Lijuan Zhang

Lijuan Zhang Zirui Song

Zirui Song- 1School of Digital Economy and Management, Leshan Vocational and Technical College, Leshan, China

- 2Department of Accounting and Finance, University of Western Australia, Perth, WA, Australia

One of the key factors influencing corporate sustainable development is green technology innovation (GTI). Our study intends to explore how digital transformation impacts corporate value through GTI. We use panel data from A-share publicly listed firms in China spanning from 2012 to 2022 as our sample. We employ textual analysis to extract keywords correlated to digital transformation from the annual reports, and construct an indicator to evaluate the digital transformation of corporates. Our findings show that digital transformation significantly enhances enterprise value by improving green technology innovation. Furthermore, the market competition and green credit moderate the mediated relationship between digital transformation and corporate value. Additionally, heterogeneity tests indicate that digital transformation has a more significant influence on value enhancement for heavily polluting corporates, non-high-tech corporates, and smaller corporates. This research offers important recommendations for practitioners on advancing sustainable business practices and provides policy recommendations for environmental protection and green development.

1 Introduction

Currently, a new circle of techno-industrial revolutions driven by information technologies such as big data, blockchain, cloud computing, and artificial intelligence, is accelerating the development of the digital economy (Pei et al., 2023). Digitalization has become one of the most important technological innovations, acting as a significant driver for stimulating high-quality development in companies (Nie et al., 2024). The wide influx of digital technologies has intensified market competition, clearly signaling the need for businesses to implement digital transition (Verhoef et al., 2021). Consequently, many companies have either completed or are ongoing digital transition. Hence, researching the role of digital transformation in advancing enterprise value is of practical significance. Enterprises increasingly view green innovation as a crucial driver of their competitive advantage and green transition (Shi et al., 2024; Wang and Wang, 2021). Unlike traditional technology innovation models, GTI is a new innovation model based on sustainable development, aiming to achieve harmonious development between humans and nature (Li, 2005). GTI is a crucial path to establishing sustainable competitive advantages (Beltramello et al., 2013) and achieving corporate sustainable development. Therefore, we choose GTI as the intermediary channel for our research in the context of the green development and sustainable development era. Namely, with the rapid development of cutting-edge information technology (IT), digitalization is becoming a key catalyst for innovation and transformation in global businesses (Wu et al., 2021). As digital transformation brings new technologies, new tools, and new models to enterprises, whether it can drive enterprises to enhance their level of GTI and, in turn, increase firm value is a question of considerable interest to both theorists and practitioners.

Prior studies have explored the impact of digital transformation on firm value, but the conclusions are complex. On the one hand, Liu and Jin (2023) argue that digital transformation triggers changes in various aspects of enterprise value creation, acting as an accelerator for reshaping the value creation capabilities of specialized and innovative enterprises. Li (2023) finds that digital transformation in enterprises can effectively elevate corporate value by enhancing the quality of internal controls and operational efficiency. Chen and Srinivasan (2024) find that companies that embrace digitalization improve their productivity, with market-to-book ratios higher than those of their industry peers. On the other hand, some academics find that the hidden costs of digital transformation often outweigh the benefits, with most companies incurring high costs during digital transformation (Hajli et al., 2015), such as increased audit fees (Yang and Lu, 2017), which are detrimental to the enhancement of corporate value. In conclusion, many scholars believe that digital transformation promotes the enhancement of firm value by innovating business models, fostering technological innovation, and improving operational efficiency. However, some scholars argue that digital transformation may increase corporate costs, thereby damaging firm value. The mixed results call for further research into the relationship between digital transformation and enterprise value (Zhang et al., 2022). While an increasing number of papers address digital transformation and corporate value, green technology innovation (GTI) is rarely considered. In that case, our research question is what role does GTI play in digital transformation impacting enterprise value? What is the mechanism behind this role? To answer these questions, we use data from Chinese listed companies between 2012 and 2022 as the research sample. The reason for selecting Chinese listed companies as the research sample is as follows. First, China has become the most important participant in the global digital economy. According to the “Digital China Development Report (2022)1,” the scale of China’s digital economy reached 50.2 trillion yuan in 2022, maintaining its position as the leading in the world. Studying the relationship between digital transformation in Chinese enterprises and their value can provide valuable insights for other global participants in the digital economy. Second, in order to conserve energy, reduce emissions, and achieve sustainable economic development, the Chinese government has implemented a series of environmental policies, such as green finance policies and green development transformation policies, which have created favorable conditions for studying the role of GTI in the relationship between digital transformation and firm value.

Based on the theory of interdependence, the relationship between individuals is interactive and complex, and is affected by specific scenarios. Therefore, we attempt to conduct further investigations into the moderating role of contextual variables on GTI in the correlation between digital transition and corporate value. Both digital transformation and GTI can be influenced by market competition. Referring to the Structure-Conduct-Performance (SCP) theory, less market competition usually implies higher market concentration. Market concentration serves as a core factor in many innovation theories, in markets with highly concentration, firms respond more strongly to the innovation of competitors and complementary technologies (Turner et al., 2010), and use both internal and external resources more vigorously to achieve superior levels of innovation output (Oerlemans et al., 2001). And GTI is a form of innovation. While digital transformation can optimize resource allocation (Tang et al., 2023), improve asset utilization (Peng and Tao, 2022), and enhance enterprise operation efficiency (Chen and Yang, 2022), further improving the GTI capability of the enterprise (Xue et al., 2022). Our study demonstrates that the lower the market competition, i.e., the higher the market concentration, the more significant the impact of digital transition on enhancing GTI.

Meanwhile, in 2012, the China Banking Regulatory Commission (CBRC) issued the Green Credit Guidelines, requiring banking financial institutions to promote green credit from a strategic perspective and enhance support for the green economy, low-carbon economy, and circular economy. Banking financial institutions actively responded to this environmental protection policy by providing low-interest loans to energy-saving and environmentally friendly enterprises, while imposing punitive high-interest loans on high-pollution and high-energy consumption enterprises. This approach aims to encourage businesses to strengthen green innovation, reduce energy consumption and emissions, and fulfill their obligations to protect the environment. Green credit is a form of financial support widely used by the Chinese government to promote environmental protection and green development (Hu et al., 2020). Green credit guides more funds into the environmental protection industry and reduces investment in high-pollution enterprises (Ding et al., 2020), encourages businesses to improve their GTI capabilities (Zhou et al., 2023; Zhu, 2022), and promotes better fulfillment of environmental responsibilities. This, in turn, helps reduce environmental costs, improve environmental performance, and enhance corporate value. Digital transformation can improve resource allocation and promote the efficient use of resources (Tang et al., 2023; Peng and Tao, 2022). Therefore, in the presence of green credit, digital transformation is more likely to enhance the level of green technological innovation in enterprises. At the same time, the higher the level of green technological innovation, the greater its role in enhancing corporate value. Our research also confirms this.

The marginal contributions of our study may be in the following several aspects. First, there is little literature related to the micro-level perspective study of digital transformation impacting company development through the mediation mechanism of GTI. We use textual analysis to extract keywords pertaining to digital transformation from annual reports and use them as proxy indicators to assess the digital transformation of enterprises. And we incorporate GTI as a mediating variable into the research framework along with digital transformation and corporate value, and uncover the mechanism by which digital transformation influences corporate value via GTI, further revealing the channels of digital transformation to enhance enterprise value. Meanwhile, it also provides new empirical evidence for how corporate digital transformation enhances corporate value and improves the level of GTI. Our work refines the study of digital transformation and corporate value, providing novel implications for promoting corporate GTI and sustainable development. Second, building on the interdependence theory, the mediating effect of GTI between digital transformation and firm value depends on certain contexts. We employ a hierarchical regression analysis method, and the empirical results reveal that market competition and green credit can moderate the mediating connection between digital transformation and firm value. We study the mediating effect of GTI between digital transformation and firm value from the perspectives of industry factors and policy factors, which provides a new research perspective.

2 Hypotheses development

2.1 The impact of digital transformation on corporate value

Digital transformation refers to the process of improving an entity by altering their value creation paths through combinations of data, computation, interaction, and networking technologies (Vial, 2021). Digital transformation enhances enterprise value by bringing changes to business management, driving technological innovation, and lowering agency costs. Firstly, digital transition helps to improve enterprise management models. By utilizing digital means, businesses can optimize their processes, reduce operational costs (Han et al., 2022), and increase operational efficiency, thereby creating greater value for the enterprise (Jiang et al., 2023). Secondly, digital transformation can bring about innovations in business models and technology for enterprises. On one side, digital transformation integrates business models with digital technologies, facilitating innovation in business models distribution channels, and marketing approaches to convey value to customer segments (Matarazzo et al., 2021), furthermore creating value for companies. On the other side, digital transition fosters the fusion of digital technology with multiple disciplines, providing the technological support needed to drive technological innovation (Yu, 2022). Consequently, it fosters technological innovation and relies on the Internet of Things, artificial intelligence, big data, and cloud computing as its foundation to achieve value creation (Li, 2023). Finally, digital transformation contributes to increasing information transparency and reducing agency costs. Digital transformation enables the entire process of internal operations and external supervision to be online, making business management activities more transparent and efficient (Zhang and Han, 2023). It can more timely and accurately convey relevant information to the outside world, increasing information transparency (Qi et al., 2020), effectively alleviating principal-agent issues, reducing principal-agent costs, there by enhancing corporate value. Based on this, the article proposes the following hypothesis:

Hypothesis 1. Digital transformation positively impacts corporate value.

