Kesen Zhang

Kesen Zhang Zhen Pan2*

Zhen Pan2* Keming Zhang

Keming Zhang- 1School of Economics and Management (With Yangtze River Economic Belt Research Institute), Nantong University, Nantong, Jiangsu, China

- 2School of Business, Nanjing Normal University, Nanjing, Jiangsu, China

- 3School of Educational Science, Nanjing Normal University, Nanjing, Jiangsu, China

- 4London School of Economics and Political Science, London, England, United Kingdom

Background: The goal of “peak carbon and carbon neutrality” has pointed out the direction for the digital transformation (DIT) of enterprises. Companies need to pay a price when they seek green development or fulfill environmental responsibility. Out of self-interest, enterprises may exaggerate their environmental performance (EP) and then greenwashing behavior appears. Whether DIT can curb greenwashing behavior is a topic worth discussing.

Objective: This paper proposes a theoretical framework for the influence of DIT on greenwashing and further discusses how government subsidies, resource slack, and external pressure affect them. The data of China’s listed A - share companies are used to test this theoretical framework.

Methods: In this paper, multiple linear regression method is used to test the theoretical mechanism, and Hausman test and instrumental variable method are used to test the correctness of the conclusions.

Results: (1) DIT has an inhibitory effect on greenwashing. (2) Government subsidies, resource slack, and public pressure positively moderate the relationship. (3) The effect of DIT does inhibit symbolic behavior, but the impact on substantive behavior is not obvious. The moderating effects of various variables are also different.

Discussion: It is suggested that the government take the lead in building more digital public participation platforms to improve the online monitoring and early warning ability of enterprises’ greenwashing behavior, tourge enterprises to configure more intelligent and digital cleaner production equipment and facilities, and to improve their environmental performance. Local governments are encouraged to seize the trend of enterprises’ digital green transformation, introduce more government subsidy policies for DIT, improve digital infrastructure and digital intellectual property protection, and escort enterprises’ green DIT. The government and the banks should cooperate to give more green preferential loans, tax relief, and other measures to enterprises undergoing green DIT.

1 Introduction

The quality and quantity of economic and social development have become the main theme of contemporary development. Countries around the world are paying more and more attention to enterprises’ performance in Environmental, Social, and Governance aspects (ESG). Promoting enterprise ESG development is of great significance to implementing the new development concept of “innovation, coordination, green, opening and sharing”, constructing the new development pattern of the “double cycle” of the Chinese economy, and realizing the national strategy of the “double carbon” goal.

The goal of “peak carbon and carbon neutrality” has pointed out the direction for the DIT (DIT) of enterprises. Companies need to pay a price when they seek green development or fulfill environmental responsibility. Out of self-interest, enterprises may exaggerate their environmental performance (EP) and then greenwashing behavior appears. According to the September 2022 A-share Green Weekly report published by the Chinese public account “Azure Map” of WeChat as an example, the report showed that 74 listed companies were exposed to environmental risks, among which the subsidiaries of Guoxuan High-tech company received more than one million environmental fines for environmental violations. The DIT may also reduce the pollution of enterprises, which is one of the choices for green development (Oberländer et al., 2018). With the vigorous development of the digital economy and industrial upgrading, can DIT restrain the greenwashing behavior of enterprises?

With the higher expectations and voices of society and government on sustainable development, it is urgent for enterprises to must content higher organizational legitimacy through green actions (DeStefano et al., 2018; Wu et al., 2021). DIT provides an opportunity for the green development of enterprises (DeStefano et al., 2018), which is an “organizational change” for enterprises (Neuhofer et al., 2015). The key to its success lies in whether it can be accepted by the institutional environment (Mikalef and Pateli, 2017). In any transformative action of an organization that breaks through the existing organization operation logic, only by solving the problem of the legitimacy construction of social thought, can the effective unification of internal and external thought and understanding come true. When the legitimacy level is not enough, the enterprises’ DIT activities will be difficult to be accepted. Therefore, the success of organizational change of “DIT” cannot be separated from organizational legitimacy (Bayo-Moriones et al., 2013; Turna, 2022). Organizational legitimate construction activities such as social responsibility or environmental responsibility are common means for enterprises to obtain legitimacy recognition from stakeholders. As a legitimacy construction activity that may be beneficial to enterprises but has negative externalities (Silva, 2021), whether greenwashing will be restricted by DIT is a hot topic of high academic research value.

In September 2020, Shenzhen Stock Exchange revised the Assessment Measures for Information Disclosure of Listed Companies in Shenzhen Stock Exchange, proposing for the first time the active disclosure of listed companies’ ESGs, and assessing the disclosure of listed companies’ social responsibilities. More and more enterprises begin to increase investment in ESG, attach importance to ESG practice, and strengthen the disclosure of ESG-related information. Based on meeting the regulatory requirements, they respond to the demands of investors and other stakeholders for non-financial information. Under the background of the rapid development of the digital economy, enterprises should seize the major strategic opportunities brought by the rapid development of digital information technology, accelerate the deep integration of digital technology with the production, research and development, management, sales, and service of enterprises, and realize the transformation from the traditional production mode to the development of digital intelligence. On the one hand, the digital transformation of enterprises can reduce the cost of enterprises to fulfill social responsibility and improve the efficiency of responsibility, to provide material incentives for enterprises to improve the quality of ESG information disclosure. On the other hand, it will also be beneficial to improve the investment capacity of investors’ ESG and the ESG governance capacity of the supervision department, to further promote the development of ESG in China. Therefore, by studying the effect and mechanism of enterprise digital transformation on enterprise ESG, this paper aims to reveal the internal and external factors and realization path of enterprise ESG, to provide theoretical support and empirical evidence to promote the development of enterprise ESG in China.

This paper analyzes enterprise ESG information disclosure quality from the perspective of greenwashing, takes the A-share listed companies in Shanghai and Shenzhen from 2008 to 2018 as research samples, constructs enterprise digital transformation indicators through text analysis and word frequency statistics, and empirically tests the influence of enterprise digital transformation on enterprise greenwashing. Through a series of robustness tests and endogeneity treatment, the credibility of the conclusions of this paper is ensured. Further, this paper empirically examines the role of enterprise digital transformation on enterprise greenwashing behavior from two aspects: external legitimacy pressure and internal resources (resource slack and government subsidies).

The marginal contributions are as follows: Firstly, this paper puts enterprise digital transformation and enterprise greenwashing behavior into the same analytical framework, studies the role of digital transformation in restraining enterprise greenwashing behavior from the perspective of building and enhancing enterprise ESG practical ability, reveals the non-economic effects created by digital transformation, expands the research ideas of enterprise ESG concept in the digital economy era, and provides a new perspective for enterprises to improve their social responsibility level. Secondly, this paper reveals the mechanism of enterprise digital transformation to restrain enterprise greenwashing behavior from three channels: external legitimacy pressure, redundant resources, and government subsidies, which opens the black box of causality between enterprise digital transformation and enterprise greenwashing behavior to some extent and has certain practical significance. Thirdly, from the two sub-indicators of greenwashing, symbolic behavior, and substantive behavior, this paper examines the effect of enterprise digital transformation on restraining enterprise greenwashing behavior, which provides empirical evidence for further promoting the high-quality development of enterprises.

Therefore, whether it is based on practical problems or theoretical research gaps, it is necessary to deeply study the impact of DIT on greenwashing. Hypothesis development, model setting, empirical analysis, and conclusion constitute the rest of this paper.

2 Theoretical analysis and hypothesis development

China’s new environmental information disclosure system made clear that we should earnestly promote the construction of the disclosure system of enterprise internal environmental information, and improve the standards of information disclosure content, and technical specifications. In recent years, DIT has been involved in social life and enterprise management system. DIT has triggered the transformation of corporate governance and operation mode. There is potential for greater transparency in ESG disclosures. The emission sources of pollutants involved in ESG are numerous and dispersed, the calculation method is complex and the workload is huge. To reduce the difficulty and cost of work, enterprises often choose to “greenwash” ESG reports. Can DIT improve the capacity-construction level of enterprise ESG disclosure? Will it further improve “greenwashing” management mechanism? The deep thinking of the above questions has also become the starting point.

2.1 Literature review

Past studies have addressed related topics through the impact of digital technology, institutional pressures, redundant resources, and government subsidies on environmental sustainability. The review section shows a significant trend on this topic, as the results indicate that there is still no agreement on the outcome of the variables. Thus, this makes the title all the more compelling and inspires a significant contribution to mutual understanding.

2.1.1 Environmental effect of institutional pressure

Based on the institutional isomorphism theory of DiMaggio and Powell, institutional pressures are divided into mandatory, normative, and imitative isomorphism institutional pressures, and the three institutional pressures have different manifestations of environmental responsibility effect (DiMaggio and Powell, 1983).

Mandatory homogeneity originates from the formal and informal pressure exerted by political organizations and social groups on enterprises, such as the regulatory pressure formed by regulations, policies, and systems formulated by the government and professional organizations (DiMaggio and Powell, 1983). Mandatory isomorphism is inviolable. If it is not followed, even if the survival of the enterprise is not threatened in the short term, the enterprise will pay a high price, including the additional cost generated by the economic penalty, and the negative impact on the social image and relationship resources of the enterprise (DiMaggio and Powell, 1983). In recent years, China has successively issued a series of laws and regulations requiring enterprises to fulfill their environmental responsibilities (Udemba and Tosun, 2022), such as the Clean Production Promotion Law of the People’s Republic of China, the Environmental Information Disclosure Guidelines for Listed Companies and the new Environmental Protection Law of the People’s Republic of China. Under the increasing pressure of the mandatory system, enterprises will have to take more substantive environmental behaviors to improve environmental performance. We will reduce “greenwashing” that goes against the environmental protection wishes of government regulators. The study shows that government regulation can significantly affect corporate environmental information disclosure behavior (de Villiers et al., 2014). Mandatory homogenous pressure will intensify enterprise environmental Information (Zeng et al., 2012; Sun et al., 2019a; Aragòn-Correa et al., 2020).

Normative homogeneity is mainly derived from industry norms, norms, ethics, and values formulated for members by professional organizations such as trade associations, non-governmental organizations (NGOs) and social groups (DiMaggio and Powell, 1983). Unlike mandatory isomorphism, normative isomorphism emphasizes the influence of positive guidance on the behavior of the company within the corresponding organization. Professional trade associations spread consensus concepts to their members, directly influence the values of member organizations, and guide their managers to make compliance decisions. Environmental NGOs are non-profit organizations composed of enterprises and institutions with rich environmental expertise. They are committed to environmental protection, focusing on the solution of environmental problems and the improvement of the current environmental situation. Enterprises implementing environmental governance may receive strong support and promotion from environmental NGOs, and obtain a variety of tangible and intangible resources. It is conducive to forming a virtuous circle of mutual promotion of economic performance and environmental performance and growing into the benchmark of industry development. Moreover, this demonstration effect will drive other members of the organization to actively fulfill their responsibilities of energy conservation and environmental protection, and disclose more substantive environmental information. In addition, compared with government regulatory departments, environmental NGOs have more professional and adequate environmental knowledge and can effectively screen out symbolic environmental information disclosure without substantive information. In the same situation, normative homogeneity pressure will intensify the enterprise’s environmental information disclosure (Palazzo and Scherer, 2006; Zeng et al., 2012; Marquis et al., 2016; Sun et al., 2019b; Cai et al., 2020).

