines the signaling role of financial subsidies in enterprise financing and the regulatory role of fiscal decentralization on innovation efficiency. The following research conclusions are drawn. First, financial subsidies have a positive impact on the innovation efficiency of start-up enterprises in general, and there is also an interactive relationship between them, but there are industry differences in the impact of financial subsidies on the innovation efficiency of start-up enterprises; Second, there are regional differences in the impact of financial subsidies on the innovation efficiency of start-up enterprises, and the financial multiplier effect is more evident in big cities such as the first tier (new first tier); Third, financial subsidies with strong continuity can more stimulate the innovation efficiency of start-up enterprises; Fourth, on the whole, the signaling mechanism of financial subsidies has played a role in the financing process of start-up enterprises, but this mechanism has only been significantly reflected in industrial enterprises; Fifth, fiscal decentralization negatively regulates the impact of fiscal subsidies on innovation efficiency in the start-up period, which is more significant in the public utility industry and industrial enterprises. Based on this, the following policy recommendations are targeted.

First, governments (especially those of small and medium-sized cities) should improve the market system and optimize the business environment. The imperfection of the innovation protection system and the implementation mechanism are essential weaknesses in the governance of small and medium-sized cities. Institutional defects increase enterprises’ innovation costs and make innovation more vulnerable to imitation and copying, reducing the incentive effect of financial subsidies on enterprise innovation. Therefore, the government should further promote market-oriented reforms in small and medium-sized cities, optimize the business environment, and improve the intellectual property protection system and financial support system, so as to create a favorable external environment for small and medium-sized science and technology innovation enterprises to enhance their innovation efficiency.

Second, strengthen the institutionalization, relative stability, and sustainability of subsidies. As an important source of funds for start-ups, the Chinese government’s financial subsidy mechanism must be institutionalized to form an innovation incentive effect for small and medium-sized science and technology start-up enterprises and a signaling effect for other investment institutions. Currently, there are many irregularities in the application of financial subsidies in China, which makes it difficult for financial subsidy policymakers to grasp the actual market rules, reducing the sustainability of the financial subsidy policies. Institutionalizing financial subsidy policies not only solves the problem of capital abuse but also reduces the information asymmetry between the government and the market. Specific institutional measures can include standardization of administrative approval and institutionalization of R&D funds.

Third, enhance the industrial pertinence and accuracy of policies. The government should continue to deepen the reform and provide more preferential policies for small and medium-sized science and technology innovation enterprises in the start-up stage. However, the “one-size-fits-all” subsidies cannot achieve the optimal allocation of resources. The government needs to provide personalized and precise subsidies for different industries, optimize the subsidy structure and the direction and field of capital investment, and play a better leverage role (Wang et al., 2020). For example, the government should gradually change the supervision and management mechanism to improve the efficiency of capital utilization for some public utilities that occupy huge government subsidies but have limited innovation efficiency improvement. Government subsidies are issued concerning market competition and supplemented by subsidy policies.

On the other hand, with the global economic downturn and epidemic, governments at all levels can actively establish government guidance funds to support small and medium-sized technology-based start-ups to reduce financial pressure. In addition to providing funds, the government guidance funds also have the advantages of improving enterprise management, strategic planning and strong sustainability. At the same time, small and medium-sized science and technology innovation enterprises in the start-up period, less constrained by organizational inertia and bureaucratic system, should actively find potential innovation opportunities in the market to attract government support.

Fourth, enhance market competitiveness and give full play to the signaling role of subsidies. The industry competition level is an essential basis for the strength of the subsidy signaling effect. Government subsidies should be more market-oriented. Through subsidies, the government should transmit to external investors the list of enterprises that the government is concerned about and open up information channels between investors and enterprises to help potential start-up enterprises broaden external financing channels and reduce financing constraints. On the one hand, enterprises use financial subsidies to signal “self-publicity” to attract the attention of external institutional investors and gather other innovative elements, thereby enhancing innovation efficiency. On the other hand, they should take the initiative to pay attention to the government’s subsidy policies and respond positively to them, reducing the selection cost of external investors by obtaining financial subsidies to obtain external resources better to support innovation.