2.2 The effect of digital transformation on GTI

According to data from the World Economic Forum, the reduction in carbon emissions across various sectors owing to digital technologies is expected to reach 12.1 billion tons by 2030. Reducing urban carbon emissions requires the driver of GTI, with carbon-reducing technologies and GTI being key to enterprises’ energy saving and emission cuts (Guo et al., 2022). From an industrial structure perspective, the comprehensive permeation and widespread use of digital technologies in the industrial sector have promoted the transition of industries towards smart and green development (Ding and Qin, 2021). As individual entities within their industries, enterprises can reshape their business models, supply chains, and supply-demand relationships through digital transformation, achieving innovations in products and technology (Zhou and Chen, 2022). Digital transformation significantly promotes technological innovation by efficiently integrating external innovation resources, quickly and conveniently connecting innovation entities (Han et al., 2022). Of course, this technological innovation also includes GTI. Therefore, digital transformation helps enhance the level of GTI in corporations. On one side, improving the level of digital transformation not only increases transparency of corporate information and strengthens positive market expectations but also stimulates greater research and development input, thereby boosting GTI in enterprises (Liu and He, 2024). On the other side, alleviating firm financing constraints is beneficial for conducting the activities of GTI (Guo et al., 2021). Digital transformation alleviates financial constraints, mitigates agency conflicts, and enhances growth capacity, thereby promoting green technological innovation in companies (Jing et al., 2022). Meanwhile, digital transformation continuously transforms innovative methods and processes by acquiring more green innovation resources and support, enabling more intelligent and convenient extraction of green innovation outcomes (Chen and Zhang, 2023). This allows enterprises to obtain more green patents and enhance green innovation quality of companies. Building on the above analysis, our research proposes the hypothesis below:

Hypothesis 2. Digital transformation positively impacts enterprises’ GTI.

2.3 The mediating mechanism of GTI

In accordance with the “Guiding Opinions on Building a Market-Oriented GTI System” jointly issued by China’s National Development and Reform Commission and the Ministry of Science and Technology in 2019, GTI is increasingly recognized as a key emerging area in the latest wave of global industrial revolution and technological rivalry. GTI serves a key role in the building of eco-civilization and the sustainable growth of corporates. At the micro level, green innovation markedly contributes to high-quality business development (Li and Cui, 2024). On one side, GTI can improve the manufacturing efficiency of companies, reduce unit manufacturing costs, decrease pollution emissions, lower the costs associated with regulatory non-compliance due to pollution issues, enhance environmental performance, and further translate into economic performance (Wang et al., 2021). Meanwhile, GTI generates an “isolation mechanism” that allows businesses to obtain marginal profits and competitive advantages (Chang, 2011), significantly enhancing enterprise value and competitiveness (Chen and Laisb, 2006). On the other side, improving the level of business GTI helps to advance green innovation in outputs and processes, thereby strengthening businesses’ green competitiveness and increasing their economic and social value (Yu et al., 2010). In summary, GTI can enhance corporate value. Meanwhile, based on Hypothesis 2, digital transformation helps to advance GTI in corporations. Building on this, our study posits that digital transformation enhances firm value by advancing the level of GTI, indicating that GTI acts as a bridging role between digital transformation and firm value. Hence, we present the hypothesis below.

Hypothesis 3. GTI exerts a positive mediating effect between enterprise digital transformation and corporate value.

2.4 The moderating role of market competition in the mediating mechanism of GTI

Competition is an important factor influencing firm productivity (Nickell, 1996). According to the Structure-Conduct-Performance (SCP) theory, industry concentration affects firms’ behavior, which in turn influences their financial performance, and high concentration usually implies lower levels of competition. However, the priority shifts to dealing with the pressure from competitors imitating the brand, prompting enterprises to seek out new technologies and develop personalized portfolios in their mature stage (Lanzolla et al., 2021). And the emergence of new technologies favors intangible asset-intensive and high-productivity enterprises, promoting their transition towards an intangible asset-intensive economy and enhancing innovation (Zhang, 2019). The allocation of resources tilts towards large enterprise, and changes in market structure serve as a primary driver in determining the speed and trajectory of technological evolution (Zhang, 2019). Digital transformation can potentially facilitate enterprises’ green innovation by optimizing resource allocation, fostering innovation, and leveraging network effects (Tang et al., 2023). The digital transformation brings new technologies for enterprises, and it leads to an enhanced capacity for GTI (Zheng and Zhang, 2023). The enhancement in market concentration contributes to promoting the green innovation capabilities (Wang and Zhang, 2024). So we present the hypothesis below:

Hypothesis 4. The mediated relationship of enterprise digital transformation with corporate value is moderated by market competition. Specifically, for enterprises facing less intense market competition, the positive relationship between digital transformation and GTI is more pronounced.

2.5 The moderating role of green credit in the mediating mechanism of GTI

The green credit policy is a crucial component of the nation’s environmental governance framework (Zhang et al., 2024). With the issuance of the Green Credit Guidelines, more funds are made available in China to support the development of the environmental protection industry, which is beneficial for enterprises to engage in green technological innovation. Moreover, the implementation of the Green Credit Guidelines has put pressure on high-polluting enterprises, forcing them to adopt GTI (Zhu, 2022). At the same time, in order to avoid environmental penalties, enterprises need to increase their investment in environmental protection and improve the efficiency of these investments (Liang and Liu, 2017). Green credit has increased financial support for environmental protection projects in enterprises (Tian et al., 2024). Digital transformation can improve the efficiency of resource allocation within enterprises (Kumari, 2021; Liu et al., 2024; Jiang and Li, 2024), optimize investments, and thereby enhance the level of GTI in enterprises. The improvement of GTI levels can reduce environmental costs (Wang et al., 2021), gain competitive advantages and marginal profits (Chang, 2011; Chen and Laisb, 2006; Yu et al., 2010), thereby enhancing enterprise value. Based on this, we present the hypothesis below:

Hypothesis 5. The mediated relationship of enterprise digital transformation with corporate value is moderated by green credit. Namely, green credit not only positively moderates the relationship between corporate digital transformation and GTI but also positively moderates the impact of GTI on corporate value.

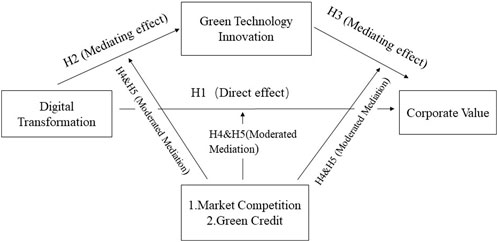

The general framework of our research is explained in Figure 1.

Figure 1. Conceptual framework.

3 Research design

3.1 Data sample

Our study picks the annual data of A-share public enterprises on the Shanghai and Shenzhen Stock Exchanges in China from 2012 to 2022 as the original sample and applies the filters below to the data: first, eliminating samples from the finance sector; second, eliminating ST and *ST samples; third, eliminating abnormal and absent data samples. After excluding the above samples and performing a 1% winsorization on all continuous variables, we obtain a final dataset of 33,050 sample observations. The data for this study originates from the CNRDS, WIND, CSMAR, and annual financial reports of public companies. Our dataset’s industry categorization standard abides by the “Guidelines for Industry Classification of Listed Companies” issued by the China Securities Regulatory Commission. Data statistical analysis in this study is conducted using Python and Stata16 software.