Imitative homogeneity is the corresponding feedback made by enterprises based on their cognition and understanding in the institutional environment. In the face of uncertain and complex environmental conditions, managers are unable to make accurate judgments based on the available information, so they tend to observe the reactions of other competitors and choose to imitate competitors in the industry, which eventually leads to the convergence of enterprise behavior and structure, especially among enterprises in the same industry. The same is true of corporate environmental responsibility and the choice of “greenwashing” environmental information. Enterprise managers and stakeholders can learn about other enterprises’ environmental practices and whether they “greenwash” the disclosed environmental information. When they know that other enterprises (especially industry leaders) disclose their relevant environmental information in a detailed and complete manner, enterprises may passively improve the content and quality of environmental information disclosure in order not to “lag”. When some companies greenwash their environment, others may follow suit. Some studies at home and abroad have examined the imitative homogeneity of environmental information disclosure. For example, De Villiers et al. found in their research that BHP Billiton is regarded as the benchmark of sustainable development enterprises, and its sustainable development reports are widely imitated by other enterprises (de Villiers et al., 2014). Finally, the sustainable development reports of all enterprises gradually converge. In the same situation, imitative homogeneity pressure will inhibit environmental information disclosure (Zeng et al., 2012; Cai et al., 2020; Lu et al., 2020).

2.1.2 Environmental effect of resource slack

Resource slack, referred to as slack, is an excess resource freely used by enterprises and a potential internal reserve resource (Bourgeois, 1981a), which can be divided into absorbed redundancy and unabsorbed redundancy according to its inherent viscosity and high liquidity. The academic community generally believes that resources slack are a key predictive variable of enterprise innovation behavior because redundant resources are an important buffer resource for organizations to cope with environmental changes and a key catalyst for promoting the implementation of technological innovation projects. Abundant redundant resources are conducive to alleviating the conflict of objectives, improving cohesion (Tan and Peng, 2003), and coping with the impacts and challenges brought by changes and environmental turbulence (Nohria and Gulati, 1996). However, the key to whether redundant resources are conducive to the sustainable development of enterprises lies in the inherent characteristics of redundant resources and the influence of the external environment. In different usage situations, the utility of redundant resources to sustainable development will also show obvious heterogeneity.

Absorbed resource slack (ARS) refers to the part of resources that have been occupied in the production and operation process of an enterprise but have not reached full capacity (Jifri et al., 2016). These resources have strong specificity, are embedded in fixed assets and production operations, and have certain utilization value and greater development potential. If enterprises can fully tap its potential value and potential, it will play a certain role in promoting the transition or transformation from general innovation to green sustainable development. To achieve the balance between operation and green sustainability, enterprises need to rationally allocate the absorbed redundant resources, which are usually dominated by green utilization innovation and supplemented by green exploration innovation. Through an effective division of labor and coordination between “utilization” and “exploration” innovation activities, risks brought by sustainable development strategies can be effectively resisted and reduced, and the efficiency and success rate of green sustainable development can be improved (Kortmann, 2015). To realize green collaborative innovation, it is necessary to allocate and share ARS from a systematic and global perspective, to ensure the synergy of green exploratory innovation and utilization innovation. However, the more the ARS accumulates inside the enterprise, the longer the fixation time, and the more likely it is to be deposited in the existing organization, resulting in resource stickiness and structural rigidity, making it difficult for the enterprise to reuse and allocate it (Greve, 2003). In addition, over-fixed resources in the organizational process will produce a siphon phenomenon, and enterprises will face the problem of polarization when allocating ARS. In the process of realizing sustainable development, enterprises are difficult to find the optimal allocation route that balances “utilization” and “exploration” of required resources. Nor can it solve the dilemma in the collaborative “utilization” and “exploration” green innovation activities. Therefore, the more the ARS accumulates, the more difficult it is for enterprises to achieve the balance and coordination of green sustainable development. ARS generally inhibits the sustainable development of the enterprise (Huang and Li, 2012; Ranasinghe et al., 2022; Zhou et al., 2022).

Unabsorbed resource slack (URS) is additional resources that are not utilized by the enterprise and can be redeployed in emergencies. Due to the low commitment of unabsorbed redundant organizations, strong mobility, and flexibility, organizations have more freedom of choice, which is conducive to enterprises to cope with the complex and changeable external environment and provide higher flexibility for enterprises to implement green development strategy (Esposito De Falco and Renzi, 2015). When new energy technologies or environmental protection opportunities appear in the market, URS can be quickly put into green exploratory activities, which is conducive to enterprises’ exploration of new products, new technologies, and new services, resulting in an increasing in “exploration” share and a decreasing in “utilization” share (Tabesh et al., 2019). At the same time, the plump URS will enable enterprises to obtain higher super profits from exploratory green activities, which is easy to make enterprises blindly confident and more actively seek new markets with greater development prospects. The growth of high returns brought by URS will also stimulate enterprises to enter the emerging strategic business areas too aggressively, which will aggravate enterprises’ excessive investment and management neglect of sustainable development projects, which will not only increase the development of unnecessary projects but more importantly, potentially great risks, thus making enterprises trapped in the dilemma of infinite circular exploration (Hughes et al., 2021). Finally, it leads to sustainable development strategy bubble. Therefore, the more URS an enterprise has, the more likely it is to lead to the imbalance or dislocation of “utilization” and “exploration” in the process of sustainable development, thus restricting the development of enterprises’ green and balanced innovation. When enterprise resources are relatively scarce, the two strategies of “utilization” and “exploration” in the sustainable development strategy will conflict or confront each other because of the competition for resources. From this perspective, unabsorbed redundancy may reduce the quality of environmental information disclosure for sustainable development (Chen et al., 2017).

However, URS can be flexibly converted between two different types of green activities. Abundant URS can effectively alleviate the dilemma and contradiction of “resource competition” between two types of green sustainable development activities (Chen and Miller, 2007), and help enterprises to resist various risks in the process of sustainable development, to enable enterprises to maintain normal operation. “Utilization” and “exploration” in sustainable development activities should be effectively coordinated to enhance complementarity and compatibility (Vagnani, 2015).

2.1.3 Environmental effect of government subsidy

The current academic circle mainly holds the following three views on the impact of government subsidies on enterprises’ green activities: (1) positive correlation view. This view holds that there is a positive correlation between government subsidies and green activities, that is, government subsidies have a positive stimulative effect on green activities. Green subsidies, environmental subsidies, research and development subsidies, and other resources reduce the uncertainty of green innovation projects to a certain extent, and enhance the confidence of enterprises in carrying out green activities (Philip et al., 2022). Szucs (2018) believes that the high input, high risk, and positive externalities of green innovation will lead to the lack of motivation for enterprises to carry out green environmental protection activities, while government subsidies can provide direct financial support for enterprises to carry out environmental protection activities, thus reducing the input cost of enterprises and stimulating the enthusiasm of enterprises to improve their environmental performance (Szücs, 2018). Kleer (2010) pointed out that the “certification effect” of government subsidies can add tangible and intangible assets to enterprises’ green innovation (Kleer, 2010). On the one hand, government subsidies can convey good information for enterprises to the outside world, which is conducive to enhancing investors’ understanding and trust of enterprises, to expand the financing channels for enterprises’ green activities and alleviate financial constraints. On the other hand, enterprises that receive government subsidies will receive more social attention and supervision. External pressure forces enterprises to pay more attention to self-regulation and formulate and implement green development strategies that meet the interests of various parties (Xu et al., 2021; Udemba et al., 2022).

(2) Negative correlation. Some scholars have also pointed out that government subsidies will intensify the rent-seeking behaviors of enterprises, resulting in the crowding out effect of enterprises to cater to the government, which restrains their green activities. Government subsidies may increase the excess salary and in-service consumption of top managers, making government subsidies a tool for corporate authorities to gain personal gain (Wang et al., 2022a). To obtain government subsidies, enterprises need to maintain a good relationship with the government and choose the game strategy of welcoming the government, which may induce enterprises to use government subsidies for non-green innovation activities, resulting in resource crowding out of environmental protection activities (Ilinitch et al., 1998). Enterprises that receive government subsidies may have opportunistic behaviors to cater to the government and managers, resulting in the crowding out effect of government subsidies on both green technology innovation and green practical patent innovation, which weaken the environmental performance of enterprises (Ayayi and Wijesiri, 2022).

(3) Nonlinear relationship. Some scholars have found that there is a nonlinear relationship between government subsidies and enterprises’ green environmental protection activities, such as inverted U-shaped (Boeing, 2016).

2.2 Hypothesis development

Enterprises can’t achieve leapfrog development and growth without DIT. With the continuous development of “digitalization”, enterprises have taken “DIT” as a key strategy to improve their performance and win a good reputation to obtain the legitimate demands of relevant stakeholders (Anser et al., 2020; Weber-Lewerenz, 2021). Existing studies of DIT mainly focus on total factor productivity, economic and environmental performance (Vial, 2021). In terms of total factor productivity, DIT can enable enterprises to have stronger product manufacturing and industrial supply chain data reserve in terms of material properties and process parameters, to improve the product performance, shorten product production cycle and increase the TFP of enterprises. However, there may also be a nonlinear relationship between them or no relationship at all. In terms of financial performance, the “IT paradox” shows that Digitization can affect the financial performance of enterprises positively or negatively. On the one hand, it is indispensable for enterprises to arrange production plans, track market product demand and improve internal operational efficiency (Qin et al., 2022), and DIT optimizes internal and external communication methods to reduce business costs and improve financial performance. On the other hand, DIT will also bring an additional cost burden, which leads to no obvious positive impact (Ekata, 2012; Hajli et al., 2015; Lu, 2018; Qi et al., 2022). In the field of EP (Environmental performance), there are three views on the impact of DIT on EP: DIT can realize the green design and production process in the life cycle of enterprise products, reduce the consumption of natural resources and improve EP (Lu, 2018; Lu, 2018); DIT will also bring additional “potential costs” by affecting the production scale, product structure, and process efficiency, and reduce the environmental performance of enterprises (Kunkel and Matthess, 2020; Kunkel and Matthess, 2020); Non-linear relationship also exists between DIT and EP, and the moderating effects of different resources slack between them show significant differences. To sum up, it can be seen that the related research on DIT has a certain depth, but no consistent research results have been obtained yet, and few works of literature mention the impact of DIT on greenwashing. As one of the research hotspots in the field of corporate environmental responsibility, greenwashing is the result of the game between enterprises and related stakeholders, and it is also subject to the external institutional environment and resource constraints of enterprises. With “greenwashing” getting more and more attention from the public, discussing the influence of DIT on greenwashing behavior has become a highlight of this research.