Fifth, promote the efficient and balanced allocation of financial resources. To avoid the redundancy and inefficient use of financial resources, the government should pay more attention to the subsidy targets so that the limited resources can play the most positive role. The government should subsidize not only enterprises but also talents, thus promoting the balanced allocation of financial funds. Small and medium-sized science and technology innovation enterprises in the start-up stage should emphasize internal management and strategic planning and improve the enterprise management system. The allocation of R&D funds should pay attention to the structural ratios and balance, reasonably match innovation input elements, and focus on innovation output to improve the efficiency of using funds. Start-up enterprises must attach importance to talent introduction, give full play to talent efficiency, appropriately reduce the funding input and improve the talent input to improve the innovation performance of enterprises.

8 Limitations and future recommendations

This study still has some limitations and shortcomings in the research process. Firstly, the classification of industries in this paper is rather general, and whether the empirical results can be extended to start-ups in other types of industries is subject to further research. Secondly, the single indicator used in this paper is insufficient to measure enterprises’ innovation efficiency. In the future, a combination of input and output indicators can be used to portray the innovation efficiency of enterprises based on the availability of data.

Finally, in theory, the government should try to avoid long-term equity investment. Although the empirical results of this paper show that continuous financial subsidies have generally improved the innovation efficiency of start-ups, future research should clarify the timing and mechanism of the introduction of financial subsidies and attach importance to the leading role of the market in the process of enterprise innovation.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Author contributions

HR guided the data analysis work in the paper and undertook part of the revision work of the external audit opinions. MA revised the article. His revision increased the readability of the article and adjusted the logic of the language to make the whole article more in line with the publishing requirements.

Funding

The study is funded by the National Social Science Fund Project (18BGL061).

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Aschhoff, B. (2009). The effect of subsidies on R&D investment and success. Do subsidy history and size matter? Rochester: ZEW-Centre for European Economic Research Discussion Paper. No.09-032.

Beck, N., and Katz, J. N. (1995). What to do (and not to do) with time-series cross-section data. Am. Polit. Sci. Rev. 89 (3), 634–647. doi:10.2307/2082979

Chen, Q. Advanced econometrics and stata application (Second Edition) [M]. Beijing: Higher Education Press, 2014

Chen, S., and Gao, L. (2012). Central local relations: Measurement of fiscal decentralization and Re evaluation of its mechanism [J]. Management World, 43–59.06. doi:10.19744/j.cnki.11-1235/f.2012.06.005

Chen, Y., and Tian, H. (2020). The impact of government R&D subsidies on enterprise innovation efficiency - research based on SFA-CDM model [J]. Res. Technol. Econ. Manag. (09), 27–33.

Dickinson, V. (2011). Cash flow patterns as a proxy for firm life cycle. Account. Rev. 86 (6), 1969–1994. doi:10.2308/accr-10130

Duan, S., and Yang, B. (2020). Research on the innovation incentive effect of financial subsidies and tax preferences--annotation from the scale and life cycle of private technological enterprises [J]. Sci. Technol. Prog. Countermeas. 37 (16), 120–127.

Elahi, E., and Khalid, Z. (2022). Estimating smart energy inputs packages using hybrid optimisation technique to mitigate environmental emissions of commercial fish farms. Appl. Energy 326, 119602. doi:10.1016/j.apenergy.2022.119602

Elahi, E., Khalid, Z., Tauni, M. Z., Zhang, H., and Lirong, X. (2021a). Extreme weather events risk to crop-production and the adaptation of innovative management strategies to mitigate the risk: A retrospective survey of rural Punjab, Pakistan. Technovation 117, 102255. doi:10.1016/j.technovation.2021.102255

Elahi, E., Khalid, Z., and Zhang, Z. (2022a). Understanding farmers’ intention and willingness to install renewable energy technology: A solution to reduce the environmental emissions of agriculture. Appl. Energy 309, 118459. doi:10.1016/j.apenergy.2021.118459