3.2 Variables

3.2.1 Dependent variable

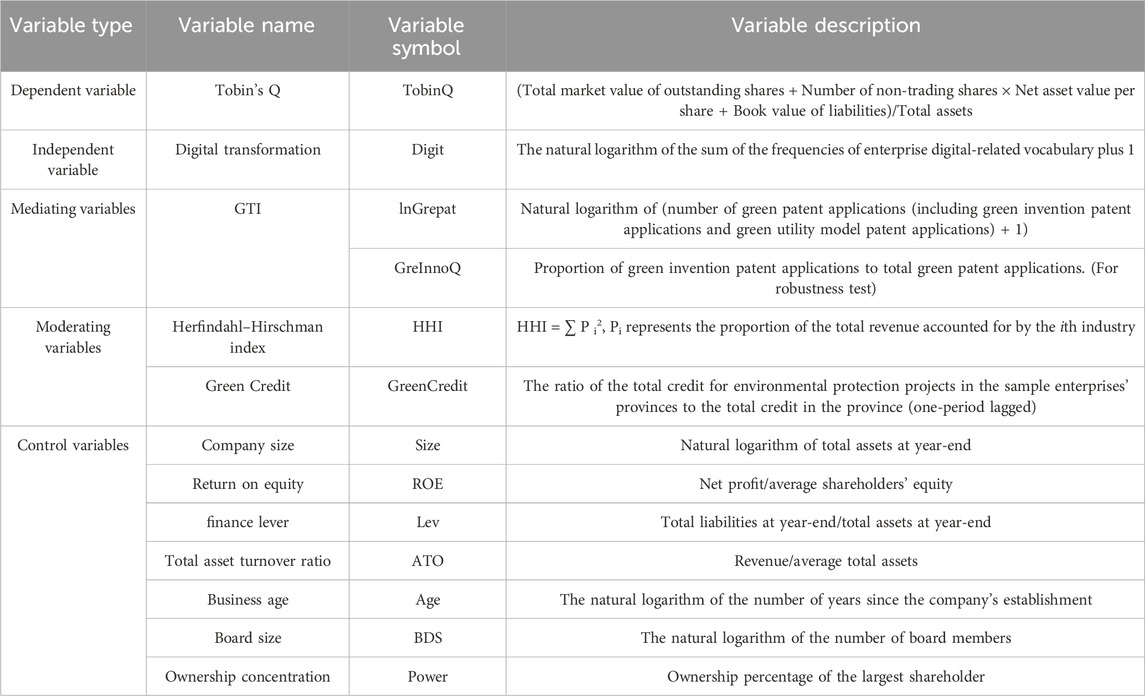

In our study, the enterprise value, as the dependent variable, is measured by Tobin’s Q (TobinQ). The Tobin’s Q ratio is the ratio of a corporate’s asset market value to their replacement cost, reflecting the market assessment of the corporate’s existing assets and the expectations for future growth potential. Although the numerator of Tobin’s Q is the market value of assets, which is susceptible to fluctuations in the stock market, there may be instances where the actual value of the firm is either overestimated or underestimated. The Tobin’s Q ratio considers risk and is less prone to distorting a corporate’s value compared to other measures (Lindenberg and Ross, 1981), it and the market-to-book value of equity ratio are, in theory and practice, equivalent metrics for assessing value creation (Varaiya et al., 1987). While a company conducting digital transformation and GTI focus more on the company’s long-term sustainability, which is associated with the company’s long-term valuation and future growth expectations. Therefore, compared to other financial performance indicators, choosing the Tobin’s Q ratio is more suitable for our research’s theme. Our research draws on the approach of Zhang and Long (2022) and Gharaibeh and Qader (2017), using Tobin’s Q ratio as a metric for measuring a corporate’s value. Since it is hard to obtain the replacement cost of Chinese public companies, we use total assets instead when making calculations. Meanwhile, Chinese listed companies currently have both circulating and non-circulating shares. For non-circulating shares, because of the absence of market data, we use the quantity of non-circulating shares multiplied by the net asset value per share to calculate their value. Refer to Table 1 for the detailed calculation formula.

Table 1. Explanation of key variables.

3.2.2 Independent variable

3.2.2.1 Digital transformation (Digit)

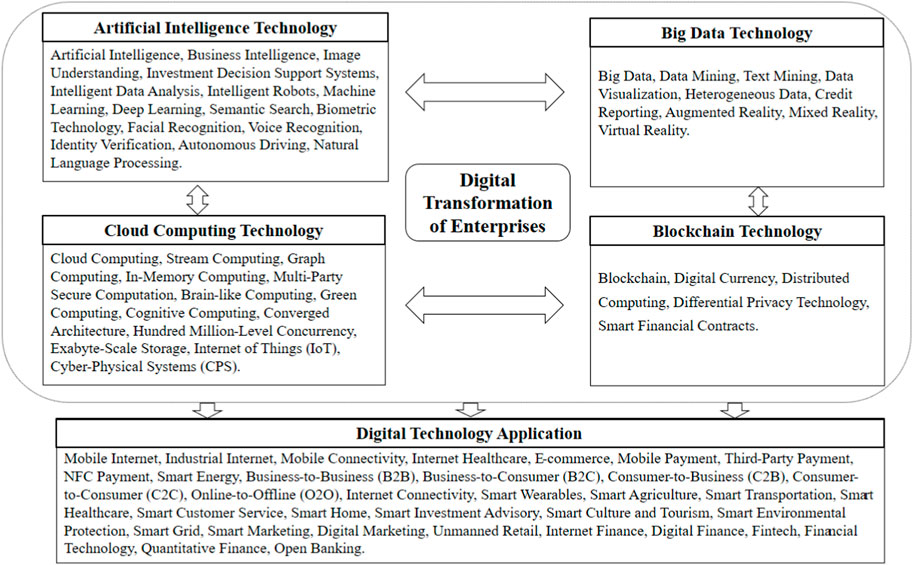

Our study draws on the approach of Wu et al. (2021), Guo et al. (2023), and Tong et al. (2024), utilizing Python tools for textual analysis to extract keywords relevant to digital transition from annual reports of public enterprises. The keywords are categorized into five dimensions: artificial intelligence technology, big data technology, cloud computing technology, blockchain technology, and digital technology applications (see Figure A1). Vocabulary frequencies are then counted for each category, and the gross vocabulary frequency for digital transformation is got by summing these counts. Because of the right-tailed distribution of the entire dataset, the total vocabulary frequency is incremented by 1 and subsequently determining the natural logarithm.

3.2.3 Mediating variables

3.2.3.1 GTI (InGrepat)

The extent of enterprise green innovation output is directly represented by the amount of enterprise green patent applications, comprising both green invention patent applications and green utility model patent applications. Referring to the approaches of Wang et al. (2021), Xu and Cui (2020), and Yu et al. (2019), the amount of green patent applications serves as a proxy indicator to measure an enterprise’s GTI in our research. Given that the data is right-skewed, the measure of corporate GTI is obtained by incrementing the number of corporate green patent applications by one and applying the natural logarithm. Our study emulates the approach of Zhang and Long (2022), utilizing the proportion of green invention patent applications relative to total green patent applications (GreInnoQ) as a robustness test indicator for GTI.

3.2.4 Moderating variables

3.2.4.1 Market competition (HHI)

The Herfindahl–Hirschman Index (HHI) is utilized to assess market competition (Harris, 1998; Hasan et al., 2018), it is a common index to measure the degree of market competition. Zou et al. (2015) indicates that the HHI serves as the most effective metric for analyzing market competition relative to other methods. Hence, we choose the HHI index to measure market competition. The greater the HHI index, the less the market competition, the higher the market concentration.

3.2.4.2 Green Credit (GreenCredit)

Green Credit (GreenCredit). Green credit refers to the credit financing provided by banking financial institutions to support the environmental protection industry, promote green civilization, and develop a green economy (Li et al., 2020). The banking sector in China is usually directly influenced by the government, with credit policies and interest rate policies often closely related to national economic policies. Green credit is the most widely used fiscal support by the Chinese government to promote green development (Hu et al., 2020). We measure the level of local government attention to and support for environmental protection and green development using the ratio of the total credit for environmental protection projects in the sample enterprises’ provinces to the total credit in the province. Considering the lag effect of green credit, we use the one-period lagged GreenCredit as the indicator for measuring green credit.

3.2.5 Control variables

Given that other elements may also impact firm value, our study selects the following controlled variables: company size (Size), return on equity (ROE), finance lever (Lev), total asset turnover (ATO), firm age (Age), board size (BDS), and ownership concentration (Power).

Details regarding the key variables above are included in Table 1.

3.3 Empirical model

3.3.1 Basic model and mediation effect model

To verify the research Hypothesis 1, Hypothesis 2, and Hypothesis 3, our study accounts for industry and year, and establishes the following model.

In the above models, i signifies the corporate, t signifies the year, the dependent variable TobinQ signifies enterprise value, the independent variable Digit signifies the firm’s digital transformation index, and the mediator variable Mediator represents the firm’s GTI. ControlVar indicates the aforementioned control variables, Industry signifies industry virtual variables, Year signifies year virtual variables, and ε is the model’s stochastic disturbance term. Equation 1 is employed to test Hypothesis 1. If the regression outcomes of this model indicate that α1 is significantly positive, it shows that digital transformation can notably enhance firm value, thus supporting Hypothesis 1, Equation 2 is utilized to examine hypotheses H2. If the coefficient β1 in the regression results of the Equation 2 is significantly positive, which reveals that digital transformation can notably enhance GTI, thus supporting hypotheses H2. Referencing the approaches of Wen et al. (2004) and Tong et al. (2024), the hypotheses H3 are tested using a combined approach involving Equations 1–3, specifically to explore the mediatory effect of GTI. We follow the specific steps for step-by-step verification (referred to as the three-step verification method). First test Equation 1, then test Equation 2. If coefficients α1 and β1 are both significantly positive, proceed to test Equation 3. If coefficient λ2 in Equation 3 is also significantly positive, it indicates a significant mediating effect. Building on this, if regression coefficient λ1 in Equation 3 is also significantly positive, it shows that part of the influence of digital transition on corporate value is achieved through GTI, implying that enterprise GTI exerts a marked partial mediating effect.

3.3.2 Moderated mediation model

To verify the research Hypothesis 4, we draw on the method by Muller et al. (2005), Preacher and Hayes (2004), and Hasan et al. (2018). Accounting for industry and year, our study establishes the following model.

In the Equations 4–6, the moderator variables

4 Empirical research results and analysis

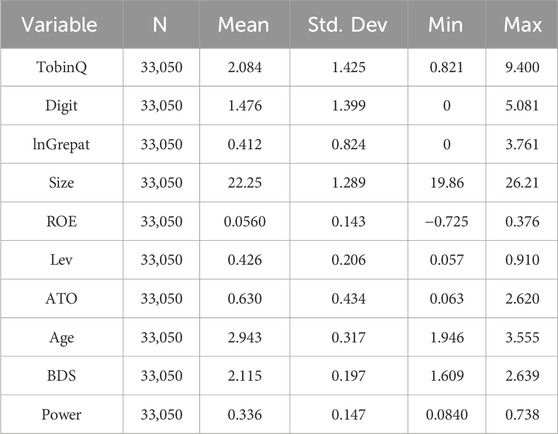

4.1 Descriptive statistics

The statistical description of the key variables is shown in Table 2. As shown in Table 2, the Tobin’s Q value ranges from 0.821 to 9.400, indicating a significant variation in the value of the sample companies. Featuring a mean of 2.084 and a standard deviation of 1.425, this implies that the majority of enterprises have a Tobin’s Q value around 2, which accords with the current situation in the Chinese market. The range of corporate digital transformation indicator values is from 0 to 5.081, featuring a mean of 1.476 and a standard deviation of 1.399. The data follows a right-skewed distribution, which indicates that the whole digitalization level of sample enterprises is relatively low, suggesting that there exists still significant potential for the implementation of emerging information technologies within Chinese companies. The average of the GTI index is 0.412, with a 0.824 standard deviation. This indicates that there exists a significant disparity in GTI among the sampled enterprises, and overall, it is relatively low.