Based on this, this paper explores the influence of DIT on greenwashing and further examines how internal resources (resources slack) (Du et al., 2016; Qi et al., 2022), and external pressure (public pressure) affect the effect of DIT on greenwashing. The research results not only help to enrich the research perspectives in the field of resource-based theory and legitimacy theory (Yang et al., 2022), but also further expand the relevant mechanism of DIT on greenwashing, and provide useful inspiration and reference for China to effectively manage greenwashing behavior and improve the level of corporate environmental responsibility under the background of high-quality development (Xu et al., 2023).

DIT is a radical organizational change, which crosses the boundaries of traditional organizational behavior and faces challenges such as competitive logic, institutional complexity, and legitimacy (Greenwood et al., 2011). According to institutional theory, any organizational behavior and operation mode are affected by social expectation and social identity (Jifri et al., 2016; Wu et al., 2021). Enterprises’ DIT activities will undoubtedly face many legal obstacles, and the common means to overcome these legal obstacles is to fulfill a higher level of environmental responsibility. However, few works of literature explore the impact of DIT on greenwashing behavior, to cross the threshold of legitimacy and obtain organizational legitimacy. The influence of DIT on enterprises’ greenwashing behavior may be situationally dependent. Another objective of this paper is to expand the boundary conditions for the effect of DIT on greenwashing. According to the resource-based view, internal resource allocation and external resource exploitation are the basis to exert various economic activities including DIT (Hinings et al., 2018). Based on the above analysis, DIT is an organizational change for enterprises, which needs to meet the requirements of institutional legitimacy and have the support of resources (Ahmed et al., 2023).

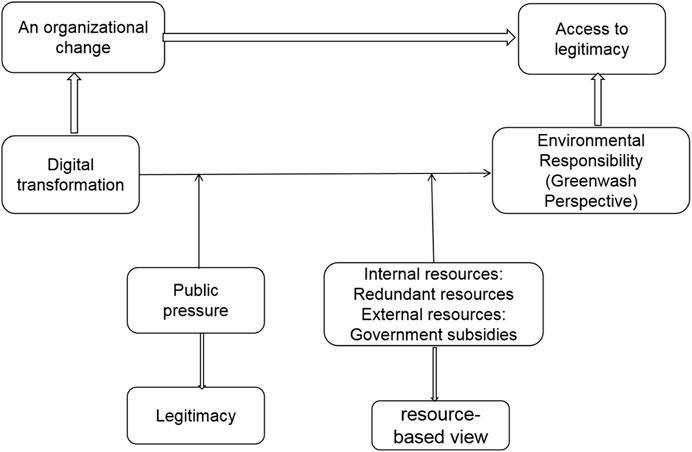

Greenwashing is the result of the interaction between external institutional constraints and enterprise resource allocation. It is a difference between the ideal level of environmental responsibility and the actual level (Liu et al., 2022), and also a way for enterprises to obtain legitimacy (Song et al., 2011; Mateo-Márquez et al., 2022). This paper explores its potential mechanism from the dual perspectives of legitimacy and resources: the motivation of enterprises to cope with external pressure is to obtain legitimacy, greenwashing is a way to obtain legitimacy, and the resources owned by the company provide a “coping ability” for enterprises to implement greenwashing. The role of government subsidies, redundant resources, and public pressure in the governance of greenwashing behavior of enterprises are analyzed under the background of DIT. The research framework of this paper is obtained (Figure 1).

FIGURE 1. Research framework.

2.2.1 Digital transformation and greenwashing

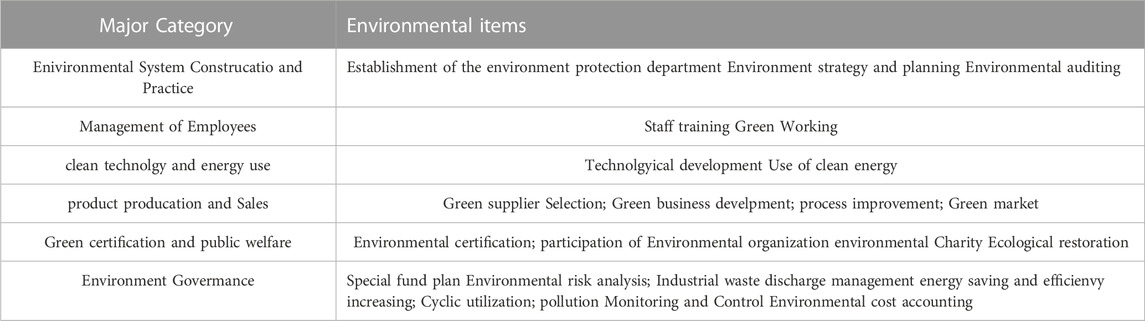

DIT has become the general trend in China (Chalmers et al., 2021; Wu et al., 2021). With new concepts, new business forms, and new models, DIT is integrating into all areas of social development. Enterprises start from the real transformation value concept, from the aspects of product design innovation, intelligent production and operation management, and personalized user service to construct DIT. It can be seen from these contents that DIT will have a positive impact on the organization mode, operation and management mode, business model, and the restructuring of the company’s organizational boundaries, and make the enterprise organizational structure more networked, accurate market positioning, refined marketing, and flexible manufacturing. The measurement of greenwashing runs through the enterprise organization mode, operation management mode, and business mode, including environmental system construction and practice, staff management, clean technology, product production and sales, green certification and public welfare, and environmental governance (Walker and Wan, 2012; Gou, 2013; Zhang et al., 2022). Therefore, DIT can affect enterprises’ greenwashing behavior.

Greenwashing is an act of false environmental protection propaganda and self-dressing by enterprises, and it is a form of “pseudo-environmental responsibility”. This kind of inconsistent performance of the environmental responsibility can help companies achieve the goal of building a reputation at a low cost. At the same time, it is also a language strategy for companies to game with environmental protection appealers, and environmental protection supervision departments. Even in the process of vigorously promoting the construction of ecological civilization by the Chinese government, there are still many “greenwashing” enterprises that “compete against the wind”. For example, in the environmental performance list of listed companies in the non-ferrous metal mining and dressing industry released on 5 August 2022, by the Weilan Map WeChat official account, 1,992 companies associated with 24 listed companies all have greenwashing behaviors to varying degrees. In addition to the investment of the company’s resources and the supervision of external forces, the governance of greenwashing requires the innovation of cleaner production technologies and models, and digital transformation can help companies to more effectively conduct research and development of green technologies and green production models at a low cost. So, whether digital transformation can curb greenwashing behavior of enterprises is the focus of this paper.

Greenwashing is a form of selective information disclosure, which is essentially an ESG reporting information disclosure behavior. Whether DIT can enable enterprises to better manage and disclose ESG information will also directly affect the greenwashing behavior of enterprises. Most of the contents of ESG reports belong to the category of non-financial performance, which requires high coordination between departments and makes it difficult to collect and evaluate data. However, in reality, most enterprises have not established a complete system and information data platform for the collection process, statistical method, traceability requirements, audit, and verification of environmental data and information, so the underlying data foundation of enterprises is very weak. The disclosures rely on extensive estimates and assumptions, encouraging companies to “greenwash” their ESG reports. Therefore, the breakthrough point to crack enterprise greenwashing lies in reducing the cost of environmental responsibility information data and improving the efficiency of integrating environmental responsibility information (Bai and Sarkis, 2017).

First of all, DIT has the ability to data resource integration and improves the efficiency of data processing. Through the implementation of full-process data management, with the help of the Internet of Things technology, such as automatic collection, summary storage, intelligent computing, and other technical links, the cost of data processing is greatly reduced and the efficiency of data use is improved (Gobbo et al., 2018). The operation data resources of enterprise digital assets are collected and integrated, and the data information base is built to simplify ESG data management and upgrade the underlying data. Promoting enterprise management innovation and system reform will ultimately enable enterprises to prevent the “greenwashing” behavior of ESG reports, help enterprises improve the quality of disclosure of ESG reports, and reduce the motivation of greenwashing.

Secondly, enterprise DIT has the effect of reducing the cost of environmental responsibility information. The application of digital technology can improve the efficiency of corporate decision-making and operation management, enhance the ability of corporate environmental responsibility practice, and reduce the cost of corporate environmental information disclosure. Improving the transparency of corporate environmental information is conducive to improving the level of corporate ESG governance, to reduce environmental responsibility information in the way of “greenwashing".

In conclusion, enterprise DIT can effectively restrain enterprise greenwashing behavior.

H1: DIT weakens greenwashing.

2.2.2 The moderating effect of government subsidies

High risk and great uncertainty may be the situation faced by enterprises in the process of DIT. Enterprises are likely to lack the necessary resources and capabilities and not have sufficient transformation motivation. At this time, government subsidies are particularly important for the DIT. Existing literature has examined the effectiveness of government subsidies from multiple perspectives such as firm innovation, firm performance, total factor productivity, and social responsibility (Wu and Hua, 2021; Wang et al., 2022b; Chen He, 2022; Duan et al., 2022). Government subsidies referred to in this paper include government subsidies for enterprises in a broad sense, such as tax incentives and environmental protection subsidies (Ji and Wang, 2017; Li et al., 2020a).

The government subsidy policy is likely to promote DIT activities and improve the performance of environmental responsibility. The improvement of environmental responsibility performance will prompt enterprises to disclose higher-quality environmental information (Li et al., 2020b), to reduce the level of greenwashing. According to this logic, the moderating effect of government subsidies is analyzed.

Government subsidies can have three effects: easing corporate financing constraints, innovation-driven effects, and enhancing corporate competition effects (ME Porter, 2007; Cheng and Ding, 2022). First of all, the special funds of subsidy policies can reduce the financial constraint of enterprises and achieve the purpose of improving cash liquidity (Cull et al., 2015; Chen et al., 2020), government subsidies promote enterprises to steadily invest limited resources into the practice of digital green transformation, share the risks of digital transformation and upgrade clean production process of enterprises to a certain extent (Xiao et al., 2022). While financing constraints are alleviated, enterprises have more resources to invest in environmental responsibility and improve their performance in environmental responsibility (Li et al., 2022). Second, government subsidies have an innovation-driven effect. The lack of innovation motivation is one of the practical problems faced by enterprises in the long-term operation process. Many studies have shown that government subsidies can improve the innovation output of enterprises by increasing R&D investment, promoting the effective allocation of internal resources, helping enterprises attract external financing, and other ways (Li et al., 2018; Feng et al., 2019; Cheng and Ding, 2022). Digital product, processes, processes, business models, and other innovation achievements will have a greater driving effect on digital transformation (Liu et al., 2020; Xingwu et al., 2020). In addition, the improvement of innovation ability can also provide the necessary software and hardware basic conditions for continuous DIT activities. The realization of energy-saving and emission-reduction targets requires advanced “software and hardware facilities” as a precondition. Enterprises’ energy-saving emission reduction supporting facilities are upgraded, and environmental performance is also improved, thereby reducing greenwashing behaviors of enterprises (Liu et al., 2011). Finally, government subsidies enhance the competitiveness of enterprises. Government subsidies play an incentive role through the market mechanism, which is conducive to giving play to the subjective initiative of enterprises and making the best competitive decisions based on their conditions (Duan et al., 2022). Government subsidies promote DIT, enhance their market competitiveness, help enterprises expand market share and gain more profits, and in turn promote enterprises to invest more resources in environmental responsibility construction, improve the quality of environmental information disclosure and reduce greenwashing behavior (Duan et al., 2022).

