Zhenyang Qian1

Zhenyang Qian1 Sanglin Zhao

Sanglin Zhao Hao Deng

Hao Deng Måns Gustaf

Måns Gustaf- 1School of Tailong Finance, Zhejiang Gongshang University, Hangzhou, China

- 2School of Engineering Management, Hunan University of Finance and Economics, Changsha, China

- 3School of Business, Society and Engineering, Mälardalen University, Västeras, Sweden

A commentary on

The synergistic effect of digital transformation technology and supply chain finance: empirical evidence from 500 listed companies

by Liu Z, Zhang J and Cao L (2025). Front. Phys. 13:1664273. doi: 10.3389/fphy.2025.1664273

1 Introduction

Liu et al.'s research focuses on the intersection of digital transformation [1], Supply Chain Finance (SCF), and technological innovation, enriching the lack of large sample and cross industry empirical evidence (especially in the Chinese context) on the collaborative evolution of the three. This study is based on panel data from 500 A-share listed companies from 2014 to 2021, integrating the theory of coevolution and economic effects. The entropy weight TOPSIS model and coupled coordination degree model are used to quantitatively analyze the synergistic effects of supply chain finance and technological innovation. The core conclusion is that technological innovation is the dominant order parameter in the process of collaborative evolution, and the coupling coordination has increased from 0.5432 in 2015 to 0.8185 in 2021, providing practical value for theoretical and policy formulation. Previous studies research on digital transformation have similar insights and are meaningful. This has inspired our comments [2–5]. This commentary will acknowledge the advantages of the study and point out directions for further exploration to enhance its theoretical and practical impact.

2 Advantages of original research

2.1 Rigorous research design and data scale

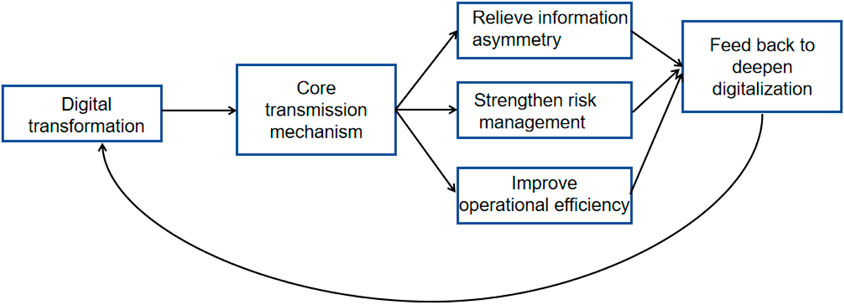

One of the core advantages of Liu et al.’s research lies in its reliance on large sample cross industry data (covering manufacturing, service, and high-tech industries) and multi-source data sources (Wind/CSMAR financial data, patent database technology innovation data, enterprise report supply chain finance data). This design addresses the limitations of previous studies that relied heavily on case analysis or single industry data, significantly enhancing the external validity of the conclusions. In addition, the study used two complementary models simultaneously, the entropy weight TOPSIS model for comprehensive performance evaluation and the coupling coordination degree model for system interaction analysis, to ensure the robustness of the quantitative results of the “technology finance” synergy effect and avoid excessive reliance on a single analytical tool (Figure 1).

Figure 1. Diagram of impact mechanism.

2.2 Dual correlation between theory and practice

The study uses the theory of collaborative evolution as the analytical framework, going beyond simple descriptive association analysis and providing a deeper explanation of why technological innovation dominates the collaborative evolution process: digital tools such as blockchain, artificial intelligence, and the Internet of Things can solve the traditional pain points of supply chain finance (information asymmetry, high risk), while supply chain finance provides stable financial support for technological innovation. This has important guiding significance for industrial upgrading in the context of global uncertainty.

3 Limitations and future exploration directions

3.1 Insufficient analysis of industry heterogeneity

Although the study claims to cover “multiple industries”, the coupling coordination data has not been broken down by industry. For example, the synergy effect of the manufacturing industry (as shown in the “curve A” mentioned in the study, which significantly benefits from economies of scale) may be stronger than that of the small-scale service industry (“curve C”), as the manufacturing industry relies more on supply chain finance (for inventory/raw material financing) and technological innovation (for automation upgrades). The lack of in-depth analysis of this industry heterogeneity has limited the supportive role of research in formulating industry-specific policies, such as policymakers being unable to design differentiated incentive measures for high-tech industries and traditional manufacturing industries.

3.2 Insufficient exploration of policy mechanisms

The study listed “Made in China 2025” as a driving factor for improving coupling coordination, but did not distinguish the differences in the impact of specific policy tools (such as R&D subsidies and supply chain finance pilots). For example, is there a difference in the synergistic effect between the blockchain based supply chain finance pilot (mentioned in the policy implications) and general tax incentives? The lack of such refined analysis makes the correlation between “policy intervention and technology finance synergy” more indirect, reducing the accuracy of the author’s proposed sandbox recommendations for technology and financial monitoring.

3.3 Over reliance on data from listed companies

The research sample focuses on listed companies, but excludes non listed small and medium-sized enterprises. According to the author’s own argument, small and medium-sized enterprises are the main beneficiaries of supply chain finance. Although listed companies can provide high-quality financial data, there are significant differences in their financing channels (such as equity financing) compared to non listed small and medium-sized enterprises (which rely more on supply chain finance). This limitation raises a key question: can the observed synergies be extended to the core group that supply chain finance aims to serve (non listed small and medium-sized enterprises)?