Table 2. Descriptive statistics results.

4.2 Baseline regression analysis

4.2.1 Digital transformation and corporate value

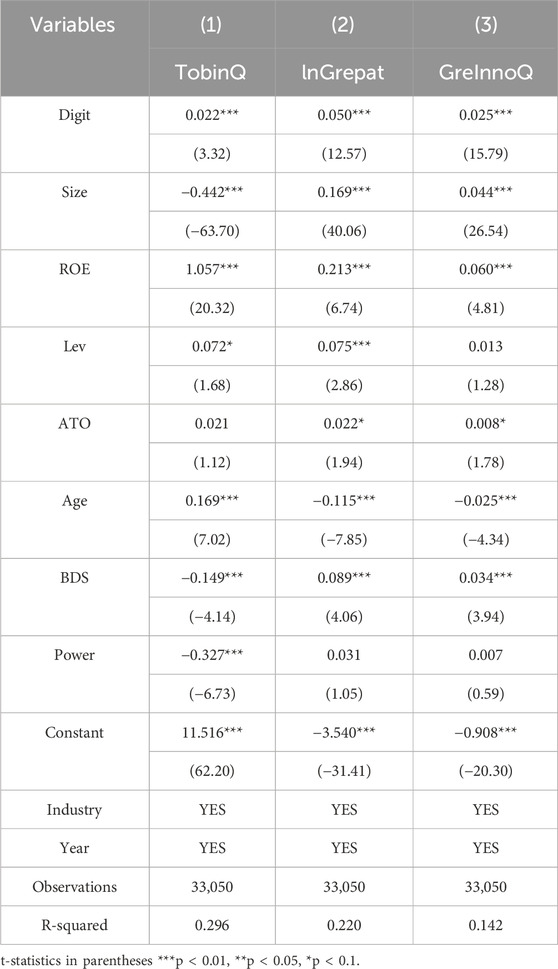

To test Hypothesis 1, Equation 1 has been established. The regression outcomes of Equation 1 are presented in Column (1) of Table 3. After accounting for the influence of industry-specific factors, time-varying effects, and other contributing factors, the coefficient estimate for Digit is 0.022 (p < 0.01), It verifies that digital transformation promotes the enhancement of corporate value, thus confirming Hypothesis 1.

Table 3. Digital transformation and corporate value, digital transformation and GTI.

4.2.2 Digital transformation and GTI

To verify Hypothesis 2, Equation 2 has been set. Column (2) of Table 3 show the regression outcomes of Equation 2, where the coefficient for digital transformation is 0.050 (p < 0.01). It suggests that digital transformation can enhance enterprises’ GTI, thereby confirming Hypothesis 2.

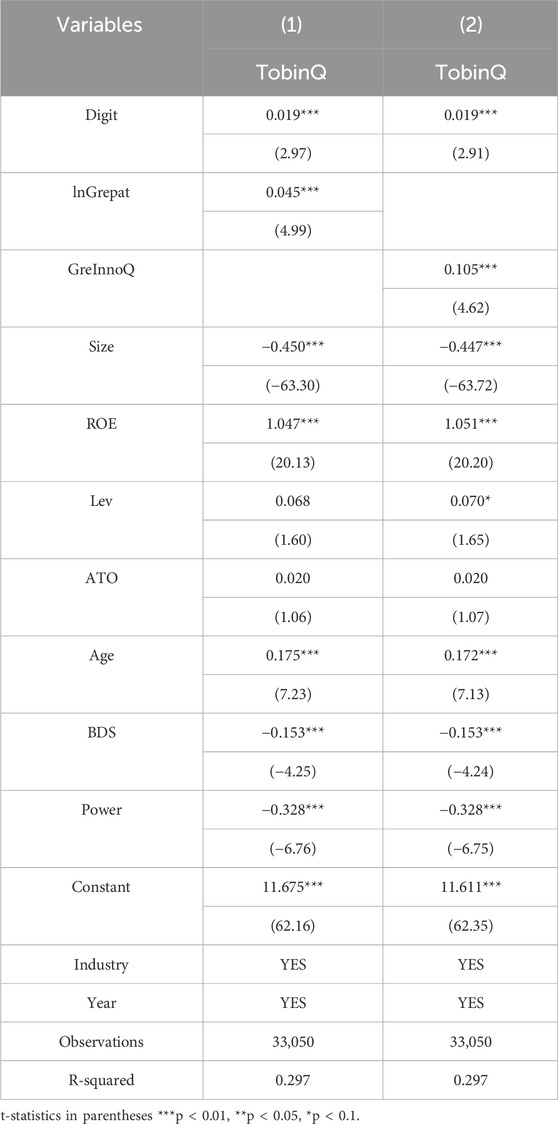

To ensure the robustness of the result, we replaced the dependent variable, substituting the lnGrepat with GreInnoQ, and conducted the regression analysis again. The result is documented in Column (3) of Table 3, where the coefficient of Digit is 0.025 (p < 0.01). It indicates that the conclusion that digital transition enhances enterprises’ GTI remains robust.

4.3 Robustness test

To validate the Hypothesis 1 and ensure the reliability of the research conclusion, we carry out a set of robustness checks, including instrumental variable method, replacing an independent variable, and adjustment for sample periods. Empirical results consistently confirm that digital transformation of enterprises significantly enhances firm value.

4.3.1 Instrumental variable method

In order to alleviate potential endogeneity concerns in this research, such as unaccounted variable bias, inverse causality, and sampling bias, we introduce the instrumental variable method. Drawing on the approaches of Yang and Liu (2018) and Tong et al. (2024), our study uses the degree of urban digitalization as an instrumental variable, denoted as City_Dig, to represent the degree of urban digitalization. Following the “China Internet Development Report 2019” released at the 6th World Internet Conference, the digital technology development levels of 31 provinces in mainland China are ranked. Cities with a high digitalization index consisting of Beijing, Shanghai, Shenzhen, Hangzhou, Xiamen, Guangzhou, Wuhan, Nanjing, Zhuhai, and Suzhou, have the variable City_Dig set to 1, while other cities have the variable City_Dig set to 0. Since the degree of urban digitalization can influence the digital transition of domestic enterprises by providing necessary infrastructure and fostering a conducive technological environment, it meets the correlation criterion for an instrumental variable. To address exogeneity, we argue that urban digitalization is largely driven by long-term factors such as government policies or infrastructure development that are independent of unobserved firm-specific shocks affecting digital transition.

We employ the two-stage least squares (2SLS) for the final parameter estimation. The estimated outcomes are displayed in Table 4. Column (1) of Table 4 displays the first-stage estimation outcomes. We observe that the coefficient for City_Dig is 0.16 (p < 0.01), with an F-value greater than 10. It reveals that the instrumental variable for urban digitalization level is positively related to the endogenous explanatory variable of corporate digital transformation. It conforms to the correlation test for the instrument variable. In the second stage, the estimated outcomes in Column (2) of Table 4 reveal that the coefficient for the predicted value of digital transformation (Prediction—Digit) is 0.371 (p < 0.01), with an F-value greater than 10, and it remains significant and positive. After accounting for endogeneity effects, the relation between digital transformation and corporate value remains unchanged.

Table 4. Instrumental variable method test results.

4.3.2 Substitute the explanatory variable

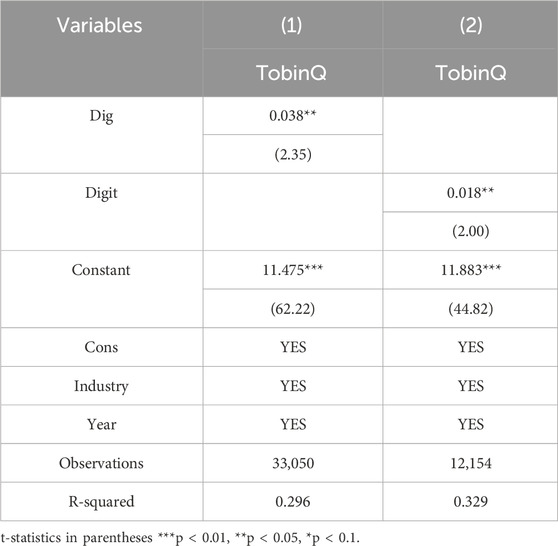

In the descriptive analysis of the main sample presented earlier, some enterprises have been in the process of digital transition while others have not. Among the companies that have undergone digital transition, some may disclose more keywords correlated to digital transformation than what is actually the case in their annual reports, while others may disclose fewer. To remove the potential effect of these scenarios on the evidence-based outcomes, we conduct a robustness check by substituting the independent variable. Following the method of Zhang et al. (2022), our study sets a dummy variable Dig based on whether a firm has undergone digital transition. Firms that have undergone digital transition are set a value of 1, while firms that have not are set a value of 0. And then the variable is embedded into Equation 1 for re-estimation. The regression outcomes are listed in column (1) of Table 5. The coefficient for Dig is 0.038 (p < 0.05), revealing that digital transformation enhances firm value, thus reaffirming Hypothesis 1.

Table 5. Robustness checks by replacing explanatory variables and adjusting the sample period.

4.3.3 Adjust the sample period

Since 2015, China’s digital economy has stepped into a phase of accelerated development (Global Times, 2020). When studying digital transformation, some scholars have chosen 2015 as the starting year for their research. However, in 2015, China experienced a stock market crash (Tang et al., 2020). Considering that major stock market events can impact corporate value performance, we exclude the year 2015 from the analysis. Meanwhile, as the influence of the global COVID-19 pandemic on enterprise investment and operations during the sample period, we ultimately select the data period from 2016 to 2019 for robustness check. The empirical outcomes are listed in column (2) of Table 5, where the coefficient of Digit is 0.018 (p < 0.05). It indicates that the conclusion that digital transition enhances firm value remains robust.