In conclusion, government subsidies can mainly promote the DIT by alleviating financing constraints, innovation-driven, competitive effects, and other channels, and then inhibit greenwashing behavior.

H2: Government subsidies positively affect the effect of DIT on greenwashing

2.2.3 The moderating effect of resource slack

Academic circles have reached different conclusions on whether resource slack is beneficial or harmful to enterprises (Xu et al., 2015; Pan et al., 2020). To meet the needs of survival, enterprises need to accumulate redundancy in the growth process, to avoid the consumption of organizational redundancy when the resource demand increases rapidly or the enterprise is faced with difficulties. Resource slack helps to enhance the innovation ability of enterprises and alleviate various conflicts caused by resource scarcity in the organization (Palmer and Wiseman, 1999). On the other hand, resource slack will increase enterprise costs and reduce enterprise operation efficiency (Cheng and Kesner, 1997). Resource slack can make the enterprise satisfied with the status quo and reduce the ability to respond to unexpected situations (Love and Nohria, 2005). Resource slack facilitates managers’ over-investment and blind diversification (Mishina et al., 2004). However, whether resource slack plays a promoting role or a negative role should be analyzed in different situations.

Absorbed resource slack (ARS) is idle resources that are oriented to specific applications and closely related to key business processes. They usually exist as costs and are mainly used in production activities rather than innovation activities, such as overhead, idle workshops, and products being processed. It is characterized by high asset specificity and weak conversion and utilization capabilities, making it difficult to achieve rapid and flexible reconfiguration of resources (Bourgeois, 1981b; Sharfman et al., 1988).

ARS provides hardware guarantee for the digital green transformation (Singh, 1986; Pan et al., 2021), because in the process of digital “green” transformation, enterprises need to complete the deep integration of digital technology and enterprise procurement, production, operation, management, marketing, and other links, it is necessary to establish a completely digital system and information data platform and realize the upgrade of the underlying data. These need advanced digital equipment as hardware support (Li, 2022). At this time, the ARS can give play to their “asset specific attribute” effect and convert a large number of redundant resources into digital fixed assets such as intelligent green production lines and intelligent pollution detection equipment (Zhong and Ren, 2023), to give play to the green operation and production effect of enterprise digital transformation and provide hardware guarantee. The green environmental protection practices of enterprises are strengthened, and the quality of environmental information disclosed is further improved, which is conducive to reducing the occurrence of green bleaching. Thereby, the following hypothesis is proposed.

H3a: Absorbed redundant resources positively affect the effect of DIT on greenwashing.

Unabsorbed resource slack (URS) refers to unconstrained resources in operation management, service innovation, and other aspects, which are not limited to specific technical fields, and help enterprises to implement new strategies such as new product development and new market entry (Huang and Li, 2009), such as cash, cash equivalents, credit lines, and highly flexible machine capacity. The characteristics of URS are that they are not limited in the scope of use and have a wide range of resource mobilization, which usually have natural advantages for unconventional investment activities of enterprises (Singh, 1986; Wang and Cheng, 2014).

This paper holds that the URS have two effects to inhibit the greenwashing behavior of enterprises. One is to alleviate the financial constraints required for green practice activities such as green innovation in the process of DIT. Secondly, it can produce the accumulation effect of green innovation data, which changes from quantitative to qualitative one, and further enhance the “digital” green innovation activities of enterprises.

First, the URS alleviates the financial constraint effect. With the application of DIT to the field of green activities gradually enriched, enterprises are faced with an increasing demand for DIT funds. Due to the characteristics of “flexibility and wide use”, unabsorbed resources slack can be converted into green R&D manpower input and green R&D capital input to strengthen the effect of green innovation activities of DIT.

Secondly, URS has the effect of green innovation data accumulation. As more and more URS are invested into the DIT process of enterprises, green innovation R&D personnel accumulate more and more green technology knowledge through the “learning effect”, which promotes the overall accumulation of green innovation data of enterprises, and finally accelerates the green innovation activities of enterprises.

To sum up, the above two effects can indirectly improve the quality of environmental information disclosure of enterprises, so as to inhibit greenwashing.

Accordingly, the hypothesis is put forward.

H3b: URS positively affects the effect of DIT on greenwashing.

2.2.4 Moderating effect of public pressure

Public pressure belongs to normative institutional pressure, which refers to the pressure generated by social values and codes of conduct in the field of an organization to drive specific behaviors of an enterprise (Zeng et al., 2022). Faced with the requirements of values and codes of conduct related to the media, the public, and social legitimacy, enterprises will try to maintain consistent standards and norms of behavior with members in the same system field to meet social expectations. This study uses media attention to represent the normative institutional pressure on enterprises.

The high degree of media attention shows that corporate behavior is widely exposed in public view and influenced by public judgment and public opinion (Guo et al., 2018). Media attention plays a role in restraining and guiding the development of enterprises and urges enterprises to “learn from the weak and strive for strength” (Turna, 2022). Specifically, as listed companies that are focused on and carry out environmental protection verification, they tend to maintain their reputation, take actions to enhance their green image, and give full play to the low-carbon value of DIT technology by using digital technology resources to carry out DIT application and green innovation and expand the idea of creating green value, to cope with the external normative system pressure, gain social legitimacy recognition and stabilize the market position (Liu, 2022). Therefore, the higher the media attention is, the stronger the positive promotion of DIT application to green innovation. Enterprises are more inclined to release high-quality environmental responsibility information to curb greenwashing.

H4: Public pressure positively affects the effect of DIT on greenwashing.

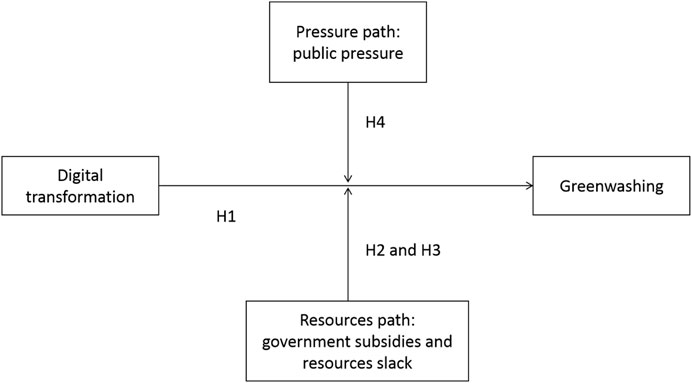

In summary, this paper uses government subsidies, resource slack, and public pressure as moderator variables to construct a theoretical model of digital transformation and corporate greenwashing, as shown in Figure 2.

FIGURE 2. Mechanism framework.

3 The econometric model and variable description

This paper uses the data of Shanghai and Shenzhen A-share enterprises from 2008 to 2018, A total of 6,510 samples are collected from the. The greenwashing data and digital transformation data in the annual report were sorted out by the text analysis method according to current research (Walker and Wan, 2012; Gou, 2013; Zhang et al., 2022). The left data were from CSMAR database and WIND database. This study excludes ST companies, ST* companies, companies cross-listed on AB shares and AH shares, and companies in the financial industry.

3.1 Econometric model

In this study, model (1) was used to test hypothesis H1, and model (2) was used to test hypothesis H2 ∼ hypothesis H4.

i and t represent enterprise and year respectively,

(1) Dependent variable

The dependent variables are greenwash or Green. There are mainly two Sub-index of “greenwashing” (Bowen and Aragon-Correa, 2014). Greenwashing is measured by the ratio or the difference between symbolic act score and substantive act score (Walker and Wan, 2012; Gou, 2013). Please refer to Appendix 1 for the scoring indicators. If there is a symbolic line or substantive behavior, the value is 1; otherwise, it is 0 (Walker and Wan, 2012; Gou, 2013; Zhang et al., 2022). Due to space limitation, please open the attachment named “For review the measure process of greenwashing”, the document details the greenwashing measurements.

From the Shenzhen Stock Exchange’s release of the Guide to Environmental Responsibility Information of Listed Companies in 2007 to the release of the New Environmental Protection Law by the Ministry of Environmental Protection in 2015 (Liu, 2022), the environmental indicators published by listed companies have been improved step by step. At the same time, this paper combines the research progress of the academic circle on the greenwashing index (Lyon and MaxwellGreenwash, 2011; Lyon and Montgomery, 2015), and finally obtains the evaluation system of this paper’s greenwashing index (Appendix 1). The evaluation index of greenwashing behavior is more consistent with the institutional background of listed companies in China.

(2) Core explanatory variable

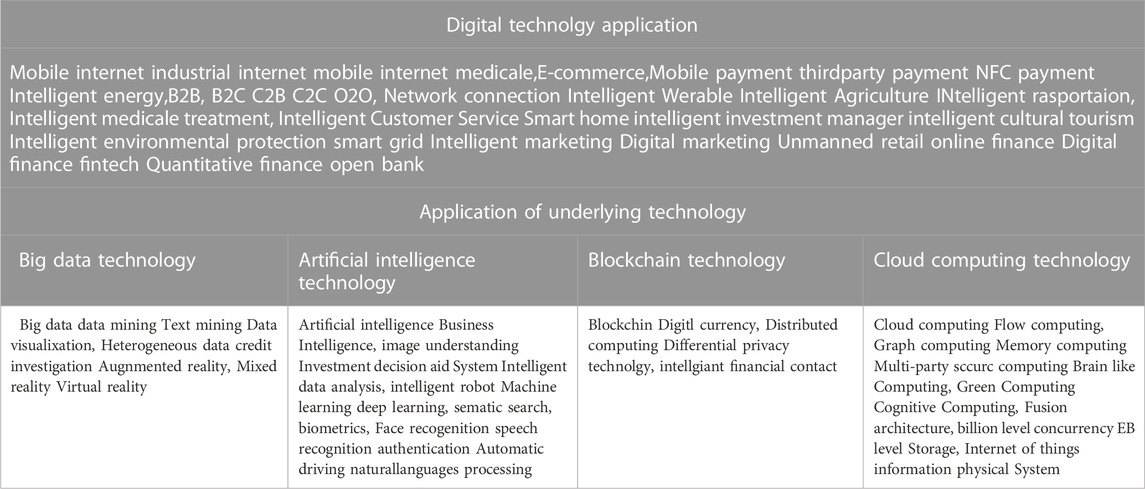

Digital transformation, following the approach of converting qualitative material to quantitative data, this paper uses specific keywords to construct digital-related indicators (see the Appendix 2) (Wu et al., 2021). Digital transformation includes two modules: the application of underlying technology and the practical application of technology. The first module includes four smaller modules: Artificial Intelligence, Block chain, Cloud Computing, and Big Data technical frameworks (Wu et al., 2023). There are three main ways to measure digital transformation: the total number of digital word frequencies of listed companies (Words), the logarithm of the total number of word frequencies plus 1, and the weight of the number of keywords in a company’s annual report to the total number of similar keywords of all enterprises in the same industry in that year as the measurement index of digital transformation (Wu et al., 2021; Wang et al., 2022c; Dong and Zhang, 2022; Pan et al., 2022), the latter two are used as proxy variables for digital transformation in robustness test.