Elahi, E., Zhang, H., Lirong, X., Khalid, Z., and Xu, H. (2021b). Understanding cognitive and socio-psychological factors determining farmers’ intentions to use improved grassland: Implications of land use policy for sustainable pasture production. Land Use Policy 102, 105250. doi:10.1016/j.landusepol.2020.105250

Elahi, E., Zhang, Z., Khalid, Z., and Xu, H. (2022b). Application of an artificial neural network to optimise energy inputs: An energy-and cost-saving strategy for commercial poultry farms. Energy 244, 123169. doi:10.1016/j.energy.2022.123169

Hou, S., and Song, L. (2019). Financial incentives, financing incentives and enterprise R&D innovation [J]. China Circ. Econ. 33 (07), 85–94.

Howell, S. T. (2017). Financing innovation: Evidence from R&D grants. Am. Econ. Rev. 107 (4), 1136–1164. doi:10.1257/aer.20150808

Huang, H., Zhai, S., and Chen, J. (2016). Enterprise life cycle, financing methods and financing constraints - research based on the effect of investor emotion regulation [J]. Financial Res. (07), 96–112.

Kang, Z. (2018). Did government subsidies promote the improvement of enterprise patent quality? [J] Sci. Sci. Res. 36 (01), 69–80. doi:10.16192/j.cnki.1003-2053.2018.01.009

Li, S., and Shi, J. (2021). Research on the impact of deleveraging policy on enterprise innovation-empirical evidence from the automobile industry[J]. Industrial Technol. Econ. 40 (10), 94–99.

Lin, Z., Lin, H., and Deng, X. (2015). Research on the impact of government subsidies on enterprise patent output [J]. Sci. Sci. Res. 33 (06), 842–849. doi:10.16192/j.cnki.1003-2053.2015.06.006

Liu, J., and Wu, B. (2021). Research on innovation efficiency of China's entrepreneurial enterprises in the initial stage [J]. Econ. Manag. Rev. 37 (02), 150–160. doi:10.13962/j.cnki.37-1486/f.2021.02.014

Mao, J., Zhang, R., and Guan, C. (2022). Digital economy, fiscal decentralization and enterprise innovation [J]. J. Southwest Univ. Natl. Humanit. Soc. Sci. Ed. 43 (08), 118–129.

Pei, L. (2018). The interaction between scientific and technological talents gathering and high tech industry development [J]. Sci. Sci. Res. 36 (05), 813–824. doi:10.16192/j.cnki.1003-2053.2018.05.006

Razzaq, A., Qing, P., Abid, M., Anwar, M., and Javed, I. (2019). Can the informal groundwater markets improve water use efficiency and equity? Evidence from a semi-arid region of Pakistan. Sci. Total Environ. 666, 849–857. doi:10.1016/j.scitotenv.2019.02.266

Razzaq, A., Tang, Y., and Qing, P. (2021). Towards sustainable diets: Understanding the cognitive mechanism of consumer acceptance of biofortified foods and the role of nutrition information. Int. J. Environ. Res. Public Health. 18 (3), 1175. doi:10.3390/ijerph18031175

Shi, J., and Li, X. (2021). Government subsidies and enterprise innovation capacity: A new empirical discovery [J]. Econ. Manag. 43 (03), 113–128. doi:10.19616/j.cnki.bmj.2021.03.007

Shi, Y., and Wang, T. (2022). Government support and enterprise innovation [J]. Syst. Eng. Theory Pract. 42 (08), 2002–2016.

Shi, Z., and Xie, C. (2015). Bank competition, financing constraints and technological innovation in strategic emerging industries [J]. Macroecon. Res. (08), 117–126. doi:10.16304/j.cnki.11-3952/f.2015.08.012

Song, H., Ni, X., and Zhang, J. (2020). Can the government guidance fund promote technological innovation--- Empirical Research Based on China's Technological Startups [J]. Manag. Rev. 32 (03), 110–121.