4.4 The mediation effect of GTI

To verify Hypothesis 3, we set Equation 3. Column (1) of Table 6 presents the regression outcomes of Equation 3. Referring to Wen et al.’s (2004) three-step verification method, and according to the mediating mechanism where digital transformation influences GTI, which in turn impacts corporate value, we conduct a mediation effect test based on the regression outcomes of Equations 1, 2 in Table 3 and Equation 3 in Column (1) of Table 6. Our study finds that the coefficients of Digit in Equations 1, 2 are both statistically notably positive. Meanwhile, in Equation 3 of Column (1) of Table 6, the coefficient of the mediating variable GTI is 0.045 (p < 0.01), indicating that GTI has a significant positive mediation effect between digital transformation and firm value. According to Column (1) of Table 6, after controlling for GTI, the coefficient of Digit in Equation 3 remains statistically significant positive, indicating that GTI acts as a positive partial mediator. Firstly, digital transformation enhances the GTI of enterprises by boosting research and development capabilities, alleviating financial constraints, and enhancing innovation output. Secondly, GTI helps enterprises lower resource waste, cut costs, enhance manufacturing efficiency, improve environmental performance, and thereby increase enterprise value.

Table 6. Regression results of the mediating effect of GTI.

To verify the robustness of the intermediary effect, we use the following two methods. Firstly, we also replace lnGrepat with GreInnoQ and add it to Equation 3, with the empirical results shown in column (2) of Table 6. Where the coefficient of GreInnoQ is 0.105 (p < 0.01), combining the results of Equations 1, 2, it indicates that Hypothesis 3 still holds. Secondly, we employ the Sobel test to examine the aforementioned mediating paths. The test outcomes reveal that the mediating effect of GTI accounts for 51.53%, Z = 10.42 (p = 0.000) Thus, the mediating effects are confirmed once again. According to the empirical analysis above, we find that digital transformation markedly fosters value creation by enhancing GTI of firms. Hypothesis 3 is supported by the findings.

4.5 Moderated mediation analysis

According to the interdependence theory, the mediating effect will be affected by specific scenarios (moderating variables). In order to further investigate whether the intermediary effect of GTI is affected by market competition and green credit, or whether the impact of GTI on corporate value depends on market competition and green credit, or both of them exist. We constitute moderated mediation model (Equations 4–6) and apply layer regression analysis, the results are listed in columns (1) (2) (3) of Tables 7, 82.

Table 7. Moderated mediation analysis: the effect of market competition.

Table 8. Moderated mediation analysis: the effect of green credit.

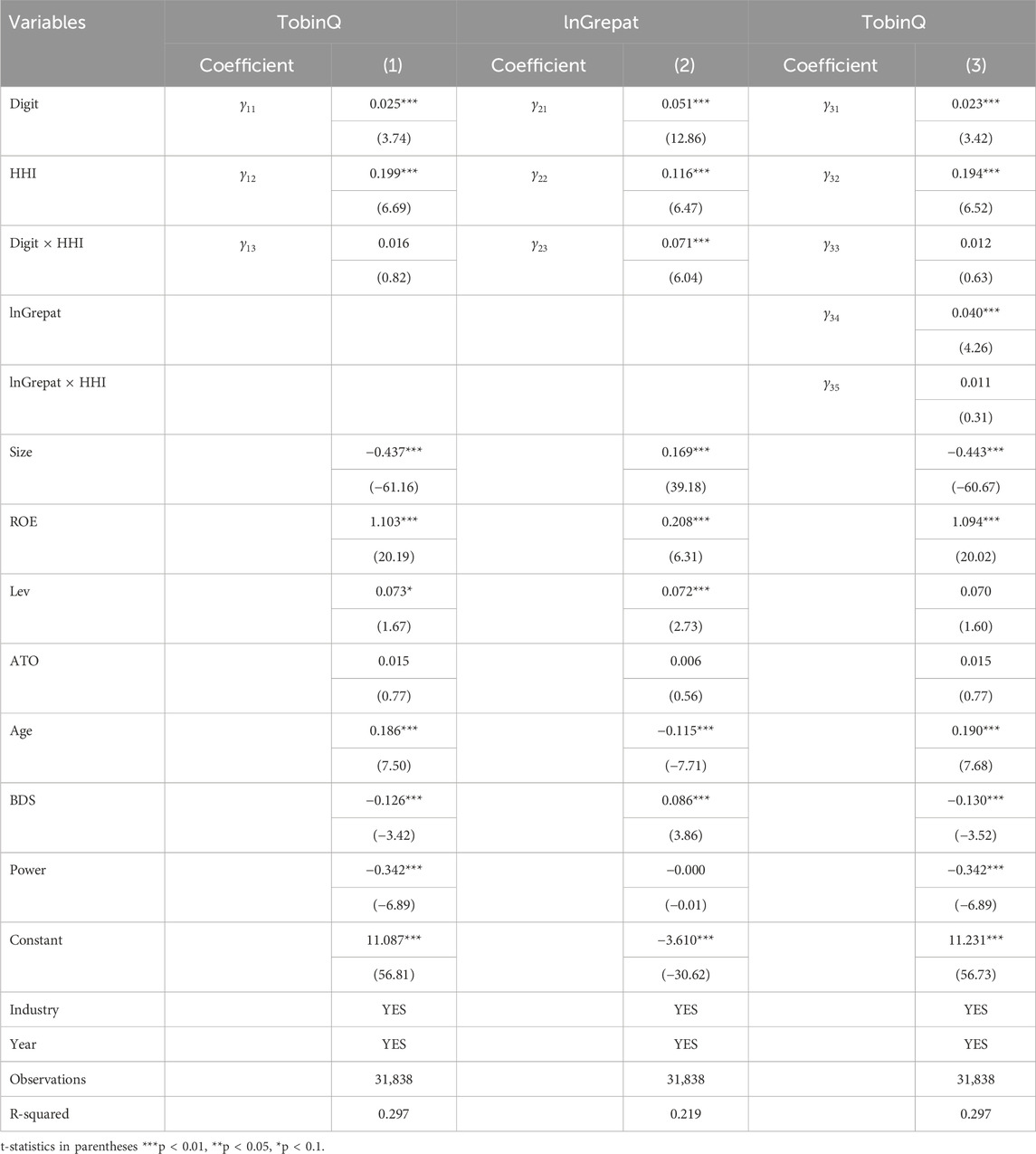

Table 7 shows the moderating role of market competition in the mediating effect. In column (1) of Table 7, we record

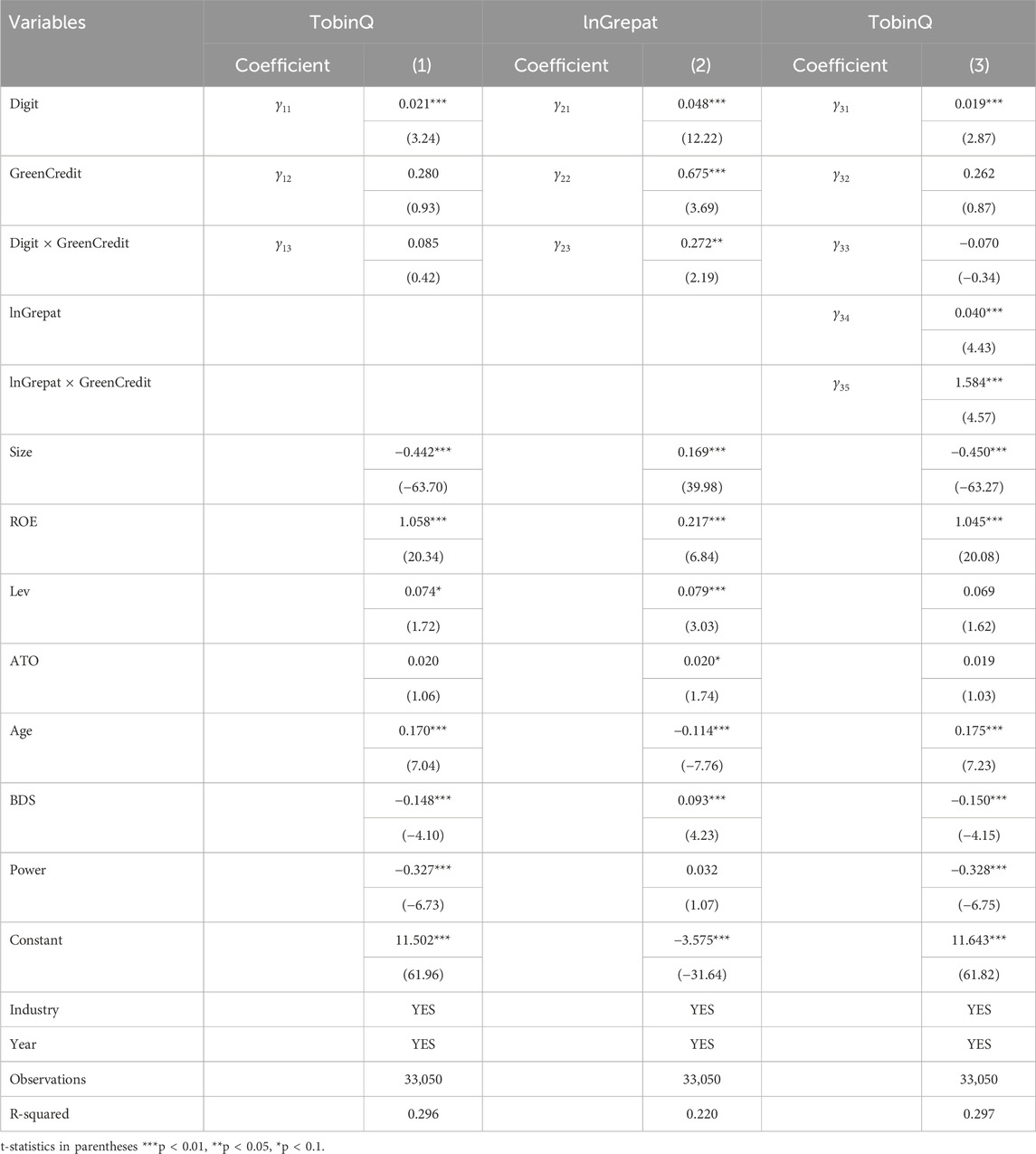

Table 8 shows the moderating role of green credit in the mediating effect. Based on columns (1) to (3) of Table 8,