(3) Moderating variables

Government subsidies, the government subsidies selected in this article (Subsidy1), In this paper, the ratio of government subsidy amount to operating cost is used as the proxy variable of government subsidy (Zhang et al., 2022).

Resource slack, resource slack is divided into unabsorbed resource slack (Ubsorb1) and absorbed resource slack (Absorb1). The ratio of cash and cash equivalents to current liabilities is used to measure the unabsorbed resource slack. The greater the value of this index, the more cash assets the enterprise reserves for future business activities and the more resources available for development and utilization (Xu et al., 2015). The cost-profit rate is used to measure the absorbed redundant resources. This index reflects the redundant resources that have been internalized in the enterprise system (Xu et al., 2015).

Public pressure, this paper use “Baidu search index” to measure the external public pressure (lnMedia) faced by listed companies, and the logarithm of Baidu index plus 1 is taken (Clarkson et al., 2008).

(4) Control variables

Following existing studies (Berrone et al., 2017; Zhang, 2022), enterprise Size (Size), enterprise age (Long), enterprise operating performance (Roa), environmental regulation (lnPM), asset-liability ratio (Debt), industry concentration (HHI_ A), green R&D level (Patents), equity concentration (Top) and industry dummy variable (Industry) and year dummy variable (Year), and individual fixed effects dummy variables are also set.

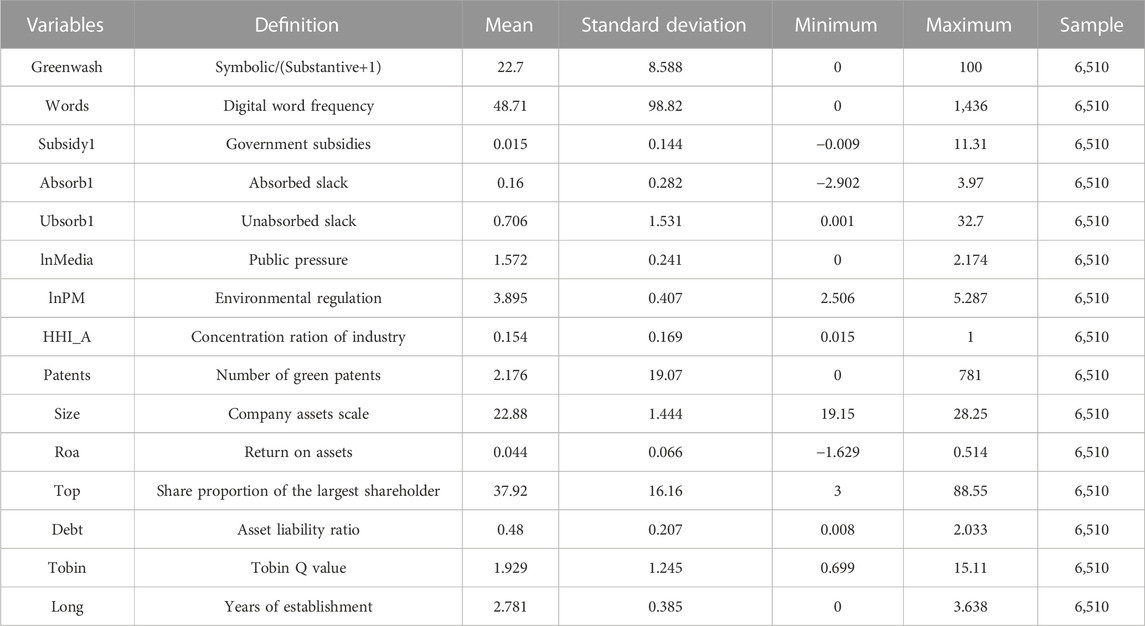

3.2 Variable description

The descriptive statistical results of each variable are shown in Table 1. It can be seen from the average and standard deviation that different enterprises have great differences in the levels of greenwashing and digital transformation.

TABLE 1. Descriptions of the main variables.