4 Discussion

Liu et al.'s research fills a key gap in the field of technological and financial co evolution, and its quantifiable analytical framework provides replicable tools for global researchers and policymakers. However, addressing the above limitations will further enhance the impact of the research:

Breaking down data by industry can support targeted policy formulation; Analyzing the differences in specific policy tools can clarify which intervention measures are most effective in promoting synergies and avoiding a one size fits all policy; For example, the EU’s “Digital Europe Plan” links supply chain digitization with green transformation goals, while the US’s “Chip and Science Act” prioritizes technological innovation in semiconductor supply chains to enhance resilience. Policy tools: Singapore’s “Digital Supply Chain Initiative” provides grants to small and medium-sized enterprises to adopt digital supply chain finance platforms and establish cross-border data sharing frameworks to reduce information asymmetry, while Japan’s “New Forms of Capitalism” policy combines research and development subsidies with regulatory sandboxes for integrating fintech supply chain finance. Regulatory environment impact: Strict data privacy regulations, such as the EU GDPR, may slow down cross-border supply chain data sharing but enhance trust, while more flexible frameworks, such as Singapore’s Personal Data Protection Act, which exempts business cooperation, will accelerate the adoption of digital SCF, but require strong cybersecurity measures.

Incorporating data from non listed small and medium-sized enterprises can better align research with the core mission of supply chain finance (supporting small and medium-sized enterprises). On the one hand, it can more accurately reflect the actual service effect of supply chain finance. Listed companies have diversified financing channels such as equity financing and bond issuance, and have a lower dependence on supply chain finance. The synergy effect between digital transformation and supply chain finance may be weaker than that of non listed small and medium-sized enterprises, as the latter rely more on digital supply chain finance tools to reduce information asymmetry and improve financing efficiency; By incorporating data from non listed companies, it is possible to more accurately evaluate the performance of synergies among the ‘truly needed groups’. On the other hand, it can provide more accurate basis for policy-making. For example, if the data shows that the synergy effect of non listed manufacturing small and medium-sized enterprises is the strongest, then policies can be targeted towards such enterprises to avoid misallocation of policy resources to the group of listed enterprises with lower demand for supply chain finance, truly achieving the goal of policy serving the core mission.

Overall, this study has laid a solid foundation for further research on digital transformation and supply chain finance. If further improvement can be made in the analysis of industry heterogeneity and policy refinement, it will more effectively guide enterprises and governments to unleash the full potential of “technology finance” synergy.

Author contributions

ZQ: Data curation, Methodology, Supervision, Formal analysis, Validation, Resources, Software, Writing – original draft, Writing – review and editing. SZ: Writing – original draft, Writing – review and editing. HD: Writing – original draft, Writing – review and editing. MG: Writing – original draft, Writing – review and editing.

Funding

The author(s) declare that no financial support was received for the research and/or publication of this article.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Correction note

This article has been corrected with minor changes. These changes do not impact the scientific content of the article.

Generative AI statement

The author(s) declare that no Generative AI was used in the creation of this manuscript.

Any alternative text (alt text) provided alongside figures in this article has been generated by Frontiers with the support of artificial intelligence and reasonable efforts have been made to ensure accuracy, including review by the authors wherever possible. If you identify any issues, please contact us.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

1. Liu Z, Zhang J, Cao L. The synergistic effect of digital transformation technology and supply chain finance: empirical evidence from 500 listed companies. Front Phys (2025) 13:1664273. doi:10.3389/fphy.2025.1664273

2. Esamah A, Aujirapongpan S, Rakangthong NK, Imjai N. Agile leadership and digital transformation in savings cooperative limited: impact on sustainable performance amidst COVID-19. J Hum Earth, Future (2023) 4(1):36–53. doi:10.28991/hef-2023-04-01-04

3. Nguyen QM, Hang NPT, Dao LT. Exploring the nexus between digital economy and green growth: insights from emerging economies. Emerg Sci J (2024) 8(4):1622–41. doi:10.28991/esj-2024-08-04-022

4. Zhao S, Deng H, Cao J, Gustaf M. Digital transformation of construction enterprises and carbon emission reduction: evidence from listed companies. Front Environ Sci (2025) 13:1570182. doi:10.3389/fenvs.2025.1570182

Keywords: listed company, digital transformation, supply chain, synergistic effect, empirical evidence

Citation: Qian Z, Zhao S, Deng H and Gustaf M (2025) Commentary: The synergistic effect of digital transformation technology and supply chain finance: empirical evidence from 500 listed companies. Front. Phys. 13:1694604. doi: 10.3389/fphy.2025.1694604

Received: 01 September 2025; Accepted: 03 October 2025;

Published: 15 October 2025; Corrected: 17 October 2025.

Edited by:

Grigorios L. Kyriakopoulos, National Technical University of Athens, GreeceReviewed by:

Omid A. Yamini, Southbank Institute, AustraliaCopyright © 2025 Qian, Zhao, Deng and Gustaf. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Måns Gustaf, Z3VzdGFmZWR1QHllYWgubmV0