4.6 Heterogeneity analysis

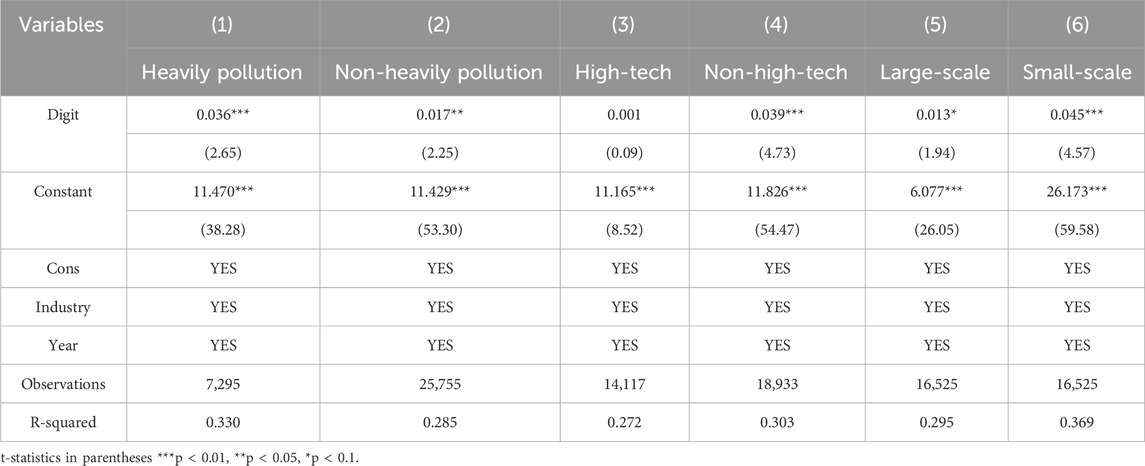

4.6.1 Heterogeneity in heavy pollution characteristics

Unlike other enterprises, heavily polluting companies, because of their severe pollution, elevated energy consumption, and excessive discharges, urgently require leveraging GTI to develop green products, lower energy consumption, and decrease contamination, thereby lowering compliance costs and achieving a green transformation. Based on this, the sampled enterprises are separated into heavily polluting and non-heavily polluting enterprises in accordance with the “Environmental Inspection Industry Classification Management Directory of Listed Companies” issued in 2008. Then we conduct multiple regression by group, and the estimated outcomes are listed in columns (1) and (2) of Table 9. The Digit coefficient for heavily polluting firms is 0.036 (p < 0.01), while the Digit coefficient for non-heavily polluting firms is 0.017 (p < 0.05). Due to the markedly higher coefficient of digital transformation for heavily polluting companies compared to non-heavily polluting companies, it illustrates that digital transformation has a higher value-enhancing effect on heavily polluting companies compared to other companies. The result shows that digital transition, by improving the level of GTI within these enterprises, is more efficient in heavily polluting enterprises, promoting greater enhancement of corporate value and achieving sustainable development.

Table 9. Results of heterogeneity analysis.

4.6.2 Heterogeneity in high-tech characteristics

The different attributes of technology also influence the action of digital transformation in promoting corporate value. Drawing on industry classification standards in China, the sample enterprises are classified into high-tech and non-high-tech enterprises for grouped multiple regression analysis. The regression outcomes are listed in columns (3) and (4) of Table 9. The coefficient of Digit for high-tech companies doesn’t meet the significance criteria, while the coefficient of Digit for non-high-tech companies is 0.039 (p < 0.01). Thus, it is obvious that the effect of digital transformation on enhancing the value of high-tech corporates is not significant. Since high-tech companies already possess more advanced technologies compared to non-high-tech companies, digital transformation for them is akin to adding icing on the cake. However, digital transformation can remarkably increase the value of non-high-tech firms. This difference validates the performance of digital transformation in promoting corporate transformation and upgrading, as well as balanced development among enterprises. It also shows that there exists a partial replacement effect between digital transformation and high-new technology.

4.6.3 Heterogeneity in enterprise scale

To examine whether the role of digital transition on enterprise value differs by company size, we group the sample companies into large-scale and small-scale companies in accordance with the median company size, then conduct regression analysis. In Table 9, columns (5) and (6) show the analysis outcomes. The coefficient for digital transformation in large-scale enterprises is 0.013 (p < 0.1). For small-scale enterprises, the coefficient is 0.045 (p < 0.01). The results indicate that digital transformation more notably benefits smaller companies compared to larger ones. The reasons behind this may be twofold. On one hand, larger enterprises typically possess abundant resources and more robust internal control systems. Before undergoing digital transformation, larger enterprises already feature strong business models, innovation capabilities, resource integration abilities, and decision-making skills. Consequently, the effect of digital transition on promoting their operations is not as significant as it is for smaller enterprises. On the other hand, compared to larger enterprises, smaller-scale businesses are generally less mature in various aspects but have greater potential for growth. Therefore, after undergoing digital transformation, they can more rapidly integrate resources, optimize business processes, innovate business models and product offerings, thereby significantly enhancing enterprise value.

5 Discussion and conclusion

Numerous prior studies have investigated the relationship between digital transformation and firm value, but few have incorporated GTI as a channel in their research. GTI, distinct from traditional technological innovation, plays an important role in achieving sustainable development for enterprises (Li, 2005; Beltramello et al., 2013). Therefore, this paper investigates the correlation between digital transformation, GTI, and corporate value, and further explores the moderating effect of market competition on these relationships.

Aligned with past findings, we find that digital transformation can promote the enhancement of corporate value. However, we extend our research by also investigating the influence of digital transformation on corporate value in relation to attributes such as heavy pollution, high-tech status, and company size. We find that the positive influence of digital transformation on corporate value is more pronounced in heavily polluting companies, non-high-tech companies, and smaller companies. This indicates that the attributes of different companies can influence how digital transformation improves corporate value.

We consider GTI as an intermediary channel between digital transformation and corporate value, we argue that GTI serves as a partial mediator in the relationship. Specifically, digital transformation enhances the level of green innovation within companies by alleviating financing constraints, gaining more resources and support for green technological innovation, and continuously improving innovation methods and processes (Jing et al., 2022; Chen and Zhang, 2023). The improvement in a company’s green innovation level helps reduce environmental pollution costs, gain marginal profits and competitive advantages, and increase enterprise value (Wang et al., 2021; Chang, 2011; Chen and Laisb, 2006), thereby promoting the sustainable development of the company.

In addition, we further analyze market competition’s and green credit’s moderating effect on the mediating relationship between digital transformation and enterprise value. We find that for companies facing lower market competition intensity, digital transformation is more effective in promoting GTI. In other words, companies with lower market competition intensity have more resources, face less competitive pressure, and are more sensitive to the technological innovations of competitors (Zhang, 2019; Turner et al., 2010). With the support of digital technology, these companies can allocate resources more efficiently, improve resource utilization, and respond more quickly to market changes (Chen and Yang, 2022; Zhang and Long, 2022), thereby channeling more funds and technological resources into green technological innovation. Meanwhile, we also find that green credit not only positively moderates the relationship between corporate digital transformation and GTI but also positively moderates the impact of GTI on corporate value. Our findings confirm that green credit promotes the improvement of GTI levels through digital transformation. This is because green credit increases financial support for corporate environmental projects (Tian et al., 2024), while digital transformation effectively utilizes and allocates these resources (Kumari, 2021; Liu et al., 2024; Jiang and Li, 2024), thereby enhancing the level of GTI in enterprises. We also confirm that the presence of green credit contributes to the role of GTI in enhancing corporate value. This is because the provision of green credit promotes the improvement of GTI, which in turn helps reduce environmental costs caused by pollution (Wang et al., 2021). Additionally, the production of green products enables companies to gain competitive advantages and social credibility (Yu et al., 2010), thereby increasing corporate value. As green credit is a policy strategy employed by the Chinese government to promote environmental protection and green development, its issuance reflects the level of importance local governments attach to environmental protection and green growth. The above also highlights the level of government attention and support for environmental protection, which plays a crucial role in fostering corporate green innovation and green development. As enterprises are important agents of society, when they all fulfill their environmental responsibilities, prioritize environmental protection, or achieve green transformation, our environment will be greatly improved.