4 Results and discussion

4.1 Benchmark regression results

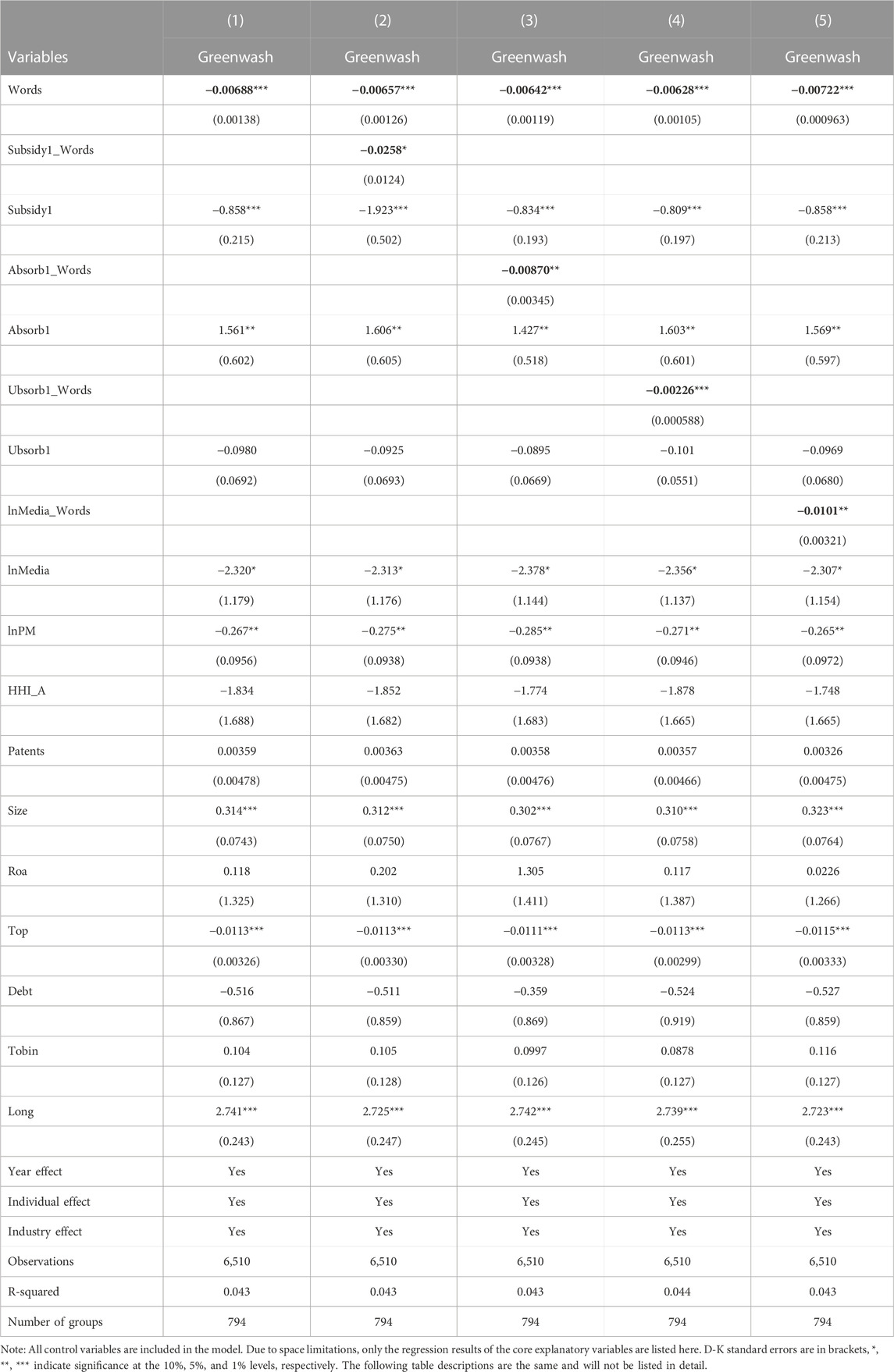

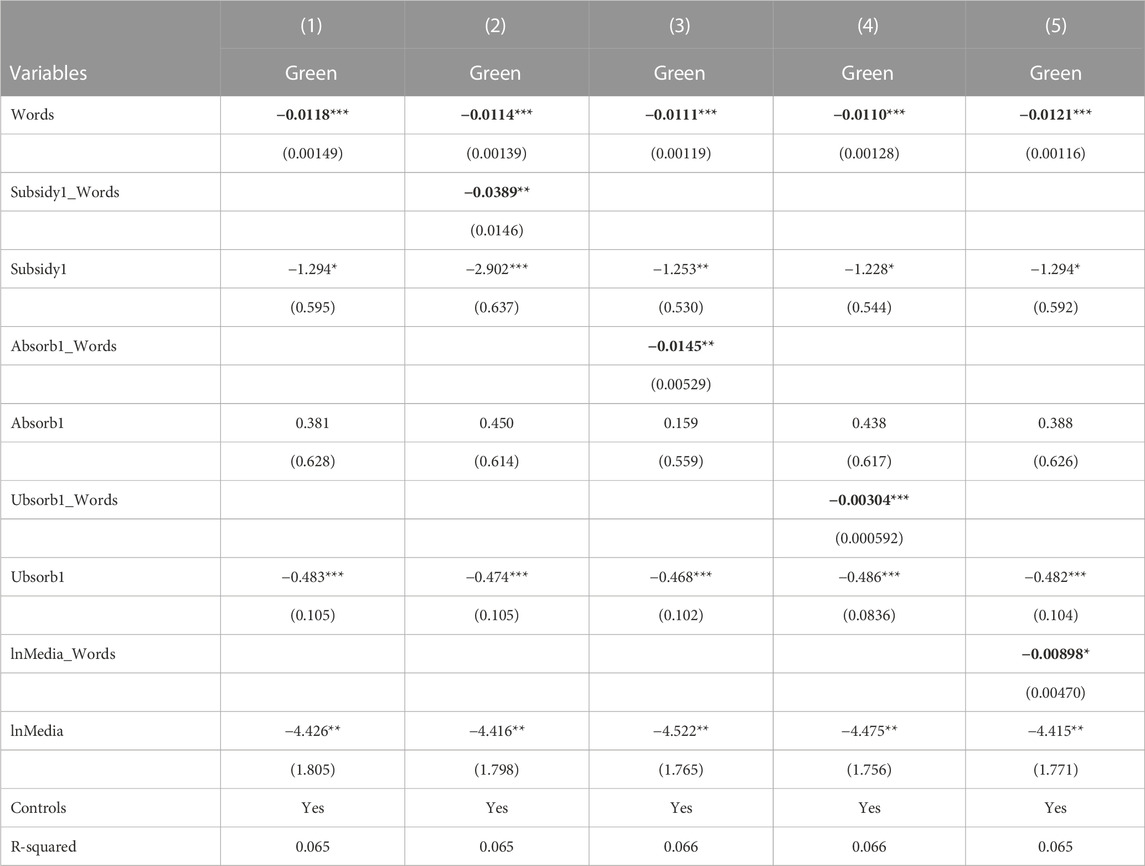

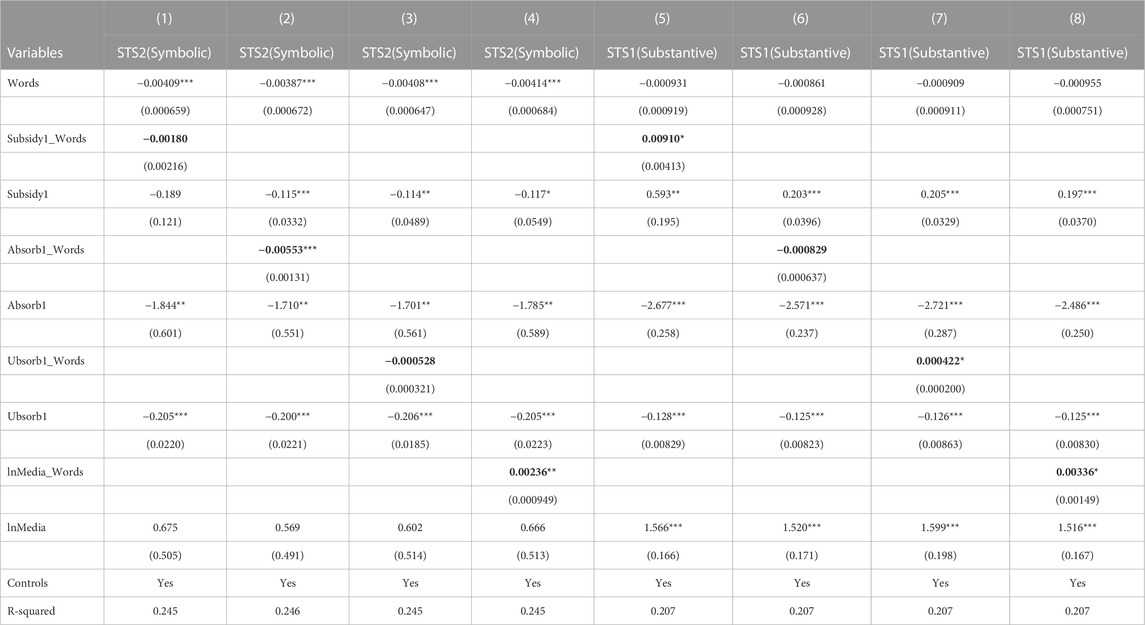

The first row of columns (1)–(5) in Table 2 respectively reports the impact of digital transformation (Words) on the greenwashing behavior of enterprises (Peng et al., 2022). The results show that the coefficients of Words are significantly negative at the level of 1%, indicating that digital transformation can inhibit the greenwashing behavior of enterprises. Hypothesis H1 is verified.

TABLE 2. Benchmark regression results.

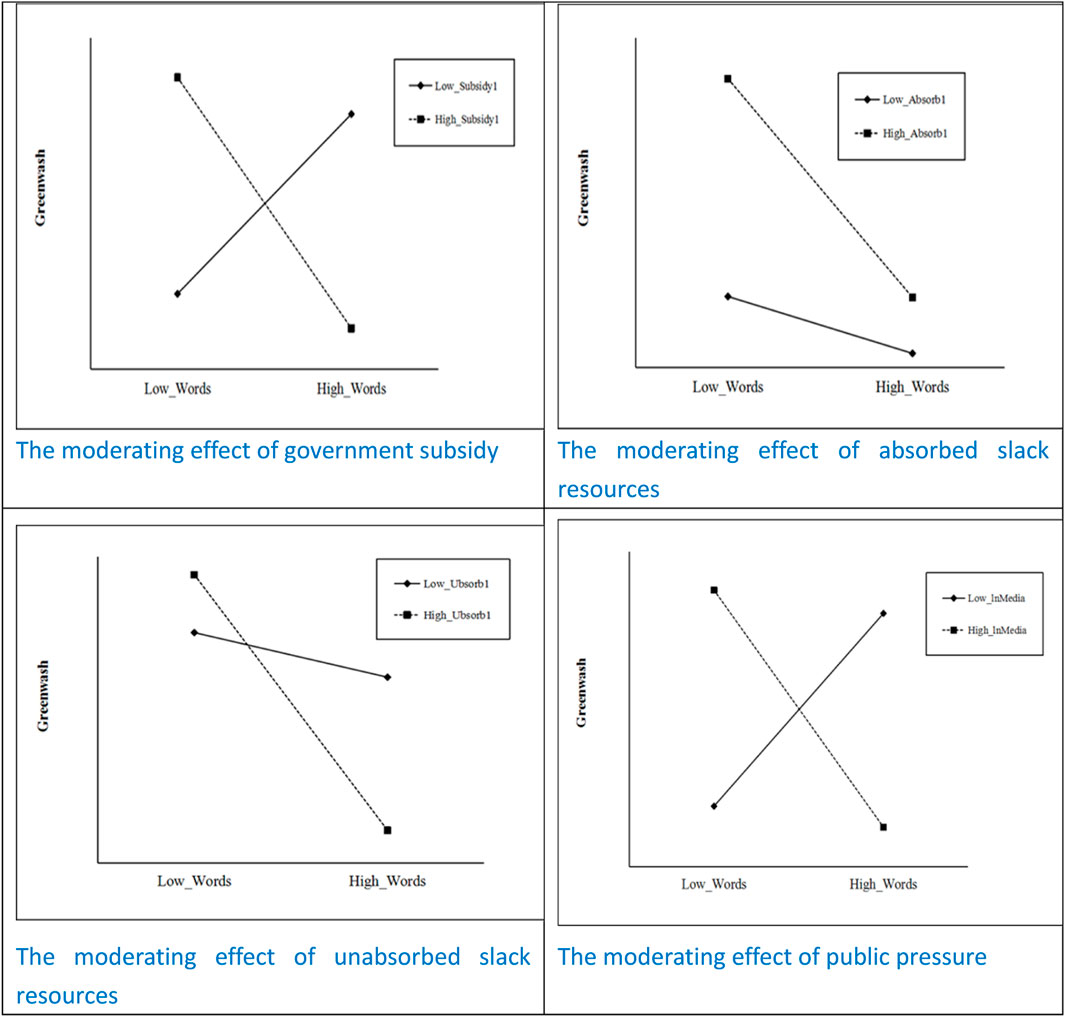

Columns (2)–(5) are the results of examining the moderating effects of government subsidies (Subsidy1_Words), absorbed resource slack (Absorb1_Words), and unabsorbed resource slack (Ubsorb1_Words), and public pressure (lnMedia_Words). Hypotheses H2-H4 are verified.

Column (2) shows that the moderating effect of government subsidies, Subsidy1_Words, is negative and significant at the 5% level, indicating that government subsidies positively moderate the relationship between DIT and greenwashing (Jialin et al., 2022). The alleviation of the financing constraint effect, innovation effect, and competition effect brought by government subsidies has improved the enthusiasm of enterprises to perform overall environmental responsibility and weakened greenwashing behavior.

Columns (3) and (4) report the moderating effects of absorbed and unabsorbed redundant resources respectively. The coefficients of Absorb1_Words and Ubsorb1_Words are significantly negative, indicating that both types of resource slack positively moderate the relationship between digital transformation and greenwashing. Hypotheses H3a and H3b are proved.

Column (5) reports that the moderating effect of public pressure, Subsidy1_Words, is negative and significant at the 5% level, indicating that public pressure positively moderates the relationship between digital transformation and greenwashing. Because of its timeliness and extensive supervision, public participation can quickly promote enterprises to shorten the green digital transformation cycle and inhibit greenwashing. Hypothesis H4 is certified. Figure 3 shows the moderating effect diagram.

FIGURE 3. The moderating effect figure.

4.2 Robustness test

It is considered that there may be reverse causality and endogeneity problems caused by DIT and greenwashing.

According to the econometric model set in this paper, the influence of heteroscedasticity should be excluded when testing the endogeneity of panel data. Therefore, the Hausman endogeneity method was used to test the endogeneity of DIT with one stage lag. p-value = 0.5294, indicates that the lag period of DIT is an exogenous variable (Gujarati et al., 2012).

First, the measurement method of the dependent variable was changed, and Greenwash was replaced by Green (Green = STS1-STS2) to perform the regression. Secondly, DIT is measured by the proportion of digital word frequencies of a company in the total number of digital word frequency of all companies in the same industry. Finally, taking the mean value of DIT of other enterprises in the same industry as the instrumental variable, the two-stage least squares method was used for regression.

4.2.1 Change the measurement method of the dependent variable and core explanatory variable

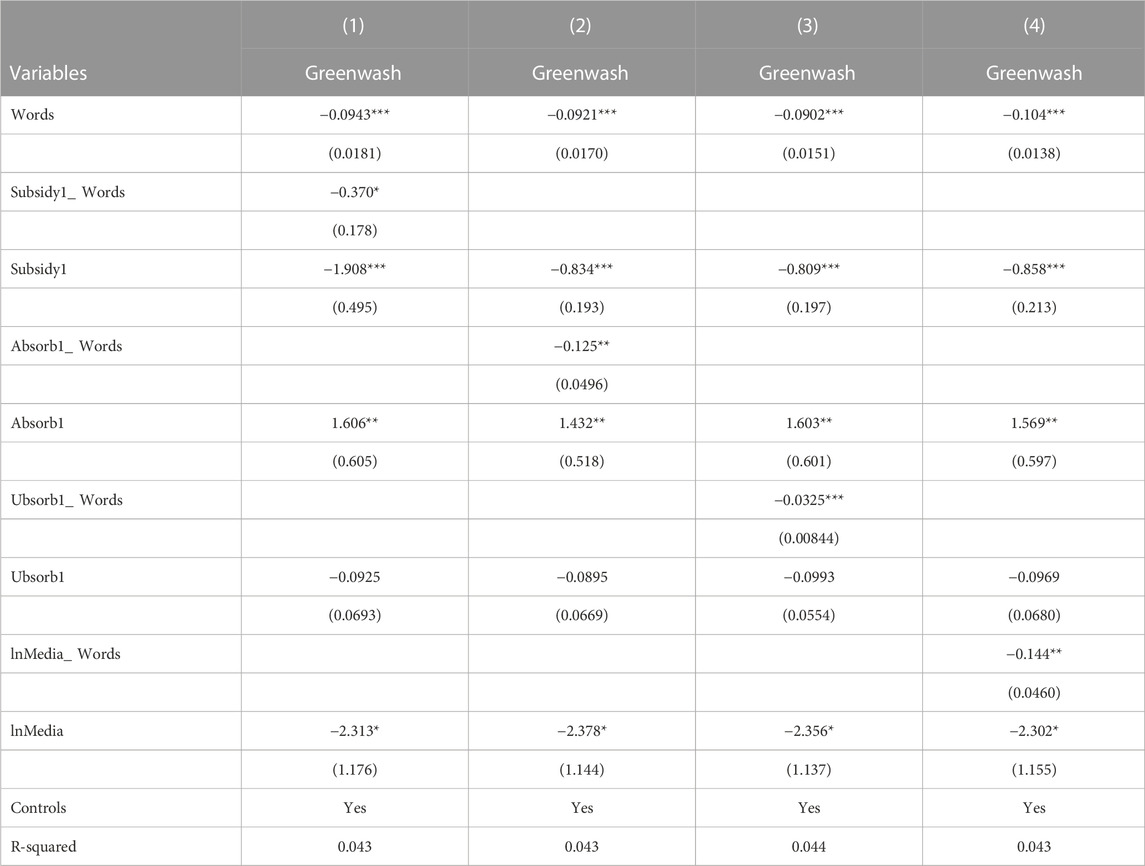

Table 3 shows the regression results after changing the measurement method of Greenwash, replacing Greenwash with Green. Table 4 takes the ratio of the word frequency of enterprises to the total word frequency of the same industry as the regression result of the proxy variable of DIT.