Stiglitz, J. E. (2000). The contributions of the economics of information to twentieth century economics. Q. J. Econ. 115 (4), 1441–1478. doi:10.1162/003355300555015

Tang, Y., and Qing, P. (2021). Towards sustainable diets: Understanding the cognitive mechanism of consumer acceptance of biofortified foods and the role of nutrition information. Int. J. Environ. Res. Public Health 18, 1175. doi:10.3390/ijerph18031175

Tong, A., and Chen, W. (2016). Empirical study on the impact of government subsidies on enterprise R&D investment -- A new perspective based on the political linkage of private listed companies in small and medium board[J]. Sci. Sci. Res. 34 (07), 1044–1053. doi:10.16192/j.cnki.1003-2053.2016.07.010

Van Horen, N. (2005). Do firms use trade credit as a competitiveness tool?-- Evidence from Developing Countries[R]. Munich: World Bank Working Paper. doi:10.2139/ssrn.562410

Wang, L., Zhou, Y., Wang, N., and Li, K. (2020). Research on China's science and technology finance support system based on life cycle [J]. Sci. Technol. Manag. Res. 40 (10), 36–41.

Wang, X., and Yang, B. (2022). Research on the impact of government subsidies on the innovation performance of software enterprises [J]. Sci. Sci. Res. 40 (03), 555–564. doi:10.16192/j.cnki.1003-2053.20210304.001

Wen, M. (2017). Continuity of government R&D subsidies and enterprise R&D investment-empirical analysis based on 185 listed manufacturing companies[J]. Public Adm. Rev. 10 (01), 116–140.

Xia, Q., and He, D. (2020). Did government R&D subsidies promote enterprise innovation? Explanation from the perspective of signal theory [J]. Sci. Technol. Prog. Countermeas. 37 (01), 92–101.

Xie, X. (2010). Empirical study on SME collaborative innovation network and innovation performance [J]. J. Manag. Sci. 13 (08), 51–64.

Yang, Y., Jiang, W., and Luo, L. (2015). Who is using government subsidies for innovation--- the joint adjustment effect of ownership and factor market distortion [J]. Beijing : Management World, 75–86.01

Yu, B. (2017). Business credit, signal effect and bank financing - empirical analysis based on A-share manufacturing listed enterprises [J]. Secur. Mark. Guide (01), 34–42.

Yu, Z., and Wang, J. (2022). Research on the impact of government subsidies on enterprise innovation in different life cycles [J]. Financial Res. 48 (01), 19–33. doi:10.16538/j.cnki.jfe.20211016.303

Zhang, Q., Razzaq, A., Qin, J., Feng, Z., Ye, F., and Xiao, M. (2022). Does the expansion of farmers’ operation scale improve the efficiency of agricultural production in China? Implications for environmental sustainability. Front. Environ. Sci. 683. doi:10.3389/fenvs.2022.918060

Zhang, X., and Zhang, X. (2022). Fiscal decentralization, tax competition and green development [J]. Statistics Decis. Mak. 38 (05), 126–131. doi:10.13546/j.cnki.tjyjc.2022.05.024

Zheng, L., Yang, S., and Lu, J. (2019). Heterogeneous impact of government subsidies on total factor productivity of manufacturing enterprises [J]. Econ. Manag. 41 (03), 5–20.

Keywords: financial subsidies, start-up enterprises, innovation efficiency, heterogeneity, China

Citation: Zhou Y, Wang L, Ren H, Wang L, Zhang S and Aamir M (2022) Influence of financial subsidies on innovation efficiency of start-up enterprises. Front. Environ. Sci. 10:1060334. doi: 10.3389/fenvs.2022.1060334

Received: 03 October 2022; Accepted: 31 October 2022;

Published: 17 November 2022.

Edited by:

Arshian Sharif, Sunway University, MalaysiaReviewed by:

Umair Akram, RMIT University, VietnamMatheus Koengkan, University of Aveiro, Portugal

Gladson Chikwa, University of Bradford, United Kingdom

Copyright © 2022 Zhou, Wang, Ren, Wang, Zhang and Aamir. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Lun Wang, d2FuZ2x1bm1iYUB5bnVmZS5lZHUuY24=