Our study provides following implications. First, our research shows that digital transformation can enhance corporate value. Enterprises should emphasize the application and secondary development of digital technologies, and increase resource investment and mechanism building for digital transformation. Second, GTI serves as a mediator between digital transformation and corporate value. Enterprises need to incorporate GTI into their development plans within their digital transformation strategies. By increasing investment and leveraging digital technology to integrate and optimize resources, thereby boosting GTI. Third, we find that for enterprises facing lower market competition intensity, digital transformation is prone to promote GTI. Therefore, enterprises should adjust their strategies in a timely manner during their development, avoiding fierce market competition, and investing in GTIs that can bring long-term benefits. By leveraging digital technologies, they can boost the efficiency of R&D, cut innovation costs, and achieve green transformation and sustainable development. Forth, we also find that green credit not only promotes the enhancement of GTI through digital transformation but also contributes to the improvement of GTI’s impact on corporate value. Green credit is a policy strategy employed by the Chinese government to promote environmental protection and green development, and its issuance reflects the level of importance and support that local governments place on environmental protection and green growth. Therefore, local governments should guide and support environmental protection and green development through policies and financial incentives. They should also guide and supervise banking and financial institutions to support local environmental industries and corporate green development by setting up reasonable green credit programs.

Our study has two main limitations. First, in addition to being influenced by market competition and green credit, the mediating relationship of GTI between digital transformation and firm value is also influenced by other external environmental factors, such as pollution emissions. Therefore, future research can further expand the study of these influencing factors. Second, Digital transformation may be defined differently across various markets or regions, raising concerns about its generalizability. Researchers may conduct in-depth study on digital transition in other markets or regions. Finally, relying on green patent applications as a proxy for GTI may oversimplify the complexity of green innovation activities. We call for further research to explore indicators that can comprehensively evaluate green innovation activities.

Data availability statement

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding author.

Author contributions

LZ: Conceptualization, Data curation, Funding acquisition, Writing–original draft, Writing–review and editing. ZS: Formal Analysis, Investigation, Methodology, Validation, Writing–review and editing.

Funding

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article. The research is partially funded by Leshan Vocational and Technical College under the major program “Research on Accounting for Digital Teaching Resources in Universities (KY2024001)”.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Supplementary material

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenvs.2025.1485881/full#supplementary-material

Footnotes

1https://www.cac.gov.cn/2023-05/22/c_1686402318492248.htm

2When conducting the analysis of moderated mediation effects, the missing values for the HHI indicator are removed, leaving 31,838 observations.

References

Beltramello, A., Haie-Fayle, L., and Pilat, D. (2013). “Why new business models matter for green growth,” in OECD Green Growth Papers, 2013-01 (Paris: OECD Publishing). doi:10.1007/s11142-023-09753-0

Chang, C. H. (2011). The influence of corporate environmental ethics on competitive advantage: the mediation role of green innovation. J. Bus. Ethics 104 (3), 361–370. doi:10.1007/s10551-011-0914-x

Chen, H., and Zhang, L. (2023). ESG performance, digital transformation and enterprise value enhancement. J. Zhongnan Univ. Econ. Law (03), 136–148. doi:10.19639/j.cnki.issn1003-5230.2023.0030

Chen, W., and Srinivasan, S. (2024). Going digital: implications for firm value and performance. Rev. Account. Stud. 29 (29), 1619–1665. doi:10.1007/s11142-023-09753-0

Chen, Y., and Yang, M. (2022). Digital transformation, business mode innovation and business efficiency. Econ. Forum 36, 135–146.

Chen, Y. S., and Laisb, W. (2006). The influence of green innovation performance on corporate advantage in taiwan. J. Bus. Ethics 67 (04), 331–339. doi:10.1007/s10551-006-9025-5

Ding, N., Ren, Y. N., and Zuo, Y. (2020). Do the losses of the green-credit policy outweigh the gains? A PSM-DID cost-efficiency analysis based on resource allocation. J. Financ. Res. 4, 112–130.

Ding, Y., and Qin, Z. (2021). The impact of information and communication technology on green economic efficiency: an empirical study based on the panel tobit model. Study Pract. (4), 32–43. doi:10.19624/j.cnki.cn42-1005/c.2021.04.004

Gharaibeh, A. M. O., and Qader, A. A. A. A. (2017). Factors influencing firm value as measured by the Tobin’s Q: empirical evidence from the Saudi Stock Exchange (TADAWUL). Int. J. Appl. Bus. Econ. Res. 15 (6), 333–358.

Global Times (2020). China launches another public test of digital currency in Suzhou, supporting online and offline payment. Glob. Times. Available at: https://www.globaltimes.cn/page/202012/1209124.shtml.

Guo, F., Yang, S., and Cai, Z. (2021). Does the construction of innovative cities improve the quantity and quality of enterprise innovation? Micro-evidence from Chinese industrial enterprises. Industrial Econ. Res. (03), 128–141. doi:10.13269/j.cnki.ier.2021.03.010

Guo, F., Yang, S., and Cai, Z. (2023). Does digital transformation of enterprises improve the quantity and quality of green technology Innovation? Text analysis based on annual reports of Chinese listed companies, 146–162. doi:10.19592/j.cnki.scje.400349

Guo, F., Yang, S., and Ren, Y. (2022). The digital economy, green technology innovation and carbon emissions—empirical evidence from Chinese city-level data. J. Shaanxi Normal Univ. Philosophy Soc. Sci. Ed. (03), 45–59. doi:10.15983/j.cnki.sxss.2022.0507

Hajli, M., Sims, J. M., and Ibragimov, V. (2015). Information technology (IT) productivity paradox in the 21st century. Int. J. Prod. Perform. Manag. 64 (4), 457–478. doi:10.1108/ijppm-12-2012-0129

Han, G., Chen, T., and Liu, T. (2022). Digital transformation and enterprise capacity utilization: empirical findings from Chinese manufacturing enterprises. J. Finance Econ. 48 (9), 154–168. doi:10.16538/j.cnki.jfe.20220714.301

Harris, M. S. (1998). The association between competition and managers' business segment reporting decisions. J. Account. Res. 36 (1), 111–128. doi:10.2307/2491323

Hasan, I., Kobeissi, N., Liu, L., and Wang, H. (2018). Corporate social responsibility and firm financial performance: the mediating role of productivity. J. Bus. Ethics 149, 671–688. doi:10.1007/s10551-016-3066-1

Hu, Y., Jiang, H., and Zhong, Z. (2020). Impact of green credit on industrial structure in China: theoretical mechanism and empirical analysis. Environ. Sci. Pollut. Res. 27, 10506–10519. doi:10.1007/s11356-020-07717-4

Jiang, W., and Li, J. (2024). Digital transformation and its effect on resource allocation efficiency and productivity in Chinese corporations. Technol. Soc. 78, 102638. doi:10.1016/j.techsoc.2024.102638

Jiang, X., Wang, R., Guan, L., and Du, C. (2023). The impact of intelligent finance on financial performance from the perspective of digital transformation. Friends Account. (20), 44–51.

Jing, Y., Wen, W., and He, Y. (2022). Impact of digital transformation on corporate green innovation: evidence from China’s manufacturing listed companies. Finance Trade Res. (07), 69–83. doi:10.19337/j.cnki.34-1093/f.2022.07.006

Kumari, S. (2021). Kanban and AI for efficient digital transformation: optimizing process automation, task management, and cross-departmental collaboration in agile enterprises. Blockchain Technol. Distri. Syst. 1 (1), 39–56.

Lanzolla, G., Pesce, D., and Tucci, C. L. (2021). The digital transformation of search and recombination in the innovation function: tensions and an integrative framework. J. Prod. Innovation Manag. 38 (1), 90–113. doi:10.1111/jpim.12546

Li, P. (2005). Study on the subject system of green technology Innovation. Stud. Sci. Sci. 23, 414–418. doi:10.3969/j.issn.1003-2053.2005.03.024

Li, X., and Cui, M. (2024). Can green innovation promote high-quality development of enterprises? An examination based on internal and external pathways. J. Finance Econ. (02), 61–71. doi:10.19622/j.cnki.cn36-1005/f.2024.02.005

Li, Y., Hu, H., and Li, H. (2020). Empirical analysis of the impact of green credit on the upgrading of China’s industrial structure: based on Chinese provincial panel data. Econ. Problems 1, 37–43. doi:10.16011/j.cnki.jjwt.2020.01.005

Li, Z. (2023). Research on the impact of digital transformation on the promotion of enterprise value and transmission path. Econ. Problems (11), 25–32. doi:10.16011/j.cnki.jjwt.2023.11.007

Liang, D., and Liu, T. (2017). Does environmental management capability of Chinese industrial firms improve the contribution of corporate environmental performance to economic performance? Evidence from 2010 to 2015. J. Clean. Prod. 142, 2985–2998. doi:10.1016/j.jclepro.2016.10.169

Lindenberg, E. B., and Ross, S. A. (1981). Tobin's $q$ ratio and industrial organization. J. Bus. 54, 1–32. doi:10.1086/296120

Liu, S., and Jin, J. (2023). Digital reinvention of the value creation capacity for specialized and sophisticated enterprises: theory, mechanism, pattern and path. Res. Financial Econ. Issues (11), 3–13. doi:10.19654/j.cnki.cjwtyj.2023.11.001

Liu, Y., and He, Q. (2024). Digital transformation, external financing, and enterprise resource allocation efficiency. Manag. Decis. Econ. 45 (4), 2321–2335. doi:10.1002/mde.4136

Liu, Z., Tong, L., and Zhong, H. (2024). Digital transformation and green technology innovation in enterprises: evidence from listed manufacturing companies. Soc. Sci. Guangdong (01), 37–47.