TABLE 3. Regression results of changing the dependent variable.

TABLE 4. Regression results of changing the independent variable.

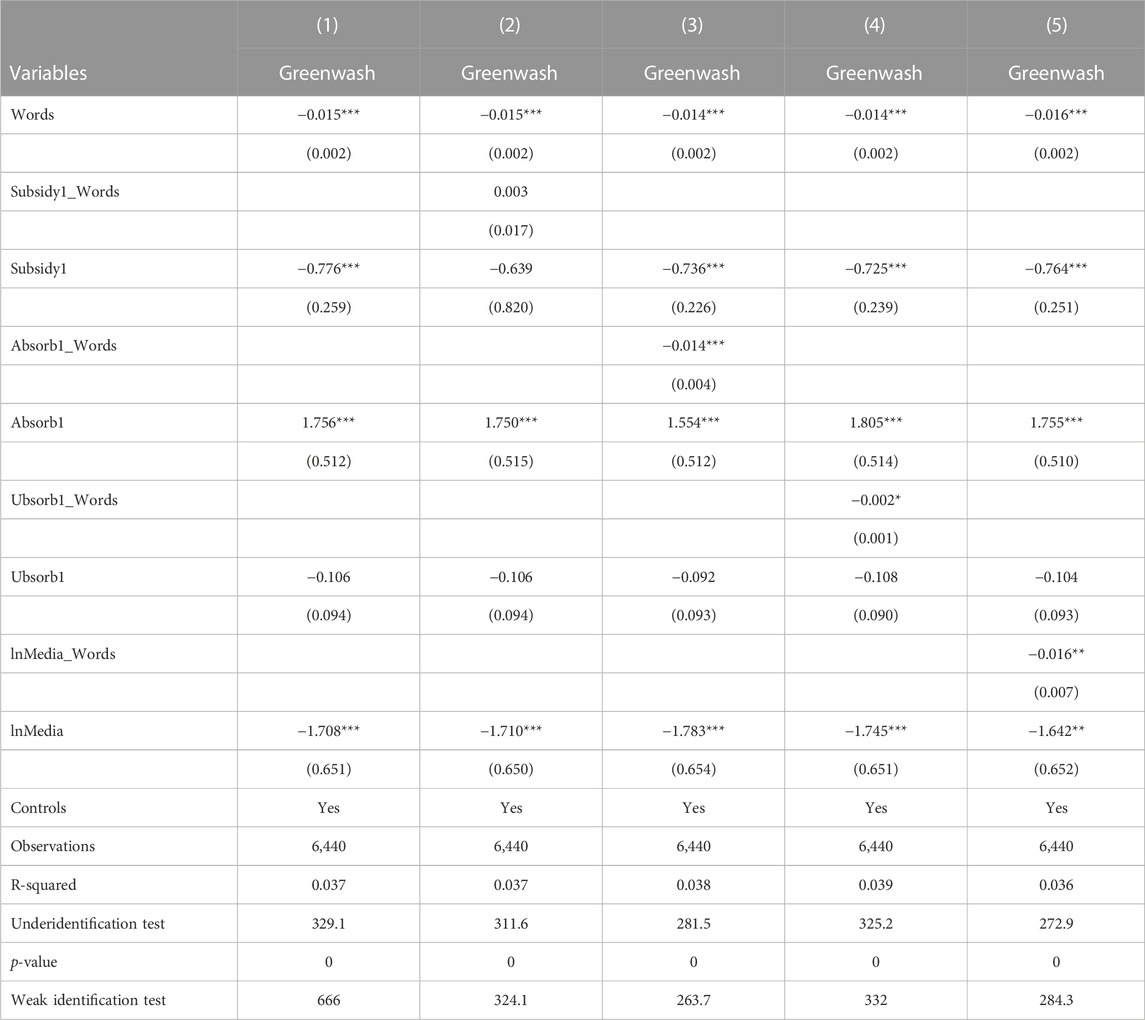

4.2.2 Two-stage least squares

The most commonly used method to solve the endogeneity problem is to find instrumental variables, and then get more consistent estimation results through the two-stage least square method. We refer to the processing method of Fishman and Svensson (Fisman and Svensson, 2007), and take the mean value of DIT of other enterprises in the same industry as the instrumental variable, because the characteristic variable of the whole sample is not directly affected by the DIT of a single enterprise, but directly related to the explanatory variable. The Underidentification test and Weak identification test results show that this variable meets the requirements of tool variables.

As can be seen from Table 5, except that the Subsidy1_Words is not significant, the coefficients of other interactive variables show robustness. There are two reasons for this situation. First of all, it may be that in recent years, China has called for digitalization and greening, and enterprises that do well in digital transformation can obtain financial support from the government, such as government subsidies. As a result, the DIT of enterprises in the same industry has the effect of the sheep flocks, so the coefficient of this interaction term is not significant. The second reason is that any study has flaws. Statistics are only used to explain economic phenomena, so it cannot guarantee that all regression results can meet the requirements of statistics.

TABLE 5. Regression results of IV-2SLS.

4.3 Further analysis

According to the definition of greenwashing proposed by the school of institutional theory, greenwashing is the difference between symbolic behavior and substantive behavior.

The main effects of DIT are analyzed as follows: In the first case, both symbolic and substantive behaviors are weakened, but the symbolic behavior is weakened even more. In the second case, both symbolic and substantive behaviors are enhanced, but substantive behaviors are enhanced more. In the third case, symbolic behavior is weakened and substantive behavior is strengthened. In the above three cases, the greenwashing behavior of enterprises will be weakened. As can be seen from the regression results in Table 6, the first case occurs. The symbolic behavior is significantly weakened, while the coefficient (Words) of the substantive behavior is negative but not significant.

TABLE 6. Regression results of symbolic behavior and substantive behavior.

This paper further explores the moderating effects of government subsidies, resource slack, and public pressure on symbolic behavior (STS2) and substantive behavior (STS1). It is necessary to strengthen the practical activities of substantive environmental behavior and weaken the activities of symbolic environmental behavior to govern the greenwashing behavior of enterprises. Table 6 shows that the main effect of digital transformation does suppress symbolic behavior, but the effect on substantive behavior is not obvious.

In the moderating effect, only absorbed resource slack positively moderated symbolic behavior. Government subsidies and unabsorbed resource slack negatively moderate substantive environmental behavior, indicating that the incentive effect of government subsidies is significant, which can encourage enterprises to actively purchase more intelligent and digitally cleaner production equipment and improve their substantive environmental practices. The moderating effect of public pressure is negative in both symbolic and substantive behaviors. By comparing the coefficient of lnMedia_Words in column (4) and column (8) (0.00336 > 0.00236), it can be seen that The moderating effect of public pressure on substantive behavior is significantly stronger than that on symbolic behavior. Therefore, the total effect of the moderating effect of public pressure is positively moderating the relationship between digital transformation and greenwashing.

5 Conclusion and suggestions

5.1 Conclusion

Our research is based on the requirement for enterprises to improve their ESG level to achieve the goal of “carbon neutrality and carbon peak” in China. For their own interests, when enterprises fulfill their social responsibilities, there will be greenwashing behavior, which has a significant impact on the realization of sustainable development goals in China. It is necessary to study how to control the greenwashing behavior of Chinese enterprises. Our research objectives are determined and mentioned in the introduction. The questions are as follows: Can digitalization provide solutions for enterprises to achieve green transformation and restrain their greenwashing behavior? What are the main internal and external factors affecting enterprises’ greenwashing behavior? How do these internal and external factors affect the relationship between digitization and greenwashing?

The empirical results confirm that digitization inhibits greenwashing behavior. The selected moderating variables public pressure, government subsidies, and unabsorbed slack resources also have an inverse relationship with greenwashing, while the slack resources have a positive proportional relationship with greenwashing. The results of the study here show the signs and ability of Chinese enterprises to achieve sustainable development, which has important significance for environmental protection in China’s rapid economic development. The moderating effect also supports that Chinese enterprises will allocate internal resources to sustainable goals when faced with legitimacy pressure.

The specific research results are as follows: First, digital transformation will inhibit symbolic behavior and greenwashing behavior; Second, government subsidies, absorbed resource slack, and unabsorbed resource slack play a positive moderating role in the relationship between digital transformation and enterprise greenwashing. Third, in the moderating effect of symbolic behavior and substantive behavior, only absorbed resource slack positively moderated symbolic behavior, while government subsidies and unabsorbed resource slack negatively moderated substantive environmental behavior. The negative moderating effect of public pressure on substantive behavior is significantly stronger than that of symbolic behavior.

5.2 Suggestions

First of all, the empirical results show that institutional pressure has restrained corporate greenwashing behavior. With the introduction of more environmental protection rules and regulations in China, listed companies are encouraged to digitally transform and disclose more social responsibility information. In particular, Shenzhen Stock Exchange and Shanghai Stock Exchange are encouraged to further improve the social responsibility disclosure system of listed companies, to form normal supervision of the social responsibility of listed companies and reduce greenwashing. In terms of the public, we can make use of the “digital platform” that interacts with the public, give full play to the power of informal institutions such as non-governmental organizations, effectively supervise the greenwashing behavior of enterprises, and at the same time reduce the cost of government supervision. It is suggested that the government take the lead in building more digital public participation platforms, such as public environmental centers and WeChat blueprints, to improve the online monitoring and early warning ability of enterprises’ greenwashing behavior, to urge enterprises to configure more intelligent and digital cleaner production equipment and facilities, and to improve their environmental performance.

Secondly, government subsidies can effectively restrain enterprises from greenwashing. Therefore, this paper suggests that the government should play the role of “green guidance”. Specific suggestions are as follows: First, local governments are encouraged to seize the trend of enterprises’ digital green transformation, introduce more government subsidy policies for digital transformation, improve digital infrastructure and digital intellectual property protection, and escort enterprises’ green digital transformation. Secondly, enterprises take advantage of the “green signal” function of government subsidies to actively attract investors to invest more capital layout and deepen green digital transformation.

Finally, for enterprises, digital transformation is an “organizational change” and needs more resources to support it. The government will take the lead and the banks will cooperate to give more green preferential loans, tax relief, and other measures to enterprises undergoing green digital transformation, to fill the “slack resources” of enterprises undergoing digital transformation, ease their financing constraints and help enterprises overcome the difficulties of digital transformation smoothly.