Matarazzo, M., Penco, L., Profumo, G., and Quaglia, R. (2021). Digital transformation and customer value creation in Made in Italy SMEs: a dynamic capabilities perspective. J. Bus. Res. 123, 642–656. doi:10.1016/j.jbusres.2020.10.033

Muller, D., Judd, C. M., and Yzerbyt, V. Y. (2005). When moderation is mediated and mediation is moderated. J. Personality Soc. Psychol. 89 (6), 852–863. doi:10.1037/0022-3514.89.6.852

Nickell, S. J. (1996). Competition and corporate performance. J. political Econ. 104 (4), 724–746. doi:10.1086/262040

Nie, S., Li, S., and Li, H. (2024). Whether digital transformation can improve enterprise’s environmental-social-governance performance: the moderating effect of mechanism test and internal and external collaborative governance. Ecol. Econ. (01). Available at: https://link.cnki.net/urlid/53.1193.F.20240125.1332.004.

Oerlemans, L. A., Meeus, M. T., and Boekema, F. W. (2001). Firm clustering and innovation: determinants and effects. Pap. regional Sci. 80 (3), 337–356. doi:10.1111/j.1435-5597.2001.tb01803.x

Pei, X., Liu, Y., and Wang, W. H. (2023). Digital transformation of enterprises: driving factors, economic effects and strategic choices. Reform (5), 124–137.

Peng, Y., and Tao, C. (2022). Can digital transformation promote enterprise performance? —from the perspective of public policy and innovation. J. Innovation and Knowl. 7 (3), 100198. doi:10.1016/j.jik.2022.100198

Preacher, K. J., and Hayes, A. F. (2004). SPSS and SAS procedures for estimating indirect effects in simple mediation models. Behav. Res. Methods, Instrum. and Comput. 36 (4), 717–731. doi:10.3758/bf03206553

Qi, H., Cao, X., and Liu, Y. (2020). The influence of digital economy on corporate governance: analyzed from information asymmetry and irrational behavior perspective. Reform (04), 50–63.

Shi, R., Zhou, H., Li, X., Miao, X., and Zhao, X. (2024). Green finance, investor preferences, and corporate green innovation. Finance Res. Lett. 66, 105676. doi:10.1016/j.frl.2024.105676

Tang, M., Liu, Y., Hu, F., and Wu, B. (2023). Effect of digital transformation on enterprises' green innovation: empirical evidence from listed companies in China. Energy Econ. 128, 107135. doi:10.1016/j.eneco.2023.107135

Tang, S., Wu, X., and Zhu, J. (2020). Digital finance and enterprise technology innovation:structural feature, mechanism identification and effect difference under financial supervision. Manag. World 36 (5), 52–66. doi:10.19744/j.cnki.11-1235/f.2020.0069

Tian, J., Sun, S., Cao, W., Bu, D., and Xue, R. (2024). Make every dollar count: the impact of green credit regulation on corporate green investment efficiency. Energy Econ. 130, 107307. doi:10.1016/j.eneco.2024.107307

Tong, Z., Li, B., and Yang, L. (2024). Digital transformation, competitive strategy and value creation: a test based on enterprise life cycle theory. Sci. and Technol. Prog. Policy (01), 1–10. doi:10.6049/kjjbydc.H202308136

Turner, S. F., Mitchell, W., and Bettis, R. A. (2010). Responding to rivals and complements: how market concentration shapes generational product innovation strategy. Organ. Sci. 21 (4), 854–872. doi:10.1287/orsc.1090.0486

Varaiya, N., Kerin, R. A., and Weeks, D. (1987). The relationship between growth, profitability, and firm value. Strategic Manag. J. 8 (5), 487–497. doi:10.1002/smj.4250080507

Verhoef, P. C., Broekhuizen, T., Bart, Y., Bhattacharya, A., Qi Dong, J., Fabian, N., et al. (2021). Digital transformation: a multidisciplinary reflection and research agenda. J. Bus. Res. 122, 889–901. doi:10.1016/j.jbusres.2019.09.022

Vial, G. (2021). Understanding digital transformation: a review and a research agenda. Manag. Digit. Transform., 13–66. doi:10.1016/j.jsis.2019.01.003

Wang, M., Li, Y., and Wang, Z. (2021). U-shaped relationship between enterprises, environmental performance and economic performance of green technology innovation and the moderation effect of government competition regulation. Sci. Manag. Res. 39 (5), 107–116. doi:10.19445/j.cnki.15-1103/g3.2021.05.016

Wang, X., and Wang, Y. (2021). Research on the green innovation promoted by green credit policies. J. Manag. World (06), 173–188. doi:10.19744/j.cnki.11-1235/f.2021.0085

Wang, Y., and Zhang, W. (2024). Green credit policy, market concentration and green innovation: empirical evidence from local governments’ regulatory practice in China. J. Clean. Prod. 434, 140228. doi:10.1016/j.jclepro.2023.140228

Wen, Z., Zhang, L., Hou, J., and Liu, H. (2004). Testing and application of the mediating effects. Acta Psychol. Sin. 49 (5), 614–620.

Wu, F., Hu, X., Lin, X., and Ren, X. (2021). Enterprise digital transformation and capital market performance: empirical evidence from stock liquidity. Manag. World (07), 103–144. doi:10.19744/j.cnki.11-1235/f.2021.0097

Xu, J., and Cui, J. (2020). Low-carbon cities and firms’ green technological innovation. China Ind. Econ. (12), 178–194. doi:10.19581/j.cnki.ciejournal.2020.12.008

Xue, L., Zhang, Q., Zhang, X., and Li, C. (2022). Can digital transformation promote green technology innovation. Sustainability 14 (12), 7497. doi:10.3390/su14127497

Yang, D., and Liu, Y. (2018). Why can Internet plus increase performance. China Ind. Econ. 36 (5), 80–98. doi:10.19581/j.cnki.ciejournal.2018.05.005

Yang, D., and Lu, M. (2017). Does the Internet business model affect the audit fees of listed companies? Auditing Res. 33 (6), 84–90. doi:10.3969/j.issn.1002-4239.2017.06.012

Yu, J., Chen, H., and Wang, J. (2010). Empirical study on the cycle economy and green competitiveness of listed companies in jiangsu province. Sci. and Technol. Prog. Policy (04), 82–85.

Yu, L., Zhang, W., and Bi, Q. (2019). Can environmental taxes force corporate green innovation? Audit and economy research, 79–89. doi:10.3969/j.issn.1004-4833.2019.02.008

Yu, W. (2022). Integrated model and competitive advantage of enterprise digital transformation. J. Tech. Econ. and Manag. (2), 63–68. doi:10.3969/j.issn.1004-292X.2022.02.012

Zhang, C., Chen, P., and Hao, Y. (2022). The impact of digital transformation on corporate sustainability-new evidence from Chinese listed companies. Front. Environ. Sci. 10 (10), 1–14. doi:10.3389/fenvs.2022.1047418

Zhang, J., and Long, J. (2022). Digital Transformation,Dynamic Capability,and enterprise innovation performance: empirical evidence from high-tech listed companies. Econ. Manag. (03), 74–82. doi:10.3969/j.issn.1003-3890.2022.03.010

Zhang, J., Wu, M., Chen, T., and Gao, B. (2024). Green credit, financing constraints, and corporate investment: from the perspectives of scale and efficiency. North Am. J. Econ. Finance 73, 102188. doi:10.1016/j.najef.2024.102188

Zhang, L. (2019). Intangible-investment-specific technical change, concentration and labor share. Working Paper. (UniCredit Foundation Piazza Gae Aulenti, 3 UniCredit Tower A 20154: Milan Italy).

Zhang, Y., and Han, C. (2023). Digital transformation, technological innovation, and market value of enterprises: empirical evidence from listed “specialized, refined, and innovative” companies. Statistics and Decis. 14, 163–167. doi:10.13546/j.cnki.tjyjc.2023.14.030

Zheng, Y., and Zhang, Q. (2023). Digital transformation, corporate social responsibility and green technology innovation-based on empirical evidence of listed companies in China. J. Clean. Prod. 424, 138805. doi:10.1016/j.jclepro.2023.138805

Zhou, K., Tao, Y., Wang, S., and Luo, H. (2023). Does green finance drive environmental innovation in China? Emerg. Mark. Finance Trade 59 (8), 2727–2746. doi:10.1080/1540496x.2023.2190847

Zhou, S., and Chen, Y. (2022). Research on the impact of digital economy on high-quality economic of service industry structure upgrading. J. Industrial Technol. Econ. (5), 111–121. doi:10.3969/j.issn.1004-910X.2022.05.013

Zhu, X. (2022). Does green credit promote industrial upgrading? analysis of mediating effects based on technological innovation. Environ. Sci. Pollut. Res. 29 (27), 41577–41589. doi:10.1007/s11356-021-17248-1

Zou, H., Zeng, S. X., Lin, H., and Xie, X. M. (2015). Top executives’ compensation, industrial competition, and corporate environmental performance: evidence from China. Manag. Decis. 53 (9), 2036–2059. doi:10.1108/md-08-2014-0515

Appendix 1

FIGURE A1. Structured characteristic word map of enterprise digital transformation.

Keywords: digital transformation, green technology innovation, corporate value, sustainable development, market competition, green credit

Citation: Zhang L and Song Z (2025) Digital transformation, green technology innovation and corporate value. Front. Environ. Sci. 13:1485881. doi: 10.3389/fenvs.2025.1485881

Received: 25 August 2024; Accepted: 13 January 2025;

Published: 05 February 2025.

Edited by:

Jinyu Chen, Central South University, ChinaReviewed by:

Kai Zhang, Shandong University of Finance and Economics, ChinaAlessandra Lardo, University of Naples Parthenope, Italy

Copyright © 2025 Zhang and Song. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Lijuan Zhang, MTgyMjgzOTcwMDRAMTYzLmNvbQ==