5.3 Shortcomings and prospects

This paper analyzes and verifies the effect and boundary conditions of digital transformation on greenwashing behavior of enterprises, but there are still some limitations. This paper discusses the moderating effects of government subsidies, resources slack, and public pressure on the relationship between digital transformation and enterprise greenwashing from the perspective of the resource-based view and legitimacy theory. However, other resources and legitimacy pressure also affect the relationship between digital transformation and enterprise greenwashing. For example, political connections and formal institutional legitimacy pressure can be further explored in the future from the perspective of corporate governance such as the board of directors and executive education level to further explore the boundary conditions of digital transformation affecting enterprise greenwashing behavior.

Data availability statement

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding authors.

Author contributions

K-SZ, ZP, and K-MZ were responsible for the overall development of this study, including the planning of sample collection, data analysis, writing, and polishing of the manuscript. K-SZ and FJ was in charge of the data collection, the construction of the research framework, and analysis of this study. All authors contributed to the article and approved the submitted version

Acknowledgments

The authors thank the supports from National Natural Science Foundation of China (Grant No.71972104) and National Government-sponsored Doctoral Program of China (202206860022).

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Supplementary material

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenvs.2023.1179419/full#supplementary-material

References

Ahmed, M., Hafeez, M., Kaium, M. A., Ullah, S., and Ahmad, H. (2023). Do environmental technology and banking sector development matter for green growth? Evidence from top-polluted economies. Environ. Sci. Pollut. R. 30, 14760–14769. doi:10.1007/s11356-022-23153-y

Anser, M. K., Yousaf, Z., Usman, M., and Yousaf, S. (2020). Towards strategic business performance of the hospitality sector: Nexus of ICT, E-marketing and organizational readiness. Sustainability-Basel 12, 1346. doi:10.3390/su12041346

Aragòn-Correa, J. A., Marcus, A. A., and Vogel, D. (2020). The effects of mandatory and voluntary regulatory pressures on firms’ environmental strategies: A review and recommendations for future research. Acad. Manag. Ann. 14, 339–365. doi:10.5465/annals.2018.0014

Ayayi, A. G., and Wijesiri, M. (2022). Is there a trade-off between environmental performance and financial sustainability in microfinance institutions? Evidence from south and southeast asia. Bus. Strateg. Environ. 31, 1552–1565. doi:10.1002/bse.2969

Bai, C., and Sarkis, J. (2017). Improving green flexibility through advanced manufacturing technology investment: Modeling the decision process. Int. J. Prod. Econ. 188, 86–104. doi:10.1016/j.ijpe.2017.03.013

Bayo-Moriones, A., Billón, M., and Lera-López, F. (2013). Perceived performance effects of ICT in manufacturing SMEs. Ind. Manage Data Syst. 113, 117–135. doi:10.1108/02635571311289700

Berrone, P., Fosfuri, A., and Gelabert, L. (2017). Does greenwashing pay off? Understanding the relationship between environmental actions and environmental legitimacy. J. Bus. Ethics 144, 363–379. doi:10.1007/s10551-015-2816-9

Boeing, P. (2016). The allocation and effectiveness of China’s R&D subsidies-Evidence from listed firms. Res. Policy 45, 1774–1789. doi:10.1016/j.respol.2016.05.007

Bourgeois, L. J. (1981). On the measurement of organizational slack. Acad. Manage Rev. 6, 29–39. doi:10.2307/257138

Bourgeois, L. J. (1981). On the measurement of organizational slack. Acad. Manag. Rev. 6, 29. doi:10.2307/257138

Bowen, F., and Aragon-Correa, J. A. (2014). Greenwashing in corporate environmentalism research and practice: The importance of what we say and do. Organ Environ. 27, 107–112. doi:10.1177/1086026614537078

Cai, X., Zhu, B., Zhang, H., Li, L., and Xie, M. (2020). Can direct environmental regulation promote green technology innovation in heavily polluting industries? Evidence from Chinese listed companies. Sci. Total Environ. 746, 140810. doi:10.1016/j.scitotenv.2020.140810

Chalmers, D., Matthews, R., and Hyslop, A. (2021). Blockchain as an external enabler of new venture ideas: Digital entrepreneurs and the disintermediation of the global music industry. J. Bus. Res. 125, 577–591. doi:10.1016/j.jbusres.2019.09.002

Chen He, H. Y. (2022). The impact of government innovation subsidies on enterprises' digital transformation South China Finance. Sustainability 14, 1. doi:10.3390/su142114003

Chen, H., Zeng, S., Lin, H., and Ma, H. (2017). Munificence, dynamism, and complexity: How industry context drives corporate sustainability. Bus. Strateg. Environ. 26, 125–141. doi:10.1002/bse.1902

Chen, Q., Lin, S., and Zhang, X. (2020). The effect of China’s incentive policies for technological innovation:incentivizing quantity or quality. China Ind. Econ., 79–96.

Chen, W. R., and Miller, K. D. (2007). Situational and institutional determinants of firms' R&D search intensity. Strateg. Manage J. 28, 369–381. doi:10.1002/smj.594

Cheng, J. L. C., and Kesner, I. F. (1997). Organizational slack and response to environmental shifts: The impact of resource allocation patterns. J. Manage 23, 1–18. doi:10.1177/014920639702300101

Cheng, Q., and Ding, H. (2022). Research on the impact of tax incentives onthe digital transformation of resource-based enterprises. Chin. J. Manag. 19, 1125–1133.

Clarkson, P. M., Li, Y., Richardson, G. D., and Vasvari, F. P. (2008). Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Organ. Soc. 33, 303–327. doi:10.1016/j.aos.2007.05.003

Cull, R., Li, W., Sun, B., and Xu, L. C. (2015). Government connections and financial constraints: Evidence from a large representative sample of Chinese firms. J. Corp. Financ. 32, 271–365. doi:10.17016/ifdp.2015.1129

de Villiers, C., Low, M., and Samkin, G. (2014). The institutionalisation of mining company sustainability disclosures. J. Clean. Prod. 84, 51–58. doi:10.1016/j.jclepro.2014.01.089

DeStefano, T., Kneller, R., and Timmis, J. (2018). Broadband infrastructure, ICT use and firm performance: Evidence for UK firms. J. Econ. Behav. Organ 155, 110–139. doi:10.1016/j.jebo.2018.08.020

DiMaggio, P. J., and Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 48, 147–160. doi:10.2307/2095101

Dong, Z., and Zhang, Z. (2022). Does the business environment improve the sustainable development of enterprises? Sustainability-Basel 14, 13499. doi:10.3390/su142013499

Du, W. D., Pan, S. L., and Huang, J. (2016). How a latecomer company used IT to redeploy slack resources. Mis Q. Exec. 15, 1.

Duan, W., Ak, B., and Ar, C. (2022). Acc, D. Government subsidies' influence on corporate social responsibility of private firms in a competitive environment. J. Innov. Knowl. 7, 100189.

Ekata, G. E. (2012). The IT productivity paradox: Evidence from the Nigerian banking industry. Electron. J. Inf. Syst. Dev. Ctries. 51, 1–25. doi:10.1002/j.1681-4835.2012.tb00361.x

Esposito De Falco, S., and Renzi, A. (2015). The role of sunk cost and slack resources in innovation: A conceptual reading in an entrepreneurial perspective. Entrep. Res. J. 5, 167–179. doi:10.1515/erj-2015-0019

Feng, Z., Chen, K., and Dai, X. (2019). Does the weighted tax deduction for R&D costs promote firms’innovative capability?——— the full perspective of innovation chain. Sci. Res. Manag. 40, 73–86.

Fisman, R., and Svensson, J. (2007). Are corruption and taxation really harmful to growth? Firm level evidence. J. Dev. Econ. 83, 63–75. doi:10.1016/j.jdeveco.2005.09.009

Gobbo, J. A., Busso, C. M., Gobbo, S. C. O., and Carreão, H. (2018). Making the links among environmental protection, process safety, and industry 4.0. Process Saf. Environ. 117, 372–382. doi:10.1016/j.psep.2018.05.017

Gou, Q. W. (2013). Can both substantive and symbolic environmental management get paid? - an empirical study based on China listing corporation. Adv. Mater. Res. 807-809, 760–763. doi:10.4028/www.scientific.net/amr.807-809.760

Greenwood, R., Raynard, M., Kodeih, F., Micelotta, E. R., and Lounsbury, M. (2011). Institutional complexity and organizational responses. Acad. Manag. Ann. 5, 317–371. doi:10.5465/19416520.2011.590299

Greve, H. R. (2003). A behavioral theory of R&D expenditures and innovations: Evidence from shipbuilding. Acad. Manage J. 46, 685–702. doi:10.5465/30040661

Gujarati, D. N., Porter, D. C., and Gunasekar, S. (2012). Basic econometrics. New York City: Tata mcgraw-hill education.

Guo, R., Zhang, W., Wang, T., Li, C. B., and Tao, L. (2018). Timely or considered? Brand trust repair strategies and mechanism after greenwashing in China—from a legitimacy perspective. Ind. Mark. Manag. 72, 127–137. doi:10.1016/j.indmarman.2018.04.001

Hajli, M., Sims, J. M., and Ibragimov, V. (2015). Information technology (IT) productivity paradox in the 21st century. Int. J. Product. Perfor 64, 457–478. doi:10.1108/ijppm-12-2012-0129

Hinings, B., Gegenhuber, T., and Greenwood, R. (2018). Digital innovation and transformation: An institutional perspective. Inf. Organ-Uk 28, 52–61. doi:10.1016/j.infoandorg.2018.02.004

Huang, J., and Li, Y. (2012). Slack resources in team learning and project performance. J. Bus. Res. 65, 381–388. doi:10.1016/j.jbusres.2011.06.037

Huang, J. W., and Li, Y. H. (2009). The mediating effect of knowledge management on social interaction and innovation performance. Int. J. Manpow. 30, 285–301. doi:10.1108/01437720910956772

Hughes, M., Hughes, P., Morgan, R. E., Hodgkinson, I. R., and Lee, Y. (2021). Strategic entrepreneurship behaviour and the innovation ambidexterity of young technology-based firms in incubators. Int. Small Bus. J. 39, 202–227. doi:10.1177/0266242620943776

Ilinitch, A. Y., Soderstrom, N. S., and Thomas, T. E. (1998). Measuring corporate environmental performance. J. Acc. Public Pol. 17, 383–408. doi:10.1016/s0278-4254(98)10012-1

Ji, X., and Wang, D. Financial Mismatch,Government subsidies,and China’s foreign direct investment. Econ. Rev. 2017, 62–75.

Jialin, S., Yiyi, S., Taoyong, S., and Luyu, W. (2022). The dilemma of winners: Market power, industry competition and subsidy efficiency. Chin. Manag. Stud. 16, 1161–1181. doi:10.1108/cms-10-2020-0457

Jifri, A. O., Drnevich, P., and Tribble, L. (2016). The role of absorbed slack and potential slack in improving small business performance during economic uncertainty. J. Strategy Manag. 9, 474–491. doi:10.1108/jsma-03-2015-0024

Kleer, R. (2010). Government R&D subsidies as a signal for private investors. Res. Policy 39, 1361–1374. doi:10.1016/j.respol.2010.08.001

Kortmann, S. (2015). The mediating role of strategic orientations on the relationship between ambidexterity-oriented decisions and innovative ambidexterity. J. Prod. Innov. Manag. 32, 666–684. doi:10.1111/jpim.12151